Business

UK Treasury to slash overseas aid in Budget as asylum seeker costs rise

International development organisations warn country’s contribution could slump to its lowest level in 17 years

CryptoCurrency

3 Heavily Shorted Stocks That Are Down More Than 75% Since 2021. Can They Turn Things Around?

Investing in struggling stocks that are also heavily shorted can be an incredibly risky move. But if these types of stocks are able to turn things around and prove their doubters wrong, the upside can also be significant. It’s not a suitable investment strategy for most investors, but if you have a high risk tolerance, there are three potential contrarian plays to consider.

Medical Properties Trust (NYSE: MPW), Beyond Meat (NASDAQ: BYND), and Plug Power (NASDAQ: PLUG) are three beaten-down stocks that many short-sellers are betting will continue to struggle. Below, I’ll look at just how heavily shorted these stocks are, what has to happen for them to turn things around, and whether they are worth potentially investing in today.

Medical Properties Trust: 50% short interest

A real estate investment trust (REIT) can sometimes be an attractive investment for its recurring dividend income and stability. But a REIT is only as stable as its tenants. And Medical Properties Trust is a REIT which has had problems with key tenants in the past, including Steward Health, which filed for bankruptcy protection earlier this year.

The turbulence in Medical Properties’ earnings has resulted in a disastrous performance for the stock, which is down a whopping 79% since 2021. And while the REIT has distanced itself from Steward Health and is relying on new tenants, short interest remains incredibly high at around 50% of the stock’s float.

For Medical Properties to turn things around, it needs to prove that it can get back to generating positive earnings numbers and that its new tenants are much safer. The healthcare REIT has incurred a net loss for three consecutive quarters. It’ll take time for Medical Properties to demonstrate it’s a safer option for investors, and with the company cutting its dividend twice since last year, it won’t be easy for many investors to trust this stock.

With interest rates potentially coming down further next year, I think there could be a contrarian play here as REITs may become more attractive investments amid lower rates. And with so much bearishness priced into its valuation, Medical Properties may not have to perform too well to impress the market these days. This is a highly risky stock, but there are reasons to consider taking a chance on it. The safe option, however, would be to wait at least a couple of quarters to see if Medical Properties is able to find some stability in its earnings.

Beyond Meat: 40% short interest

Another heavily shorted stock is Beyond Meat. The fake meat company hasn’t been doing well for multiple reasons. Not only has demand been unimpressive, but its gross margins are also often negative, which makes it difficult to see a path to profitability for the business anytime soon. With short interest as high as 40%, investors clearly aren’t believing the hype around Beyond Meat’s plant-based foods. Since 2021, Beyond Meat has lost a staggering 95% of its value; it’s nearly impossible for the stock to have performed worse since then.

In the trailing 12 months, Beyond Meat’s net loss of $314.4 million is nearly as high as its revenue of $317.8 million. Unfortunately, there’s no easy way to see a turnaround for Beyond Meat. It needs a plant-based product that is in high demand and for which it can charge a high enough price to significantly bolster its margins. And until that happens, it’s difficult to even see a path for a turnaround.

This food stock may be too risky an investment, even for contrarian investors.

Plug Power: 29% short interest

Shares of Plug Power are also down more than 90% since 2021 as the hype surrounding hydrogen energy has crumbled drastically in recent years. The company has reported massive losses, which make Beyond Meat’s numbers almost look decent. Over the past four quarters, Plug has incurred a net loss of nearly $1.5 billion on sales of $684.5 million. And like Beyond Meat, it regularly reports a negative gross margin, which is a huge red flag for investors. Short interest in Plug Power is just under 30%.

If you’re a believer in hydrogen energy, you might be tempted to take a chance on Plug Power. But the risk is that the company may not be around even if hydrogen energy takes off and becomes the preferred power solution in the future. While Plug Power may boast about a leadership position in the hydrogen industry, that hasn’t amounted to a strong financial position for the business, and that’s what’s arguably more important for investors.

Plug Power reported $285.2 million cash (including restricted cash) as of the end of June. And for a company that has burned through $422.5 million in just the past six months from its day-to-day operating activities, the problem is clear: The business needs to drastically slow its cash burn and cut expenses. Regardless of the potential in hydrogen, it’ll be all for naught if Plug Power continues to accumulate these types of losses. That’s why I think it may be the riskiest stock on this list, and the one which may have the hardest path to turning things around.

