Business

M&A Can Be a Big Opportunity. These Stocks Look Like They Could Pop If Deals Close.

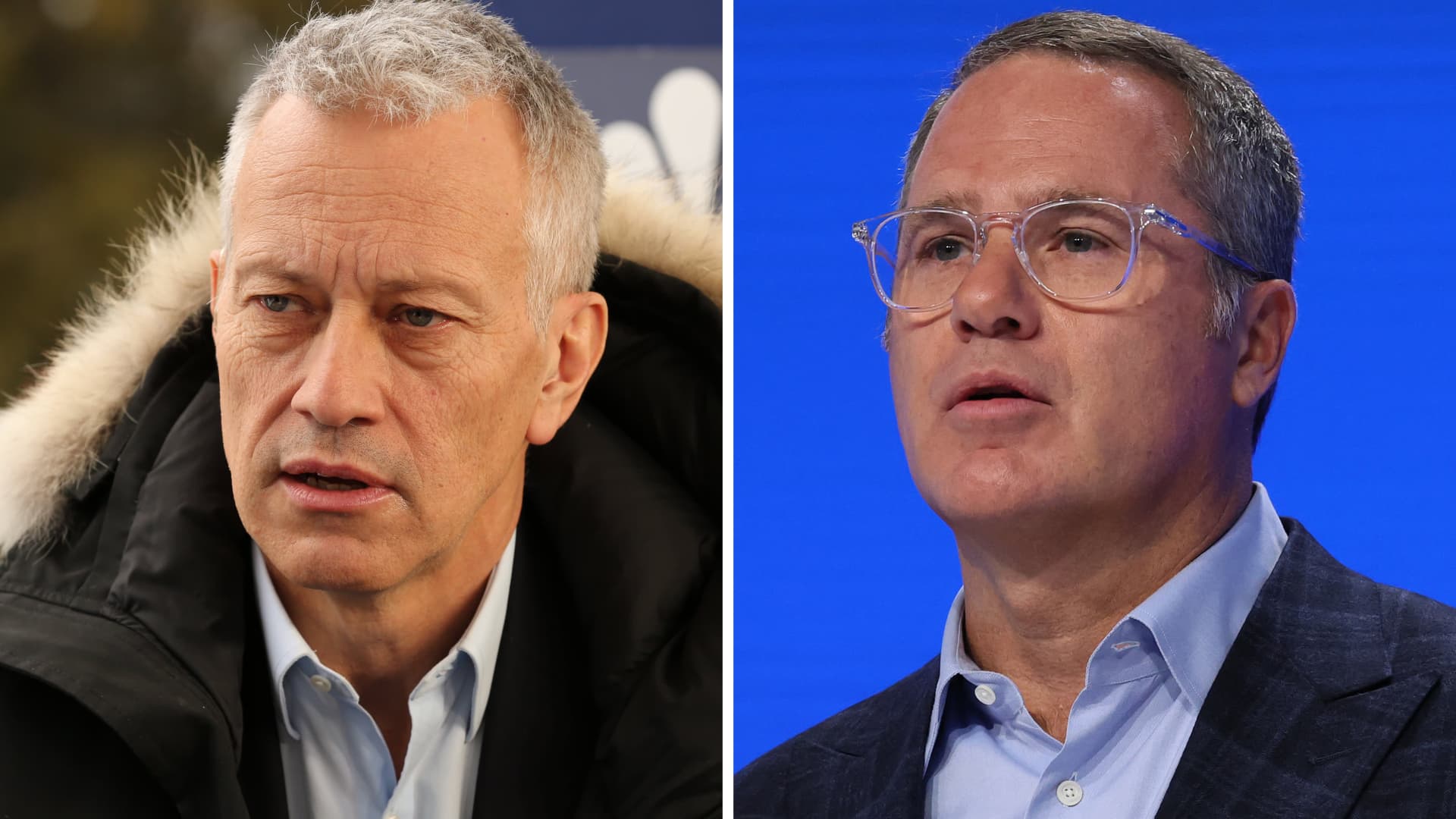

Two major CEOs told CNBC in recent months that the rise of artificial intelligence contributed to their decisions to hand over the reins and step down from their positions.

