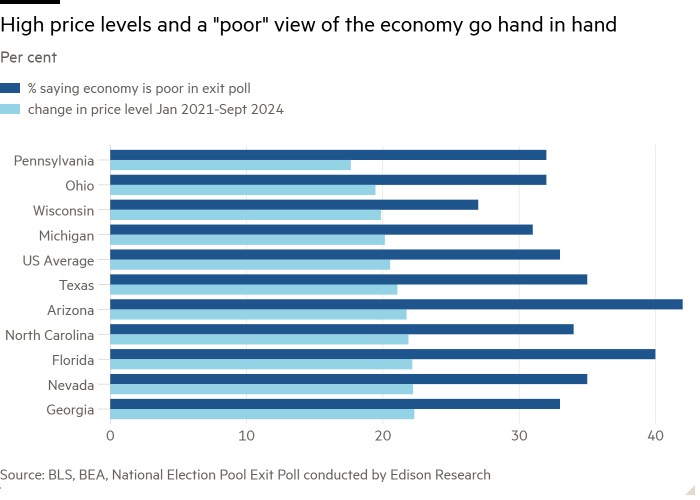

— America is continental. US GDP, unemployment and inflation data are particularly poor reflections on the economic experiences of households and businesses in different states and counties. For that, one must dig down for local and income-level statistics. — A high-growth, high-spending economy is not necessarily a sign of a healthy economy. Many Americans are spending a high proportion of their money on rent, healthcare, and food, not discretionary items — and fuelled by debt. — “Inflation falling, unemployment low=good” is too simplistic when people feel price-levels (cumulative inflation) and job security (opportunities and real wage growth) more palpably.

Frankly, none of this is new. Political fealty, culture wars, and disinformation may all play a part. But, for all those still unconvinced that people’s lived experience of the economy mattered as much as the exit polls and voxpops suggest, here are ten charts we’ve been monitoring all year.

1) A 17-22 per cent rise in the price level across swing states since January 2021 has not gone unnoticed:

2) The cheapest US products have seen the fastest increase in price level; implying lower-income households have faced even higher inflation (aka cheapflation):

3) The change in price level exceeds the change in wage level across most swing states too:

4) Debt delinquencies are also rising faster than the US average in key states:

5) A reminder of how Americans spend their money on services. The bulk of household spending is going towards non-discretionary items such as rent and healthcare:

6) Some workers have had more luck in the post-pandemic labour market than others. The visible relative performance can impact how individuals feel about whether the economy is working for them:

7) Unemployment may still be low, but those on the lowest incomes have grown most worried about losing their job since the start of the year:

8) Americans of all income levels seem to be hearing downbeat news concerning government economic policies. Outsiders may see US exceptionalism on their screens, but the realities on the ground are different, and the wealthier can shoulder it better:

9) All income groups feel worse off than they did when Biden started his term, although it is more stark for the bottom and middle thirds of earners:

10) And finally. The stock market is not the real economy. America’s asset-poor see minimal upside to soaring equity and house prices:

SAINSBURY’S has issued a major update regarding the closure of more Argos stores.

The supermarket chain, which owns Argos, plans to shut nine more standalone locations in the upcoming financial year.

1

Argos has already closed dozens of stores over the last two yearsCredit: Getty

This move is part of an ongoing strategy to transition the brand’s presence from traditional high street stores to integrated concessions within Sainsbury’s supermarkets.

Advertisement

It comes as Sainsbury’s interim results released yesterday showed sales at Argos slipped by 5% in the 28 weeks to September 14.

Sainsbury’s general merchandise and clothing sales also declined by 1.5% during this period.

Argos’ owner added: “For the full financial year we expect to open 13 Argos stores within Sainsbury’s and close nine standalone stores.”

Sainsbury’s has not yet disclosed the locations of the next round of Argos store closures.

Advertisement

The company also stated that it has not yet informed employees at the stores that will be affected.

A spokesperson for Argos told The Sun: “The transformation of our Argos store and distribution network has been progressing at pace for several years now, improving availability, convenience and service for customers.”

“As part of this, we are continuing to open new Argos stores and collection points in many of our Sainsbury’s supermarkets, enabling customers to purchase thousands of technology, home and toy products from Argos while picking up their groceries.”

