Crypto World

GENIUS Act Expands FDIC Oversight of Stablecoin Issuers

The US Federal Deposit Insurance Corporation (FDIC) is advancing a regulatory framework for stablecoin issuers that operate under its supervision, in line with the GENIUS Act. The FDIC’s board voted to publish a proposal establishing minimum standards on reserves, redemption mechanics, capital requirements, risk management and custody for stablecoin issuers and the insured depository institutions (IDIs) that fall under its purview. Signed into law roughly nine months ago, GENIUS grants the FDIC authority to oversee stablecoin activity within the banks it supervises, with a broad aim of bringing more robust oversight to a fast-growing corner of the digital-asset ecosystem. The agency noted that the proposed rules would apply to reserve-backed payment stablecoins and are scheduled to take effect on January 18, 2027, unless earlier action is taken.

The FDIC underscored that, while the proposed rule would insure reserve deposits backing a payment stablecoin, it would not extend FDIC insurance to stablecoin holders themselves. In its view, treating holders as insured depositors would be inconsistent with GENIUS Act provisions, which limit deposit insurance coverage to traditional deposit accounts rather than tokenized payments. Nevertheless, the FDIC argued that by elevating the regulatory and supervisory standards around stablecoin reserves and governance, the rules would create a more secure environment for users who rely on stablecoins for smoother payments and liquidity needs.

Key takeaways

- The FDIC proposes standards on reserves, redemption, capital, risk management and custody for stablecoin issuers and supervised banks, aligning with the GENIUS Act framework.

- FDIC insurance would cover reserves backing payment stablecoins, but not the stablecoin holders themselves, reflecting GENIUS Act’s limits on deposit insurance for digital-asset tokens.

- The GENIUS Act authorized FDIC oversight of stablecoin activity within its supervision footprint; the regulatory timetable points to a January 18, 2027 effective date for many rules, with potential earlier actions.

- The FDIC’s initiative is part of a broader, multi-agency push to regulate stablecoins, with the OCC also moving to implement GENIUS Act provisions and potentially covering a broader range of activities.

- Public input is invited through a 60-day comment window on 144 questions, signaling an extensive consultation process as regulators shape the regime.

Regulatory architecture under GENIUS Act takes shape

The FDIC’s move represents a meaningful step in translating the GENIUS Act’s broad mandate into concrete, bank-centered standards for stablecoins. By focusing on reserve management and governance, the proposal aims to reduce liquidity and credit risk that could arise if stablecoin reserves are not held in a prudent and auditable manner. The agency’s emphasis on custody and risk management signals a priority on how reserves are held and safeguarded, a critical concern for both issuers and users who rely on the stability of these digital tokens in everyday payments and cross-border transfers.

The GENIUS Act, enacted last year, gave the FDIC new authority to supervise stablecoin activity within the banking system it already oversees. That framework is designed to ensure that as stablecoins grow in breadth and usage, the institutions backing them adhere to consistent, enforceable standards. In the FDIC’s view, this approach should provide greater assurance that payment-stablecoin networks operate with heightened governance and capital resilience, reducing potential shock transmission to the broader financial system.

What would be insured—and what would not

A central nuance in the FDIC proposal is the distinction between reserve insurance and holder protection. The agency confirmed that reserve deposits backing a payment stablecoin would fall under the FDIC’s insured deposits framework, at least for the portion of funds held in its supervised banks. However, this protection would not extend to the token holders themselves. The FDIC argued that treating stablecoin holders as insured depositors would run counter to GENIUS Act limitations on insurance coverage for payment-stablecoin users. In practice, this means that while the rails and buffers supporting a paid stablecoin could be shielded by insurance-like guarantees, the value risk borne by holders would remain separate from traditional deposit protections.

Despite the stance on holder protection, the FDIC stressed that the proposed rules would nonetheless enhance security and oversight for those using payment stablecoins by subjecting reserve management and custody to elevated standards. In its view, that combination should foster greater confidence among users and counterparties who rely on stablecoins for on-chain settlements, remittances and retail payments, especially during periods of market stress.

Feedback, timing and a wider regulatory arc

Public participation is a centerpiece of the FDIC’s approach. The agency invited the public to comment on 144 questions related to how it should regulate stablecoin issuers, with a 60-day window for responses. The consultation process follows a December 19 release detailing an earlier GENIUS Act implementation step that established an application procedure for insured depository institutions seeking approval to issue payment stablecoins through subsidiaries. The current proposal thus sits within a broader, staged effort to codify how financial institutions can participate in the stablecoin economy under federal supervision.

The FDIC’s activity is part of a coordinated federal push on digital-asset regulation. The Office of the Comptroller of the Currency (OCC) is also advancing GENIUS Act implementations, and the OCC’s track is described as broader in scope than the FDIC’s, covering national bank subsidiaries and certain nonbank issuers. The dual-track approach underscores how U.S. regulators are attempting to thread the needle between fostering innovation in digital payments and ensuring they do so within well-defined risk-management and consumer-protection boundaries.

Why this matters for markets, users and builders

For stablecoin issuers and banks alike, the FDIC’s proposal could redefine the cost and feasibility of issuing payment-stablecoins through FDIC-supervised institutions. A set of uniform reserve and custody standards can reduce fragmentation across different banking partners and issuer structures, providing a clearer pathway for compliance and oversight. This, in turn, may affect how quickly issuers can scale, how they structure reserve holdings, and how custodial arrangements are designed to meet heightened standards. While the insurance of reserves could boost confidence among users and counterparties, issuers may face additional capital and operational requirements that influence product design, liquidity management and the speed of settlement in volatile market conditions.