It’s one of the latest insights into how America’s corporate leaders are sizing up the AI transition.

Coca-Cola CEO James Quincey told CNBC’s “Squawk Box” on Thursday that his decision to step down from his role was influenced by larger “waves of the organizational momentum.”

“My job is also to think who’s the best team to put on the field to get the next wave done,” Quincey said. “And I concluded that, actually, it was time to put someone else on the field for the next wave of growth.”

Quincey, who has served as CEO of the beverage giant since 2017, will be succeeded by current COO Henrique Braun, effective at the end of this month.

“In a pre-AI, a pre-gen-AI mode, we made a lot of progress. But now there’s a huge new shift coming along,” Quincey said.

While he said he’s leaning into the technological advances, he believes the beverage company needs “someone with the energy to pursue a completely new transformation of the enterprise.”

That person, Quincey said, is Braun, who he believes will uniquely equip the company to embrace its next chapter.

Quincey’s comments echo sentiments from former Walmart CEO Douglas McMillon in December ahead of his departure from that role.

McMillon, who had held the position as CEO of the global retailer since 2014, told CNBC’s “Squawk Box” at the time that he had decided to hand over the role to someone “faster.” John Furner, who was previously head of Walmart U.S., took over the top job on Feb. 1.

“With what’s happening with AI, I could start this next big set of transformations with AI, but I couldn’t finish,” McMillon told CNBC.

“About a year ago, I really started feeling like this next run, you could see what agentic commerce was gonna look like, the vision for AI shopping, and I started thinking about everything that needs to happen over the next few years, and it really caused me to think that now was the right time [to step down],” he said.

Walmart in December made the move to list on the Nasdaq, something McMillon said was symbolic of the progress the company has made with technology.

The retailer has been incorporating AI to optimize its supply chain, provide assistants for customers and more.

“I think what you’re going to see from the Walmart team is they’re just going to keep scaling what we’ve already started, build some new stuff on top, and then use AI to transform it all,” he said.

Business

(VIDEO) Galaxy Z Fold 7 Hinge Rated for 500,000 Folds, Samsung Claims Major Durability Leap

Samsung’s Galaxy Z Fold 7, the company’s thinnest and lightest book-style foldable yet, features a folding display certified to withstand 500,000 folds — more than double the rating of its predecessor and enough to theoretically last over a decade for typical users, according to the company and independent certification.

The enhanced durability comes as Samsung continues to push foldable technology into the mainstream, addressing long-standing consumer concerns about hinge wear, screen creases and overall longevity in devices that bend repeatedly. Released in July 2025 following its unveiling at Galaxy Unpacked in Brooklyn, the Z Fold 7 has drawn attention not just for its slimmed-down design but for engineering advances aimed at making foldables feel more like traditional slab smartphones in daily use.

Samsung Display, which supplies the flexible OLED panel, said the inner screen remained fully functional after 500,000 folds in testing conducted over 13 days at 25 degrees Celsius (77 degrees Fahrenheit) by Bureau Veritas, a respected certification firm. The company attributes the improvement to a 50% thicker shock-resistant Ultra Thin Glass (UTG) layer and new high-elastic adhesive materials that better absorb stress.

For context, the Galaxy Z Fold 6 was rated for 200,000 folds, a figure Samsung promoted as sufficient for about five years of average use or 10 years with lighter handling. The jump to 500,000 folds on the Z Fold 7 represents a 150% increase, with Samsung claiming the device could endure more than 10 years for average users folding it roughly 100 times daily or about six years for heavy users exceeding 200 folds per day.

That math is straightforward but optimistic: 500,000 folds divided by 100 daily cycles equals roughly 13.7 years. Real-world variables — temperature, dust exposure, drop impacts and user habits — can affect outcomes. Samsung notes the panel is rated for 300,000 folds at 60 degrees Celsius (140 degrees Fahrenheit) and just 60,000 folds at -20 degrees Celsius (-4 degrees Fahrenheit), highlighting sensitivity to extreme conditions.

