Money

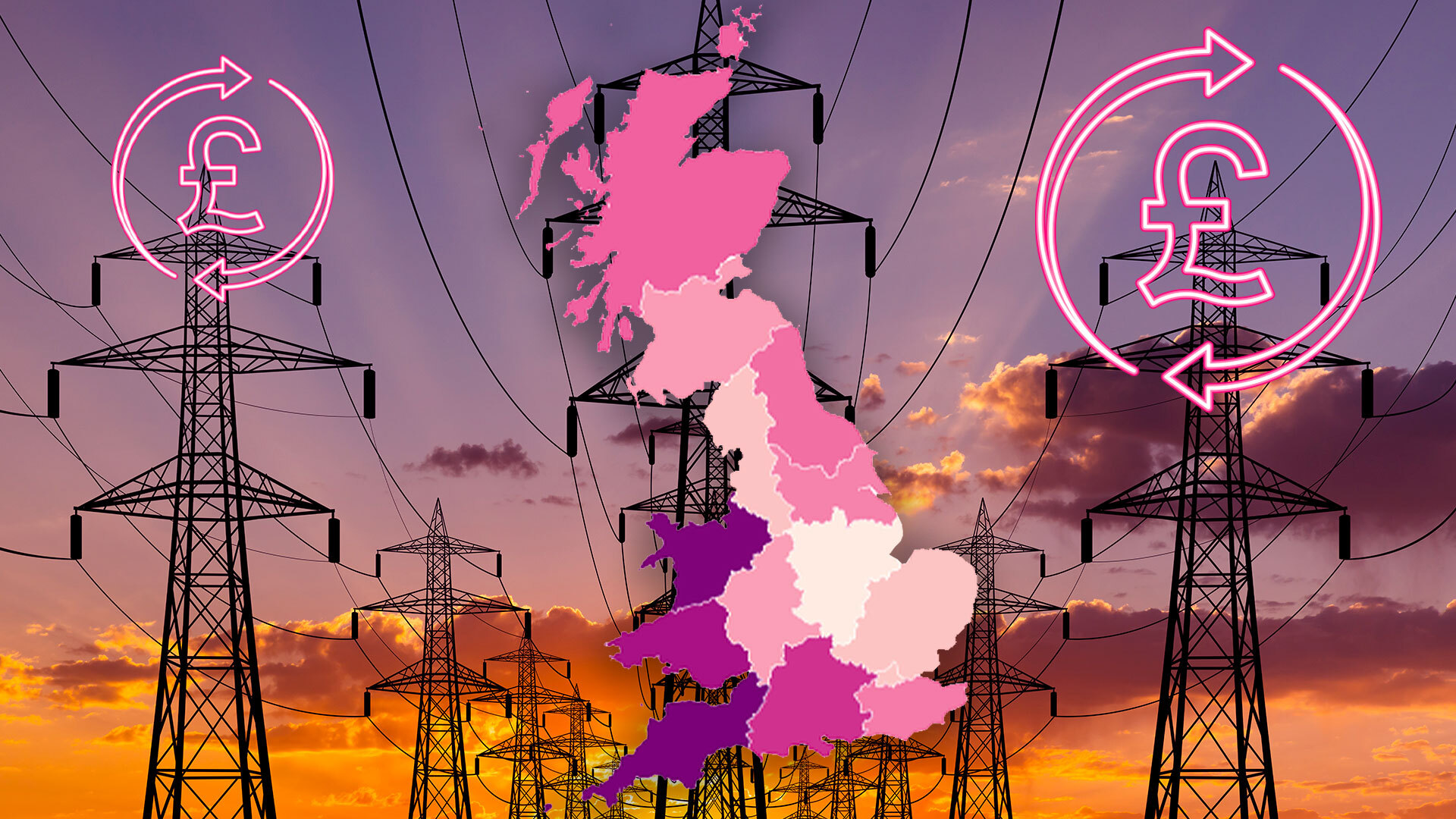

Map reveals how much energy bills will rise in your area from today – and why you could pay MORE than the price cap

MILLIONS will see their energy bill rise by £149 as Ofgem’s new price cap comes into force today, Tuesday, October 1.

Households previously paid £1,568 a year but the figure is now set to rise by nearly £150 to £1,717.

Around 29million customers on their energy providers’ standard variable tariff (SVT) are expected to see their bills rise.

Ofgem updates its price cap every three months, setting a ceiling on how much suppliers can charge for each unit of gas or electricity.