From a risk perspective, the emphasis on robust governance around reserves and redemption mechanics is aimed at mitigating a key class of failure modes that previously rattled stablecoin markets. If implemented as proposed, the rules could help prevent liquidity stress scenarios that arise when reserves are illiquid or poorly controlled, contributing to a more stable on-chain economy at a time when stablecoins have become a central component of on-chain commerce and liquidity provision.

Investors and builders will want to watch how the agencies harmonize their rules, how fast the 2027 effective date approaches, and how the public comment shapes final language. The interplay between the FDIC’s rules and the OCC’s broader GENIUS Act program will be particularly consequential, potentially creating a unified federal approach to stablecoins that could set global benchmarks for custodian standards, reserve transparency and prudential requirements for issuers.

Beyond the technical details, the broader takeaway is that the U.S. is moving toward a more formalized, bank-centric governance model for stablecoins. This shift could influence where stablecoin reserves are held, how issuers structure their corporate and regulatory relationships, and how users evaluate the safety and reliability of digital payment rails in the coming years.

Keep an eye on how the public comments frame the discussion. The 60-day input period will likely surface perspectives from banks, stablecoin issuers, consumer advocates and other stakeholders, shaping the final iteration of these rules and their ultimate impact on the evolving landscape of digital payments in the United States.

As regulators prepare to publish the final rules, market participants should assess potential stress-test scenarios, reserve-management practices and custody structures that could become industry benchmarks. The GENIUS Act’s intent is clear: bring higher standards and greater scrutiny to a sector that touches everyday commerce, while preserving the core benefits that stablecoins offer in terms of efficiency and interoperability across financial rails.

Readers should remain attentive to updates from both the FDIC and the OCC as they expand on their respective GENIUS Act plans, and to how issuers adapt their product designs in response to the evolving regulatory terrain.

The FDIC’s latest step marks a significant milestone in the ongoing effort to codify the security and reliability of stablecoins within the U.S. financial framework. The next few months will reveal how the 144 questions are addressed and how the final rules translate into real-world change for stablecoin participants across banking and digital-asset markets.

Closing perspective: As the regulatory scaffolding around stablecoins thickens, market participants should watch closely how the finalized rules balance innovation with safety, and how the two regulatory tracks converge to shape a more predictable, bank-backed landscape for digital payments.

- Toncoin whales have accumulated over 189,700 TON in three months.

- Heavy accumulation comes as TON activates the Catchain 2.0 upgrade.

- TON price rose to intraday highs of $1.32, could eye $1.89-$2.40 next.

Toncoin (TON), the cryptocurrency token of the Telegram-supported TON Blockchain, is trading higher on the day amid signs of renewed investor interest.

On Friday, the Toncoin price hovered at $1.30 as large holders, or “whales,” scooped up more tokens. The accumulation comes amid a tentative broader market recovery.

Toncoin price tests $1.30 zone amid whale accumulation

Toncoin’s price has climbed 4% in the past 24 hours, hovering near the critical $1.30 resistance zone.

The token reached an intraday high of $1.32 during the Asian trading session.

Buyers helped push trading volume up, with the metric spiking 104% as of writing to $160 million, marking a 45% increase from the previous day’s average.

This uptick arrives as Bitcoin holds above $71,000 amid bets on a new leg to $80,000.

Notably, TON’s momentum aligns with this backdrop, particularly as the network’s 100 largest whale addresses have collectively scooped up an additional 189,730 $TON over the past three months.

This accumulation persists despite broader market headwinds.

Analysts at Santiment highlighted what’s likely bullish in a post:

“Even with the #29-ranked coin in crypto losing two-thirds of its market cap since its local top in early August 2025, this heavy accumulation is a promising sign that a relief rally may come quickly once crypto markets finally turn the page from this bear cycle.”

Whale activity often points to fresh confidence in a project, and the aggressive buying shows interest in Toncoin’s underlying ecosystem.

The token is tied to the Telegram-integrated TON blockchain, which continues to expand through decentralized applications and mini-apps.

TON price is looking to bounce higher as the community cheers the Catchain, an upgrade designed to boost network throughput and block processing capacity.

In a post on X, Telegram CEO Pavel Durov commented on how bullish this upgrade is for Toncoin, noting that it marks the first step in a 7-stage Make TON Great Again (MTONGA) vision.

The TON blockchain just got upgraded and is now 10× faster.

Block rate increased 6×.

Transactions are now instant, subsecond.

This was step 1 of 7 to Make TON Great Again (MTONGA).

Next step: cut the already low transaction fees by 6×.

— Pavel Durov (@durov) April 9, 2026

What’s next for Toncoin price?

Such large-scale buying often precedes price reversals, as these investors position for potential rebounds.

Toncoin’s technical picture indicates that the price remains entrenched in a downtrend that began in June 2025, when it peaked above $8.20.

Persistent selling has resulted in a 84% decline in its value.

Bulls are not out of the woods yet, but a decisive break above $1.35 could ignite fresh upside momentum.

In this case, a potential target in a fresh rally would be the next resistance cluster around $1.89-$2.00. Significant supply pressure could follow at $2.40, an area of prior profit-taking deals.

Conversely, if sellers regain control, primary support levels beckon at $1.15.

A drop below $1.00 could accelerate selling toward $0.85, the multi-month low.

Key takeaways

-

Impersonation scams can be low-tech yet highly effective, using fake websites that closely mimic trusted cryptocurrency platforms to deceive users.

-

The CoinDCX case shows how a 7.16 million rupee fraud complaint escalated into legal action before it was identified as an impersonation case.

-

The fake domain coindcx.pro, not the real platform, was used to mislead the victim and carry out the fraud.

