Crypto World

Stablecoin Uncertainty Could Hit Banks More Than Crypto Firms

Regulatory ambiguity around stablecoins is constraining traditional banks from fully deploying their digital-asset infrastructures, even as the industry remains bullish about the potential to streamline payments and treasury operations. Industry observers say banks have already invested heavily in the rails needed to support tokenized money, but official classifications—whether stablecoins are treated as deposits, securities, or a distinct payment instrument—continue to hold back scale. Colin Butler, executive vice president of capital markets at Mega Matrix, argues that the hesitation is real: without clear guidance, counsel and boards hesitate to authorize large capital expenditures for infrastructure that might have to be rebuilt in response to evolving rules.

The reality on the ground is nuanced. Several heavyweight banks have already laid down significant groundwork. JPMorgan has advanced its Onyx blockchain payments network, a pathway for faster, blockchain-enabled transfers. BNY Mellon has rolled out digital asset custody services, signaling a move toward custody-ready digital money. Citigroup has tested tokenized deposits, a step toward integrating digital representations of cash into traditional banking workflows. Yet even with this progress, the broad deployment of these systems across the balance sheet remains tempered by the regulatory fog over classification and treatment of stablecoins. As Butler notes, “the infrastructure spend is real, but regulatory ambiguity caps how far those investments can scale because risk and compliance functions will not greenlight full deployment without knowing how the product will be classified.”

Beyond the bank wall, the broader market continues to reflect the tension between stablecoin infrastructure investment and regulatory clarity. The article’s context notes that stablecoins remain the backbone of a growing segment of digital payments, with ongoing attention from policymakers and industry groups about how to codify their use in everyday commerce. Among the tangible signals cited are the large-scale efforts by institutions to build the rails that would support stablecoins, juxtaposed with the lack of a final decision on their status—that is, whether they should be treated as deposits, as securities, or as a new category altogether. In the meantime, the industry’s posture remains one of cautious progress rather than wholesale transformation.

On the macro side, executives and analysts point to a persistent yield gap between stablecoins and traditional bank deposits. The article highlights that exchanges commonly offer roughly 4%–5% yields on stablecoin balances, while a typical U.S. savings account yields less than 0.5%. That divergence matters because it shapes deposit flows and risk appetite. The historical reference to the 1970s—when investors rotated into money market funds in search of higher yields—serves as a reminder that capital can be nimble when returns are attractive enough and the transfer process is frictionless. Today, the transfer from a bank account to a stablecoin wallet can be completed in minutes, amplifying any yield-driven migration across the ecosystem. Still, observers caution against expecting a sudden, destabilizing wave of deposits. Fabian Dori, chief investment officer at Sygnum, cautions that trust, regulation, and operational resilience remain prerequisites for large-scale shifts, even as the yield differential creates meaningful competitive pressure.

As regulators weigh policy options, one potential consequence is a shift toward alternative structures that aim to preserve yield even when stablecoins themselves face tighter rules. The article discusses synthetic dollar tokens and derivatives-based yield mechanisms as possible complements or substitutes for traditional stablecoins. Ethena’s USDe, for instance, is cited as a product that can generate yield through derivatives markets rather than through traditional reserves. If policymakers tighten the no-yield rules for stablecoins, some market participants might gravitate toward these more opaque, offshore-style structures. Butler warns that such a shift could have the opposite of the intended effect: capital seeking returns may migrate to less-regulated spaces, potentially diminishing consumer protections in the process. The dynamics imply that regulators must weigh not only the benefits of limiting certain activities but also the possibility that overreach could inadvertently channel funds into riskier, harder-to-track corners of the market.

Key takeaways

- Banks have built significant stablecoin infrastructure, but deployment is throttled by unresolved regulatory classifications that block full-scale capital expenditure.

- Major financial institutions have progressed in tokenized money workflows (Onyx by JPMorgan, digital asset custody by BNY Mellon, and tokenized deposits explored by Citi), signaling readiness to scale pending rules.

- The yield gap between stablecoins and bank deposits could incentivize faster deposit migration, particularly among corporates and fintechs, if risk controls remain manageable.

- Policy moves to restrict yields could unintentionally drive activity into less-regulated or offshore structures unless safeguards are strengthened.

- As the debate evolves, the most consequential outcomes will hinge on how regulators articulate the treatment of stablecoins and related digital assets within the existing financial framework.

Tickers mentioned: $USDC

Market context: The debate over stablecoin classification sits at a crossroads of regulation, institutional treasury strategy, and crypto-market liquidity. With banks edging toward production-ready digital rails but awaiting a definitive policy framework, market participants are watching how policy shapes the economics of stablecoins and their utility in everyday payments.

Why it matters

The central question is whether stablecoins can function as bridges between fiat and digital cash within a regulated banking system. If policymakers settle on a formal, bank-like treatment—as deposits or a payment instrument—banks could deploy full-scale digital-cash rails, reducing settlement times, lowering counterparty risk, and enabling more efficient treasury operations. The potential for widespread adoption could reshape wholesale payments and cross-border settlement, offering a path to faster, cheaper, and more auditable transfers.

At the same time, the industry faces the risk that overly restrictive interpretations could dampen innovation or push activity into less transparent channels. The interplay between regulation and technology will likely define whether stablecoins act as productive digital cash or remain a niche instrument for speculative trading and yield optimization. For users and builders, the key takeaway is that the value of stablecoins in the real economy depends on a clear, risk-balanced framework that preserves consumer protections while enabling scalable infrastructure.

For bankers, the alignment of regulatory expectations with practical deployment is a gauge of whether digital assets become a mainstream tool for corporate treasuries and consumer payments. If the rules cohere with how banks already operate—risk controls, capital requirements, and compliance protocols—the adoption curve could accelerate. If not, the industry may endure a bifurcated market in which banks proceed cautiously while crypto-native firms continue to operate under a lighter regulatory regime.

What to watch next

- Regulatory proposals or legislation clarifying how stablecoins will be classified and treated for capital, deposits, and securities.

- Announcements from major banks on scaled deployments of Onyx-like rails or custody services as guidance becomes clearer.

- Any shifts in yield restrictions or supervisory expectations that could influence stablecoin issuer strategies and investor behavior.

- Emergence of synthetic-dollar products or derivatives-driven yield mechanisms and how regulators respond to these alternatives.

- Broader adoption signals from corporates and fintechs evaluating stablecoin-based treasury solutions or payment rails.

Sources & verification

- Colin Butler, executive vice president of capital markets at Mega Matrix, comments on regulatory ambiguity and bank deployment constraints.

- JPMorgan’s Onyx payments network development and its role in supporting stablecoin infrastructure.

- BNY Mellon’s digital asset custody services and the OpenEDEN initiative for tokenized assets.

- Citi’s SDX tokenization efforts for private markets and related pilot programs.