It was created five years ago to protect customers from being overcharged by suppliers.

This includes your standing charge which is a daily fixed amount you have to pay no matter how much electricity you use.

But it is worth bearing in mind that the £1,717 figure is just an estimation given by the energy regulator.

It is calculated assuming that a typical household uses 2,700 kWh of electricity and 11,500 kWh of gas over a 12-month period.

Those who use less electricity will pay less, while those who use more will have to pay more.

The exact amount you pay is based on several factors, including where you live, your supplier and how you pay for your gas and electricity.

There are 14 different “Distribution Network Operators” across Britain, who can dictate your energy costs.

For example, those in Northern Scotland will see their bills rise to £1724.47 up from £1577.66 starting today.

While households in North West of England will see their bills increase to £1,689 up from £1,533.

Those in the South West will pay the most, with the average annual bill costing £100 more at £1,766 a year.

These varying prices occur because generating gas or energy is cheaper in some areas than others.

Your regional standing charge, which is how much you pay to stay connected to the grid, also varies depending on where you live.

For example, those living in the northern region (North East England) pay the highest standing charge in the country.

A typical household here will now be charged £379 as of today.

While prices are expected to be high for the next three months, experts are predicting a fall come January.

Cornwall Insight has published a new forecast predicting a £20 drop in the new year to £1,697.

Dr Craig Lowrey, principal consultant at Cornwall Insight said October’s rise is a “temporary blip”.

He said: “Typically some of the coldest months of the year, often bring with them the biggest energy bills, and – while our latest forecast is welcome news – it remains subject to the volatile wholesale gas and electricity markets.”

Why you could be charged more

If you are worried about the price of the regional standing charge in your area, it is worth being aware of these tips.

For example, taking regular meter readings can let you update your supplier on your energy usage so you are not overcharged.

It is important to take a meter reading around the time of the price cap change to make sure all your energy usage up until that point is charged at the lower rate.

If you are confused about how to take a meter reading you can read our article here.

How do I calculate my energy bill?

BELOW we reveal how you can calculate your own energy bill.

To calculate how much you pay for your energy bill, you must find out your unit rate for gas and electricity and the standing charge for each fuel type.

The unit rate will usually be shown on your bill in p/kWh.The standing charge is a daily charge that is paid 365 days of the year – irrespective of whether or not you use any gas or electricity.

You will then need to note down your own annual energy usage from a previous bill.

Once you have these details, you can work out your gas and electricity costs separately.

Multiply your usage in kWh by the unit rate cost in p/kWh for the corresponding fuel type – this will give you your usage costs.

You’ll then need to multiply each standing charge by 365 and add this figure to the totals for your usage – this will then give you your annual costs.

Divide this figure by 12, and you’ll be able to determine how much you should expect to pay each month from April 1.

If you have a smart meter then you do not need to take a reading as this does it automatically.

You should contact your supplier if you are keen to install one as it is usually done free of charge.

There are also a number of government support packages available to those who are struggling financially.

The Sun recently published an article on all the bill help worth over £5,000 which you can check out here.

Make sure you pay the lowest rates

There are two types of rates that you can pay on your energy bill, fixed or a standard variable rate.

A fix is when you lock in a set price for a certain period which is usually 12 months.

That is different to a standard variable rate which can go up or down depending on Ofgem’s price cap, which changes every three months.

A number of energy suppliers have reduced the rate of their fixed deals, meaning customers have a chance to save if they switch.

For example, EDF has launched a 1,568-a-year fixed deal for a typical energy user paying by direct debit.

This deal is £149 cheaper than the upcoming cap.

It is worth bearing in mind that you will still be charged more if you use more energy.

You check out the best fix rate deals below:

Money

My neighbour piled heaps of dirt to peer OVER my 6ft fence & into my garden – but I told on them & won

A HOMEOWNER was ordered to flatten their garden after raising its height to peer over their neighbour’s 6ft fence.

An argument broke out after the offender piled dirt to create a terrace which caused a “significant degree of overlooking”.

3

3

The resident, who lives in Dinas Powys in Wales, laid artificial grass over the raised bed for a barbeque and summer house – all the same height as their patio doors.

Furious by the lack of privacy, the neighbour complained to the local council.

Council staff paid a visit and were not impressed with what they saw.

The Vale of Glamorgan’s planning committee found that the height of the garden had been increased by 600mm and would need to be lowered by 300mm.

However, the resident refused to flatten their garden and instead submitted a planning application.

