Crypto World

Arthur Hayes Deploys Net Liquidity Strategy: Not Buying BTC Now Even If He Has Only $1

Arthur Hayes has officially stopped buying Bitcoin ($BTC). The BitMEX co-founder says he will not deploy fresh capital until the Federal Reserve explicitly expands the money supply.

With Bitcoin struggling to break resistance, Hayes is tracking a specific “Net Liquidity” metric that suggests the current rally lacks fundamental fuel.

He is waiting for the centralized banking cartel to restart the money printer before chasing the market any higher.

Discover: The best pre-launch crypto sales

Why Arthur Hayes Is Slamming the Brakes on Bitcoin

Hayes’s hesitation stems from his Net Liquidity framework, a formula that subtracts the Treasury General Account (TGA) and Reverse Repo (RRP) balances from the Fed’s total balance sheet.

While nominal prices are high, real dollar liquidity has not expanded enough to support a sustained breakout above $90,000. Hayes views the current market as a trap for traders expecting a straight line up.

“If I had $1 to invest right now, would I be putting it into Bitcoin? No. I would wait,” Hayes said on a podcast. He argues that while geopolitical tensions usually drive safe-haven assets, the only thing that truly matters for Macro Crypto cycles is fiat debasement.

This thesis is reinforced by market data showing Bitcoin decoupling from traditional bond yields, a divergence that historically signals impending volatility.

Hayes warns that without an immediate pivot back to Quantitative Easing, the “American war machine” alone cannot sustain asset prices. He believes the market is pricing in liquidity that hasn’t arrived yet. If the Fed refuses to loosen its monetary policy, Hayes predicts the current chop could move downwards.

He is positioning for a scenario where the TGA drains slowly, leaving risk assets starved for capital in the short term. Only when the printing press whirs to life will the Net Liquidity conditions turn green for aggressive accumulation.

The Levels to Watch for Bitcoin

Bitcoin Price Analysis currently shows a market caught between institutional accumulation and macro exhaustion. Bitcoin is trading under the $90,000 psychological ceiling, a level that has rejected bulls multiple times. Hayes suggests that a failure here could trigger a slide toward $60,000, flushing out late longs.

$60,000 is the level that matters most. If price action breaks below this support, Hayes anticipates a “massive sell-off” driven by cascading liquidations. Concurrently, Wall Street is buying Bitcoin strategically but is not yet invested enough to chase breakouts unconditionally.

Conversely, the bull case requires a definitive reclaim of $90,000 on high volume. If spot buyers can push through this resistance, the path to $100,000 opens up quickly, invalidating the bearish liquidity thesis.

Traders looking for confirmation might look at simple math that nailed the last BTC bottom to identify safe entry points if Hayes’ predicted dip materializes.

If Net Liquidity remains flat, Bitcoin likely ranges sideways or bleeds slowly. But if the Fed is forced to cut rates due to external shocks, the $90,000 cap will likely shatter overnight.

Discover: The best new cryptocurrencies

The post Arthur Hayes Deploys Net Liquidity Strategy: Not Buying BTC Now Even If He Has Only $1 appeared first on Cryptonews.

Marex’s Nvidia‑linked “prediction market bond” pays 7% if NVDA stays the world’s most valuable company for a year, wrapping Polymarket‑style odds into principal‑protected credit.

Summary

- Marex issues a bond-like note that pays a 7% coupon if Nvidia remains the world’s most valuable company in one year while returning principal if it does not.

- The structure mirrors a principal‑protected structured note, shifting prediction‑market style bets into regulated credit markets with Marex as issuer and credit risk.

- The deal comes as prediction markets like Polymarket see institutional capital inflows and Nvidia’s market cap hovers around $4.3 trillion, cementing its role at the center of the AI trade.

Marex Group has created and sold what it calls the first “prediction market bond,” a structured note that pays a 7% annual coupon in $ if Nvidia Corp. is still the world’s largest company by market value in one year, and simply returns principal if it is not. London‑based Marex is marketing the instrument to institutional clients as a way to express views typically traded on event‑driven platforms such as Kalshi and Polymarket, but without the all‑or‑nothing loss profile of traditional prediction markets. According to Bloomberg, the payoff hinges on a single observable outcome: Nvidia’s standing in the global equity league table at maturity, with investors exposed primarily to Marex’s own credit risk rather than direct equity downside.

The structure blends a zero‑coupon bond with an embedded derivative replicating the odds implied by event markets and options desks, effectively “gambling the yield” while preserving principal, as several market commentators on X noted. One user, @trevorlasn, summarized the economics bluntly: “you get 7% upside with principal protection? that’s just a structured note with better marketing lol,” while @StephGuildNYC asked, “Isn’t this just a principal protected structured note? They’ve been around for ages.”

Another commentator, @JamesChristoph, cautioned that “the risk reward here sounds good, but the payoff is quite bad,” echoing longstanding criticism that structured notes often favor issuers over buyers. In a separate X thread, @MickBransfield framed the deal more expansively: “marex issued a bond that pays 7% if nvidia stays the world’s largest company for a year. prediction markets just got a prospectus.”

Nvidia, currently valued at roughly $4.3 trillion in market capitalization, sits at the center of the global AI trade and remains the world’s most valuable listed company by a margin of more than $400 billion over Apple, according to recent market data. The note’s 7% $ coupon effectively prices the probability that Nvidia can retain that top slot for another year, a question that has been actively traded on on‑chain prediction venues as investors debate how far the AI cycle can run. Those venues have grown rapidly: Polymarket alone saw about $12 billion in trading volume in January 2026, generating over $11 million in on‑chain fees as users speculated on politics, commodities, and crypto prices. Intercontinental Exchange, parent of the New York Stock Exchange, has committed $2 billion to the sector, including a fresh $600 million investment in Polymarket, underscoring how event contracts are bleeding into mainstream market infrastructure. In a recent crypto.news story on Polymarket’s integration with Solana via Jupiter, prediction markets were described as “expanding rapidly heading into 2026,” a backdrop that helps explain why Marex is now wrapping such outcomes into regulated credit products.

The Marex deal also lands as crypto‑native prediction markets deepen their ties to traditional assets, with Polymarket rolling out stock and commodity contracts powered by Pyth Network’s price feeds and centralized exchanges like Deepcoin integrating “event contracts” tied to macro and crypto outcomes. Another crypto.news story highlighted how Vitalik Buterin has deployed roughly $440,000 across Polymarket, booking about $70,000 profit by fading “crazy mode” tail‑risk bets, illustrating how sophisticated traders already treat these markets as yield‑like instruments rather than pure gambling. Against that backdrop, Marex’s bond can be read less as a one‑off curiosity and more as an explicit bridge between on‑chain event speculation and off‑chain structured credit, one that denominates prediction risk in $ coupons instead of tokens.

