Business

Commonwealth Bank of Australia Raises Home Loan Rates Second Time This Month Amid RBA Hikes

SYDNEY — Commonwealth Bank of Australia, the nation’s largest lender, has increased home loan interest rates for the second time in March 2026, adding further pressure to mortgage holders already grappling with higher borrowing costs following two Reserve Bank of Australia cash rate rises this year.

DAVID GRAY/AFP via Getty Images

On Tuesday, CBA announced a 0.30 percentage point increase to all its fixed-rate home loan products, effective Friday, March 28. The move follows the bank’s earlier 0.25 percentage point hike to variable rates, effective March 27, in response to the RBA’s March 17 decision to lift the official cash rate by 0.25 percentage points to 4.10 per cent.

The latest fixed-rate adjustment pushes some owner-occupier fixed loans as high as 7.19 per cent and investor loans to 7.04 per cent, depending on loan-to-value ratio and product type. This comes after CBA passed on the full 0.25 per cent RBA increase to variable rates earlier in the month, with changes taking effect on March 27.

CBA Group Executive for Retail Banking Angus Sullivan said the bank’s priority remains supporting customers through clear communication and practical assistance options, including repayment pauses or switching to interest-only periods where eligible. However, the back-to-back increases have drawn criticism from consumer groups concerned about affordability strains on Australian households.

Impact on Borrowers

For a typical $600,000 mortgage with 25 years remaining, the combined March hikes could add roughly $90 to $100 or more to monthly repayments, depending on the product mix and whether the loan is fixed or variable. Borrowers on fixed rates rolling off in coming months face particularly sharp resets if they move to higher current fixed or variable offerings.

The RBA’s March decision marked the second cash rate increase of 2026, following a 0.25 percentage point hike in February that took the target from 3.60 per cent to 3.85 per cent before the latest move to 4.10 per cent. The board’s vote was split, with five members supporting the rise and four preferring to hold steady, citing persistent inflation risks and tighter labour market conditions.

All major banks — CBA, Westpac, NAB and ANZ — passed on the full March variable rate increase, with slight variations in effective dates. Westpac’s variable hike takes effect March 31, while CBA, ANZ and NAB implemented theirs on March 27.

Fixed-rate products have also faced upward pressure. CBA’s latest 0.30 per cent adjustment across fixed terms reflects funding cost increases and market expectations of potentially higher rates persisting into 2026.

Broader Market Context

Sydney and other capital city homeowners, already dealing with elevated property prices and cost-of-living pressures, now confront a higher-for-longer interest rate environment. Analysts note that three consecutive rate hikes — February, March and a potential May move — could add up to $8,000 annually to repayments for some metropolitan borrowers, according to earlier forecasts from major banks and comparison sites.

Consumer advocates have urged borrowers to review their loans, contact their lender early for hardship assistance if needed, and consider fixed-rate options or refinancing where savings are available. However, with many lenders tightening or raising fixed rates, refinancing opportunities have narrowed for some customers.

CBA’s announcements align with actions by other big four banks, though smaller lenders and non-banks have shown mixed responses, with some passing on less than the full RBA increase to remain competitive.

Customer Support Measures

In its statement, CBA emphasised support tools for affected customers, including:

- Repayment pause or reduction options for eligible borrowers facing temporary hardship.

- Switching between principal-and-interest and interest-only repayments.

- Access to financial counselling and budgeting assistance through partnerships.

- Online calculators and rate comparison tools on its website to help customers understand personalised impacts.

Fixed Versus Variable Rate Considerations

The dual hikes in March highlight the differing dynamics of fixed and variable products. Variable rates respond directly to RBA moves and funding costs, while fixed rates incorporate market expectations of future rate paths. With the cash rate now at 4.10 per cent and inflation risks skewed higher due to global uncertainties, including Middle East tensions, many economists anticipate the RBA may hold or hike further in coming months.

Borrowers on expiring fixed rates this year could see significant step-ups when reverting to variable rates or new fixed terms. Financial advisers recommend stress-testing budgets at rates 3 percentage points above current levels, as required by responsible lending rules.

Outlook for Mortgage Holders

The RBA has signalled a data-dependent approach, with the next board meeting scheduled for May. Markets currently price in limited immediate further hikes but acknowledge upside risks to inflation from wages growth, capacity constraints and external shocks.

For CBA customers, the March changes mean variable-rate borrowers will see the increase reflected in their April statements, while fixed-rate customers face the new pricing on new or refinanced loans from Friday onward.

Homeowners are advised to:

- Log into their CBA online banking or app to view personalised rate impacts.

- Contact CBA’s customer support line or relationship manager for tailored assistance.

- Compare rates across lenders, noting that some smaller institutions may offer more competitive packages.

- Consider locking in fixed rates if they provide payment certainty, though current levels remain elevated.

- Explore government or lender support schemes if facing genuine repayment difficulty.

While the cash rate remains well below peaks seen in 2022-2023, the rapid reversal of some prior easing has caught many households off guard after a period of relative stability. Consumer groups continue to call for greater transparency from banks on margin management and funding costs during such cycles.

As Australia navigates this tighter monetary policy phase, borrowers with larger loans or those in high-cost cities like Sydney and Melbourne face the greatest relative burden. Early engagement with lenders remains the most effective strategy for managing increased repayments.