The company blamed the closure of the stores on the investment required to develop and modernise the Irish part of its business as “not viable”.

HISTORY OF ARGOS

FOUNDED in 1972 by Richard Tompkins, Argos revolutionised the British retail landscape with its unique catalogue-based shopping model.

The first store opened in Canterbury, Kent and quickly expanded, becoming a household name.

Advertisement

Customers could browse the extensive Argos catalogue, fill out a purchase slip, and collect their items from the in-store collection point.

The retailer was sold to British American Tobacco Industries in 1979 for £32million before being demerged and listed on the London Stock Exchange in 1990.

In April 1998, the company was acquired by GUS plc.

Throughout the decades, Argos adapted to changing consumer habits, embracing e-commerce early on and launching its website in 1999.

Advertisement

This allowed customers to reserve items online for in-store pick-up, blending the convenience of digital shopping with the immediacy of physical retail.

By 2006, Argos became part of the Home Retail Group which was demerged from its parent GUS plc.

At the time, Home Retail Group also owned Homebase and Habitat.

In 2016, Argos, along with its Home Retail Group sister brand Habitat, was acquired by Sainsbury’s.

Advertisement

Since the acquisition, the Argos brand has been integrated into Sainsbury’s operations, significantly expanding its presence through dedicated concessions within Sainsbury’s supermarkets across the UK.

However, due to declining sales, Sainsbury’s discontinued Argos’ iconic printed catalogue in 2020.

Despite these setbacks, Argos has remained true to its roots, offering a wide range of products from toys and electronics to furniture and jewellery.

SALES UP AT SAINSBURY’S

Despite a decline in sales for both Argos and Sainsbury’s general merchandise and clothing, grocery sales surged by 5% in the 28 weeks leading up to September 14.

Advertisement

The retailer said it was boosted by strong Taste the Difference premium range sales and Nectar membership pricing.

Simon Roberts, chief executive of Sainsbury’s, said: “Our food business is going from strength to strength and we’re making the biggest market share gains in the industry, with continued strong volume growth.

“More and more customers are coming to us for their big food shop, recognising our winning combination of value, quality and service.

“As we head into the festive season, there is real energy and excitement at Sainsbury’s and Argos, and we’re expecting another strong performance.”

Advertisement

Sainsbury’s total underlying pre-tax profit was up 4.7% to £356million.

The supermarket chain is also expected to open 13 new supermarkets in the coming months.

Ten of these new stores, scheduled to open soon, were acquired from DIY retailer Homebase, while the remaining three were purchased from Co-op Food.

She also announced a reduction to the threshold at which businesses start paying NI contributions from £9,100 to £5,000.

It’s estimated that the move will raise £25billion – the equivalent of around £800 per employee for each firm.

Businesses, particularly within the hospitality sector, have warned that the increased financial burden could lead to higher operating costs, which may ultimately be passed on to consumers through price rises.

Advertisement

Mr Roberts said the NI hike would cost Sainsbury’s an extra £140million.

The Entertainer has scrapped plans to open two new stores due to the extra costs associated with the NIC hike.

On Tuesday, the chief executive of Primark’s parent company, Associated British Foods, said he felt “the weight of tax rises” in the Budget was falling on the UK high street.

The Office for Budget Responsibility (OBR) also said last week that the Treasury’s sharp increase in spending would lead to higher inflation in the coming months.

INFLATION is a measure of the cost of living. It looks at how much the price of goods, such as food or televisions, and services, such as haircuts or train tickets, has changed over time.

Usually people measure inflation by comparing the cost of things today with how much they cost a year ago. The average increase in prices is known as the inflation rate.

Advertisement

The government sets an inflation target of 2%.

If inflation is too high or it moves around a lot, the Bank of England says it is hard for businesses to set the right prices and for people to plan their spending.

High inflation rates also means people are having to spend more, while savings are likely to be eroded as the cost of goods is more than the interest we’re earning.

Low inflation, on the other hand, means lower prices and a greater likelihood of interest rates on savings beating the inflation rate.

