Major floods and landslides in Nepal have killed at least 100 people across the Himalayan nation, officials have reported.

Dozens more were still missing on Sunday after two days of intense rainfall, which has inundated the valley around the capital Kathmandu.

People have been left stranded on rooftops with workers carrying out rescuers on rafts. Thousands of homes near rivers have also been flooded and many highways blocked.

Despite rain forecast to continue to Tuesday, there were signs of some easing on Sunday.

Advertisement

So far, more than 3,000 people have been rescued according to a government spokesman.

But flash floods, along with landslides, have caused many deaths.

Five people, including a pregnant woman and a four-year-old girl, died when a house collapsed under a landslide in the city Bhaktapur, to the east of Kathmandu, state media reports.

Two bodies were removed from a bus buried by a landslide in Dhading, west of Kathmandu. Twelve people, including the driver, were said to be onboard.

Advertisement

Six football players were also killed by a landslide at a training centre operated by the All Nepal Football Association in Makwanpur, to the south-west of the capital.

Others have been swept up in the floodwaters. In one dramatic scene, four people were washed away by the Nakkhu River in the southern Kathmandu valley.

“For hours, they kept on pleading for help,” Jitendra Bhandari, an eyewitness, told the BBC. “We could do nothing.”

Hari Om Malla lost his truck after it was submerged by water in Kathmandu.

Advertisement

He told the BBC that water had “gushed” into the cabin as the rain intensified on Friday night.

“We jumped out, swam, and got away from it – but my purse, bag and mobile have been swept away by the river. I have nothing now. We stayed the whole night in the cold.”

Government spokesman Prithvi Subba Gurung told the state-run Nepal Television Corporation the flooding had also broken waterpipes, and affected telephone and power lines.

According to state media, 10,000 police officers, as well as volunteers and members of the army, have been mobilised as part of search and rescue efforts.

Advertisement

The Nepalese government urged people to avoid unnecessary travel, and banned driving at night in the Kathmandu valley.

Most highways – including the ones connecting Kathmandu valley with the rest of the country – also remain blocked in several places.

Air travel was also affected on Friday and Saturday, with many domestic flights delayed or cancelled.

Monsoon season brings floods and landslides every year in Nepal.

Advertisement

Scientists say, though, that rainfall events are becoming more intense due to climate change.

A warmer atmosphere can hold more moisture, while warmer ocean waters can energise storm systems, making them more erratic.

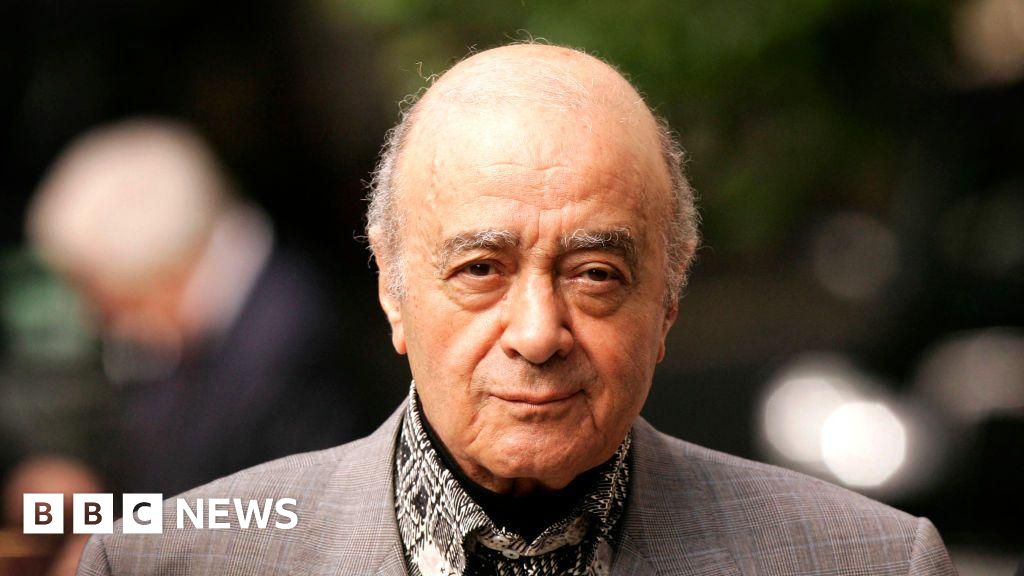

In 2010 the Gulf state of Qatar bought luxury department store Harrods for £1.5bn, via its sovereign wealth fund, the Qatar Investment Authority.

