Crypto World

Micron (MU) Stock Plummets 15% Despite Record-Breaking Quarterly Performance

Key Takeaways

- Micron shares declined approximately 15% across four consecutive trading sessions following exceptional Q2 fiscal 2026 results

- Quarterly revenue reached $23.86 billion, representing nearly a 200% surge from the prior year’s $8.05 billion

- According to CEO Sanjay Mehrotra, current production capacity meets only 50% to 66% of major customer demand

- Competitor SK Hynix announced plans for an $8 billion EUV equipment investment and potential $10 billion U.S. stock listing — intensifying competitive dynamics

- Leading Wall Street firms including Bank of America, Morgan Stanley, and JPMorgan elevated their price projections following the earnings announcement

Micron delivered exceptional quarterly results last week. Wall Street’s reaction? A double-digit decline.

Following the release of Q2 fiscal 2026 earnings on Wednesday, Micron shares have experienced consecutive daily losses spanning four trading sessions. The negative price action has left many observers perplexed, particularly considering the impressive financial metrics.

Quarterly revenue totaled $23.86 billion — representing approximately a threefold increase from the $8.05 billion Micron generated during the comparable quarter last year. Management also projected gross margin percentages hovering around 80% for the upcoming quarter.

Despite the recent downturn, Micron shares have surged more than 300% over the trailing twelve months. The memory chip manufacturer stands as the sole technology company among America’s top 10 market leaders posting year-to-date gains, while Oracle and Microsoft have both retreated over 20%.

Citi’s semiconductor analyst Atif Malik attributed the selloff primarily to investor profit-taking. “Higher FY27 capex and peak gross margin concerns (81% > Nvidia’s 75%) likely induced some profit taking after a strong stock run into the print,” he noted.

Production Capacity Lags Behind Customer Requirements

CEO Sanjay Mehrotra spoke openly about current supply constraints during an interview with CNBC’s Squawk on the Street on Thursday.

“Memory today is very tight supply and supply cannot be brought up that easily,” he explained. Major clients are presently obtaining only “50% to two-thirds of their requirements.”

This supply squeeze stems directly from artificial intelligence demand. Micron, SK Hynix, and Samsung collectively dominate the high-bandwidth memory segment that powers AI processors from manufacturers such as Nvidia and AMD.

The explosion in AI infrastructure investments has elevated memory pricing while keeping availability constrained. Mehrotra indicated the company’s robust financial performance directly mirrors these market dynamics.

Major financial institutions including Bank of America, Morgan Stanley, and JPMorgan raised their valuation targets for Micron following the quarterly disclosure, suggesting analysts remain optimistic about longer-term prospects despite near-term share price weakness.

South Korean Rival Escalates Competition

Compounding investor concerns this week, SK Hynix unveiled two significant strategic initiatives that unsettled Micron shareholders.

The Seoul-based chipmaker submitted regulatory documentation on Tuesday revealing intentions to acquire approximately $8 billion worth of extreme ultraviolet (EUV) lithography systems from ASML through the end of 2027 — representing a substantial commitment to advanced manufacturing capabilities.

Simultaneously, Korea Economic Daily published reports indicating SK Hynix is evaluating a potential U.S. stock exchange listing that could generate up to $10 billion in capital. U.S. investors presently face restricted access to SK Hynix equity, with most exposure limited to over-the-counter trading or exchange-traded funds such as the iShares MSCI South Korea ETF.

A domestic U.S. listing could fundamentally alter investment flows within the memory semiconductor sector. SK Hynix currently commands a forward price-to-earnings multiple of approximately 4.8 times, compared to Micron’s 5.3 times valuation, based on FactSet data.

During Tuesday’s midday trading session, Micron shares declined an additional 2.4%, prolonging the post-earnings retreat to four consecutive sessions.

The US banking lobby is mounting a last-minute push to stall the CLARITY Act just days before its scheduled Senate Banking Committee markup on May 14.

Summary

- Five major banking groups jointly rejected the Tillis-Alsobrooks stablecoin yield compromise, calling it insufficient days before the May 14 markup.

- Senators Lummis and Tillis publicly defended the deal, warning that banking opposition may be aimed at killing the CLARITY Act altogether.

- Prediction markets currently price the bill’s odds of becoming law in 2026 at over 60%, with the White House targeting a July 4 presidential signature.

The American Bankers Association, the Bank Policy Institute, the Consumer Bankers Association, the Financial Services Forum, and the Independent Community Bankers of America issued a joint statement this week rejecting the compromise stablecoin yield language drafted by Senators Thom Tillis and Angela Alsobrooks. The coalition said the proposed language falls short of its policy goals and leaves dangerous loopholes that could trigger deposit flight from traditional banks.

The banking groups argue that Section 404 of the CLARITY Act still permits crypto platforms to offer rewards tied to account balances and how long users hold assets, which they say amounts to offering deposit interest under a different name. “Research demonstrates that yield-earning stablecoins could reduce all consumer, small-business, and farm loans by one-fifth or more,” the coalition said in its joint statement, adding that it is “imperative that Congress get this right.”

Lummis and Tillis push back

The response from the bill’s sponsors was immediate. Senator Cynthia Lummis, who chairs the Senate Banking Subcommittee on Digital Assets, posted on X that the finalized bipartisan text “is the culmination of months of hard work to deliver a compromise on yield we can all live with.” Senator Tillis, who co-authored the deal, was sharper in his pushback, warning that certain factions within traditional finance may simply oppose any version of the CLARITY Act and are using the stablecoin yield debate as a mechanism to stall the legislation indefinitely.

Tillis’s closing line in his public defense left little room for ambiguity: “Some in the banking industry may not want either of these things to happen, and we respectfully agree to disagree.” The synchronized public defense from Lummis and Tillis signals the bipartisan coalition behind the compromise is holding firm as the markup window narrows.

The CLARITY Act cleared the House 294 to 134 in July 2025 and passed the Senate Agriculture Committee in January 2026, but has repeatedly stalled in the Senate Banking Committee over the stablecoin yield dispute. As crypto.news reported, senators including Cynthia Lummis and Bernie Moreno have said that failure before the May 21 Memorial Day recess could push the next viable window to 2030.

What comes next

Senate Banking Committee Chairman Tim Scott confirmed the markup hearing for May 14 at 10:30 am. The White House has set a July 4 target for passage, with crypto adviser Patrick Witt describing the stablecoin yield deal as closed. Ripple CEO Brad Garlinghouse said at Consensus Miami 2026 this week that the past week represented a “big positive shift” in Senate momentum.

Galaxy Digital head of research Alex Thorn has estimated the bill’s passage odds at roughly 50-50, while prediction markets currently put the figure above 60%. A HarrisX poll released this week found that 52% of registered US voters support the CLARITY Act, with 47% saying they would consider backing a candidate outside their preferred party if that candidate supported the legislation and theirs did not.

For the bill to reach the president’s desk, it must clear the Senate Banking Committee markup, survive a 60-vote floor threshold, be reconciled with the Senate Agriculture Committee version, and then reconciled with the House-passed text. Each of those steps carries its own risk of failure.

Key Highlights

- Shares of APH declined 6.29% as investors took profits after a robust earnings-driven rally

- First quarter 2026 earnings per share reached $1.06 versus analyst expectations of $0.95; sales totaled $7.62B against forecasts of $7.08B

- Analysts at Wall Street Zen and Zacks moved their ratings to “Hold” from “Buy”

- Chief Executive Richard Norwitt offloaded more than 515,000 shares during February for approximately $75.9M

- Average analyst price target stands at $176.53 supported by 13 Buy recommendations and 2 Hold ratings

Shares of Amphenol (APH) tumbled 6.29% on Friday, beginning the session at $127.72, as market participants retreated following a sustained period of appreciation.

