Money

Wealth Management for High-Net-Worth Individuals

The Importance of Personalized Wealth Management

Wealth management for high-net-worth individuals (HNWIs) is not a one-size-fits-all service. It requires tailored strategies that address specific financial needs and goals. HNWIs often deal with complex financial portfolios that include investments, real estate, and business interests. Therefore, expert wealth managers create customized financial plans to ensure their clients’ wealth grows, is protected, and is transferred efficiently. Personalized wealth management also involves tax planning, estate planning, and risk mitigation, all crucial for preserving and enhancing wealth over time.

Key Services in Wealth Management

Wealth management for HNWIs encompasses a range of financial services designed to meet unique requirements. These services typically include investment management, financial planning, and estate planning. Wealth managers also provide advice on tax efficiency, retirement planning, and philanthropic activities. Investment strategies are especially important, as they involve balancing risk and return to achieve long-term financial goals. Comprehensive wealth management goes beyond simple oversight; it ensures that all aspects of an individual’s financial life are integrated into a cohesive plan.

Tailored Investment Strategies

Tailored investment strategies are a fundamental aspect of high net worth individuals wealth management. Each client’s financial objectives, risk tolerance, and time horizon are considered when creating a personalized portfolio. Wealth managers often incorporate a mix of asset classes, including equities, bonds, real estate, and alternative investments, to diversify risk. They also regularly review and adjust the portfolio based on market conditions and client goals. These strategies help ensure that investments align with long-term financial objectives, maximizing returns while managing risks effectively.

Tax Planning and Optimization

Effective tax planning is a vital component of wealth management for HNWIs. With higher incomes and more complex financial portfolios, tax efficiency is essential to preserve wealth. Wealth managers work with tax specialists to develop strategies that reduce tax liabilities while complying with regulations. These strategies may include tax-loss harvesting, charitable donations, and retirement account contributions. By taking advantage of tax-efficient investment vehicles and structures, high-net-worth individuals can maximize their after-tax returns, ensuring their wealth continues to grow without unnecessary tax burdens.

Estate and Legacy Planning

Estate planning is crucial for high-net-worth individuals to ensure the smooth transfer of assets to heirs or chosen beneficiaries. Wealth managers collaborate with estate planning attorneys to create comprehensive plans that minimize estate taxes and protect family wealth for future generations. Key elements of estate planning include wills, trusts, and charitable giving strategies. Legacy planning also involves preparing heirs to manage inherited wealth responsibly. By addressing these aspects in advance, HNWIs can protect their legacy and ensure financial security for future generations.

Risk Management and Asset Protection

Wealth managers prioritize risk management by developing strategies that protect assets against potential financial threats. For high-net-worth individuals, this may include diversifying investments, obtaining appropriate insurance, and setting up legal structures like trusts. These measures help mitigate risks associated with market volatility, lawsuits, and other financial threats. Wealth managers also conduct regular reviews to ensure that their clients’ risk exposure aligns with their financial goals. By incorporating comprehensive risk management, HNWIs can secure their wealth against unforeseen circumstances.

Philanthropic Planning and Charitable Giving

Many high-net-worth individuals integrate philanthropy into their wealth management strategies. Wealth managers offer guidance on charitable giving plans that align with the client’s values while also providing tax benefits. Charitable giving strategies may include establishing donor-advised funds, private foundations, or direct donations. These approaches allow individuals to support causes they care about while also receiving potential tax deductions. Thoughtful philanthropic planning ensures that charitable donations are structured to maximize both the impact of the gift and the financial benefits for the donor.

Retirement Planning for HNWIs

Retirement planning is another critical aspect of wealth management for high-net-worth individuals. Unlike traditional retirement planning, which focuses primarily on income replacement, HNWIs often have more complex considerations, such as maintaining a lifestyle, managing multiple properties, and funding philanthropic endeavours. Wealth managers create strategies that ensure clients can sustain their desired lifestyle throughout retirement while continuing to grow their wealth. This involves balancing income generation, tax efficiency, and risk management to create a retirement plan that meets both current and future needs.