It was denied by the council, who deemed the change to the garden and the infringement on their neighbour’s privacy “unacceptable”.

A Vale of Glamorgan Council spokesperson told The Sun: “Every planning application is different with each considered on its merits.

“In this case, it was decided that the development would involve and unacceptable loss of privacy for a neighbouring property so the application was rejected.”

Whilst the majority of councillors on the planning committee agreed that the garden’s height was inappropriate, Cllr Christine Cave said the decision was “hypocritical “.

A former primary school in the area had portable homes erected through special planning powers.

The temporary accommodation was passed for Ukrainian refugees, but the councillor argued that they were tall enough to see into people’s gardens – like the raised garden.

“When we made the site visit [to Eagleswell in Llantwit Major] and we actually asked why the ground had been built up and why the buildings could then be overlooking into peoples’ gardens.

“This seems a bit hypocritical to me here, that the council have done exactly the same on a much grander scale with huge overlooking of peoples’ gardens and now we are being told it is not permissible.”

Vale of Glamorgan Council allowed the development of the site at Llantwit Major through what is known as permitted development rights.

The planning powers are usually used in an emergency, but the scheme must eventually get planning permission within 12 months of the construction starting.

The council’s planning committee voted to allow the 90 units permission to remain for a minimum of five more years.

3

For income investors, there are typically three legs to the stool – the yield, total return and a stable, or growing, dividend stream.

For income investors, there are typically three legs to the stool – the yield, total return and a stable, or growing, dividend stream.

Key to a successful strategy above all else is generating a real yield, ensuring income is not eroded by inflation over time.

Prior to the global financial crisis of 2008, when interest rates sat comfortably higher than inflation, this real yield was relatively easy to achieve.

Over the decade that followed, however, the economic environment reversed, with interest rates languishing below inflation, meaning cash held in the bank, and accordingly asset prices, lost value in real terms.

As long as rates remain above inflation, income investing once again looks more appealing

Subsequent rounds of quantitative easing suppressed yields on fixed-income assets and investors were forced to look to more growth-oriented assets.

Today, however, the picture looks very different. Inflation and interest rates have crossed over once again, with the former sitting below the latter. This creates an environment more favourable for both yields on bonds and equities.

While it is hard to say with certainty how long this will last, as long as rates remain above inflation, income investing once again looks more appealing.

In the case of fixed-income yields within the UK market, those available from both gilts and corporate bonds fell drastically in the aftermath of the financial crisis.

Income investors no longer need to look to riskier areas of the market to secure the same yield

However, with the base rate as it stands today, the economic backdrop is much more supportive of fixed-income yields. This is because fixed-income securities adjust to cash rates given the additional risk involved in investing in them.

The implication for income-seeking investors is that they no longer need to look to riskier areas of the market to secure the same yield. Instead, it is possible to remain in the relatively safe areas along the capital-risk spectrum.

In contrast, yields from equities have been relatively static over the last decade, as fixed-income yields dropped off and then subsequently rose strongly.

Yields from the UK equity market today stand at around 4% and at around 2% for global equities due to the dominance of the US, which has typically paid lower levels of income.

The outlook for dividends has been steadily improving, with strong gains posted year-on-year

But that is only part of the story.

Another major element to the overall picture is dividend stability. Dividends took a significant hit during the pandemic – in the UK to the tune of 40%, in part due to UK banks being forced to suspend payments and the impact of travel restrictions on oil companies’ profitability, both fertile sectors for income investors.

Since then, however, the outlook for dividends has been steadily improving, with strong gains posted year-on-year.

Indeed, in the first quarter of 2024, some 93% of dividend paying companies globally either increased their payouts or held them steady, demonstrating the robustness of these businesses as a source of income. Even firms considered high growth stocks – the likes of Meta and Alibaba – started to pay a dividend, albeit from a low base.

The combination of these elements means it is now possible to secure much higher levels of yield without incurring additional risk.

Investors might consider adding some spicier funds to the mix offering exposure to high yield debt, or equity strategies that employ an options overlay

Nonetheless, it is important to blend income styles with strategies that reinvest dividends to secure the compounding effect, thereby producing an attractive total return complemented by more defensive approaches focused on more stable or growing dividend streams – stocks that are sometimes referred to as bond-proxies.

These may lag in more exuberant market conditions but their return profile tends to be steadier, with the added attraction of offering some downside protection.

Finally, investors might consider adding some spicier funds to the mix offering exposure to high-yield debt, or, on the equities side, strategies that employ an options overlay to enhance income, albeit by sacrificing some capital appreciation.