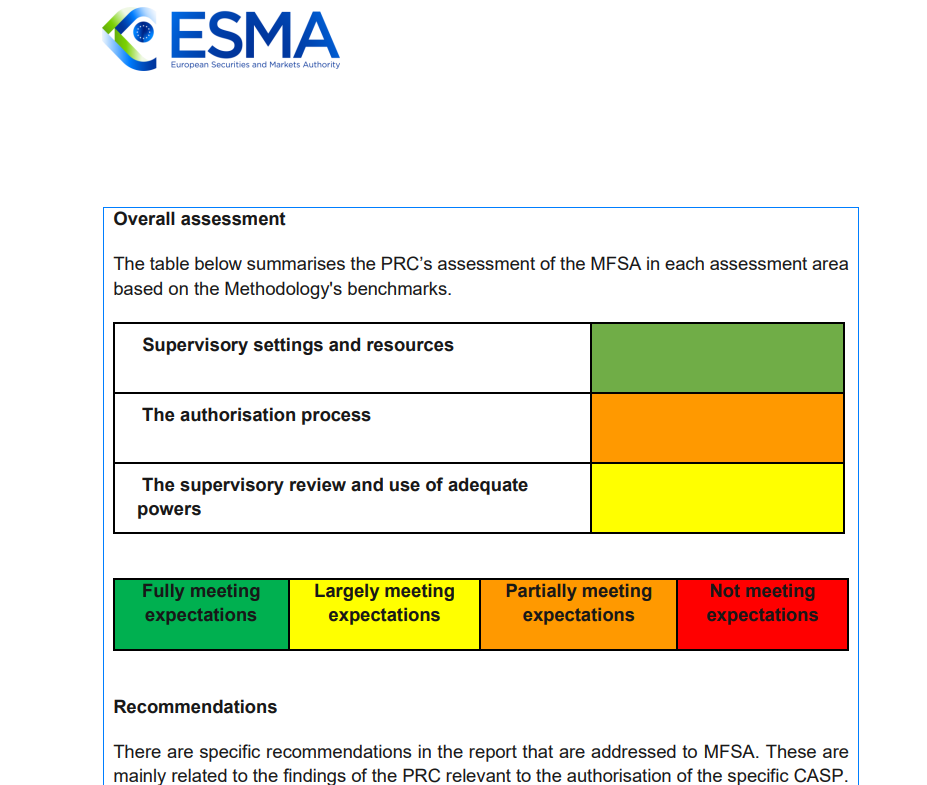

Europe’s next crypto battle is no longer about whether to regulate the industry, but who gets to hold the pen. European Union leaders are weighing a European Commission proposal to hand direct supervision of the bloc’s largest crypto asset service providers (CASPs) to the Paris-based European Securities and Markets Authority (ESMA), shifting front-line control away from national regulators.

France, Austria and Italy believe the move is overdue. In a joint September 2025 paper, their market authorities called for “a stronger European framework,” arguing centralized oversight is needed to address “major differences” in how countries authorize firms and curb regulatory shopping.

Malta’s Financial Services Authority (MFSA) is not convinced. A spokesperson told Cointelegraph it is “premature to introduce structural changes” like centralized supervision. The Markets in Crypto Assets Regulation (MiCA) regulation has only recently become fully applicable, and its “impact on the market and market players is still being assessed,” they said.

The dispute matters because MiCA lets companies win authorization in one member state and then passport services across the EU. That means the question of who supervises crypto firms is no longer just administrative, but goes to how Europe will balance market integration, investor protection and national regulatory authority.

While a recent Bloomberg report framed the fight as one small state against the commission, Ian Gauci of Maltese law firm GTG, one of the architects of Malta’s original crypto rulebook, told Cointelegraph, “That is not what this is.” He said Malta’s arguments “are not jurisdictional” and “go to the structure itself and how it will behave wherever it is applied in the Union.” The MFSA said its position was not about national advantage but about “regulatory timing and effectiveness” and preserving Europe’s attractiveness to crypto firms.

Related: What happens as Europe enforces MiCA and the US delays crypto rules

Centralizing supervision under one roof

The ESMA already leads the supervisory convergence work, coordinating peer reviews of national authorities, including a fast-track review of one of Malta’s CASP authorizations, widely reported to be OKX. The review found Malta met expectations on supervisory settings, but that the firm’s authorization “should have been more thorough.”

Supporters of centralization say that the episode makes the case. A spokesperson from the ESMA told Cointelegraph that a single supervisor for major cross-border companies would deliver “more efficient and harmonized supervision,” strengthen investor protection and reduce “the risk of forum shopping.” France, Austria and Italy similarly warned in their position paper that divergent practices could undermine investor protection and Europe’s digital asset market.

Gauci said he was not opposed to a stronger EU-level role where it is justified. But he argued that centralization should be targeted at genuinely systemic cross-border firms with clearly identified risks, rather than applied as a blanket fix for uneven supervision.

Malta warns centralization may go too far

OKX rejects the idea that companies pick smaller jurisdictions to capture regulators. Its European CEO, Erald Ghoos, told Cointelegraph that, unlike some competitors, the exchange had been supervised by Malta under a high-standard regime since 2021 and its MiCA authorization reflected a multi-year relationship, “not an expedited process.” With MiCA still rolling out, he argued that there was no evidence the current model is failing, making centralization look more like a “political decision.”

Related: What happens as Europe enforces MiCA and the US delays crypto rules

Ghoos said the case for concentrating supervisory power at the EU level had not yet been demonstrated.

Gauci accepts that inconsistencies exist but argues that the solution is to use existing tools. “Make peer reviews bite,” set timelines and impose consequences for persistent failure, rather than rewriting MiCA’s allocation of powers, he said.

His deeper concern is structural: Large firms operate as single systems, but the proposal would split oversight across ESMA, national authorities and the Anti-Money Laundering Authority (AMLA), while the Digital Operational Resilience Act (DORA) expects an integrated view of information technology risk. “Once you split supervision like this, that unity disappears,” he warned, leaving accountability fragmented in a crisis.

The real question, he said, is whether Europe values supervisory depth or scale. Early movers built expertise and proximity in a fast-moving industry; strip that away too quickly, and Europe risks replacing it with distance, removing the “incentive for jurisdictions to invest in serious supervisory capacity in the first place,” and encouraging the offshore drift policymakers want to avoid.

Magazine: 6 weirdest devices people have used to mine Bitcoin and crypto

Crypto World

XRP Price Prediction: Goldman Sachs Holds $153M in XRP ETFs While Pepeto’s 150x Presale Math Outpaces Every Large Cap Target

Goldman Sachs disclosed $153.8 million in spot XRP ETFs across four funds, making it the largest institutional XRP ETF holder at 73% of all disclosed positions combined, according to TheCCPress. The position sits inside a broader $2.36 billion crypto portfolio spanning BTC, ETH, XRP, and SOL.

