Money

Integrating Diagrams in Business Financial Planning – Finance Monthly

Financial planning is of utmost importance in the constantly evolving business landscape. Some innovative companies are engaging diagrams and other visual tools to connect complicated financial data with clear, actionable insights.

Effective utilization of diagrams allows these businesses to spot trends, optimize budgeting allocations, and forecast more accurately.

This article will elaborate on how companies can use diagrams to ensure financial success.

Visualizing Data Trends

Data trends hold lots of insight into the company’s growth trajectory, market performance, and emerging risks or opportunities. While traditional tables and spreadsheets inform, spotting trends instantly takes time.

Diagrams such as line charts, heat maps, and waterfall charts turn such numbers into easily interpretable visuals, making it easier for businesses to identify patterns and plan their strategy.

Line charts convey trends in revenue or costs over various points in time. You can choose heat maps on Miro’s diagram templates to visualize a set of performance measures over any management aspect, helping your organization put together a rough analysis of which set of departments and product lines require attention and which are thriving.

Waterfall charts are becoming increasingly popular among financial analysts to show incremental effects contributing to profit and those drawing resources from profit.

Waterfall charts let one label income and expense categories as they contribute or detract to profitability step by step. This helps set more targeted budgets and operational shifts.

Enhancing Budget Allocation

Diagrams provide a more visual way of dispersing resources based on need, performance, or return on investment (ROI).

Pie charts, tree maps, and bar graphs are examples of diagrams that make it easier for organizations to see where budget money is allocated to analyze whether it is being appropriately distributed among various projects or departments.

- Pie Chart and TreeMap Displays of Departmental Budgets: Some organizations use pie charts to allocate and overview department budgets and clearly show which departments incur the highest costs or investments.

Then, there are tree maps that visualize the nested subcategories inside significant categories so that companies can track spending from both macro and micro perspectives.

- Comparative Bar Graphs for Tracking ROI: Comparative bar graphs for ROI analysis across departments or campaigns allow finance teams to see which investments quickly deliver the most significant returns.

This attachment of value is handy for companies with multiple product lines or initiatives because such products allow for prioritizing high-ROI projects to minimize expenditure on something that does not return value.

Creating Financial Projections and Scenarios

Forecasting diagrams, like predictive graphs and sensitivity analysis charts, enable businesses to visualize different possible futures. Such visualization allows companies to make moves beforehand to remediate variances of expected value.

Sensitivity analysis diagrams allow businesses to adjust the variables and visualize the underlying financial template.

For example, through changes in sales growth rates or interest, finance teams can prepare for best-case, worst-case, and moderate cases to support an adaptive approach to budgeting.

In predicting revenue growth and cost changes over time, tech-based companies increasingly use predictive modelling and multi-line graphs based on historical data. Using such tools helps with a more precise revenue forecast, which allows for appropriate scaling of content investments or subscriber acquisition costs.

Advanced Reporting and Real-Time Dashboards

Companies increasingly turn to interactive dashboards and real-time reporting to make rapid decisions. Interactive charts allow users to easily interact with the data, making it exceedingly easy to focus on specific areas. Live and dynamic reporting helps the financial roles recognize and act upon issues as they arise, maintaining flexibility in financial planning.

Real-time dashboards allow companies to track KPIs, for example, cash flows, revenues, and expenses, with the help of dynamic bar graphs, pie charts, and gauges. Companies can update operational budgets and marketing spending in real time because the information is continuously updated based on live data.

The Role of AI in Automated Diagram Creation for Financial Planning.

Artificial Intelligence (AI) is bringing a sophisticated new dimension to financial planning by providing functions for automatic diagram creation from live data feeds. An AI algorithm can identify patterns in the data, automatically generate predictive models, and recommend the most appropriate visualizations.

AI-powered financial planning tools can analyze historical data to build automated forecasting diagrams so that businesses visualize future revenue, costs, and cash flow. For instance, AI-anchored facilitates real-time forecasting updates, furthering financial planning accuracy and freeing the finance team from other resource-consuming manual functions.

Some machine learning algorithms can spot variations from a given pattern in financial information and present this using colour-coded visuals and alerts. Companies such as Walmart employ these kinds of tools, indicating specific trends in sales data that allow finance teams to make prompt corrective changes.

Endnote

Innovative companies can leverage diagrams to turn complex financial data into easy-to-understand visuals that enhance data comprehension, budgeting accuracy, and strategic planning.

From predicting the future to tracking KPIs in real-time, these visual tools bring the financial health of organizations into clear view and permit well-informed and timely decision-making.

Introducing AI and real-time dashboards into financial planning allows for an even more sophisticated and dynamic application of diagrams, giving businesses the insight needed to thrive in a highly competitive market.

When I enquire of Karen Barrett what she likes doing outside work, her answer is somewhat surprising: “I love knocking down walls.”

This, it turns out, is part of a wider interest in property renovation, but her response makes a change from ‘socialising with friends’ or ‘going to the cinema’. Then again, there’s a lot about Barrett that makes her stand out.

The founder and chief executive of Unbiased, the UK’s leading platform connecting people to financial advisers, oversees a business that works with more than 27,000 advisers and manages over £80bn in assets.

In the 15 years since its launch, it’s estimated that Unbiased has helped 10 million people access the right IFA, while also facilitating other crucial services such as mortgage brokerage and accountancy.

I had noticed that advisers were brilliant but often struggled to get their brand in front of the right customers

Pretty impressive for someone who started out with a team of just five and scant knowledge of how to run a business.

As she admits, “Google was definitely my friend in the early days, but you’ve just got to have a go.”

