Money

Parent gets paid £677 in compensation after fighting unfair ‘free hours’ nursery fees – could YOU claim money back too?

A PARENT has been awarded £677 in compensation from his local council after complaining that his daughter’s nursery charged him fees for free childcare hours, The Sun can reveal.

Earlier this year, we exposed how nurseries had begun charging parents new fees following the introduction of extra free childcare hours in April, which goes against government guidance.

3

We have seen evidence of “supplementary fees”, “registration fees” and new “consumables charges” being added, even where parents have offered to provide those consumables themselves.

Under government guidance, nurseries cannot charge so-called top-up fees, non-refundable registration fees or any other fees not clearly identified as for consumables, for free childcare hours.

Charging fees for consumables is allowed, but they should not be made a condition of accessing a free place and an alternative should be offered, such as providing your own items, the guidance says.

The extra free childcare hours in April was the first phase of a plan to offer 30 free hours to all eligible parents of children between nine months and three years old by September 2025.

But at the time, a number of parents reported seeing new fees being added to their invoices.

Nurseries have long argued that they don’t receive enough funding from the Government to offer free hours and need to find ways to make up the shortfall.

But the Government says the funding it provides is adequate.

Following our investigation earlier this year, the Department for Education said it was collecting evidence of nurseries charging extra fees for free hours and would intervene if it believed it was a widespread issue.

The Sun has now learned that one parent has won back £677 from his local council after complaining that his nursery was charging him a “supplementary fee” per hour of free childcare.

Alex Hays* from near Dover in Kent, was awarded £677 by Kent County Council following a five-month battle over the fees.

Alex and his wife only claimed 20 hours of childcare a week for their three-year-old daughter, so all of these hours were funded.

But he said their nursery, Kid Ease in Swingfield, near Dover, charged them £1.50 per hour, or £150 a month, in so-called supplementary fees for those funded hours.

Then in March this year, Kid Ease emailed Alex a letter that let him know these fees would be rising to £1.95 an hour.

3

The letter from the childcare provider, seen by The Sun, blamed the fee hike on a “turbulent economy” and “inflationary pressures” putting it under financial pressure.

“Together, these factors mean we will need to introduce a fee increase from 1st April 2024,” the letter said.

It went on to say parents would now be charged a supplementary fee of £1.95 per hour of funded childcare.

3

At this point, Alex began researching whether parents could be charged supplementary fees and discovered this was actually against government guidelines.

“I knew they probably shouldn’t have been charging the fees, but when they increased them I decided I’d had enough,” Alex said.

“I asked for an itemised breakdown of what the fees were paying for, but they just said it was for consumables like food and refused to give me an actual breakdown.”

Alex and his wife then decided to formally complain to Kent County Council, which appointed a third party, The Education People, to investigate.

After 12 weeks with no response, they escalated the case to the Local Government Ombudsman, which gave The Education People 28 working days to provide a final response.

Finally, in September, The Education People found in favour of Alex, and, in an email seen by The Sun, said it was working with Kid Ease to ensure it complies with the Kent Provider Agreement going forward.

Alex and his wife paid a total of £909 in extra fees for claiming free childcare hours to Kid Ease nursery and received back £677 in compensation – roughly 75%.

This was because they had £4 per day deducted for lunches for 58 days, totalling £232.

The family has since moved their daughter to another nursery.

Alex is now urging other parents to complain if they are being charged any extra fees for free hours.

“The guidelines are very clear, working parents absolutely cannot be forced to pay extra fees by providers and shouldn’t feel that they have to in order to receive or continue receiving free childcare,” he said.

“If you are a parent and want to pay fees for additional services, that’s completely up to you, but I’d encourage you to at least ask what it’s paying for.”

A Department for Education spokesperson told The Sun: “We have published statutory guidance for local authorities which makes clear that extra charges for consumables or additional hours should not be made a condition of accessing a free place – and continue to monitor this issue closely.”

The Sun contacted Kent Council for further comment. It is understood that Kid Ease is challenging the decision by The Education People.

Kid Ease states it may charge a “supplementary fee” for funded hours in its most recent terms and conditions available online.

Here’s what Kid Ease said

A spokesperson for Kid Ease said the following:

“Concerning the parent’s complaint, Kid Ease investigated this matter thoroughly and submitted considerable evidence to Kent County Council. Unfortunately, the Council made its initial decision in respect of the complaint without reference to Kid Ease. The decision has been formally challenged, and whilst the Council considers our challenge, we are unable to comment in detail.

“We can, however, confirm Kid Ease is fully aware of and at all times complies with statutory guidance on FEE and supplementary charges for free childcare places. We do not charge top up fees or registration fees. Additional fees are only charged for consumables as well as costs such as trips and specialist tuition, all of which are permissible.

“Permissible charges for consumables and services are communicated to all parents, both verbally and in writing, prior to parents making their choice. By email, this parent confirmed these permissible charges had been explained and requested sessions with supplementary fees.