Equity mutual funds saw a strong performance last week, with over 8% returns for the category. Among the top performers, international funds like Mirae Asset Global X Artificial Intelligence & Technology ETF FoF led the pack with an 8.49% gain.

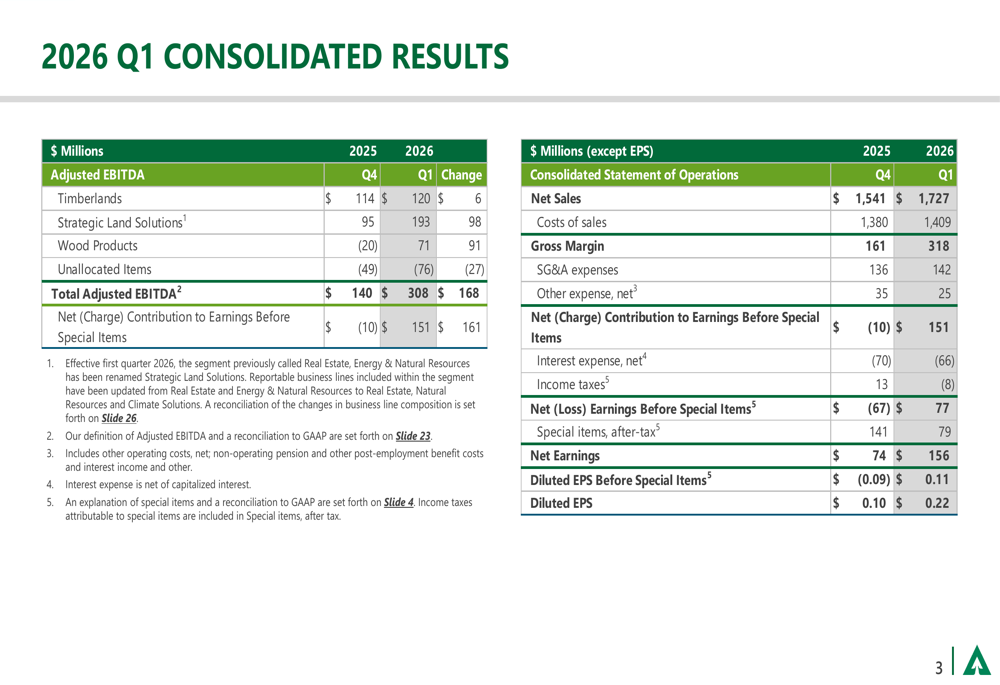

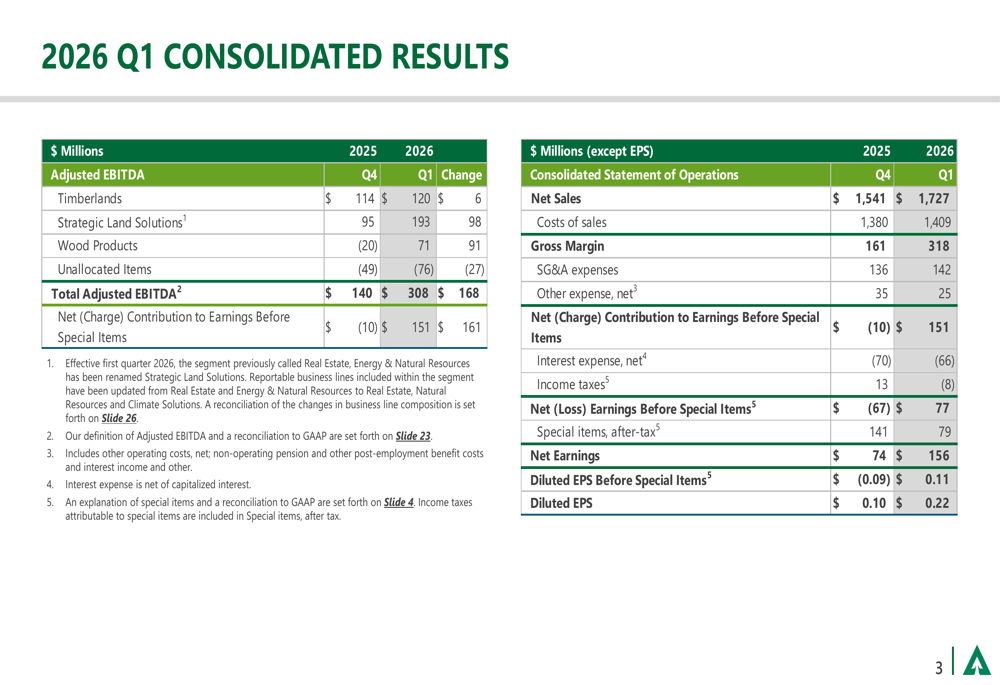

Weyerhaeuser Q1 2026 slides: EBITDA surges on climate deal

Operator

Good day, and thank you for standing by. Welcome to the Alarm.com First Quarter 2026 Earnings Conference Call. [Operator Instructions] Please be advised today’s conference is being recorded. I would now like to hand the conference over to your speaker today, Matthew Zartman. Please go ahead.

Matthew Zartman

Vice President of Strategic Communications & Investor Relations

Thank you. Good afternoon, everyone, and welcome to Alarm.com’s First Quarter 2026 Earnings Conference Call. Please note that this call is being recorded. Joining us today are Steve Trundle, our CEO; and Kevin Bradley, our CFO.