-

Scammers built a complete fake ecosystem using websites, Telegram channels and social media to create credibility.

While coverage of the cryptocurrency industry often focuses on market volatility, smart contract vulnerabilities and shifting government policies, some serious threats are remarkably low-tech. Deception often wears a familiar face. A fraudulent website that perfectly mirrors a legitimate exchange can cause both financial and reputational damage.

The CoinDCX impersonation incident is a stark case study of this pattern. What began as a 7.16 million rupee ($77,000) fraud complaint eventually escalated into police proceedings against the exchange’s leadership. However, the court’s intervention ultimately shifted the blame away from the actual platform, revealing that the culprit was a sophisticated digital facade operated by scammers.

A fake CoinDCX, but a real complaint

The case originated from a complaint filed by a 42-year-old insurance consultant based in Mumbra, a suburb in the Thane district within the Mumbai metropolitan region. The complainant alleged that he had been defrauded of about 7.16 million rupees. During the scam, he believed he was dealing with CoinDCX, which was presenting investment opportunities to him.

The offer allegedly included assurances of 10% to 12% monthly returns and references to a crypto franchise-style model linked to the platform. These elements, namely the promise of high returns and the apparent legitimacy of the brand, formed the core of the alleged fraud.

What sets this case apart is what happened next. Instead of being identified as an impersonation scam, the complaint escalated into legal action that led to the arrest of the company’s co-founders, Sumit Gupta and Neeraj Khandelwal.

The role of coindcx.pro in this case

Central to the incident was a counterfeit website, coindcx.pro, which the victim interacted with instead of the real CoinDCX website, coindcx.com.

Such fake domains are a common method in impersonation scams. They appear visually similar, seem trustworthy and deliberately exploit the brand’s established credibility.

According to statements issued by CoinDCX, no money connected to this matter was processed through its exchange systems. The scam did not originate within the platform itself. Instead, external actors allegedly used its name and reputation as bait.

Did you know? Domain impersonation scams often use subtle tricks, such as replacing letters, for example “o” with “0,” or adding extra words, to make fake websites nearly indistinguishable from real ones at a glance.

How the fraudsters built a fake ecosystem

The impersonation reportedly extended well beyond a single domain. The scammers also built supporting infrastructure, such as Telegram channels and social media accounts, to reinforce the illusion of legitimacy. This reflects a broader trend in crypto scams today, where perpetrators no longer rely on a single deceptive element but instead build an entire parallel ecosystem.

For the victim, this setup created a seamless and consistent experience: a website, an associated community and representatives, all seemingly connected to a recognized brand.

How the case escalated

The complaint was filed at the Mumbra police station in Thane on March 16, 2026. As the investigation progressed, CoinDCX’s co-founders were taken into custody in Bengaluru.

This turn of events highlights a key complexity in impersonation cases. When victims mention a prominent company in a complaint, it can take time to distinguish genuine involvement from misuse of the brand name. In fast-moving investigations, this lack of clarity can sometimes lead to action against legitimate companies before all the facts are established.

The case reached a critical stage when it came before a Thane magistrate court. The court granted bail to CoinDCX’s co-founders and noted that no prima facie case had been established against them. It observed that the complainant had been deceived by individuals impersonating the company’s promoters, not by the company itself. The victim also admitted having had no interaction with the company’s co-founders.

Did you know? Cybercriminals often buy expired or similar-looking domains in bulk, enabling them to launch multiple fake versions of a popular crypto platform within hours once a scam template proves effective.

A wider pattern of fake domains

The CoinDCX case is not an isolated incident.

According to the company, it reported more than 1,200 fake websites impersonating its platform between April 2024 and January 2026. This suggests that, for fraudsters, impersonation is not a sporadic tactic but a scalable strategy.

CoinDCX also stated that the first information report (FIR) filed against its co-founders was false.

Creating a domain that closely mimics a well-known platform is relatively inexpensive. When combined with messaging apps and social media, it allows fraud networks to recreate an appearance of trust at scale.

Why high monthly returns remain a key trigger

A central feature of the alleged scam was the promise of 10% to 12% monthly returns.

Such claims are a common element in financial fraud. In the cryptocurrency space, they are often paired with urgency, exclusivity or an association with a recognized platform.

From a behavioral perspective, these promises serve two key roles:

In many cases, the perceived legitimacy of the brand helps overcome doubts that might otherwise arise from the unusually high returns.

Did you know? Many impersonation scams reuse the same scripts and layouts across different brands, allowing a fake site built for one exchange to be repurposed for another within days.

Legal and reputational fallout of the CoinDCX incident

Although the court found no case against CoinDCX’s co-founders, the incident highlights the wider consequences of impersonation scams.

For companies and their executives, such events can result in:

For users of any exchange, seeing it associated with negative news can be unsettling. Those who have invested through the platform may fear financial loss. Even when a recovery process exists, few would want to become involved in a difficult and often lengthy procedure.

The case also raises important questions about how law enforcement handles digital impersonation, where identities can be replicated far more quickly than they can be verified.

CoinDCX’s response

In the aftermath of the incident, CoinDCX announced a 100 crore rupee ($10.76 million) initiative called the Digital Suraksha Network (DSN), focused on fraud prevention and user awareness.

The reported measures include:

-

An AI-driven WhatsApp helpline

-

APIs for sharing fraud-related data

-

Collaboration with law enforcement for training and improved response

While these steps cannot completely eliminate the risk of impersonation, they reflect a move toward more proactive defense and stronger coordination across the ecosystem.

What users should take away

The CoinDCX impersonation case offers several practical lessons:

-

Verify domains carefully. Even minor variations can indicate a fraudulent site.

-

Be cautious of promises of fixed or unusually high monthly returns.