The implications for income investors, typically those in or approaching retirement and therefore needing to replace a salary with an alternative source of income, are important.

Earlier this year, the Financial Conduct Authority’s review of the pensions freedoms introduced some 10 years ago found income portfolios had been largely neglected for such individuals.

While annuities are once again looking attractive as a means of delivering a baseline level of retirement income, a much broader range of natural income generating solutions are now coming into play that sit above that, helping to ensure that, in retirement, the financial liabilities linked to funding a comfortable lifestyle can continue to be met.

Daniel Pereira is investment manager at Square Mile Investment Consulting and Research

AN online calculator can reveal exactly how much your bills will increase by this winter following today’s energy price cap rise.

Bills are set to increase for millions of households after energy regulator Ofgem increased the maximum price firms can charge consumers for energy.

1

The energy price cap has risen from £1,568 a year to £1,717 from today, affecting millions of customers on standard variable tariffs.

The average household paying by direct debt for dual fuel can expect to see their annual bill go up by about £149 annually, or around £12 a month – a 10% increase.

But bear in mind the exact amount you pay could be higher or lower than this depending on your usage and the tariff you are on.

To help consumers find out exactly what they’ll be paying in energy costs this winter AI household money-saver Nous.co has created an online calculator.

As well as calculating your bills Nous.co can also help you find deals that might save you money as well as suggesting tips for reducing usage.

Nous.co co-founder and chief executive, Greg Marsh, said: “Lots of UK households will again be struggling with gas and electricity bills this winter, and some may even be forced to make the tough choice between heating and other essentials.

“It’s crucial to make sure you’re not overpaying for your bills. Fortunately – there are savings to be made if you’re smart about it.

“Simple things like adjusting your thermostat, monitoring your credit balance, taking regular meter readings and switching off unused appliances can help keep costs down.

“Most households can also save the better part of £150 on their energy bills, without committing to a fixed deal, plus hundreds more on their mobile and broadband by switching providers”

You can find Nous.co’s calculator here.

Ofgem estimates around 29million households on standard variable tariffs will be affected by the increased price cap.

The increases set out by the regulator apply to average-use households, but this can vary considerably.

That’s because those figures are calculated assuming that a typical household uses 2,900 kWh of electricity and 12,000 kWh of gas across a 12-month period.

If you use more than this the price will be higher as it is the unit cost that is capped not the overall amount billed.

So from today the price a supplier can charge for gas has risen from 5.48p per kWh, to 6.24p.

The price of electricity has also risen from 22.36p per kWh to 24.50p.

Meanwhile, standing charges, which cover things like maintaining the network and operational costs, have risen to 31.66p from 31.41p a day for gas and from 60.12p to 60.99p for electricity.

The way you pay for energy can also impact how much you pay and the £1,717 price cap applies specifically to those who pay by direct debit.

For those on prepayment meters the cap is £1,669 for an average household and it stands at £1,829 for those paying on receipt of bills.

If you’re on a fixed tariff there will be no change to your bill, as you’ve locked in the price for a set period.

If you haven’t already it’s important to take and submit a meter reading today to ensure you pay the lower rate for energy usage up until the point the price is increased.

If you don’t do this, you will be given an estimated bill which means some of your energy usage before October 1 could be charged at the new higher rate.

If you have a smart meter, you don’t need to take a reading as information is automatically sent to your supplier.

Despite the price cap rise, average bills remain considerably lower than during the peak of the energy crisis, which was fuelled by Russia’s invasion of Ukraine in February 2022.

The war caused a spike in an already turbulent wholesale energy market, driving up costs for suppliers and customers.

The new cap is £117 – 6% – cheaper compared to the same period last year when it stood at £1,834.

Before the energy price shock a standard annual bill was £1,084.

The energy price cap is adjusted every three months to reflect changes in underlying costs.

The price cap for January 1 to 31 March 2025, will be published on November 25.

If you’re worried about costs this winter MoneySavingExpert.com’s Martin Lewis has revealed how households can save money on their energy bills.

What energy bill help is available?

THERE’S a number of different ways to get help paying your energy bills if you’re struggling to get by.

If you fall into debt, you can always approach your supplier to see if they can put you on a repayment plan before putting you on a prepayment meter.

This involves paying off what you owe in instalments over a set period.

If your supplier offers you a repayment plan you don’t think you can afford, speak to them again to see if you can negotiate a better deal.