- Notes on the yield differential between stablecoins (4%–5%) and traditional bank deposits (<0.5% on average savings accounts).

Regulatory uncertainty and the bank-stablecoin battleground

Regulatory clarity remains the linchpin for accelerating or curbing the evolution of stablecoins in the banking system. Banks have signaled readiness by building the infrastructure to support faster settlement, improved liquidity management, and more versatile treasury operations. Yet without a concrete policy framework, risk and compliance teams cannot greenlight expansive deployment. The balance sheet implications—capital requirements, risk-weightings, and liquidity rules—depend on how regulators categorize these digital currencies. If stablecoins are designated as a form of payment instrument, banks could treat them similarly to short-term cash equivalents. If they are securities, the implications would shift toward investor protection and custody standards. A distinct category might offer a hybrid path but would require new supervisory guidance. In practice, the industry is waiting for a decision that could unlock or constrain tens of billions in investment that have already been mobilized toward digital-asset rails.

Meanwhile, market participants are testing the waters with what is already permissible. JPMorgan’s Onyx initiative demonstrates how far large institutions have progressed in integrating blockchain-enabled transfers into mainstream banking workflows. BNY Mellon’s digital custody ventures underscore the demand for secure, regulated storage of tokenized assets. Citi’s exploration of tokenized deposits signals a broader interest in tokenized cash within the regulated banking ecosystem. Taken together, these signals show that the infrastructure is not theoretical: it exists and is ready for scale, contingent on regulatory clarity.

As the debate continues, the risk-reward calculus for banks hinges on whether yields in the stablecoin space can be managed alongside traditional cash-management objectives and risk controls. If policymakers move toward a framework that favorably accommodates stablecoins as digital cash or as a permissible payment instrument, the banking sector could accelerate collaboration with crypto-native entities to deliver faster, cheaper, and more auditable payment flows. If, however, the rules dampen commercial incentives or impose heavy restrictions on yield and liquidity management, the incentive to invest in these rails could wane, slowing the migration of treasury functions to digital assets. In that scenario, crypto-native platforms may continue to operate under different risk regimes, while banks maintain a cautious stance until policy aligns with their risk appetite and capital planning. The stakes are high because the outcome will shape not only the speed of adoption but also the degree to which the broader financial system embraces or resists tokenized money as a core component of modern finance.

Crypto World

Remittix Has Real Utility As Dogecoin & Pepe Traders Snap Up $RTX Tokens As Presale Set To End

Capital rotation is becoming increasingly visible across the meme coin sector as traders reassess where the next major opportunities may emerge. Dogecoin remains far below its 2021 peak, still trading near the $0.09 level after losing more than 75% of its all-time high value. Pepe is facing similar pressure, with recent market activity highlighting that PEPE continues to trade deep below its previous highs as sentiment across meme tokens cools.

As volatility continues to shake confidence in purely momentum-driven assets, many investors are beginning to look toward projects built around real-world utility. One project drawing increasing attention is Remittix, whose RTX token is currently in the final stage of its presale. With a live PayFi platform targeting the $50 billion global remittance fee market and only $6 million remaining in the current allocation, the shift in investor focus is becoming more noticeable. Here’s how Dogecoin, Pepe, and Remittix currently compare as the market narrative begins to evolve.

Dogecoin: Bearish Structure Despite Whale Accumulation

The Dogecoin price opened 2026 around $0.118 and has since fallen to about $0.095 in an extended downtrend that began after DOGE failed to get back above $0.25 in early 2025. Technical indicators are still bearish. 19 of 28 signals are flashing red and the Fear and Greed Index for Dogecoin price movement is at 18.

There are counterpoints. Whales purchased 1.7 billion DOGE worth $285 million in early March, and analyst Javon Marks has identified a bullish reversal on the monthly chart with targets as high as $1.25. The beta launch of X Money on Elon Musk’s platform also briefly lifted the Dogecoin price. But sustained momentum has not followed.

Dogecoin price predictions range from $0.10 to $0.19 and these are conservative scenarios offering limited upside for traders accustomed to parabolic rallies. That tepid outlook is one reason former DOGE holders now buy RTX tokens instead.

Pepe News: Liquidity Drains as the Meme Fades

The news about Pepe just now proves what many dreaded. PEPE is trading at approximately $0.0000033 which is lower as compared to its highest point of $0.0000280. The market cap has been shrinking to $1.4 billion and 22 out of 30 technical indicators are bearish. Liquidity has been meager with reserved spirit extending to Q4 2025.

Optimistic Pepe news entails long term projections. Changelly is projecting a recovery to $0.0000098 by December 2026 should the conditions improve. CoinPedia expects to get between $0.0000037 and $0.0000073 this year.

But without utility or a revenue model, PEPE remains dependent on social media cycles. That fragility is why Pepe news headlines mention capital rotation into utility tokens and why traders are instead buying RTX tokens as a hedge against meme fatigue.

Remittix: The Utility Play Drawing Meme Coin Profits

While meme-coin speculation continues to dominate social feeds, a growing number of traders are quietly reallocating profits into projects with clearer utility. That shift has become particularly visible among Dogecoin and Pepe holders, many of whom are now accumulating Remittix as the project’s presale moves toward its closing phase.

The interest is not purely speculative. Remittix is positioning itself within the rapidly emerging PayFi sector, focusing on infrastructure that allows cryptocurrencies to interact more seamlessly with traditional financial systems. Instead of relying on hype cycles, the platform is designed to enable direct crypto-to-fiat settlement, a function that addresses one of the most persistent frictions in digital asset adoption.

Five Core Remittix features explain why:

- Crypto-to-Fiat Bridge Across 30+ Currencies. Users send payments in over 100 cryptocurrencies and recipients receive local bank deposits with same-day processing.

- CertiK Grade A Security. Remittix ranks number one among pre-launch tokens on CertiK Skynet with full team verification.

- Zero Foreign-Exchange Fees. A flat-rate model eliminates the hidden charges that traditional remittance providers depend on.

- Staking Yields Up to 18% APY. No buy or sell tax on RTX, zero vesting for presale buyers, and tiered staking from 4% to 18%.

- Confirmed Exchange Listings. BitMart and LBank are locked in, with a third major listing expected at the $30 million milestone.

For traders watching the Dogecoin price stagnate and reading Pepe news about contracting liquidity, the chance to buy RTX tokens represents a fundamentally different proposition.

Remittix Opportunity: Where DOGE and PEPE Stand Today

Analysts have expressed optimism that Dogecoin price may recover if whale accumulation translates into buying pressure, and positive Pepe news could surface if meme sentiment cycles back. But neither asset offers the structural utility that investors increasingly demand.

Investors currently buying RTX tokens are betting on a different thesis: that a working payments platform with audited security and confirmed listings will outperform speculation over the medium term. With the presale in its final stage, a limited-time 15% affiliate bonus paid in USDT and claimable every 24 hours, gives participants an additional reason to act before the window closes.