Getting started

As a child, Barrett was “quite good at a number of things”, but she never had a clear idea of what she wanted to pursue as a career.

Graduating from Newcastle University with a degree in economics and marketing, a natural flair for communication and creativity led to a job with Mortgage Express, then part of Lloyds TSB.

“I loved working there,” she claims. “They pioneered products such as buy-to-let, self-cert and buy-and-build mortgages.

“I set up their first internet connection in 1999, which was also my introduction to the internet. At that stage, it was all dial-up, waiting for ages to connect, but I realised you could put brochures, content and information online for people to consume — all quite revolutionary.”

I’d like to see targeted advice become more accessible, especially for those who aren’t served by the market

A move to Abbey National (now Santander) followed, and then onto IFA Promotion, where Barrett stayed for a decade, working her way up to become marketing director. It was this experience, she says, that gave her “a real understanding of the financial advice sector, and the consumer and professional pain points”.

Her experience in different-sized companies also convinced Barrett that she preferred smaller teams and a more autonomous environment.

“Now I run my own business, it’s interesting to see that the seeds were always there. When I was at Mortgage Express, there were only about 150 people and you were allowed to just go ahead and do things. I enjoyed the autonomy.”

A personal journey

However, it wasn’t just a desire for independence that spurred Barrett to set up Unbiased in 2009.

That same year, her second child was born with a heart condition, which led to the family spending several months in hospital.

It’s about generating value for employees and customers, and delivering on your promises

“It was only then I realised that I hadn’t made any financial plans for such an eventuality,” remembers Barrett.

“Despite advising others, I hadn’t taken my own planning to heart. And it made me realise that I needed an adviser who wasn’t just someone my parents had used.

“My son is fine now, but that experience gave me the push to go all in with Unbiased. Once you face something so personal, you think, ‘Why not? I’ll find another job if it doesn’t work out.’ It gave me the confidence to pursue it fully.”

Fulfilling a need

Barrett realised that, for both clients and advisers, there was a gap in the market that her new company could fill.

“Throughout my career, I had noticed that advisers were brilliant but often struggled to get their brand in front of the right customers. And, on the consumer side, people often didn’t realise they needed advice or assumed it wasn’t for them.

As we’ve grown and hired more senior people, having a laser focus on metrics has become crucial

“I recall a research group with these ladies aged 60–70. None of them had taken pension advice, despite having had good careers. They’d taken advice from people like their son’s friend, who was a bank manager, but not from a qualified adviser.

“That experience made it clear there was a place for Unbiased — connecting clients looking for the right adviser with advisers seeking a good, consistent flow of quality enquiries to help plan their business.”

Barrett’s previous roles had also taught her the importance of technology, when building Unbiased. From the start, the firm embraced data-led processes to make the adviser and client experience as efficient as possible.

“That’s where the Unbiased algorithm was born — learning from a few pieces of data to match people with the right adviser.

“Our platform has evolved from there to offer a full conversion tool that tracks client interactions, nudges customers and integrates with CRM systems, providing data insights about successful enquiries.”

We’re a marketplace business, so we have to keep the clients happy while also satisfying our paying customers: the advisers

Crucially, it’s the volume of traffic that has enabled the business to become more precise, creating different journeys for different advice needs. This, in turn, has driven growth — over the past few years, Unbiased has delivered around £20bn in assets under management to its adviser customers, 75% of which is new to the industry.

Learning on the job

For all her success, however, Barrett’s journey hasn’t been an easy one. She emphasises that “resilience is key” when starting and running a business.

“You have to dig deep and keep going. It’s not easy, especially when you’re trying to achieve a lot with limited resources.

“Our business now has about 90–95 people, with specialists in all sorts of fields, from PPC [pay-per-click] to SEO [search engine optimisation]. But, when you’re starting out, you face constant challenges with money, time and people.

I knew I wanted a good business with a strong brand, happy customers and a healthy environment

“Also, you don’t know what you don’t know, so you make decisions based on the data you have at the time, and later you look back and wonder, ‘What was I thinking?’

“You’ll always make mistakes, but hopefully you won’t make the same one twice.”

Although Barrett found herself, at the start, “looking up even the most basic things”, she took inspiration from those around her.

“Networks are really important,” she says. “In general, I’ve found the financial services industry to be a fantastic network of people who are happy to share their knowledge. You learn as you go.

“For example, I remember going on holiday and reading a book called Scaling Up by Verne Harnish. It feels overly structured and staid now, but it inspired me to think about how I could make what we had bigger and bring it to more people.”

I recall a research group with these ladies aged 60–70. None of them had taken pension advice, despite having had good careers

Unbiased raised funds in late 2019 and again in 2022 as the business grew and expanded to the US. This enabled Barrett to hire an experienced chief operating officer, and she describes having someone to bounce ideas off as “invaluable”.

“Initially, I was working alone, which suited me because I’m independent anyway — I don’t need to be constantly checking in with anyone. But it was a real benefit to find people who were happy to pay it forward and to give you a bit of time.”

Important lessons

Even with more support around her and a thriving company, Barrett faces challenges every day, some of which are inherent to Unbiased’s model.

“We’re a marketplace business, so we have to keep the clients happy while also satisfying our paying customers: the advisers,” she points out.

“There’s always a tension between the two. We spend a lot of our marketing budget targeting clients, but our revenue comes from another party entirely.

On the consumer side, people often didn’t realise they needed advice or assumed it wasn’t for them

“It’s all about finding the right balance.”

When I ask her to identify the most important factors in running a business, she highlights three things: people, numbers and usability.

