Helen Holland died two weeks after she was struck by a police motorbike

A Metropolitan Police officer has been charged over the death of an 81-year-old woman who was killed in a crash with a motorcycle that was part of an escort for the Duchess of Edinburgh.

Helen Holland, 81, was struck in Earl’s Court, west London, on 10 May 2023. She died in hospital two weeks later.

The Crown Prosecution Service (CPS) said it had authorised a charge of causing death by careless driving against Christopher Harrison, 67, following a review of the evidence by the Independent Office for Police Conduct.

He is due to appear at Westminster Magistrates’ Court on 6 November.

Advertisement

‘Massive internal injuries’

Rosemary Ainslie, head of the CPS special crime division, said that with criminal proceedings now active there should be “no reporting, commentary or sharing of information online which could in any way prejudice these proceedings”.

Ms Holland was fatally injured at the junction of West Cromwell Road and Warwick Road.

Following the crash, her son Martin told the BBC she died after sustaining “multiple broken bones and massive internal injuries”.

Advertisement

After her death was announced, a Buckingham Palace spokesperson said: “The Duchess of Edinburgh is deeply saddened to hear that Helen Holland has passed away.

“Her Royal Highness’s deepest condolences and sympathies go to all of Ms Holland’s family.”

Exploring Press Freedoms: Updates on Julian Assange’s Extradition

Advertisement

/

Advertisement

Advertisement

We kick off this year focusing on press freedoms. We welcome back to the program independent journalist Kevin Gosztola, author of Guilty of Journalism: The Political Case Against Julian Assange. Gosztola joins the program to discuss the latest updates on Assange’s extradition case, the CIA spying lawsuit and a Congressional resolution process that’s begun. Later in the program we air a conversation between Kevin Gosztola and our cohost Eleanor Goldfield from last year. Kevin joined Eleanor at Red Emma’s in Baltimore to talk about his book,Guilty of Journalism.

A long-serving former Harrods executive has claimed that his offer to become boss of the department store chain Fenwick was withdrawn because of his time working under Mohamed Al Fayed.

Al Fayed, who owned the luxury London store for more than two decades, has been accused of sexual assault or rape by more than 20 women following a BBC investigation.

Niegel Blow, who worked for 14 years at Al Fayed’s companies, said he “never heard about or witnessed” grooming, sexual assaults or rape.

He said he had been deemed “guilty by association” by Fenwick. Fenwick declined to comment.

Advertisement

“I worked at Harrods in senior roles from 2002 to 2007. I can confirm that, during my time at the business, I never heard about or witnessed any such behaviour by Mr Al Fayed.”

“I believe Fenwick’s action is unjustified, unfair and in breach of contract,” Mr Blow told the BBC.

Mr Blow also criticised the BBC over its reporting of executives who had worked with Al Fayed.

“It would appear that the BBC team is prepared to tarnish or ruin the reputation of every senior person who worked at Harrods during Mr Al Fayed’s ownership, under the serious and damaging misapprehension that of course they must have known.”

Advertisement

A BBC spokesperson said: “We stand fully behind our journalist and our journalism. This story, which was fully in the public interest, was produced in line with the BBC’s editorial standards, including contacting Mr Blow before publication.”

On Tuesday, Fenwick told the BBC that Nigel Blow had said he would no longer be taking up the position as their chief executive later this month.

No reason for the decision was given.

Mr Blow’s statement on Friday said that the Fenwick chair Sian Westerman told him it was not able to proceed with the employment “in order to safeguard the reputation of the Fenwick business.”

Advertisement

Fenwick declined to comment on this claim. The retailer, which is best known for its 140-year-old store in Newcastle, has eight stores around the UK.

Mr Blow joined Harrods in 1992.

There were several reports of Al Fayed’s alleged abuse of women in the following years including a profile in Vanity Fair alleging sexual misconduct against staff, an ITV documentary and a book detailing alleged sexual assaults.

Mr Blow said that Harrods staff had their offices, phones and cars bugged, and at one point he was followed by the Harrods security team.

Advertisement

“On multiple occasions I saw transcripts of my own telephone calls on Mr Al Fayed’s desk. Such behaviour prompted me to seek alternative employment from 2006,” he said.