“All FEE funded sessions are provided free and invoiced at £0 and parents always have a choice of free sessions or free sessions with supplementary fees.

“Kid Ease disagrees with and is challenging Kent County Council’s decision because we consider it to be unlawful and not in accordance with the Government’s and their own Guidance.

“Kid Ease has always followed Government Guidance & the Kent Provider Agreement and is mystified by the Council’s conclusion. The Council has not specified which part of the Guidance Kid Ease has allegedly breached.”

New fees for free childcare hours

Alex is one of a number of parents who has complained that they began being charged new fees when extra free childcare hours kicked in.

Earlier this year, one parent told The Sun they began being charged a compulsory £29 daily “consumables charge”, regardless of whether they were only claiming free hours or not.

They were also charged a £55 “non-refundable registration fee” just for registering for their free hours, which is explicitly against government guidance.

An email to the parent, whose child attended a nursery in West Byfleet, Surrey, said: “All children claiming funding of either 15 or 30 hours per week will be required to pay a daily fee for consumables.

“When claiming a funded-only place, parents are required to pay a non-refundable £50 registration fee.”

Another parent from Huddersfield reported seeing a compulsory consumables charge worth “1x daily rate” appear on her monthly invoice, worth an extra £61. She only claimed free childcare hours.

Unfortunately, many parents are afraid to stand up their nursery because they’re scared of their place being withdrawn – but it’s important to remember these charges actually aren’t allowed to be compulsory under government rules

Martyn James

Since our previous investigation, The Sun has learned the West Byfleet nursery has written to parents informing them it will be removing the compulsory charge for free childcare hours.

But many parents are still faced with these fees – and experts say that parents are too afraid to complain for fear of losing their childcare place.

Consumer expert Martyn James said: “Unfortunately, many parents are afraid to stand up their nursery because they’re scared of their place being withdrawn.

“But it’s important to remember these charges actually aren’t allowed to be compulsory under government rules.”

What fees can nurseries charge?

Nurseries are allowed to charge for consumables, even for free childcare hours. This can cover things like food, nappies or other items used during the day.

However, these fees cannot be compulsory. The nursery must offer a reasonable alternative, such as allowing you to provide your own consumables or forfeiting trips out.

Under government guidance, nurseries are not allowed to charge:

- A top-up fee (any difference between a provider’s normal charge to parents and the funding they receive from the LA to deliver the free place)

- A non-refundable registration fee. (A fee to register for a place that is not returned to you when you take up that place. This may also be called an “enrolment fee”, “admissions fee” or “booking fee”)

- Any additional fees on top of your funded hours that are not specifically identified as being for any consumables – although providing these yourself should be an alternative option

The government advises that parents should speak to their local authority or provider about any additional charges on top of the childcare hours they receive through the entitlement, including any alternative options they offer.

How to complain if you think you’re being charged unfairly for free hours

If you’re unhappy with the fees your nursery or childminder is charging you, your first port of call should be to speak to your provider.

Ask them for a breakdown of what any extra fees are paying for, and remind them of government guidance.

If they refuse to provide a breakdown or offer an alternative, raise a formal complaint.

They should have a formal complaints process they can share with you.

If you don’t agree with the outcome of the complaint, you can speak to Citizens Advice for further assistance or legal advice.

Or, like Alex, contact your local council to start a complaint that way.

It’s best to keep any evidence you can to back up your claim, such as emails detailing any charges, or correspondence refusing to provide a breakdown or alternative options.

Mr James advised: “If you’re worried about losing your place, consider speaking to your local council to let them know anonymously, or ask Citizens Advice if it can intervene without revealing who you are.”

*name changed to protect identity

Do you have a money problem that needs sorting? Get in touch by emailing squeezeteam@thesun.co.uk

CryptoCurrency

Oregon’s most populous county adds gas utility to $51B climate suit against fossil fuel companies

PORTLAND, Ore. (AP) — Oregon’s Multnomah County, home to Portland, has added the state’s largest natural gas utility to its $51.5 billion climate lawsuit against fossil fuel companies over their role in the region’s deadly 2021 heat- dome event.

The lawsuit, filed last year, accuses the companies’ carbon emissions of being a cause of the heat-dome event, which shattered temperature records across the Pacific Northwest. About 800 people died in Oregon, Washington state and British Columbia in the heat wave, which hit in late June and early July 2021.

An amended complaint was filed this week, adding NW Natural to a lawsuit that already named oil giants such as ExxonMobil, Chevron and Shell as defendants. It accuses NW Natural, which provides gas to about 2 million people across the Pacific Northwest, of being responsible for “a substantial portion” of greenhouse gas emissions in Oregon and deceiving the public about the harm of such emissions.

NW Natural said it can’t comment in detail until it has completed reviewing the claims.

