Money

The Sun launches interactive tool to check benefits – see if you get winter fuel payments or pension credit this winter

TODAY, The Sun launches a free tool to help you check whether you will get the Winter Fuel Payment this year.

The free benefits checker is in partnership with poverty charity Turn2Us. It quickly tells you if you’re missing out on any cash. 2

If you are unable to access the internet you could ask a friend or relative to help you do the check.

We were flooded with calls and emails earlier this week, with many readers asking whether they were entitled to pension credit or other benefits.

In her July statement, Chancellor Rachel Reeves announced that this winter only households in England and Wales that receive Pension Credit or certain means tested benefits will be entitled to the Winter Fuel payment.

Previously it was available to everyone aged over 66.

New government figures estimate that 770,000 pensioners are at risk of missing out this winter.

The benefit, which is worth up to £300, unlocks a host of other awards including a free TV licence and cheaper water bills worth up to £3,900.

Michael Clarke, from Turn2us: “It’s crucial that people are supported by friends and family to check they are getting all the support available to them.

“In just 10 minutes, the Turn2us Benefits Calculator will tell people if they are eligible.”

You will need some personal information to hand about your current income, including state and private pensions, and any benefits you currently receive.

2

If you are eligible to apply for Pension Credit you can call the DWP helpline on: 0800 99 1234

When you claim you will need your national insurance number and details of any savings and investments, plus information on housing costs such as mortgage interest, service charges or ground rent.

You must lodge a claim by December 21 to get the Winter Fuel Payment this year.

FIX YOUR ENERGY BILLS?

If you’re not on a fixed tariff then it may be worth considering one. Many of the top fixed tariffs are now cheaper than the price cap and could save you money. You can compare tariffs using uSwitch.com or Moneysavingexpert.com.

WARM HOME DISCOUNT

The Warm Home Discount is £150 one-off payment towards electricity bills. You will usually get it automatically – but you need to apply if you’re on a low income in Scotland.

You should check with your energy supplier if you’re on a low income and think you are eligible.

HOUSEHOLD SUPPORT FUND

You can apply to your local council for help if you’re on a low income. Search the name of your local council and ‘household support fund’ to find out details on how you can apply. Eligibility criteria and the amount you will get varies based on where you live – but some households have got up to £500.

ENERGY GRANTS

Many of the UK’s biggest energy suppliers have grants in place to help struggling customers. For example, British Gas offers grants of up to £2,000. .

Ask your supplier if there is anything they can offer

FREE INSULATION OR BOILERS

You may be able to get free or cheap insulation to help reduce your home’s energy bills. Check here: https://www.gov.uk/apply-great-british-insulation-scheme

GET FREE DEBT HELP

THERE are several groups which can help you with your problem debts for free.

- Citizens Advice – 0800 144 8848 (England) / 0800 702 2020 (Wales)