The xrp price prediction turned bullish, but the wallets that built generational crypto wealth never did it watching a large cap grind from $1.31 to $4. They found the presale where the math worked and committed before the window sealed. That is Pepeto right now.

Goldman spread its position evenly across Bitwise, Franklin Templeton, Grayscale, and 21Shares, according to 24/7 Wall St. The May 13F will reveal whether the bank held through XRP’s 40% Q1 decline.

For the xrp price prediction, Goldman’s conviction is structurally bullish. But accumulating a regulated wrapper around an established coin delivers exposure, not the multiplier distance a presale to listing event creates.

XRP Price Prediction and the Best Exchange Presale of 2026

Pepeto

By the time most people hear about a token, the early multiplier is gone. Pepeto flips that timeline, placing the reader inside the presale before the Binance listing creates the gap everyone else chases.

Goldman holding $153 million validates the xrp price prediction, but generational crypto portfolios were built during presales where the founder had proven the thesis, the product was live, and the cost sat at fractions of a cent. Pepeto checks all three.

The project is a complete exchange from the architect behind Pepe’s $11 billion run on a 420 trillion supply with zero shipped features. PepetoSwap processes every trade at zero cost, and the bridge routes assets across Ethereum, BNB Chain, and Solana without gas.

SolidProof cleared every contract before the first commitment, a former Binance executive directs exchange operations, and 189% APY staking compounds daily for every wallet inside. $8.64 million flowing in at a Fear and Greed reading of 8 tells you who is committing: addresses that verified the codebase and modeled the listing before deploying.

The cofounder’s previous project reached $11 billion on a 420 trillion supply without a single working tool. Covering the distance between $0.0000001862 and that valuation is 150x, and the live infrastructure underneath makes the old ceiling look like the starting point. Every presale round that closes brings the Binance order book closer, and the addresses filling positions today did not commit without running the arithmetic first.

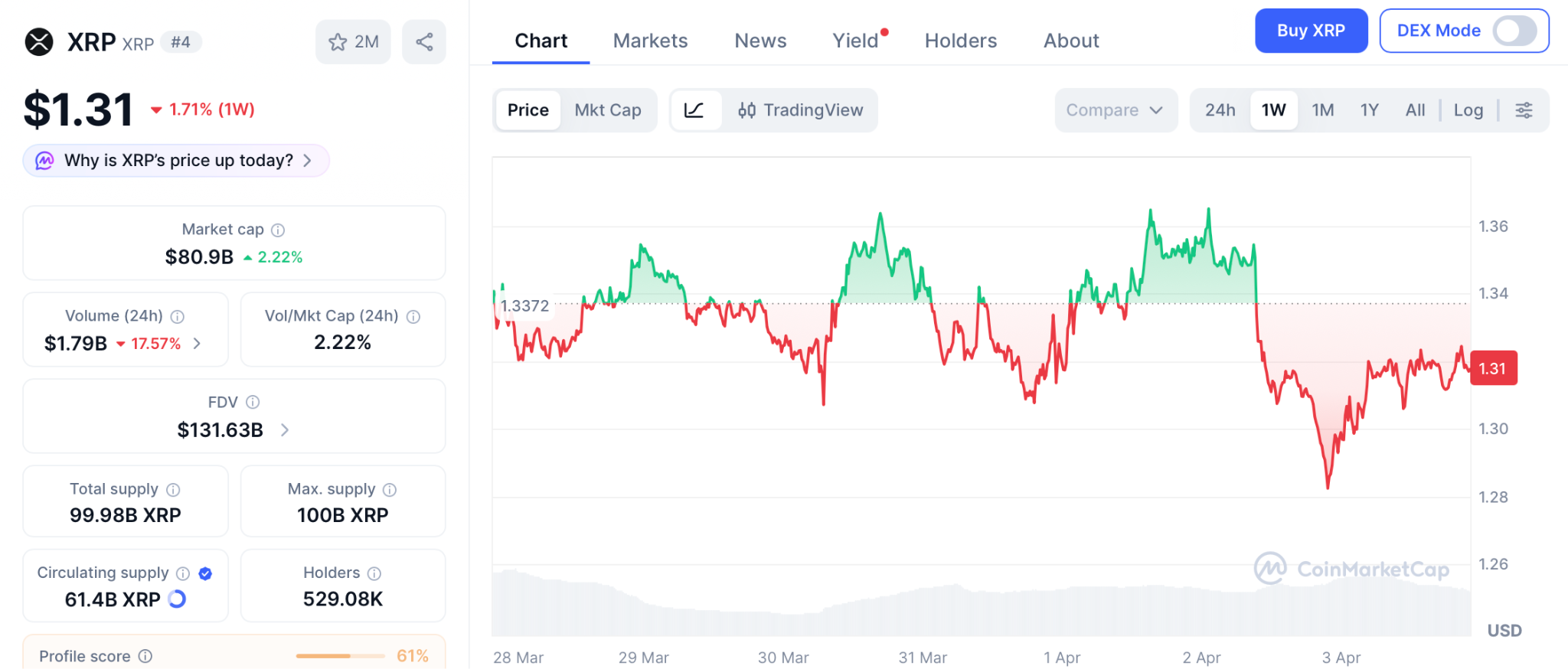

XRP

XRP trades at $1.31 on April 2 according to CoinMarketCap, down 30% year to date despite Goldman’s position and $1.44 billion in cumulative ETF inflows. The xrp price prediction hinges on the CLARITY Act advancing through the Senate Banking Committee in late April.

A breakout above $1.45 opens $1.80, roughly 37%. For holders, that is a welcome recovery. But the xrp price prediction math from $1.31 does not compare to a presale targeting the market cap the same cofounder already achieved.

Solana (SOL)

SOL sits at $79.81 on April 2 according to CoinMarketCap, pressured by the Drift exploit. Even a return to the $260 all time high is roughly 3.3x. The gap between that and presale to listing math is where portfolios diverge permanently.

XRP Price Prediction Is Bullish but the Presale Math Tells a Different Story

The xrp price prediction will unfold over quarters as Goldman’s next 13F lands and the CLARITY Act works through Congress. Pepeto’s presale will not wait for either.

Right now, $8.64 million sits inside the presale from wallets that moved during a Fear and Greed reading of 8. Those addresses are not guessing. They modeled the listing, verified the audit, and committed while the rest of the market was frozen. Every day that passes, the Binance listing gets one day closer and the presale gets one day shorter. There is no mechanism to extend it, no second round after it closes, and no way to buy at $0.0000001862 once the exchange opens.