The decline seems driven by profit-taking dynamics rather than fundamental deterioration in the company’s operations. APH had experienced a significant run-up prior to its earnings announcement, prompting some investors to lock in gains.

The company’s first quarter 2026 performance exceeded expectations across key metrics. Earnings per share landed at $1.06, comfortably surpassing the Wall Street consensus of $0.95. Revenue figures impressed at $7.62 billion, substantially outpacing the anticipated $7.08 billion — representing a remarkable 58.4% year-over-year increase.

Looking ahead to Q2 2026, management provided earnings guidance between $1.14 and $1.16 per share. The Street’s current projection for full-year earnings stands at $4.76 per share.

Despite the impressive quarterly performance, market participants appear to be reassessing valuation levels. APH currently commands a price-to-earnings multiple of 36.70 alongside a PEG ratio of 1.20.

Analyst Rating Adjustments Create Headwinds

Wall Street Zen downgraded APH from “Buy” to “Hold” over the weekend. Zacks implemented an identical rating change in March, pointing to valuation considerations as the primary rationale.

However, the overall analyst community maintains a constructive outlook. Among the 15 firms covering the stock, 13 maintain Buy recommendations while only 2 assign Hold ratings. The consensus price objective rests at $176.53.

Evercore boosted its price target to $180 with an “Outperform” stance following the earnings release. Truist demonstrated even greater confidence, elevating its target to $200 while maintaining its “Buy” rating. Barclays similarly preserved its “Overweight” recommendation with a $180 price target.

Executive Share Sales Raise Questions

Chief Executive Officer Richard Adam Norwitt divested 515,281 shares throughout February at a mean price of $147.27, generating proceeds of approximately $75.9 million. This transaction reduced his direct stake by 21.09%.

Collectively, company insiders have disposed of 646,056 shares during the past 90 days — generating combined proceeds near $94.6 million.

While insider transactions don’t necessarily indicate problems ahead, the magnitude and timing of these sales have caught investors’ attention.

Institutional investors continue to maintain substantial holdings at 97.01% of outstanding shares. Multiple smaller investment firms established new positions during Q4 and Q1, though at relatively modest scale.

An additional consideration affecting investor sentiment involves a recent senior notes offering that elevated the debt-to-equity ratio to 1.18. While not particularly concerning, this development adds another variable for balance sheet-focused investors to monitor.

The stock’s 52-week trading range extends from $80.32 to $167.04. The 50-day moving average currently sits at $137.31, while the 200-day moving average registers at $139.35 — both positioned above the present trading price.

APH has generated a year-to-date return of 1.30%, and technical indicators continue to flash a Buy signal. The company maintains its regular quarterly dividend distribution.

Dogecoin’s three-week surge has run out of road. DOGE hit a local peak above $0.116 two days ago before reversing sharply, posting a -3.37% 24-hour decline and a -1% seven-day drop according to CoinGecko, and the key question now is whether this is a brief consolidation or the start of a steeper leg down and how does it affect Maxi Doge.

The rally had carried DOGE roughly 29% from its mid-April low near $0.091, but analysts were already skeptical: no fundamental catalyst ever clearly explained the move.

Trading volume surged 55.80% to over $3 billion in the last 24 hours, signaling panic-adjacent activity rather than conviction buying.

Speculation around X Money integration and SpaceX’s IPO briefly lifted sentiment, but neither story materialized into hard news. Broader crypto market momentum has also stalled, compounding pressure on high-beta meme assets like DOGE.

Can Dogecoin Price Recover Above $0.12 This Week?

DOGE is currently trading near $0.107 across major exchanges, with immediate support at the $0.10 recent low identified on KuCoin and resistance clustered at the $0.115 48-hour high.

A clean break back above resistance would require a catalyst, and none is confirmed on the near-term calendar. The 24-hour volume spike (north of $3 billion) looks more like distribution than accumulation at this stage.

Dogecoin price bull case it to hold $0.105, reclaims $0.116, and macro tailwinds from a dovish Fed surprise push it toward the $0.13–$0.14 range.

Possible, not probable. However, this scenario will be invalidated if support at $0.10582 breaks on elevated sell volume, opening a path toward $0.09 or lower, still miles above the $0.091 floor printed in mid-April, but psychologically brutal for retail holders.

Context matters here. DOGE remains -66.9% from its all-time high of $0.7316 (May 2021) and -76% from its 2025 peak of $0.48, per Coinbase data.

A recovery to even half its cycle high would require a multi-billion-dollar capital rotation that simply isn’t visible in current order flow. This suggests the path of least resistance remains sideways-to-lower until a genuine macro or ecosystem catalyst emerges.

How Maxi Doge Is Looking to Replace Dogecoin, Is It Early to Get?

When an established meme coin stalls at a fraction of its former highs, capital tends to rotate.

Early-stage presales absorb some of that restless liquidity, and Maxi Doge ($MAXI) has been doing exactly that, approaching $5 million raised with $4.7 million collected at the time of writing.

MAXI DOGE runs on Ethereum (ERC-20) at a current presale price of $0.0002817, pairing a meme-first identity, a 240-lb canine embodying 1000x leverage trading energy (the tagline is “never skip leg-day, never skip a pump,” which is either genius or deranged, possibly both), with structural mechanics including a Maxi Fund treasury for liquidity and partnerships, holder-only trading competitions with leaderboard rewards, and dynamic staking APY.

The positioning is deliberate: where DOGE offers nostalgia, MAXI is pitching grind culture and community upside for buyers entering near the ground floor.

As with any presale, token price discovery post-launch carries real risk, and there are no guarantees of liquidity or returns.

The post Dogecoin Rally Has Stopped: Maxi Doge ICO Approaching $5 Million appeared first on Cryptonews.

To most people, trading in cryptocurrencies like bitcoin , boils down to a simple question: Will prices go up or down?

But there’s another dimension to trading, which is volatility, a measure of how volatile prices could be regardless of direction. It’s already a hugely popular trade in stock markets, and now CME wants to bring it to bitcoin.

The world’s leading derivatives marketplace announced this week its plan to debut Bitcoin volatility futures on June 1, pending regulatory approval.

Unlike traditional bitcoin futures, the new contracts will not track the cryptocurrency’s price directly. Instead, they will refer to the CME CF Bitcoin Volatility Index (BVX), which represents the market’s expectations for bitcoin volatility over the next 4 weeks.

In simple terms, traders will be able to bet on whether bitcoin markets are about to become more chaotic or more stable, without necessarily taking a view on whether prices themselves are heading higher or lower.

“Crypto market participants are seeking regulated products that provide opportunities to gain digital assets exposure when markets move,” Giovanni Vicioso, global head of cryptocurrency products at CME Group, said in the press release. “With our new Bitcoin volatility futures, traders will be able to invest or hedge against the future volatility of bitcoin, allowing them to access a critical new layer of risk management.

Note that offshore exchanges such as Deribit offer futures tied to their own bitcoin volatility indices, but these volatility markets remain relatively small and outside the scope of participation for most U.S. institutions. Moreover, the onshore crypto market still lacks a mature, CME-style bitcoin volatility futures product, so volatility exposure and hedging is primarily achieved through options and other synthetic structures.