Diversification and Alternative Investments

High-net-worth individuals often have access to a broader range of investment opportunities, including alternative investments such as private equity, hedge funds, and real estate. Wealth managers guide clients in selecting strategic investments that complement their existing portfolios and align with their risk tolerance. Diversification is crucial in protecting against market volatility and ensuring that wealth grows steadily. By incorporating alternative investments into a diversified portfolio, wealth managers help clients achieve superior returns while mitigating the risks associated with traditional asset classes.

Financial Planning for Business Owners

Many high-net-worth individuals are business owners who face unique financial challenges. Wealth managers offer specialized services that address both personal and business financial needs. This includes succession planning, liquidity management, and tax-efficient strategies for managing or transferring business ownership. A well-structured wealth management approach ensures that business owners can maximize the value of their business while protecting personal assets. By integrating personal and business financial planning, wealth managers help clients navigate the complexities of wealth preservation and growth.

Family Governance and Wealth Education

For many high-net-worth families, maintaining and growing wealth across generations is a significant concern. Wealth managers assist in creating family governance structures that establish clear guidelines for managing family assets and decision-making processes. Additionally, wealth education programs help younger generations understand the responsibilities that come with managing significant assets. By promoting financial literacy and open communication, wealth managers ensure that family wealth is preserved and responsibly managed for future generations. Family governance structures help maintain family harmony while fostering long-term financial success.

The Role of Technology in Wealth Management

Technological advancements are transforming the wealth management industry, offering high-net-worth individuals greater access to financial tools and insights. Digital platforms enable wealth managers to monitor portfolios in real-time, adjust investment strategies, and provide detailed reporting. Wealth management firms also use advanced analytics and artificial intelligence to optimize financial strategies and predict market trends. This integration of technology enhances the decision-making process and allows wealth managers to offer more personalized and effective services. As technology continues to evolve, it will play an increasingly important role in wealth management for HNWIs.

Conclusion

Wealth management for high-net-worth individuals requires a comprehensive approach that addresses investment strategies, tax efficiency, risk management, and estate planning. Tailored financial solutions ensure that each client’s unique needs are met, whether through diversification, strategic investments, or philanthropic planning. By earning clients’ trust and offering expert guidance, wealth managers help HNWIs protect and grow their wealth, ensuring financial security for both current and future generations. The strategic integration of technology and professional expertise allows for more effective wealth management in today’s evolving financial landscape.

Three new permanent executive directors have been appointed to the board of The Pensions Regulator (TPR).

The appointments, which will “help deliver TPR’s new regulatory approach”, were approved by pensions minister Emma Reynolds.

The new directors are Nina Blackett, executive director of strategy, policy and analysis, Gaucho Rasmussen, executive director of regulatory compliance and Neil Bull, executive director of market oversight.

They will help accelerate the shift in TPR’s regulatory approach to meet the challenges and opportunities of a changing pensions market.

Blackett has served as both director of digital services and interim director of strategy, policy and analysis since joining TPR in September 2023.

She brings considerable experience in leading digital transformation in finance, healthcare and education to her new role.

Neil Bull has more than 25 years of experience in the commercial pensions sector and brings a deep understanding of the pensions market and risk management to the role.

He previously served as TPR’s head of investment before becoming interim director of market oversight in April 2024.

Gaucho Rasmussen is a regulatory and enforcement leader with extensive experience in organisational change and development.

He joins TPR from Amazon, where he has been advising on regulatory compliance across Europe.

Prior to this, Gaucho held positions as director of enforcement at both Ofcom and the Competition and Markets Authority (CMA).

TPR chief executive Nausicaa Delfas said: “The pensions market is rapidly changing and moving towards fewer, larger schemes, bringing new opportunities and new risks. We are evolving as a regulator to meet these challenges.

“Gaucho, Neil and Nina will each play a critical part in accelerating the shift in our regulatory approach that will help us to protect, enhance and innovate in a changing pensions market, and become a more efficient and effective regulator.”

In February, TPR announced the establishment of three new regulatory functions – regulatory compliance, market oversight and strategy, policy and analysis.

Money

Toob app ‘down’ as thousands report issues with broadband provider and blast ‘useless’ internet

THE Toob app is “down” as thousands report issues with the broadband provider and blast the “useless” internet.

Downdetector received more than 3,500 complaints about the service just before 12.25pm today.

1

The vast majority – 82 per cent – of those were to do with the internet.

URW said 63% of its affected units have either been re-let or are still occupied by the existing tenants with the remainder affecting vacancy levels.