In 1997 the Observer published detailed allegations of bugging of Harrods executives and staff carried out on Al Fayed’s orders – and the ITV documentary played excerpts from the tapes.

Mr Blow is currently chief executive of the department store chain Morley’s, based in Wimbledon, though he resigned the position to take up the new job.

The McRib burger will be back on the Golden Arches menu from October 16Credit: Getty

3

Advertisement

One user called it “the Greatest McDonalds burger of all time” .Credit: Gary Stone

3

Another commenter said: “My absolute favourite, welcome back Ribby. Please don’t leave us again”.Credit: Getty

Taking to social media, many expressed their enthusiasm for the burger’s return with one user calling it “the Greatest McDonalds burger of all time” .

Another commenter said: “My absolute favourite, welcome back Ribby. Please don’t leave us again”.

Whilst others wrote: “It’s what dreams are made of” and “cannot wait, it’s been way too long”.

Advertisement

Another user added: “I’m so getting one I loved them back in the day”

The pork-based patty, which is lathered in smoky BBQ sauce, pickles and onions and encased in a homestyle bun, is back on menus for a limited time from mid October.

The burger first launched in the UK in 1981 and has been hailed as one of the best Mcdonald’s burgers of all time by some fans.

Thomas O’Neill, head of menu at McDonald’s UK, said: “We have heard our fans loud and clear – the fan petitions and pleas on social – and after almost a decade of anticipation, we are thrilled to bring back this iconic menu item.

Advertisement

“Knowing how well-loved the McRib is, we had very little choice – we had to make it happen.”

Though the fast-food chain’s owners have not revealed how long the popular burger will be on the menu for, limited edition foods are usually around for about six weeks.

It will be on sale for £4.49 as an individual item or £6.19 as part of a medium extra-value meal deal, which means it comes with fries and a medium drink.

McDonald’s worker reveals how McRibs are made and stored in messy trays in ‘nasty’ video

At 509 calories, the burger is more calorific than a Double Cheeseburger, McChicken and Bacon Double Cheeseburger as well.

Advertisement

Despite most diners excitement some have not been so keen, with one social media user likening the product to “gas station food”.

“I must be the only one that thinks it’s horrible,” said another.

Whilst another commenter wrote: “Yay, another reason for me to stay away from McDonald’s” .

One user even joked: “How about the McHeartAttack or the McBigBelly?”

But, he added, the burger felt quite sickly because of the abundance of BBQ sauce, which he felt was too sweet.

McRib’s addition comes after McDonald’s confirmed the arrival of a pack of mini hash browns, which will come in a portion of five or 15, with prices starting from £1.49.

These will roll out from October 16 but it is unclear whether or not the snack will become a permanent feature on the menu.

Shigeru Ishiba is a distinguished figure in Japanese politics, widely recognized for his expertise in defense and agricultural policy. He was a prominent contender in multiple Liberal Democratic Party (LDP) leadership races and was just elected Japan’s 102nd prime minister. His latest book, My Policies, My Destiny, offers profound insights into his political philosophy, which he defines as that of a “conservative liberal.” This label underscores Ishiba’s nuanced approach to governance — an idealism that seeks not just to solve the nation’s pressing issues, but to fundamentally elevate it and its people.

Ishiba’s idealism (or “Ishibaism”) has long placed him at odds with the late Prime Minister and LDP President Shinzo Abe, whose vision for Japan centered on bolstering national power and economic dominance. By contrast, Ishiba advocates “purer” solutions that aim for deeper structural improvements. This divergence is central to his critique of “Abe politics,” which he sees as prioritizing short-term gains over long-term national rejuvenation.

Ishiba and incumbent Prime Minister Fumio Kishida are committed to refocusing Japan’s growth strategies on rural regions, which have been disproportionately affected by economic disparities. While Ishiba is inclined towards fiscal discipline, he is unlikely to pursue immediate austerity measures; rather, he will probably consider carefully timed tax increases to finance rising defense expenditures.

Ishiba’s policies to manage economic turmoil

In March 2024, the Bank of Japan (BOJ) raised interest rates for the first time in 17 years. This signals an end to its negative interest rate policy in response to persistent inflationary pressures. In July, the yen dropped to its lowest value in 38 years; a second rate hike followed. Political pressure had been building for such hikes to address the yen’s devaluation.