Advertisement

But if inflation is too low some people may put off spending because they expect prices to fall. And if everybody reduced their spending then companies could fail and people might lose their jobs.

Stockholm-based Truecaller, known for its apps that help you verify and identify contacts, announced the appointment of Rishit Jhunjhunwala as its group CEO, effective January 9, 2025. Jhunjhunwala is the current Chief Product Officer and Managing Director of India operations.

The posting comes after CEO Alan Mamedi and Chief Strategy Officer Nami Zarringhalam announced their decision to step down from their operational roles. The Stockholm exchange-listed company also rescheduled the publication of its interim report following the changes.

“I am very excited as well as honoured that the board along with Alan and Nami have appointed me as the CEO… Having worked closely with Alan and Nami since 2015, I know these are big shoes to fill, but I amconfident to continue tirelessly working towards getting us closer to our mission to make future communication more safe and secure,” said Jhunjhunwala, the incoming CEO of Truecaller.

India-born Swedish national

Rishit Jhunjhulwala was born and raised in India. He moved to Sweden, joining Trucaller in 2015 and stayed till 2022. In between, he took on the role of the MD of Truecaller India and has held it since 2021. He is now a Swedish citizen.

Jhunjhulwala currently looks after two of Truecaller’s major revenue-making arms, advertising and “Truecaller for Business”.

Before joining Truecaller, Jhunjhulwala helped in founding Cloudmagic Inc, the Bengaluru and Florida-based company that operates Newton Mail. He also served as the Vice President of Strategic Programs at then-July Systems, which later got injected into the cloud platform, Cisco Spaces, after its acquisition in 2018. Back in 2000, the incoming Truecaller CEO also co-founded Verity Technologies, a valued-added-service startup in the Indian telecommunications space.

This article is an on-site version of our Inside Politics newsletter. Subscribers can sign up here to get the newsletter delivered every weekday. If you’re not a subscriber, you can still receive the newsletter free for 30 days

Good morning. Westminster is still trying to digest the news of Donald Trump’s victory in the US election. Keir Starmer has issued a “hearty” congratulations to the president-elect, but there are multiple fronts where the incoming Washington administration will be at odds with London: here’s our guide to those areas of friction.

One of the casualties of Trump’s return is likely to be the Democrats’ “Inflation Reduction Act”, a gargantuan piece of legislation designed to spark a gold rush into American cleantech.

Advertisement

“My plan will terminate the Green New Deal, which I call the Green New Scam. Greatest scam in history, probably,” Trump said in September. “We will rescind all unspent funds under the misnamed Inflation Reduction Act.”

Closer to home I wondered what happened to the “Green Prosperity Plan”, which was meant to be Labour party’s own version of this.

But since Keir Starmer won the general election in July, the phrase has fallen into abeyance.

That’s not to say that Labour has dropped the green energy chat. Far from it.

Advertisement

The drive to decarbonise the electricity system by 2030 is one of the defining missions of the new government. (Clean energy was mentioned no fewer than eight times in the King’s Speech.)

But I’m curious — in a nerdy way — about what happened to the language and the mechanics of the thing that used to be the Green Prosperity Plan.

I’ve gone back through the big speeches from the Labour conference in September to see whether Starmer, Rachel Reeves or Ed Miliband used the phrase. They didn’t.

So what happened?

Advertisement

Until February, the GPP had an eye-watering price tag of £28bn a year, all funded by borrowing. Rewind to last winter and a genuine scrap was taking place inside the shadow cabinet about the size of the green package.

There were those — somewhat to the left in Labour terms — such as Miliband, Louise Haigh and Sue Gray (remember her) who wanted to keep it.

And then there were the likes of Rachel Reeves and Pat McFadden and Morgan McSweeney (somewhat to the right in Labour terms) who wanted to rein in the scale and scope of the GPP to avoid lethal headlines and Tory attacks.

Some shadow ministers wondered why the borrowing was only for green infrastructure rather than for new schools or hospitals or prisons.

Advertisement

Throughout that long three-month period, the Labour press machine dishonestly insisted no such debate was going on.

Starmer prevaricated for weeks on end until he made his mind up.

“As conditions change, you adjust your position,” Starmer told the hacks. Interest rates were zero when the policy was first cooked up. Now they were close to 5 per cent.