The xrp price prediction conversation will still be running when Pepeto holders are already sitting on their returns. That is not a warning. It is a calendar fact. The Pepeto official website is the only place left to act on it, and the number of hours remaining is smaller than most people assume.

Enter the Pepeto presale before the Binance listing removes today’s entry

FAQs

What is the xrp price prediction after Goldman’s disclosure?

Goldman’s $153 million XRP ETF position is structurally bullish, with targets near $2.20 if the CLARITY Act passes. Pepeto at $0.0000001862 offers 150x from presale to the market cap its cofounder already reached with Pepe.

How does Goldman’s position affect the xrp price prediction?

Institutional accumulation reduces long term downside risk, but the largest returns come from presale entries before a confirmed listing, not from regulated ETF wrappers around established coins.

Is Pepeto a stronger entry than XRP right now?

$8.64 million committed during extreme fear with audited contracts, a live exchange, and the founding mind behind an $11 billion meme project. Visit the Pepeto official website before the Binance listing seals the presale.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

In the latest interview with Cointelegraph, macro investor and former hedge fund manager James Lavish issued a stark warning to Bitcoin holders and global investors: markets may be pricing in a quick resolution to the Iran conflict — but if that assumption proves wrong, the consequences could be severe.

Lavish argued that if the conflict drags on and keeps pressure on oil prices, the result could be a fresh inflation shock, renewed fears of stagflation and a major repricing across global markets.

In his view, this scenario would put the Federal Reserve in an impossible position: unable to raise rates aggressively without risking recession, yet unable to cut rates due to persistent inflation.

That is where the conversation becomes especially relevant for Bitcoin (BTC). Lavish explains why Bitcoin has behaved differently from gold and equities in recent months, and why that relative resilience may not last in a true “correlation-to-one” panic event.

If markets suffer a deeper drawdown, he says, Bitcoin could fall another 10% to 20%, potentially revisiting the low $50,000 or even high $40,000 range.

And yet, Lavish is far from bearish in the long run.

One of the most compelling parts of the interview is his argument that such a sell-off would not destroy the Bitcoin thesis — it could actually create a major opportunity. He also explains why investors should avoid being either too levered or completely unexposed in a market driven by war headlines, bond stress and rapidly shifting expectations around Fed policy.

The interview also touches on safe haven investments, energy markets, Treasury yields and money printing.

If you want to understand how an experienced macro investor thinks about war risk, recession risk and Bitcoin’s next move, watch the full interview on our YouTube channel and don’t forget to subscribe!

This interview has been edited and condensed for clarity.

Gemini adds drag‑to‑modify tools to ActiveTrader, chasing speed‑focused traders even as GEMI stock trades well below its IPO price and users still complain about lag.

Summary

- Gemini’s ActiveTrader now lets users drag chart order lines and click “pills” to adjust price and size in real time.

- Tyler Winklevoss says the upgrade targets fast markets as Gemini stock trades under pressure post-IPO.

- The launch comes as Gemini’s GEMI shares lag Bitcoin’s rebound, raising questions about execution and product strategy.

Gemini has rolled out a new order modification feature for its ActiveTrader interface, allowing users to “drag order lines on charts to modify price and click order line pills to modify quantity,” according to co‑founder Tyler Winklevoss in a post on X. Winklevoss framed the update squarely around speed, telling followers that “markets move fast and you can too with @Gemini Active Trader,” alongside a short product demo video that had drawn roughly 29,400 views within hours of posting. The feature targets high‑frequency retail and professional users who need to adjust orders intraday without leaving the chart.

The enhancement builds on a broader Gemini push to make ActiveTrader more customizable, including earlier changes that let users drag and drop modules and activate a floating order form for chart‑centric workflows. On its support pages, Gemini notes that ActiveTrader already supports a full suite of market, limit, and advanced limit orders, including Immediate‑or‑Cancel (IOC), Fill‑or‑Kill (FOK), Maker‑or‑Cancel, and auction‑only instructions, in addition to stop‑limit functionality. By letting traders modify those orders directly from chart objects rather than static tickets, Gemini is closing the usability gap with established trading terminals that have long offered drag‑to‑adjust orders on price ladders and depth charts.

Early reactions on X highlight both enthusiasm and lingering pain points. “Fast moves fr,” wrote user @ZackD0x, while another former team member, @ignacio_ape, said the upgrade “brings me so much joy” and praised seeing ActiveTrader “continuing to grow even tho I’m no longer there.” Not all feedback was glowing: “Drag and drop is cool and all but I really just need the app to stop lagging during high volatility,” complained user @Steffan0xd, underscoring that execution reliability still matters more than interface polish when spreads blow out.

The product update lands as Gemini navigates a tougher market environment as a listed company. After a high‑profile Nasdaq debut in September 2025 that initially valued the exchange at about $4.4 billion, the firm’s GEMI stock has since fallen well below its IPO price, with Bloomberg reporting in February that Gemini “risks a hard landing” after a more than 40% plunge in Bitcoin and mounting operating losses. More recently, crypto.news reported that GEMI is trading below $6—down roughly 76% since the IPO—even as Bitcoin and Ethereum have rebounded, suggesting a growing decoupling between the exchange’s equity and the broader crypto rally.

That disconnect has forced the Winklevoss‑led platform to lean harder on product differentiation, rolling out features such as a self‑custody wallet, prediction markets and a more modular ActiveTrader interface in a bid to convert volatility into higher fee revenue. Whether the new drag‑to‑modify tools meaningfully move the needle will depend less on X engagement metrics and more on whether active traders actually route orders through Gemini instead of rival venues when the next leg of crypto volatility hits.

Bitcoin held above $67,000 on Good Friday as U.S. employers added 178,000 jobs in March — beating forecasts by a wide margin — while traditional markets sat closed for the Easter holiday, leaving crypto as the primary gauge of how investors are pricing the hawkish surprise.

Summary

- The U.S. added 178,000 nonfarm payrolls in March, well above consensus estimates, while unemployment fell to 4.3%, according to the Bureau of Labor Statistics.

- Bitcoin held above $67,000 on Good Friday with traditional markets closed, absorbing the hawkish macro signal with unusual composure.

- February’s payroll figure was simultaneously revised to a loss of 133,000 jobs, complicating the read on Fed policy going into Q2.

Bitcoin (BTC) held its footing above $67,000 on Good Friday, April 3, as the U.S. Bureau of Labor Statistics released a stronger-than-expected March jobs report that showed 178,000 nonfarm payrolls added last month — a figure that significantly exceeded consensus estimates of around 135,000. With traditional U.S. equity and bond markets closed for the Easter holiday, crypto was among the few liquid markets actively pricing in the data.

