Cheap natural gas is spurring Chinese truckers to switch to rigs powered by the fuel, damping the country’s appetite for oil and contributing to a “catastrophic” sales drop for the China unit of one of the world’s largest truckmakers.

While the country’s rapid adoption of electric cars has been in the spotlight, significant change has also been taking place in China’s freight industry.

Analysts said the swift rise of natural gas-powered trucks, particularly heavy-duty vehicles of 14 tonnes and above, had helped thrust China past peak diesel demand and moved it closer to reaching peak oil.

The trend has hit Germany’s Daimler Truck, which has focused on perfecting diesel engines and building electric and hydrogen-based engines for the future.

“Diesel demand peaked earlier than we expected,” said Sun Yang, a liquefied natural gas analyst at OilChem, who estimates this happened as early as 2018. “The speed at which LNG has replaced diesel in heavy-duty trucks has been very fast.”

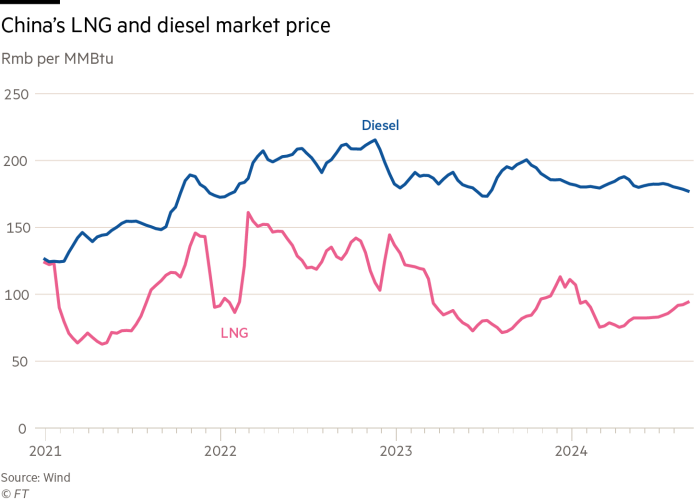

China’s diesel use is forecast to fall 4 per cent this year and will continue to slowly decline in the coming years, said analysts at investment bank CICC in September. Dong Dandan, an energy analyst at China Securities brokerage, estimated the country’s LNG truck fleet would displace about 9.2mn tonnes of diesel consumption in 2024, equivalent to 4 per cent of last year’s demand.

The switch to natural gas-powered trucks helps Beijing alleviate security concerns over imported oil. China imports about three-quarters of the resource it needs, primarily from Russia and Saudi Arabia, compared with 40 per cent for natural gas. The transition also contributes to government efforts to clean up polluted cities.

Chinese policymakers have spent the past two decades expanding domestic gasfields, as well as building pipeline networks, gas liquefaction plants and a robust network of natural gas fuelling stations.

Wang Peng, who manages a platform to buy and sell used trucks in Beijing, said diesel ones were a rare sight in western China. “They’ve been completely replaced by natural gas,” he said.

“This year, northern Chinese provinces have switched to buying natural gas heavy-duty trucks, there aren’t many diesel left,” he said. “The south is moving slower, because they don’t have as many stations to fill up.”

Natural gas trucks made up 42 per cent of China’s heavy-duty truck sales from January to August, compared with just 9 per cent in 2022, according to data from CV World, a Beijing-based commercial vehicle research provider.

Wayne Fung, a logistics expert at CMB International, said Chinese truck buyers were choosing LNG over diesel because it was cheaper, currently by 23 per cent. Chinese LNG prices have remained low due to the country’s large domestic gas production and growing volumes of pipelined gas from Russia, Turkmenistan and Myanmar.

China pays about $8 per million British thermal units for the pipelined gas, much less than for seaborne LNG imports, according to Financial Times estimates using government data.

Fung said that earlier this year the all-important “payback period” for buyers of LNG trucks to recover their investment was one year faster than for diesel, despite the roughly 25 per cent higher price tag.

Daimler’s China unit has downsized. A spokesperson said the company had taken the painful decision of letting go dozens of staff recently due to “continuous weak market demand”.

“The country is flooded with cheap natural gas from Russia,” Daimler Truck’s then-chief Martin Daum told Wall Street analysts in August. Sluggish truck sales and Daimler’s lack of a natural gas engine made it an “absolute catastrophic market”, he said.

This summer, the German company wrote off its 50 per cent stake in its Chinese joint venture with state-owned Foton Motor, which builds and sells heavy-duty trucks.

“Headquarters is far away — there is no demand for LNG engines in Europe,” said a person close to the company. “Developing one would cost millions and it’s hard to predict where the market is going.”

The growth of LNG trucking, along with the rise of electric cars, has sapped oil demand. Opec estimates that diesel accounts for a fifth to a quarter of China’s daily oil use and said demand for the fuel started falling in April.

In July, China’s diesel demand fell almost 6 per cent from a year earlier to 3.5mn barrels a day, Opec said, adding that “increasing penetration of LNG trucks and electric vehicles [were] likely to weigh on diesel and gasoline demand going forward”. It also said the country’s property crisis was weighing on demand.

Foreign experts are at odds with domestic analysts on whether China has passed peak diesel. The International Energy Agency forecast China’s diesel demand would plateau in 2025 and peak oil would occur in 2030.

But Chinese customs data shows actual crude oil imports from January to August by volume were down 3 per cent from a year earlier. Pipeline gas and LNG imports by volume rose 12 per cent per cent in the same period.

“In the past, I rarely saw an LNG truck come into my station,” said a fill-up attendant in Beijing. “There’s been an explosive increase since last year.”

You must be logged in to post a comment Login