CME’s latest offering will expand the exchange’s existing product suite, which includes bitcoin futures and options. Futures went live in December 2017 and have since become the preferred instrument for institutions seeking directional exposure and arbitrage opportunities. They have generated billions in trading volume and open interest, even surpassing offshore giant Binance at one point last year.

This trend of the institutionalization of bitcoin accelerated with the debut of 11 spot-listed bitcoin ETFs in January 2024, and the subsequent debut and rapid rise in popularity of options tied to BlackRock’s IBIT.

So, CME’s volatility futures seem like the next logical step, helping institutions manage risk beyond price direction into volatility itself, according to Sam Gaer, chief investment officer of Monarq Asset Management’s Directional Fund.

“IBIT options open interest surpassing Deribit is a clear signal of institutional demand, and vol futures are the natural next step,” Gaer told CoinDesk in a Telegram message.

Gaer pointed to the way volatility trading evolved in traditional markets, noting that the CBOE Volatility Index, VIX, also known as the fear gauge, didn’t become a deeply liquid asset class on its own. Instead, liquidity accelerated only after exchange-traded funds and broader structured products built around VIX futures created a self-reinforcing ecosystem.

In other words, the growth in volatility trading was driven by derivatives linked to the spot VIX index. Once those products existed, volume attracted more volume, eventually turning volatility into a standalone market in its own right.

“VIX futures did not reach escape velocity until the ETF ecosystem developed around the futures (not the spot index, notably), and the same flywheel dynamic applies here. Volume begets volume. If CME’s product construction and composition are clearly defined and easily disseminated, this has the potential to be a watershed moment for Bitcoin volatility as an asset class,” Gaer said.

Key Highlights

- RKLB shares climbed to a fresh 52-week peak of $105.62 following TD Cowen’s price target increase from $90 to $120 with a Buy recommendation

- First quarter 2026 revenue hit an all-time high of $200.3 million, representing a ~63% increase from the prior year and surpassing analyst projections

- Second quarter revenue outlook upgraded to a range of $225–$240 million, suggesting roughly 16% quarter-over-quarter expansion

- Total order backlog surged 108% to an unprecedented $2.2 billion, with launch services accounting for 42% and space systems making up 58%

- Major wins include a $30 million hypersonic HASTE agreement with Anduril and the strategic purchase of space robotics company Motive Space Systems

Shares of Rocket Lab (RKLB) exploded higher by 34% during Friday’s trading session, finishing at $105.55 after touching a new 52-week high of $105.62 — a dramatic leap from the previous day’s close of $78.58. Trading volume surged to 76 million shares, approximately 247% higher than the three-month daily average.

The dramatic rally followed an exceptional first quarter 2026 earnings release. The company reported record revenue of $200.3 million, representing a 63% year-over-year increase that exceeded Wall Street consensus estimates. The per-share loss narrowed to just $0.07, also outperforming analyst expectations.

TD Cowen wasted no time responding to the strong results. The investment firm boosted its RKLB price objective from $90 to $120 while reaffirming its Buy recommendation, providing additional momentum to an already explosive trading day.

The impressive performance extended beyond just top-line figures. Rocket Lab’s total backlog expanded by 108% to reach an all-time high of $2.2 billion. The composition shows increasing diversification, with 42% attributed to launch services and 58% coming from space systems operations.

Executives also elevated their second quarter revenue projection to a range of $225 million through $240 million. Such performance would represent another quarterly record and indicate approximately 16% growth from the first quarter.

Strategic Contracts and Defense Partnerships

Along with the quarterly performance, Rocket Lab unveiled multiple strategic agreements supporting its forward outlook.

The aerospace company secured what it described as its largest-ever launch agreement, encompassing numerous Neutron and Electron missions for a client that wasn’t publicly disclosed. This deal provides substantial revenue certainty to an already expanding backlog.

Rocket Lab also secured a $30 million HASTE hypersonic launch agreement with Anduril Industries. This collaboration brings together two prominent players in the defense technology sector.

Additionally, a Space Force demonstration project with Raytheon was revealed, further validating strong demand for Rocket Lab’s launch services within the defense industry.

During the quarter, Rocket Lab completed the acquisition of Motive Space Systems, a space robotics company, in a strategic move that could position the firm for expanded involvement in upcoming exploration initiatives.

Wall Street Perspectives

Analyst sentiment leans positive overall, though opinions vary across the Street. Roth MKm increased its price objective from $90 to $100 while maintaining a Buy recommendation prior to the earnings announcement. Cantor Fitzgerald maintained its Overweight stance with an $85 target back in March.

Conversely, Wells Fargo launched coverage in April with an Equal Weight rating and a $60 price target — significantly beneath current trading levels. KeyCorp moved RKLB to Sector Weight in January.

According to MarketBeat consensus data, the stock carries a “Moderate Buy” rating with a mean price target of $90. That average now trails the actual stock price considerably after Friday’s surge.

Recent insider transactions have leaned toward selling activity. Chief Financial Officer Adam Spice offloaded approximately 62,744 shares at $69.59 during March. Insider Frank Klein disposed of 36,768 shares at $71.95 around that same period. Total insider sales over the previous 90 days reached roughly 233,449 shares valued at approximately $16.5 million.

Institutional investors control 71.78% of outstanding shares. The stock’s 50-day moving average currently stands at $72.88, while the 200-day moving average rests at $68.50, both significantly trailing current price levels.

Following Friday’s rally, Rocket Lab’s market capitalization now stands at roughly $61 billion.

Bitcoin is trading below $80,000 as Friday’s U.S. nonfarm payrolls news lands with a sharp miss. April job growth clocked just 62,000 against March’s 172,000. It’s a deteriorating labor market that has previously turbocharged Fed pivot expectations and sent risk assets higher.

However, the complication arrives immediately. The average hourly earnings are running at 3.8% year-on-year, up from 3.5% previously, a wage growth print that keeps the inflation alive and the Federal Reserve’s hands partially tied.

The $120,000 Bitcoin thesis needs both sides of this equation to cooperate. A soft labor market clears one path. It signals the Fed can hold or cut rates, lifting risk assets and reducing the opportunity cost of holding BTC. But sticky wages block that path.

Discover: The best pre-launch token sales

The Jobs Miss News for $120,000 Bitcoin

The macro logic is straightforward. A hiring slowdown of this magnitude reinforces the case that the U.S. labor market is cooling fast enough to keep the Federal Reserve from tightening further. Markets are currently pricing in steady interest rates through 2026. A print this soft could push that hike expectation further out, which is the definition of a dovish repricing.

For Bitcoin, that transmission mechanism is direct. Lower rate expectations compress the dollar, reduce the yield on competing assets, and historically correlate with BTC accumulation by institutional players. The August 2025 playbook is instructive: a 22,000-job payroll news propelled Bitcoin above $113,000 as rate-cut odds surged to near certainty.

The technical picture, though, demands respect for where Bitcoin actually sits right now. Alex Kuptsikevich, chief market analyst at FxPro, puts the structure plainly:

Bitcoin has retreated from its 200-day moving average after briefly entering overbought territory near the upper boundary of its uptrend channel, with the lower channel boundary sitting near $77,500 and a broader trend break requiring a fall below $75,000.

Discover: How Bitcoin’s daily cycles are shaping its path back above $82,000

Wage Growth Is the Variable the Market Can’t Ignore

The 3.8% year-on-year wage growth figure is the speed bump embedded in today’s otherwise Bitcoin-friendly data. Wages at this level sustain services inflation, the stickiest component of the CPI basket, and give the Fed legitimate cover to hold interest rates higher for longer regardless of how weak the headline payrolls print looks.