“However, NW Natural believes that these new claims are an attempt to divert attention from legal and factual laws in the case. NW Natural will vigorously contest the County’s claims should they come to court,” it said in an emailed statement.

According to the Center for Climate Integrity, it is the first time a gas utility has been named in a lawsuit accusing fossil fuel companies of climate deception. There are currently over two dozen such lawsuits that have been filed by state, local and tribal governments across the U.S., according to the group.

The amended complaint also added the Oregon Institute of Science and Medicine, which describes itself as a research group on its website, to the lawsuit. The group has opposed the concept of human-caused global warming. A request for comment sent Friday to the email address on its website was returned to sender.

Multnomah County is seeking $51.5 billion in damages, largely for what it estimates to be the cost of responding to the effects of extreme heat, wildfire and drought.

“We’re already paying dearly in Multnomah County for our climate crisis — with our tax dollars, with our health and with our lives,” county chair Jessica Vega Pederson said in a statement. “Going forward we have to strengthen our safety net just to keep people safe.”

After the initial complaint was filed last year, ExxonMobil said the lawsuit didn’t address climate change, while a Chevron lawyer said the claims were baseless.

When contacted for comment Friday, Shell said it was working to reduce its emissions.

“Addressing climate change requires a collaborative, society-wide approach,” it said in an emailed statement. “We do not believe the courtroom is the right venue to address climate change, but that smart policy from government and action from all sectors is the appropriate way to reach solutions and drive progress.”

The case is pending in Multnomah County Circuit Court.

By Allison Lampert and David Shepardson

(Reuters) -Boeing will cut 17,000 jobs — 10% of its global workforce — delay first deliveries of its 777X jet by a year and record $5 billion in losses in the third quarter, as the U.S. planemaker continues to spiral during a month-long strike.

CEO Kelly Ortberg said in a message to employees that the significant downsizing is necessary “to align with our financial reality” after an ongoing strike by 33,000 U.S. West Coast workers halted production of its 737 MAX, 767 and 777 jets.

“We reset our workforce levels to align with our financial reality and to a more focused set of priorities. Over the coming months, we are planning to reduce the size of our total workforce by roughly 10 percent. These reductions will include executives, managers and employees,” Ortberg’s message said.

Boeing shares fell 1.1% in after-market trading.

The sweeping changes are a big move by Ortberg, who arrived in August at the helm of the beleaguered planemaker promising to reset relations with the union and its employees.

Boeing recorded pre-tax earnings charges totaling $5 billion for its defense business and two commercial plane programs. On Sept. 20, Boeing ousted the head of its troubled space and defense unit Ted Colbert.

Boeing, which reports third-quarter earnings on Oct. 23, said in a separate release it now expects revenue of $17.8 billion, a loss per share of $9.97, and a better-than-expected negative operating cash flow of $1.3 billion.

Analysts on average were expecting Boeing to generate quarterly cash burn of negative $3.8 billion, according to LSEG data.

Thomas Hayes, equity manager at Great Hill Capital, said by email that the layoffs could put pressure on employees to end the strike.

“Striking workers who temporarily do not have a paycheck do not want to become unemployed workers who permanently do not have a paycheck,” Hayes said. “I would estimate the strike will be resolved within a week as these workers do not want to find themselves in the next batch of 17,000 cuts.”

Reaching a deal to end the work stoppage is critical for Boeing, which filed an unfair-labor-practice charge on Wednesday accusing the machinists union of failing to bargain in good faith. Ratings agency S&P estimated the strike is costing Boeing $1 billion a month and the company risks losing its prized investment-grade credit rating.

Ortberg also said Boeing has notified customers that it now expects first delivery of its 777X in 2026 due to challenges in development, the flight-test pause and the work stoppage. Boeing had already faced issues with certification of the 777X that had significantly delayed the plane’s launch.

“While our business is facing near-term challenges, we are making important strategic decisions for our future and have a clear view on the work we must do to restore our company,” Ortberg added.

Boeing will end its 767 freighter program in 2027 when it completes and delivers the remaining 29 planes ordered but said production for the KC-46A Tanker will continue.

The company said in light of the job cuts it would end a furlough program for salaried employees announced in September.

Even before the strike began on Sept. 13, the company had been burning cash as it struggled to recover from a January mid-air panel blowout on a new plane that exposed weak safety protocols and spurred U.S. regulators to curb its production.

Boeing on Friday faced a court hearing in Texas in front of a judge who will decide whether to accept the planemaker’s offer to plead guilty to fraud under a deal with the Justice Department.

Boeing has agreed to pay up to a $487.2 million fine, spend at least $455 million on improving safety and face three years of court-supervised probation and independent oversight.

Also Friday, a federal watchdog said the Federal Aviation Administration was “not effective” in overseeing Boeing production.

Reuters reported this week Boeing is examining options to raise billions of dollars through a sale of stock and equity-like securities.