- StepChange – 0800138 1111

- National Debtline – 0808 808 4000

- Debt Advice Foundation – 0800 043 4050

Money

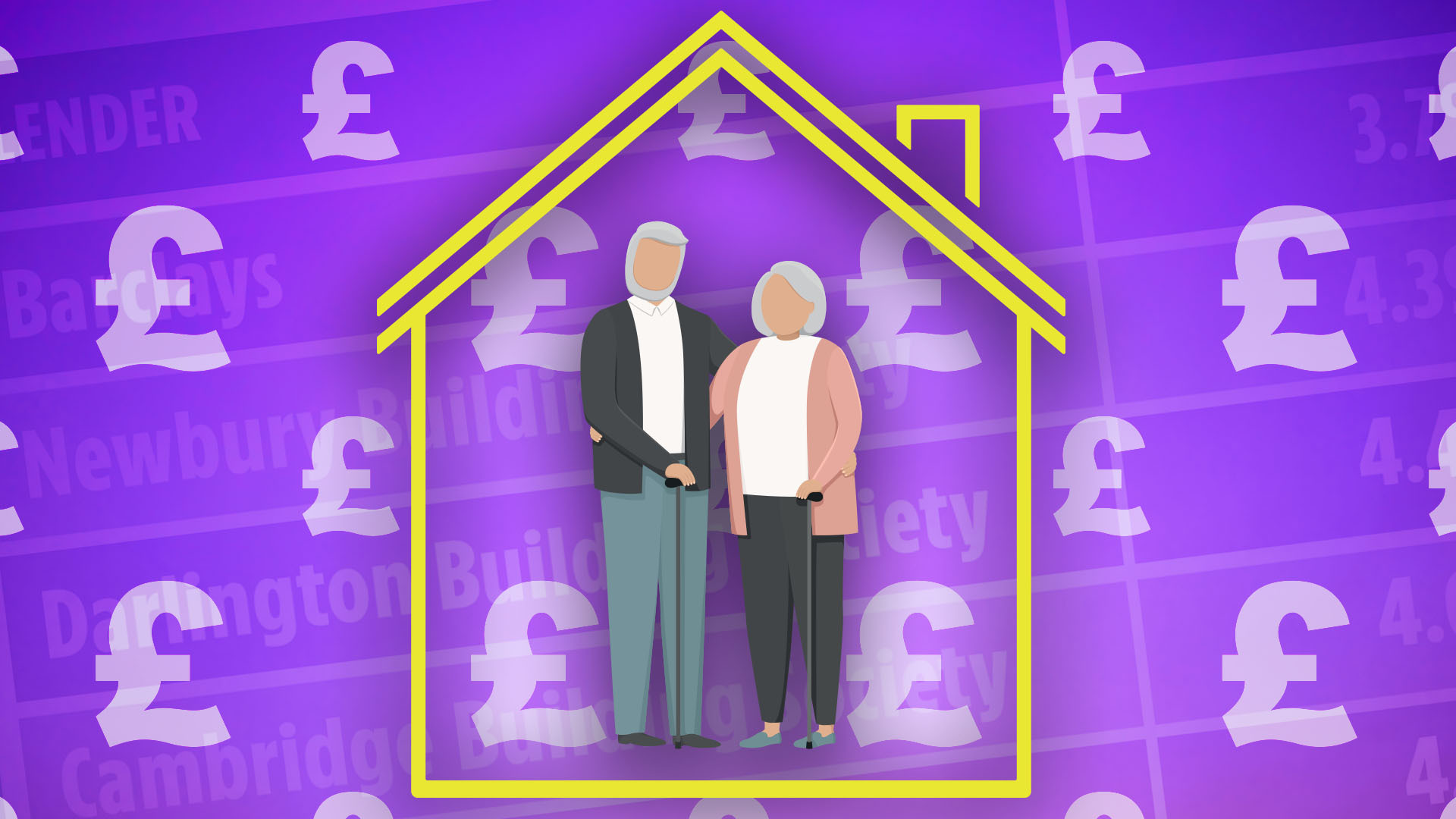

Full list of firms who will offer mortgages to over-60s – and the best rates you can apply for

GETTING a mortgage past retirement age used to be a hurdle that was hard to jump over, but older home buyers and borrowers have more options than ever before.

Lenders have become more flexible in their criteria and deals for homeowners heading into their later years.

1

Some providers now have no maximum age limit at all, giving older borrowers the chance to get the home they want.

It comes as first-time buyer ages have gradually increased over the past few years, as higher house prices mean it is more difficult than it used to be to get on to the property ladder.

At the same time, people are living for longer and working past the traditional State Pension age in many cases.

In some cases, this may be out of financial necessity but it can also be for enjoyment and to keep mentally or physically active in later life.

As a result, lenders have adapted to changing patterns.

Chris Sykes, at financial firm Private Finance, said: “Lenders have indeed become more flexible in this space in recent years.

“It might sound like some people’s worst nightmare to have finance into later life, but for some it’s a lifeline as they can’t pay for food with bricks.

“Others haven’t been able to get on the property ladder as early in life as they would have liked, and some would rather pay monthly but raise capital for children or even grandchildren to buy.”

Whatever the reason for wanting to borrow, the chances are that there will be lenders willing to look at your case.

Chris added: “Mainstream lenders are taking employed and self employed income later and later in life, often to 75 now, some to 80 even.

“But the lenders who really specialise in this space is specialist building societies.”

Big lenders usually have set criteria for mortgage applicants which will specify things such as the age you will need to be by the time your mortgage ends.

However, specialist lenders such as building societies are more likely to look at applicants on a case-by-case basis.

As long as these lenders think you will still be able to afford to make the mortgage repayment at a later age, you could find that you are accepted at almost any age.

In some cases, pension payments will even be an accepted form of income whereas in the past it wasn’t.

Mr Sykes said: “Building societies are having to innovate in their criteria in order to win business so can be flexible.

“Often as you get into your 70s, lenders are looking at incomes guaranteed into later life, such as pensions. investments and buy to lets.

“But also if you own a business that pays you and is family-run, for example.”

Lenders typically assess whether you can qualify for a mortgage based on your income through your job.

The best mortgage rates for over-60s

A borrower who is 60 and looking for a five-year fixed-rate mortgage today has plenty of choice and can get sub 4% rates.

The scenario assumes the borrower has an income of £50,000 and wants the mortgage for a 25-year term on a loan to value of 60%, according to data supplied by broker John Charcol,

The lowest rate is with Barclays with a competitive offering of 3.7%, it’s the only high street lender in the top five.

The rest of the leading rates are from building societies with Newbury offering 4.39%, Darlington 4.49%, Cambridge 4.69% and Family 4.74%.