The transmission mechanism runs in the wrong direction for BTC. Persistent wage growth feeds services prices, which feed core inflation, which feeds a Fed that cannot pivot cleanly. A Fed that can’t pivot means interest rates stay elevated, the dollar stays supported, and the risk premium attached to non-yielding assets like Bitcoin stays compressed.

As long as wage growth holds above 3.5%, the Fed’s dual mandate of maximum employment and price stability remains in active tension, and that tension limits how aggressively markets can price in easing.

The Coinbase Bitcoin Premium Index flipping into a discount this week adds another layer of caution. That index measures the price gap between Bitcoin on Coinbase versus offshore exchanges like Binance. Green readings signal U.S. institutional demand; a discount signals the opposite. The rally above $80,000 stalled precisely when that premium disappeared.

QCP Capital, the Singapore-based trading firm, frames the broader macro risk sharply:

If crude fails to de-escalate before the May 20 FOMC minutes, with Brent already just above $100 a barrel and prediction markets assigning a 97% probability to no Hormuz normalization by May 15, the stagflation narrative becomes much harder to dismiss.

Stagflation is the worst macro environment for Bitcoin’s risk-asset positioning.

Discover: The best crypto to diversify your portfolio with

The post Bitcoin News: $120K Path Hits Wage Growth Speed Bump as U.S. Miss Payrolls appeared first on Cryptonews.