The hinge itself received a significant redesign dubbed Armor Flex. It is reportedly 27% thinner and 43% lighter than the mechanism in the Z Fold 6, incorporating advanced alloys and a multi-rail structure for smoother operation and reduced gap when closed. The phone measures just 8.9 millimeters thick when folded — down from 12.1 mm on the prior model — and 4.2 mm when unfolded, weighing 215 grams. Many reviewers describe it as feeling closer to a conventional flagship like the Galaxy S25 Ultra in hand.

Early hands-on durability tests have been largely positive on structural integrity. YouTuber JerryRigEverything subjected the Z Fold 7 to bending, scratching and dusting stresses, finding the hinge held up without seizing even after significant debris exposure. The device survived repeated reverse bending without creaking or loosening in controlled torture tests, though the inner screen still scratches at Mohs hardness level 2, typical for foldable OLEDs.

Not all tests painted a flawless picture. A Korean YouTube channel, Tech-it, manually folded and unfolded a Z Fold 7 unit 200,000 times in a livestreamed stress test. The device continued functioning, but issues emerged: reboot errors starting around 6,000-10,000 cycles, creaking noises by 46,000 folds, an unidentified black liquid leaking from the hinge at 75,000 cycles, and eventual speaker failures by 175,000 folds. The folding action reportedly became smoother over time, and the hinge retained its ability to hold positions at various angles.

Samsung has not directly addressed that specific test but emphasizes that lab ratings reflect controlled, repetitive folding rather than combined real-world stressors like dust ingress, impacts or temperature swings. The Z Fold 7 retains an IP48 rating for dust and water resistance, an incremental improvement but still short of full IP68 protection found on many non-foldable flagships.

User reports in online communities, including Reddit’s r/GalaxyFold, have been mostly encouraging in the months since launch. Owners describe the hinge as feeling more solid, with minimal visible crease progression and reliable daily operation after several months of use. Some note it feels “like a normal phone” when closed, though long-term reliability beyond the first year remains an open question as the device is still relatively new in early 2026.

The Z Fold 7’s other specifications support its premium positioning. It features an 8-inch inner Dynamic AMOLED display and a 6.5-inch cover screen, both with adaptive 120Hz refresh rates. Power comes from a Snapdragon 8 Elite for Galaxy chipset, paired with up to 16GB RAM and storage options reaching 1TB. The camera system includes a new 200-megapixel main sensor — a major upgrade from the 50MP unit on the Z Fold 6 — alongside 12MP ultrawide and 10MP telephoto lenses with 3x optical zoom. Battery capacity sits at 4,400mAh with support for fast charging.

Pricing starts around $2,000, positioning it as a luxury productivity tool rather than an everyday carry for most consumers. Samsung markets the device for multitasking, with features like enhanced Galaxy AI for note-taking, translation and app continuity across the large inner screen.

Industry analysts view the durability claims as a critical step for foldable adoption. While sales of foldables have grown, many potential buyers have hesitated due to past reports of screen failures, hinge issues or creases developing within one to two years. The Z Fold 7’s improvements, combined with a slimmer profile, aim to reduce that friction.

Still, experts caution that foldables inherently involve trade-offs. The flexible screen technology, while advancing rapidly, remains more vulnerable to scratches and impacts than rigid glass. Samsung recommends using the included case or a screen protector and avoiding extreme temperatures or forcing the hinge.

Third-party repair costs for foldables can exceed $1,000 for screen or hinge replacement, making warranty coverage and careful handling important considerations. Samsung offers extended protection plans, but coverage details vary by region.

As of March 2026, the Galaxy Z Fold 7 remains Samsung’s flagship foldable, with no immediate successor announced. Rumors of a Z Fold 8 have surfaced, potentially bringing further refinements such as improved dust resistance or even higher fold ratings, but the Z Fold 7 continues to represent the state of the art in book-style foldables.

Competitors like Google with its Pixel Fold series and Chinese manufacturers including Huawei and Honor have introduced their own durable designs, some claiming IP68 ratings or alternative hinge technologies. Samsung maintains leadership in global market share for foldables, bolstered by its vertical integration in display manufacturing.