Several energy firms have grant schemes available to customers struggling to cover their bills.

But eligibility criteria varies depending on the supplier and the amount you can get depends on your financial circumstances.

For example, British Gas or Scottish Gas customers struggling to pay their energy bills can get grants worth up to £2,000.

British Gas also offers help via its British Gas Energy Trust and Individuals Family Fund.

You don’t need to be a British Gas customer to apply for the second fund.

EDF, E.ON, Octopus Energy and Scottish Power all offer grants to struggling customers too.

Thousands of vulnerable households are missing out on extra help and protections by not signing up to the Priority Services Register (PSR).

The service helps support vulnerable households, such as those who are elderly or ill, and some of the perks include being given advance warning of blackouts, free gas safety checks and extra support if you’re struggling.

Get in touch with your energy firm to see if you can apply.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

Brooks Macdonald’s new group chief executive Andrea Montague officially begins her role today (1 October).

The company confirmed in a short statement that Montague has received regulatory approval.

She was appointed in June following the retirement of CEO Andrew Shepherd after 22 years with the firm.

Montague joined the company as a chief finance officer in 2023. Previous roles include group chief risk officer at Aviva and senior roles at Standard Life and Royal London Group.

Montague, who grew up in Belfast, studied languages at Heriot-Watt University in Edinburgh. Her formative years were spent at PwC, where she qualified as a chartered accountant.

She told Money Marketing in May that Brooks Macdonald has an ambitious plan to become a top five wealth manager in the UK through both organic and inorganic growth

“I’ve got the responsibility for finance, M&A and strategy. I’m lucky to have a really strong team, which has allowed me to lean into the strategy piece for the board. So, I can think about the bigger picture and how we set up for success,” she said.

Brooks Macdonald, which was founded in 1991, oversees £18bn in funds under management. The firm provides wealth management services in the UK and internationally.

The sale of Brooks Macdonald Asset Management comes after the group had announced a strategic review as it focuses on its “core activities of high-quality investment management and financial planning within the UK”.

Money

Tens of thousands of households to get council tax reduced again after lifeline scheme extended – can you claim too?

TENS of thousands of households will get huge council tax reductions of up to 100% after a vital scheme was extended.

Officials at Durham County Council last week approved the continuation of the Council Tax Reduction scheme for households on low incomes.

1

Around 53,800 people in County Durham currently benefit from the discount, the local authority said.

Of this number more than 41,000 people receive the maximum 100% discount.

But Durham is not the only council to offer the scheme, which provides a vital lifeline to thousands of households struggling to make ends meet.

Council Tax Reduction is available nationwide to those who are on a low income or claim benefits.

If you are eligible you usually will not get an actual payment.

Instead, the council will reduce the amount of tax you have to pay.

You can apply if you own your home, rent, are unemployed or are working.

The amount you get depends on several factors including: where you live, your income, the number of children you have, the benefits you claim, your savings and pension.

Whether you qualify or not will depend on your council’s individual criteria.

How do I apply?

You need to apply directly to your local council to receive the discount.

There should be information on its website about the types of discounts and exemptions available and how to apply for them.

You can find out who your local council is by visiting gov.uk/apply-council-tax-reduction.

In your application your local council will ask you for details about your income and circumstances so they can work out if you are entitled to the reduction.

They will then calculate your bill and will tell you how much council tax if any you need to pay.

What help is available?

Milton Keynes

Milton Keynes residents who are on a low income can apply for a council tax reduction of up to 80% of their tax bill.

Those who have reached the age of 66, at which point they can claim pension credit, can get help with up to 100% of the cost of their Council Tax.

You can apply for the deduction through the council’s online portal.

Once your claim has been processed the discount will usually start on the Monday after the council received your complete claim form.

What other council tax support is available?

THERE are several other ways you can also get discounts and reductions on your council tax bill.

In some cases, you can even get the bill completely wiped with a council tax reduction.

Factors such as your household income, whether you have children, and if you receive any benefits, will influence what you get.

To apply, visit https://www.gov.uk/apply-council-tax-reduction.

You’ll need your National Insurance number, bank statements, a recent payslip or letter from the Jobcentre, and a passport or driving licence when filling out the details.

Below, we reveal all the ways you can get discounts or a reduction on your bill:

Single person discount

If you live on your own, you can get 25% off your council tax bill.

This also applies if there is one adult and one student living together in a property, or if there is one adult and one person classed as severely mentally impaired in the home.