During today’s call, we will be making forward-looking statements, which are predictions, projections, estimates and other statements about future events. These statements are based on current expectations and assumptions that are subject to and uncertainties that may cause actual results to differ materially from our current expectations. We refer you to the risk factors discussed in our Form 8-K and the associated press release, which were filed with the SEC earlier today. The call is subject to these risk factors, and we encourage you to review them.

Alarm.com assumes no obligation to update forward-looking statements or other information that speak as of their respective dates. In addition, several non-GAAP financial measures will be discussed on the call. A reconciliation of GAAP to non-GAAP measures can be found in today’s press release on our

Rupak De, Senior Technical Analyst at LKP Securities, said the mood has further deteriorated as the index also moved below the 50-day EMA on the intraday timeframe. In addition, the RSI has re-entered a bearish crossover on the daily chart, reflecting weakening momentum, he said.

“Overall, the sentiment appears weak, with heavy call writing visible around the 24,200 strike. If the Nifty sustains below 24,200 on Monday, the index could witness further correction towards the 24,050–24,000 zone. On the other hand, a move back above 24,200 may trigger a near-term recovery rally towards 24,350–24,400,” De said.

Here are the 2 stocks to buy:

Buy Coforge at Rs 1,368 | Upside: 7% | Stop Loss: Rs 1,320 | Target: Rs 1,420-1,460

Coforge Limited has witnessed a strong rebound from lower levels and recently given a breakout above the crucial Rs 1,330–1,350 resistance zone, supported by strong volumes. The stock is trading above short-term EMAs, while RSI has moved above 65, indicating improving bullish momentum. The breakout also signals a possible trend reversal after a prolonged corrective phase. A buy at CMP (Rs 1,365–1,370) can be considered with a stop loss near Rs 1,320. On the upside, the stock may head towards Rs 1,420–1,460 in the near term. Sustaining above Rs 1,330 will be important for the continuation of the positive momentum.

(Virat Jagad, Sr. Technical Research Analyst, at Bonanza Portfolio)

Buy NBCC (India) at Rs 101 | Upside: 7% | Stop Loss: Rs 97-98 | Target: Rs 104-108

NBCC (India) Limited is showing signs of a strong recovery after a prolonged correction, with the stock reclaiming all major EMAs and giving a breakout above the Rs 98–100 resistance zone. Rising volumes and RSI near 70 indicate strengthening bullish momentum. The stock has formed a higher high–higher low structure, suggesting continuation of the uptrend. A buy at CMP (Rs 100–101) can be considered with a stop loss near Rs 97–98. On the upside, the stock may head towards Rs 104–108 in the short term. Sustaining above the breakout zone of Rs 98 will remain crucial for maintaining the positive bias.

(Virat Jagad, Sr. Technical Research Analyst, at Bonanza Portfolio)

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Chart Industries earnings up next as estimates slide

CLEVELAND — KeyBank customers across the United States encountered significant disruptions Saturday as the regional bank’s online banking platform and mobile app experienced a widespread outage, preventing many from accessing accounts, making transfers or completing routine transactions on a busy weekend. While core branch and ATM services remained operational, the digital banking failure frustrated thousands of users who reported login errors, frozen screens and failed fund transfers throughout the day.

Downdetector and other outage tracking sites showed a sharp spike in user reports beginning early Saturday morning, with the majority of complaints centered on the mobile app and online banking portal. As of Saturday evening, many services had partially recovered, but intermittent issues persisted for some customers, according to real-time monitoring data. KeyBank has not issued a detailed public explanation but confirmed it is actively working to restore full functionality.

A KeyBank spokesperson said in a statement: “We are aware of the technical issues impacting our digital banking services and apologize for any inconvenience. Our teams are working urgently to resolve the matter and restore normal access as quickly as possible.” The bank encouraged customers to use branch locations, ATMs or the automated phone system for urgent needs during the disruption.

The outage comes at an inconvenient time for many customers, with Mother’s Day weekend shopping, bill payments and travel-related transactions peaking. Social media platforms filled with complaints, memes and expressions of frustration from users unable to check balances or send payments. Some reported being locked out entirely, while others could log in but faced delays or error messages when attempting transfers or deposits.

Scope of the Disruption

Reports indicate the problems primarily affected online banking and the mobile app, with users unable to view account balances, pay bills, transfer funds or deposit checks remotely. ATM and in-branch services continued without major interruptions, though some customers noted longer-than-usual wait times at branches as people sought alternatives to digital channels. International wire transfers and certain business banking features were also impacted for a period.

KeyBank serves millions of customers primarily in the Northeast and Midwest, with a strong presence in Ohio, New York, Pennsylvania and other states. The outage appeared nationwide rather than regionally concentrated, suggesting a central system or cloud-related issue rather than a localized problem.

This is not the first time KeyBank has faced digital banking challenges. Similar, though shorter, disruptions occurred earlier in 2026, prompting the bank to invest in infrastructure upgrades. Industry analysts suggest that rapid growth in digital banking usage, combined with increasing cybersecurity threats, has strained legacy systems at several regional banks.