Without clear evidence of a significant improvement in its financials, this is a stock that you’ll probably want to steer clear of.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,049!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,847!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $378,583!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 14, 2024

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Beyond Meat. The Motley Fool has a disclosure policy.

3 Heavily Shorted Stocks That Are Down More Than 75% Since 2021. Can They Turn Things Around? was originally published by The Motley Fool

By Georgina McCartney

MIDLAND, Texas (Reuters) – A new pipeline carrying shale natural gas from west Texas toward export hubs on the U.S. Gulf Coast has eased constraints that crashed local prices this year, and will help pave the way for higher U.S. oil production, energy executives said.

Pipeline companies largely quit adding new capacity following the pandemic, when shale production dried up and pipeline utilization plummeted. The 580-mile (933-km) Matterhorn Express pipeline is the first new natural-gas pipeline built in the Permian basin in three years.

Matterhorn began operations last month, relieving bottlenecks that had forced producers at times to pay other parties to receive their gas, or to seek state permits to burn the gas.

The line, a joint venture between WhiteWater Midstream, EnLink Midstream, Devon Energy and MPLX, can carry up to 2.5 billion cubic feet of gas per day, adding 14% in new regional capacity as it ramps up this year.

The Permian basin, which straddles Texas and New Mexico, accounts for half of U.S. crude output and is the second-largest shale-gas producing region.

“Matterhorn has freed up space, and the price we are getting for gas now has been positive for almost a month,” said Mike Oestmann, CEO of Midland producer Tall City Exploration. “We produced a lot of gas that we not only didn’t get paid for, we paid for it to be taken away,” he added.

Gas prices at the Waha hub in west Texas have been broadly pricing above zero since mid-September, after Matterhorn started operating. Last week, Waha prices reached their highest level since mid-June, at $2.35 per million British thermal units.

For oil and gas producers, the pipeline is helping drive up profits with gas fetching higher prices, allowing them to increase crude production growth with less gas flaring, analysts said. Natural gas is a byproduct of oil production.

“If you cannot move the gas out and you have to increase flaring levels or bring in other mitigating measures, then that just really puts a ceiling on how much oil you can produce,” said Jason Feit, advisor at consultancy Enverus.

Matterhorn will help unlock higher Permian oil output, said David Seduski, head of North American gas analysis at consultancy Energy Aspects. It estimates Matterhorn carried 0.6 bcf/d last week.

Most of the Permian’s estimated 2025 oil-production growth would be unfeasible without more gas pipeline capacity, said Seduski, who forecasts an additional 350,000 barrels per day next year.

A fifth of Permian oil producers polled in September reported plans to increase well completions once the pipeline bottleneck is cleared, according to the Federal Reserve Bank of Dallas’ quarterly energy survey.

Permian crude-oil production is forecast to rise by 6.1% to 6.27 million bpd this year, and hit 6.5 million bpd next year, according to the Energy Information Administration, due in part to improved drilling efficiency.

SHORT-TERM RELIEF

Matterhorn will likely be filled next year, resulting again in pipeline constraints, market participants said.

Permian gas production is set to swell to 24.5 bcf/d for 2024, from 22.7 bcf/d in 2023, according to the EIA. It is projected to reach 25.8 bcf/d in 2025.

“Matterhorn only gives you so long, maybe 12 to 18 months, and then you need another pipe,” Jim Simpson, CEO of advisory firm East Daley, said in an interview.

The Blackcomb gas pipeline, which reached final investment decision in July, will move another 2.5 bcf/d of natural gas from the Permian to south Texas. It will start up in the second half of 2026.

The period between Matterhorn filling and Blackcomb starting operations may depress Waha gas prices as producers face more bottlenecks, said Jay Stevens, director of market analytics at Aegis Hedging.

(Reporting by Georgina McCartney in Midland, Texas; Editing by Rod Nickel)

Chipotle Mexican Grill (NYSE: CMG) investors have been on edge since the announcement of the departure of powerhouse CEO Brian Niccol in August. The stock fell after its split in June, and it’s tentatively making its way back up as investors get comfortable with the idea that the chain can go on even without Niccol leading the way.

If the market had any more quibbles with that notion, the company just made it clear that it’s not stepping away from its strong leading position in the fast-casual restaurant space, flashing a bright buy signal to investors.

The unstoppable burrito king

Chipotle has become the go-to spot for reasonably priced fast-casual fare. It promotes itself as having fresh, healthy food, and it innovates with its menu to stay on top of trends.

It attracts an affluent clientele that’s more resilient despite inflation, and it has done well under the most adverse circumstances. It’s one of a few restaurant chains that didn’t miss a beat during the pandemic, without even one quarter of sales declines or losses.