It should have been the jewel in the Qatari crown. However, Harrods now faces serious sexual abuse allegations over the actions of its former boss, Mohamed Al Fayed.

Many of these claims were uncovered in a recent BBC investigation, but multiple legal experts have said Qatar either missed or dismissed much of what was already known about Al Fayed at the time of the purchase.

This includes a 2008 police investigation into the alleged assault of a 15-year-old girl in a Harrods boardroom.

Harrods has told the BBC it is “utterly appalled” by the allegations and has apologised to the victims.

Advertisement

It now looks as if the scandal could cost the company and its owner millions.

So what, if anything, was known by Qatar about the allegations?

‘Inadequate’ due diligence

When a company buys another company, the process of looking to see if there are any skeletons in the cupboard is known as due diligence.

Advertisement

The buyers will hire advisers who will ask the seller’s advisers questions about any issues they should know about. They may also do their own independent research.

When the owner is someone like Mohamed Al Fayed, who had several allegations surrounding him at the time of the deal, the buyer’s due diligence process should be lengthy.

“I think it would be sensible to ask detailed questions about number of claims, number of complaints – informal or formal – even if not upheld, subject of the complaints even if they were not upheld, number and value of settlements, number of NDAs (non-disclosure agreements),” says Beth Hale, a partner at law firm CM Murray.

In “exceptional cases” this information might scupper a deal, though she believes it is more likely the buyer would ask the seller to compensate them for any losses that might come from the alleged behaviour.

Advertisement

This is what Ms Hale says a business should do if it were buying a company like Harrods in 2024, but she says that 2010 was a different time.

She says this pre-#MeToo era was a “world away in terms of attitudes and approaches to sexual harassment”.

“Sexual harassment claims did not form as big a part of due diligence then as they do now.”

She says it appears that either Qatar’s due diligence was “not adequate” or that the process did bring up certain claims and it decided to continue in any event, perhaps imagining that they might not end up hurting the company too badly.

Advertisement

“Pre-#MeToo, with a couple of sexual harassment claims, a company might settle them, get an NDA, and move on.”

Catriona Watt, partner at Fox & Partners, says it looks as if Qatar may have known about the allegations but went ahead anyway.

“It seems to me that it wasn’t a complete secret. It was probably a calculated risk,” she says, adding the due diligence process “depends on the questions you ask”.

“You might say, ‘I only want to know about this if it has a value of X,”‘ she says.

Advertisement

Virginia Albert, former marketing professor and current account director at advertising agency DeVito/Verdi, also believes Qatari views on women’s rights are relevant, suggesting they may not have considered sexual abuse allegations something sufficiently serious to warrant dropping the deal.

“You could argue that brands align with brand values during mergers,” she says, adding the Gulf state would have considered if its values “aligned with what they knew, if they knew, about the values of this department store”.

Lazard, which represented the Al Fayed Trust during the deal, told the BBC: “We strongly condemn the behaviour these reports have brought to light.”

Harrods and the Qatar Investment Authority did not reply to multiple requests for comment on the due diligence process when the company was bought. In its previous response to the BBC, Harrods said it had been settling claims “since new information came to light” last year.

Advertisement

Meanwhile, Harrods’ managing director Michael Ward said on Thursday: “While it is true that rumours of [Al Fayed’s] behaviour circulated in the public domain, no charges or allegations were ever put to me by the police, the [Crown Prosecution Service], internal channels or others.

“Had they been, I would of course have acted immediately.”

Credit Suisse, now owned by UBS, represented the Qatar Investment Authority in the deal and declined to comment.

Compensation and reputation

Advertisement

Whatever Qatar knew during the deal, the impact of the allegations is likely to be substantial.

