Simply sign up to the UK inflation myFT Digest — delivered directly to your inbox.

UK inflation fell more than expected to a three-year low of 1.7 per cent in September, prompting traders to increase bets on further rate cuts from the Bank of England this year.

Wednesday’s data release by the Office for National Statistics shows that inflation has come back under the BoE’s 2 per cent target for the first time since April 2021.

Advertisement

The annual increase in consumer prices is less than the 1.9 per cent forecast in a Reuters survey of economists and compares with August’s figure of 2.2 per cent. The retreat was driven by lower airfares and petrol prices.

The numbers will come as a boost to Sir Keir Starmer’s government just two weeks before what promises to be a tough Budget containing steep tax rises. Chancellor Rachel Reeves is looking to close a funding shortfall of £40bn, according to officials close to the Budget process.

The numbers led investors to increase bets that the BoE would lower interest rates for a second time in its November meeting following its quarter-point reduction in August, and then make an additional cut in December.

Traders had previously put the chance of two quarter-point rate cuts by the end of the year at roughly 50 per cent, according to levels implied in swaps markets. That increased to 75 per cent after the inflation release. The pound was down 0.6 per cent against the dollar at $1.30 on Wednesday.

A November cut already looked “nailed on before today’s release”, said Paul Dales at Capital Economics. “The chances of that being immediately followed by another quarter-point cut at the following meeting in December has just gone up,” he added.

Governor Andrew Bailey said recently that rate-setters could be “a bit more aggressive” in lowering borrowing costs if inflation continued to fall. The comments were seen by investors as a signal that the BoE was poised to cut rates at both its November and December meetings.

Core inflation was 3.2 per cent, lower than economists’ expectations of 3.4 per cent, while the rate of services inflation fell from 5.6 per cent to 4.9 per cent, driven by lower airfare price rises.

Services inflation is seen by the central bank as a key gauge of underlying price pressures. The 4.9 per cent reading was well below the 5.5 per cent forecast published by the BoE when it last released a full assessment of the economy in August.

Advertisement

It chimes with separate ONS data this week showing that UK wage growth fell to 4.9 per cent in the three months to August, down from 5.1 per cent in the three months to July.

The decline in services inflation is “big news” for the central bank, said James Smith, UK economist at ING. “We think the Bank of England can pick up the pace of cuts beyond November.”

An acceleration in the rate-cutting cycle is possible even though headline inflation is likely to bounce back towards 2.5 per cent later this year as the downward drag from lower energy prices fades, Smith added.

Advertisement

A key input into the BoE’s December meeting will be the shape of Reeves’s October 30 Budget and the impact of her attempts to get debt under control.

Darren Jones, the chief secretary to the Treasury, said Wednesday’s inflation figures would be “welcome news for millions of families”, adding that “there is still more to do to protect working people”.

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Elon Musk appears to have won a contest with Indian telecom tycoons Mukesh Ambani and Sunil Bharti Mittal over the way satellite spectrum should be awarded, as the billionaires battle over the introduction of space-fed internet to the world’s most populous country.

Ambani, Asia’s richest man and chair of oil-to-digital services conglomerate Reliance Industries, along with Mittal’s Bharti Airtel, have been trying to persuade India’s government to auction satellite spectrum, in line with the usual competitive method in the mobile market they dominate, rather than just allocate it.

Advertisement

Musk, chief executive of SpaceX and owner of the Starlink satellite broadband service, took to his social media site X this week to say that any such moves by India would be “unprecedented, as this spectrum was long designated by the [International Telecommunication Union] as shared spectrum for satellites”. India is a member of the ITU.

Soon after, Mittal voiced his support for the auction process. Addressing a conference in New Delhi, he specifically told Prime Minister Narendra Modi, who sat in the audience, that satellite companies serving urban areas “need to pay telecom licences like everyone else”.

Ambani’s Reliance had written to the telecoms regulator and the government last week, accusing it of pre-emptively concluding that allocation was the way forward, according to a letter seen by the Financial Times and a person familiar with the matter.

But on Tuesday, Indian communications minister Jyotiraditya Scindia said there were no plans afoot to auction space spectrum. “Much appreciated!” Musk posted on X in response. “We will do our best to serve the people of India with Starlink.”