Customer Impact and Frustration

Many customers took to social media to voice their dissatisfaction. “Been trying to pay my rent for two hours — KeyBank app is completely down,” one user posted. Others expressed concern about time-sensitive payments, including mortgages, utilities and payroll deposits. Small business owners reported particular difficulty managing cash flow during the outage.

KeyBank’s customer service lines experienced longer hold times as callers sought assistance. The bank activated additional support staff and encouraged use of its automated systems where possible. Some users reported success using the website via desktop browsers when the app remained unresponsive.

Financial experts advise customers facing urgent needs to visit a physical branch with proper identification or use alternative payment methods such as cash, checks or services from other institutions if available. Once systems are fully restored, users should review account activity carefully for any delayed transactions.

Possible Causes and Technical Context

While KeyBank has not confirmed the root cause, industry observers point to several common triggers for such outages: scheduled maintenance gone wrong, cloud service provider issues, cybersecurity incidents or unexpected spikes in traffic. The timing on a Saturday — typically a lower-volume day — suggests it may have been related to backend maintenance or a third-party service failure.

Regional banks like KeyBank often rely on a mix of in-house systems and external vendors for digital platforms, increasing vulnerability to cascading failures. The increasing sophistication of cyber threats has also forced banks to implement frequent updates and patches, sometimes leading to unintended disruptions.

The Consumer Financial Protection Bureau and state banking regulators monitor such incidents closely. While isolated outages are common in the industry, repeated or prolonged disruptions can trigger greater scrutiny and potential fines if customer harm is demonstrated.

KeyBank’s Response and Recovery Efforts

The bank has prioritized restoring mobile app functionality first, given its popularity among younger and on-the-go customers. Technical teams are conducting system-wide checks to prevent recurrence. Customers affected by delayed transactions or fees incurred due to the outage are encouraged to contact support for potential reimbursement once services normalize.

KeyBank has a history of transparent communication during technology issues and typically offers goodwill gestures such as waived fees for impacted customers. An official post-incident review is expected in the coming days.

Broader Implications for Digital Banking

This outage highlights the growing reliance on digital banking and the vulnerabilities that come with it. As more consumers shift away from branches, even brief disruptions can cause significant inconvenience. Banks across the country continue investing billions in cybersecurity, cloud infrastructure and redundant systems to minimize future risks.

For KeyBank specifically, the incident may accelerate plans for platform modernization. The bank has been expanding its digital offerings in recent years to compete with larger national players and fintech disruptors. Maintaining trust through reliable service remains critical in a competitive market.

Customers are advised to keep multiple access methods available — including desktop websites, mobile apps and phone banking — and to maintain up-to-date contact information with the bank. Setting up alerts for account activity can also help catch any delayed transactions quickly.

As services continue to recover Saturday evening, KeyBank urged patience and thanked customers for their understanding. Full restoration is expected within hours, though some residual delays in transaction processing may linger into Sunday.

The incident serves as a reminder of both the convenience and fragility of modern digital banking. While KeyBank works to resolve the current issues, customers and the broader industry will be watching closely to see how quickly and effectively the bank rebounds from this disruption.

Business

Sensex to hit 3 lakh by 2036? Raamdeo Agrawal says India is the ‘Ferrari’ among markets, here’s why

Speaking at Groww India Investor Festival 2026, the market veteran said that decades of compounding, rising financialisation and structural growth trends have built the strong foundation of the Indian market. “I have seen Sensex go from 100 to 80,000 in 40 years. For me to believe the journey will be any different over the next 40 years, there is no argument for that,” Agrawal said.

Markets in South Korea and Japan have recently seen sharp surges to record highs, while Dalal Street delivered comparatively muted returns. Many analysts highlighted that the strong earnings growth by several of these markets, thanks to the AI boom, is attracting FPI flows into those markets. Agrawal, however, reaffirmed that India’s long-term structural trajectory remains unmatched, while acknowledging that some regions are currently benefiting from an AI-led earnings cycle.

Drawing a comparison between India’s Sensex and South Korea’s KOSPI, both launched in January 1980, Agrawal pointed out that while the Korean benchmark index is at around 5,000 points today, the Sensex has climbed past 80,000. “Form may be temporary, but class is permanent. India is the way to go,” he said at the event.

The market expert highlighted that India’s market capitalisation has compounded at nearly 14% annually in dollar terms over the last two decades, compared with around 7% for the US market. “Every five to six years, you double. That is the pace,” he added.

Why India creates more multibaggers

The MOFSL Chairman said his investing philosophy has always focused on finding businesses operating in fast-growing industries within fast-growing economies. Referring to an internal study inspired by Thomas Phelps’ book ‘100 to 1 in the Stock Market’, Agrawal noted that nearly 20% of companies in the NSE 500 delivered over 25% annualised returns for a decade — effectively becoming 10-baggers. The comparable figure in the S&P 500, he said, stood at just around 7%.

“Multi-bagging happens where growth is fastest. You get the maximum multi-baggers in the country which is growing fastest and in the industry which is growing fastest,” he said. Vision, courage and patience are the three things that act as the formula for identifying outsized winners, according to the market veteran. “Whenever you are hitting a big one, you are mostly alone. You need conviction to stay with it,” he added.

Investors often underestimate how compounding works over long periods, Agrawal said, adding that in a stock that delivers 100x returns over two decades, a disproportionate amount of wealth creation typically happens in the final few years. “You sit through 19 years because most of the compounding comes in the 19th and 20th year,” he said.