Advertisement

And so a scheme which had been similar on scale in GDP/head terms to the huge IRA of Joe Biden (remember him) was slashed to barely a sixth of its original size.

Three existing elements of the plan survived.

There would still be a state-owned energy company called GB Energy, costing a one-off £8.3bn over a five-year parliament, to co-invest in renewable energy schemes.

There would still be a £7.3bn “national wealth fund” to invest in the decarbonisation of heavy industry.

There would still be a national insulation scheme called the “Warm Homes Plan”, but it would be slashed from £6bn a year to just over £1.3bn a year.

Despite this humiliating U-turn, the Green Prosperity Plan continued to be a major Labour slogan in the run-up to the July election. It was still there in the manifesto document: “At the heart of our approach will be our Green Prosperity Plan”.

And then the phrase disappeared from use.

Advertisement

Green energy, energy independence, clean energy, carbon capture are still a major part of the new government’s political narrative. Starmer has staked much of his reputation on hitting the 2030 electricity decarbonisation target despite industry thinking it’s stretching to the point of being virtually impossible.

So, to some extent, the ditching of the specific phrase “Green Prosperity Plan” is a question of semantics.

Ask the Labour party what happened and they will say the language changed in favour of a new, more jazzy phrase: “Clean Energy Superpower”.

And yes, that line was used in Miliband’s conference speech and by the prime minister elsewhere. It was Miliband’s team which came up with the “superpower” language because they thought it sounded more pro-growth and more pro-investment.

Advertisement

It also played into the feedback from polling firms that “energy independence” is a line which gets traction with the public.

A Trump retreat from the green agenda could — if anything — give impetus to Europe’s attempts to attract low-carbon investment.

So far so clear. But what has happened in recent weeks to the three constituent parts of what used to be the GPP?

Great British Energy

Ministers still insist that GB Energy will get £8bn of cash over the current five-year parliament, mostly to co-invest in private renewable energy schemes.

Advertisement

But the new state-owned energy company will receive just £100mn in funding for renewables projects — and £25mn of seed capital to establish the company — in the first two years of this parliament, according to last week’s Budget.

Labour says that the details of more funding will follow in next year’s multiyear spending review. But the Association for Renewable Energy and Clean Technology said it was “disappointed” there wasn’t more initial funding.

National Wealth Fund

The National Wealth Fund was meant to be a new, standalone body which would help heavy industry decarbonise.

That’s not what happened. Instead Labour has simply rebranded the UK Infrastructure Bank (set up by Rishi Sunak three years ago) as the National Wealth Fund and promised it some extra cash.

(That is roughly a doubling of the £6bn the previous Conservative administration had hoped they would spend over the same timeframe.)

One final aside

The original premise of the prosperity plan was — you’ll remember — to borrow £28bn a year for low-carbon schemes.

Advertisement

Last week, Reeves unveiled a big rise in taxes, but also a jump in borrowing of £32bn a year, equal to 1 per cent of GDP.

That extra borrowing for capital expenditure will now be distributed right across government priorities rather than the net zero transition.

And yet that figure seems too close to be a total coincidence.

Now try this

For some of us, Wednesday was excruciating.

Advertisement

Yes, I tore a muscle playing 5-a-side football and am now housebound. Soothing me through the discomfort is Patterns in Repeat, the beautiful new album by singer-songwriter Laura Marling, who did a superb string of gigs at Hackney Church last week. Our pop critic gave it 4/5 in this review.

Have a lovely weekend.

Top stories today

Recommended newsletters for you

White House Watch — Your essential guide to what the 2024 election means for Washington and the world. Sign up here

One Must-Read — Remarkable journalism you won’t want to miss. Sign up here

After many years of the regulatory equivalent of a Gaelic shrug towards the protection market, the Financial Conduct Authority has announced a forthcoming study into the sector taking in many areas, perhaps most notably, the three Cs: commission, competition and charging.

Understandably, this has set many boardrooms a flutter, as the market’s biggest and best advisers, distributors and providers begin to consider the impact of the study and its findings on their business model.