Discover the future of PayFi with Remittix by checking out their project here:

Website: https://remittix.io/

Socials: https://linktr.ee/remittix

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Bitcoin could eventually reach $1 million per coin if it captures a larger share of the global store-of-value market currently dominated by gold and government bonds, according to Bitwise Asset Management CIO Matt Hougan.

In a report earlier this week, Hougan said bitcoin’s long-term upside depends less on short-term market cycles and more on how much of the world’s wealth preservation market the cryptocurrency absorbs over time.

“One million sounds crazy,” said Hougan. “It implies bitcoin will rise 14x from today’s price.”

He pointed to several factors supporting that forecast, among them the rapid growth of the global store-of-value market, including gold, government bonds and other defensive assets, which has expanded from roughly $2.5 trillion in 2004 to nearly $40 trillion today. Bitcoin currently represents only about 4% of that market by value.

If the largest cryptocurrency were to capture roughly half of that market under current conditions, its price could approach that $1 million mark within roughly a decade, Hougan said. If the broader store-of-value market continues expanding, bitcoin would require a smaller share to reach that level.

The $1 million price fixation

The $1 million forecast has become a recurring theme across the crypto industry. President Donald Trump’s son Eric recently doubled down on his $1 million BTC call. In August, Coinbase CEO Brian Armstrong said bitcoin could reach that price by 2030.

Jack Dorsey, who ran X (formerly Twitter) until 2021 and co-founded payments firm Block (formerly Square), said bitcoin could reach $1 million in five years. Arthur Hayes, former BitMEX CEO, believes it could come as soon as 2028. Cathie Wood’s Ark Invest projected that bitcoin could reach $3.8 million by the end of the decade. Bernstein in 2024 forecast $1 million by 2033.

So why has the $1 million target become such a widely cited benchmark for bitcoin? CoinDesk asked several market analysts.

“It’s a clean headline and shorthand for the idea that Bitcoin could rival gold as a store of value. The exact number matters less than the share of global wealth Bitcoin captures,” said Mati Greenspan, market analyst and Quantum Economics founder.

For Jason Fernandes, also a market analyst and an AdLunam co-founder, the milestone is more psychological than a precise valuation target, reflecting the belief that bitcoin could ultimately win the store-of-value debate.

However, he also believes part of the narrative is driven by marketing dynamics. “Some of the narrative is promotional because round numbers travel well and align with holder incentives,” Fernandes said, though he added that the underlying thesis is not purely hype.

“I think many investors make a ‘static denominator’ mistake, valuing bitcoin against today’s store-of-value market instead of a much larger future one,” he said.

For Fernandes, the real question is not whether $1 million bitcoin is theoretically possible, but whether institutional adoption compounds long enough to justify that price.

Analysts agree on direction, but not the timeline

Some of the analysts who shared their comments with CoinDesk said Hougan’s projection is plausible over the long term, though most frame it as a decade-scale adoption story rather than a near-term forecast.

“Geopolitical tension strengthens the Bitcoin thesis,” said Greenspan. “In uncertain times, investors look for neutral stores of value, and Bitcoin increasingly sits in that bucket alongside gold.”

Greenspan said the milestone is possible but would likely take a decade or more, requiring continued institutional adoption and broader regulatory clarity.

Fernandes said Hougan’s argument is essentially a market-share thesis. Bitcoin does not need to replace gold outright, he said; it only needs to capture a portion of a growing global store-of-value market.

“A $1 million bitcoin assumes long-term adoption and market-share gains within the global store-of-value market,” Fernandes said. “It’s a thesis about bitcoin’s end state if it matures into a major global monetary asset.”

Institutional adoption remains the key driver

Hougan has argued that bitcoin’s fixed supply of 21 million coins and its decentralized network give it characteristics similar to those of traditional stores of value, such as gold.

Fernandes said the long-term $1 million thesis depends largely on continued institutional adoption and growth in the global store-of-value market.

“BTC doesn’t need to replace gold or fiat; it only needs to capture about 17% of a projected $121 trillion store-of-value market over the next decade to justify a $1 million price,” Fernandes said.

Greenspan said geopolitical uncertainty could further strengthen bitcoin’s appeal as a neutral asset.

“In uncertain times, investors look for neutral stores of value, and bitcoin increasingly sits in that bucket alongside gold,” he said, though he added that reaching such a valuation would likely take years of sustained adoption.

Nima Beni, founder of Bitlease, said the timeline could accelerate if confidence in traditional financial assets weakens.

“Bitcoin reaches $1 million when confidence in traditional ‘safe’ assets breaks,” he said, pointing to potential sovereign debt crises or disruptions in the gold market as possible catalysts.

Despite the bullish projections, analysts said bitcoin’s path toward such valuations would depend more on long-term adoption and macroeconomic conditions than on short-term market cycles.

New forensic findings from the phone of crypto lobbyist Mauricio Novelli have revealed a draft document suggesting a possible $5 million agreement connected to Argentine President Javier Milei’s promotion of the Libra token, according to local media reports.

The document, recovered from Novelli’s iPhone during a judicial investigation into the Libra crypto scandal, outlines a three-part payment structure totaling $5 million. Screenshots of the note surfaced after expert materials held by prosecutor Eduardo Taiano since November were made public, Argentine outlet El Destape reported.

The draft note was reportedly written in English on Feb. 11, 2025, just three days before Milei posted about the Libra token on X. “Hello friends, this is the final agreement discussed with H,” the text begins, which is believed to refer to crypto entrepreneur Hayden Davis.

The document then details the payment structure. “$1.5M of liquid tokens or cash as an advance. $1.5M in liquid tokens or cash = Milei announces on Twitter that his advisor is Hayden Davis/Kelsier/the Davis family. $2M in tokens or cash = contract signed in person with Milei for blockchain/AI consulting for the Argentine government and/or Javier Milei and review with Javier and Karina,” the text reads.

Notably, the draft note does not specify who would receive the funds.

Related: Argentina turns up the heat in Libra scandal with sweeping asset freeze

Another note outlines crisis message after scandal

Investigators also recovered a separate note drafted on Feb. 16, 2025, two days after the Libra controversy erupted online. The message appears to outline a public statement intended to calm the situation.

“This is what I want for the tweet. This is the only thing that saves him, me, and us,” the note’s translation from Spanish reads. The draft message then states support for the Libra project while denying any financial involvement and attributing accusations of wrongdoing to political opponents.

Authorities believe the message may have been prepared for Milei to post on social media or reference in an interview, according to local media reports.

Novelli was in Dallas during the token’s launch. Call records show he communicated with Milei and his sister Karina shortly before and after the president’s social media post about the token. As the controversy spread online, Novelli also held multiple calls with presidential adviser Santiago Caputo while the government managed the crisis.