Some building societies have specialist conditions such as requiring you to live within a particular region of the country.

The mortgages also come with different product fees which need to be taken into account when looking at the overall value of the deal.

An independent mortgage broker can help you understand the best deals available to you in your specific circumstances.

SPECIALIST LENDING

As well as traditional mortgage products there are also specialist products available to older borrowers.

Retirement interest only mortgages, for example, have increased in popularity.

These loans are available to borrowers over 55 and allow borrowers to pay a fixed amount of interest on a loan with the underlying sum paid off from the property when the owner dies or moves into long term care.

There are currently 181 retirement interest-only mortgages available, according to data site Moneyfactscompare.co.uk, compared to 104 products in 2021.

Caitlyn Eastell from the site, said: “Many people may have existing mortgage debt as they approach retirement age or are simply choosing to continue working past typical retirement age.

“S0, it is positive news to see a rise in the number of Retirement Interest Only products available to later-life borrowers despite only being a niche sector of the market.

“RIO mortgages are a way for older homeowners to continue borrowing into retirement and may well help with monthly repayments as it removes the need to repay the capital sum, which could appeal to those who are indeed relying on their pension to make payments.

“In any case, it is important borrowers seek advice before committing and ensure they are making the correct decision to suit their needs.”

Equity release is another product that may suit older homeowners looking to borrow cash.

You’ll need to get professional advice before you take out specialist lending products.

Later life advisers can help you to navigate the options available to you whether it’s a mainstream mortgage or a specialist product is best for your particular circumstances.

How to get the best deal on your mortgage

IF you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

There are several ways to land the best deal.

Usually the larger the deposit you have the lower the rate you can get.

If you’re remortgaging and your loan-to-value ratio (LTV) has changed, you’ll get access to better rates than before.

Your LTV will go down if your outstanding mortgage is lower and/or your home’s value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you’re nearing the end of a fixed deal soon it’s worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

To find the best deal use a mortgage comparison tool to see what’s available.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You’ll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you’ll pay interest on it and so will cost more in the long term.

You can use a mortgage calculator to see how much you could borrow.

Remember you’ll have to pass the lender’s strict eligibility criteria too, which will include affordability checks and looking at your credit file.

You may also need to provide documents such as utility bills, proof of benefits, your last three month’s payslips, passports and bank statements.

A secret boiler button could slash your heating bills by a whopping £150.

There’s claims that average gas bills could go down by as much as 9per cent by turning your boiler flow temperature down.

1

Families are trying to find ways to stave off energy costs down while keeping warm during the winter months.

But energy experts from one of the UK’s biggest money saving expert’s have revealed some top tips on how to combat heating bills as temperatures plunge.

Ben Gallizzi, energy expert at Uswitch.com, said: “The boiler flow rate controls how hot the water is when it leaves the boiler and goes to your radiators. It’s separate to heating and radiator controls.

“Reducing the flow rate can make your boiler run more efficiently, which can save you energy and money.

“People with a condensing combi boiler may be able to turn down the flow temperature to save themselves some money on their energy bills.

“For combi boilers, the recommended output temperature for the radiators is 75C and at least 60C for water, which is the temperature that kills legionella bacteria.”

Flow rate control work is a key element that homeowners can use to lower their payments.

Which? Energy Editor Emily Seymour explained why it’s important.

She said: “Most homes are heated by wet central heating. The heating flow temperature of your boiler is the temperature at which water leaves your boiler on its journey to your radiators.

“By default, many boilers are set to heat this water to 75-80C. But many homes with condensing combi boilers can be suitably warmed with heating flow temperatures of 60-65°C or lower.

“Lowering that temperature means your boiler uses less gas and operates more efficiently.

“Combi boilers also let you select how hot the water supplied to your taps is. As a result, you can adjust both your heating and hot water temperature separately.

“Water comes back from radiators into your boiler when it reaches a certain lower temperature, ready to be heated up again. This is called the return temperature.

“The return temperature is likely to be 60 degrees if you have a flow temperature of 80 degrees.”

By tweaking it, you could save yourself a fair bit of cash if your home is well insulated.

Your average gas bills could go down by as much as 9per cent by turning your boiler flow temperature down – which equates to roughly £150 a year.

But for those that aren’t well insulated or have small radiators, the benefits may not be as good.

To change your boiler’s flow temperature, Emily says: “On a combi boiler, flow temperature for heating is usually shown by a radiator symbol and, for hot water, a tap symbol.

“Use the up and down arrows to adjust the temperature.”

It is important to note that the Heating & Hot Water Industry Council (HHIC) recommends that people adapt their boiler settings with the advice of a boiler engineer.

But if you have a combi boiler, you’ve made sure it’s safe and you’ve checked your boiler’s technical manual, you can adjust these settings yourself.