There will be some who are fearful. Any action from the regulator tends to cause worry. Some are thankful, having been calling for an increase in engagement in protection from the regulator for some time.

There are always processes that can be done better, to deliver better products, better services and better outcomes to customers

There are others, like me, who are hopeful. Hopeful that this study will once and for all shine the light on protection that I, and many others like me, think it deserves.

Name a perfectly functioning market and I’ll prepare to be astounded. Nowhere across financial services, retail and beyond will you find a market perfectly in sync with its customers or internal market stakeholders.

Advertisement

There are always processes that can be done better, to deliver better products, better services and better outcomes to customers.

The fast-food market could easily reduce salt, sugar and fat in its foods and maintain its revenues and standing. Indeed, the sugar tax on soft drinks has proven it possible. But it is yet far from common practice.

The UK is one of – if not the – most price-competitive market in the world. We offer cover at a low price – some might say too low

Closer to home, the general insurance market could, despite regulatory intervention in recent years, ensure all its products deliver value for money on an ongoing basis.

Protection, too, has aspects that could be changed to improve the market and the outcomes it delivers customers. Products could be simpler to understand and deploy to underserved markets. Cover could be more in keeping with modern changing lives – able to flex according to circumstances. Processes at application and claim could be improved from those which, today, are often still legacy; often manual and sometimes opaque.

Advertisement

However, there is masses to celebrate, too. The UK is one of – if not the – most price-competitive market in the world. We offer cover at a low price – some might say too low. We are also continually seeing providers entering new channels and new product lines – helping drive more choice.

This is the growth we need. This is the growth a financially resilient society needs

We have come a long way on process simplicity, too. Yes, we have more to do but insurers, distributors and advisers now have better, more streamlined processes to serve their protection clients – from sourcing the right product at the right premium to accessing GP helplines from the growing set of value-added benefits, now included as standard within most policies.

This, in itself, should be celebrated – providers have made the important step to offer more holistic, ‘always-on’ policies capable of delivering value even when their core purpose (to cover a claim) isn’t required.

Let’s not lose sight of these facts and continue to share them, both together and in public. A connected market is a better market. A positive discourse is better than a negative discourse. Let’s celebrate the things we do well, in private and in public.

Advertisement

As we begin to predict what the study will focus on and what the outcomes for the market will be, I remain hopeful. Ours is a market which performs an important role in society, a role we should ensure we and those who engage with it always appreciate.

Like most markets, there are things we could do better. Many of these things would help us, not necessarily to do more for our customers but to do the same for more customers. This is the growth we need. This is the growth a financially resilient society needs.

Let’s celebrate protection.

Paul Yates is product strategy director at iPipeline

The biggest public-sector lender in India, SBI, announced its second-quarter results on Friday afternoon, triggering a slide in the stock price despite trading in the green in the morning trade.

For the quarter, State Bank of India (SBI) net profit jumped 27.9 per cent year-on-year to Rs 18,311 crore, beating market estimates. SBI also recorded a credit growth of 14.93 per cent year-on-year. Consolidated net profit saw a yearly improvement of 23 per cent to reach Rs 19,782 crore.

Despite beating the market outlook, shares slipped post the earnings announcement by at least 2.3 per cent in afternoon trade. SBI shares had traded higher in morning trade on Friday ahead of the quarterly results, hitting a high of Rs 863.50.

Investors were also looking at the asset quality, and the gross Non-Performing Assets (NPA) ratio at the quarter-end stood at 2.13 per cent. Compared to the same period last year, this was an improvement of 42 basis points. Provisions for bad assets almost doubled to Rs 3,631 crore.

For banks, a lower NPA is better. A higher NPA ratio means that the bank has too many non-functioning loans. SBI’s net NPA for Q2 was 0.53 per cent compared to 0.57 per cent from the previous quarter.

On Thursday, the State Bank of India also announced the launch of an innovation hub in Singapore in partnership with the local collaborative innovation platform for financial institutions, APIX.

After many years of the regulatory equivalent of a Gaelic shrug towards the protection market, the Financial Conduct Authority has announced a

After many years of the regulatory equivalent of a Gaelic shrug towards the protection market, the Financial Conduct Authority has announced a

You must be logged in to post a comment Login