The post URW forecasts drop in vacancy levels after bankruptcies hit 191 units appeared first on Property Week.

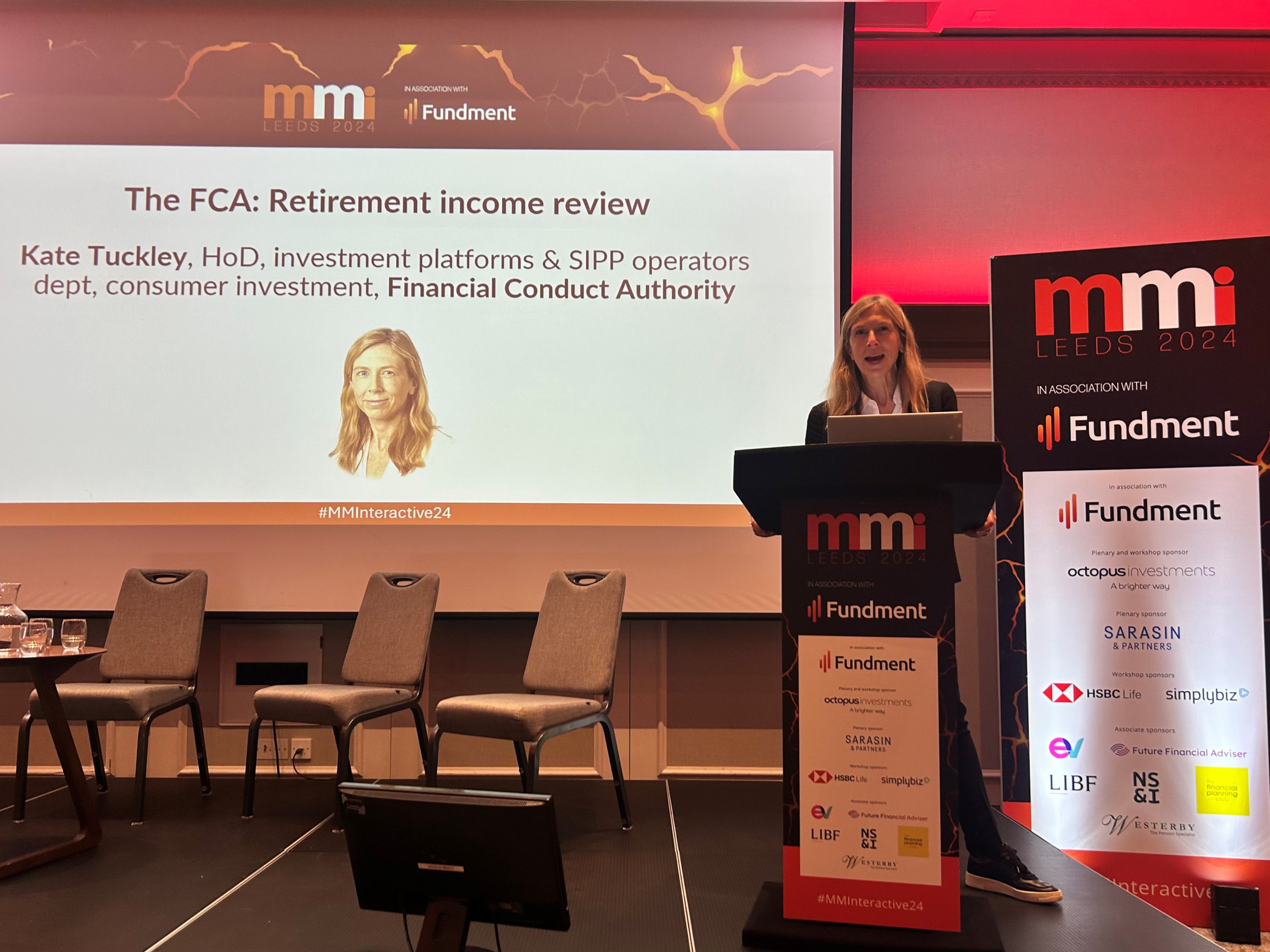

Accurate risk profiling is the “foundation of good advice”, the Financial Conduct Authority’s head of investment platforms Kate Tuckley has insisted.

She said moving from accumulation to decumulation is likely to change a customer’s attitude to risk, so this should be reassessed.