This setting is accessible to anyone and it can be changed using your boiler controls.

4 ways to keep your energy bills low

Laura Court-Jones, Small Business Editor at Bionic shared her tips.

1. Turn your heating down by one degree

You probably won’t even notice this tiny temperature difference, but what you will notice is a saving on your energy bills as a result. Just taking your thermostat down a notch is a quick way to start saving fast. This one small action only takes seconds to carry out and could potentially slash your heating bills by £171.70.

2. Switch appliances and lights off

It sounds simple, but fully turning off appliances and lights that are not in use can reduce your energy bills, especially in winter. Turning off lights and appliances when they are not in use, can save you up to £20 a year on your energy bills

3. Install a smart meter

Smart meters are a great way to keep control over your energy use, largely because they allow you to see where and when your gas and electricity is being used.

4. Consider switching energy supplier

No matter how happy you are with your current energy supplier, they may not be providing you with the best deals, especially if you’ve let a fixed-rate contract expire without arranging a new one. If you haven’t browsed any alternative tariffs lately, then you may not be aware that there are better options out there.

Money

I tested supermarkets own-brand Digestives – winner was more than £1 cheaper than McVitie’s & I couldn’t tell difference

IF you feel like you are getting a crumby deal on big-name biscuits, you’d be right.

A packet of McVitie’s Digestives has shrunk by as much as 28 per cent since 2014, despite prices rising by 129 per cent over the past decade.

9

So could the supermarket versions offer better value?

It’s crunch time as Laura Stott tries the own-brand digestives.

Aldi Belmont Digestives – 29 biscuits, 400g, 57p

9

IN true Aldi dupe style, the packet looks very like the McVitie’s one, which costs over a quid more.

But put these in a biscuit tin and it’s doubtful anyone will notice the difference.

And you get the most biccies per packet too.

Rating: 5/5

Tesco Digestives – 28 biscuits, 400g, 70p

9

THESE looked the part, but tasted disappointing and the texture is too dry.

The packet claims the biccies are crumbly and crunchy.

Instead they tasted dusty, with a few falling apart before I had a chance to dunk them in my cuppa.

Rating: 1/5

M&S Digestives – 25 biscuits, 400g, 80p

9

WHILE pricier than other super- market versions, these deluxe digestives from M&S are still good value compared with McVitie’s.

Sweeter than some on test but in a rich, mellow and smooth way.

Extremely tasty.

Rating: 4/5

Lidl Tower Gate Digestives – 26 biscuits, 400g, 57p

9

A GREAT value option from Lidl without compromising on flavour – they taste rich and sweet.

They also held up well during a cup-dunk.

But a shame there were fewer in the pack than many other own-brand offerings.

Rating: 4/5

Sainsbury’s Digestives – 28 biscuits, 400g, 70p

9

WITH a darker colour, these had a more wholesome flavour and were thick, offering a good crunch.

The biccies also had a milky and nice malty aftertaste and paired well with a cuppa.

A quality product at a great price.

Rating: 3/5

Asda Digestives – 27 biscuits, 400g, 70p

9

A GREAT-value offering with plenty to go round.

Sweeter than others on test, with an orangey hue and not very chunky, but the taste still hit the spot.

These also had a lovely aroma too, which made it hard to stop at just one.

Rating: 3/5

Morrisons Digestives – 27 biscuits, 400g, 70p

9

A GOOD ratio of crumble to crunch that stood up well in the cuppa dunk.

The flavour was pleasant too – not overtly sweet and with plenty in the packet.

These were thicker than some of the others, adding a pleasant texture.

Rating: 3/5

McVitie’s Digestives – 24 biscuits, 360g, £1.80, Tesco

9

AT well over a £1 more per packet than most supermarket versions, there are also fewer biccies, with only 24 inside.

They are enjoyable – but paying nearly two quid for them left a rather bad taste.

Rating: 2/5

A SHOPPER has warned people to “keep an eye out” after they bagged a garden chair that was reduced by 90%.

Lucky saver Christina shared her bargain in a post on Facebook after finally receiving delivery of the rocking seat.

2

2

The Maya Mango Rocking Chair she purchased had been reduced by a whopping 90%.

Instead of its regular retailing price of £214.99, Christina managed to nab it for just £21.99.

It had been listed on retail site Studio, which is owned by the Frasers Group alongside Sports Direct and House of Fraser.

Christina’s post on Facebook group Extreme Couponing and Bargains UK read: “Studio bargain.

Read More on Deals and Sales

“Took about a week to arrive.

“I’ve seen it go in and out of stock.. keep an eye out.”

More than 100 users were quick to comment underneath the post, desperate to grab the deal for themselves.

One said: “I want one of these for my bedroom.”