If you live with someone who doesn’t have to pay council tax, such as a carer or someone who is severely mentally impaired, you could get a larger reduction too, of up to 50%.

And, if you live in an all-student household, you could get a 100% discount.

Retirees

Pensioners may also find themselves eligible for a council tax reduction.

If you receive the Guarantee Credit element of Pension Credit, you could get a 100% discount.

If not, you could still get help if you have a low income and less than £16,000 in savings.

And a pensioner who lives alone will be entitled to a 25% discount too.

The discount will be paid directly into your Council Tax account and you will then receive a reduced bill.

Leeds

Households in Leeds can apply for a council tax discount of up to 75%.

The size of the discount depends on your income.

To be eligible you must not have savings, investments or property worth more than £16,000 unless you or your partner claim Pension Credit.

If you are a pensioner then you may be able to claim a 100% discount but the size of the reduction depends on your income and situation.

You can apply through the council’s online form or by calling 0113 222 4404.

Manchester

In Manchester council tax support is available but it will not cover all of your bill.

Working-age people in the city who are liable for Council Tax must still pay at least 15% of their bill.

What energy bill help is available?

THERE’S a number of different ways to get help paying your energy bills if you’re struggling to get by.

If you fall into debt, you can always approach your supplier to see if they can put you on a repayment plan before putting you on a prepayment meter.

This involves paying off what you owe in instalments over a set period.

If your supplier offers you a repayment plan you don’t think you can afford, speak to them again to see if you can negotiate a better deal.

Several energy firms have grant schemes available to customers struggling to cover their bills.

But eligibility criteria varies depending on the supplier and the amount you can get depends on your financial circumstances.

For example, British Gas or Scottish Gas customers struggling to pay their energy bills can get grants worth up to £2,000.

British Gas also offers help via its British Gas Energy Trust and Individuals Family Fund.

You don’t need to be a British Gas customer to apply for the second fund.

EDF, E.ON, Octopus Energy and Scottish Power all offer grants to struggling customers too.

Thousands of vulnerable households are missing out on extra help and protections by not signing up to the Priority Services Register (PSR).

The service helps support vulnerable households, such as those who are elderly or ill, and some of the perks include being given advance warning of blackouts, free gas safety checks and extra support if you’re struggling.

Get in touch with your energy firm to see if you can apply.

Council tax reductions will only help with the remaining 85%.

However, residents who are pension-age can still get help which will pay for their whole bill.

Generally, the less income you have the more help you can get to pay your council tax bill.

But if you have £16,000 or more in savings then you do not qualify for any support.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

Standard Life has partnered with Raindrop and launched a free-to-all pension-finding tool to help Britons track down their missing pensions.

This comes as Standard Life research has shown that 19% of people with multiple pensions believe they have lost track of at least one pension pot.

Standard Life, part of Phoenix Group, said that despite the benefits of consolidating pensions, such as a greater ability to track performance and boost understanding of how much is being saved for the future, 73% of those with more than one workplace pension said they have not consolidated.

Just under a third (32%) are unsure of how to start consolidating and 12% find the process too difficult.

It has been estimated that 2.8 million pension pots in the UK, valued at over £26.6bn, remain unclaimed. Additionally, the average person has at least 11 employers in their working lifetime.

In order to find a lost pension, a user just needs to provide their former employer’s name and the time period they worked for the company. This is in contrast to supplying details of the pension provider “as is often the case when consolidating pension pots”.

Raindrop’s technology then begins the tracing process, which on average takes just 4-6 weeks. During this time, a dedicated case manager is on-hand to provide updates on the process.

Once a person’s lost pensions have been traced, they will be better informed about their income prospects and able to take the necessary steps to prepare for their retirement.

Standard Life managing director of retail direct Dean Butler said: “We know that people who actively plan for their retirement are more confident and financially secure but if you don’t know where all your savings are, you can’t begin to calculate their value, making planning unnecessarily difficult.

“Sometimes people have a vague idea of having a pension with a previous employer, but just don’t know how to go about finding it. Our new pension-finding service removes the major hurdles that people face and allows them to regain control of their pensions savings. We want to help them trace any missing pensions, so they don’t ever lose them again and are better prepared to organise their retirement savings.”

Raindrop co-founder Vivan Shridharani added: “Millions of UK savers have lost pensions, often unsure of how to begin their search. As each new generation has more jobs than the last, the number of lost pensions continues to grow. We’re committed to helping savers, with a simple solution to easily find their lost pensions and help them better prepare for their financial future.