These options include selling common stock as well as securities such as mandatory convertible bonds and preferred equity, according to the sources. One of the sources said they suggested to Boeing that it should raise around $10 billion.

The company has about $60 billion in debt and posted operating cash flow losses of more than $7 billion for the first half of 2024.

Analysts estimate that Boeing would need to raise between $10 billion and $15 billion to maintain its ratings, which are now one notch above junk.

“For those of us that have watched Boeing closely, the company’s announcement of delayed delivery and labor downsizing across all management and employment levels is not much of a surprise as their cash and credit reserves dwindle,” said Michael Ashley Schulman, partner at Running Point Capital Advisors. “Their credit rating and share price has been at risk for the better part of a decade because of mismanagement and the stubbornness displayed in the strike may be the straw that breaks the camel’s back.”

(Reporting By Allison Lampert and David Shepardson. Additional reporting by Shivansh Tiwary; editing by Rod Nickel, David Gregorio and Diane Craft)

Benzinga and Yahoo Finance LLC may earn commission or revenue on some items through the links below.

Are you looking for reliable income stocks to add to your portfolio this month? Dividend Aristocrats – companies with at least 25 consecutive years of dividend growth – offer some of the most compelling opportunities due to their stability and consistent payouts.

Let’s check out three dividend aristocrats, including two real estate investment trusts (REITs), that you could buy today.

Don’t Miss:

Essex Property Trust

Essex Property Trust (NYSE:ESS) owns and manages apartment communities across West Coast markets in the United States. As of June 30, its portfolio comprised 255 apartment communities containing over 62,000 apartment units.

Essex pays a quarterly dividend of $2.45 per share, which equates to an annualized dividend of $9.80 per share and gives its stock a yield of about 3.4% at the time of this writing.

Essex has been a Dividend Aristocrat for years. It has raised its annual dividend payment for 29 consecutive years and its 6.1% hike in February puts it on track for 2024, the 30th consecutive year with an increase.

McDonald’s Corporation

McDonald’s (MCD) is the world’s largest food service retailer, with more than 40,000 locations in over 100 countries. The company proudly notes that independent local business owners own and operate approximately 95% of its restaurants.

McDonald’s pays a quarterly dividend of $1.77 per share, which equates to an annualized dividend of $7.08 per share and gives its stock a yield of about 2.3% at the time of this writing.

While its yield may be under 3%, McDonald’s makes up for this with its impressive track record of dividend growth. It has raised its annual dividend payment for 47 consecutive years and its 6% hike in September marked the 48th consecutive year with an increase.

Trending: This billion-dollar fund has invested in the next big real estate boom, here’s how you can join for $10.

This is a paid advertisement. Carefully consider the investment objectives, risks, charges and expenses of the Fundrise Flagship Fund before investing. This and other information can be found in the Fund’s prospectus. Read them carefully before investing.

Federal Realty Investment Trust

Federal Realty Investment Trust (NYSE:FRT) owns and manages retail and mixed-use properties across major U.S. markets, including Boston, Chicago, Miami, New York City and Philadelphia. As of June 30, its portfolio comprised 102 properties containing approximately 27 million square feet.

Federal Realty pays a quarterly dividend of $1.10 per share, which equates to an annualized dividend of $4.40 per share and gives its stock a yield of about 4% at the time of this writing.

Federal Realty has the longest consecutive record of dividend growth in the REIT industry. It has raised its annual dividend payment each of the last 56 years and its 0.9% hike in August marked the 57th consecutive year with an increase.

Wondering if your investments can get you to a $5,000,000 nest egg? Speak to a financial advisor today. SmartAsset’s free tool matches you up with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you.

Keep Reading:

This article Dividend Aristocrats to Buy in October: 3 Stocks for Steady Growth and Income originally appeared on Benzinga.com

Shipments of artificial intelligence (AI) servers have shot up remarkably in the past couple of years as cloud service providers have been investing huge amounts of money in infrastructure that’s capable of training AI models, as well as for AI inferencing purposes to deploy those models in real-world applications.

Market research firm TrendForce estimates that the global AI server market could hit a whopping $187 billion in revenue this year, up by 69% from 2023. Several companies are already benefiting big time from this huge end-market opportunity. From chip manufacturers such as Nvidia to custom chip producers such as Broadcom and server solutions providers such as Dell Technologies, there are multiple ways to invest in the booming AI server market.

In this article, however, we will take a closer look at the prospects of Micron Technology (NASDAQ: MU) and Marvell Technology (NASDAQ: MRVL), two companies that make critical components that go into AI servers.

Micron Technology’s high-bandwidth memory chips are in terrific demand

High-bandwidth memory (HBM) is used in AI server chips such as graphics processing units (GPUs) because of its ability to enable faster transfer of data to reduce processing times and boost performance, as well as reduce power consumption. The demand for HBM is so strong that Micron says that it has sold out its entire capacity for this year and the next.