Another added: “I have one so comfy would recommend it.”

Others tagged their friends and family saying “keep an eye out for me please.”

One unlucky shopper, however, had the misfortune of buying the item at a much higher price just weeks before.

They said: “Oh my gutted, I bought this 4 weeks ago at 100 quid.”

Since Christina’s post, however, the item has now disappeared from Studio‘s website, indicating it may now be out of stock.

However, Christina added that while it’s not currently showing, it “keeps coming back and going again” like many other items at the moment.

This means there may be hope it returns at its major discount soon.

Studio is currently running a warehouse closing down sale, where it offers up to 90% off countless products.

It always pays, however, to compare prices so you know you’re getting the best deal.

There are countless other garden chairs listed online but many cost much more money.

The cheapest rocking garden chair we could find is currently listed at £45 from IKEA.

However, if you want one that looks most similar to the Studio product, Temu currently has a chair priced at £101.

Prices can also vary day to day and by what deals are on at the time, plus remember you might pay for delivery if you’re ordering online.

You can compare prices on platforms like Google Shopping.

How to bag a bargain

SUN Savers Editor Lana Clements explains how to find a cut-price item and bag a bargain…

Sign up to loyalty schemes of the brands that you regularly shop with.

Big names regularly offer discounts or special lower prices for members, among other perks.

Sales are when you can pick up a real steal.

Retailers usually have periodic promotions that tie into payday at the end of the month or Bank Holiday weekends, so keep a lookout and shop when these deals are on.

Sign up to mailing lists and you’ll also be first to know of special offers. It can be worth following retailers on social media too.

When buying online, always do a search for money off codes or vouchers that you can use vouchercodes.co.uk and myvouchercodes.co.uk are just two sites that round up promotions by retailer.

Scanner apps are useful to have on your phone. Trolley.co.uk app has a scanner that you can use to compare prices on branded items when out shopping.

Bargain hunters can also use B&M’s scanner in the app to find discounts in-store before staff have marked them out.

And always check if you can get cashback before paying which in effect means you’ll get some of your money back or a discount on the item.

Solstock | E+ | Getty Images

A version of this article first appeared in CNBC’s Inside Wealth newsletter with Robert Frank, a weekly guide to the high-net-worth investor and consumer. Sign up to receive future editions, straight to your inbox.

Wealthy millennials and Gen Zers are redefining the world of charitable giving, seeing themselves more as activists than donors, according to a new study.

Wealthy donors under the age of 43 are more likely to volunteer, fundraise and act as mentors for charitable causes rather than just give money, according to a new survey from Bank of America Private Bank. The survey of more than 1,000 respondents with more than $3 million in investible assets also found that young philanthropists want more public attention for their giving compared to Gen Xers and baby boomers.

The shift in the way the next generations give, as well as the causes they favor, is likely to remake the charitable landscape. Rather than simply writing checks to causes they care about, the next generation of givers wants to be deeply involved in trying to fix the biggest social and environmental problems.

“They view themselves as holistic social change agents,” said Dianne Chipps Bailey, managing director and national philanthropic strategy executive for philanthropic solutions at Bank of America Private Bank. “I think they have a better sense of agency in this world. They’re really looking to move their capital in a much more comprehensive robust way to achieve their social impact goals.”

Both younger and older multi-millionaires are highly charitable. According to the study, 91% of the respondents had given to charity in the past year. More than two-thirds of both older and younger respondents said they are motivated by “making a lasting impact.”

Yet their reasons for giving and their methods vary widely by age. Donors under the age of 43 are slightly more likely to volunteer and are twice as likely to help raise charitable donations from friends or peers rather than just giving directly. They’re more than four times as likely to act as mentors. And they’re more interested in serving on nonprofit boards rather than limiting their contributions to capital.

Older donors give from of a sense of responsibility. Those over the age of 44 were more than twice as likely to give due to “obligation” than younger donors. Those under 43 were more likely to cite self-education and the influence of their social circle as drivers of their philanthropy.

Some of the differences between generations may be rooted in life cycles and wealth. The younger wealthy are still building their fortunes and inheriting their wealth, so they’re more likely to give their time and help fundraise. Still, Bailey said the focus on peer networks and activism will likely endure even as they get older and wealthier.

“You can think of philanthropy as the five T’s – time, talent, treasure, testimony and ties,” she said. “The older generation is focused on the treasure (giving funds). The younger generations are leaning into the other four.”

The young wealthy also support different causes. They’re twice as likely to support efforts related to homelessness, social justice, climate change and the advancement of women and girls. Philanthropists over 44 were far more likely to support religious organizations, the arts and military charities.

“When you think about what [the younger generation] has been through in recent years, 2020, where they saw it all exposed, they’re leaning into the response,” Bailey said. “And it’s sustained. So many people move their giving with the headlines, but they’ve really dug in deeply. It’s not a moment but a movement.”