“People first of all, because you can’t do it without people, and you certainly can’t do it alone. I have a team of seven with whom I work closely daily, and we have regular meetings to check in on our KPIs [key performance indicators] and plan ahead.

“One of the things I’m proudest of is that our employees genuinely love working with each other. We’ve got a chief people officer and, if you look on Glassdoor, you’ll see we’re quite transparent. It’s about being one team with one dream.

“Second, the numbers. As we’ve grown and hired more senior people, having a laser focus on metrics has become crucial — whether it’s revenue or growth or Ebitda or whatever. You need to identify those North Star numbers and be on them all the time. And, if you’re wavering off them, how are you getting back on?

When I was at Mortgage Express, there were only about 150 people and you were allowed to just go ahead and do things. I enjoyed the autonomy

“Last, there’s usability and the health of the overall business. Before we secured investment, I didn’t always know exactly what I was aiming for, but I knew I wanted a good business with a strong brand, happy customers and a healthy environment. So, we keep an eye on competitors, but mainly in terms of how close they’re getting to what we’re doing.

“It’s about generating value for employees and customers, and delivering on your promises.”

Forging forward

On the adviser side, Unbiased is working with larger advice businesses and has partnered with brands such as Canaccord, M&G and PensionBee, to help advisers adapt to the increasing demands for efficiency and growth.

“We’ve seen a lot of private-equity investment and consolidation in the market,” says Barrett. “That’s definitely focused advisers’ minds on getting consistent streams of new business so they can grow at a regular rate.

Google was definitely my friend in the early days, but you’ve just got to have a go

“This has led them to our platform, where they can plan what type of customer they want to onboard and with what regularity, then support their efficiencies and pro-growth targets. That’s really driving business for us.”

For Barrett, making this process ever more granular is the key goal. The platform, she says, is “very much a vertically integrated funnel, and those integrations are getting stronger all the time”.

She adds: “The vision would be to have one view of a customer, their likelihood to convert, and an understanding of the length and level of investment.

“So, looking at the data, what will we have delivered to them in five or 10 years?”

It’s clear that the success of Unbiased owes a lot to this attention to detail. But what about the 92% of people who don’t receive any financial advice at present?

“There’s clearly room for growth,” agrees Barrett.

“I’d like to see targeted advice become more accessible, especially for those who aren’t served by the market.”

When I tell her that becoming a parent last year made me think more profoundly about my financial future, she seizes on this.

Despite advising others, I hadn’t taken my own financial planning to heart

“We see people like you a lot — those who suddenly become more responsible when they become parents. They need life assurance, a bigger mortgage or savings.

“We love creating journeys for them on our website, guiding them through typical life events.

“At the end of the day, it’s all about connectivity.”

On that reassuring note, we shake hands and I head back out to the London streets.

If our conversation is anything to go by, “knocking down walls” is more than just a hobby for Barrett.

Barrett in brief

What do you like to do outside work?

I have three children who keep me busy! And I enjoy property renovations, though I haven’t done one for a couple of years. My family also has a passion for cars. My dad was a car enthusiast, and I’ve inherited that interest.

What motivates you the most?

I love providing a service that genuinely helps people. It’s very fulfilling to be part of something that enables people to make better decisions about their lives.

What frustrates you the most?

Probably bureaucracy. It can be so complicated to navigate processes, especially when you’re starting out in business.

What’s a surprising fact about you?

I’m incredibly competitive! Whether it’s a game of poker at work or just trying to win at something, I always want to come out on top.

This article featured in the November 2024 edition of Money Marketing.

If you would like to subscribe to the monthly magazine, please click here.

RENTERS have admitted they rarely consider bill costs before moving – leaving 76 per cent shocked and stung by fees.

A poll of 2,000 tenants found 54 per cent rushed through the process to move in as soon as possible, prioritising location over the heating and energy costs.

2

2

But now 46 per cent feel they have no control over their bills, leaving 34 per cent cutting back elsewhere to afford them and 17 per cent feeling helpless at home.

And 24 per cent have even considered moving elsewhere due to the costs getting out of control.

Prior to picking up the keys, 51 per cent didn’t get much or any information from the landlord about how much they would likely have to pay for these essentials.

What’s more, 21 per cent are contractually prohibited from changing their energy supplier, with nearly half not realising this when they signed their lease.

This has left 36 per cent taking matters into their own hands by carrying out tasks to make their property more energy efficient – despite potentially breaking their tenancy agreements.

Paul White, commercial director at DIY store B&Q, which commissioned the research, said: “The research shows tenants are taking matters into their own hands, trying to improve energy efficiency in their homes – even when rental agreements typically limit what they’re allowed to change.

“Of those looking to make small but effective changes, there are a few low-cost solutions that are unlikely to breach rental agreements.

“Adding radiator reflectors to direct heat back into the room and using heavy curtains can help keep in warmth.

“These minor adjustments can make a real difference and provide renters some control over their energy costs, even if their property isn’t perfectly insulated.”

Of those who have made energy improvements around their rented home, 42 per cent have bled the radiators, and 39 per cent have installed draught seals around doors and windows.

A quarter (25 per cent) have insulated pipes and 23 per cent went as far as insulating the loft.

Half (53 per cent) of renters surveyed wanted to make these changes to stop energy bills spiralling out of control, and 44 per cent wanted to address issues with heating and cooling certain areas of the home.

But for 35 per cent, their DIY was driven by an eagerness to reduce their environmental impact.

The research, conducted via OnePoll, also found that there’s more renters can do to protect themselves before moving into new homes.

In fact, 69 per cent aren’t likely to check the age of appliances, while 67 per cent doubt they will inspect for draughts.