Advertisement

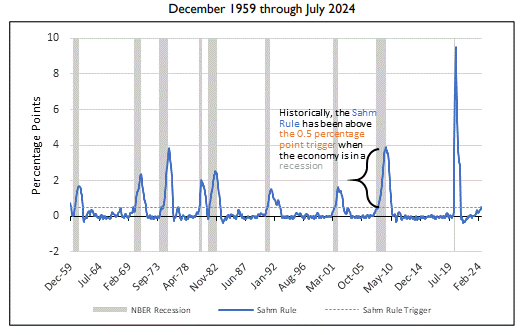

By early August, Japan’s stock market experienced a historic decline. It was partly triggered by concerns over the BOJ’s hawkish stance — a stance advocating immediate, vigorous action — and a hard slowdown in the US economy predicted by the Sahm Rule. Yet a soft landing was also predicted, as the US economy is currently strong. The decline caused political sentiment in Nagatachō — the district in Tokyo where the prime minister resides — to shift.

The Salm Rule observes the unemployment rate over the past 12 months to identify economic struggle; if the rate increases by half a percent or more in a three-month period, the rule is triggered. This usually happens at the start of a recession. Via Federal Reserve Bank of St. Louis.

Ishiba is expected to uphold the principle of central bank independence, a cornerstone of sound monetary policy as exemplified by institutions like the US Federal Reserve (or the Fed). By maintaining the BOJ’s autonomy, economists evaluate that Ishiba will allow Governor Kazuo Ueda the space needed to pursue further rate normalization, which will enhance Japan’s economic stability.

Ishiba emphasized that the government is in no position to direct monetary policy. However, he expressed his expectations that Japan’s economy will continue to progress sustainably under the BOJ’s accommodative stance, ultimately eradicating deflation. He underscored the importance of maintaining close collaboration with the central bank to observe market trends calmly and cautiously, while engaging in careful communication with market participants.

Advertisement

Prior to the prime minister’s remarks, Ueda indicated that the BOJ is strongly supporting Japan’s economy through its highly accommodative monetary policy. Future adjustments to monetary easing are contingent on economic and inflationary developments aligning with BOJ projections. Regardless, Ueda noted that there is ample time to evaluate these conditions, and the BOJ will proceed carefully.

Ueda further clarified that there were no specific requests made by the prime minister regarding monetary policy. Additionally, the joint 2013 accord between the government and the BOJ, prioritizing the early elimination of deflation and sustainable economic growth, was not part of their discussion.

Takaichi’s opposition to monetary tightening

Ishiba plans to appoint former Chief Cabinet Secretary Katsunobu Kato as Minister of Finance. Kato, who is a former member of the Ministry of Finance, was first elected to the House of Representatives in the 2003 general election. He served as Deputy Chief Cabinet Secretary during the Abe administration and championed the continuation of Abe’s economic policy, “Abenomics,” during the party presidential election. As always, this is the mysterious LDP way of saying, “inadequate knowledge and strategies can lead to harm.”

Sanae Takaichi, another strong conservative-leadership contender from the House of Representatives, is a staunch advocate of continued monetary easing. She has publicly opposed the BOJ’s rate hikes. During a recent online discussion, she argued that tightening monetary policy at this juncture would be premature, calling it “foolish.” Takaichi’s stance has raised fears about potential political interference in the central bank’s operations, reminiscent of certain US political figures like former President Donald Trump, who seeks to exert control over the Fed.

Advertisement

Meanwhile, some observers worry about having a repeat of the United Kingdom’s experience in 2022: The government of then-UK Prime Minister Liz Truss employed aggressive fiscal expansion which, compounded by concurrent rate hikes by the Bank of England, led to sharp currency depreciation and a surge in interest rates. Observers caution Japan to avoid a similar scenario, where ill-considered political statements trigger a destabilizing “Truss shock.” Indeed, Takaichi’s remarks have already contributed to volatility in the foreign exchange market, causing fluctuations in the US dollar/Japanese yen rate.