The implications of the generational shift in giving will be profound for wealth advisors and nonprofits, advisors say. Since many younger donors inherited their wealth, they’re far more likely to use giving vehicles created by their family. They were more than four times more likely to use charitable trusts, family foundations and donor advised funds.

Bailey said the next generation wants to talk about philanthropy as part of an initial discussion with a wealth advisor — even before talking about their investment plan.

“They have a hunger to know more, to learn more about philanthropy,” Bailey said. “They’ve already got these complex [giving] vehicles at the ready, so the education piece is critical both for nonprofits and for the advisors.”

With charity increasingly dominated by wealthy donors, and with the next generations expected to inherited over $80 trillion in the coming decades, courting the young rich will be critical.

“You need their perspective and you’re going to need their money,” Bailey said.

Advisors to the young rich also need to be generous with their praise. Younger donors are more than three times more likely to gauge the success of their philanthropic efforts by public recognition, according to the survey. Nearly half say they are likely to associate their names with their philanthropic efforts, while more than two-thirds of older donors give anonymously.

“Praise them, celebrate them, give them visibility,” she said.

Just don’t call them “philanthropists.” A report from Foundation Source found that 80% of young donors want to be seen as “givers,” while 63% also like the terms “advocate” or “changemaker.” Only 27% accepted the label of “philanthropist.”

Money

Martin Lewis issues warning to anyone aged under 22 – do you have £2,000 in a forgotten account?

MARTIN Lewis has issued a warning to anyone under 22 who could have £2,000 sitting in a forgotten account.

Child Trust Funds are long-term, tax-free savings accounts which were set up for every child born between September 2002 and January 2 2011.

2

2

The Money Saving Expert said on X that those aged 22 and under could have the Child Trust Fund set up and access it for free.

But he also warned that some firms are attempting to charge individuals to “get your own money” – but Lewis says “don’t pay.”

The Government deposited £250 for every child during that time period, or £500 if they came from a low income family earning around £16,000 a year or below.

An extra £250 or £500, depending on their families’ economic status, was deposited when the child turned seven.

read more on martin lewis

In 2010, this was reduced to £50 for better off households and £100 for those on a lower income.

The scheme was eventually scrapped in 2011 as part of cost-cutting measures following the 2009 financial crisis and was later replaced with Junior ISAs.

Currently, parents or friends can deposit up to £9,000 into the child’s account tax-free, with the money usually invested into shares.

The youngest children across Britian to have these accounts are about 13 years old, so have around five years before they can access the cash.

It is important to note that savings in these accounts are not held by the Government but are held in banks, building societies or other saving providers.

The money stays in the account until it’s withdrawn or re-invested.

Young people can take control of their Child Trust Fund at 16, but can only withdraw funds when they turn 18 and the account matures.

However, new figures released by the HMRC have found that more than 670,000 18-22 year olds are yet to claim their Child Trust Fund.

The tax office said that the average savings pot is worth £2,212.

Angela MacDonald, HMRC’s second permanent secretary and deputy chief executive, said the government wants to “reunite young people with their money and we’re making the process as simple as possible.”

She added: “You don’t need to pay anyone to find your Child Trust Fund for you, locate yours today by searching ‘find your Child Trust Fund’ on GOV.UK.”

How to track down a Child Trust Fund

If you were born in the UK between 2002 and 2006 it is worth checking to see if you have cash in a Child Trust Fund.

Parents were either given a voucher to set one up or HMRC set one up on a child’s behalf.

There are a number of third party groups offering to search for Child Trust Funds but it worth noting that they will charge a fee so you might loose a chunk of your money.

The Government has a free tool you can use online to help track down your fund.

You can find this by searching for “find a Child Trust Fund” on GOV.UK.

LOST CASH

By Charlene Young, pensions and savings expert at AJ Bell

MANY parents and children aren’t aware they even have the account, or don’t know who the money is with or how to track it down.

More than a quarter of CTF accounts were set up by the government because parents failed to do so within the 12-month window.

This highlights why so many are unclaimed – as the parents either weren’t aware or won’t remember that an account was even set up for their child, let alone where the money is now.

Any child born between 1 September 2002 and 2 January 2011 who hasn’t already got details of their account should track it down.

Once you’ve tracked down the money you can choose what to do with it. Your options are to transfer it to an adult ISA or withdraw the money. Until then your money will just sit in an account that no one else has access to, possibly paying very high charges.

Anything you transfer to an adult ISA at maturity will not count towards your annual ISA allowance, which is £20,000 for over 18s.

For many young people who have CTFs but are still under 18, it will make sense to transfer it to a Junior ISA, where the charges will likely be lower, and you’ll have a much bigger investment choice.