And 63 per cent are even unlikely to check the EPC rating of the next potential property.

Paul White from B&Q added: “Renters and homeowners alike can feel that they are unable to take control of their household bills.

“We have plenty of energy efficiency solutions, from thermostatic controls to draught excluders, which can help make it easier for customers to control and reduce their energy use, and to keep their bills from becoming overwhelming.

“As a first port of call, I’d recommend visiting our Energy Savings hub at diy.com for free tips and advice.

“Here, people can also take advantage of our free Energy Saving Service, offering personalised advice on the steps they can take to improve the energy efficiency of their home.”

Your landlord’s responsibilities

Your landlord must do anything your tenancy agreement says they have to do.

On top of this, your landlord is also generally responsible for keeping in repair:

- The structure and outside of your home including the walls, roof, foundations, drains, guttering, external pipes, windows and external doors

- Basins, sinks, baths, toilets and their pipework

- Water and gas pipes

- Electrical wiring

- water tanks

- Boilers

- Radiators

- Gas fires

- Fitted electrical fires

- Fitted heaters

The responsibility to do these repairs cannot be removed by anything your tenancy agreement says.

Your landlord cannot pass on the cost of any repair work they are responsible for to you.

Your landlord only has to make repairs when they know there is a problem so tell them about any repairs that are needed.

Since the Financial Conduct Authority moved to a portfolio supervision model, this portfolio strategy letter has emerged as the most relevant communication for our sector.

While the Business Plan is still essential reading, the portfolio strategy letter gives more sector-specific insight, including what the FCA’s priorities are and, crucially, what its expectations are of advice firms.

It’s great to read that the regulator is looking to increase its industry engagement with an acknowledgement of the insights this can bring. At the same time, it is important all firms are on top of the FCA’s communications.

There will be no excuses if the FCA subsequently finds issues within the retirement income advice or control framework

Although only three pages long, there is a wealth of information contained within the hyperlinks to keep us all busy. Here are some of the key headlines and actions firms should be taking:

1. Retirement income advice

Since 2019, when the FCA announced its second quality of advice review would focus on retirement income, it has been clear this is a major area of emphasis. Since then, the FCA has completed and released the findings of its thematic review of retirement income advice.

Leading with this subject again indicates it was not satisfied with the overall findings from its review.

Consolidators should review their business plans, strategy documents, policies and procedures

With the Dear CEO letter that accompanied the findings of the thematic review, chief executives were written to three times in under two years about the importance of their firms ensuring retirement income leads to good customer outcomes. There will be no excuses if the FCA subsequently finds issues within the retirement income advice or control framework.

Having clearly set out its findings and expectations in relation to areas such as know-your-customer information, risk profiling and cashflow modelling, it is essential firms can demonstrate they have gone through the FCA’s report and can confirm what action they have taken to satisfy themselves that their customers are receiving good outcomes.

2. Ongoing advice services

Our sector has been discussing ongoing advice reviews all year. In fact, this focus almost overshadowed the findings from the FCA’s thematic review of retirement income advice in March.

While we await the findings from the FCA’s thematic review of ongoing advice later this year, there is still more firms should be doing. This includes reviewing their fair value statements to ensure they demonstrate their service provides value for clients.

CEOs were written to three times in under two years about the importance of their firms ensuring retirement income leads to good customer outcomes

It’s also important to review your ongoing advice policy to ensure it clearly confirms the services clients will receive, the disengagement process and the process for paying refunds where services are not delivered in accordance with the client agreement.

Firms should also ensure they monitor their ongoing advice service appropriately. Historically, business assurance has focussed on new business but, with the vast majority of clients receiving ongoing advice, this needs to be a key focus of business assurance going forward.

3. Much-anticipated consolidation review

Consolidation has been a key feature of our sector for many years. Given the FCA’s last thematic review was in 2017, it is no surprise to read it is planning thematic work in this area.

With the vast majority of clients receiving ongoing advice, this needs to be a key focus of business assurance going forward

Consolidators should review their business plans, strategy documents, policies and procedures, including integration plans and management information, in advance of the thematic review. It is important to be able to demonstrate clients are receiving clear communication and good outcomes.

The FCA has explicitly stated firms should undertake adequate due diligence on client books. With its key priority of reducing and preventing serious consumer harm, it is important firms can demonstrate the work they have undertaken where the due diligence on the client bank and more general due diligence identifies concerns.

David Boyhan is technical director at TCC

VINTED went down this morning, leaving hundreds of shoppers and sellers locked out of their accounts.

Between 9am and 10.40am, over 717 users reported issues with the second-hand marketplace on DownDetector.

2

2

According to the website, over 78% of customers could not use the app.

Another 19% said they could not log in to their account on the website.

It soon became clear that the issue was not due to a glitch but rather “scheduled maintenance”.

Affected users received the following message when trying to log in: “Vinted is temporarily down for scheduled maintenance.

“We’re making improvements to Vinted which will take a few hours to successfully complete.

“This will delay some of the activities you may be running on the platform, but they will resume once the system is back up.

“We’re sorry for the inconvenience caused by this. Thanks for your patience.”

People took to X (formally Twitter) to complain.

One user said: “Vinted is down are you kidding me.”

Another said: “Is there an issue with the app today? I keep getting an error.”

“The scheduled maintenance better improve the servers and add a feature to filter by price,” said a third user.

One customer told The Sun that they’re still getting notifications about sales but can’t click through to view what items have been purchased.

We’re making improvements to Vinted which will take a few hours to successfully complete

Vinted

However, others joked about the temporary outage, with one user saying: “The amount of money I’m saving right now because Vinted is down is crazy.”