Advertisement

This year, the Financial Times reported that Mittal and Ambani were frontrunners to introduce satellite internet services ahead of Musk’s Starlink, which has yet to receive licences. The Indian businessmen enjoy a near duopoly in telecoms domestically and EY-Parthenon estimates that space broadband is a potential $1bn annual revenue market for the country.

“We have deep pockets and we can spend money to buy extra spectrum . . . this will keep small players away,” said a person close to Reliance. “If it is not auction, and allocation, because it’s a new technology, a lot of unwanted players might enter.”

India’s parliament late last year enacted a law that allowed allocation of satellite-based spectrum, instead of the country’s traditional auction method. Last month, the telecoms regulator requested feedback from industry players, with a deadline set for later in October.

Bharti Airtel, which plans to launch satellite internet in a joint venture with Anglo-French group Eutelsat OneWeb, said in a statement that operators serving urban areas and retail customers should go through the auction process.

Advertisement

It’s more about ensuring that the telecom industry remains in control of the local players rather than foreigners coming in and dictating their agenda

A person close to the company said only services reaching currently unserved communities should be assigned spectrum, to allow for a “level playing field” after Indian operators invested “billions of dollars” in terrestrial connections.

“The local guys are arguing there should be uniformity in the rules,” said Vivekanand Subbaraman, technology analyst at Ambit Capital in Mumbai. “Principally, they want these companies to be subject to the same licensing norms, the same spectrum norms.”

However, another industry expert described the tussle as an “ego battle”.

“It’s more about ensuring that the telecom industry remains in control of the local players rather than foreigners coming in and dictating their agenda,” they said. “I can’t think of any other explanation, it’s not like there’s a scarcity of spectrum, it’s abundant.”

Advertisement

A simple assignment of spectrum may hand Musk’s company, the largest and most successful of its kind, a “first-mover advantage”, while an auction process would allow Indian players time to get their products market-ready, said the person close to Reliance.

Musk told Modi last year that he wanted to bring Starlink, which operates more than 6,000 low-orbit satellites, to India to connect remote communities.

Musk also has his eye on the long-term potential of India as a location for a Tesla plant, despite cancelling a trip to New Delhi earlier this year to prioritise talks with and focus on its Asian rival China.

Reliance, along with India’s space and telecoms regulators, did not respond to requests for comment.

I am always excited to see what the Financial Conduct Authority considers to be good and bad practice with respect to the price and value outcome under Consumer Duty.

With the latest update published last month, my quivering anticipation has proved to be well founded.

Although the work carried out by the regulator focuses on cash accounts (including platforms) and GAP insurance, there are clear messages for firms in other financial services sectors.

Much of the dark art of compliance is interpreting regulatory missives not directly related to one’s own sector, and there are elements of this publication that are plainly relevant outside its area of primary focus.

Much of the dark art of compliance is interpreting regulatory missives not directly related to one’s own sector

The first key signal is the very positive approach the FCA is taking. There is clear recognition that Consumer Duty is a developing beast, not something where everything could be perfect on day one. There have been so many examples of poor practice in the industry over a long period of time that the culture that led to those incidents cannot be turned on its head in a matter of a few months. That’s just unrealistic.

Advertisement

I am also greatly encouraged by the FCA’s use of words such as ‘appropriate’ and ‘proportionate’ and by its acknowledgement of the need to make continual improvements. Any firm that views the implementation of Consumer Duty as a one-off exercise will find itself in regulatory hot water sooner or later.

Proportionality is hard to define but it seems a small firm with a limited range of services will not be expected to take the same steps a financial behemoth will need to undertake – that would be disastrous for any new entrant and all markets need such firms to innovate and shake up established norms.

Any firm that views the implementation of Consumer Duty as a one-off exercise will find itself in regulatory hot water sooner or later

But what of those messages?

Well, the paper starts with a clear statement that the price and value outcome should not be considered in isolation, so we are not simply involved in a race to the bottom in terms of price. It is of little overall benefit to clients if they get a cheap product they don’t understand, or if they receive little or no support and poor service.

Advertisement

Nevertheless, it does seem the FCA has focused initially on price, because the price point must be the very foundation of value.

The other outcomes remain important, but it is quite impossible for the overall objectives of Consumer Duty to be met if prices are set unjustifiably high. That is always going to represent a fundamental misalignment of interests. While all businesses must make profits, those with the best chance of long-term success are the ones that do so fairly. From that stems a clear correlation between the best long-term interest of business and those of their clients.