“By partnering with Standard Life, one of the UK’s largest pensions providers, we hope to empower savers to locate lost pots and take control of their long-term financial planning.”

Since the launch of Raindrop, a pension-finding platform, in 2021, it has located over £325m in lost pension savings across more than 27,000 pots.

In order to obtain these results, Standard Life commissioned Opinium to conduct research among 2,000 UK adults between 6 and 10 September 2024.

-

Womens Workouts1 week ago

Womens Workouts1 week ago3 Day Full Body Women’s Dumbbell Only Workout

-

Technology2 weeks ago

Technology2 weeks agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoHow to wrap your mind around the real multiverse

-

Science & Environment2 weeks ago

Science & Environment2 weeks ago‘Running of the bulls’ festival crowds move like charged particles

-

News1 week ago

News1 week agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoSunlight-trapping device can generate temperatures over 1000°C

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoLiquid crystals could improve quantum communication devices

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoPhysicists are grappling with their own reproducibility crisis

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoQuantum ‘supersolid’ matter stirred using magnets

-

News2 weeks ago

News2 weeks agoYou’re a Hypocrite, And So Am I

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoQuantum forces used to automatically assemble tiny device

-

Sport2 weeks ago

Sport2 weeks agoJoshua vs Dubois: Chris Eubank Jr says ‘AJ’ could beat Tyson Fury and any other heavyweight in the world

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoWhy this is a golden age for life to thrive across the universe

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoNuclear fusion experiment overcomes two key operating hurdles

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoCaroline Ellison aims to duck prison sentence for role in FTX collapse

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoLaser helps turn an electron into a coil of mass and charge

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoNerve fibres in the brain could generate quantum entanglement

-

News2 weeks ago

Israel strikes Lebanese targets as Hizbollah chief warns of ‘red lines’ crossed

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoCardano founder to meet Argentina president Javier Milei

-

Science & Environment1 week ago

Science & Environment1 week agoMeet the world's first female male model | 7.30

-

Womens Workouts1 week ago

Womens Workouts1 week agoBest Exercises if You Want to Build a Great Physique

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoWhy we need to invoke philosophy to judge bizarre concepts in science

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoBitcoin miners steamrolled after electricity thefts, exchange ‘closure’ scam: Asia Express

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoDZ Bank partners with Boerse Stuttgart for crypto trading

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoEthereum is a 'contrarian bet' into 2025, says Bitwise exec

-

Womens Workouts1 week ago

Womens Workouts1 week agoEverything a Beginner Needs to Know About Squatting

-

News1 week ago

News1 week agoFour dead & 18 injured in horror mass shooting with victims ‘caught in crossfire’ as cops hunt multiple gunmen

-

Womens Workouts1 week ago

Womens Workouts1 week ago3 Day Full Body Toning Workout for Women

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoA slight curve helps rocks make the biggest splash

-

News2 weeks ago

News2 weeks ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoQuantum time travel: The experiment to ‘send a particle into the past’

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoDorsey’s ‘marketplace of algorithms’ could fix social media… so why hasn’t it?

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoRedStone integrates first oracle price feeds on TON blockchain

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoBitcoin bulls target $64K BTC price hurdle as US stocks eye new record

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoLow users, sex predators kill Korean metaverses, 3AC sues Terra: Asia Express

-

Sport2 weeks ago

Sport2 weeks agoUFC Edmonton fight card revealed, including Brandon Moreno vs. Amir Albazi headliner

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoBlockdaemon mulls 2026 IPO: Report

-

News2 weeks ago

News2 weeks agoBrian Tyree Henry on voicing young Megatron, his love for villain roles

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoCoinbase’s cbBTC surges to third-largest wrapped BTC token in just one week

-

Travel1 week ago

Travel1 week agoDelta signs codeshare agreement with SAS

-

Politics6 days ago

Politics6 days agoHope, finally? Keir Starmer’s first conference in power – podcast | News

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoBeing in two places at once could make a quantum battery charge faster

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoHow one theory ties together everything we know about the universe

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoFuture of fusion: How the UK’s JET reactor paved the way for ITER

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoHow do you recycle a nuclear fusion reactor? We’re about to find out

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoTiny magnet could help measure gravity on the quantum scale

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoCrypto scammers orchestrate massive hack on X but barely made $8K

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks ago‘No matter how bad it gets, there’s a lot going on with NFTs’: 24 Hours of Art, NFT Creator

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoSEC asks court for four months to produce documents for Coinbase