The BLS release, filed under code USDL-26-0580 and embargoed until 8:30 a.m. ET, showed the unemployment rate ticking down to 4.3% from 4.4% in February. At the same time, February’s payroll figure was sharply revised to a net loss of 133,000 jobs — a downward swing that softens the headline beat considerably and suggests the labor market has been weaker than previously reported entering 2026.

Bitcoin decouples — quietly

What stood out on Good Friday was what Bitcoin did not do. With stocks offline and macro traders watching from the sidelines, BTC held its ground rather than selling off on the hawkish implications of a strong jobs print. A 178,000-job print reduces the Federal Reserve’s urgency to cut rates, which typically pressures risk assets like crypto. But Bitcoin absorbed the signal without a meaningful downside.

That composure fits a pattern visible across recent weeks. As crypto.news has reported, Bitcoin has been trading primarily in response to geopolitical headlines around the ongoing U.S.–Iran conflict, with macro data playing a secondary role in near-term price discovery. The February jobs shock — when the economy shed 92,000 payrolls — had briefly pushed BTC below $70,000 before markets stabilized. Friday’s print delivered the opposite surprise, yet the price reaction was equally muted.

What this means for the Fed and crypto

“Relatively strong employment data means the Fed feels less pressure to reduce interest rates,” analysts at Bitfinex noted in a recent macro briefing. “It will likely remain laser-focused on inflation, which it sees as a major risk tied to Trump’s trade policy.” Higher rates tend to strengthen the dollar and weigh on Bitcoin ETF inflows — a dynamic that has shaped much of crypto’s performance in early 2026.

With U.S. markets closed until Monday, the full institutional reaction to Friday’s data will only become clear when equities reopen. Bitcoin’s ability to hold $67,000 through a holiday weekend — under both a strong jobs print and continued war risk from the Middle East — may offer early evidence that the asset is finding a floor.

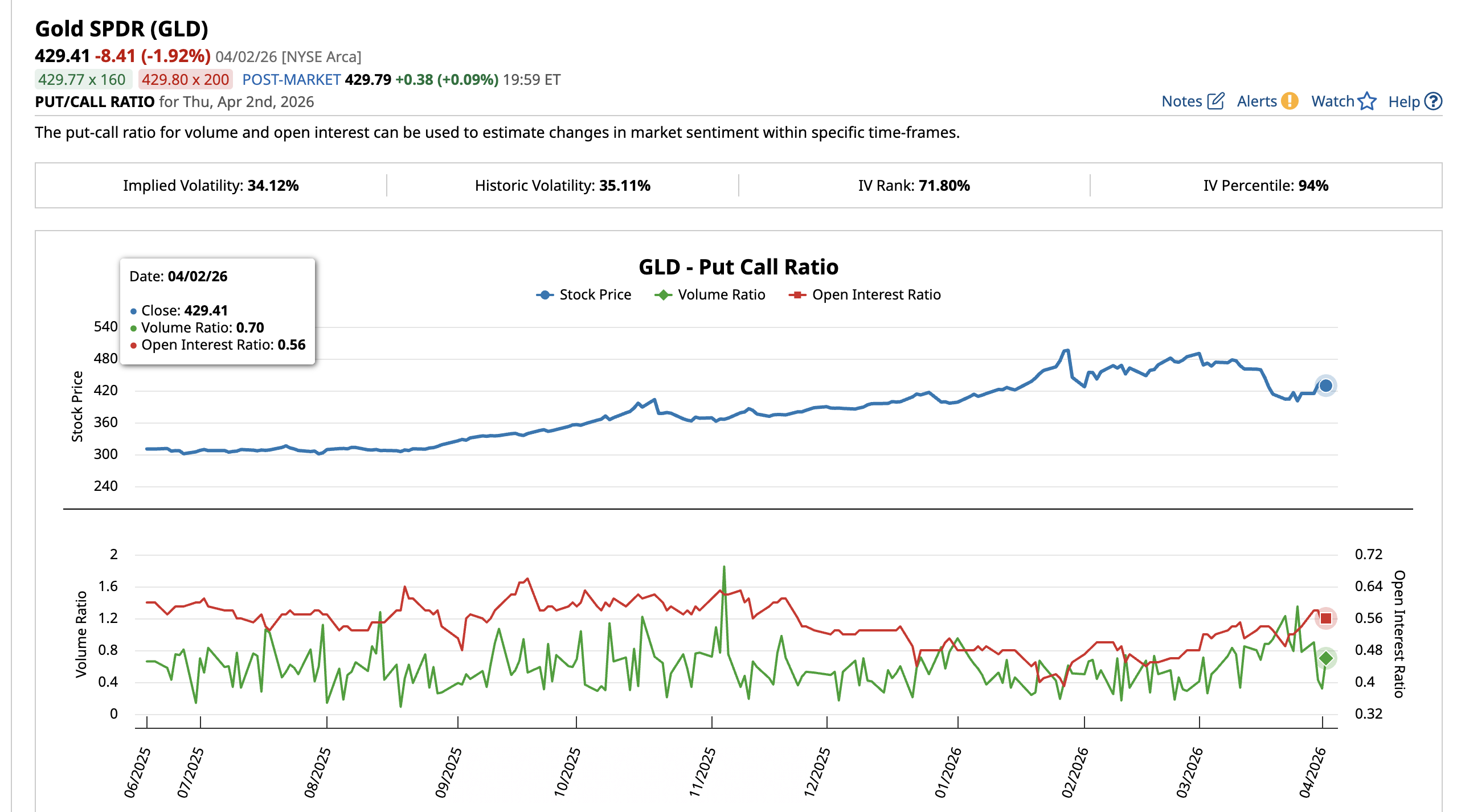

Gold (XAU/USD) price trades near $4,676 on April 3, up roughly 17% since touching a low of $4,105 on March 23. The rally looks convincing. However, a proprietary correlation metric, shifting options positioning, and a nuanced reading of the latest Commitment of Traders report suggest the current advance may be building on the wrong foundation.

Gold’s strongest rallies have historically begun after the metal decoupled from oil, not while both moved higher together. The 17% bounce is riding the same trade that preceded every correction this cycle, and a controlled dip that breaks that link could end up being more constructive than further upside.

Gold Is Rising but the Correlation That Matters Is Already Turning

Since March 23, gold price has been climbing inside an ascending channel on the 8-hour chart. The structure is not a bear flag, as the channel has extended beyond the typical duration, but it is also not confirmed bullish until the upper boundary breaks decisively.

The XAU-WTI Correlation Matrix, a BeInCrypto custom indicator that measures the 50-period rolling correlation between gold spot (OANDA:XAUUSD) and WTI crude oil (TVC:USOIL), currently reads -0.10. The reading has declined from the positive zone it occupied in March but seems to be rising again.