“Advisers should not assume that a risk profile remains the same, either when moving into decumulation or from previous advice meetings,” she added.

She made the comments during a keynote speech at Money Marketing Interactive in Leeds yesterday (24 October).

“A key risk is capacity for loss – the ability to absorb losses in retirement, which is critical given the lower future earning potential.

“Many customers may have been able to recover losses during their working years, but this changes in retirement.”

She cited the FCA’s thematic review of retirement income advice, which found that some advisers’ files did not show that capacity for loss had been assessed, or where it had been assessed.

“Clear consideration of this is crucial to demonstrate the suitability of advice,” she said.

“Cash flow modelling (CFM) tools can be used for capacity for loss assessments. However, firms need to assess both attitude to risk and capacity for loss consistently.

“Tools such as standard questionnaires can be useful, but you should be aware of their limitations, especially when the language or questions are not tailored to decumulation, which can lead to incorrect profiling.

“Whatever approach is used, firms must demonstrate that their methods are suitable for retirement income advice.”

Pension freedoms came into effect in 2015, giving consumers more choice and less prescription in how they meet their retirement income needs.

“They can take as much or as little as they like, or even fully cash out if they choose,” said Tuckley.

“As you know, there’s no longer a requirement to buy an annuity, and drawdown is no longer just for the wealthy.

“However,” she warned, “more choice brings more complexity, not just for consumers but also for advisers.

“Most consumers have moved away from guaranteed income for life and keep their pension savings invested, which presents a big challenge for advisers.”

She said advisers need to help consumers manage ongoing risks and make complex decisions about meeting their income needs sustainably.

The FCA is following up on the thematic review and is “completing further work” on retirement income advice, which Tuckley said will continue to be a “priority” in its strategy.

“We want to explore this in more depth to understand how firms are responding to our report,” she said.

The regulator aims to publish further findings in the first quarter of 2025.

Money

Exact date to turn on your heating named by thousands of households but waiting just seven days could save you £84

THOUSANDS of households have named the date they are planning on turning their heating ahead of winter.

But, wait just a few days after this date and you could save yourself almost £100.

1

A study of 2,000 homeowners with central heating found that three quarters plan on waiting until October 31 to turn their radiators on.

But, you could actually save yourself £84 if you waited just a week longer and turned it on on November 7.

That’s based on a household using a 24kW gas boiler for eight hours a day for seven days straight.

Of course, you could save more or less than this based on your usage, but it shows how delaying by just a week could be well worth it.

The study, carried out by utilita Energy also found that despite not having done so yet, 52% are looking forward to warming up their homes next week.

To help them refrain from switching on their boiler, 60% have been layering up, while 24% have resorted to electric blankets.

But even throughout the coldest months, 57% claim they will only put the heating on ‘for an hour or two’ to minimise costs.

What’s more, 45% plan on using an electric heater as well as their main central heating this winter, with 34% assuming it’s a cheaper option.

And 15% plan to completely replace the gas central heating with a portable electric heater – despite it costing three to four times more per hour, Utilita energy efficiency experts revealed.

A spokesperson for the energy supplier, which commissioned the research, said: “The first time you turn on the heating in winter marks the true arrival of the colder months – filling your home with warmth and comfort.

“We hope this important heating behaviour study will help people to realise the false economy of using a portable electric heater to subsidise or replace gas central heating, and afford budgeting households as much as 75% more heat hours this winter.”

The study also found half of households claim to be confident in working out the cost of an electric heater versus gas central heating.

According to the OnePoll.com data, 59% financially prepare for the rise in energy spend when it reaches the colder months, and the heating needs to come on.

Although 76% admit they will reach for the thermostat at the first sign of feeling uncomfortable or cold and 27% give into requests from other household members.

More than half (54%) will be prompted by a drop in the outside temperature, with it reaching an average of nine degrees Celsius before considering igniting up the boiler.

The living room is typically the room that gets heated up (33%), but 26% choose to turn the heating on throughout the entire house.

The Utilita Energy spokesperson added: “When comparing electric heaters to central heating, it’s important to consider both cost and comfort.

“While electric heaters can offer quick, localised warmth and are ideal for heating individual rooms, central heating provides consistent, zonal heating that’s far better for those on a budget.”