Crypto World

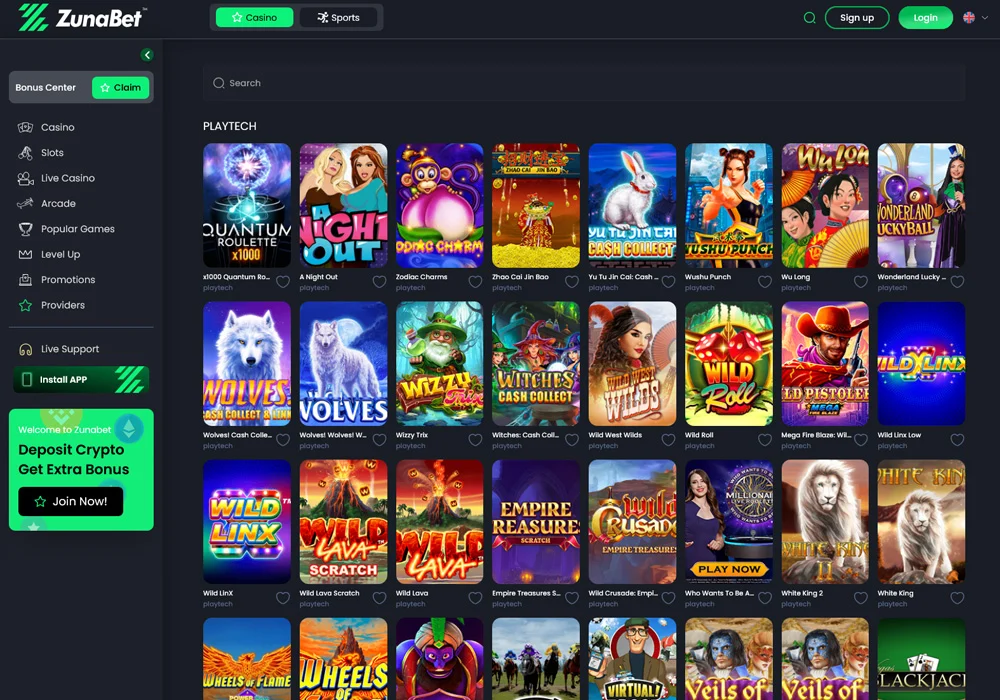

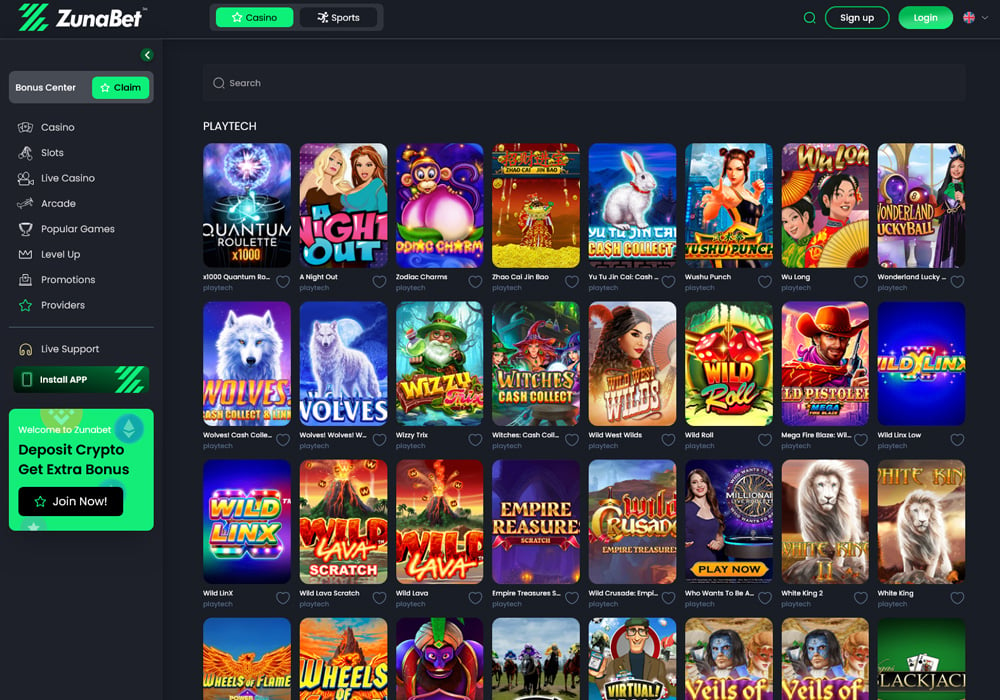

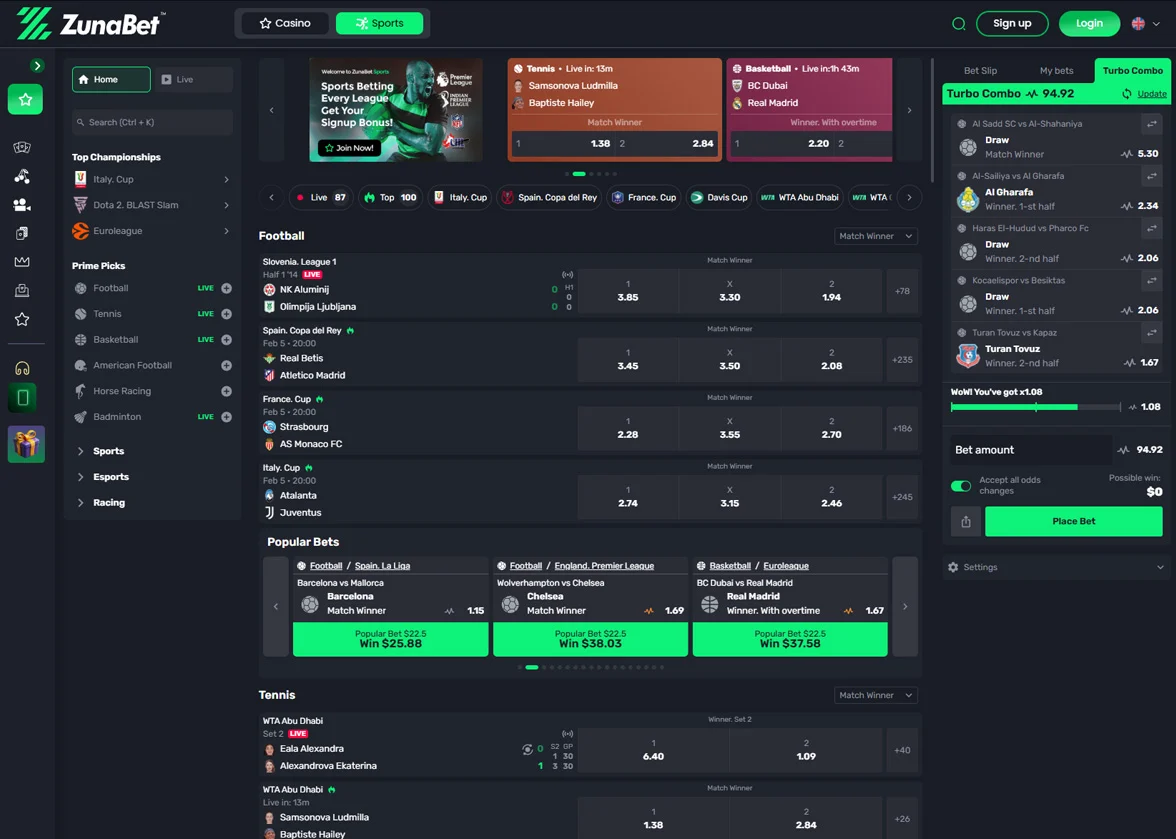

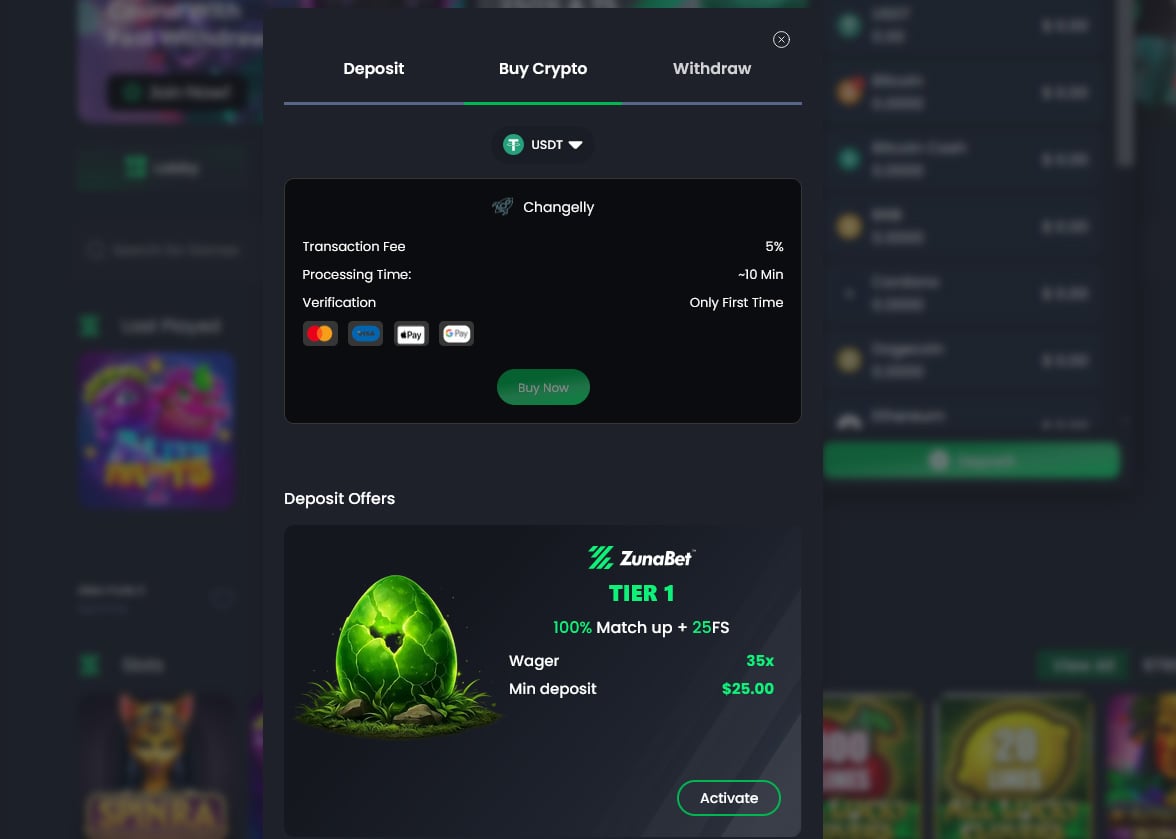

Stake.com Built The Crypto Casino Name. Bet365 Built The Sportsbook Name. ZunaBet Is Building What Comes After Both.

Name recognition in online gambling is built on specialisation. Stake.com built its name by specialising in the crypto gambling community — a platform that understood what crypto-native players valued, built its product around those values, and became the name most associated with crypto casino culture globally. Bet365 built its name by specialising in sportsbook comprehensiveness — a platform that understood what serious sports bettors needed, built an unmatched market coverage product, and became the name most associated with comprehensive sports betting internationally.

Both names reflect genuine specialisation and genuine achievement. Both continue to attract the players their specialisation was built for.

In 2026 a platform is emerging that does not specialise in the same narrow direction as either established name. ZunaBet launched this year with a product that takes what both names do best and builds a more complete offering around it — crypto-native infrastructure at the level of the best crypto casinos, a game library that exceeds what either established platform offers in depth and provider diversity, a sportsbook that covers traditional sports and esports comprehensively, and a loyalty program that delivers transparent direct returns to every player regardless of volume. This article examines all three and explains what comes after specialisation.

Stake.com: What the Crypto Casino Name Was Built On

Stake.com’s name in crypto gambling was built on a foundation of genuine community and genuine crypto credentials. The platform understood that the crypto gambling audience valued more than just accepting Bitcoin — they valued the transparency that crypto culture emphasises, the community that forms around shared platforms and content creators, and the in-house gaming experience that reflects the provably fair principles the space had developed.

The Stake Originals library is the product of that understanding — in-house games built with transparent mechanics, available exclusively on the platform, and carrying the distinctive identity of a product built from within crypto culture rather than adapted toward it. The community that formed around Stake.com through streamer partnerships and player engagement is genuine and it produced the brand recognition the platform carries.

The crypto payment credentials are real. Native cryptocurrency processing rather than third-party layers. Withdrawals at the speed the infrastructure allows. A payment experience that reflects genuine crypto infrastructure rather than fiat banking with cryptocurrency as an option.

The limitations surface when the product is examined beyond its specialisation. The third-party game library — outside Stake Originals — is narrower than the largest dedicated casino platforms. Players who want extensive coverage from the industry’s top third-party providers find the selection more limited than what platforms built specifically around provider diversity offer. The sportsbook covers major markets but is not the product’s primary focus and reflects that in its depth. The loyalty structure delivers clear value at high volumes but is less transparent and calculable for the regular player at moderate activity levels. Geographic restrictions apply in several significant markets.

