In the GB News Pensions and Retirement Q&A, Jasmine Birtles answers questions from GB News members. You can email your question to money@gbnews.uk.

Question:Hi. My husband died 20 years ago and I get a 50 per cent payment of his pension. What does it mean that inherited pensions now come into the inheritance tax (IHT) bracket?

Jasmine replies: You are referring, of course, to the announcement made by Chancellor Rachel Reeves in the latest Budget where she said that private pensions will be subject to inheritance tax from April 6, 2027.

This change reverses the 2015 decision by George Osborne to exempt pension pots from IHT. Currently, private pensions are not considered part of a deceased person’s “estate” and are free from inheritance tax.

But from 2027, pensions will be treated as part of the estate, and heirs may be liable for IHT if the addition of the pension pot pushes the value of the estate over the threshold for paying IHT.

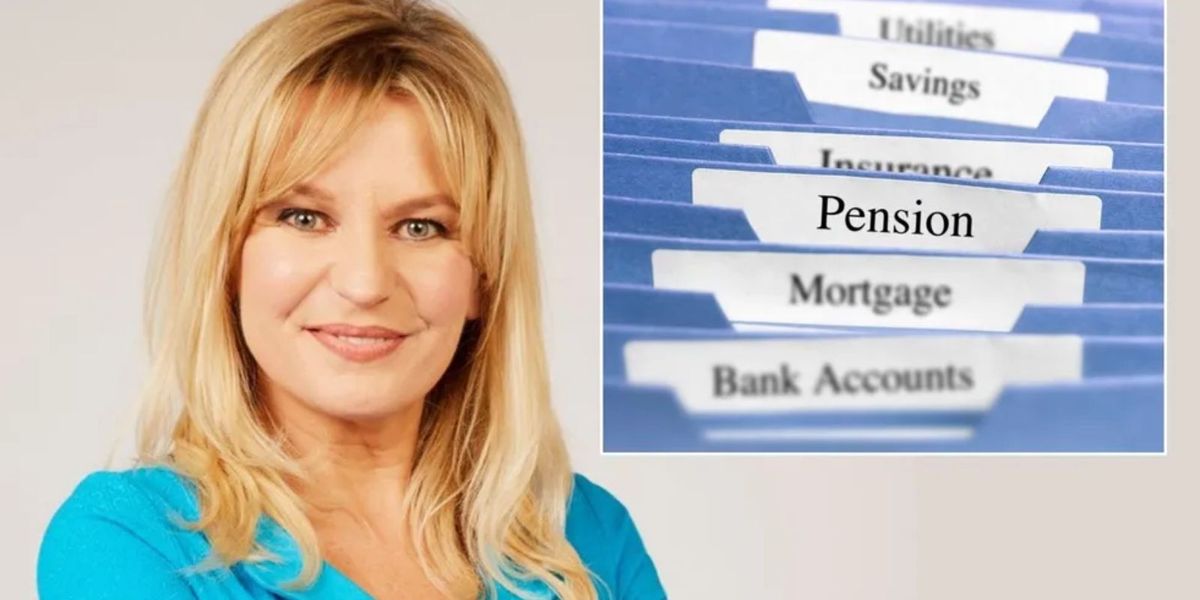

Jasmine Birtles answers questions from GB News members in the exclusive pensions and retirement Q&A

JASMINE BIRTLES | GETTY

However, married couples will still be able to inherit assets from each other free of inheritance tax, including unused portions of their nil-rate bands.

However, your query is specifically to do with the pension payments that you are receiving from your husband’s own pension.

That is a different thing as Robert Seller, Director of the tax and business advisory firm, Blick Rothernberg, explained.

He said: “From the information provided, it would appear clear that she is actually receiving a pension annuity. This is linked to her husband’s previous employment.

“The Government’s proposed new rules on inheritance tax do not capture this type of income or funds are otherwise ‘drawn down’ from the pension fund by the taxpayer.

“Rather, the new IHT rules are designed to specifically capture ‘uncrystallized pension funds’. For example, these are sums which remain in someone’s pension fund at death.

“In effect, the Government’s changes innately target money purchase DC (defined contribution) pension funds, as final salary/defined contribution (DC) arrangements are not innately linked to any specific ‘pot-of-money’ in the way that someone’s savings in a DC fund are.

“[These] cannot therefore be passed on to one’s children or grandchildren in the way that unused DC savings have been. Before the proposed changes were announced, it was possible to transfer the pension savings which remained in one’s pension fund to children or grandchildren on a tax-free basis in many cases.

“This is on the basis that the fund did not count as part of someone’s estate upon death, even though the children or grandchildren were benefitting from these savings.”

I also spoke to Mike Ambery, the Retirement Savings director at Phoenix Group’s Standard Life, who said: “I’m so sorry to hear of your husband’s passing. Please don’t worry, there should be no change to the payment you receive from your husband’s pension.

“Based on our understanding, the changes announced at the Autumn Budget refer to unspent pension pots, which are set to become liable for inheritance tax from 2027.

“It sounds like you are receiving a spousal benefit from your husband’s DC pension, which would not be liable. Assets passed between spouses are also generally exempt from IHT, regardless of the value of the estate. This is known as the ‘spousal exemption’.”

Jasmine Birtles is a personal finance expert, TV and radio presenter and author of 38 books. Her website, MoneyMagpie.com, covers all aspects of personal finance from money-saving and money-making ideas to investment and pensions information. She is a keynote speaker at conferences around the world.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

+ There are no comments

Add yours