-

Treat Telegram groups and social media handles as unverified unless they are officially confirmed.

-

Ensure that all transactions are conducted only through official platforms.

In many cases, the difference between a legitimate service and a scam is not advanced technology but careful verification.

Crypto World

ServiceNow (NOW) Stock Plunges Nearly 8% Amid Geopolitical Chaos and AI Disruption Concerns

Key Takeaways

- ServiceNow (NOW) shares plummeted approximately 7.86% on Friday, April 10, 2026, settling near $89.81.

- Renewed Middle East conflict following a ceasefire breakdown sparked widespread market anxiety and contributed to the decline.

- Anthropic unveiled Managed Agents, fully autonomous AI tools capable of handling complex workflows, sparking concerns over traditional SaaS model obsolescence.

- Famed short seller Michael Burry briefly posted (then removed) commentary suggesting Anthropic poses a competitive threat to Palantir, amplifying SaaS sector concerns.

- Year-to-date, NOW has declined 38.3% and currently trades 56% beneath its 52-week peak of approximately $211.

ServiceNow (NOW) faced a brutal trading session Friday, with shares collapsing nearly 8% to close around $89.81 as twin headwinds slammed the enterprise software provider in an already shaky market environment.

SaaS investors endured a particularly punishing day across the board.

The initial pressure originated from geopolitical developments. News emerged of a ceasefire violation in the Middle East, sparking renewed investor anxiety and triggering broad risk-off sentiment. This stood in stark contrast to the situation just ten days prior, when NOW had rallied 6.2% following President Trump’s comments about constructive diplomatic engagement with Iran. Friday’s session wiped away most of those gains.

The second blow struck more directly at ServiceNow’s core business model. Anthropic rolled out Managed Agents, a new class of autonomous artificial intelligence systems designed to execute sophisticated, multi-stage workflows independently. Market participants viewed this development as potentially disruptive to conventional SaaS platforms that rely on human operators to manage business processes.

Burry’s Brief Commentary Intensifies Selling Pressure

Michael Burry, the prominent investor famous for prescient contrarian positions, briefly published and subsequently removed a social media statement asserting that Anthropic was “eating Palantir’s lunch.” Though fleeting, the remark highlighted growing investor concerns about established SaaS companies’ exposure to emerging AI-native competitors and added momentum to Friday’s downturn.

While Burry’s quickly-deleted commentary offered no new hard data about ServiceNow’s operations, it resonated in an already nervous trading environment.

NOW shares have now surrendered 38.3% of their value year-to-date. Trading at $89.81, the stock languishes more than 56% below its 52-week high of $211.48 achieved in mid-2025. An investor who purchased $1,000 of NOW stock five years ago would currently hold approximately $858 in value.

The stock has experienced 11 single-day moves exceeding 5% over the past twelve months, indicating Friday’s sharp decline, while severe, fits within recent volatility patterns.

Fundamental Performance Remains Robust

Despite the stock’s punishing performance this year, ServiceNow’s core business metrics continue showing strength. The company reported full-year 2025 revenue of $13.3 billion, representing 21% growth versus the prior year. Subscription revenue, which provides stable recurring cash flows, contributed $12.9 billion to that figure.

ServiceNow closed 2025 with $28.2 billion in remaining performance obligations—a forward-looking indicator of committed future revenue—reflecting 27% year-over-year expansion.

The company has also taken proactive steps to counter the AI competitive threat. ServiceNow has established partnerships with both Anthropic and OpenAI, and earlier this year completed the acquisition of Moveworks, an AI agent technology provider serving major enterprises including Toyota and Unilever. That acquisition’s technology has been integrated into Autonomous Workforce, a product introduced in February that ServiceNow claims can autonomously handle 90% of routine IT support requests.

Shares last changed hands at $89.81, having touched a session low of $88.66.

Update April 10, 2026, 10 am UTC: This article has been updated to add more details from the announcement.

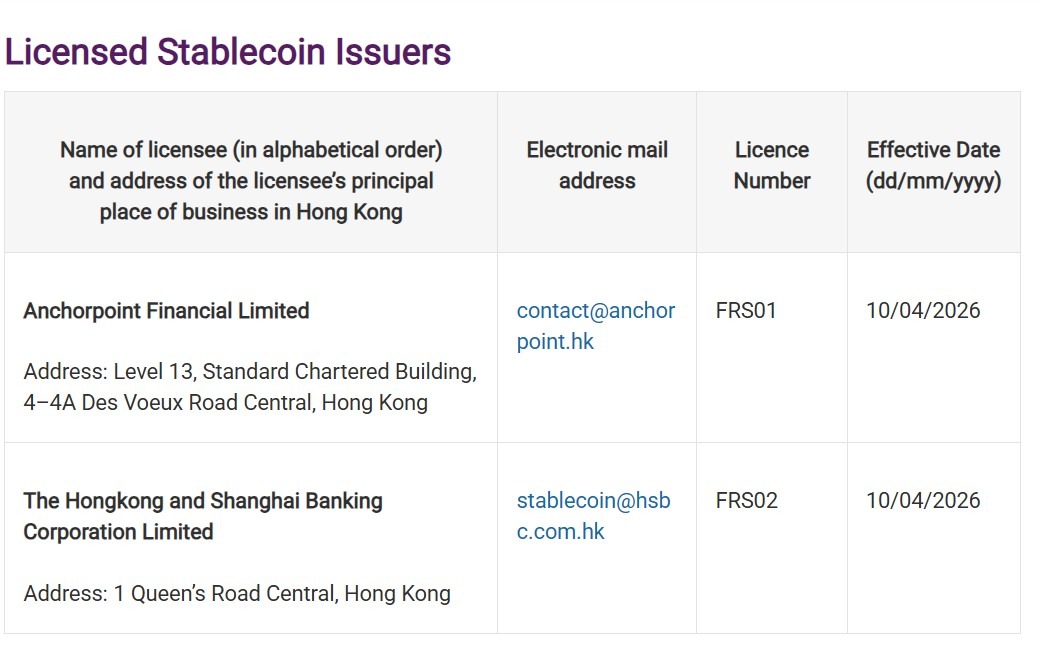

Hong Kong has issued its first stablecoin issuer licenses, approving Anchorpoint Financial and the Hongkong and Shanghai Banking Corporation under a new regulatory framework overseen by the Hong Kong Monetary Authority (HKMA).