First, there is the total cost of payments to the survivors of the alleged sexual abuse by Al Fayed, which multiple legal experts have told the BBC could be in the millions, with each individual claim likely to cost the firm a six-figure sum.

Harrods has accepted vicarious liability for some of the claims, a legal term meaning it accepts ultimate responsibility for Al Fayed’s alleged actions.

It could also be liable for alleged failings as an employer for charges such as negligence or failing to provide a safe working environment, experts predicted.

Advertisement

Defending the legal case and hiring an independent investigator to look into the claims are also expected to be six-figure sums.

However, the real damage is expected to be reputational.

“People are going to be really, really pissed,” says Ms Albert, adding that many will want to see Harrods dealing with the serious allegations from the survivors swiftly and thoroughly.

“There’s so much more visibility now than there was.”

Advertisement

What might save Harrods, she says, is the loyalty of its long-time shoppers, but the high-price point will make it much easier for casual customers who dislike the way the retailer is perceived to have treated women to go elsewhere.

She predicts boycotts and says the business may struggle to recover unless customers see action, rather than just words.

RETIRING early might sound like an impossible goal, but anyone can manage it if they know the tips and tricks to saving at the right time and in the right way.

The good news is that even small changes can make massive difference to how much you have saved and when you can afford to stop work.

1

Find out what tips and tricks you need to know to retire earlyCredit: Alamy

A new movement, known as the FIRE movement (financial independence, retire early) are looking to retire as soon as possible.

Advertisement

But you don’t need to be this extreme – there are realistic ways to retire early without working too hard.

The earlier you start making small changes, though, the easier it is, and if you leave retirement saving too late, you might actually have to retire later than you’d prefer.

We spoke to Robert Cochran, a pensions expert at Scottish Widows, to uncover the secret to retiring early and comfortably.

You can watch the video above to hear more about his top tips.

Advertisement

Start early

Cochran’s first tip is to get saving as soon as possible. There are two reasons for this, the first is straightforward – starting earlier means more savings.

For instance, if you saved £100 a month into your pension from aged 16, you’d have £46,800 by the time you were 55, without any investment growth, employer contributions, or tax relief.

But, if you started at 40, you’d only have £22,500.

The more important consideration is investment growth, which compounds over time. Essentially this means that the returns you earn on your pensions are reinvested, which, so the money grows exponentially.

Advertisement

Cochran explained: “Einstein said that compound interest was the eighth wonder of the world, these who know it will grow it, and those who don’t will pay it.”

For instance, if you pay a thousand pounds into a pension, and it earns 5%, in the first year you would get £50 added, in the second you’d have £1,050 invested and get £52.50 back.

The year after that you would get £55.13 added, and by year 10 you’d be getting £77.57 in interest – all without saving any extra money.

If you keep adding to the pension each year, the results are even more stark. For instance, if you saved £1,000 a year into a pension with growth of 5%, from age 18-55, you’d have £107,709.55 to retire on.

Advertisement

Pensioner proves age is no barrier as he is set to become a personal trainer aged 78

Of that, £69,709.55 would be interest paid, which is essentially free money that you’ve earned on your savings.

If you were paying minimum auto-enrolment levels on the average UK full time salary, which works out as around £2,797 a year, you’d have £301,263.60 to retire on aged 55. But if you didn’t start saving till you were 30, you’d have just £142,964.33.

Consider saving into a pension for your children

Parents are allowed to open Junior SIPPs for their children, which is a way of saving money for their retirement.

You’re allowed to save up to £3,600 a year, 20% of which comes in the form of tax relief from the Government. That means you can save £240 a month before tax relief.

Advertisement

If you do this from birth until they are 18, you’ll have over £64,800 saved for them.

Even if they never pay another penny in themselves, they’d have £394,075.17 by age 55, with returns of 5%. If they wait until they’re 60 to access the cash, they could have half a million pounds to retire on.

Cochran said: “You can actually pay contributions in for children. So, imagine somebody’s born and then you pay in contributions for them till they’re age 18… and then you leave that money to grow by the time they’re 60.

“That money could be worth £1 million. And that’s purely through compound and growth.”