Surely, good practice is to set charges which break the mould, recognise economies of scale and really focus on client interests?

As for specific examples, the first one that leaps out and that has bedevilled the industry for a very long time is unnecessarily complex pricing structures. The regulator even suggests some of these may have been established with the intention to confuse clients. I’d be surprised if that situation is deemed acceptable for any length of time.

The regulator is at pains to stress its role is not to set prices. However, there is evidence of price clustering around a comfort zone (as has been the case for many years in retail funds).

Advertisement

The FCA’s director of competition Graham Reynolds was recently quoted as saying firms should benchmark their prices against an appropriate peer group, which, to me, doesn’t do anything to encourage competition.

While price isn’t everything, it is very much the starting point

Surely, good practice is to set charges which break the mould, which recognise economies of scale, and which really do focus on client interests? There are myriad examples in other sectors of companies which have done just that, and which have thrived as a result. Look at the budget airlines, which democratised air transport a generation ago.

There may be some compromises to be made, but provided those are understood at the outset, many will welcome price savings.

While price isn’t everything, it is very much the starting point. There are plenty of good reasons why more expensive products or services may be chosen, but any adviser doing so must always be clear about why such a choice is in the best interest of their clients.

Advertisement

David Ogden is head of compliance at Sparrows Capital

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Woodside Energy, Australia’s largest oil and gas developer, will delist its shares from the London Stock Exchange next month, in the latest blow to the UK market’s status as a natural resources hub.

Perth-based Woodside listed shares in the UK when it merged with BHP’s oil and gas assets in 2022, to allow British shareholders in the mining company to maintain their exposure to the assets.

Advertisement

Yet the company, which has a market capitalisation of A$47bn (£24bn), said on Wednesday that the cost of maintaining the secondary listing was no longer justified.

Meg O’Neill, chief executive of Woodside, told the Financial Times that the UK listing accounted for only 1 per cent of Woodside’s issued share capital, and that most of its large UK-based institutional investors opted to hold its ASX-listed stock.

The decision comes after BHP moved its primary stock market listing to Australia in 2022 as part of a plan to unify its dual corporate structure, depriving the FTSE 100 index of one of its biggest constituents. The shift was announced the previous year, when the miner unveiled the deal to sell its petroleum business to Woodside.

London fell behind New York, Toronto and Sydney this year as a global venue for mining company listings, with investors warning it was in danger of being “sidelined” by a sector it once dominated if a few major groups headed overseas.

Advertisement

Rival Rio Tinto, which has a dual listing with shares on both the LSE and ASX, has also come under pressure from an activist investor to unify its share structure on the Australian exchange, but has argued against the move.

Woodside shares boomed after the merger with BHP as the price of liquefied natural gas soared following Russia’s invasion of Ukraine. Its UK stock has fallen back by about 30 per cent in the past 12 months and the company has looked for other deals to boost its growth profile. It held talks with local rival Santos before acquiring two US assets this year.

The UK-listed Woodside shares have been slightly weaker than the ASX stock over the past year. The former are expected to stop trading on November 19.

Advertisement

Australian property listings company REA planned to launch a secondary listing in London as part of its cash-and-shares offer to acquire UK rival Rightmove earlier this year but could not strike a deal with its target.

Woodside raised its production forecast for the year on Wednesday and lowered its guidance for capital expenditure spending, which pushed its revenue for the third quarter above analyst expectations.

O’Neill said that while the oil price had been under pressure over concerns about Chinese demand, the LNG price had been stronger heading into winter in Europe and Asia. “The market is finely balanced,” she said.

The founder of MoneySavingExpert.com said: “While ‘boosting your State Pension’ doesn’t sound sexy, this is about big money, and we’ve had huge successes.

“It’s the most lucrative thing many under age 73 can do, some gain £10,000s.

“The deadline’s half a year away, but the process ain’t quick, so start now.”

Martin added that for every £825 or less you pay to buy NI years, many stand to gain over £5,400.

Advertisement

Typically, strict time limits apply to buying back these years.

How to track down lost pensions worth £1,000s

However, when the new state pension was introduced in 2016, the rules were relaxed to aid the transition.

This relaxation was initially set to end in April 2023 but has been extended until April 2025.