In the 2024 second quarter, sales were up 18.2% year over year, driven by an 11.1% increase in comparable-restaurant sales. Operating margin expanded from 17.2% to 19.7%, and earnings per share (EPS) were up from $0.25 last year to $0.33 this year. That might have been somewhat inflated by stock-split hype, but it wasn’t an unusual quarter for the company.

It’s still opening up new stores at a fast clip, with 52 in the quarter and about 285 expected for the full year. It plans to reach about 7,000 in North America, up from around 3,500 today, giving it plenty of years of growth from new stores alone, but it’s starting to look into international markets as well.

What Chipotle is up to

Chipotle wasn’t always this successful. It was dealing with some major fallout after E-coli was discovered in its restaurants, and Niccol was brought in to turn things around.

The question on investors’ minds has been whether or not it can keep up its success without its leader. Niccol is a star at developing working processes and creating team leaders out of management. He also knows how to cultivate a brand and market it.

Now that he has infused this culture into the company at all levels, the likelihood is that the new management, under interim CEO and former chief operating officer Scott Boatwright, will keep things moving along. So far, Chipotle has not brought in outsiders; it’s letting the insiders steer the ship, and that certainly looks like the right move. It doesn’t need a new brand.

Last week, the company made some announcements that should inspire confidence in the new management. It launched a fund called Cultivate Next in 2022 to invest in companies that align with its vision of creating a better world and helping further its goal of 7,000 stores. Through this fund, it’s now investing in two new concepts.

The first is an Australia-based supply chain platform called Lumachain that uses artificial intelligence (AI) to trace products as they move through the supply chain from farm to store in real time.

The second is a fast-casual dining concept called Brassica that’s focused on Eastern Mediterranean food. It’s like a Chipotle with a different spin, reminiscent of Cava. It has only six stores right now, but with Chipotle’s resources and by following its proven model, that could seriously expand.

Does this point to new directions for Chipotle? Not right now, but it could certainly pull some tricks like that out of its sleeve. If it goes well, the chain has the funds and opportunities to reach into many different concepts that could expand its potential and achieve an even longer growth runway.

Cultivate Next has already invested in several other programs, and this could be an incubator for serious growth initiatives in tech, AI, and restaurant concepts. Chipotle stock jumped on the news.

You won’t get a deal on this stock

Chipotle’s price-to-earnings ratio (P/E) has been rich for a long time, and you might have already missed the chance to buy it on the cheap. Even that’s relative: The P/E hadn’t dipped below 48 even at the recent low. However, now it’s back up to 58.

That speaks to investor confidence in Chipotle stock. With Niccol or not, Chipotle has an excellent, reliable growth model that has returned incredible gains for investors in the past. New management is showing its strength and its willingness to be bold in the signature Chipotle fashion, and the company is in a good position to keep creating shareholder value well into the future.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,121!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,917!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $370,844!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 14, 2024

Jennifer Saibil has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill. The Motley Fool recommends Cava Group and recommends the following options: short December 2024 $54 puts on Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

1 Reason Chipotle Mexican Grill Stock Is Flashing a Giant Buy Signal Right Now was originally published by The Motley Fool

Utilities have been on fire this year as enthusiasm over booming AI electricity demand pushes the sector higher.

Case in point: The S&P 500 Utilities ETF (XLU) is up a whopping 29% so far this year — the best-performing sector to date, compared to the broader index’s 23% rise.

Much of the gains stem from enthusiasm over power producers that stand to benefit from the electrification boom — which includes Big Tech’s massive appetite for AI data centers and electric vehicles.

By 2050, electricity is projected to become the largest source of energy worldwide, according to a recent McKinsey study.

Also, five of the top 10 returning companies in the S&P 500 this year have been energy companies, noted Matt Sallee, president of Tortoise Capital. “Utilities and midstream infrastructure are going to be secondary beneficiaries of the AI theme,” he said in a recent note.

There’s no better example of that investor fever than the S&P 500’s top performer this year, power producer Vistra Corp (VST).

Shares of the Irving, Texas-based company are up 243% year to date, outperforming even AI heavyweight Nvidia (NVDA), up 186% during the same period.

On Thursday, JPMorgan analysts initiated coverage of Vistra along with two other Wall Street favorites, Talen Energy (TLN) and Constellation Energy (CEG) — all with an Overweight rating,

The analysts said the independent power producers (IPPs) stand to benefit from “a paradigm shift in power demand” amid structural tailwinds like manufacturing on-shoring, electrification trends, and data-center development.