Bet365: What the Sportsbook Name Was Built On

Bet365’s name in sports betting was built on 25 years of singular investment in one direction — the most comprehensive sportsbook coverage possible. The product that resulted is the industry reference point for market access. Major global sports at full depth, minor events that other platforms do not price, in-play coverage running on competitions that competitors close before they begin, live streaming of events embedded in the platform. The name reflects genuine product leadership in the category it specialised in.

The casino grew alongside the sportsbook. A large library from established providers, strong live dealer content, polished and consistent platform experience. The product is broad and reflects the investment of an operator with the time and resources to build at scale.

The limitations are the limitations of a traditional platform built for a traditional player. Geographic restrictions eliminate the platform for the US market and several others. The loyalty program is structured around invite-only VIP tiers — the general player base operates without meaningful loyalty visibility or a clear pathway toward the levels where rewards matter. Crypto support is minimal. Fiat banking timelines apply throughout.

For the crypto-native player Bet365’s limitations are not incidental — they are structural. The platform was built for a different payment infrastructure, a different loyalty expectation, and a different player profile than the one arriving in growing numbers in 2026.

ZunaBet: Building What Comes After Both

ZunaBet launched in 2026 under Strathvale Group Ltd, operating under an Anjouan gaming license and registered in Belize. The team carries over 20 years of combined industry experience. It is not Stake.com’s community-first crypto brand and it is not Bet365’s 25-year sportsbook institution. It is a crypto-first, internationally accessible platform built to take what both names do well and construct a more complete product around those strengths while addressing what both leave open.

The game library builds what comes after both platforms’ casino offerings. ZunaBet carries 11,294 titles from 63 providers. Stake.com’s strength is Originals — a distinctive in-house product — but its third-party coverage is narrower. Bet365’s casino is substantial but not at the provider diversity level that ZunaBet reaches. Evolution for the full live dealer catalogue. Pragmatic Play across multiple product categories. Hacksaw Gaming for the high-volatility mechanics that experienced players seek. Yggdrasil for its distinctive design philosophy. BGaming for the crypto-native aesthetic. Sixty-three different creative approaches producing content with different mechanics, different volatility profiles, and different visual identities. The library sustains long-term engagement through genuine variety rather than the distinctive identity of Originals or the adequate breadth of an established casino product.

The sportsbook builds what comes after both platforms’ sports coverage for the modern player. Football, basketball, tennis, NHL, and other major global sports alongside CS2, Dota 2, League of Legends, and Valorant as genuine primary markets. Virtual sports and combat sports complete a sportsbook built around the full range of what the 2026 player bets on. The esports coverage in particular goes beyond what either established name prioritises seriously.

The payment infrastructure builds what comes after both platforms’ payment approaches. More than 20 cryptocurrencies supported natively — BTC, ETH, USDT across multiple chains, SOL, DOGE, ADA, XRP, and others. No platform processing fees. Withdrawals settling in minutes. Apps across iOS, Android, Windows, and MacOS with 24-hour live chat support. The crypto credentials are genuine and the breadth of coin support exceeds what either established platform offers.

Payments: What Each Name Built and What Comes After

The payment comparison traces three different positions on the crypto-traditional spectrum.

Stake.com built native crypto payments for the crypto-native player. The infrastructure is genuine and the withdrawal experience reflects it. The specialisation is real.

Bet365 built fiat banking payments for the traditional sports bettor. The infrastructure reflects 25 years of fiat-era operation. Bank transfer, card payment, e-wallet — each with associated timelines. The specialisation is equally real and equally limiting for the player outside its profile.

ZunaBet builds what comes after both — native crypto infrastructure at the level of the best crypto casinos but with a coin breadth that exceeds the typical crypto casino offering. Twenty-plus coins supported natively. Withdrawals in minutes. No fees beyond network costs. The payment position takes Stake.com’s crypto authenticity and extends it across a wider range of currencies and a more complete platform.

For the player who valued Stake.com’s crypto payments but wanted more — ZunaBet’s payment infrastructure is what more looks like.

Loyalty: What Each Name Built and What Comes After

The loyalty comparison reveals three different approaches to rewarding regular players.

Stake.com built a loyalty structure around rakeback and bonuses that delivers clear value at the upper end of the volume curve. The community-driven rewards ecosystem is genuine. For the regular player at moderate volume the structure is less transparent and the effective return less clearly calculable in advance.

Bet365 built a loyalty structure around invite-only VIP tiers. The rewards at those tiers are genuine. For the general player base the structure offers minimal visibility and no accessible pathway toward the levels that matter.

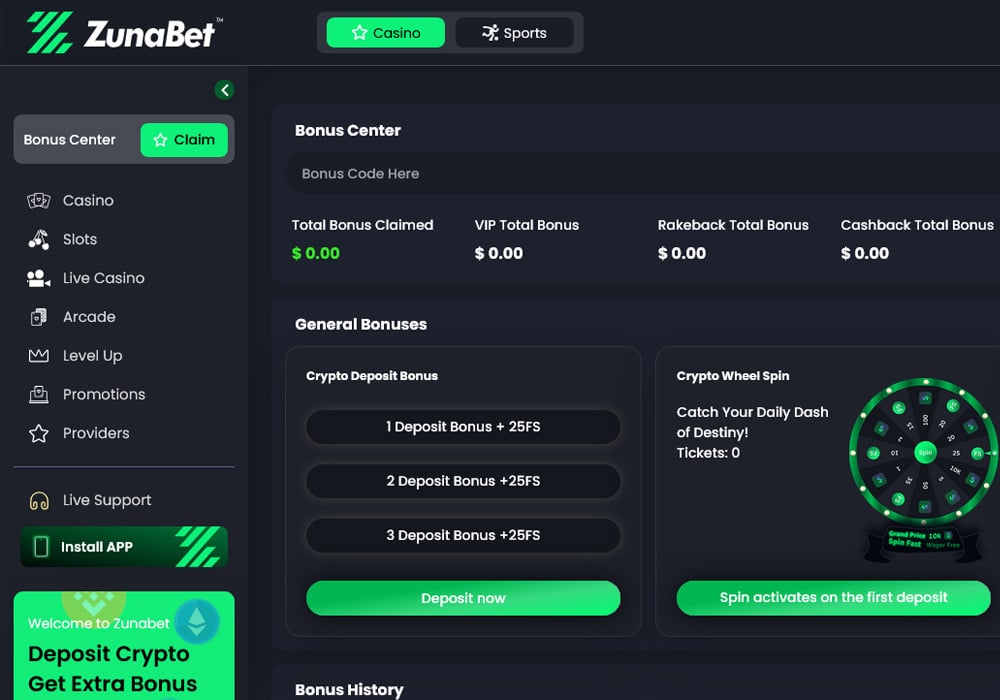

ZunaBet builds what comes after both through the dragon evolution loyalty system. Six tiers — Squire, Warden, Champion, Divine, Knight, and Ultimate — with a gamified mascot called Zuno and direct rakeback rates of 1%, 2%, 4%, 5%, 10%, and 20%. All tiers open to all players. All rates applying to all activity — casino and sportsbook alike. No conversion. No invitation. The transparency that Stake.com’s culture values is built into the structure explicitly and the accessibility that Bet365’s VIP system lacks is available from tier one.

Twenty percent at the Ultimate tier. Calculable before joining. Consistent throughout membership. Additional tier benefits — up to 1,000 free spins, VIP club access, double wheel spins — extend the structure beyond the core rakeback.