Related: Argentine exchange Ripio bets on peso stablecoins amid cautious 2026 outlook

Libra hit $4 billion after Milei post before crashing

In February last year, Milei posted on X about the Libra (LIBRA) memecoin, which briefly reached a $4 billion market capitalization before plunging 94% within hours.

The crash wiped out hundreds of millions in investor funds and prompted opposition lawmakers to call for Milei’s impeachment. Milei later said he had merely “spread the word” about the token rather than promoted it.

Magazine: 2026 is the year of pragmatic privacy in crypto — Canton, Zcash and more

Crypto World

5 Undervalued AI Stocks for 2026: Oracle (ORCL), AMD, Micron (MU), TSMC and Dell Lead the Pack

While the artificial intelligence revolution has minted numerous success stories, many headline-grabbing companies now carry valuations that price in years of perfect execution. The real opportunities may lie with the less glamorous players—those providing the essential building blocks of AI infrastructure, from semiconductors and memory to cloud platforms and enterprise servers. Here are five stocks trading at attractive valuations despite their critical roles in the AI ecosystem.

Oracle’s Transformation Into an AI-Driven Cloud Giant

Once dismissed as a dinosaur in the database industry, Oracle is rewriting its narrative with impressive momentum.

The company’s most recent quarterly results showed total revenue climbing 22%, while cloud revenue surged 44% and Oracle Cloud Infrastructure accelerated an impressive 84% year-over-year. Perhaps most striking was the 325% jump in remaining performance obligations to $553 billion—representing committed future revenue already in the pipeline. Management has confidently raised its fiscal 2027 revenue guidance to $90 billion.

Wall Street may still be valuing Oracle through the lens of its legacy software business, but the reality is dramatically different. As the company’s revenue composition shifts increasingly toward high-margin AI cloud services, the valuation gap becomes more apparent. Should Oracle successfully monetize its massive backlog, significant upside potential remains.

AMD Emerges as a Legitimate Nvidia Competitor

While AMD is not Nvidia, the narrative that it’s perpetually behind is outdated.

Advanced Micro Devices, Inc., AMD

AMD delivered record quarterly revenue of $10.3 billion in Q4 2025, maintaining a healthy 54% gross margin. The data center division generated $5.4 billion in revenue—a 39% increase from the prior year—fueled by robust adoption of both EPYC server processors and Instinct AI accelerators.

The compelling case for AMD lies in its valuation relative to peers and its diversified revenue streams. Unlike pure-play AI chip companies, AMD benefits from multiple growth vectors including AI GPUs, traditional server CPUs, embedded solutions, and general cloud infrastructure expansion. Investors who believe AMD will continue capturing market share in high-performance computing may find today’s valuation attractive.

Micron: The Essential Memory Provider Wall Street Overlooks

Artificial intelligence infrastructure demands massive quantities of high-bandwidth memory, and Micron stands among the select few manufacturers capable of delivering at volume.

First-quarter fiscal 2026 results showcased revenue of $13.6 billion—a 57% year-over-year increase. Micron also achieved record free cash flow and announced increased capital expenditures to expand production capacity for next-generation HBM (high-bandwidth memory).

Memory chip manufacturers historically face cyclical demand patterns, making investors hesitant to assign premium valuations. However, AI workloads may be establishing a structural shift in memory demand that defies traditional cycles. If HBM remains in tight supply as expected, Micron could command a higher valuation multiple than legacy memory producers typically receive.

TSMC: The Indispensable Manufacturer Behind AI’s Biggest Names

TSMC fabricates the cutting-edge processors that enable virtually every significant AI innovation. Companies from Nvidia and AMD to Apple depend entirely on TSMC’s manufacturing capabilities.

Fourth-quarter 2025 results demonstrated revenue growth of 25.5% in U.S. dollar terms, accompanied by a 62.3% gross margin and 54% operating margin. The momentum continued into 2026, with January and February revenue climbing 29.9% compared to the same period in the previous year.

TSMC shares have traditionally traded at a discount to American semiconductor peers due to geopolitical risks associated with Taiwan. Yet from a pure operational and financial perspective, TSMC rivals or exceeds nearly any large-cap chip company. As AI hardware demand keeps advanced node capacity fully utilized, the company’s earnings trajectory appears increasingly robust.

Dell’s Explosive AI Server Growth Flies Under the Radar

Dell has transformed into a critical supplier of AI infrastructure, though many investors haven’t yet recognized this evolution.

Fiscal fourth-quarter 2026 results revealed overall revenue growth of 39%, but the real story was in AI-optimized servers, where revenue exploded 342% to reach $9 billion. Dell entered the current year with an extraordinary $43 billion backlog of AI server orders—providing revenue visibility that few hardware manufacturers can match.

The market continues pricing Dell largely as a personal computer company, creating a disconnect between perception and reality. With AI servers representing an expanding portion of total revenue, the valuation gap between Dell’s legacy image and its actual business composition is becoming harder to ignore. Value-oriented investors seeking AI exposure are increasingly recognizing this opportunity.

Final Thoughts

Oracle, AMD, Micron, TSMC, and Dell may not generate the same headlines as the most prominent AI stocks, but they’re providing the essential infrastructure—processors, memory chips, manufacturing capacity, cloud platforms, and complete systems—that enables the entire AI revolution. For investors concerned that the obvious AI beneficiaries already reflect lofty expectations, these five companies offer an alternative pathway to capitalize on the same secular growth trend.

Bitcoin (CRYPTO: BTC) has hovered near the $71,000 level as large holders ramp up exposure, according to Santiment’s latest weekly assessment. The analysis highlights a renewed shift by wallets that hold 10 to 10,000 BTC, which Santiment described as a bullish signal if it endures. The share of the total supply controlled by this cohort rose to 68.17% from 68.07% a week earlier, signaling a persistent tilt toward big holders even as prices stabilize. Retail demand, meanwhile, remains fragile; the Crypto Fear & Greed Index was in Extreme Fear at 16 on Sunday, underscoring ongoing caution among everyday investors. Bitcoin was around $71,350 at the time of publication, marking a roughly 6% rise over the past week. On the liquidity side, US spot BTC ETFs logged their first five-day inflow streak of 2026, bringing in roughly $767.32 million this week, a reminder that regulated products continue to channel capital into the market.

For context, Santiment’s notes on on-chain behavior were complemented by a broader view of market sentiment. The firm’s observations on wholesale accumulation come as traders weigh the implications of a shift in ownership toward larger addresses. The wholesale activity is particularly relevant when juxtaposed with the persistence of cautious sentiment among retail participants, a dynamic that has characterized much of Bitcoin’s range-bound work over recent months. The interplay between accumulation by whales and the slower pace of retail adoption has created a tug-of-war that market participants are watching closely, especially in areas where technicals align with on-chain signals to form a potential base for price stability.