-

Business2 weeks ago

How Labour donor’s largesse tarnished government’s squeaky clean image

-

Technology2 weeks ago

Technology2 weeks agoiPhone 15 Pro Max Camera Review: Depth and Reach

-

News2 weeks ago

Brian Tyree Henry on voicing young Megatron, his love for villain roles

-

Womens Workouts2 weeks ago

Womens Workouts2 weeks agoHow Heat Affects Your Body During Exercise

-

Womens Workouts2 weeks ago

Womens Workouts2 weeks agoKeep Your Goals on Track This Season

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoUK spurns European invitation to join ITER nuclear fusion project

-

News2 weeks ago

News2 weeks agoChurch same-sex split affecting bishop appointments

-

Technology2 weeks ago

Technology2 weeks agoFivetran targets data security by adding Hybrid Deployment

-

CryptoCurrency2 weeks ago

$12.1M fraud suspect with ‘new face’ arrested, crypto scam boiler rooms busted: Asia Express

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoDecentraland X account hacked, phishing scam targets MANA airdrop

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoCertiK Ventures discloses $45M investment plan to boost Web3

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoBeat crypto airdrop bots, Illuvium’s new features coming, PGA Tour Rise: Web3 Gamer

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoTelegram bot Banana Gun’s users drained of over $1.9M

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoVonMises bought 60 CryptoPunks in a month before the price spiked: NFT Collector

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks ago‘Silly’ to shade Ethereum, the ‘Microsoft of blockchains’ — Bitwise exec

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoEthereum falls to new 42-month low vs. Bitcoin — Bottom or more pain ahead?

-

Business2 weeks ago

Thames Water seeks extension on debt terms to avoid renationalisation

-

Politics2 weeks ago

‘Appalling’ rows over Sue Gray must stop, senior ministers say | Sue Gray

-

Science & Environment1 week ago

Science & Environment1 week agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

News1 week ago

News1 week agoWhy Is Everyone Excited About These Smart Insoles?

-

News5 days ago

News5 days agoUS Newspapers Diluting Democratic Discourse with Political Bias

-

Politics2 weeks ago

Politics2 weeks agoTrump says he will meet with Indian Prime Minister Narendra Modi next week

-

Technology2 weeks ago

Technology2 weeks agoCan technology fix the ‘broken’ concert ticketing system?

-

Health & fitness2 weeks ago

Health & fitness2 weeks agoThe secret to a six pack – and how to keep your washboard abs in 2022

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoSingle atoms captured morphing into quantum waves in startling image

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoHow Peter Higgs revealed the forces that hold the universe together

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoA tale of two mysteries: ghostly neutrinos and the proton decay puzzle

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks ago2 auditors miss $27M Penpie flaw, Pythia’s ‘claim rewards’ bug: Crypto-Sec

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoLouisiana takes first crypto payment over Bitcoin Lightning

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoJourneys: Robby Yung on Animoca’s Web3 investments, TON and the Mocaverse

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks ago‘Everything feels like it’s going to shit’: Peter McCormack reveals new podcast

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoSEC sues ‘fake’ crypto exchanges in first action on pig butchering scams

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoBitcoin price hits $62.6K as Fed 'crisis' move sparks US stocks warning

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoVitalik tells Ethereum L2s ‘Stage 1 or GTFO’ — Who makes the cut?

-

News2 weeks ago

News2 weeks agoBrian Tyree Henry on his love for playing villains ahead of “Transformers One” release

-

Womens Workouts2 weeks ago

Womens Workouts2 weeks agoWhich Squat Load Position is Right For You?

-

News1 week ago

News1 week agoBangladesh Holds the World Accountable to Secure Climate Justice

-

TV1 week ago

TV1 week agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Technology1 week ago

Technology1 week agoRobo-tuna reveals how foldable fins help the speedy fish manoeuvre

-

Science & Environment6 days ago

Science & Environment6 days agoX-rays reveal half-billion-year-old insect ancestor

-

News2 weeks ago

the pick of new debut fiction

-

Technology2 weeks ago

Technology2 weeks agoIs carbon capture an efficient way to tackle CO2?

-

Health & fitness2 weeks ago

Health & fitness2 weeks agoThe maps that could hold the secret to curing cancer

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoThe physicist searching for quantum gravity in gravitational rainbows

-

CryptoCurrency2 weeks ago

CryptoCurrency2 weeks agoHelp! My parents are addicted to Pi Network crypto tapper

You must be logged in to post a comment Login