How to save money on your heating

There are countless ways you can save money on your heating bill this winter.

Blocking draughts in your home can easily save you £40 a year, according to the Energy Saving Trust.

Draught excluders typically cost around £20 to £40, but you can also use your own items laying about the house.

You can use radiator foil, which you put behind the appliances to reflect heat back into the room too.

You can get a roll of the handy stuff in Screwfix for just £7.51.

Heat activated fans can be placed on wood burners and even certain types of gas fire to throw heat into the main part of the room too.

You can pick these up from the likes of B&Q for as little as £15.

What energy bill help is available?

There’s a number of different ways to get help paying your energy bills if you’re struggling to get by.

If you fall into debt, you can always approach your supplier to see if they can put you on a repayment plan before putting you on a prepayment meter.

This involves paying off what you owe in instalments over a set period.

If your supplier offers you a repayment plan you don’t think you can afford, speak to them again to see if you can negotiate a better deal.

Several energy firms have grant schemes available to customers struggling to cover their bills.

But eligibility criteria vary depending on the supplier and the amount you can get depends on your financial circumstances.

For example, British Gas or Scottish Gas customers struggling to pay their energy bills can get grants worth up to £2,000.

British Gas also offers help via its British Gas Energy Trust and Individuals Family Fund.

You don’t need to be a British Gas customer to apply for the second fund.

EDF, E.ON, Octopus Energy and Scottish Power all offer grants to struggling customers too.

Thousands of vulnerable households are missing out on extra help and protections by not signing up to the Priority Services Register (PSR).

The service helps support vulnerable households, such as those who are elderly or ill, and some of the perks include being given advance warning of blackouts, free gas safety checks and extra support if you’re struggling.

Get in touch with your energy firm to see if you can apply.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

It’s no secret that tech stocks have been powering the market gains over the past few years, and software stocks were among the biggest drivers of this growth.

Multiple factors are propelling the software industry forward, such as the rapid advancement of AI technology, high demand for IT solutions, and the ongoing expansion of the global digital economy.

Wedbush tech expert Daniel Ives has been watching the tech industry, and his take on it points to continued strength supported by AI and cloud expansion.

“Solid enterprise spending, digital advertising rebound, and the AI Revolution will drive tech stocks higher into year-end in our view,” Ives opined. “We believe 70% of global workloads will be on the cloud by the end of 2025, up from less than 50% today.”

Keeping that in mind, Ives goes on to add that the time has come to hit buy on two software stocks. They may not be household names, but according to the TipRanks data, both stocks are Buy-rated – and Ives sees significantly more upside to each than the consensus on the Street. Let’s take a closer look.

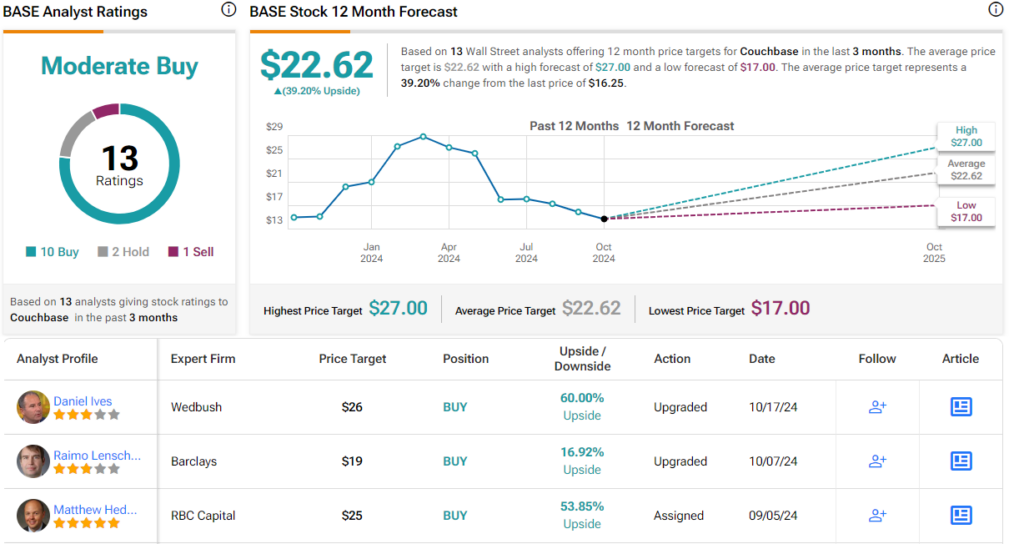

Couchbase (BASE)

We’ll start with Couchbase, a modern database platform provider that offers users and developers everything they need to support a wide range of applications – from cloud, to edge, to AI. Couchbase bills itself as a one-stop-shop for data developers and architects, making its services available through its powerful database-as-a-service platform, Capella. Organizations using the service can quickly create applications and services that deliver premium customer experiences, giving top-end performance at affordable prices.