For consumers debating a foldable purchase, the 500,000-fold rating provides reassurance on paper. Translating lab results to daily life depends heavily on usage patterns. Light users who open the device primarily for media consumption or productivity may see the hinge last well beyond the warranty period. Heavy users treating it like a pocket notebook could test the limits sooner.

Samsung’s own guidance suggests the Z Fold 7 is built for years of service, but as with any smartphone, factors like software updates — expected through at least 2032 — battery degradation and evolving user needs will influence replacement cycles more than pure mechanical endurance.

The evolution from the original Galaxy Fold in 2019, which faced early screen reliability issues, to the Z Fold 7 illustrates rapid progress in materials science and mechanical engineering. Crease visibility has diminished, hinges operate more smoothly, and overall build quality has improved to rival traditional phones in many respects.

Yet durability remains a narrative Samsung must continue proving in the hands of millions of users. Independent long-term studies and repair data over the next 12-24 months will offer clearer insight into whether the 500,000-fold promise holds up under varied global conditions.

In the meantime, the Galaxy Z Fold 7 stands as a bold statement that foldables can be both innovative and robust enough for everyday carry. Prospective buyers are advised to weigh the unique multitasking benefits against the premium price and the reality that, while vastly improved, these devices still require mindful handling compared to conventional smartphones.

Technical support and software optimizations continue to refine the experience post-launch, with updates addressing minor hinge behaviors or display calibration. As the foldable ecosystem matures, accessories like specialized cases and screen films further enhance protection.

Ultimately, the Z Fold 7’s fold endurance rating marks a significant milestone, potentially accelerating mainstream acceptance of bendable phones. Whether it truly delivers a decade of reliable service will be determined one fold at a time.

U.S. envoy Witkoff says Iran is seeking an off-ramp

Andersons Inc (ANDE) director Bowe sells $1.09 million in stock

Barclays is scaling back lending to smaller businesses and private credit firms after suffering losses linked to the collapse of several high-risk lenders, in a move that signals growing caution across the banking sector.

The lender is understood to be reducing its exposure to asset-based lending for smaller borrowers and shifting its focus towards larger, more established corporate debt providers. The strategy change follows the failures of firms including Market Financial Solutions and Tricolor Holdings, which have triggered losses and heightened concerns about risk within the fast-growing private credit market.

According to reports, Barclays has withdrawn from a number of deals and increased pricing on others to reflect the higher perceived risk environment. The move reflects a broader reassessment of private credit, a sector that has attracted significant investment in recent years due to its promise of higher returns, often in the range of 8 to 10 per cent annually.

However, those returns are frequently underpinned by leverage, amplifying both gains and potential losses. Recent events have exposed vulnerabilities in the sector, including concerns over transparency, asset valuations and rising default rates in a higher interest rate environment.

The collapse of Market Financial Solutions has been particularly damaging. The lender entered administration earlier this year after a High Court judge ordered an investigation into alleged fraud and financial mismanagement. Insolvency practitioners have since claimed there is compelling evidence of serious irregularities, including the possibility that some loans may be entirely unsecured.

Central to the investigation are allegations of “double pledging”, where the same property is used as collateral for multiple loans, a practice that can render assets unrecoverable if borrowers default. Alongside Barclays, several global financial institutions are understood to have exposure to the failed lender.

Barclays chief executive C.S. Venkatakrishnan acknowledged the issue last week, describing the bank’s exposure as “disappointing” but indicating that total losses would remain below £500 million.

The bank’s actions are also under scrutiny. Barclays froze Market Financial Solutions’ accounts last November, a move that insolvency practitioners have suggested may indicate concerns about potential money laundering or other criminal activity. Investigations are ongoing, including oversight from the Financial Conduct Authority.

The fallout has extended beyond the UK. The collapse of Tricolor Holdings, a US-based subprime automotive lender, has added to concerns about the resilience of private credit markets globally, particularly as higher borrowing costs strain borrowers and investors alike.