The HKMA announced the initial batch of licensees on Friday, marking the first approvals under its stablecoin regime.

Anchorpoint Financial is the stablecoin joint venture formed by Standard Chartered Bank (Hong Kong), Animoca Brands and Hong Kong Telecommunications. The Hongkong and Shanghai Banking Corporation Limited is HSBC’s Hong Kong-based banking entity and one of the city’s three note-issuing banks.

The first approvals highlight Hong Kong’s cautious approach, with regulators appearing to favor bank-linked and institution-backed issuers in the regime’s opening phase.

The announcement comes after weeks of unconfirmed reports about potential licensees and a missed March timeline, marking a cautious start to Hong Kong’s stablecoin licensing rollout. HKMA Chief Executive Eddie Yue said in February that a very small number of issuers would be licensed in March, a timetable the HKMA ultimately missed before granting the first approvals.

Hong Kong’s stablecoin regime took effect on Aug. 1, 2025, and requires issuers of fiat-referenced stablecoins to obtain an HKMA licence and meet rules covering reserve backing, redemption, governance and Anti-Money Laundering controls.

Hong Kong rolls out stablecoin regime after delays

The stablecoin regime also gives the HKMA power to investigate violations and take enforcement action, including fines, suspensions and license revocations.

Yue said the new regime gives stablecoin issuers a regulated framework to operate in Hong Kong while requiring safeguards around user protection and risk management.

The licensed issuers are expected to launch their operations in the coming months, according to the HKMA.

Related: Hong Kong, Shanghai authorities to test blockchain for cargo trade data

On April 1, the HKMA said it was actively advancing the licensing process after missing its earlier March timeline.

Earlier media reports also pointed to possible frontrunners. On March 13, HSBC and a Standard Chartered-backed venture were tipped as likely recipients, but the regulator had not confirmed any names at the time.

Cointelegraph reached out to the HKMA for more information, but had not received a response by publication.

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

BEIJING — China’s ties with countries such as Iran and Russia have raised expectations of a bigger diplomatic role, but Beijing remains focused on protecting its own domestic interests, including global exports.

That stance underpins Beijing’s circumspect acknowledgment of reports that it pushed Iran toward this week’s temporary ceasefire. A New York Times report cited three Iranian officials as saying China played a role, while AFP cited U.S. President Donald Trump.

China has made “active efforts” to end the conflict, Foreign Ministry Spokesperson Mao Ning said Wednesday, when asked by the press about the reports. She emphasized that Foreign Minister Wang Yi had made 26 phone calls to representatives of countries including Russia, Saudi Arabia, Germany and Iran since the U.S.-Israel strikes on Iran began on Feb. 28.

But Beijing stopped short of confirming direct mediation.

China called for an “immediate stop” to military operations after U.S.-Israel strikes against Iran in late February. When asked on March 3 about Iran’s counterattacks, China’s Foreign Ministry did not mention Tehran specifically, urging instead for “all parties” to prevent the conflict from spreading.

“What Beijing did is not really about direct intermediation,” said Zongyuan Zoe Liu, a senior fellow for China studies at the Council on Foreign Relations.

“What Beijing did is, more precisely, broker[ed], facilitated the ceasefire,” she said Friday on CNBC’s “The China Connection. “From that perspective there’s nothing [that has] changed with regards to Beijing’s foreign policy. It does not mean Beijing is becoming more active.”

Instead, she noted Beijing is concerned about the risk of a global downturn from the war that would hurt its export-oriented economy.

Net exports contributed to about one-third of China’s GDP last year, despite heightened U.S. tariffs, leaving its economy exposed to disruptions in global trade.

IMF Managing Director Kristalina Georgieva warned Thursday that global growth would slow even if the ceasefire holds, citing lingering uncertainty around the Strait of Hormuz.

The strait handles about one-fifth of global oil supply, connecting the Persian Gulf on the coast of Saudi Arabia with the rest of the world. While China is the primary buyer of Iranian oil and relies on the waterway for just under half of its seaborne oil imports, that represents just 6.6% of China’s total energy consumption.

Still, China faces “immense pressure due to rapidly rising energy costs, and hopes the Strait of Hormuz will be reopened soon,” said Hai Zhao, a director of international political studies at the Chinese Academy of Social Sciences, a state-affiliated think tank.

As of January, Beijing held enough crude stockpiles to meet demand for three to four months, according to estimates. Data show that Iran has been sending oil through the strait to China since the war began.

However, gasoline prices in China jumped 11% in March from the prior month, and authorities have raised the official domestic gasoline prices twice in six weeks, by a total of 1,580 yuan per metric ton, or about 60 cents per U.S. gallon. The average price in the U.S. has gone up by more than $1 per gallon during that time.

Higher energy costs are also squeezing factory margins, adding to price pressures across China’s manufacturing sector.