It means that from May 2025, you will only be able to buy back six tax years, starting from 2019.

Advertisement

Although several months remain until this deadline, Martin has urged his readers to “just get on with this and do it now.”

Before considering purchasing any missing years, checking if you can obtain some years for free with NI credits is essential.

We have outlined the process you need to follow to boost your state pension below.

What is National Insurance?

Advertisement

NATIONAL Insurance is a tax on your earnings, or profits if you’re self-employed.

These contributions make you eligible for things like the state pension and certain benefits.

You’ll usually pay National Insurance Contributions (NICs) when you’re over the age of 16 and earning a certain amount.

For example, if you earn £1,000 a week, you pay nothing on the first £242.

Advertisement

Earn over that and you pay 10% on the next £725 – so £72.50. Then you pay 2%o on the rest, so £33, which works out as 66p.

For the self-employed rates are slightly different.

You can also get something known as National Insurance in some circumstances when you’re not working, for example when you have kids and claim certain benefits.

NICs are usually taken automatically by your employer and paid to HMRC, so you don’t need to do anything.

Advertisement

You can see how much NICs you pay on your wage slip.

Anyone working for themselves usually has to pay NICs themselves when completing a self-assessment tax return.

CHECK YOUR YEARS

If you think you’re missing National Insurance years, the first thing to do is check you State Pension forecast.

You can check this as well as the State Pension age through the government’s new ‘Check your State Pension’ tool online at www.gov.uk/check-state-pension.

Advertisement

The tool is also available through the HMRC app, which you can download free on the Apple App Store and Google Play Store.

You’ll need to log in using your Personal Tax Account login details. If you don’t already have an online HMRC account, you can register at gov.uk.

It shows you how much your state pension could increase by and what NI years you’ll need to buy to achieve this.

You’ll then be able to pay for these missing years securely online, without having to call up separately.

Advertisement

You’ll need to pay for these in full – you can’t pay in instalments.

You can’t use the online service if you’re already getting your State Pension.

Instead, you’ll need to call the Pension Service on 0800 731 0469.

However, before you commit to buying new National Insurance years it’s vital you check whether you were entitled to free credits at any point.

Advertisement

CHECK FOR NATIONAL INSURANCE CREDITS

Before making a voluntary contribution, it is important to check if the gaps in your contributions can be filled with free NI credits.

For example, those on certain benefits should qualify for Class 1 credits.

This includes parents with active claims for child benefit.

Advertisement

You can check the full list of people eligible to claim credits by visiting www.gov.uk/national-insurance-credits/eligibility.

It explains the circumstances where you’ll need to claim and when you’ll get it automatically.

TOP UP YOUR NATIONAL INSURANCE YEARS

In some cases, buying back missing years can be really valuable.

But earning back the years isn’t free, so your voluntary contributions come at a price.

Advertisement

If you fill gaps between 2006/07 and 2015/16, you’ll pay the 2022/23 rates for contributions.

It is worth £15.85 a week, which means it costs £824.20 to buy one year of contributions.

As the state pension was £185.15 per week in 2022/23, this boost would add £5.29 per week or around £275 per year.

Although you’d have to pay £8,242 (10 lots of £824.20), the annual state pension boost would be around £2,750.

Advertisement

Someone who was retired for 20 years would get back around £55,000 in total (before tax).

Anyone under 73 can make voluntary pension contributions, as it’s assumed everyone under this age will claim the new state pension.

If you’re below the state pension age, you can check your state pension forecast by visiting www.gov.uk/check-state-pension to determine if you’ll benefit from paying voluntary contributions.

You can also contact the Future Pension Centre by calling 0800 731 0175.

Advertisement

If you’ve reached state pension age, contact the Pension Service to find out if you’ll benefit from voluntary contributions.

You can contact this service in several different ways by visiting www.gov.uk/contact-pension-service.

You can usually pay voluntary contributions for the past six years.

For example, you have until April 5, 2030, to compensate for gaps in the tax year 2023 to 2024.

The deadline has been extended for making voluntary contributions for the tax years 2016 to 2017 or 2017 to 2018.

You now have until April 5, 2025, to pay.

Find out how to pay for your contributions by visiting www.gov.uk/pay-voluntary-class-3-national-insurance.

Advertisement

How does the State Pension work?