The Bharti Airtel bet that shaped his investing career

Raamdeo Agrawal reminisced about his early investment in Bharti Airtel. In 2003, after studying the economics of network businesses and speaking with Sunil Bharti Mittal, the market expert became convinced that India’s mobile revolution would create enormous value.

At the time, India had only around 50 million fixed-line phones for a population of more than one billion. Agrawal estimated Bharti Airtel could generate Rs 27,000–28,000 crore in profits over the following five years, even though its market capitalisation was only around Rs 5,000 crore.

He bought Bharti Airtel’s shares at around Rs 19–30 apiece, despite scepticism from peers and friends. “I was alone all the way through,” he recalled. While he sold some shares early under pressure, he held on to a significant portion as the stock multiplied several times over. His final exit came years later at around Rs 650, translating into roughly a 25-fold return.

The next generation of winners

Agrawal pointed out that India’s expanding capital markets ecosystem can create the next wave of multi-baggers. “We are adding nearly 3 million new customers every month…We already have more than 220 million demat accounts. By 2031–32, we could reach 500–600 million,” he said.

Rising retail participation will create opportunities across brokers, exchanges, asset managers, wealth platforms and depositories, he said, admitting to missing out on the sharp rally in BSE despite understanding the sector deeply.

“The stock went up almost 50 times, and I did not make a single paisa,” he said with a laugh.

Today’s quick commerce momentum is similar to Bharti Airtel in 2003

Agrawal drew parallels between India’s quick commerce industry and the early days of telecom. He said the firms operating in the segment are still in the heavy cash-burn phase, but the underlying network effects could eventually create very large businesses.

“This is a Bharti moment,” he said, referring to the potential scale of India’s quick commerce opportunity. He cited comments from global retail executives, including leadership at Walmart, describing India’s quick commerce ecosystem as a glimpse into the future of retail.

What Raamdeo Agrawal avoids completely

Despite his appetite for growth, Agrawal said that he maintains strict filters while evaluating businesses. He avoids companies generating return on equity below 20% and pays close attention to receivables cycles as an indicator of business quality.

“If return on equity is 9 or 10%, I do not even want to enter the meeting,” he said, adding that management quality remains his biggest filter. “They will go to hell and take you along,” he said, referring to promoters with compromised governance standards.

Agrawal also stressed the importance of visiting factories and observing operations first-hand instead of relying solely on management presentations.

Sensex at 3 lakh by 2036?

Agrawal remained bullish on India’s long-term macroeconomic trajectory, projecting that per capita income could double over the next six to seven years. The market veteran expects Sensex to touch 1.5 lakh by 2030 and potentially 3 lakh by 2036, driven by sustained earnings growth and rising participation in financial assets. “Three lakh in 12 years is more guaranteed than one-and-a-half lakh in six years,” he said. “That is how compounding works,” he said at the event.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Business

Bonus issues, stock splits & dividends: SBI among 18 stocks turning ex-date this week. Do you own any?

Kothari Petrochemicals – Dividend

Kothari Petrochemicals has set May 11 (Monday) as the record date to determine shareholder eligibility for its interim dividend of Rs 1 per share (10%) with a face value of Rs 10 each. The dividend will be paid on or before June 3.

Manappuram Finance – Dividend

Manappuram Finance has set May 11 (Monday) as the record date to determine shareholder eligibility for its interim dividend of Rs 0.50 per share (25%) with a face value of Rs 2 each.

PAE – Dividend

PAE, whose core activity includes marketing and distributing automotive components, has set May 11 (Monday) as the record date to determine shareholder eligibility for its interim dividend of Rs 0.20 per share with a face value of Rs 10 each. Notably, the stock will also turn ex-record date for its 6:1 bonus issue on May 25.

Aptus Pharma – Bonus issue

Aptus Pharma has set May 12 (Tuesday) as the record date for its 3:2 bonus issue. This means that the shareholders who own the shares of the company as on the record date will get 3 bonus shares for every two shares held.

Godrej Consumer Products – Dividend

FMCG-major Godrej Consumer Products has fixed May 12 (Tuesday) as the record date to determine the eligibility of shareholders to receive its interim dividend of Rs 5 per share (500%) with a face value of Rs 1 each. The dividend will be paid on or before June 4.

NRB Bearings – Dividend

Needle roller bearing manufacturer NRB Bearings has fixed May 13 (Wednesday) as the record date to determine the eligibility of shareholders to receive its interim dividend of Rs 2.25 per share (112.5%) with a face value of Rs 1 each.

Brookfield India Real Estate Trust REIT – Dividend

Brookfield India Real Estate Trust REIT has fixed May 14 (Thursday) as the record date to determine the eligibility of shareholders set to receive its prospective dividend, which will be considered and approved by its board of directors during its meeting on Monday.

Oberoi Realty – Dividend

Oberoi Realty has fixed May 14 (Thursday) as the record date to determine the eligibility of shareholders to receive its fourth interim dividend of Rs 2 per share (20%) with a face value of Rs 10 each. The dividend will be paid on or before May 22.

Anand Rathi Wealth – Dividend

Anand Rathi Wealth has fixed May 15 (Friday) as the record date to determine the eligibility of shareholders to receive its interim dividend of Rs 7 per share.