“We do not see competitive market supply growth matching this demand, enabling IPPs to capture outsized margins for an extended period of time,” wrote JPMorgan’s Jeremy Tonet and his team.

As Yahoo Finance’s Julie Hyman pointed out, recent headlines like Microsoft (MSFT) teaming up with Constellation Energy to restart a nuclear reactor at Three Mile Island, and Amazon (AMZN) buying up a data center campus from Talen Energy have put Big Tech and its insatiable need for electricity into the spotlight.

But XLU’s massive performance this year begs the question — has it topped?

With the broader markets at all-time highs, it may be a good idea to keep investing in defensive stocks like utilities that provide dividends, said Burns McKinney, managing director and senior portfolio manager at NFJ Investment Group.

“There does seem to be a little bit more meat on the bone,” said McKinney, referring to more growth ahead.

If XLU holds its 29.1% year-to-date gains, it will be the best-ever yearly performance for the sector.

Ines Ferre is a senior business reporter for Yahoo Finance. Follow her on X at @ines_ferre.

Click here for in-depth analysis of the latest stock market news and events moving stock prices

Read the latest financial and business news from Yahoo Finance

CryptoCurrency

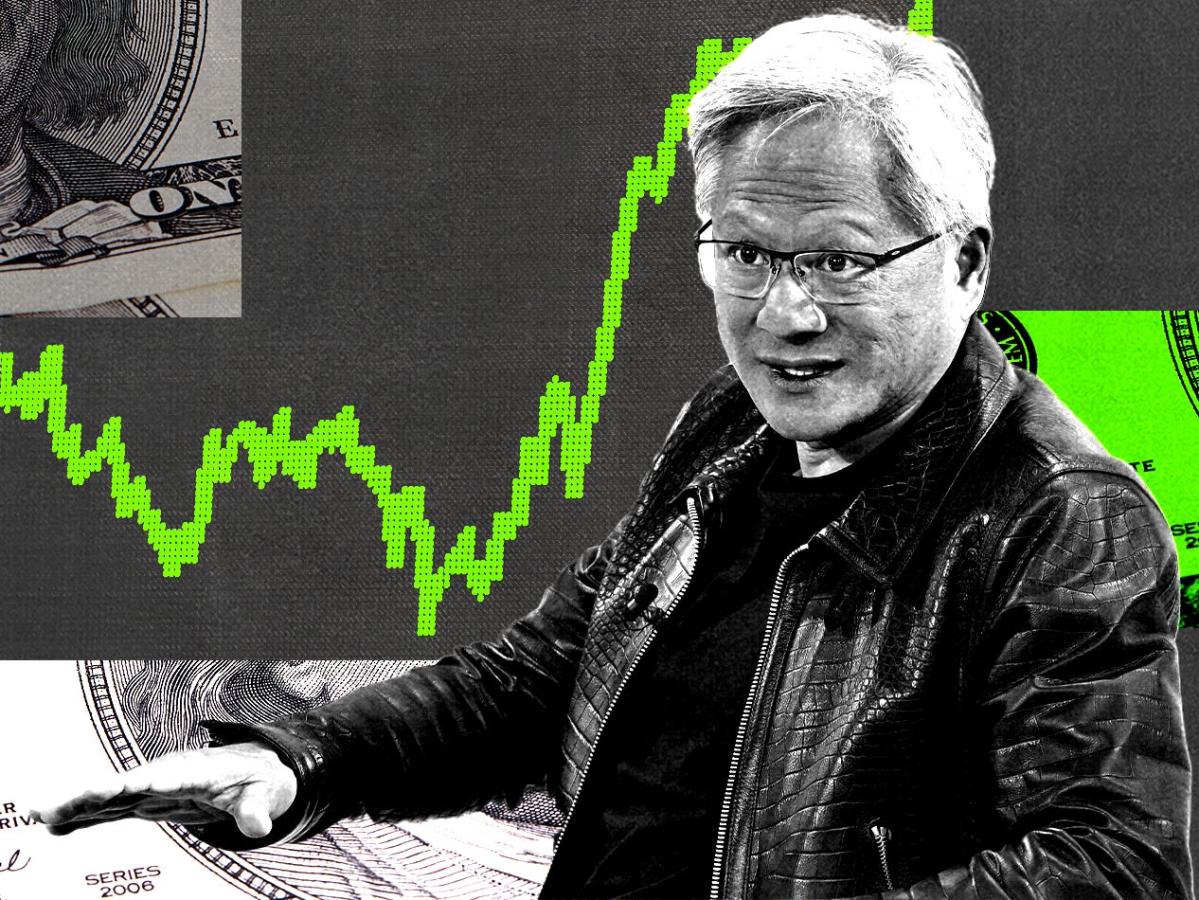

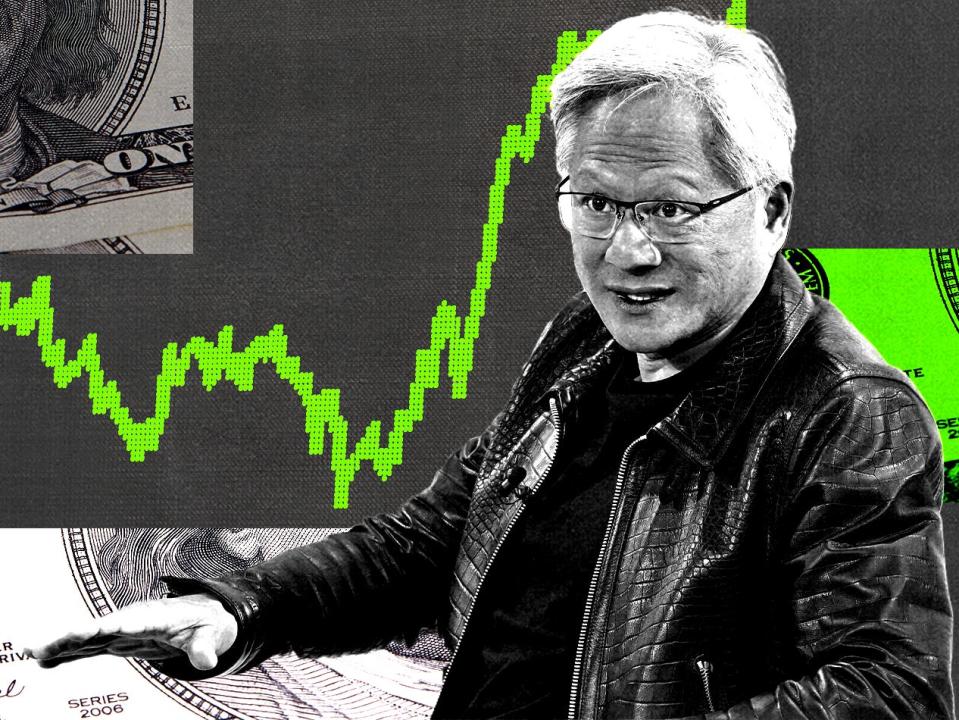

Nvidia stock has another 38% upside amid a ‘generational opportunity’ in AI, Bank of America says

-

Bank of America analysts raised their price target for Nvidia stock to $190 a share this week.

-

They see the AI market growing to $400 billion, giving Nvidia a “generational opportunity.”

-

They point to Nvidia’s strong lead among competitors, helped by its enterprise partnerships.