Even better, Micron management points out that it “will have a more diversified HBM revenue profile” for 2026 thanks to the new business that it has landed for its latest HBM3E chip. The chipmaker points out that it has already begun shipments of this new chip to its customers for approval.

Micron claims that HBM3E consumes 20% less power and provides 50% more capacity as compared to rival offerings. The company expects to start the production ramp of HBM3E in early 2025 and increase its output as the year progresses. Even better, Micron is confident that it will continue to gain more share in the HBM market.

Singapore-based news channel CNA points out that Micron is reportedly aiming to grab 20% to 25% of the HBM market by next year. That is likely to give Micron’s growth a big boost next year as it expects the HBM market’s revenue to jump to an impressive $25 billion in 2025 from just $4 billion in 2023.

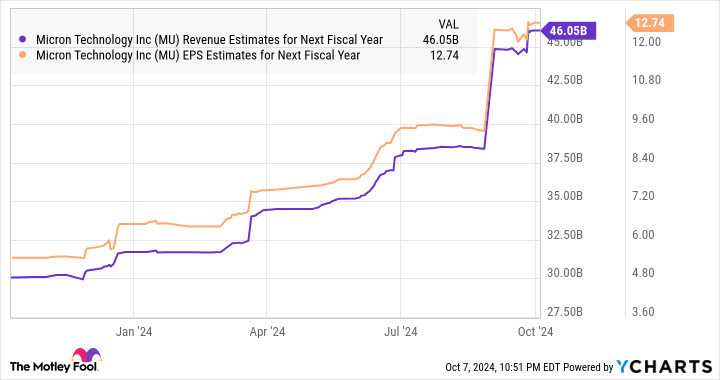

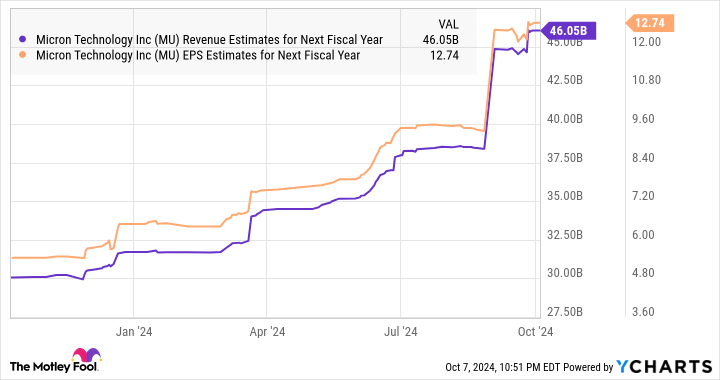

An expansion of the end market along with Micron’s focus on grabbing a bigger share of the HBM space are the reasons the company’s revenue is expected to jump by a stunning 52% to $38 billion in the current fiscal year (which started on Aug. 30). Meanwhile, analysts are forecasting Micron’s earnings to increase to $8.94 per share from $1.30 per share in the previous year.

Micron is expected to keep growing at a terrific pace in the next fiscal year as well.

Buying shares of Micron Technology right now could turn out to be a smart move for investors looking to benefit from the growing deployment of AI servers. The stock has a forward earnings multiple of just 11, while its price/earnings-to-growth ratio (PEG ratio) of just 0.16 further reinforces the fact that it is incredibly undervalued with respect to the growth that it is forecast to deliver.

Marvell Technology is getting a nice boost because of its custom AI chips

Marvell Technology is known for manufacturing application-specific integrated circuits (ASICs), which are custom chips designed to perform specific tasks. It is worth noting that the demand for these custom chips deployed in AI servers is increasing since major cloud service providers such as Meta Platforms, Alphabet‘s Google, and Amazon are looking to reduce their costs by developing in-house processors.

As a result, ASICs are expected to account for 26% of the overall market for AI server chips in 2024. Even better, the deployment of ASICs in AI servers is expected to increase at a nice clip in the future and open a potential revenue opportunity worth an impressive $150 billion. Marvell is already capitalizing on this lucrative opportunity.

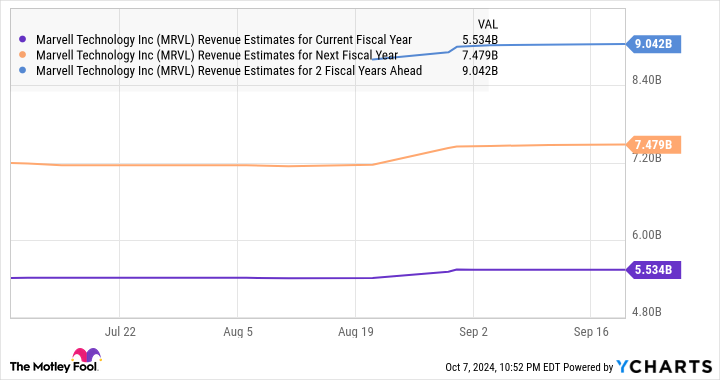

The company’s overall revenue was down 5% year over year in the second quarter of fiscal 2025 (for the three months ended Aug. 3) to $1.27 billion thanks to the weakness in the carrier infrastructure, consumer, automotive, and enterprise networking end markets. However, it delivered a tremendous year-over-year increase of 92% in data center revenue to $881 million.