Aptus Value Housing Finance India – Dividend

Aptus Value Housing Finance India has fixed May 15 (Friday) as the record date to determine the eligibility of shareholders to receive its second interim dividend of Rs 2.50 per share (125%) with a face value of Rs 2 each.

Biogen Pharmachem Industries – Bonus issue

Biogen Pharmachem Industries has fixed May 15 (Friday) as the record date to determine the eligibility of shareholders for its 1:6 bonus issue. The company had announced in April that it will issue “1 new equity shares of Rs.1 each for every 6 existing equity shares of Rs.1 each fully paid up”.

Dev Labtech Venture – Bonus issue, stock split

Dev Labtech Venture has set May 15 (Friday) as the record date for 1:1 bonus issue and 1:2 stock split. As part of the bonus issue, eligible shareholders will get one bonus share for every share held in the company as on the record date. As part of the stock split, each share of the company will be split into two shares.

Gopal Snacks – Dividend

Gopal Snacks has fixed May 16 (Saturday) as the record date to determine the eligibility of shareholders to receive its prospective third interim dividend which may be considered and approved by its board of directors during its meeting scheduled on Tuesday. As the record day falls on a weekend when markets are closed, May 15 will be the effective record date.

HBG Hotels – Dividend

HBG Hotels has fixed May 15 (Friday) as the record date to determine the eligibility of shareholders to receive its interim dividend of Rs 0.15 per share (1.5%).

IEX – Dividend

Indian Energy Exchange (IEX) has fixed May 15 (Friday) as the record date to determine the eligibility of shareholders to receive its final dividend of Rs 2 per share with a face value of Rs 1 each.

Kennametal India

Kennametal India has fixed May 15 (Friday) as the record date to determine the eligibility of shareholders to receive its interim dividend of Rs 40 per share (400%).

Nexus Select Trust

Nexus Select Trust has fixed May 15 (Friday) as the record date to determine the eligibility of shareholders to receive its prospective dividend that its board may consider and approve during its upcoming meeting this week.

State Bank of India

State Bank of India (SBI) declared a dividend of Rs 17.35 per equity share for the financial year ended March 31, 2026. The bank has fixed May 16 (Saturday) as the record date for determining the eligibility of shareholders entitled to receive the dividend. As the record date falls on a weekend when markets are closed, May 15 will be the effective record date. The dividend payment is scheduled to be made on June 4, 2026, the bank said in a regulatory filing on Friday.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

When wildlife TV personality Forrest Galante sat down for his monthly call with YouTube consultant Paddy Galloway, he received some bad news.

No more turtles.

Galante has 2.5 million YouTube subscribers. He’s been producing wildlife programming for more than a decade, including a docuseries on Animal Planet and a show on the History Channel. He owns his own production company. Generally speaking, Galante’s got a good feel for what his audience wants.

But it was Galloway, something of a guru in the still-burgeoning YouTube creator economy, who identified that whenever Galante showed turtles in his videos, viewer engagement dropped. It was consistent and significant.

“Maybe it’s just turtles are more commonplace and they’re kind of slow and they don’t really do much,” Galloway said in an interview. “We noticed three or four videos in a row, when Forrest was showing turtles, the viewers were just kind of disengaged, and they were leaving.”

This is the kind of insight that many of the most popular YouTube creators, including Jimmy Donaldson, known to the world as MrBeast, and sports creator Jesse Riedel, also known as Jesser, have paid Galloway to provide.

As YouTube creatorship cracks open millions, or potentially even billions, of dollars for the most-watched personalities, Galloway has made a name for himself as one of the best of a growing class of YouTube consultants — a bona fide YouTube whisperer.

“I think he’s an absolute genius,” said Galante.

“Super smart guy,” Riedel told CNBC.

“I don’t want to say Paddy has changed my life completely,” said Humphrey Yang, a former financial advisor whose YouTube channel has more than 2 million subscribers. “But he’s definitely helped a lot.”

YouTube’s media dominance

YouTube will showcase many of its top creators on Wednesday in New York City’s Lincoln Center for its annual upfront advertising presentation, which it calls Brandcast. Like YouTube’s influence in modern media, the event has grown in size and prestige every year as YouTube’s viewership share rises.

YouTube makes up 12.7% of all streaming in the U.S., according to Nielsen’s most recent “The Gauge” report. Netflix is second with 8.4%, followed by Disney with 5%.

Sixty-seven million people consider themselves online content creators, according to a 2025 Goldman Sachs report. That number could rise to more than 100 million by 2030, Goldman estimates.

About 10,000 U.S. YouTube channels have more than 1 million subscribers, according to a YouTube spokesperson. For many of these creators, YouTube can be a lucrative full-time job. But to make a business out of the largely free platform, videos need to get consistent clicks — preferably in the millions.

With YouTube’s recommendation algorithm constantly evolving, many creators have been turning to strategists to maintain success on the platform.

“From zero [subscribers] to 1 million, you don’t need it, but from 1 million to 10 million, or 1 million to 100 million, you definitely need a strategist,” Aniket Mishra, a YouTube growth strategist, told CNBC.

In recent years, videos best watched on TV, rather than on mobile devices, have surged in popularity as YouTube has taken over more and more connected-TV viewing, rivaling subscription streaming services such as Netflix and Disney+.