Recent developments have also unsettled investors, with some private credit funds restricting withdrawals amid rising uncertainty. Analysts say this reflects a shift in sentiment as the sector faces its first significant stress test since its rapid expansion following the global financial crisis.

For Barclays, the decision to pivot towards larger corporate clients suggests a more conservative approach to risk as market conditions tighten. It also raises questions about access to finance for smaller businesses, which may find credit conditions becoming more restrictive as banks reassess their exposure.

The situation underscores the growing tension within financial markets between the search for higher returns and the need for robust risk management — a balance that is being tested as economic conditions become more volatile.

As the investigations continue and the full scale of losses becomes clearer, the implications for both lenders and borrowers are likely to reverberate across the private credit landscape.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

I am a stock analyst with over 20 years of experience in quantitative research, financial modeling, and risk management. My focus is on equity valuation, market trends, and portfolio optimization to uncover high-growth investment opportunities. As a former Vice President at Barclays, I led teams in model validation, stress testing, and regulatory finance, developing a deep expertise in both fundamental and technical analysis. Alongside my research partner (also my wife), I co-author investment research, combining our complementary strengths to deliver high-quality, data-driven insights. Our approach blends rigorous risk management with a long-term perspective on value creation. We have a particular interest in macroeconomic trends, corporate earnings, and financial statement analysis, aiming to provide actionable ideas for investors seeking to outperform the market.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

New offering comes in three flavors.

Here is what we know about the behind-the-scenes mediation efforts:

What is on the table?

After announcing “very good” talks with an unnamed “top person” in Iran on Monday, Trump said Tuesday that he had sent a plan and that it “all starts with, they cannot have a nuclear weapon.”

A 15-point proposal to stop the fighting has been conveyed to Iran via Pakistan, Pakistani officials have confirmed.

But the exact contents remain unknown and the identity of Trump’s “top person” is a mystery, if he exists at all.

The New York Times and Al Jazeera have reported that Trump is proposing a one-month ceasefire during which the two sides would restart talks about the same issues they were discussing before the war.

These include a US demand that Iran hand over its enriched uranium stockpile, stop any further enrichment, and agree to limits on its missile programme, as well as cease support for militant groups in the region.

If Iran met US conditions and opened up the strategic Strait of Hormuz for shipping, which it has effectively closed, Trump is offering relief from all sanctions, the reports suggest.

After saying that Iran wanted to make a deal “so badly”, the US president warned Thursday that they “better get serious soon”.

The head of the UN nuclear watchdog Rafael Grossi has said a meeting in Islamabad at the weekend is under discussion.

What does Iran say?

Publicly, no Iranian official has confirmed any negotiations, but the language used is ambiguous.

Iranian Foreign Minister Abbas Araghchi said messages were “being exchanged through friendly countries or through certain different individuals” but insisted that “this is neither called dialogue nor negotiation”.

But he added that “if it is necessary for a position to be taken, it will certainly be decided”.

Pakistani and Egyptian officials have confirmed they are serving as diplomatic backchannels.

What are Iran’s demands?

According to an unidentified Iranian official cited by Iran’s Press TV on Wednesday, Tehran has sent five conditions for an end to hostilities.

These include ending “aggression and assassinations”, setting up a mechanism guaranteeing that neither Israel nor the United States would resume the war, as well as financial compensation.

They also include a cessation of hostilities on all fronts, meaning Israel would stop bombarding Tehran-backed Hezbollah in Lebanon and possibly Hamas in Gaza.

The official also said Tehran wanted international recognition of its sovereignty over the Strait of Hormuz.

On March 11, Iranian President Masoud Pezeshkian laid out Iranian terms as “recognising Iran’s legitimate rights, payment of reparations, and firm international guarantees against future aggression”.

The Wall Street Journal reported that Tehran was also demanding the closure of US military bases in the Gulf.

Can compromises be found?

Analysts say the conflict has strengthened hardliners in Tehran where the rhetoric is defiant and increasingly confident.

Trump has bombed the country twice amid negotiations, first in June last year and again on February 28.