There is a good chance that Marvell’s data center business will continue to grow at a healthy clip as the company’s AI chip production is set to ramp up, as pointed out by CEO Matt Murphy on the latest earnings conference call:

Our AI custom silicon programs are progressing very well with our first two chips now ramping into volume production. Development for new custom programs we have already won, including projects with the new Tier 1 AI customer we announced earlier this year, are also tracking well to key milestones.

As a result, Marvell is expecting its data center business’s growth to “accelerate into the high teens sequentially on a percentage basis” in the current quarter, which would be an improvement over the 8% sequential growth it reported in the previous quarter. This explains why Marvell’s guidance for the current quarter points toward an improvement in its financial performance.

The company is expecting revenue of $1.45 billion in fiscal Q3, up from $1.42 billion in the same quarter last year. So, Marvell is set to return to growth from the current quarter, and analysts are expecting it to deliver robust growth over the next couple of fiscal years.

Additionally, analysts are expecting Marvell’s earnings to increase at a compound annual growth rate of 21% for the next five years. So, investors looking to get their hands on a semiconductor stock to benefit from the growing demand for custom AI chips can consider adding Marvell Technology to their portfolios. Its growth is set to accelerate thanks to the tremendous opportunity in the AI server market.

Should you invest $1,000 in Micron Technology right now?

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $826,130!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of October 7, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Nvidia. The Motley Fool recommends Broadcom and Marvell Technology. The Motley Fool has a disclosure policy.

Artificial Intelligence (AI) Servers Are Set to Become a $187 Billion Industry in 2024: 2 Hot Stocks That Are Set to Soar Thanks to This Massive Opportunity was originally published by The Motley Fool

-

Chinese stocks are poised for a huge run-up in the next year, according to Renaissance Macro’s Jeff deGraaf.

-

The research firm CEO said perfect conditions are aligning for additional gains exceeding 50%.

-

Other notable investors have been looking to buy the dip in Chinese stocks amid continued stimulus efforts.

China’s stock rally isn’t over — and the nation could have the perfect cocktail of ingredients to stage a monster run-up over the next year, according to one Wall Street forecaster.

Jeff deGraaf, the CEO of Renaissance Macro Research, says he sees China’s benchmark stock index climbing to 6,000 over the next year. That implies a 54% increase from the CSI 300’s current levels, thanks to the right mix of conditions in Beijing that should power equities higher, he told Bloomberg on Friday.

“Skepticism, valuation, stimulus, momentum and a trend change,” deGraaf said of China’s investing environment, adding that it was “one of the best set-ups” he’s seen over his 35-year career.

Chinese stocks have been on a roller coaster in recent weeks after Beijing announced its latest monetary stimulus package, which included lowering interest rates and pumping the stock market with $114 billion. The package sparked the steepest rally in Chinese stocks since 2008 before it quickly fizzled, a sign investors were disappointed Beijing didn’t announce more stimulus measures.

Markets, though, are expecting the nation to announce a fresh fiscal stimulus package at a briefing on Saturday, potentially reviving the bull case for stocks. Most investors expect China to add 2 trillion yuan, or $283 billion, in fiscal stimulus through 2025, according to a Bloomberg poll of market participants.

“We see the policy response as self-preservation, a reaction to the weakness and a potential Mario Draghi-esque ‘Do what it takes’ moment for China,” deGraaf said, later urging investors to “keep stops in place” when betting on Chinese stocks.

Other traders on Wall Street have shown interest in buying the dip in Chinese equities, despite fear that Beijing’s economic slowdown could stick around.

Investors poured a record $39.1 billion into Chinese stock funds in the week ending October 9, according to EPFR Global data cited by Bank of America in a note.

“We buy any China dips,” BofA strategist Michael Hartnett wrote in a note. Stimulus efforts will continue to “be used aggressively to boost domestic animal spirits and demand,” he added.

Additionally, the Shenzhen Huaan Hexin Private Investment Fund Management Co., a Chinese hedge fund up 800% since 2017, also says it’s buying the dip in technology stocks listed in Hong Kong. The Hang Seng Index has dropped 3% over the last five trading days, but is still up 27% from levels at the start of the year.

“Such a correction is more like a buying opportunity,” Yuan Wei, the fund’s founder, said in an interview with Bloomberg this week. “If you compare to their fundamentals, the stocks remain very cheap.”

China’s onshore market has a 50% chance of starting a new bull run, as opposed to a short-term bounce, and the bear market in equities should be over by now, Yuan said.

“The market is just rebounding from an extremely bearish level to a level that’s still undervalued,” he later added.