The Welcome Bonus

ZunaBet new players receive a bonus across three deposits totalling up to $5,000 plus 75 free spins. First deposit matched 100% up to $2,000 with 25 free spins. Second deposit matched 50% up to $1,500 with 25 spins. Third deposit matched 100% up to $1,500 with 25 spins.

Stake.com and Bet365 offer their own promotional structures for new and existing players. Current terms vary and should be confirmed directly on each platform.

The Player That Comes After Both Names

The player ZunaBet was built for is the player that comes after both established names’ primary audiences. Not the Stake.com community member whose primary relationship with the platform is through streamers and Originals. Not the Bet365 sports bettor whose primary criterion is traditional market coverage. The player who wants crypto-native infrastructure across twenty-plus coins, a game library from sixty-three providers, serious esports coverage, and a loyalty program that states its return clearly before they commit to earning it.

ZunaBet launched in 2026 and is still establishing the track record that both established names built over years of consistent operation. That gap is real and players should weigh it honestly.

But what comes after both names — the platform that takes crypto authenticity, game library depth, sportsbook breadth, and loyalty transparency and combines them in a single product — launched in 2026. That platform is ZunaBet and the player it was built for is finding it.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Payward, the parent company of cryptocurrency exchange Kraken, has filed an application with the U.S. Office of the Comptroller of the Currency (OCC) for a national trust company charter. If approved, the plan would establish Payward National Trust Company to provide fiduciary custody and related services primarily for digital assets, signaling a step toward deeper integration with traditional banking infrastructure for crypto firms.

In a Friday notice, Payward said the OCC charter, if granted, would build on its current Special Purpose Depository Institution (SPDI) status established in Wyoming through Kraken Financial, and on its Federal Reserve master account, which gives it access to the U.S. payment system. The move aligns with a regulatory trend that has already seen the OCC grant similar charters to other digital-asset firms and marks a potential shift in how crypto firms access insured custody and standard banking rails.

A national trust company provides the certainty institutions require and establishes the infrastructure to build the next generation of custody,” Kraken co-CEO Arjun Sethi said. “This is not about being first; it is about getting the framework right so markets can scale with clarity, interoperability, and long-term vision for what clients will demand as these systems mature.”

The OCC’s actions to date have drawn scrutiny as it weighs applications from a mix of crypto incumbents. Earlier, the agency approved national trust charters for Ripple Labs, BitGo, Circle, Fidelity Digital Assets and Paxos in December, part of a broader push to formalize the custody and banking infrastructure underpinning digital assets. The agency’s leadership, including Jonathan Gould, Trump-era nominee who heads the OCC, has attracted attention for deploying charters in this sector while considering other high-profile filings, such as World Liberty Financial’s crypto-related bid.

Payward notes that the OCC application would extend the capabilities of Kraken Financial, the Wyoming-SPDI subsidiary, and would complement its existing Federal Reserve master account access. The charter would, in effect, aim to bridge the gap between digital-asset custody and the traditional financial system, providing a regulated framework that institutions often require for scale and interoperability.

Kraken’s broader growth ambitions and regulatory context

While the OCC process unfolds, Kraken’s parent company has been actively pursuing growth through other avenues, hinting at a broader strategy that goes beyond custody. In May, Kraken’s leadership indicated the firm could pursue a U.S. initial public offering (IPO) in the coming years—an aspiration the executives described as being “about 80% ready” to realize by 2027, contingent on market conditions and regulatory clarity. That timeline aligns with the company’s recent activity in expanding its service footprint, including partnerships and acquisitions intended to broaden its product suite beyond spot trading and into custody, derivatives and cross-border settlement.

The same period saw Kraken exiting an array of strategic deals. Payward announced the BitNominal acquisition to expand its derivatives capabilities in the U.S., and it has also disclosed a separate agreement related to Reap, a move that underscores the exchange’s push into crypto-asset offerings that require more sophisticated market infrastructure and risk management. These developments sit alongside Kraken’s broader plan to participate in the evolving ecosystem where custody, settlement, and compliance form the backbone of institutional-grade crypto services.

Kraken’s strategy also interacts with a regulatory backdrop that has become increasingly influential for crypto firms seeking to scale in the United States. The OCC’s willingness to extend charters to a growing set of digital-asset firms signals a potential path to a more formalized banking relationship for crypto companies. Still, the approvals have coincided with ongoing scrutiny over the pace and nature of such charters, particularly as the regulator weighs applications from a spectrum of players with varying business models and risk profiles. Observers will be watching how these titling decisions affect custody standards, customer protection, and the reliability of settlement rails as crypto markets mature.

What to watch next for custody, banking rails, and the crypto market

As Payward’s OCC filing proceeds, investors and users should monitor several lanes of development. First, the fate of the national trust charter itself will shape how other crypto firms structure custody and fiduciary services—potentially lowering conversion frictions for institutions seeking insured, regulated custody arrangements. Second, regulators’ evolving stance on crypto banking infrastructure—especially the interplay between SPDI-like structures and Fed settlement accounts—could influence the cost and timeliness of on- and off-ramps for institutional participants. Third, Kraken’s broader growth plan, including any public listing timeline and the success of its acquisitions and partnerships, will affect the company’s ability to finance its expansion and compete for custody, derivatives, and cross-border services in a crowded market.

Market participants should also note the tension between rapid innovation and regulatory oversight. While the OCC’s track record in approving trust charters for some major players signals a pathway for legitimate crypto custody services, policymakers continue to weigh consumer protection, anti-money-laundering controls, and systemic risk considerations. The coming months should reveal how these factors shape the trajectory of Kraken and similar firms as they seek greater alignment with traditional financial rails while preserving the benefits of decentralized finance and digital-asset innovation.

As this regulatory journey unfolds, observers should keep an eye on any updates around the OCC’s assessments, the timeline for Payward’s charter decision, and the implications for custody standards across digital assets. The outcome could influence a broader shift in how crypto firms access banking services and custody infrastructure, potentially altering the competitive landscape for U.S.-based exchanges and the institutions that serve them.

The US-Iran war has shaken global markets, with safe-haven gold facing headwinds while oil stocks, crypto, and rallied. Yet one commodity has outpaced every major asset class by more than 40 times.

Potato contracts for difference (CFDs) surged roughly 705% in under a month, dwarfing every major asset class.

Follow us on X to get the latest news as it happens

Potatoes Just Outperformed Bitcoin This Month

The 705% jump came during a green month for risk assets. Bitcoin (BTC) gained 13.1% over the past month. Ethereum (ETH) added 6.2%, while the broader crypto market rose 10.8%.

US equities also rallied. The Nasdaq Composite climbed 15%, the S&P 500 added 9.07%, and the Dow Jones Industrial Average rose 2.95%.

Commodity gains were mixed. According to data from Trading Economics, Brent crude rose 5.86%, gasoline jumped 16.1%, and silver added 8.37%. Gold slipped 0.25%, and West Texas Intermediate (WTI) crude fell 2.08%.

Even the strongest performers fell short of the 705% potato CFD move by more than 40 times.

Why Potato Derivatives Are Surging

It’s important to note that the pump reflects financial markets reacting to volatility in the Iran war, not any actual scarcity in physical potato inventories. Euro News reported that the price per 100 kilograms has climbed from roughly €2.11 on April 21 to €18.50 since April 21.

“As potatoes are a nutrient-intensive crop, the sudden lack of affordable fertiliser has direct implications for future yields and current market valuations. To make matters worse, the regional instability has made primary shipping lanes increasingly hazardous, complicating the logistics of agricultural trade,” the outlet wrote.