Vinted last went down at the end of October when more than 1,000 users complained about being unable to use the second-hand marketplace.

Payments won’t be affected

As the issue was related to scheduled maintenance, the temporary outage should not have affected your payments.

However, if you’re struggling to get your cash from Vinted, get in touch through the app (once it’s back up) and let customer service know you haven’t received your money.

You’ll usually need to provide evidence to show you haven’t received the money, such as your latest bank statements.

This will delay some of the activities you may be running on the platform, but they will resume once the system is back up

Vinted

There is also information on Vinted’s help page for users who haven’t seen their money hit their bank account.

Visit vinted.co.uk/help/73-my-withdrawal-has-failed to find out more.

You can contact the website’s member support team directly via the app if you are still experiencing issues.

If you’re still having issues or aren’t happy with how you have been treated, you may be able to complain to a third-party dispute resolution service, such as Complain.biz.

More Vinted news

Vinted launched a “pro” version of the app last month, which allows sellers to register as sole traders and be identified as professional sellers

The upgrade is free to use and users can sell unlimited items for free.

However, The Sun revealed the second-hand seller had paused new registrations to its professional selling feature after it made some users’ National Insurance (NI) numbers available, putting them at risk of fraud.

HM Revenue & Customs (HMRC) advises that you should not share your NI number with anyone who does not need it to prevent identity fraud.

The Sun has learned that the Independent Commissioner’s Office (ICO) is investigating the breach after several sellers reported it.

Commenting on the issue, a spokesperson for Vinted said: “For a small number of Vinted Pro members, their NI number was visible on their profile page.

“While our teams were working on fixing the issue completely, we temporarily halted the ability to upgrade accounts to Vinted Pro.

“We apologise to anyone that was affected and encourage members who have questions to reach out to our member support team.”

Do you need to pay tax on items sold on Vinted?

QUICK facts on tax from the team at Vinted…

- The only time that an item might be taxable is if it sells for more than £6,000 and there is profit (sells for more than you paid for it). Even then, you can use your capital gains tax-free allowance of £3,000 to offset it.

- Generally, only business sellers trading for profit (buying goods with the purpose of selling for more than they paid for them) might need to pay tax. Business sellers who trade for profit can use a tax-free allowance of £1,000, which has been in place since 2017.

- More information here: vinted.co.uk/no-changes-to-taxes

Money

Six ways to save water and slash energy bills by £200 a year including money-guzzling device to switch off