As for US demands, Tehran has insisted since 2003 it is not seeking a nuclear weapon but has a right to enrich for civilian nuclear energy purposes.

It has also refused curbs on its ballistic missile programme or discussions about its support for militant groups such as Hezbollah or the Houthis in Yemen.

Tehran’s demand for reparations is likely a non-starter, as is any suggestion of the US closing Gulf military bases.

It is not clear how its sovereignty over the Strait of Hormuz would work, or how meaningful security guarantees could be formulated, unless they involved outside powers such as Russia or China.

So is there no hope?

The outcome may come down to how badly Trump wants to end the war, and whether Iran’s leaders view their interests as being best served by a ceasefire.

Trump would walk away claiming victory, saying he has destroyed Iran’s military and nuclear capabilities.

The Islamic republic could also claim victory, pointing to how its forces resisted four weeks of US and Israeli onslaught while also landing blows on US interests in the region and in Israel.

“Both sides need to be able to claim victory and save face, whatever deal they agree on,” a diplomat based in the Middle East told AFP on condition of anonymity. “The process will take some time.”

But even with a ceasefire, the question of Iran’s nuclear programme and its 440-kilogram stockpile of highly enriched uranium remains unresolved.

Some analysts believe the talks are a smokescreen as Trump prepares a ground offensive to re-open the Strait of Hormuz by force or seize Iranian oil assets.

Iran has signalled it would use its Houthi allies in Yemen to attack shipping in the Red Sea, which would open up a new front in a war of spiralling economic, political and military repercussions.

Business

Commonwealth Bank of Australia Raises Home Loan Rates Second Time This Month Amid RBA Hikes

SYDNEY — Commonwealth Bank of Australia, the nation’s largest lender, has increased home loan interest rates for the second time in March 2026, adding further pressure to mortgage holders already grappling with higher borrowing costs following two Reserve Bank of Australia cash rate rises this year.

DAVID GRAY/AFP via Getty Images

On Tuesday, CBA announced a 0.30 percentage point increase to all its fixed-rate home loan products, effective Friday, March 28. The move follows the bank’s earlier 0.25 percentage point hike to variable rates, effective March 27, in response to the RBA’s March 17 decision to lift the official cash rate by 0.25 percentage points to 4.10 per cent.

The latest fixed-rate adjustment pushes some owner-occupier fixed loans as high as 7.19 per cent and investor loans to 7.04 per cent, depending on loan-to-value ratio and product type. This comes after CBA passed on the full 0.25 per cent RBA increase to variable rates earlier in the month, with changes taking effect on March 27.

CBA Group Executive for Retail Banking Angus Sullivan said the bank’s priority remains supporting customers through clear communication and practical assistance options, including repayment pauses or switching to interest-only periods where eligible. However, the back-to-back increases have drawn criticism from consumer groups concerned about affordability strains on Australian households.

Impact on Borrowers

For a typical $600,000 mortgage with 25 years remaining, the combined March hikes could add roughly $90 to $100 or more to monthly repayments, depending on the product mix and whether the loan is fixed or variable. Borrowers on fixed rates rolling off in coming months face particularly sharp resets if they move to higher current fixed or variable offerings.

The RBA’s March decision marked the second cash rate increase of 2026, following a 0.25 percentage point hike in February that took the target from 3.60 per cent to 3.85 per cent before the latest move to 4.10 per cent. The board’s vote was split, with five members supporting the rise and four preferring to hold steady, citing persistent inflation risks and tighter labour market conditions.

All major banks — CBA, Westpac, NAB and ANZ — passed on the full March variable rate increase, with slight variations in effective dates. Westpac’s variable hike takes effect March 31, while CBA, ANZ and NAB implemented theirs on March 27.

Fixed-rate products have also faced upward pressure. CBA’s latest 0.30 per cent adjustment across fixed terms reflects funding cost increases and market expectations of potentially higher rates persisting into 2026.

Broader Market Context

Sydney and other capital city homeowners, already dealing with elevated property prices and cost-of-living pressures, now confront a higher-for-longer interest rate environment. Analysts note that three consecutive rate hikes — February, March and a potential May move — could add up to $8,000 annually to repayments for some metropolitan borrowers, according to earlier forecasts from major banks and comparison sites.