The pattern is consistent. In mid-October, the correlation dropped to around -0.88. and stayed negative through early November. That was when gold price launched its strongest rally. This shows that Gold performs best when it decouples from oil entirely, acting as an independent safe haven.

Every time the correlation peaked in positive territory, gold corrected. In late January, the reading hit approximately 0.85, and gold dropped over the following weeks. In early March, another positive peak aligned with the $5,422 high before the sell-off resumed.

The current -0.10 reading places the correlation in transition. The 17% bounce since March 23 happened during this transitional phase, which means it was partially driven by the same oil-linked sentiment rather than independent safe-haven demand.

This is why a controlled dip would be constructive. If gold price pulls back while oil continues to rise, the correlation would accelerate toward the -0.70 zone, exactly where gold has launched every sustained independent rally this cycle.

The rally does not need to continue to be bullish for gold. The correlation needs to finish resetting. Options traders have already begun reacting to the bounce, and their positioning reveals whether the current move has genuine conviction.

Bullish Bets Replaced Bearish Ones but the Foundation Is Reactive

The SPDR Gold Shares ETF (GLD) put-call ratio captures how options traders are positioning around gold price. On March 26, the put-call volume ratio stood at 1.35, meaning significantly more puts than calls were trading. Bearish sentiment dominated. The open interest ratio at the time was 0.53.

By April 2, the volume ratio had collapsed to 0.70 as call activity surged and put volume faded. The open interest ratio rose to 0.56, indicating new long positions were being opened. The bearish bets that dominated during the March sell-off have been replaced by fresh bullish exposure.

Traders likely responded to the 17% bounce by rotating from protective puts into directional calls. When bullish bets crowd in at the same time the oil correlation surges (current state), the newly opened long positions become vulnerable.

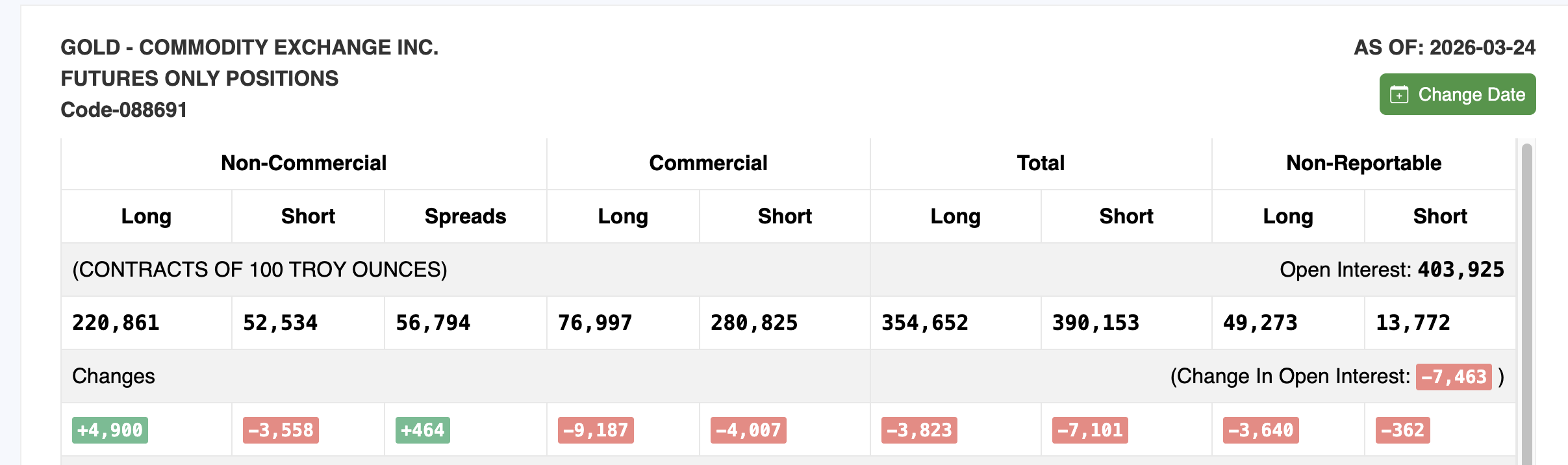

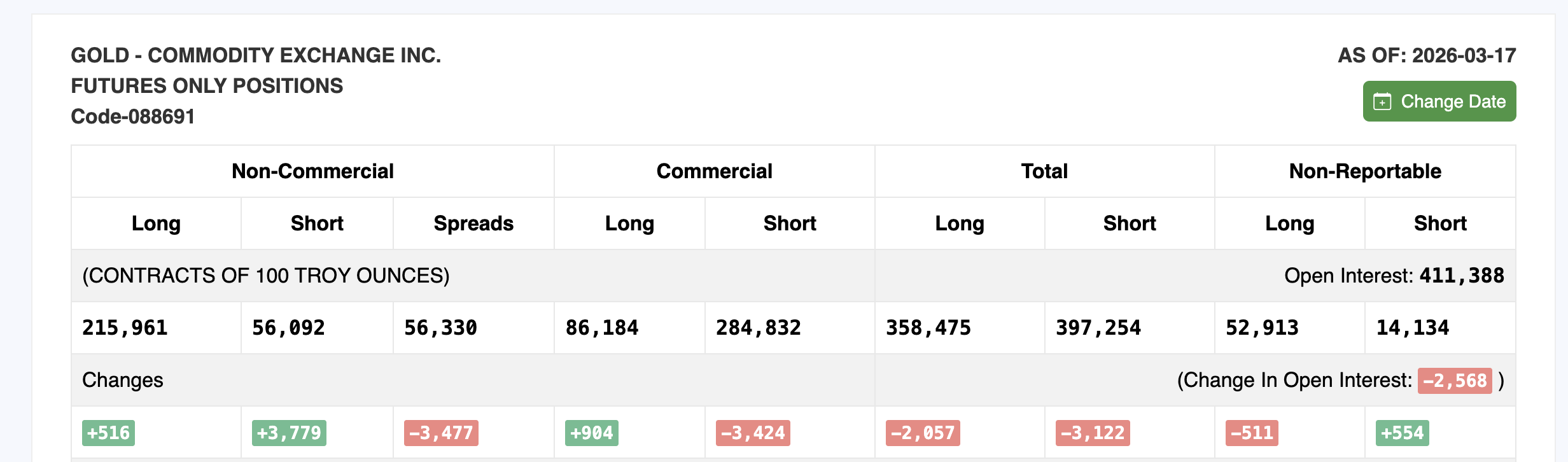

The Commitment of Traders (COT) report, published weekly by the Commodity Futures Trading Commission (CFTC), reinforces this reading. The March 24 report, the latest available, shows non-commercial (speculative) long positions increased by 4,900 contracts to 220,861. Short positions fell by 3,558 to 52,534. On the surface, this looks bullish.