Creators say the Alphabet-owned platform has responded by favoring longer videos, often exceeding 30 minutes. That shift means higher production value and bigger investment from creators. It also means the potential to earn more money.

Since 2021, YouTube has paid out over $100 billion to creators, and an increasing share of that money is flowing to those producing content for bigger screens, YouTube said. The number of channels earning more than $100,000 from TV screens jumped 45% year over year, the company reported.

Regardless, success on the platform remains a simple task of getting viewers through the door, and these strategists maintain that they are the best equipped to optimize a creator’s videos.

“The reason people pay us top dollar is because we have been doing it for the longest, and we have the best success rate,” Galloway said. “Our average increase in views after a year — so, year-on-year after working with us — is 350%.”

The YouTube whisperer

Galloway’s interest in YouTube consulting began out of self-interest. He started posting YouTube videos of his own in 2006, just a year after the service first began, and wanted to figure out why certain videos went viral so his own could gain popularity, he told CNBC.

Within a few years, Galloway’s search for the ingredients of virality became the subject of his videos. He began creating self-dubbed “YouTube Masterclass” videos such as “How Peter McKinnon gained 1 million subscribers in under 1 year” and “Here’s How Mr Beast BLEW UP – How He Grew His YouTube Channel.”

YouTube personality Jimmy Donaldson, better known as MrBeast, arrives for the 36th Annual Nickelodeon Kids’ Choice Awards at the Microsoft Theater in Los Angeles on March 4, 2023.

Michael Tran | Afp | Getty Images

Galloway grew his channel to about 500,000 subscribers, and the videos got Donaldson’s attention. Galloway began working directly for Donaldson, providing him with strategy ideas. Donaldson is now the undisputed king of YouTube with 483 million subscribers.

Galloway worked with Riedel from 2021 through January of this year, encouraging him to change his focus from daily vlogs to bigger concept ideas that pulled in more viewers.

“He was like, ‘You need to make videos that anybody can enjoy,’” Riedel said. “A lot of my videos were personal joke after personal joke. Right in the intro, if you watched it and you didn’t know me or my jokes, you’d be like, ‘What am I watching?’”

After years of plateauing at roughly 3 million subscribers, Riedel saw his subscriber number begin to soar. Today, Riedel is the largest sports-focused creator on YouTube with more than 41 million subscribers.

Content creator Jesser attends a game between the Brooklyn Nets and the Los Angeles Clippers at Intuit Dome in Los Angeles, Jan. 15, 2025.

Juan Ocampo | National Basketball Association | Getty Images

Galloway’s secrets often center around two simple concepts: headline and thumbnail image.

“We will deliberate a title — just one title — for like 30 minutes,” said Yang, who’s worked with Galloway since early 2022. “Changing a couple of the words in the title can have a huge impact on how the actual video does.”

Galloway has a staff of seven people who analyze what’s working on YouTube and how to create the best content target to perform well on the platform. He also owns three other companies, including one, Upright Media, that helps with the production and editing of videos.

Galloway’s largest clients have daily Slack communication with his team to discuss thumbnails and to run detailed diagnostics of video performance.

What’s the return on investment?

At his peak, Galloway said, he had a waitlist of 5,000 people and was only able to work with about 10 clients at a time.

His services aren’t cheap.

Paddy Galloway.

Courtesy: Paddy Galloway

Galloway typically charges flat fees for his work “starting in the $15,000 a month range” he said, though rates can go “considerably higher” depending on the project. That price gets clients full-time service — “in the weeds with you every day,” he said.

“It was like, ‘Oh my god, we’re paying this big amount of money for this unknown factor, will we ever get a return?” said Galante, of the turtle-light wildlife videos.

Strategist Mishra said he works primarily with business owners who have built YouTube channels around their products or services. He said he charges between $1,500 and $12,000 a month, depending on how much work he takes on, and said the creators who hire him have already figured out the basics on their own and hit a ceiling.

Mishra said his advice is often to study what is already working in a certain niche and replicate it.

American wildlife biologist Forrest Galante watches a wild crocodile caught in a motorcycle tire on the Palu River, Central Sulawesi, Indonesia, March 11, 2020.

Mohamad Hamzah | Nurphoto | Getty Images

“Copy with taste,” he said. “It’s very important that you have some kind of unique angle, but make sure the formatting of the videos, the pacing and everything else is similar to an outlier idea that is already proven in the niche.”

And while these strategists can’t promise guaranteed subscribers or views, they say their value lies in familiarity with what the platform rewards.

“What I do is I promise you knowledge, and hopefully with enough knowledge, growth comes next,” said Mario Joos, who spent nearly three years as retention director for MrBeast. “The algorithm will just reward what people want to watch.”

Though the highest level of advisory services can run into the thousands of dollars, an initial call with a YouTube coach can cost as little as $250, Joos said. He described the next level of service as “consultant” — someone who is providing advice but not actually helping a creator implement it. That’s Joos’ role today, he said.

The final rung is pure strategist — a role Joos had when he was working with MrBeast, he said, and the rung Galloway falls into.

“Now it’s not just like you’re telling the creator to execute on the knowledge. You are applying the knowledge,” said Joos. “You leave notes on videos. You go through the ideation process. And when there’s 100 ideas on the table, you look into them, you think about them, and you may even come up with the ideas. So that’s what a strategist does there. They have expertise.”