AT the moment the current State Pension is paid to both men and women from age 66 – but it’s due to rise to 67 by 2028 and 68 by 2046.

The state pension is a recurring payment from the government most Brits start getting when they reach State Pension age.

But not everyone gets the same amount, and you are awarded depending on your National Insurance record.

Advertisement

For most pensioners, it forms only part of their retirement income, as they could have other pots from a workplace pension, earning and savings.

The new state pension is based on people’s National Insurance records.

Workers must have 35 qualifying years of National Insurance to get the maximum amount of the new state pension.

You earn National Insurance qualifying years through work, or by getting credits, for instance when you are looking after children and claiming child benefit.

Advertisement

If you have gaps, you can top up your record by paying in voluntary National Insurance contributions.

To get the old, full basic state pension, you will need 30 years of contributions or credits.

You will need at least 10 years on your NI record to get any state pension.

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

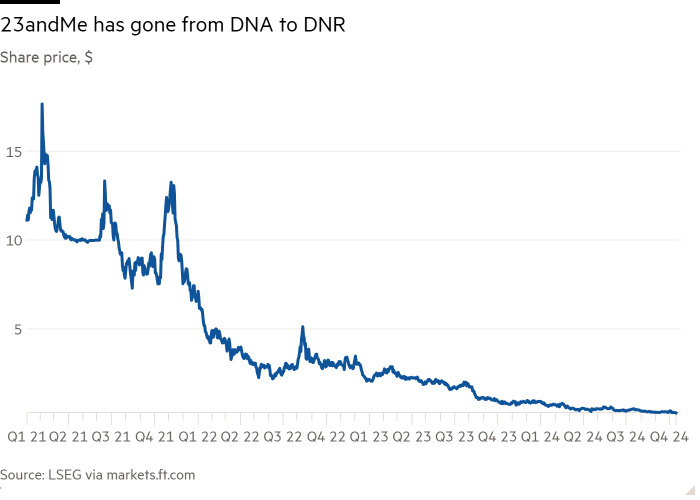

Even before its birth as a public company, 23andMe never really had a chance. The DNA-testing firm’s shares have slid, revenue has disappointed and profit has not materialised. Co-founder Anne Wojcicki now wants to take 23andMe private, at a meagre price. This misfortune is the result of both nature and nurture.

As business models go, 23andMe was stunted from the start. Customers pay to spit into a tube, mail it back and learn what is written in their genes. Results can range from discovery of genes associated with serious medical conditions to more frivolous revelations, such as the genetic propensity to hate other people’s eating noises.

Advertisement

The problem is that after that big reveal, there is not much scope for recurring business. Back when 23andMe’s backers exploited frothy market conditions to merge with a special purpose acquisition company, the company forecast $400mn of revenue by 2024, boosted by activities such as drug development. It made just $220mn.

Wojcicki is to blame, though a wider slide in valuations of experimental drugmakers didn’t help. The godparents share some responsibility: Citigroup and the late Credit Suisse brought 23andMe to market in 2021. Citi’s analyst declared the $10 stock to be worth $14, only for the share price to halve in just over six months.

Even an injection of Richard Branson’s DNA didn’t help. The Virgin mogul set up the Spac that acquired 23andMe and handed it a public listing. His involvement in other blank-cheque firms has flopped too. An investment in eco-disinfectant maker Grove Collaborative has shrunk by 97 per cent. Of the two space companies Branson sold to Spacs, Virgin Galactic’s operations are on hold and Virgin Orbit went bankrupt.

The best hope for 23andMe is a takeover by Wojcicki, who proposed buying the portion of the company she doesn’t own for 40 cents a share in July. That was rejected by independent directors, who subsequently resigned. With the stock trading at 27 cents, it no longer looks so mean.

Still, it’s not clear what Wojcicki would get. No fewer than 13 US states — covering one-third of the population — have passed laws forcing companies to get consent from genetic data providers before a transfer to a new owner, say privacy advocates at the Electronic Frontier Foundation. If many say no, the value of 23andMe’s main asset may melt away before the ink is dry on a deal.

Advertisement

That’s more reason for investors to take what they can get and learn from their mistakes — namely, piling into a fragile, unproven business model in a hyped-up market. Genetic testing makes it possible to anticipate future challenges from the get-go. Backers of 23andMe did nothing of the sort.

You must be logged in to post a comment Login