Globally traded Brent crude futures remained below $100 a barrel on Friday, despite limited signs of a recovery in shipping through the Strait of Hormuz. Recent Iran attacks on a crucial Saudi pipeline have also slashed the kingdom’s oil output, Saudi Arabia’s state news agency said Thursday.

The backdrop

China’s diplomatic positioning builds on its role in restoring diplomatic ties between Iran and Saudi Arabia three years ago, ending three decades of animosity. The move was notable given U.S. interests in the Middle East, while elevating China’s profile in the region.

That history means Beijing can play the role of mediator once both sides are willing to reduce conflict, Zhao said.

But he noted that China lacks the capability or inclination to pressure either side into negotiating. Instead, China’s support gives Pakistan’s mediation efforts more heft, he said.

Pakistan, which shares borders with China and Iran, is set to host Iranian and U.S. leaders in Islamabad this weekend for ceasefire talks. The extent of Beijing’s involvement with the summit remains unclear.

Subscribe now

“We support the mediation efforts by countries including Pakistan,” Chinese Foreign Ministry Spokesperson Mao said this week. She noted Beijing has called on all parties to end hostilities as soon as possible, for regional peace. “China has made active effort to this end.”

In late March, China and Pakistan published a plan for “restoring peace and stability” in the Middle East, including a ceasefire, peace talks and the restoration of normal passage of ships through the Strait of Hormuz.

Pakistan abstained from voting on a UN Security Council resolution this week that would have encouraged countries to coordinate their defensive efforts in order to reopen the strait. Veto-wielding Security Council members China and Russia objected and planned to issue an alternative resolution.

Iran has made clear that ships must obtain its permission to pass through the strait, Sultan Ahmed Al Jaber, CEO of Abu Dhabi National Oil Co., said Thursday in a social media post. “The Strait of Hormuz is not open. Access is being restricted, conditioned and controlled.”

Before the war, Iran had occasionally harassed, attacked or seized vessels transiting the strait as tensions with the U.S. escalated.

“China welcomes any chance to present itself as a constructive, responsible power while the Trump administration is seen as the source of the instability,” CFR’s Liu said.

But she warned that the broader geopolitical dynamics remain unchanged.

“The underlying structural tension between Beijing’s dependence on a rules-based global order and Washington’s growing willingness to disrupt that order remains entirely unresolved,” she said.

“That is the story worth tracking beyond the immediate ceasefire.”

— CNBC’s Asriel Chua contributed to this report.

Japan’s cabinet has approved a draft amendment that would classify cryptocurrencies as financial products, marking a shift in how the country regulates the sector.

The proposal brings crypto assets under the Financial Instruments and Exchange Act, a framework used for stocks and other securities, Nikkei reported. If passed during the current parliament session, the law could take effect as early as fiscal 2027.

Until now, Japan has treated crypto mainly as a payment tool under the Payment Services Act. That approach focused on custody, anti-money laundering checks and exchange registration. The new rules would ban insider trading and require issuers to publish annual disclosures.

Penalties would also rise. Operating without registration could bring up to 10 years in prison, up from three, and fines could increase to 10 million yen ($62,800). The Securities and Exchange Surveillance Commission would gain broader authority to police the market.

In a press conference, Minister for Financial Services Satsuki Katayama said the move will “expand the supply of growth capital in response to changes in the financial and capital markets, ensuring market fairness, transparency, and the protection of investors.”

Bitcoin treasury firm Nakamoto (NAKA) is resorting to a familiar Wall Street playbook as it looks to lift its beating-down share price and stay on Nasdaq.

The company is seeking approval for a “reverse stock split” that would combine shares at a ratio to be set between 1-for-20 and 1-for-50, according to a preliminary proxy filing (Schedule 14A), as it has seen a collapse in its share price to around $0.22. Prices are down roughly 99% from its May 2025 peak.

A reverse stock split reduces the number of shares outstanding while increasing the share price proportionally, for example turning 20 shares at $0.20 into one share at $4. While it does not change the company’s underlying value, it is commonly used to regain compliance with Nasdaq’s $1 minimum bid requirement and avoid delisting. Nasdaq mandates listed companies to maintain a minimum bid price of $1 per share, and firms that fail to ensure that within a specific period risk being delisted.

Nakamoto recently sold about 5% of its bitcoin holdings, leaving it with 5,058 BTC, pointing to ongoing liquidity management.

Other bitcoin treasury firms have taken similar steps, including Strive Asset Management earlier this year. Most DAT shares have taken a beating in recent months, tracking the collapse in BTC’s spot price to roughly $70,000 from over $126,000 in October.

Alongside the reverse split, the company, in a Form S-3 filing, registered more than 400 million shares for potential resale by existing investors. This does not raise new capital, but creates a large overhang that could weigh on the stock.

The company also has a shelf registration allowing up to roughly $7 billion in future securities issuance. This is separate from an at the market (ATM) program of up to approximately $5 billion, which would allow it to sell newly issued shares directly into the market over time.

Flare published a governance proposal on Thursday that would make it one of the first layer-1 blockchains to capture maximal extractable value (MEV) at the protocol level rather than letting it flow to the small number of specialized actors who profit from transaction ordering across virtually every major chain.

MEV is the revenue that block builders extract by reordering, inserting or censoring transactions within a block. On most blockchains, this value flows to external searchers and builders who effectively impose a hidden tax on ordinary users through front-running, sandwich attacks and arbitrage.

External estimates put annual MEV revenues at tens of millions on networks like Arbitrum, upwards of $500 million on Ethereum, and as much as $1 billion on Solana. Flare’s three-stage proposal would route the revenue into the protocol’s own token economics.