The Capella platform brings the popular as-a-service subscription model to the database industry. The company can support database services for a wide range of AI applications, including the latest gen-AI tech, as well as database search, mobile access, and analytic functions. Customers can also choose self-managed services through Couchbase’s servers, with on-premises management for both multicloud and community apps.

Couchbase’s database service has found success in a wide range of fields, including the gaming, healthcare, entertainment, retail, travel, and utility sectors. The company’s customer base includes such major names as Verizon, UPS, Walmart, Cisco, Comcast, GE, and PayPal.

Turning to the financial results, we see that Couchbase reported its fiscal 2Q25 figures at the start of last month. The top line of $51.6 million was up almost 20% year-over-year and came in just over the forecast, beating expectations by nearly a half-million dollars. At the bottom line, the company ran a net loss of 6 cents per share in non-GAAP measures, but that was 3 cents per share better than had been anticipated.

-

Technology4 weeks ago

Technology4 weeks agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment1 month ago

Science & Environment1 month agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment1 month ago

Science & Environment1 month agoHyperelastic gel is one of the stretchiest materials known to science

-

Science & Environment1 month ago

Science & Environment1 month ago‘Running of the bulls’ festival crowds move like charged particles

-

Science & Environment1 month ago

Science & Environment1 month agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Technology1 month ago

Technology1 month agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment4 weeks ago

Science & Environment4 weeks agoX-rays reveal half-billion-year-old insect ancestor

-

Science & Environment1 month ago

Science & Environment1 month agoSunlight-trapping device can generate temperatures over 1000°C

-

Science & Environment1 month ago

Science & Environment1 month agoLiquid crystals could improve quantum communication devices

-

Technology4 weeks ago

Technology4 weeks agoUkraine is using AI to manage the removal of Russian landmines

-

TV3 weeks ago

TV3 weeks agoসারাদেশে দিনব্যাপী বৃষ্টির পূর্বাভাস; সমুদ্রবন্দরে ৩ নম্বর সংকেত | Weather Today | Jamuna TV

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum ‘supersolid’ matter stirred using magnets

-

Science & Environment1 month ago

Science & Environment1 month agoLaser helps turn an electron into a coil of mass and charge

-

News3 weeks ago

News3 weeks agoMassive blasts in Beirut after renewed Israeli air strikes

-

Football3 weeks ago

Football3 weeks agoRangers & Celtic ready for first SWPL derby showdown

-

Technology3 weeks ago

Technology3 weeks agoSamsung Passkeys will work with Samsung’s smart home devices

-

News3 weeks ago

News3 weeks ago▶ Hamas Spent $1B on Tunnels Instead of Investing in a Future for Gaza’s People

-

Science & Environment1 month ago

Science & Environment1 month agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Womens Workouts1 month ago

Womens Workouts1 month ago3 Day Full Body Women’s Dumbbell Only Workout

-

Business3 weeks ago

Business3 weeks agoWhen to tip and when not to tip

-

MMA3 weeks ago

MMA3 weeks ago‘Uncrowned queen’ Kayla Harrison tastes blood, wants UFC title run

-

Sport3 weeks ago

Sport3 weeks agoBoxing: World champion Nick Ball set for Liverpool homecoming against Ronny Rios

-

News3 weeks ago

News3 weeks agoNavigating the News Void: Opportunities for Revitalization

-

Technology4 weeks ago

Technology4 weeks agoMicrophone made of atom-thick graphene could be used in smartphones

-

Sport3 weeks ago

Sport3 weeks agoMan City ask for Premier League season to be DELAYED as Pep Guardiola escalates fixture pile-up row

-

Science & Environment1 month ago

Science & Environment1 month agoPhysicists have worked out how to melt any material