The money will still be locked up until you turn 18, but the tax-free benefits of ISA investing still apply. You can transfer the entire CTF into a Junior ISA and still add up to £9,000 to it in the same tax year.

You’ll need to have a few personal details to hand to do the search, including your date of birth and National Insurance (NI) number.

Your NI number remains the same for your entire life. It’s made up of two letters, six numbers and a final letter.

You can find this number on your payslips or by downloading the HMRC app, which can be downloaded on the Apple or Google Play Store.

When you’re done filling this out, HMRC will then send you a letter revealing what company has your Child Trust Fund.

What to do once you have claimed the money

Usually, people put the cash straight into a bank account, invest it, or transfer it into an ISA.

You can also ask your Child Trust Fund Provider to give you the money and get it cashed into your bank account.

This way you’ll need to share the bank account details you wish to transfer the cash into with HMRC.

But if you’d rather invest it, you can transfer it into an ISA.

The Sun recently broke down whether or not an ISA is right for you, which you can read here.

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to unsnarl a tangle of threads, according to physics

-

Womens Workouts2 weeks ago

Womens Workouts2 weeks ago3 Day Full Body Women’s Dumbbell Only Workout

-

Technology3 weeks ago

Technology3 weeks agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Science & Environment3 weeks ago

Science & Environment3 weeks ago‘Running of the bulls’ festival crowds move like charged particles

-

News3 weeks ago

the pick of new debut fiction

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow to wrap your mind around the real multiverse

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoSunlight-trapping device can generate temperatures over 1000°C

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLiquid crystals could improve quantum communication devices

-

News3 weeks ago

News3 weeks agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum forces used to automatically assemble tiny device

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy this is a golden age for life to thrive across the universe

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNerve fibres in the brain could generate quantum entanglement

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists are grappling with their own reproducibility crisis

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoLaser helps turn an electron into a coil of mass and charge

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoNuclear fusion experiment overcomes two key operating hurdles

-

Science & Environment2 weeks ago

Science & Environment2 weeks agoX-rays reveal half-billion-year-old insect ancestor

-

Business2 weeks ago

Eurosceptic Andrej Babiš eyes return to power in Czech Republic

-

News4 weeks ago

News4 weeks ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoCaroline Ellison aims to duck prison sentence for role in FTX collapse

-

News3 weeks ago

News3 weeks agoYou’re a Hypocrite, And So Am I

-

Sport3 weeks ago

Sport3 weeks agoJoshua vs Dubois: Chris Eubank Jr says ‘AJ’ could beat Tyson Fury and any other heavyweight in the world

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA slight curve helps rocks make the biggest splash

-

News3 weeks ago

News3 weeks ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Technology2 weeks ago

Technology2 weeks ago‘From a toaster to a server’: UK startup promises 5x ‘speed up without changing a line of code’ as it plans to take on Nvidia, AMD in the generative AI battlefield

-

Football2 weeks ago

Football2 weeks agoFootball Focus: Martin Keown on Liverpool’s Alisson Becker

-

News3 weeks ago

News3 weeks agoNew investigation ordered into ‘doorstep murder’ of Alistair Wilson

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoRethinking space and time could let us do away with dark matter

-

Business2 weeks ago

Should London’s tax exiles head for Spain, Italy . . . or Wales?

-

MMA2 weeks ago

MMA2 weeks agoConor McGregor challenges ‘woeful’ Belal Muhammad, tells Ilia Topuria it’s ‘on sight’

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoFuture of fusion: How the UK’s JET reactor paved the way for ITER

-

Technology2 weeks ago

Technology2 weeks agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoWhy we need to invoke philosophy to judge bizarre concepts in science

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoA tale of two mysteries: ghostly neutrinos and the proton decay puzzle

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoUK spurns European invitation to join ITER nuclear fusion project

-

News3 weeks ago

Israel strikes Lebanese targets as Hizbollah chief warns of ‘red lines’ crossed

-

Technology2 weeks ago

Technology2 weeks agoQuantum computers may work better when they ignore causality

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCardano founder to meet Argentina president Javier Milei

-

News3 weeks ago

The Project Censored Newsletter – May 2024

-

News3 weeks ago

News3 weeks agoWhy Is Everyone Excited About These Smart Insoles?