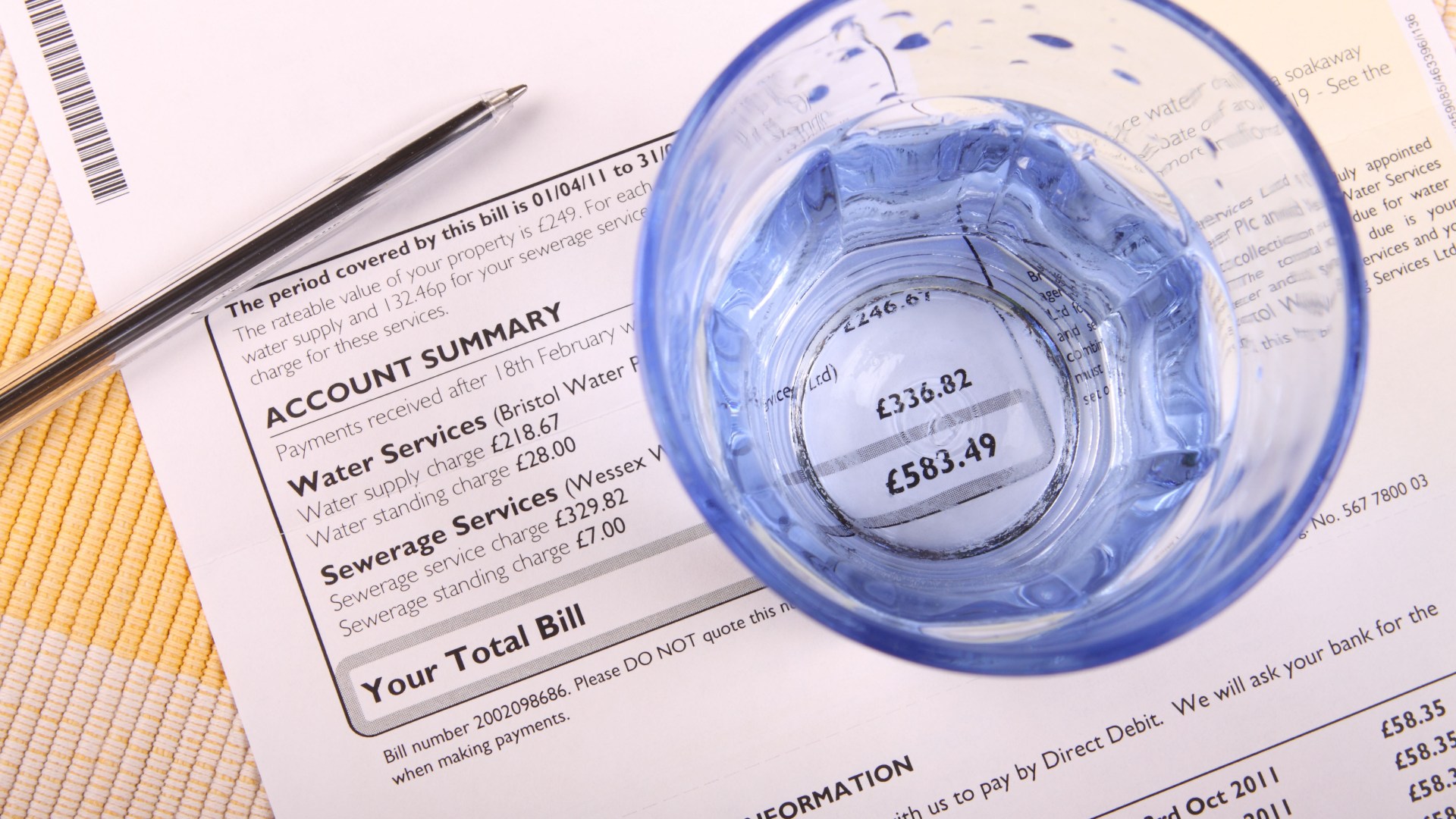

MILLIONS of households could save money on their water bills by making just six simple changes to how they use water.

Annual water bills are set to rise by about £27.40 to £473 from next year, according to water regulator Ofwat.

1

Between 2025 and 2030 they are forecast to rise again by an average of £19 a year.

The increases will put pressure on households already finding it difficult to make ends meet.

Around 18% of households are already struggling to pay their bills but this will climb to 40% if the changes go ahead, according to the Consumer Council for Water.

But experts at bathroom supplier Wholesale Domestic say a family of four who make small changes to their home could save more than £200 a year.

Read more on household bills

Switch to water-efficient fixtures – £50

“One of the simplest and most effective ways to save money on your energy bills is to use water-efficient fixtures,” said Brian Toward from Wholesale Domestic.

“Modern showers and taps come with aerators and flow restrictors that reduce water usage without compromising on pressure.”

The devices are very easy to install and can be fitted either inside the spout of a tap or attached to the end of it.

Prices start at around £6.50 for four.

Meanwhile, a shower head aerator is installed in the same way as a basic shower head, which means they are one of the easiest ways to reduce your water consumption.

You can pick up one of the devices for about £8.

Switching to a water-saving shower head could reduce the water you use by up to 40%.

Overall, a family of four could save around £50 a year by cutting down their water consumption with these efficient fixtures.

Lower the temperature of your water heater – £50

Your water heater temperature controls how hot water will be when it comes out of your tap or shower head.

But most households have it set far higher than needed explains Mr Toward.

How to save on your energy bills

SWITCHING energy providers can sound like a hassle – but fortunately it’s pretty straight forward to change supplier – and save lots of cash.

Shop around – If you’re on an SVT deal you are likely throwing away up to £250 a year. Use a comparion site such as MoneySuperMarket.com, uSwitch or EnergyHelpline.com to see what deals are available to you.

The cheapest deals are usually found online and are fixed deals – meaning you’ll pay a fixed amount usually for 12 months.

Switch – When you’ve found one, all you have to do is contact the new supplier.

It helps to have the following information – which you can find on your bill – to hand to give the new supplier.

- Your postcode

- Name of your existing supplier

- Name of your existing deal and how much you payAn up-to-date meter reading

It will then notify your current supplier and begin the switch.

It should take no longer than three weeks to complete the switch and your supply won’t be interrupted in that time.

“By reducing your water heater temperature to around 55°C you can still have hot showers without wasting excess energy,” he said.

“Lowering the thermostat even slightly can make a significant difference over time and save you around £45-50 a year.

Most water heaters will have a knob on the front which controls the water temperature.

Turn this to the left to reduce its flow temperature.

Do not turn your temperature down too much as this could cause harmful bacteria to grow in the water.

Take shorter showers – £20

It’s an age old tip but reducing the length of your shower can help you to save significantly on your water bills.

Heating accounts for a large part of every household’s energy consumption.

“If every member of your household reduces their shower time by just one minute, you could save hundreds of litres of water each month,” Mr Toward suggests.

“Based on a family of four this could be a saving of around £20 a year in energy bills.”

Fix dripping and leaking fixtures – £35

Although the amount of water coming out of a leaking tap may look small, it can slowly add up over the course of a year.

“A slow-dripping tap can waste up to 5,500 litres of water a year,” Mr Toward warns.

“Not only is it a waste of water but it’s a direct hit to your energy bills if it’s a hot tap.”

If you get it fixed you could save up to £35 a year based on UK water heating costs.

Leaking toilets are another culprit.

Toilets take up about 30% of the total water used in a household according to water saving organisation Save Water Save Money.

A constantly running toilet can waste over 200 litres of water a day.

Install a thermostatic mixer shower – £30

If you have an electric shower, consider changing to a thermostatic mixer shower.

These showers mix hot and cold water more precisely than an electric shower which can prevent overheating and wasted energy.

By doing so they can help to regulate water temperature more effectively and reduce the energy needed to heat the water.

Prices start from around £75.

Swapping to a thermostatic shower can shave around £30 a year off your energy bill, especially if combined with a more efficient boiler.

Use your towel dryer wisely – £20

Towel radiators and heated towel rails have become popular in many bathrooms but they can waste energy if not used wisely.

Mr Toward advises: “Limit the time you have your towel rail on as many are left running for far longer than necessary, which can eat up electricity.”

Instead, set a timer or use a programmable rail to save between £15 and £20 annually.

How else can I save on my household bills?

You could apply for a water meter to shave hundreds of pounds off your water bill every year.

Water meters charge you for the amount of water you use, so consider your household use before you get one.

If you get through a lot of water then it may not be worth getting one.

The Consumer Council for Water has a free water meter calculator which will tell you how much you could save.

Meanwhile, you could get water-saving devices from your water company.