The yen depreciated from 143,000 to 146,000 following Takaichi’s rally, reversing the earlier appreciation from 146,000 to 142,000 that occurred after Ishiba’s selection. Via TradingView

Ishiba envisions the creation of an “Asian NATO” as essential for securing robust regional deterrence, with serious consideration of nuclear sharing with the US. He also desires a revision of the US–Japan Status of Forces Agreement, addressing concerns related to jurisdiction, environmental protection and the balance of legal authority between both nations over military activities and personnel.

In line with this strategic vision, it appears that he is willing to prioritize short-term economic gains over central bank independence. This signals a potential shift in his economic approach moving forward.

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

As Wall Street frets over the looming US presidential election, the giant asset managers are also looking at other ballot box issues: those of their investors.

Bludgeoned for the past two years by US Republicans alleging political wokeism, BlackRock, State Street and Vanguard are now gradually offering investors the chance to vote at companies’ annual shareholder meetings. This marks a significant shift as investors historically have relied on asset managers to vote for them on issues such as board directors, executive pay and various shareholder petitions.

Advertisement

BlackRock chief executive Larry Fink says the change will strengthen “shareholder democracy”. The firm now offers pass-through voting in more than 650 global funds totalling $2.6tn in equity assets. On October 15, State Street is starting a pilot programme that opens its first European exchange-traded fund for voting choice. And in the months ahead, Vanguard is looking to expand its voting programme that launched last year, the firm has said.

Such moves might help asset managers avert some of the criticism that has come their way as shareholder voting became intertwined with battles over issues such as climate change or workplace diversity. But voting choice is not a panacea for them.

Asset managers have typically relied on voting policies developed by proxy voting agencies, in particular the dominant duo Institutional Investors Services and Glass Lewis. And now investors at the big asset managers are being given the opportunity to vote in line with a choice of one of the thematic policies developed by the agencies.

Some curious differences in voting policies might make proxy agencies and asset managers open to more scrutiny. For example, the agencies offer Catholic faith-based voting policies with very different outcomes. When it comes to voting for board directors, ISS’s Catholic policy is stricter. The policy recommended voting against board directors in the S&P 500 index a whopping 77 per cent of the time. By contrast, Glass Lewis’s Catholic policy is more merciful. It recommended objecting to less than a quarter of S&P 500 board directors.

Advertisement

How could ISS and Glass Lewis come to such different outcomes based on the same religious faith?

ISS has built its Catholic voting screen in part from the US bishops policies, and considers voting against directors if a company does not have 40 per cent of its board from “under-represented gender identities”. Glass Lewis’s Catholic policy has a lower requirement of 20 per cent of board directors to be women.

“These things are not binary, black-and-white approaches. It is a bit more of a spectrum of approaches,” says John Wieck, chief operating officer at Glass Lewis. “There will certainly be a fair amount of overlap. But there could be differences,” as there are between the two advisers’ benchmark voting policies.

Such divergence is apparent elsewhere too. Shareholder advisers also offer a policy for public pension funds. The ISS pension policy supported 80 per cent of all environmental and social shareholder resolutions. But Glass Lewis’s policy supported just 40 per cent of environmental and social issues.

Advertisement

Asset managers have been hesitant to say which investors are using various voting policies, or which ones are most popular. Vanguard said last month nearly half of investors offered voting choices simply deferred to Vanguard’s voting policy as usual. BlackRock says investors holding less than a quarter of the $2.6tn of assets available for voting choice have taken advantage of the programme.

Still, voting choice should prompt companies to think differently about their investor relations, says Georgia Stewart, chief executive at Tumelo, a provider of shareholder voting technology, Historically, companies simply needed to communicate with their institutional investors. But shareholder voting is starting to splinter in ways that investor relations departments have not appreciated yet, she says.

Voting choice also finally gives investors who prioritise environmental, social and governance issues a chance to take a stronger line with their votes. Some have felt frustrated that many ESG funds have shown a long reluctance to support environmental and social shareholder proposals in votes. Companies might now face more support for such resolutions.

“We are heading to an era where the end investors’ choice is king,” says Lindsey Stewart, director of stewardship research at Morningstar. Still, voting choice is unlikely to end the political problems for asset managers, ISS and Glass Lewis. Stewart adds: “A lot of political individuals and groups have these organisations in their crosshairs and I don’t think they are going to let go anytime soon.”