Advertisement

Don’t leave cash on the table

Cochran’s third tip is to make sure that you’re never missing out on free money that’s available.

The first thing to consider is auto-enrolment. Most people aged between 22 and 64 who are employed are auto-enrolled into a pension.

The minimum auto-enrolment level is 8% of your qualifying earnings, which is made up of a mix of money deducted from your salary, tax relief, and contributions from your employer.

It is possible to opt-out of auto-enrolment, but not only does that mean you won’t be saving, you’ll also miss out on the contributions from your workplace. That means you’re giving up free money from your boss, and you’ll lose the tax relief too.

Advertisement

Even if you’re not eligible for auto-enrolment, for instance if you’re under 22, or earn less than £10,000 a year from a single employer, you might be able to opt in.

For instance, if you earn more than £6,240, you can choose to join the scheme and your employer will still have to pay contributions.

Another key thing to look out for is matching, which is when your employer says it will pay more money into the scheme if you do, up to a maximum.

Cochran explained: “Go back to your employer and find out the maximum contribution you’re entitled to get from them.

Advertisement

“If you’re not receiving it, go ahead and ask for it. It might mean that you have to pay a little bit more, but do not leave cash on the table.”

Track down lost pensions

The Pension Policy Institute says that there is £26.6billion in lost pensions money.

Typically, this is where people have saved into a scheme but then moved job or house and forgotten about the pot.

Cochran said: “Use the Government’s free pension tracing service and find out what you’ve got.”

Advertisement

To get started, gather all the pensions paperwork you do have, and make a list of every employer you’ve worked for or private pension you’ve opened.

The tracing service will tell you who ran the scheme at the time, and how to contact them. Then, you can get in touch and check whether they have any retirement savings in your name.

Make a plan

The fifth thing to do if you want to retire early is make a concrete plan.

Cochran said: “You need to know what you’re going to be doing in retirement… so, look towards your future. Use the tools and calculators that are there to help you.”

Start by working out how much you need to have squirrelled away, and don’t be scared by illustrative examples.

For instance, the Pensions and Lifetime Savings Association (PLSA) retirement living standards research says that a single person who wants a comfortable retirement will need £43,100 a year to live on.

But of course, this is higher than the average UK salary, and there are lots of people who live comfortably on much less.

Advertisement

The amount you need will be determined by how early you want to retire, your life expectancy, your salary and typical monthly expenditure, and whether you own your home or not.

If you’re over 50, you can book a free and impartial session with a Pension Wise adviser who can share important information and make sure you understand all the facts before you decide to retire.

What are the different types of pensions?

WE round-up the main types of pension and how they differ:

Advertisement

Personal pension orself-invested personal pension (SIPP) – This is probably the most flexible type of pension as you can choose your own provider and how much you invest.

Workplace pension – The Government has made it compulsory for employers to automatically enrol you in your workplace pension unless you opt out. These so-called defined contribution (DC) pensions are usually chosen by your employer and you won’t be able to change it. Minimum contributions are 8%, with employees paying 5% (1% in tax relief) and employers contributing 3%.

Final salary pension – This is also a workplace pension but here, what you get in retirement is decided based on your salary, and you’ll be paid a set amount each year upon retiring. It’s often referred to as a gold-plated pension or a defined benefit (DB) pension. But they’re not typically offered by employers anymore.

New state pension – This is what the state pays to those who reach state pension age after April 6 2016. The maximum payout is £203.85 a week and you’ll need 35 years of National Insurance contributions to get this. You also need at least ten years’ worth to qualify for anything at all.

Basic state pension – If you reach the state pension age on or before April 2016, you’ll get the basic state pension. The full amount is £156.20 per week and you’ll need 30 years of National Insurance contributions to get this. If you have the basic state pension you may also get a top-up from what’s known as the additional or second state pension. Those who have built up National Insurance contributions under both the basic and new state pensions will get a combination of both schemes.

King Charles III has reflected on his mother’s final days in Scotland, saying it is a “uniquely special place” for the royal family.

The late Queen’s love for Balmoral Castle in Royal Deeside, was well known, and where she spent many summers – as a small child and in later life with Prince Philip.