However, total open interest dropped by 7,463 contracts to 403,925 from the previous March 17 report. When longs increase but total open interest falls, it typically means the rally is being driven by short covering rather than fresh buying conviction.

The shift between the two reports aligns with what the GLD put-call data shows. Bearish participants were caught by the 17% rally and scrambled to reposition. This dynamic can sustain a move temporarily but historically does not provide the foundation for a durable gold price advance. The price levels now determine the next path for gold.

Gold Price and the Correlation Paradox

The 8-hour chart with Fibonacci levels frames every critical gold price level. Gold currently sits at $4,676 within the ascending channel.

For the rally to extend, gold needs an 8-hour close above $4,802. Above that, $5,043 acts as the next major resistance. A move through $5,043 would bring $5,422, the March 1 high, back into focus.

However, if gold reaches $5,043 or higher before the correlation completes its reset into deep negative territory, the rally risks repeating the same pattern that preceded both prior corrections. A move higher while the correlation lingers near neutral rather than resetting below -0.70 would leave the advance on an incomplete foundation.

On the downside, $4,490 at the 0.236 Fib represents the first support. Below that, $4,297 at the 0.382 Fib and $4,141 at the 0.5 level come into play. The $4,105 floor from March 23 aligns closely with the 0.5 zone and represents the base of the 17% rally.

Here is where the paradox resolves. A gold price pullback toward $4,105 while oil continues to rise would possibly push the correlation back toward negative territory.

A dip that breaks the oil correlation sets up a stronger foundation for the next sustained move, while a continued rally that keeps both assets moving together leaves gold in the same overheated zone that triggered every correction this cycle. An 8-hour close above $4,802 extends the channel rally but keeps the correlation risk alive, while a pullback toward $4,105 that breaks the oil link could paradoxically be the most bullish outcome for gold’s medium-term path.

The post Why a Gold Price Dip Could Be More Bullish Than Its Current 17% Rally appeared first on BeInCrypto.

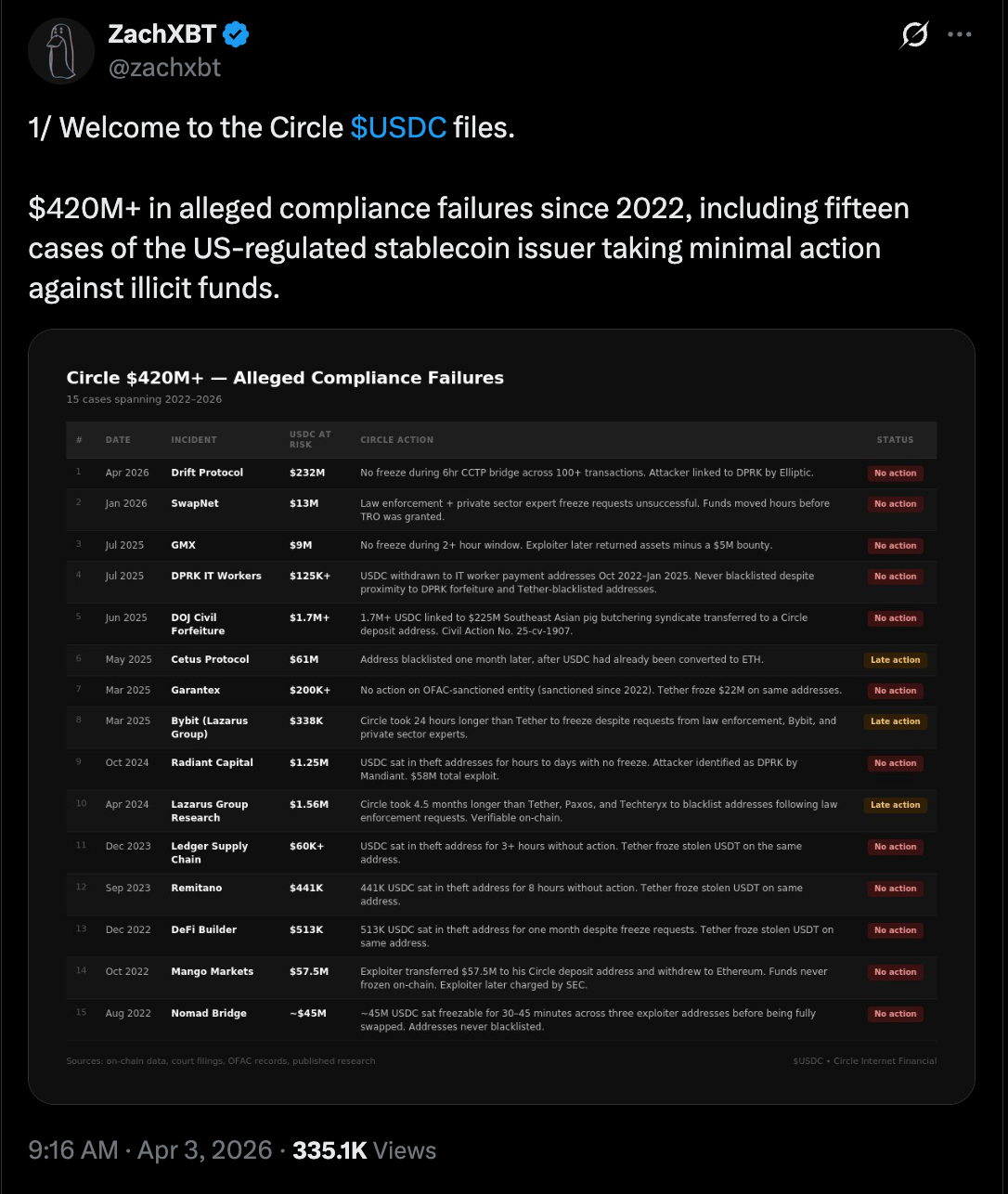

Onchain detective ZachXBT claims that Circle, the issuer of the USDC (USDC) stablecoin, has failed to freeze or blacklist about $420 million in illicit fund flows since 2022.

Circle can freeze illicit funds and blacklist wallet addresses, but either took “minimal” action to freeze illicit flows or failed to act in 15 separate hack-and-fraud cases, including those linked to North Korean (DPRK) state-affiliated hackers, ZachXBT said.

The stablecoin issuer allegedly failed to freeze $9 million in USDC from the GMX decentralized exchange (DEX) hack in July 2025, and blacklisted wallets linked to the $200 million Cetus DEX hack in May 2025 after USDC was converted into Ether (ETH), according to ZackXBT.