In a separate frame of reference, the market has been responding to regulatory and product-structure developments that shape how new participants access Bitcoin. ETF inflows, now aided by a broader appetite for regulated exposure, can lend a degree of liquidity that supports price discovery. At the same time, analysts caution that this is not a simple, linear uptrend; episodes of volatility can arise if large holders react to evolving risk cues or if retail conviction fluctuates sharply. The balance between on-chain momentum and macro-driven appetite for regulated products continues to define Bitcoin’s core narrative as the year progresses.

Past on-chain patterns also color expectations. A week earlier, Santiment noted a marked reversal among whales after a sprint of buying earlier in the month. In a Mar. 6 report, the firm highlighted that whales had sold roughly 66% of the Bitcoin they had purchased between Feb. 23 and Mar. 3, just as Bitcoin breached the $70,000 level and briefly touched $74,000. The takeaway is not that whales cannot sustain accumulation, but that their activity can pivot rapidly in response to price moves, implying that a potential bottom may require a clearer alignment of broader market participants around a stable price range. The market’s tendency to reward the consensus with a lag remains a recurring theme that analysts stress when evaluating the durability of any bottom signal. Willy Woo, a prominent on-chain commentator, recently framed Bitcoin’s price action as “solidly in the middle of its bear market through a lens of long-range liquidity,” a reminder that structural factors can influence how the market transitions from caution to confidence over time.

The current environment also reflects a broader appetite for regulated crypto exposure. The five-day inflow streak into US spot Bitcoin ETFs is a notable marker of renewed institutional interest, a trend that has historically added a layer of liquidity and can help moderate sharp downside moves. The inflows come as traders observe how on-chain activity interacts with price levels and how new participants engage with the asset through regulated vehicles. While this liquidity backdrop can support a steadier price path, it does not by itself guarantee a sustained rally, particularly in a market where sentiment remains guarded and retail participation shows mixed signals. In the mix of factors shaping near-term moves, the balance between whales’ accumulation and retail behavior, alongside evolving ETF dynamics, will likely influence Bitcoin’s trajectory over the coming weeks.

Key takeaways

- Whale accumulation around $71k offers a potential floor if the trend persists, signaling renewed on-chain demand from large holders.

- The rising share of supply held by wallets with 10–10,000 BTC suggests ownership concentration is increasing, which could impact price dynamics if these addresses sustain net buying.

- Retail demand remains a wildcard, with Extreme Fear readings implying a cautious market that could slow any rapid upside despite bullish on-chain signals.

- Regulated exposure via US spot BTC ETFs contributed to a five-day inflow streak of roughly $767.32 million, adding liquidity that can influence near-term price action.

- Historical whale behavior—selling into strength—serves as a reminder that large holders can shift momentum quickly, creating risk for a sustained rally without broader participation.

Tickers mentioned: $BTC

Sentiment: Neutral

Price impact: Positive. Bitcoin’s price has moved higher in the week, reflecting on-chain accumulation and improving liquidity conditions from ETF inflows.

Trading idea (Not Financial Advice): Hold. The current mix of whale accumulation and cautious retail sentiment suggests waiting for clearer directional cues before committing to a new position.

Market context: A liquidity backdrop is evolving as US spot BTC ETFs post renewed inflows, complementing on-chain signals and shaping potential price moves as investors reassess risk and regulatory considerations.

Why it matters

On-chain behavior remains a critical lens through which investors assess Bitcoin’s near-term health. The consolidation of ownership among larger addresses can indicate a readiness to anchor prices at higher levels, especially if these participants sustain their accumulation into key support zones. If whales continue to accumulate while smaller holders trim their activity, the market could be positioning for a more durable base rather than a transient spike. This dynamic matters because it can reduce the likelihood of rapid, sharp declines and increase the odds of a steadier ascent should risk sentiment improve modestly.

Retail sentiment, captured by the Fear & Greed Index, matters because it often acts as a contrarian indicator. When everyday investors grow increasingly optimistic, the market may face a pullback if the enthusiasm outpaces underlying fundamentals. Conversely, persistent caution can delay upside while prices remain tethered to macro and on-chain cues. The emergence of ETF inflows adds another layer to the equation: while inflows are not a guarantee of a sustained rally, they can augment liquidity and provide a stepping-stone for broader participation, including institutional players who seek regulated exposure. Together, these factors sketch a market that could wobble near a confluence of on-chain signals, regulatory dynamics, and liquidity shifts rather than follow a simple, predictable trajectory.

In practical terms, traders and investors should watch how whale and retail balances evolve in tandem. A sustained rise in the share of BTC held by the 10–10,000 BTC cohort could reinforce a floor, especially if accompanied by continued ETF inflows. However, a resurgence in retail buying could introduce additional volatility, particularly if it coincides with macro developments or shifting risk appetite. The market’s path forward will likely hinge on the resilience of on-chain signals and the depth of liquidity provided by regulated products as the year progresses.

What to watch next

- Monitor the balance between whale and retail wallet activity; a persistent tilt toward large holders could support a higher floor.

- Track the Crypto Fear & Greed Index for shifts in sentiment that could precede a change in buying patterns.

- Observe ETF inflows beyond this week’s levels to gauge whether regulated exposure remains a tailwind for liquidity and price discovery.

- Watch price action around $71k and nearby psychological levels to assess how momentum players respond to resistance zones.

- Stay alert to macro developments and regulatory signals that could alter risk appetite for the crypto sector.

Sources & verification

- Santiment weekly summary on wallet balances and the share of supply held by 10–10,000 BTC addresses.

- On-chain discussion of whale dynamics and potential bottom formation from Santiment.

- Crypto Fear & Greed Index reading (Extreme Fear) for the period referenced.

- Bitcoin price context around $71,350 with seven-day performance data (CoinMarketCap).

- U.S. spot Bitcoin ETF inflows totaling approximately $767.32 million in the week reviewed.