-

Science & Environment1 month ago

Science & Environment1 month agoWhy this is a golden age for life to thrive across the universe

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum forces used to automatically assemble tiny device

-

News1 month ago

News1 month ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Business3 weeks ago

DoJ accuses Donald Trump of ‘private criminal effort’ to overturn 2020 election

-

MMA3 weeks ago

MMA3 weeks agoPereira vs. Rountree prediction: Champ chases legend status

-

News3 weeks ago

News3 weeks ago‘Blacks for Trump’ and Pennsylvania progressives play for undecided voters

-

Sport3 weeks ago

Sport3 weeks agoWales fall to second loss of WXV against Italy

-

MMA3 weeks ago

MMA3 weeks agoDana White’s Contender Series 74 recap, analysis, winner grades

-

Sport3 weeks ago

Sport3 weeks agoAaron Ramsdale: Southampton goalkeeper left Arsenal for more game time

-

Science & Environment1 month ago

Science & Environment1 month agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

Science & Environment1 month ago

Science & Environment1 month agoA slight curve helps rocks make the biggest splash

-

Technology1 month ago

Technology1 month agoMeta has a major opportunity to win the AI hardware race

-

Science & Environment1 month ago

Science & Environment1 month agoNerve fibres in the brain could generate quantum entanglement

-

Science & Environment1 month ago

Science & Environment1 month agoHow to wrap your mind around the real multiverse

-

Technology4 weeks ago

Technology4 weeks agoRussia is building ground-based kamikaze robots out of old hoverboards

-

MMA3 weeks ago

MMA3 weeks agoJulianna Peña trashes Raquel Pennington’s behavior as champ

-

Technology3 weeks ago

Technology3 weeks agoMusk faces SEC questions over X takeover

-

Football3 weeks ago

Football3 weeks agoWhy does Prince William support Aston Villa?

-

Technology3 weeks ago

Technology3 weeks agoThis AI video generator can melt, crush, blow up, or turn anything into cake

-

Sport3 weeks ago

Sport3 weeks agoSturm Graz: How Austrians ended Red Bull’s title dominance

-

News3 weeks ago

News3 weeks agoFamily plans to honor hurricane victim using logs from fallen tree that killed him

-

Science & Environment1 month ago

Science & Environment1 month agoNuclear fusion experiment overcomes two key operating hurdles

-

Technology1 month ago

Technology1 month agoWhy Machines Learn: A clever primer makes sense of what makes AI possible

-

Science & Environment1 month ago

Science & Environment1 month agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

News1 month ago

News1 month ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Money3 weeks ago

Money3 weeks agoWetherspoons issues update on closures – see the full list of five still at risk and 26 gone for good

-

Technology3 weeks ago

Technology3 weeks agoThe best budget robot vacuums for 2024

-

Technology3 weeks ago

Technology3 weeks agoGmail gets redesigned summary cards with more data & features

-

Business3 weeks ago

Sterling slides after Bailey says BoE could be ‘a bit more aggressive’ on rates

-

Technology3 weeks ago

Technology3 weeks agoMicrosoft just dropped Drasi, and it could change how we handle big data

-

Sport3 weeks ago

Sport3 weeks agoChina Open: Carlos Alcaraz recovers to beat Jannik Sinner in dramatic final

-

MMA3 weeks ago

MMA3 weeks agoPereira vs. Rountree preview show live stream

-

Sport3 weeks ago

Sport3 weeks agoCoco Gauff stages superb comeback to reach China Open final

-

Entertainment3 weeks ago

Entertainment3 weeks agoNew documentary explores actor Christopher Reeve’s life and legacy

-

Sport4 weeks ago

Sport4 weeks agoWorld’s sexiest referee Claudia Romani shows off incredible figure in animal print bikini on South Beach

-

Business3 weeks ago

Bank of England warns of ‘future stress’ from hedge fund bets against US Treasuries

-

Business3 weeks ago

Business3 weeks agoChancellor Rachel Reeves says she needs to raise £20bn. How might she do it?