The King suggested she “chose” to spend her last moments there in 2022, despite her previous concerns that if her death occurred in the Highlands it may be logistically difficult for others.

The comments were made in a speech by King Charles – dressed fittingly in a kilt – to mark 25 years of the Scottish Parliament.

Advertisement

He attended its opening in 1999 – when he was Prince Charles – and has visited several times since.

“Speaking from a personal perspective, Scotland has always had a uniquely special place in the hearts of my family and myself,” the King said, adding his “beloved grandmother was proudly Scottish.”

Queen Elizabeth II died on 8 September 2022, aged 96, at her Scottish estate.

“My late mother especially treasured the time spent at Balmoral, and it was there, in the most beloved of places, where she chose to spend her final days,” the King said.

Advertisement

The late Queen also spent much of Prince Philip’s last years with him on the estate, where they stayed together during the Covid-19 lockdown. In November 2020, the couple celebrated their 73rd wedding anniversary there.

“We did try and persuade her that that shouldn’t be part of the decision-making process,” the Princess Royal recalled in a BBC documentary last year.

“I hope she felt that that was right in the end, because I think we did.”

Advertisement

Balmoral has been one of the royal family’s residences since 1852, when the estate and its original castle were bought by Prince Albert, Queen Victoria’s husband. The current Balmoral Castle was commissioned after the house at the time was deemed too small.

It was private property belonging to the Queen and is not part of the Crown Estate.

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

New legislation that puts companies on the hook for employees committing fraud could lead to a significant increase in plea-bargain-style deals with the prosecutor, according to the head of the UK Serious Fraud Office.

SFO director Nick Ephgrave said deferred prosecution agreements — or DPAs — could come back with “a vengeance” once a new offence that puts the onus on businesses to prevent fraud comes into force, which is expected to be next year.

Advertisement

Under a DPA, first introduced in the UK a decade ago, a criminal prosecution against a company is suspended if the business approaches the SFO and agrees to terms — approved by a judge — such as co-operating with investigations against individuals, paying a fine and abiding by certain conditions. This allows companies to avoid criminal convictions and long trials.

“DPAs I think are a really helpful and useful tool in the armoury,” said Ephgrave, who took over the helm a year ago this month.

“I think they could really come back with a bit of a vengeance when we have the duty to prevent fraud offence active.” The new rules “could lead to an uptick in DPA-type referrals”, he added.

“DPAs . . . avoid what is often going to be a very costly and lengthy trial, and get the benefit for victims . . . and or the benefit to the country of enormous fines, which then go back into the coffers,” he added.

Advertisement

The SFO has previously secured a dozen DPAs against companies including Rolls-Royce and Airbus.

A former police officer and the first non-lawyer to run the SFO, Ephgrave is trying to resurrect the agency’s reputation after a number of high-profile failures.

Under previous director Lisa Osofsky the prosecutor closed several investigations against blue-chip companies, saw convictions quashed in cases after mis-steps, and struggled to recruit staff.

The SFO is currently embroiled in a lawsuit with Eurasian Natural Resources Corporation, formerly the target of an investigation, that could see the agency forced to pay potentially millions of pounds to the mining group in compensation.

Advertisement

Ephgrave said the SFO was “disappointed” by the court’s decision over its liability in the case and “will enter into the quantum negotiations resolutely”, but declined to comment further while the litigation is still live.

Ephgrave is also pushing to introduce payment for whistleblowers in the UK, which may require new legislation.

While he has yet to discuss the plans directly with new government, he said he hoped such an initiative would be introduced during his five-year tenure.

His comments come the day after the chair of the UK’s financial regulator faced calls to resign over his mishandling of whistleblower details.

Advertisement

Ashley Alder from the Financial Conduct Authority refused to quit on Thursday despite protest groups criticising him after an internal review that cleared him of wrongdoing for forwarding messages from two whistleblowers inside the business.

Millions of households could be in line for cost-of-living payments worth up to £3,225 this winter.

For those under financial pressure, several schemes offering support to help you get through the cold period.