Nvidia stock has been on a tear all year, but investors can brace for even more gains ahead, Bank of America analysts say.

In a Thursday note, the analysts raised their price objective on the stock from $165 to $190. That implies a 38% upside from its price of about $138 a share at midday on Friday.

The analysts point to exponential growth in the AI market in the coming years, which they say will give Nvidia a “generational opportunity” as the chip titan continues to strengthen its lead in the market.

The analysts see the AI accelerator market growing to $280 billion by 2027, and toward upwards of $400 billion over time — marking huge growth from $45 billion in 2023.

As AI models continue to grow rapidly—with developers like OpenAI, Google, and Meta launching new large language models several times per year—the need for computing will only grow, the analysts predict.

Each new major LLM generation, especially those developed for larger size and better reasoning capabilities, will require greater training intensity, they add.

“We continue to see the pace of new model development increase. LLMs in particular are being developed for both larger size and better reasoning capabilities, which both require greater training intensity,” the analysts said.

They also point to Nvidia’s strong partnerships with enterprise customers like Accenture, ServiceNow, Oracle, and others, which show the growing presence of AI at big companies and Nvidia’s role as partner of choice.

“NVDA’s engagements span multiple verticals (e.g., Accenture, ServiceNow, Microsoft), and offerings such as AI Foundry, AI Hubs, NIMs are key levers to its AI leadership, not only on the hardware side but also on systems/ecosystems side,” the analysts said.