Get in touch with your supplier for more information or visit savewatersavemoney.co.uk.

Companies also cap the bills of households who are struggling through the WaterSure scheme.

To apply you must be on benefits and need to use lots of water for medical reasons or because your household has a certain number of children.

You must have a water meter or be waiting to get one installed.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

He will manage the industrial and logistic company’s relationships with its capital partners and the formation of new managed vehicles.

The post PLP appoints William Sprott as head of investment management appeared first on Property Week.

-

Science & Environment2 months ago

Science & Environment2 months agoHow to unsnarl a tangle of threads, according to physics

-

Technology1 month ago

Technology1 month agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment2 months ago

Science & Environment2 months agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment2 months ago

Science & Environment2 months ago‘Running of the bulls’ festival crowds move like charged particles

-

Technology2 months ago

Technology2 months agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment1 month ago

Science & Environment1 month agoX-rays reveal half-billion-year-old insect ancestor

-

Money1 month ago

Money1 month agoWetherspoons issues update on closures – see the full list of five still at risk and 26 gone for good

-

Science & Environment2 months ago

Science & Environment2 months agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Science & Environment2 months ago

Science & Environment2 months agoSunlight-trapping device can generate temperatures over 1000°C

-

Sport1 month ago

Sport1 month agoAaron Ramsdale: Southampton goalkeeper left Arsenal for more game time

-

Science & Environment2 months ago

Science & Environment2 months agoPhysicists have worked out how to melt any material

-

Technology1 month ago

Technology1 month agoGmail gets redesigned summary cards with more data & features

-

Football1 month ago

Football1 month agoRangers & Celtic ready for first SWPL derby showdown

-

MMA1 month ago

MMA1 month ago‘Dirt decision’: Conor McGregor, pros react to Jose Aldo’s razor-thin loss at UFC 307

-

Technology1 month ago

Technology1 month agoUkraine is using AI to manage the removal of Russian landmines

-

News1 month ago

News1 month agoWoman who died of cancer ‘was misdiagnosed on phone call with GP’

-

Science & Environment2 months ago

Science & Environment2 months agoLaser helps turn an electron into a coil of mass and charge

-

Sport1 month ago

Sport1 month agoBoxing: World champion Nick Ball set for Liverpool homecoming against Ronny Rios

-

Technology1 month ago

Technology1 month agoEpic Games CEO Tim Sweeney renews blast at ‘gatekeeper’ platform owners

-

Business1 month ago

how UniCredit built its Commerzbank stake

-

Science & Environment2 months ago

Science & Environment2 months agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Science & Environment2 months ago

Science & Environment2 months agoLiquid crystals could improve quantum communication devices

-

Technology1 month ago

Technology1 month agoRussia is building ground-based kamikaze robots out of old hoverboards

-

News1 month ago

News1 month ago‘Blacks for Trump’ and Pennsylvania progressives play for undecided voters

-

Technology1 month ago

Technology1 month agoSamsung Passkeys will work with Samsung’s smart home devices

-

MMA1 month ago

MMA1 month agoDana White’s Contender Series 74 recap, analysis, winner grades

-

Science & Environment2 months ago

Science & Environment2 months agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment2 months ago

Science & Environment2 months agoWhy this is a golden age for life to thrive across the universe

-

Technology1 month ago

Technology1 month agoMicrosoft just dropped Drasi, and it could change how we handle big data

-

MMA1 month ago

MMA1 month ago‘Uncrowned queen’ Kayla Harrison tastes blood, wants UFC title run

-

News1 month ago

News1 month agoNavigating the News Void: Opportunities for Revitalization

-

Entertainment1 month ago

Entertainment1 month agoBruce Springsteen endorses Harris, calls Trump “most dangerous candidate for president in my lifetime”

-

MMA1 month ago

MMA1 month agoPereira vs. Rountree prediction: Champ chases legend status

-

News1 month ago

News1 month agoMassive blasts in Beirut after renewed Israeli air strikes

-

Technology1 month ago

Technology1 month agoCheck, Remote, and Gusto discuss the future of work at Disrupt 2024

-

Sport1 month ago

Sport1 month ago2024 ICC Women’s T20 World Cup: Pakistan beat Sri Lanka

-

News1 month ago

News1 month agoRwanda restricts funeral sizes following outbreak

-

TV1 month ago

TV1 month agoসারাদেশে দিনব্যাপী বৃষ্টির পূর্বাভাস; সমুদ্রবন্দরে ৩ নম্বর সংকেত | Weather Today | Jamuna TV

-

Technology1 month ago

Technology1 month agoWhy Machines Learn: A clever primer makes sense of what makes AI possible

-

Technology1 month ago

Technology1 month agoMicrophone made of atom-thick graphene could be used in smartphones

-

Business1 month ago

Business1 month agoWater companies ‘failing to address customers’ concerns’

-

News1 month ago

News1 month agoCornell is about to deport a student over Palestine activism

-

Business1 month ago

Business1 month agoWhen to tip and when not to tip

-

Business1 month ago

Top shale boss says US ‘unusually vulnerable’ to Middle East oil shock

-

News1 month ago

News1 month agoHull KR 10-8 Warrington Wolves – Robins reach first Super League Grand Final

-

Sport1 month ago

Sport1 month agoWXV1: Canada 21-8 Ireland – Hosts make it two wins from two

-

Science & Environment2 months ago

Science & Environment2 months agoQuantum forces used to automatically assemble tiny device

-

News2 months ago

News2 months ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

MMA1 month ago

MMA1 month agoKayla Harrison gets involved in nasty war of words with Julianna Pena and Ketlen Vieira