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMeet the world's first female male model | 7.30

-

News3 weeks ago

News3 weeks agoFour dead & 18 injured in horror mass shooting with victims ‘caught in crossfire’ as cops hunt multiple gunmen

-

Womens Workouts2 weeks ago

Womens Workouts2 weeks ago3 Day Full Body Toning Workout for Women

-

Technology2 weeks ago

Technology2 weeks agoRobo-tuna reveals how foldable fins help the speedy fish manoeuvre

-

Technology2 weeks ago

Technology2 weeks agoGet ready for Meta Connect

-

Health & fitness2 weeks ago

Health & fitness2 weeks agoThe 7 lifestyle habits you can stop now for a slimmer face by next week

-

Sport2 weeks ago

Sport2 weeks agoWatch UFC star deliver ‘one of the most brutal knockouts ever’ that left opponent laid spark out on the canvas

-

Technology3 weeks ago

Technology3 weeks agoThe ‘superfood’ taking over fields in northern India

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe maps that could hold the secret to curing cancer

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoThe secret to a six pack – and how to keep your washboard abs in 2022

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoBeing in two places at once could make a quantum battery charge faster

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLow users, sex predators kill Korean metaverses, 3AC sues Terra: Asia Express

-

Politics3 weeks ago

UK consumer confidence falls sharply amid fears of ‘painful’ budget | Economics

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoBest Exercises if You Want to Build a Great Physique

-

Womens Workouts3 weeks ago

Womens Workouts3 weeks agoEverything a Beginner Needs to Know About Squatting

-

TV3 weeks ago

TV3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoCNN TÜRK – 🔴 Canlı Yayın ᴴᴰ – Canlı TV izle

-

Servers computers2 weeks ago

Servers computers2 weeks agoWhat are the benefits of Blade servers compared to rack servers?

-

Technology2 weeks ago

Technology2 weeks agoThe best robot vacuum cleaners of 2024

-

Business1 week ago

Ukraine faces its darkest hour

-

Business3 weeks ago

JPMorgan in talks to take over Apple credit card from Goldman Sachs

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoQuantum time travel: The experiment to ‘send a particle into the past’

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin miners steamrolled after electricity thefts, exchange ‘closure’ scam: Asia Express

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDorsey’s ‘marketplace of algorithms’ could fix social media… so why hasn’t it?

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDZ Bank partners with Boerse Stuttgart for crypto trading

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBitcoin bulls target $64K BTC price hurdle as US stocks eye new record

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow one theory ties together everything we know about the universe

-

News3 weeks ago

News3 weeks agoChurch same-sex split affecting bishop appointments

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoTiny magnet could help measure gravity on the quantum scale

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoBlockdaemon mulls 2026 IPO: Report

-

Sport3 weeks ago

Sport3 weeks agoUFC Edmonton fight card revealed, including Brandon Moreno vs. Amir Albazi headliner

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoEthereum is a 'contrarian bet' into 2025, says Bitwise exec

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCoinbase’s cbBTC surges to third-largest wrapped BTC token in just one week

-

News2 weeks ago

News2 weeks agoUS Newspapers Diluting Democratic Discourse with Political Bias

-

Politics3 weeks ago

Politics3 weeks agoTrump says he will meet with Indian Prime Minister Narendra Modi next week

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoDecentraland X account hacked, phishing scam targets MANA airdrop

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoPhysicists have worked out how to melt any material

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoRedStone integrates first oracle price feeds on TON blockchain

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks ago‘No matter how bad it gets, there’s a lot going on with NFTs’: 24 Hours of Art, NFT Creator

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoHow do you recycle a nuclear fusion reactor? We’re about to find out

-

Business3 weeks ago

Thames Water seeks extension on debt terms to avoid renationalisation

-

Business3 weeks ago

How Labour donor’s largesse tarnished government’s squeaky clean image

-

Politics3 weeks ago

‘Appalling’ rows over Sue Gray must stop, senior ministers say | Sue Gray

-

Technology3 weeks ago

Technology3 weeks agoiPhone 15 Pro Max Camera Review: Depth and Reach

-

News3 weeks ago

News3 weeks agoBrian Tyree Henry on voicing young Megatron, his love for villain roles

-

News3 weeks ago

Brian Tyree Henry on voicing young Megatron, his love for villain roles

-

MMA3 weeks ago

MMA3 weeks agoRankings Show: Is Umar Nurmagomedov a lock to become UFC champion?

-

Travel2 weeks ago

Travel2 weeks agoDelta signs codeshare agreement with SAS

-

Politics2 weeks ago

Politics2 weeks agoHope, finally? Keir Starmer’s first conference in power – podcast | News

-

News4 weeks ago

News4 weeks agoHow FedEx CEO Raj Subramaniam Is Adapting to a Post-Pandemic Economy

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoLouisiana takes first crypto payment over Bitcoin Lightning

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoCrypto scammers orchestrate massive hack on X but barely made $8K

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoTelegram bot Banana Gun’s users drained of over $1.9M

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMost accurate clock ever can tick for 40 billion years without error

-

CryptoCurrency3 weeks ago

CryptoCurrency3 weeks agoSEC asks court for four months to produce documents for Coinbase

You must be logged in to post a comment Login