Even at that level, potato prices remain well below where the market traded over the past two years, as European producers work through a substantial supply glut. Thus, traders are repricing futures based on risks and the broader effects of the Iran conflict.

“Traders are seemingly repricing futures contracts and no longer prioritising the current reality of oversupply. While for European consumers, this does not presently translate to a massive increase in the cost of a basic dietary staple, the move in potato CFDs highlights an anxious market attempting to price the several and encompassing economic effects of the Iran war,” the report read.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post The Best Trade of the Month Wasn’t Crypto or Oil, It Was Potatoes appeared first on BeInCrypto.

Crypto World

5 Chip Stocks Dominating Investor Attention This May: Nvidia (NVDA), AMD (AMD), and More

Key Takeaways

- Semiconductor stocks are experiencing a powerful rally fueled by artificial intelligence demand, with the PHLX Semiconductor Index posting its strongest outperformance versus the S&P 500 in more than 12 months

- Nvidia (NVDA) maintains the most bullish analyst consensus in the sector, boasting 48 buy recommendations and no sell ratings

- AMD (AMD) delivered first-quarter revenue of $10.25 billion with data-center sales surging 57%, prompting over 20 analysts to lift their price targets

- Micron Technology (MU) posted its strongest five-day performance since 2008, jumping 30% on surging demand for AI memory chips

- ASML Holding stands as the only company in this group facing sell-side skepticism, with 2 sell ratings among 21 buy calls

Artificial intelligence continues to dominate market momentum, and semiconductor companies remain squarely in the spotlight. As we move through May 2026, five chip stocks have emerged as the primary focus for investors tracking this critical sector.

The semiconductor benchmark index has recently delivered its most impressive outperformance against the broader S&P 500 in over a year. This rally has spread across multiple chip categories, including graphics processors, memory manufacturers, equipment providers, and connectivity specialists.

Let’s examine the five semiconductor equities capturing the most investor attention right now.

Nvidia (NVDA)

Nvidia maintains its position as the undisputed leader in artificial intelligence silicon. The company’s graphics processing units remain the foundation for both training and deploying sophisticated AI models, while its comprehensive software stack and networking infrastructure position it as far more than just a chip vendor.

Analyst sentiment couldn’t be clearer. According to MarketBeat tracking, Nvidia commands 48 buy ratings, 4 strong buy calls, 2 hold recommendations, and zero sell ratings. This represents one of the most lopsided professional consensus views across the entire equity market.

The primary concern centers on valuation. Following its substantial price appreciation, future gains hinge on whether the company can continue exceeding already elevated earnings forecasts.

Advanced Micro Devices (AMD)

Advanced Micro Devices stands as Nvidia’s primary competitor in the AI chip arena. The company recently reported first-quarter adjusted earnings per share of $1.37 on revenues totaling $10.25 billion, with data-center sales surging 57% compared to the prior year.

Advanced Micro Devices, Inc., AMD

AMD provided second-quarter revenue guidance of approximately $11.2 billion, exceeding Wall Street’s consensus estimates. Following the earnings release, no fewer than 20 brokerage firms increased their price objectives.

Analyst ratings currently stand at 30 buys, 2 strong buys, and 12 holds with no sell recommendations. The challenge lies in rising expectations that have climbed rapidly alongside the share price.

Broadcom (AVGO)

Broadcom offers investors artificial intelligence exposure extending beyond traditional GPU chips. The company’s involvement spans custom AI processors, networking equipment, and infrastructure spending by major technology platforms.

Industry reports have connected Broadcom to custom chip development projects with OpenAI, though questions regarding project financing and customer diversification have also emerged. Analyst sentiment reflects 27 buys, 2 strong buys, and 4 holds with no sell ratings.

Micron Technology (MU)

Micron represents the memory-focused investment opportunity within this group. AI data centers demand high-bandwidth memory solutions, positioning Micron as a direct beneficiary of this infrastructure buildout.

MarketWatch noted that Micron recorded its strongest weekly performance since 2008, advancing 30% across five consecutive trading days and eclipsing JPMorgan’s market capitalization. The analyst community assigns 30 buys, 5 strong buys, and 4 holds with zero sell ratings.

The cautionary element is memory’s historically cyclical nature, where pricing power can deteriorate rapidly if industry supply expands.

ASML Holding

ASML manufactures the specialized lithography systems essential for producing state-of-the-art semiconductors. Without ASML’s equipment, companies including Nvidia, AMD, and TSMC cannot fabricate their most advanced chip designs.

This positions ASML as a critical supply chain enabler rather than a chip producer. The stock carries 21 buys, 3 strong buys, 6 holds, and 2 sell ratings — making it the sole company in this group with any bearish recommendations. Export restrictions and lumpy capital equipment spending patterns represent the principal risk factors.

Bottom Line

The semiconductor industry is responding to genuine infrastructure demand, not speculative enthusiasm. AI computing facilities require processors, memory, and the manufacturing equipment to produce them — and these five companies occupy strategic positions across that value chain. Analyst coverage remains overwhelmingly positive across the group, though valuations have appreciated considerably, requiring investors to carefully balance growth potential against current pricing.

The Best Parts Of Ageing, According To Men Over 50

Man City vs Brentford LIVE: Team news and line-ups from crucial Premier League clash

Probing the link between inflammation and schizophrenia

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World1 day ago

Crypto World1 day agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

NewsBeat6 days ago

NewsBeat6 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Crypto World2 days ago

Crypto World2 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Tech5 days ago

Tech5 days agoImage AI models now drive app growth, beating chatbot upgrades

-

News Videos6 days ago

News Videos6 days agoAP Dhillon – Old Money (Official Audio)

-

NewsBeat2 days ago

NewsBeat2 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Fashion22 hours ago

Fashion22 hours agoWeekend Open Thread: Marianne Dress

-

Entertainment7 days ago

New Netflix Movies in May 2026 — My Top 3 Picks to Stream

-

Sports7 days ago

Sports7 days agoFive killed in Texas plane crash identified as Amarillo pickleball players

-

Crypto World7 days ago

Crypto World7 days agoPi Network Mandates Protocol 23 Upgrade for All Mainnet Nodes Before May 15 Deadline

-

Entertainment7 days ago

Anna Nicole Smith’s Daughter Attends 2026 Kentucky Derby

-

Crypto World7 days ago

Crypto World7 days agoBitcoin mining equities rise in 2026 as BTC lags behind

-

Entertainment7 days ago

Entertainment7 days agoMelissa Joan Hart and More Stars Attend 2026 Kentucky Derby

-

Entertainment7 days ago

Venus Williams’ Best Met Gala Looks Over the Years

-

Business6 days ago

Business6 days agoLuka Doncic Injury Update: Doncic’s Hamstring Recovery Slows Lakers’ Hopes Against Thunder: Can He Run Yet?

-

Business3 hours ago

Business3 hours agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Entertainment7 days ago

Entertainment7 days agoNetflix’s 10-Part Miniseries Based on a True Story Is a Perfect Weekend Binge

-

Entertainment6 days ago

“Storage Wars” star Darrell Sheets' ex-wife breaks silence on his death

-

Sports6 days ago

Sports6 days agoIs Man United v Liverpool on TV? Channel, streaming and how to watch Premier League fixture

-

Business7 days ago

Business7 days agoKuwait International Airport Resumes Operations After Closure as Regional Tensions Ease in 2026

You must be logged in to post a comment Login