Mr Bailey said that if inflation remains in check the Bank might be able to be “more activist” over reducing borrowing costs.

The comments have led several experts to bring forward predictions for interest rate cuts.

British interest rates currently sit at 5%. The rate – which is used by banks to determine the interest on mortgages and loans – was reduced from 5.25% in August.

READ MORE ON BANK OF ENGLAND

Members of the Bank’s Monetary Policy Committee (MPC) voted to keep rates at 5% at the latest vote in September, but economists are currently pricing in another reduction at next month’s meeting.

Advertisement

Gabriel McKeown, head of macroeconomics at Sad Rabbit Investments said: “Governor Bailey’s bombshell comments have opened the floodgates to more aggressive rate cuts, with the prospect of sub-3% mortgages, once dismissed as a pipe dream, now emerging as a tantalising possibility for homeowners.

“These views significantly depart from earlier comments advocating for gradual rate reductions, leading swap rates to fall sharply.

“Markets are now pricing in an all but certain chance of a rate cut at the Bank’s next meeting in November.”

He added that the prospect of reduced borrowing costs and increased competition in the mortgage market should help drive the rate-slashing momentum towards the end of 2024.

Advertisement

Elsewhere, Adam Stiles managing director at Helix Financial Partners pointed out that Skipton Building Society is already offering a sub-3% product transfer mortgage at 2.89% – although it comes with a hefty 3% fee and is up to 60% loan-to-value.

Best schemes for first-time buyers

Mr Stiles told The Sun: “If the Bank of England delivers one more rate cut, which seems likely after Andrew Bailey’s hints this week, that could quickly feed through into swap rates, which determine lenders’ fixed rates.

“However, we are only likely to see sub-3% rates at lower loan-to-values. We don’t expect to see them widespread at higher loan-to-values until we have a few more rate cuts, which is possible by mid-2025.”

Dariusz Karpowicz, who is director at Albion Financial Advice, said that it’s not “unrealistic” that we’ll see rates drop below 3%.

Advertisement

He said: “All the signs point to it – some rates below 3%! Swap rates are falling, and Andrew Bailey is hinting at a potential decrease. The economic outlook is improving, and lenders are already trimming rates almost every week.

“It’s not unrealistic to see rates dipping below 3% for lower LTVs before year’s end. Of course, only an unexpected ‘black swan’ event could derail this positive momentum.”

What is happening to swap rates?

A swap rate is a rate based on what the markets think interest rates will be in the future.

If the rates rise, then mortgage lenders will look to increase their rates so that they don’t lose out.

Advertisement

The BoE comments have had a “positive” impact on swap rates.

A number of lenders have already announced repricing and more are expected to follow suit, according to mortgage broker SPF Private Clients.

Mark Harris, chief executive of mortgage broker SPF Private Clients, says: “A more aggressive approach to rate reductions has been welcomed by the markets, with swaps falling on the back of the Governor’s comments, which should feed through to even lower mortgage pricing.

“A number of lenders are already in the process of repricing – Coventry [building society]’s two and five-year fixes which top the best buy tables at 3.89 and 3.69% respectively are being pulled tonight, while HSBC is repricing downwards today and NatWest and Barclays are repricing tomorrow.

Advertisement

“Santander is also repricing tomorrow and is likely to top the ‘best buys’ with its new deals – a two-year purchase option at 3.84% for those borrowing 60% loan-to-value and a five-year fix at 3.68%, also at 60% LTV.”

He said the ongoing rate war among lenders is “great news” for borrowers as there are some “really compelling” deals being launched, which will go some way to helping affordability.

Different types of mortgages

We break down all you need to know about mortgages and what categories they fall into.

A fixed rate mortgage provides an interest rate that remains the same for an agreed period such as two, five or even 10 years.

Advertisement

Your monthly repayments would remain the same for the whole deal period.

There are a few different types of variable mortgages and, as the name suggests, the rates can change.

A tracker mortgage sets your rate a certain percentage above or below an external benchmark.

This is usually the Bank of England base rate or a bank may have its figure.

Advertisement

If the base rate rises, so will your mortgage but if it drops then your monthly repayments will be reduced.