-

News3 weeks ago

News3 weeks agoWoman who died of cancer ‘was misdiagnosed on phone call with GP’

-

Technology3 weeks ago

Technology3 weeks agoTexas is suing TikTok for allegedly violating its new child privacy law

-

Technology3 weeks ago

Technology3 weeks agoThe best shows on Max (formerly HBO Max) right now

-

Sport3 weeks ago

Sport3 weeks ago2024 ICC Women’s T20 World Cup: Pakistan beat Sri Lanka

-

Technology3 weeks ago

Technology3 weeks agoEpic Games CEO Tim Sweeney renews blast at ‘gatekeeper’ platform owners

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMarkets watch for dangers of further escalation

-

MMA3 weeks ago

MMA3 weeks agoAlex Pereira faces ‘trap game’ vs. Khalil Rountree

-

News3 weeks ago

News3 weeks agoGerman Car Company Declares Bankruptcy – 200 Employees Lose Their Jobs

-

MMA3 weeks ago

MMA3 weeks agoUFC 307 preview show: Will Alex Pereira’s wild ride continue, or does Khalil Rountree shock the world?

-

MMA3 weeks ago

MMA3 weeks ago‘I was fighting on automatic pilot’ at UFC 306

-

MMA3 weeks ago

MMA3 weeks agoKetlen Vieira vs. Kayla Harrison pick, start time, odds: UFC 307

-

News1 month ago

the pick of new debut fiction

-

News1 month ago

News1 month agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Football3 weeks ago

Football3 weeks agoSimo Valakari: New St Johnstone boss says Scotland special in his heart

-

Technology3 weeks ago

Technology3 weeks agoJ.B. Hunt and UP.Labs launch venture lab to build logistics startups

-

News3 weeks ago

News3 weeks agoHull KR 10-8 Warrington Wolves – Robins reach first Super League Grand Final

-

Technology3 weeks ago

Technology3 weeks agoOpenAI secured more billions, but there’s still capital left for other startups

-

Business3 weeks ago

The search for Japan’s ‘lost’ art

-

Business3 weeks ago

Business3 weeks agoStark difference in UK and Ireland’s budgets

-

News3 weeks ago

News3 weeks agoBalancing India and China Is the Challenge for Sri Lanka’s Dissanayake

-

News3 weeks ago

News3 weeks agoHeavy strikes shake Beirut as Israel expands Lebanon campaign

-

TV3 weeks ago

TV3 weeks agoLove Island star sparks feud rumours as one Islander is missing from glam girls’ night

-

TV3 weeks ago

TV3 weeks agoPhillip Schofield accidentally sets his camp on FIRE after using emergency radio to Channel 5 crew

-

News3 weeks ago

News3 weeks agoHeartbreaking end to search as body of influencer, 27, found after yacht party shipwreck on ‘Devil’s Throat’ coastline

-

Technology3 weeks ago

Technology3 weeks agoPopular financial newsletter claims Roblox enables child sexual abuse

-

Business3 weeks ago

Head of UK Competition Appeal Tribunal to step down after rebuke for serious misconduct

-

Technology3 weeks ago

Technology3 weeks agoApple iPhone 16 Plus vs Samsung Galaxy S24+

-

TV3 weeks ago

TV3 weeks agoMaayavi (මායාවී) | Episode 23 | 02nd October 2024 | Sirasa TV

-

Politics3 weeks ago

Rosie Duffield’s savage departure raises difficult questions for Keir Starmer. He’d be foolish to ignore them | Gaby Hinsliff

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoNHS surgeon who couldn’t find his scalpel cut patient’s chest open with the penknife he used to slice up his lunch

-

Money3 weeks ago

Money3 weeks agoPub selling Britain’s ‘CHEAPEST’ pints for just £2.60 – but you’ll have to follow super-strict rules to get in

-

Technology3 weeks ago

Technology3 weeks agoIf you’ve ever considered smart glasses, this Amazon deal is for you

-

News3 weeks ago

News3 weeks agoLiverpool secure win over Bologna on a night that shows this format might work

-

Technology3 weeks ago

Technology3 weeks agoAmazon’s Ring just doubled the price of its alarm monitoring service for grandfathered customers

-

Technology3 weeks ago

Technology3 weeks agoHow to disable Google Assistant on your Pixel Watch 3

-

Business3 weeks ago

Can liberals be trusted with liberalism?

-

Technology3 weeks ago

Technology3 weeks agoA very underrated horror movie sequel is streaming on Max

You must be logged in to post a comment Login