In the first stage, block building moves from individual validators to a designated builder, initially run by the Flare Entity, with a fallback to the current model if the builder is unavailable. In the second, block building moves into Flare Confidential Compute, making the process publicly auditable. The third stage merges the builder and proposer into a single entity, shifting existing validators to a verification role.

The proposal also creates FIRE, the Flare Income Reinvestment Entity to collect revenue from multiple protocol sources including attestation fees, FAsset and Smart Account fees, confidential compute fees and the captured MEV. FIRE’s primary mandate is reducing FLR token supply through open-market buybacks and burns.

Several changes would take effect immediately after approval. Annual FLR inflation would drop to 3% from 5%, with the hard cap cut to 3 billion tokens per year from 5 billion. A 20-fold increase to the base gas fee, from 60 gwei to 1,200 gwei, would raise estimated annual FLR burn from roughly 7.5 million to 300 million at current transaction volumes. Even after the increase, a standard Flare transaction would cost a fraction of a cent.

Flare has deep roots in the XRP ecosystem, having distributed its initial token supply through an airdrop to XRP holders in 2023. Its FAssets system, which has produced over 150 million FXRP, is designed to bring smart contract functionality to assets on blockchains like XRPL that do not natively support it.

The network reports over $160 million in total value locked as of late March 2026, with more than 887,000 active addresses.

The US Bureau of Labor Statistics (BLS) will publish the March Consumer Price Index (CPI) data on Friday. The report is expected to show a jump in inflation, driven by the upsurge seen in crude Oil prices after the United States (US) and Israel launched a joint attack on Iran.

The monthly CPI is forecast to rise 0.9%, following the 0.3% increase recorded in March, while the annual reading is seen climbing to its highest level since May 2024 at 3.3%, from 2.4% in February. Core CPI figures, which exclude volatile food and energy prices, are expected to come in at 0.3% and 2.7%, on a monthly and yearly basis, respectively.

Since the beginning of the conflict in the Middle East on February 28, the barrel of West Texas Intermediate (WTI) is up about 40%, even after the sharp decline seen following the announcement of a two-week ceasefire between the US and Iran earlier this week. In March, WTI gained nearly 50%, rising from about $67 per barrel to settle near $100 by the end of the month.

Previewing the inflation data, “the recent surge in crude prices will be the main factor behind the 0.9% m/m jump in the CPI. The Y/Y rate will leap close to 1pp to 3.3% in March, a two-year-high,” said TD Securities analysts.

“Core inflation will stay shielded from the oil shock for now, rising 0.27% m/m. We look for tariff pass-through to continue playing a role by lifting goods prices. Supercore inflation likely stayed firm at 0.3%,” they added.

What to Expect in the Next CPI Data Report?

CPI figures for March will reflect the impact of high oil prices on inflation, which shouldn’t be surprising. Even if the annual CPI inflation rises 3.3% in March, as forecast, investors could see that as a temporary increase in case they remain confident that Oil prices will come down significantly, with a permanent truce in the Middle East allowing the Strait of Hormuz to remain open.

However, the growing uncertainty about the sustainability of a ceasefire and Iran’s condition to retain control of the strait in a peace agreement complicates the picture and raises doubts about a steady pullback in Oil prices. Hence, the developments in the Middle East are likely to shape inflation expectations, rather than the March CPI reading itself.

The Minutes from the Federal Reserve’s (Fed) March meeting showed that a number of policymakers are already pushing back the timing of potential rate cuts, reflecting lingering concerns that inflation could prove more persistent than expected.

In fact, a large majority flagged the risk that price pressures could stay elevated for longer, particularly if higher Oil prices feed through more broadly.

“Provided that underlying inflation excluding energy remains contained, the Fed can afford to look through the oil-price shock and refrain from raising rates amid a mixed US labor market backdrop,” BBH analysts said.

How Could the US Consumer Price Index Report Affect Eur/USD?