TLDR

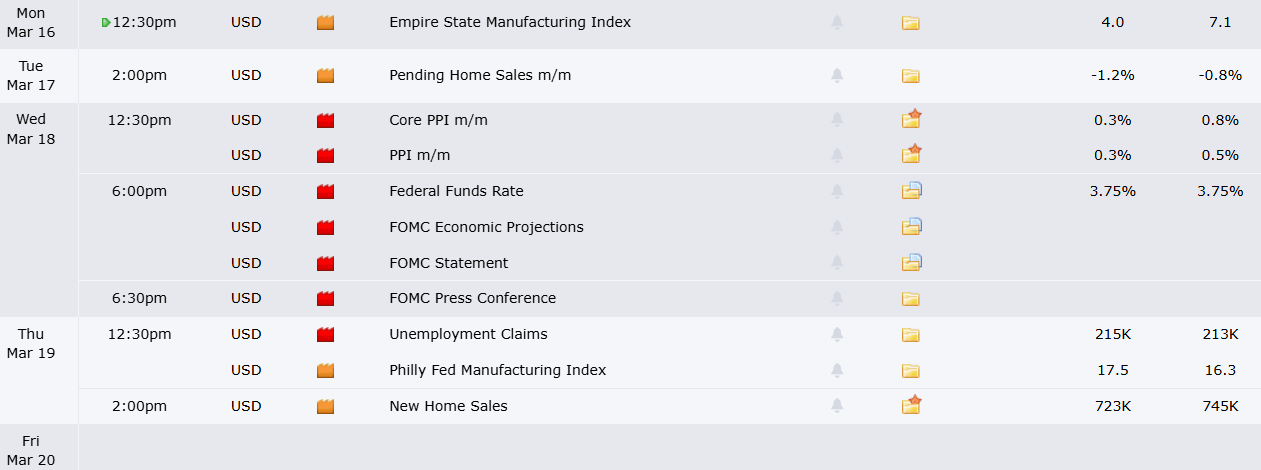

- Federal Reserve convenes Wednesday with expectations of maintaining rates between 3.5%–3.75%, focus shifts to Powell’s commentary

- Crude oil surged past $100 per barrel following Iran conflict that has disrupted Strait of Hormuz shipping routes

- Micron Technology delivers quarterly results Wednesday following remarkable stock surge of over 300% in past year

- Major earnings releases include FedEx, Dollar Tree, Alibaba, and multiple retail companies

- Goldman Sachs forecasts Q4 oil averaging $93/barrel if Strait of Hormuz blockade continues for two months

Equity markets extended their losing streak to three consecutive weeks as escalating tensions in Iran drove crude oil to heights last witnessed during the 2022 energy emergency. The S&P 500 declined 1.6% for the week. The Dow Jones Industrial Average shed 2%. The Nasdaq Composite retreated 1.3%.

Investors now face a calendar-packed week featuring a Federal Reserve policy announcement, numerous corporate earnings reports, and Nvidia’s signature developer conference.

The Federal Open Market Committee convenes Wednesday for its latest monetary policy deliberation. The benchmark federal funds rate currently stands at 3.5% to 3.75%. Market participants are nearly unanimous in expecting no change to current policy.

Chairman Jerome Powell will conduct a press briefing following the announcement. Analysts suggest this commentary could prove more significant than the rate decision itself.

Powell faces the task of addressing internal disagreements among Fed officials. One faction advocates for additional rate reductions citing employment market weakness. Another group expresses concern about potential inflation acceleration driven by surging energy costs.

This marks Powell’s penultimate scheduled press conference before his chairmanship concludes in May.

Oil and the Strait of Hormuz

The Iranian conflict has entered its third week with no resolution in sight. The Strait of Hormuz — a narrow 21-mile channel transporting approximately 14 million barrels of crude daily — continues to experience disruptions.

Iran’s Revolutionary Guard Corps has declared it will prevent “a liter of oil” from traversing the waterway.

Crude prices temporarily exceeded $100 per barrel last Sunday, marking the first such occurrence since Russia’s Ukraine invasion in 2022. After retreating to the $80 range, prices rebounded following drone attacks on critical petroleum infrastructure and production reduction announcements from Gulf nations.

Goldman Sachs projects that sustained closure of the Strait for 60 days would result in fourth quarter Brent crude averaging $93 per barrel. US West Texas Intermediate would average $89 under this scenario.

Wednesday additionally brings February’s Producer Price Index release. The January reading revealed wholesale inflation exceeded forecasts.

Micron and the Earnings Lineup

Micron Technology unveils quarterly results Wednesday. The semiconductor memory manufacturer’s shares have surged more than 300% over the previous twelve months, propelled by artificial intelligence hardware demand. Its most recent quarter showed 60% year-over-year revenue growth and exceeded analyst profit projections.

FedEx delivers earnings Thursday. The logistics giant’s stock has climbed nearly 25% year-to-date. Analysts scrutinize FedEx’s shipping metrics for economic health indicators.

Dollar Tree also announces results, offering perspective on American consumer strength. Its previous report characterized shoppers as “stretched.”

Nuclear energy firm Oklo releases earnings Tuesday. The company recently finalized an agreement with Meta to provide electricity for data center operations.

Alibaba reports Thursday alongside plans for expanded AI investment. Chinese electric vehicle manufacturer Xpeng announces Friday.

Nvidia’s GTC 2026 conference launches Monday featuring a presentation from CEO Jensen Huang.

Perhaps due to its popularity, but Ripple’s token is often the subject of some big price predictions, many of which come from its community, known as the XRP Army, and they are hard to believe, at least at first glance.

One of the latest, though, came from Ali Martinez, a renowned crypto analyst who has shown a lack of bias toward XRP in his commentary. Moreover, he posted a massive, quite unrealistic target (at least for the time being) of $48, but he based it on technical analysis, indicating that this is the potential top during the next bull run, according to the multi-year triangle formation.

While this might sound absurd given XRP’s current price tag of $1.43 and that it would require a 3,300% surge to reach those levels, we decided to ask ChatGPT to dissect this prediction to see if there’s any merit after all.

Reality Check

The AI solution first noted that the multi-year symmetrical triangle has started forming since its 2018 peak, and this measured move is calculated by taking the height of the pattern and projecting it upward from the breakout point. In the asset’s case, the range is quite wide, from $0.20 to $3.84. The current peak was obtained in 2025 at $3.60, while the breakout level is at the whopping $10-$13 zone.

It disclaimed that such measured moves from very large patterns “often exaggerate theoretical targets” because they assume a clean breakout with sustained momentum. If XRP is to reach those levels, its market cap would make it roughly the current size of Apple and 2x that of Bitcoin. To do so, these two factors would need to occur:

- The total crypto market cap would need to expand dramatically (possibly $10-$15 trillion).

- XRP would have to capture a very large share of that capital.

ChatGPT went back to the 2016/2017 cycle when XRP posted a mind-blowing surge of 56,000%, it said, jumping from approximately $0.006 to its then-all-time high of $3.40. In 2020-2021, it gained over 1,000%, but those moves came when XRP was a lot smaller altcoin, which is not the case now.

“Compared with those numbers, 3,300% is not unprecedented in crypto, but it usually happens from much lower starting prices. From a $88 billion market cap – such moves become harder.”

Realistic Targets

After it dismissed the $48 level as a “multi-cycle moonshot” option in which too many factors have to be perfectly aligned, ChatGPT outlined more realistic targets for the cross-border token. Its conservative scenario envisions a substantial rally to somewhere between $3 and $5.

The stronger bull case, in which XRP and the company behind it would have to experience major adoption growth, the ETF inflows would need to skyrocket, and the overall market expansion must be a lot stronger, sees the asset jumping to $8-$12. The probability for this scenario was put at “moderate.”