1

Millions of households are eligible for cash support this winterCredit: Getty

With additional heating costs, not to mention Christmas expenses, the winter months can mean additional financial pressure.

Advertisement

For some this will be exacerbated by the government’s decision to limit the number of people who receive the £300 winter fuel payment from this year.

The support available includes the following…

Warm home discount – worth £150

The £150 warm home discount is available to pensioners and those on low incomes.

Those who qualify for the discount will have £150 deducted from their energy bills by the end of March 2025.

Advertisement

You’ll be eligible if you receive the guarantee credit element of Pension Credit, or are on a low income and have high energy costs.

The discount should be automatically deducted from your energy bill this winter if your eligible, but those on low-incomes living in Scotland need to apply through their energy providers.

If you were eligible for the payment last winter and did not receive it, contact your energy supplier.

If your energy supplier is unable to help write to the warm home discount scheme on 110552 Warm Home Discount Scheme, PO Box 26965, Glasgow, G1 9BW.

Advertisement

What is the energy price cap?

Winter fuel payment – £300

This year winter fuel payments will only be made to retirees on Pension Credit and several other means-tested benefits.

Under the new rules, all households claiming the following benefits will automatically receive this year’s winter fuel payment, unless they live abroad:

Only those living abroad and meeting certain conditions must apply for the cash this winter.

If you do not live in the UK, you’re only eligible for the winter fuel payment if:

You moved to an eligible country before January 1, 2021

You were born before September 23, 1958

You have a genuine and sufficient link to the UK – this can include having lived or worked in the UK and having family in the UK

You only need to claim winter fuel payment if you’ve not received it since you moved abroad.

To claim by post, you’ll need to fill in the winter fuel payment claim form and post it to the Winter Fuel Payment Centre.

Advertisement

This will be available at www.gov.uk/winter-fuel-payment/how-to-claim from September 30.

Cold weather payment – £25 a week

Cold weather payments are made to eligible residents in areas where the temperature is recorded at zero degrees Celsius or below, for seven consecutive days.

A £25 payment will be made for each seven day period of very cold weather between November 1 2024 and March 31 2025.

You may be eligible for the payments if you receive:

The bonus isn’t available to those who receive Universal Credit only but someone on Universal Credit who also receives one of the qualifying benefits will receive it.

Household Support Fund – up to £740

Struggling households can access a range of support to help with the cost of living via the Household Support Fund.

Advertisement

The fund has recently has been extended for the sixth time, with £421million set to be made available to regional councils to distribute from October 2024.

The support you can access depends on where you live, but funds can be paid out as shopping or fuel vouchers, cash payments or other means.

Under the previous round of funding households in Leicester could apply to receive £300 payments to help with utilities and essential costs.

In Plymouth eligible residents could receive a maximum of £740 in vouchers.

Advertisement

This included £240 in supermarket vouchers, £200 in energy vouchers as well as an essential item of household furniture or white goods or £300 of clothing vouchers.

Schemes vary across the country, but every council will receive funding to distribute.

To see what’s on offer where you live contact your local council.

Energy grants – up to £2,000

Energy firms are handing out up to £2,000 to help those struggling with energy costs to cover bills.

From reducing energy consumption to effectively heating your home The Sun’s guide can help you cut costs.

How to save on your energy bills

SWITCHING energy providers can sound like a hassle – but fortunately it’s pretty straight forward to change supplier – and save lots of cash.

Shop around – If you’re on an SVT deal you are likely throwing away up to £250 a year. Use a comparion site such as MoneySuperMarket.com, uSwitch or EnergyHelpline.com to see what deals are available to you.

Advertisement

The cheapest deals are usually found online and are fixed deals – meaning you’ll pay a fixed amount usually for 12 months.

Switch – When you’ve found one, all you have to do is contact the new supplier.

It helps to have the following information – which you can find on your bill – to hand to give the new supplier.

Your postcode

Name of your existing supplier

Name of your existing deal and how much you payAn up-to-date meter reading

It will then notify your current supplier and begin the switch.

It should take no longer than three weeks to complete the switch and your supply won’t be interrupted in that time.

Advertisement

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

You must be logged in to post a comment Login