-

Technology1 month ago

Technology1 month agoSingleStore’s BryteFlow acquisition targets data integration

-

Football1 month ago

Football1 month ago'Rangers outclassed and outplayed as Hearts stop rot'

-

Science & Environment2 months ago

Science & Environment2 months agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment2 months ago

Science & Environment2 months agoA slight curve helps rocks make the biggest splash

-

Technology2 months ago

Technology2 months agoMeta has a major opportunity to win the AI hardware race

-

Science & Environment2 months ago

Science & Environment2 months agoNuclear fusion experiment overcomes two key operating hurdles

-

Sport1 month ago

Sport1 month agoChina Open: Carlos Alcaraz recovers to beat Jannik Sinner in dramatic final

-

Football1 month ago

Football1 month agoWhy does Prince William support Aston Villa?

-

Technology1 month ago

Technology1 month agoLG C4 OLED smart TVs hit record-low prices ahead of Prime Day

-

News1 month ago

News1 month ago▶ Hamas Spent $1B on Tunnels Instead of Investing in a Future for Gaza’s People

-

Technology1 month ago

Technology1 month agoMusk faces SEC questions over X takeover

-

MMA1 month ago

MMA1 month agoPennington vs. Peña pick: Can ex-champ recapture title?

-

Sport1 month ago

Sport1 month agoPremiership Women’s Rugby: Exeter Chiefs boss unhappy with WXV clash

-

Sport1 month ago

Sport1 month agoShanghai Masters: Jannik Sinner and Carlos Alcaraz win openers

-

Sport1 month ago

Sport1 month agoCoco Gauff stages superb comeback to reach China Open final

-

Womens Workouts1 month ago

Womens Workouts1 month ago3 Day Full Body Women’s Dumbbell Only Workout

-

Technology1 month ago

Technology1 month agoUniversity examiners fail to spot ChatGPT answers in real-world test

-

Business1 month ago

Bank of England warns of ‘future stress’ from hedge fund bets against US Treasuries

-

Sport1 month ago

Sport1 month agoSturm Graz: How Austrians ended Red Bull’s title dominance

-

MMA1 month ago

MMA1 month ago‘I was fighting on automatic pilot’ at UFC 306

-

News1 month ago

News1 month agoGerman Car Company Declares Bankruptcy – 200 Employees Lose Their Jobs

-

Sport1 month ago

Sport1 month agoWales fall to second loss of WXV against Italy

-

Business1 month ago

DoJ accuses Donald Trump of ‘private criminal effort’ to overturn 2020 election

-

Business1 month ago

Sterling slides after Bailey says BoE could be ‘a bit more aggressive’ on rates

-

TV1 month ago

TV1 month agoTV Patrol Express September 26, 2024

-

Money4 weeks ago

Money4 weeks agoTiny clue on edge of £1 coin that makes it worth 2500 times its face value – do you have one lurking in your change?

-

Science & Environment2 months ago

Science & Environment2 months agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment2 months ago

Science & Environment2 months agoNerve fibres in the brain could generate quantum entanglement

-

Travel1 month ago

World of Hyatt welcomes iconic lifestyle brand in latest partnership

-

Technology1 month ago

Technology1 month agoQuoroom acquires Investory to scale up its capital-raising platform for startups

-

MMA1 month ago

MMA1 month agoKetlen Vieira vs. Kayla Harrison pick, start time, odds: UFC 307

-

Technology1 month ago

Technology1 month agoThe best shows on Max (formerly HBO Max) right now

-

Technology1 month ago

Technology1 month agoIf you’ve ever considered smart glasses, this Amazon deal is for you

-

MMA1 month ago

MMA1 month agoHow to watch Salt Lake City title fights, lineup, odds, more

-

Technology1 month ago

Technology1 month agoJ.B. Hunt and UP.Labs launch venture lab to build logistics startups

-

Technology1 month ago

Technology1 month agoAmazon’s Ring just doubled the price of its alarm monitoring service for grandfathered customers

-

Business1 month ago

Italy seeks to raise more windfall taxes from companies

-

Business1 month ago

‘Let’s be more normal’ — and rival Tory strategies

-

Business1 month ago

The search for Japan’s ‘lost’ art

-

Sport1 month ago

Sport1 month agoURC: Munster 23-0 Ospreys – hosts enjoy second win of season

-

Sport1 month ago

Sport1 month agoNew Zealand v England in WXV: Black Ferns not ‘invincible’ before game

-

Sport1 month ago

Sport1 month agoMan City ask for Premier League season to be DELAYED as Pep Guardiola escalates fixture pile-up row

-

News2 months ago

News2 months ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Science & Environment2 months ago

Science & Environment2 months agoHow to wrap your mind around the real multiverse

-

MMA1 month ago

MMA1 month agoUFC 307’s Ketlen Vieira says Kayla Harrison ‘has not proven herself’

-

News1 month ago

News1 month agoTrump returns to Pennsylvania for rally at site of assassination attempt

-

MMA1 month ago

MMA1 month agoKevin Holland suffers injury vs. Roman Dolidze

-

Technology4 weeks ago

Technology4 weeks agoThe FBI secretly created an Ethereum token to investigate crypto fraud

-

Business1 month ago

Business1 month agoStocks Tumble in Japan After Party’s Election of New Prime Minister

-

Technology1 month ago

Technology1 month agoTexas is suing TikTok for allegedly violating its new child privacy law

-

Technology1 month ago

Technology1 month agoOpenAI secured more billions, but there’s still capital left for other startups

You must be logged in to post a comment Login