Circle failed to freeze $232 million in illicit flows from the Drift Protocol Hack on Wednesday, despite a six-hour window in which the attackers converted USDC to ETH in over 100 separate transactions, he added.

“Circle builds good products, and I hold USDC myself. This isn’t a post about hoping they collapse,” he said, adding that the failure to freeze these illicit flows has had “real consequences for real people.” He said:

“Nine figures were lost from the ecosystem because of repeated inaction across three years on law enforcement requests, private sector requests, and their own infrastructure. The $420 million-plus only accounts for major public cases. The real figure is likely significantly higher.”

Cointelegraph reached out to Circle but did not receive an immediate response by the time of publication.

The lack of asset freezes has sparked an online debate in the crypto community about the role and responsibilities of centralized service providers, as blockchain protocols and users continue to be targeted in hacks and cybersecurity exploits that drain funds.

Related: ZachXBT claims Circle wrongfully freezing exchange wallets

Circle explores “reversible” USDC transactions

In September 2025, Heath Tarbert, the president of Circle, said that the company was exploring “reversible” USDC transactions that could be rolled back or amended in the event of hacks, theft and fraud.

Circle has frozen USDC funds and blacklisted wallets on multiple occasions, including freezing USDC held by Tornado Cash addresses sanctioned by the US Office of Foreign Assets Control in 2022.

Magazine: Meet the onchain crypto detectives fighting crime better than the cops

Brokerage services giant Charles Schwab plans to roll out spot cryptocurrency trading in the first half of 2026, pushing it deeper into digital assets.

“We remain on track to launch our spot crypto offer in the first half of 2026, starting with bitcoin and ether (ETH),” a company spokesperson told CoinDesk on Friday.

The firm has opened a waitlist for clients seeking early access to what it calls a “Schwab Crypto” account, which will allow users to buy and sell the two largest cryptocurrencies. The firm will offer the service via Charles Schwab Premier Bank, SSB.

The move builds on comments from CEO Rick Wurster, who said last July that Schwab aimed to introduce crypto trading “sometime soon” in response to client demand. He framed the effort as a way to bring digital assets into the same account view as stocks and bonds in a push toward a more unified investment platform.

Schwab’s scale could give it an edge as it enters a market long dominated by crypto-native exchanges. The firm reported $11.9 trillion in client assets in 2025, offering a built-in base of retail and institutional investors who may prefer trading crypto within a familiar brokerage environment rather than using standalone platforms.

The firm already allows clients to invest in ETFs linked to cryptocurrencies and trade bitcoin futures on its platform. It also launched the Schwab Crypto Thematic Index (STCE), an ETF that tracks the performance of companies linked to the digital asset sector.

TLDR

- Charles Schwab plans to launch spot Bitcoin and Ethereum trading later this quarter through its brokerage platform.

- The firm manages over $12 trillion in client assets and will roll out the service in phases.

- Employees will receive early access, followed by invited clients, before a full public release.

- Clients will trade Bitcoin and Ethereum directly without using a separate crypto wallet or exchange.

- Charles Schwab Premier Bank, SSB, will operate the new crypto trading service.

Charles Schwab will introduce spot Bitcoin and Ethereum trading later this quarter through its brokerage platform. The firm manages more than $12 trillion in client assets and plans a phased rollout. CEO Rick Wurster confirmed the timeline during a prior earnings call and outlined internal testing before public access.

Charles Schwab to Enable Direct Bitcoin and Ethereum Trades

Charles Schwab will allow retail clients to buy and sell Bitcoin directly within existing brokerage accounts. The company will not require a separate crypto wallet or third-party exchange account. Instead, it will integrate spot trading into its current infrastructure for easier access.

The service will operate through Charles Schwab Premier Bank, SSB, which serves as a regulated banking subsidiary. Employees will receive early access during an internal testing phase before invited clients join. After that, Schwab will open the service to all eligible customers in stages.

Wurster confirmed the launch window during an earlier earnings call with analysts. He said Schwab expects spot crypto trading to go live later this quarter. He also stated that the firm prepared for this move as regulatory conditions evolved.

Brokerage Shifts From Indirect Exposure to Spot Crypto Access

Until now, Charles Schwab has offered digital asset exposure through exchange-traded products and crypto-linked equities. The firm also provided futures contracts and thematic investment portfolios tied to blockchain companies. However, clients could not trade Bitcoin or Ethereum directly on the platform.

The upcoming launch will change that structure by enabling direct spot transactions. Clients will execute trades within their standard brokerage accounts. Schwab will process orders without routing them to an external crypto exchange.

Wurster first signaled interest in spot crypto trading in late 2024. He said the firm monitored regulatory developments closely before expanding services. He added that Schwab positioned itself to act when conditions allowed.

The firm aims to compete with established crypto trading platforms. Schwab will offer Bitcoin and Ethereum trading alongside traditional securities. This structure places Schwab in direct competition with Coinbase, Robinhood, and Webull.

Wurster addressed competition during prior remarks about the rollout. He said, “We are ready to compete in spot Bitcoin and Ethereum trading.” He emphasized that Schwab intends to provide a familiar and regulated environment for clients.

Schwab already supports crypto-linked ETFs and futures within its brokerage accounts. However, the firm will now expand into direct ownership of digital assets. The rollout will follow internal testing and controlled client access before full availability.

The brokerage also plans to introduce a stablecoin product in the future. Wurster confirmed this plan after lawmakers passed the GENIUS stablecoin bill. He said the company will move forward once it finalizes operational details.

Charles Schwab expects to complete the phased rollout later this quarter. The company will announce broader access once testing concludes. For now, the firm continues internal preparations ahead of the public debut.

JOHN MURDOCH’S DRIVE TIME: We preview all-electric BMW i3 and discover extended range version of Nissan Micra now qualifies for full UK EV grant

March Jobs Report: A Muddled Picture

Marex launches Nvidia-linked ‘prediction market bond’ with 7% coupon

-

NewsBeat7 days ago

NewsBeat7 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat1 day ago

NewsBeat1 day agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports7 days ago

Sports7 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Business20 hours ago

Business20 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Crypto World2 days ago

Crypto World2 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Entertainment6 days ago

Entertainment6 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech5 days ago

Tech5 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Tech5 days ago

Tech5 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Fashion6 days ago

Fashion6 days agoAmazon Sundays: Soft Spring Layers

-

Business2 days ago

Business2 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Fashion7 days ago

Fashion7 days agoWhen Evening Dressing Gets Colorful for Spring

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Politics4 days ago

Politics4 days agoShould Trump Be Scared Strait?

-

Crypto World4 days ago

Crypto World4 days agoU.S. rule change may open trillions in 401(k) funds to crypto

You must be logged in to post a comment Login