The analysts also said Nvidia’s financials are set up well for future gains. Given its free cash flow generation at 45%-50% margins, which is nearly double that of other Magnificent 7 stocks, Nvidia will be able to generate $200 billion in free cash flow over the next two years, they wrote.

Nvidia’s stock has skyrocketed this year, up 187% as AI continues to boom after a brief sell-off over the summer. The sector has since recovered, with chip stocks like Nvidia and TSMC trading at or near all-time highs in recent weeks.

Read the original article on Business Insider

(Bloomberg) — Warren Buffett is amplifying his bet on Sirius XM Holdings Inc., as Berkshire Hathaway Inc. keeps adding more shares of the radio broadcasting firm to its portfolio.

Most Read from Bloomberg

The conglomerate has acquired $42 million worth of shares in the three days through Friday, regulatory filings show.

Berkshire Hathaway now has a stake of about 32.5% in Sirius XM’s publicly traded stock, having become the top holder last month. That change came as billionaire John Malone’s Liberty Media split off its 83% stake and combined it with its separate tracking shares in the broadcaster.

Bershire added more of the stock to its holdings last week. The move provided some support for Sirius XM’s shares, which are down 50% this year amid expectations of lower sales.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

-

Science & Environment1 month ago

Science & Environment1 month agoHyperelastic gel is one of the stretchiest materials known to science

-

Technology4 weeks ago

Technology4 weeks agoIs sharing your smartphone PIN part of a healthy relationship?

-

Science & Environment1 month ago

Science & Environment1 month ago‘Running of the bulls’ festival crowds move like charged particles

-

Science & Environment1 month ago

Science & Environment1 month agoHow to unsnarl a tangle of threads, according to physics

-

Science & Environment1 month ago

Science & Environment1 month agoMaxwell’s demon charges quantum batteries inside of a quantum computer

-

Technology1 month ago

Technology1 month agoWould-be reality TV contestants ‘not looking real’

-

Science & Environment4 weeks ago

Science & Environment4 weeks agoX-rays reveal half-billion-year-old insect ancestor

-

Science & Environment1 month ago

Science & Environment1 month agoSunlight-trapping device can generate temperatures over 1000°C

-

Science & Environment1 month ago

Science & Environment1 month agoLiquid crystals could improve quantum communication devices

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum ‘supersolid’ matter stirred using magnets

-

Womens Workouts4 weeks ago

Womens Workouts4 weeks ago3 Day Full Body Women’s Dumbbell Only Workout

-

Technology3 weeks ago

Technology3 weeks agoUkraine is using AI to manage the removal of Russian landmines

-

TV3 weeks ago

TV3 weeks agoসারাদেশে দিনব্যাপী বৃষ্টির পূর্বাভাস; সমুদ্রবন্দরে ৩ নম্বর সংকেত | Weather Today | Jamuna TV

-

Science & Environment1 month ago

Science & Environment1 month agoLaser helps turn an electron into a coil of mass and charge

-

Science & Environment1 month ago

Science & Environment1 month agoWhy this is a golden age for life to thrive across the universe

-

Science & Environment1 month ago

Science & Environment1 month agoA new kind of experiment at the Large Hadron Collider could unravel quantum reality

-

Science & Environment1 month ago

Science & Environment1 month agoQuantum forces used to automatically assemble tiny device

-

Science & Environment1 month ago

Science & Environment1 month agoA slight curve helps rocks make the biggest splash

-

Science & Environment1 month ago

Science & Environment1 month agoNerve fibres in the brain could generate quantum entanglement

-

Science & Environment1 month ago

Science & Environment1 month agoHow to wrap your mind around the real multiverse

-

Football3 weeks ago

Football3 weeks agoRangers & Celtic ready for first SWPL derby showdown

-

Business3 weeks ago

DoJ accuses Donald Trump of ‘private criminal effort’ to overturn 2020 election

-

News3 weeks ago

News3 weeks agoMassive blasts in Beirut after renewed Israeli air strikes

-

News2 weeks ago

News2 weeks agoNavigating the News Void: Opportunities for Revitalization

-

News1 month ago

News1 month ago▶️ Hamas in the West Bank: Rising Support and Deadly Attacks You Might Not Know About

-

Science & Environment1 month ago

Science & Environment1 month agoITER: Is the world’s biggest fusion experiment dead after new delay to 2035?