Other strategists on Wall Street have made bullish calls on Chinese equities in recent weeks, with eyes on continued stimulus measures in Beijing. Goldman Sachs predicted China’s stock market could rally another 20%, thanks to “more substantial policy measures” and Chinese stocks being oversold, strategists said in a note.

Read the original article on Business Insider

(Reuters) – A U.S. appeals court on Friday put on hold approvals and permits necessary to allow a Kinder Morgan subsidiary to construct a 32-mile gas pipeline in Tennessee, at the urging of environmental groups.

The proposed Cumberland Project, set to be constructed by Kinder Morgan’s Tennessee Gas Pipeline, could transport about 245,000 dekatherms per day of additional natural gas to power supplier Tennessee Valley Authority.

On a 2-1 vote, Cincinnati-based 6th U.S. Circuit Court of Appeals put a hold on the Tennessee Department of Environment and Conservation’s order issuing a water quality certification and the Army Corps of Engineers’ issuance of a permit.

The request for a stay was filed by environmental organizations Appalachian Voices and Sierra Club, which claimed the pipeline’s construction could have detrimental impact on the environment.

The court said a stay was appropriate for it to have the time to consider the merits of the environmental groups’ case.

It said further arguments in the case would be heard in December.

A Kinder Morgan spokesperson said the company does not agree with the court’s decision, which it will continue to review while evaluating its options.

Appalachian Voices and Sierra Club did not immediately respond to Reuters’ requests for comment.

(Reporting by Vallari Srivastava in Bengaluru and Nate Raymond in Boston; Editing by Shreya Biswas)

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHyperelastic gel is one of the stretchiest materials known to science

-

Technology3 weeks ago

Technology3 weeks agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment3 weeks ago

Science & Environment3 weeks ago‘Running of the bulls’ festival crowds move like charged particles

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks ago3 Day Full Body Women’s Dumbbell Only Workout

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLiquid crystals could improve quantum communication devices

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoSunlight-trapping device can generate temperatures over 1000°C

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

News4 weeks ago

the pick of new debut fiction

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to wrap your mind around the real multiverse

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy this is a golden age for life to thrive across the universe

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNerve fibres in the brain could generate quantum entanglement

-

News3 weeks ago

News3 weeks agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum forces used to automatically assemble tiny device

-

Technology2 weeks ago

Technology2 weeks agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoX-rays reveal half-billion-year-old insect ancestor

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA slight curve helps rocks make the biggest splash

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLaser helps turn an electron into a coil of mass and charge

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists are grappling with their own reproducibility crisis

-

Business2 weeks ago

Eurosceptic Andrej Babiš eyes return to power in Czech Republic

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNuclear fusion experiment overcomes two key operating hurdles

-

News4 weeks ago

News4 weeks ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

News3 weeks ago

News3 weeks agoYou’re a Hypocrite, And So Am I

-

Sport3 weeks ago

Sport3 weeks agoJoshua vs Dubois: Chris Eubank Jr says ‘AJ’ could beat Tyson Fury and any other heavyweight in the world

-

Science & Environment4 weeks ago

Science & Environment4 weeks agoCaroline Ellison aims to duck prison sentence for role in FTX collapse

-

News3 weeks ago

News3 weeks ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Business2 weeks ago

Should London’s tax exiles head for Spain, Italy . . . or Wales?

-

Technology2 weeks ago

Technology2 weeks ago‘From a toaster to a server’: UK startup promises 5x ‘speed up without changing a line of code’ as it plans to take on Nvidia, AMD in the generative AI battlefield

-

Football2 weeks ago

Football2 weeks agoFootball Focus: Martin Keown on Liverpool’s Alisson Becker

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoRethinking space and time could let us do away with dark matter

-

News4 weeks ago

News4 weeks agoNew investigation ordered into ‘doorstep murder’ of Alistair Wilson

-

News3 weeks ago

The Project Censored Newsletter – May 2024

-

Technology2 weeks ago

Technology2 weeks agoQuantum computers may work better when they ignore causality

-

MMA2 weeks ago

MMA2 weeks agoConor McGregor challenges ‘woeful’ Belal Muhammad, tells Ilia Topuria it’s ‘on sight’

-

Sport2 weeks ago

Sport2 weeks agoWatch UFC star deliver ‘one of the most brutal knockouts ever’ that left opponent laid spark out on the canvas

-

News3 weeks ago

Israel strikes Lebanese targets as Hizbollah chief warns of ‘red lines’ crossed

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA tale of two mysteries: ghostly neutrinos and the proton decay puzzle

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoFuture of fusion: How the UK’s JET reactor paved the way for ITER

-

Technology2 weeks ago

Technology2 weeks agoGet ready for Meta Connect

-

Business2 weeks ago

Ukraine faces its darkest hour

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe secret to a six pack – and how to keep your washboard abs in 2022

-

Technology4 weeks ago

Technology4 weeks agoThe ‘superfood’ taking over fields in northern India

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoUK spurns European invitation to join ITER nuclear fusion project

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy we need to invoke philosophy to judge bizarre concepts in science

-

News3 weeks ago

News3 weeks agoWhy Is Everyone Excited About These Smart Insoles?