A standard variable rate (SVR) is a default rate offered by banks. You usually revert to this at the end of a fixed deal term, unless you get a new one.

SVRs are generally higher than other types of mortgage, so if you’re on one then you’re likely to be paying more than you need to.

Variable rate mortgages often don’t have exit fees while a fixed rate could do.

Advertisement

What are lenders doing?

This week five more mortgage lenders have announced cuts to mortgage rates.

Barclays, HSBC, Halifax, Santander and NatWest are all making several rate reductions across a range of mortgage deals.

Since the beginning of July, the lowest five-year fixed rate mortgage has fallen from 4.28% to 3.69%.

Advertisement

Elsewhere, the lowest two-year fix has fallen from 4.68% to 3.89%.

Barclays was first off the bat, announcing cuts that mainly affect first-time buyers and home movers, including some sub-4% deals for borrowers with the biggest deposits.

Its lowest two-year fix for buyers with a 40% deposit or more fell to 3.99% from today.

HSBC has implemented another wave of mortgage rate cuts.

Advertisement

It says all its residential and buy-to-let deals have now been reduced by up to 0.16 percentage points.

HSBC confirmed its two-year and five-year fixed mortgages for both home movers and first-time-buyers have been cut by up to 0.25 percentage points.

Its lowest five-year fix for those remortgaging with at least a 40% equity is now priced at 3.83%.

Halifax was next up to announce a cut taking place from today.

Advertisement

The UK’s biggest lender cut mortgage rates on selected products by up to 0.11 percentage points for home movers and first-time buyers.

Halifax also confirmed reductions of up to 0.24 percentage points for homeowners due to remortgage.

Santander and NatWest also announced a wide range of range cuts for today.

Santander’s fixed-rate deals dropped by 0.29 percentage points for home buyers and those remortgaging.

Advertisement

It means Santander now offers the lowest five-year fix on the market for home buyers purchasing with the biggest deposits.

All its mortgage rates for new build purchases are also reducing by up to 0.19% alongside all its buy-to-let fixed rates, which are dropping by up to 0.17%

Meanwhile, NatWest is also executing some healthy cuts across fixed-rate deals aimed at home buyers and remortgagers.

How to get the best deal on your mortgage

Advertisement

IF you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

If you’re remortgaging and your loan-to-value ratio (LTV) has changed, you’ll get access to better rates than before.

Advertisement

Your LTV will go down if your outstanding mortgage is lower and/or your home’s value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you’re nearing the end of a fixed deal soon it’s worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Advertisement

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Advertisement

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You’ll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you’ll pay interest on it and so will cost more in the long term.

Remember you’ll have to pass the lender’s strict eligibility criteria too, which will include affordability checks and looking at your credit file.

You may also need to provide documents such as utility bills, proof of benefits, your last three month’s payslips, passports and bank statements.

Does everyone agree sub-3% deals are looming?

In short, no. Not everyone agrees that these -3% deals are on the way.

This is largely due to positive moves being scuppered by global events and the fact that interest rates are notoriously hard to predict.

Advertisement

Not to mention that Labour’s first Budget is just a few weeks away.

Jack Tutton, director at SJ Mortgages told us: “If the pace of rate reductions that we are currently enjoying continues until the end of the year, sub-3% rates would be a real possibility.

“However, there are many things that could derail this optimism. The Autumn Budget will be the biggest hurdle. The decisions that the Chancellor takes will be a make-or-break moment for interest rates.”

Meanwhile, Elliott Culley, who is the director at Switch Mortgage Finance, says he believes there is a “slim” chance of rates hitting below 3%.

Advertisement

He said: “It would be a huge turnaround if mortgage rates were to fall below 3% by the end of the year.

“However, I would expect the chances of this happening being slim based on current domestic and world events.”

Others are pretty certain this will not be the case.

“With all the uncertainty ahead of the upcoming Budget, there is more chance of Bruno Fernandes getting Player of the Month than rates returning to sub-3%,” David Stirling Independent Financial Advisor at Mint Mortgages & Protection said.

Advertisement

“With Middle East issues escalating and causing volatility in oil prices as we enter winter, added to the potential tax hardships to come, it’s hard to see rates normalising below 3% this year.”

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

You must be logged in to post a comment Login