Even the extreme bull case puts XRP at $15-$25, and nowhere near $48. And this one would be possible if the total market cap reaches $10 trillion, and the cross-border token “captures a large narrative-driven capital inflow.” This probability was set at “low but plausible.”

The post We Asked ChatGPT if XRP Can Indeed Hit $48: Here Is the (Un)Surprising Answer appeared first on CryptoPotato.

Vienna, Austria-based crypto broker Bitpanda is leaning into a strategy it has been quietly building for years: keep its retail business anchored in Europe while expanding globally by supplying crypto infrastructure to banks and financial firms.

The company’s next phase of growth will focus less on raw user numbers and more on geographic reach, Vishal Sacheendran, vice president of global markets strategy and operations, told CoinDesk in an interview.

“It’s about having a footprint in more markets,” Sacheendran said.

That expansion is building on its steady growth. The company, which boasts more than 7 million users, reported this week €371 million ($430 million) in adjusted revenue for 2025, up 16% from the previous year, while its registered user base increased 25% to 7.4 million.

The firm is also weighing a public listing. Bitpanda is reportedly preparing for a potential IPO on the Frankfurt Stock Exchange as early as the first half of 2026, targeting a valuation between EUR 4 billion and EUR 5 billion. The plan comes as multiple crypto exchanges and infrastructure firms have either gone public or are planning to do so.

Bringing crypto to banks

The exchange spent the past decade largely focused on the European Union, where its app allows retail users to trade cryptocurrencies and other assets. But outside Europe, Sacheendran said the strategy needs to change. In some markets — especially smaller ones or those already dominated by global exchanges — launching a consumer app may not make sense.

Instead, Bitpanda wants to work through banks and financial institutions that already have distribution. “We don’t want to compete with exchanges everywhere,” he said. “There’s a big segment of the market that still trusts banks.”

The company formalized that approach earlier in March with the launch of Bitpanda Enterprise, a new institutional offering that packages the firm’s infrastructure for banks, brokers, asset managers, fintechs and corporate clients.

The unit builds on Bitpanda’s existing B2B business, previously known as Bitpanda Technology Solutions, and bundles several services into a single platform. These include API-based investment infrastructure for financial brands, institutional-grade custody, trading liquidity and settlement tools, and payment rails for crypto and stablecoins. The platform also includes token infrastructure for stablecoin issuance and systems designed to support tokenized assets.

UAE launchpad

One early example of that model came in July, when RAKBANK, one of the United Arab Emirates’ oldest lenders, launched crypto trading for retail customers through a partnership with Bitpanda. Instead of building its own infrastructure, the bank plugged into Bitpanda’s platform.

Sacheendran said deals like that often open doors elsewhere. Once one major bank adopts crypto services, others tend to follow. “When a top-tier bank starts offering it, the rest of the market takes notice,” he said.

Bitpanda’s pitch to institutional partners rests heavily on its regulatory positioning. The company has been operating under strict licensing requirements, including the European Union’s MiCA framework, widely seen as one of the most comprehensive crypto regulatory regimes.

Regulatory moat

That regulatory credibility travels, Sacheendran said, especially in emerging markets where regulators are still shaping their approach to digital assets. In many of those regions — including parts of Asia, Latin America and the Middle East — authorities are eager to develop the sector but want partners that already operate within strong compliance frameworks.

Asia-Pacific illustrates the complexity. The region is “very fragmented,” he said, with different rules in jurisdictions such as Hong Kong, Singapore, Japan and South Korea. Bitpanda’s approach there will be gradual: start small, test demand and scale where the regulatory and commercial conditions align.

On the product side, Bitpanda is evaluating derivatives trading, though Sacheendran noted that regulations differ widely across jurisdictions. He also expects tokenization to become a bigger theme in the coming years, particularly for assets such as bonds, money market funds and real estate.

Those markets could benefit from blockchain’s ability to enable around-the-clock trading and broader investor access, he said.

One area Bitpanda is unlikely to enter directly is stablecoin issuance. “We don’t build a stablecoin,” Sacheendran said, noting that the company prefers to provide infrastructure and operational support for institutions that want to launch their own.

Read more: Stricter MiCA rules could thin crypto industry across the EU, says Swiss wealth manager