Consumer advocates have urged borrowers to review their loans, contact their lender early for hardship assistance if needed, and consider fixed-rate options or refinancing where savings are available. However, with many lenders tightening or raising fixed rates, refinancing opportunities have narrowed for some customers.

CBA’s announcements align with actions by other big four banks, though smaller lenders and non-banks have shown mixed responses, with some passing on less than the full RBA increase to remain competitive.

Customer Support Measures

In its statement, CBA emphasised support tools for affected customers, including:

- Repayment pause or reduction options for eligible borrowers facing temporary hardship.

- Switching between principal-and-interest and interest-only repayments.

- Access to financial counselling and budgeting assistance through partnerships.

- Online calculators and rate comparison tools on its website to help customers understand personalised impacts.

Fixed Versus Variable Rate Considerations

The dual hikes in March highlight the differing dynamics of fixed and variable products. Variable rates respond directly to RBA moves and funding costs, while fixed rates incorporate market expectations of future rate paths. With the cash rate now at 4.10 per cent and inflation risks skewed higher due to global uncertainties, including Middle East tensions, many economists anticipate the RBA may hold or hike further in coming months.

Borrowers on expiring fixed rates this year could see significant step-ups when reverting to variable rates or new fixed terms. Financial advisers recommend stress-testing budgets at rates 3 percentage points above current levels, as required by responsible lending rules.

Outlook for Mortgage Holders

The RBA has signalled a data-dependent approach, with the next board meeting scheduled for May. Markets currently price in limited immediate further hikes but acknowledge upside risks to inflation from wages growth, capacity constraints and external shocks.

For CBA customers, the March changes mean variable-rate borrowers will see the increase reflected in their April statements, while fixed-rate customers face the new pricing on new or refinanced loans from Friday onward.

Homeowners are advised to:

- Log into their CBA online banking or app to view personalised rate impacts.

- Contact CBA’s customer support line or relationship manager for tailored assistance.

- Compare rates across lenders, noting that some smaller institutions may offer more competitive packages.

- Consider locking in fixed rates if they provide payment certainty, though current levels remain elevated.

- Explore government or lender support schemes if facing genuine repayment difficulty.

While the cash rate remains well below peaks seen in 2022-2023, the rapid reversal of some prior easing has caught many households off guard after a period of relative stability. Consumer groups continue to call for greater transparency from banks on margin management and funding costs during such cycles.

As Australia navigates this tighter monetary policy phase, borrowers with larger loans or those in high-cost cities like Sydney and Melbourne face the greatest relative burden. Early engagement with lenders remains the most effective strategy for managing increased repayments.

EchoStar: The SpaceX Deal May Already Be Priced In

Bad news skeptics – GitHub says it will employ user data to train its AI after all

THE BITCOIN TRAP IS SET…

Netanyahu plots Lebanon ‘invasion’ with new ‘buffer zone’ – grim new Israel border MAPPED

-

Crypto World6 days ago

Crypto World6 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Adidas – Corporette.com

-

NewsBeat1 day ago

NewsBeat1 day agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Politics6 days ago

Politics6 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World5 days ago

Crypto World5 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech6 days ago

Tech6 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

News Videos13 hours ago

News Videos13 hours agoParliament publishes latest register of MPs’ financial interests

-

Sports3 days ago

Sports3 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Politics7 days ago

Politics7 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business4 days ago

Business4 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Sports3 days ago

Sports3 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech4 days ago

Tech4 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports6 days ago

Sports6 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Tech4 days ago

Tech4 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

Business7 days ago

Business7 days agoDLocal: Entering 2026 At Escape Velocity

-

Politics7 days ago

Politics7 days agoScotland’s rejection of assisted dying is a victory for humanity

-

Business6 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

NewsBeat7 days ago

NewsBeat7 days agoMissile lands next to presenter during live report

-

Tech5 days ago

Tech5 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

You must be logged in to post a comment Login