-

MMA3 weeks ago

MMA3 weeks agoJulianna Peña trashes Raquel Pennington’s behavior as champ

-

Business3 weeks ago

Business3 weeks agoWhen to tip and when not to tip

-

News1 month ago

News1 month ago▶️ Media Bias: How They Spin Attack on Hezbollah and Ignore the Reality

-

Science & Environment1 month ago

Science & Environment1 month agoNuclear fusion experiment overcomes two key operating hurdles

-

Science & Environment1 month ago

Science & Environment1 month agoPhysicists have worked out how to melt any material

-

Science & Environment1 month ago

Science & Environment1 month agoTime travel sci-fi novel is a rip-roaringly good thought experiment

-

News1 month ago

the pick of new debut fiction

-

News1 month ago

News1 month agoOur millionaire neighbour blocks us from using public footpath & screams at us in street.. it’s like living in a WARZONE – WordupNews

-

Technology3 weeks ago

Technology3 weeks agoSamsung Passkeys will work with Samsung’s smart home devices

-

News2 weeks ago

News2 weeks ago▶ Hamas Spent $1B on Tunnels Instead of Investing in a Future for Gaza’s People

-

Sport3 weeks ago

Sport3 weeks agoWales fall to second loss of WXV against Italy

-

Technology3 weeks ago

Technology3 weeks agoMicrophone made of atom-thick graphene could be used in smartphones

-

MMA3 weeks ago

MMA3 weeks agoPereira vs. Rountree prediction: Champ chases legend status

-

MMA2 weeks ago

MMA2 weeks ago‘Uncrowned queen’ Kayla Harrison tastes blood, wants UFC title run

-

Sport3 weeks ago

Sport3 weeks agoWorld’s sexiest referee Claudia Romani shows off incredible figure in animal print bikini on South Beach

-

Sport3 weeks ago

Sport3 weeks agoBoxing: World champion Nick Ball set for Liverpool homecoming against Ronny Rios

-

Technology1 month ago

Technology1 month agoMeta has a major opportunity to win the AI hardware race

-

Technology4 weeks ago

Technology4 weeks agoWhy Machines Learn: A clever primer makes sense of what makes AI possible

-

News3 weeks ago

News3 weeks agoFamily plans to honor hurricane victim using logs from fallen tree that killed him

-

Sport2 weeks ago

Sport2 weeks agoCoco Gauff stages superb comeback to reach China Open final

-

MMA3 weeks ago

MMA3 weeks agoDana White’s Contender Series 74 recap, analysis, winner grades

-

Technology3 weeks ago

Technology3 weeks agoThis AI video generator can melt, crush, blow up, or turn anything into cake

-

Technology3 weeks ago

Technology3 weeks agoMusk faces SEC questions over X takeover

-

Sport3 weeks ago

Sport3 weeks agoSturm Graz: How Austrians ended Red Bull’s title dominance

-

News2 weeks ago

News2 weeks agoHeavy strikes shake Beirut as Israel expands Lebanon campaign

-

TV2 weeks ago

TV2 weeks agoLove Island star sparks feud rumours as one Islander is missing from glam girls’ night

-

News3 weeks ago

News3 weeks agoHeartbreaking end to search as body of influencer, 27, found after yacht party shipwreck on ‘Devil’s Throat’ coastline

-

News3 weeks ago

News3 weeks ago‘Blacks for Trump’ and Pennsylvania progressives play for undecided voters

-

Money3 weeks ago

Money3 weeks agoWetherspoons issues update on closures – see the full list of five still at risk and 26 gone for good

-

MMA2 weeks ago

MMA2 weeks agoPereira vs. Rountree preview show live stream

-

Sport3 weeks ago

Sport3 weeks agoMan City ask for Premier League season to be DELAYED as Pep Guardiola escalates fixture pile-up row

-

Business3 weeks ago

Bank of England warns of ‘future stress’ from hedge fund bets against US Treasuries

-

Business3 weeks ago

Business3 weeks agoChancellor Rachel Reeves says she needs to raise £20bn. How might she do it?