-

Health & fitness2 weeks ago

Health & fitness2 weeks agoThe 7 lifestyle habits you can stop now for a slimmer face by next week

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCardano founder to meet Argentina president Javier Milei

-

Politics3 weeks ago

UK consumer confidence falls sharply amid fears of ‘painful’ budget | Economics

-

MMA3 weeks ago

MMA3 weeks agoRankings Show: Is Umar Nurmagomedov a lock to become UFC champion?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMeet the world's first female male model | 7.30

-

News3 weeks ago

News3 weeks agoFour dead & 18 injured in horror mass shooting with victims ‘caught in crossfire’ as cops hunt multiple gunmen

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks ago3 Day Full Body Toning Workout for Women

-

Technology3 weeks ago

Technology3 weeks agoRobo-tuna reveals how foldable fins help the speedy fish manoeuvre

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists have worked out how to melt any material

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe maps that could hold the secret to curing cancer

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoBeing in two places at once could make a quantum battery charge faster

-

News4 weeks ago

News4 weeks agoHow FedEx CEO Raj Subramaniam Is Adapting to a Post-Pandemic Economy

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDecentraland X account hacked, phishing scam targets MANA airdrop

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLow users, sex predators kill Korean metaverses, 3AC sues Terra: Asia Express

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoBest Exercises if You Want to Build a Great Physique

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoEverything a Beginner Needs to Know About Squatting

-

TV3 weeks ago

TV3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Servers computers2 weeks ago

Servers computers2 weeks agoWhat are the benefits of Blade servers compared to rack servers?

-

Technology2 weeks ago

Technology2 weeks agoThe best robot vacuum cleaners of 2024

-

News3 weeks ago

News3 weeks agoChurch same-sex split affecting bishop appointments

-

Politics3 weeks ago

Politics3 weeks agoTrump says he will meet with Indian Prime Minister Narendra Modi next week

-

Sport3 weeks ago

Sport3 weeks agoUFC Edmonton fight card revealed, including Brandon Moreno vs. Amir Albazi headliner

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoEthereum is a 'contrarian bet' into 2025, says Bitwise exec

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow one theory ties together everything we know about the universe

-

Business4 weeks ago

JPMorgan in talks to take over Apple credit card from Goldman Sachs

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum time travel: The experiment to ‘send a particle into the past’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTiny magnet could help measure gravity on the quantum scale

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMost accurate clock ever can tick for 40 billion years without error

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin miners steamrolled after electricity thefts, exchange ‘closure’ scam: Asia Express

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDorsey’s ‘marketplace of algorithms’ could fix social media… so why hasn’t it?

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDZ Bank partners with Boerse Stuttgart for crypto trading

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin bulls target $64K BTC price hurdle as US stocks eye new record

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBlockdaemon mulls 2026 IPO: Report

-

Business3 weeks ago

Thames Water seeks extension on debt terms to avoid renationalisation

-

Politics3 weeks ago

‘Appalling’ rows over Sue Gray must stop, senior ministers say | Sue Gray

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCoinbase’s cbBTC surges to third-largest wrapped BTC token in just one week

-

News2 weeks ago

News2 weeks agoUS Newspapers Diluting Democratic Discourse with Political Bias

-

Technology2 weeks ago

Technology2 weeks agoMicrophone made of atom-thick graphene could be used in smartphones

-

Technology3 weeks ago

Technology3 weeks agoiPhone 15 Pro Max Camera Review: Depth and Reach

-

News3 weeks ago

News3 weeks agoBrian Tyree Henry on voicing young Megatron, his love for villain roles

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow do you recycle a nuclear fusion reactor? We’re about to find out

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoRedStone integrates first oracle price feeds on TON blockchain

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks ago‘No matter how bad it gets, there’s a lot going on with NFTs’: 24 Hours of Art, NFT Creator

-

Business3 weeks ago

How Labour donor’s largesse tarnished government’s squeaky clean image

-

News3 weeks ago

Brian Tyree Henry on voicing young Megatron, his love for villain roles

-

Travel3 weeks ago

Travel3 weeks agoDelta signs codeshare agreement with SAS

-

Politics2 weeks ago

Politics2 weeks agoHope, finally? Keir Starmer’s first conference in power – podcast | News

-

Technology2 weeks ago

Technology2 weeks agoUniversity examiners fail to spot ChatGPT answers in real-world test

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLouisiana takes first crypto payment over Bitcoin Lightning

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCrypto scammers orchestrate massive hack on X but barely made $8K

You must be logged in to post a comment Login