YouTube’s evolving trends

For YouTube’s most popular creators, the platform offers some consultant-like services for free, including thumbnail art guidance, guest ideas and suggestions for video introductions, according to Reed Fernandez, a strategic partner manager for YouTube’s top creators since 2021.

Fernandez is one of several hundred strategic partner managers for YouTube around the world who focus on the top 10% of YouTube creators. Fernandez’s specific team works with about 100 creators in the U.S., he said. Some of his clients include Brittany Broski, Dude Perfect and Alix Earle.

Brittany Broski at VidCon 2022 in Anaheim, California, June 23, 2022.

David Livingston | Getty Images Entertainment | Getty Images

Fernandez’s team typically approaches the creators it wants to help, based on perceived growth opportunity on the platform, Fernandez said. That makes the partnership beneficial for both YouTube and the individual creator, boosting overall engagement on the site.

“We’re looking for things like: Do we see them growing a lot year over year? We think they’re a big bet that we should try to put our full force behind to help them succeed on the platform,” said Fernandez.

Beyond consultant services, YouTube also connects some of these creators with speaking events and press junkets to extend reach and boost awareness.

Fernandez’s team can also offer insider tips on monetization, he said. He used the example of a creator whose videos were consistently just under the 8-minute threshold to qualify for mid-roll advertisements. Making their videos just 30 seconds longer, he told the creator, could make a significant difference in their earnings.

But even with YouTube’s internal support, many creators still turn to outside strategists to go deeper on the technical side.

When a viewer clicks on a YouTube video, watches it through, shares it or leaves a comment, YouTube registers that as a positive signal of interest. Videos that consistently generate those responses get surfaced more broadly and pushed onto the homepage, into recommendations and in front of new audiences.

Joos said his expertise sits specifically in retention, understanding not just whether a video performs, but exactly when viewers stop watching and why.

YouTube Studio, the backend dashboard that gives creators detailed statistics on their content, includes a retention chart that tracks audience drop-off. YouTube strategists use that data to inform everything from pacing decisions to keeping the viewer engaged until the end of the video.

Gabriel Leblanc-Picard, co-founder of Upload Strategy and the former head of ideation for MrBeast, said simplicity is the most reliable formula for success on the platform.

“Dim it down to like, if a 6-year-old could understand it,” he said. “People don’t want to watch something that is complicated, even the language that you use.”

During his time at MrBeast, Leblanc-Picard said he filtered through roughly 10,000 ideas, constantly looking for concepts that could expand the channel’s audience. One challenge he was given: Attract more female viewers to a channel whose fanbase he described as mostly “11-year-old boys.”

His answer was to develop a video about being stranded in the woods with an ex-girlfriend.

A video titled “Survive 30 Days Stranded With Your Ex, Win $250,000” was posted in March and has already surpassed 120 million views.

“At the end of the day, you’re making content for people,” Leblanc-Picard said. “The algorithm will reward what people want to watch.”

Data, Iran, US-China meeting in focus for scorching US stock market

Equity MFs delivered over 8% return last week. Check top 9

Kai Trump Celebrates College Plans With Lavish Bed Party

West Ham vs Arsenal LIVE: Premier League latest score and confirmed lineups | Football

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World2 days ago

Crypto World2 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

NewsBeat7 days ago

NewsBeat7 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Crypto World3 days ago

Crypto World3 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Marianne Dress

-

Tech6 days ago

Tech6 days agoImage AI models now drive app growth, beating chatbot upgrades

-

NewsBeat3 days ago

NewsBeat3 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Business1 day ago

Business1 day agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics1 day ago

Politics1 day agoPolitics Home Article | Starmer Enters The Danger Zone

-

Crypto World7 days ago

Crypto World7 days agoBlackRock Buys $284M In Bitcoin On May 1 As The Best Crypto To Invest In For 2026 Sits Below A Pending Binance Listing

-

Entertainment6 days ago

Entertainment6 days agoOlivia Wilde Reacts To Viral ‘Corpse’ Comparison

-

Sports7 days ago

Sports7 days agoIPL 2026: Gujarat Titans opt to bowl vs Punjab Kings; Nishant Sindhu handed debut | Cricket News

-

Sports6 days ago

Sports6 days agoInter Milan Win Serie A Title After Victory Over Parma

-

Sports7 days ago

Sports7 days agoKofi Kingston and Xavier Woods reportedly released by WWE along with others

-

Business7 days ago

Business7 days agoCan LeBron James Lead LA Past OKC Without Injured Luka Doncic?

-

Crypto World5 days ago

Crypto World5 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Entertainment7 days ago

Entertainment7 days agoOther Bennet Sister Love Triangle Cast: Ella Bruccoleri, Donal Finn

-

Sports6 days ago

Sports6 days agoEvery word of Arne Slot’s heated rant after Manchester United win vs Liverpool

-

Sports7 days ago

Sports7 days agoJoel Embiid urges Sixers fans not to sell playoff tickets to Knicks fans

-

Sports7 days ago

Sports7 days agoLa Liga: Vinicius Jr scores twice as Real Madrid win to keep Barcelona waiting for title

-

Entertainment7 days ago

Jennifer Lawrence’s Mary Jane Sneakers Are Spring’s It-Girl Shoe

You must be logged in to post a comment Login