-

MMA3 weeks ago

MMA3 weeks agoAlex Pereira faces ‘trap game’ vs. Khalil Rountree

-

Business3 weeks ago

Sterling slides after Bailey says BoE could be ‘a bit more aggressive’ on rates

-

Technology3 weeks ago

Technology3 weeks agoTexas is suing TikTok for allegedly violating its new child privacy law

-

Technology2 weeks ago

Technology2 weeks agoThe best budget robot vacuums for 2024

-

Science & Environment1 month ago

Science & Environment1 month agoPhysicists are grappling with their own reproducibility crisis

-

Science & Environment1 month ago

Science & Environment1 month agoA tale of two mysteries: ghostly neutrinos and the proton decay puzzle

-

TV3 weeks ago

TV3 weeks agoPhillip Schofield accidentally sets his camp on FIRE after using emergency radio to Channel 5 crew

-

News3 weeks ago

News3 weeks agoGerman Car Company Declares Bankruptcy – 200 Employees Lose Their Jobs

-

TV3 weeks ago

TV3 weeks agoMaayavi (මායාවී) | Episode 23 | 02nd October 2024 | Sirasa TV

-

Technology3 weeks ago

Technology3 weeks agoPopular financial newsletter claims Roblox enables child sexual abuse

-

News2 weeks ago

News2 weeks agoBalancing India and China Is the Challenge for Sri Lanka’s Dissanayake

-

News3 weeks ago

News3 weeks agoHull KR 10-8 Warrington Wolves – Robins reach first Super League Grand Final

-

MMA3 weeks ago

MMA3 weeks agoUFC 307 preview show: Will Alex Pereira’s wild ride continue, or does Khalil Rountree shock the world?

-

Business3 weeks ago

Head of UK Competition Appeal Tribunal to step down after rebuke for serious misconduct

-

Sport3 weeks ago

Sport3 weeks agoAaron Ramsdale: Southampton goalkeeper left Arsenal for more game time

-

Technology2 weeks ago

Technology2 weeks agoA very underrated horror movie sequel is streaming on Max

-

Technology2 weeks ago

Technology2 weeks agoThe best shows on Max (formerly HBO Max) right now

-

Entertainment3 weeks ago

Entertainment3 weeks ago“Golden owl” treasure hunt launched decades ago may finally have been solved

-

Sport1 month ago

Sport1 month agoJoshua vs Dubois: Chris Eubank Jr says ‘AJ’ could beat Tyson Fury and any other heavyweight in the world

-

Technology4 weeks ago

Technology4 weeks agoArtificial flavours released by cooking aim to improve lab-grown meat

-

Business3 weeks ago

Eurosceptic Andrej Babiš eyes return to power in Czech Republic

-

News1 month ago

News1 month agoYou’re a Hypocrite, And So Am I

-

Science & Environment1 month ago

Science & Environment1 month agoRethinking space and time could let us do away with dark matter

-

Science & Environment1 month ago

Science & Environment1 month agoCaroline Ellison aims to duck prison sentence for role in FTX collapse

-

News1 month ago

The Project Censored Newsletter – May 2024

-

Technology3 weeks ago

Technology3 weeks agoUniversity examiners fail to spot ChatGPT answers in real-world test

-

Technology3 weeks ago

Technology3 weeks agoEpic Games CEO Tim Sweeney renews blast at ‘gatekeeper’ platform owners

-

Science & Environment3 weeks ago

Science & Environment3 weeks agoMarkets watch for dangers of further escalation

-

Technology3 weeks ago

Technology3 weeks agoAmazon’s Ring just doubled the price of its alarm monitoring service for grandfathered customers

-

News3 weeks ago

News3 weeks agoWoman who died of cancer ‘was misdiagnosed on phone call with GP’

-

Sport3 weeks ago

Sport3 weeks agoChina Open: Carlos Alcaraz recovers to beat Jannik Sinner in dramatic final

-

Technology3 weeks ago

Technology3 weeks agoApple iPhone 16 Plus vs Samsung Galaxy S24+

-

Technology3 weeks ago

Technology3 weeks agoUlefone Armor Pad 4 Ultra is now available, at a discount

-

News3 weeks ago

News3 weeks agoReach CEO Jim Mullen: If government advertises with us, we’ll employ more reporters

-

Business3 weeks ago

Maurice Terzini’s insider guide to Sydney

-

Health & fitness3 weeks ago

Health & fitness3 weeks agoNHS surgeon who couldn’t find his scalpel cut patient’s chest open with the penknife he used to slice up his lunch

-

Money3 weeks ago

Money3 weeks agoWhy thousands of pensioners WON’T see State Pension rise by full £460 next year

-

Business3 weeks ago

The search for Japan’s ‘lost’ art

-

Technology2 weeks ago

Technology2 weeks agoHow to disable Google Assistant on your Pixel Watch 3

-

Technology2 weeks ago

Technology2 weeks agoIf you’ve ever considered smart glasses, this Amazon deal is for you

-

MMA3 weeks ago

MMA3 weeks agoHow to watch Salt Lake City title fights, lineup, odds, more

You must be logged in to post a comment Login