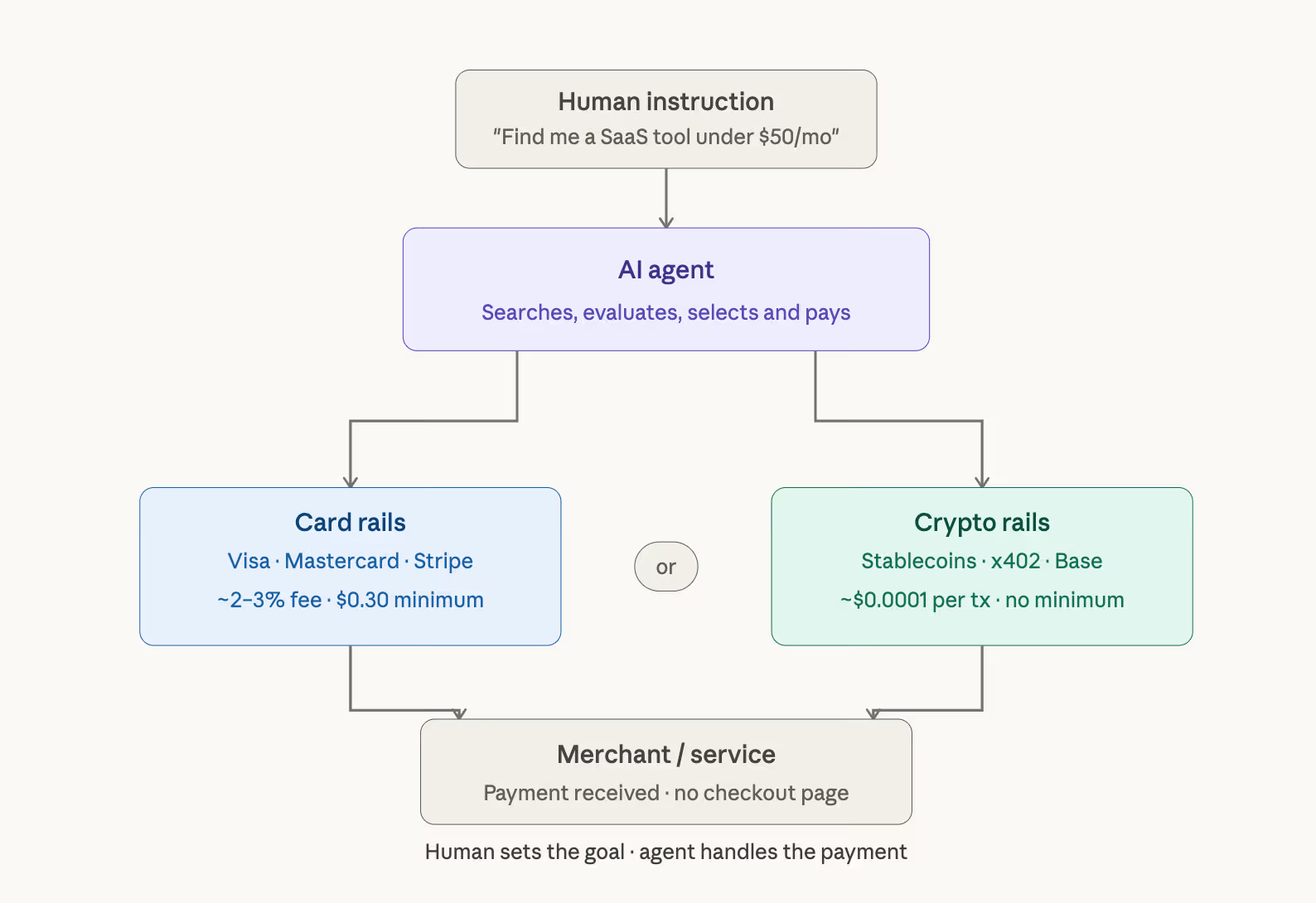

Your AI just made several payments while you read that headline. You approved none of them. Visa processed none of them. And if the crypto industry’s biggest bulls are right, that’s not a bug — it’s the entire future of the internet economy.

Coinbase founder Brian Armstrong thinks there will soon be more AI agents than humans making transactions on the internet. Binance founder Changpeng Zhao went further, predicting agents will make one million times more payments than people, all in crypto. The posts landed on the same day last week and lit up crypto X.

The core argument is structural.

AI agents can’t open bank accounts because banks require identity verification that software cannot provide, whereas a crypto wallet only needs a private key. No KYC, no compliance review, no waiting — and that asymmetry is what Armstrong was pointing at.

But the wallet problem is only half the picture. The other half is economics.

Agents don’t shop the way humans do. When an AI agent is executing a task — such as researching a topic, coordinating a supply chain, building a report — it might call dozens of specialized APIs in a single session.

Each call might be worth fractions of a cent, where it pays for GPU compute time, real-time data feeds, web scraping services, or hiring a sub-agent to handle translation. None of these transactions resembles anything Visa or Mastercard was designed to process.

Consider, for a moment, that this story was written by an agent, requested by a “chief” agent at CoinDesk tasked with increasing the site’s authority.

To produce it, that agent would have queried a real-time news API to verify Armstrong’s tweet ($0.002), pulled onchain data to search for volume figures ($0.004), cross-referenced press releases ($0.001), and pinged a financial context model for Visa protocol details ($0.003). It would finally generate the article at an additional cost, paying credits to another AI tool to actually write the piece.

The total cost of reporting is under two cents with six transactions, at the current figures offered by protocols such as x402.

In contrast, Stripe’s minimum processing fee on a single transaction is around $0.30. Running those six payments through a card network would cost more than 100 times the value of the payments themselves.

A human editor reviewing and publishing the piece might then be billed by a sub-agent that handled SEO optimization, another that ran plagiarism checks, and another that formatted for CMS software. Each micropayment is economically absurd on card rails, but trivial onchain.

This is the thesis behind x402, Coinbase’s open payment protocol that embeds stablecoin payments directly into HTTP requests — so an agent can hit a paywall, pay in USDC, and continue its task in the same interaction, no human required. Cloudflare, Circle, AWS, and Stripe are all backing it. Google’s open agent payments standard includes x402 as a settlement layer.

Every industry with high-frequency, low-value data exchange becomes a candidate.

In healthcare, an agent managing a patient’s insurance claim pays per document retrieved from a medical records API. In logistics, a procurement agent auctions freight slots across dozens of carriers in real time, settling the winning bid instantly. In the media, AI crawlers pay per article indexed rather than negotiating bulk licensing deals. In finance, a trading agent pays a specialist model fractions of a cent per risk signal consumed.

A caveat, however, is that the infrastructure is ahead of the demand.

CoinDesk reported this week that x402 currently processes around $28,000 in daily volume, with Artemis flagging roughly half of observed transactions as artificial activity rather than real commerce. The merchants x402 was built to serve are still rare.

Meanwhile, traditional finance is not standing still. Visa launched its Trusted Agent Protocol last October, and Mastercard completed Europe’s first live AI-agent bank payment inside Santander’s regulated infrastructure last week — both on existing card rails with cryptographic verification layered on top.

The most likely outcome is a split, where regulated commerce stays on card rails, while machine-to-machine payments — such as agents hiring agents, paying per API call, buying compute on demand — migrate to stablecoins because the economics demand it.

The open question is which bucket ends up bigger.

The Ethereum Foundation completed a $10.2 million over-the-counter sale of 5,000 ETH to BitMine at $2,042.96 per token as part of treasury management.

The Ethereum Foundation has completed an over-the-counter sale of 5,000 ETH to BitMine Immersion Technologies for $10.2 million, priced at $2,042.96 per token. The OTC transaction represents a strategic move by the foundation to manage its treasury and fund ongoing operations and ecosystem development initiatives.

The sale signals continued institutional engagement with Ethereum and the foundation’s active approach to treasury liquidity management. OTC deals of this scale are typically used to avoid market impact while securing capital for long-term protocol funding and ecosystem support.

Sources: Cointelegraph | KuCoin Insights | TokenPost | Our Crypto Talk | Coin Bureau

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Norovirus outbreak sickens 153 on Star Princess cruise ship, CDC says

Remittix Has Real Utility As Dogecoin & Pepe Traders Snap Up $RTX Tokens As Presale Set To End

A Brutal April Exit Looms for Taylor Sheridan’s 8-Part Spy Thriller

-

Tech4 days ago

Tech4 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

Crypto World1 day ago

Crypto World1 day agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

News Videos6 days ago

News Videos6 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Business5 days ago

Business5 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Crypto World6 days ago

Crypto World6 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Addict Lip Glow

-

Tech5 days ago

Tech5 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Sports23 hours ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

NewsBeat4 days ago

NewsBeat4 days agoResidents reaction as Shildon murder probe enters second day

-

Business7 days ago

Business7 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business4 days ago

Business4 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat6 days ago

NewsBeat6 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech6 days ago

Tech6 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Business1 day ago

Business1 day agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

NewsBeat4 days ago

NewsBeat4 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Crypto World20 hours ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business6 days ago

Business6 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

Sports6 days ago

Sports6 days agoSkateboarding World Championships: Britain’s Sky Brown wins park gold

-

Business1 day ago

Business1 day agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World5 days ago

Crypto World5 days agoWill Chainlink price reclaim $10 amid volatility squeeze?