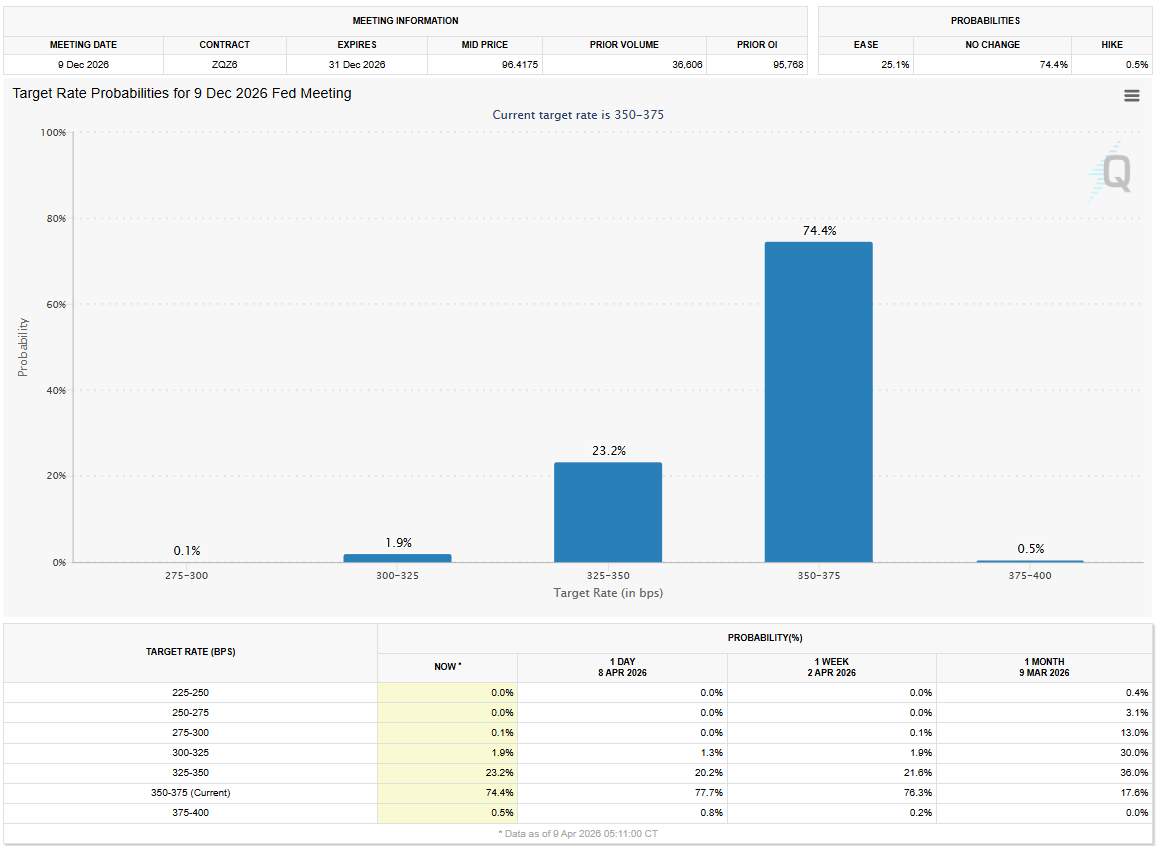

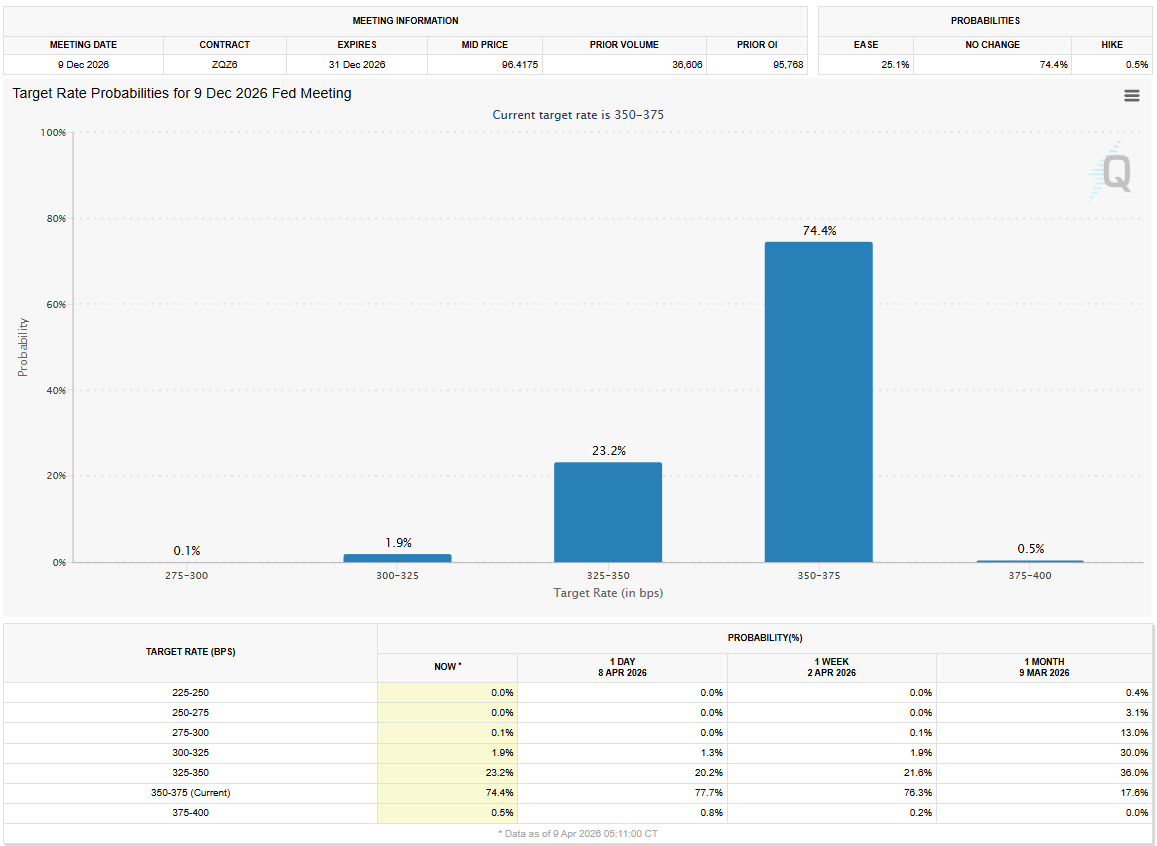

Markets currently see about a 75% chance of the Fed leaving the policy rate unchanged at 3.5%-3.75% by the end of the year, compared to a 17% probability seen on March 9, according to the CME FedWatch Tool.

A stronger-than-forecast monthly CPI print for March might not be able to influence the market pricing of the Fed’s interest-rate outlook in a significant way.

However, if a hot inflation print is combined with a re-escalation of the conflict in the Middle East and growing expectations about the naval activity in the Strait of Hormuz not going back to its pre-war state anytime soon, investors could reassess the probability of a Fed hike in response to persistent inflation. In this scenario, the US Dollar (USD) could gather strength and force EUR/USD to turn south.

Conversely, the USD could remain under bearish pressure – and allow EUR/USD to extend its rebound – in case crude Oil prices continue to come down in a steady way, regardless of the March CPI figures.

In summary, March inflation prints are unlikely to trigger a significant market reaction, while market focus remains on the US-Iran crisis and its impact on Oil prices.

Eren Sengezer, FXStreet European Session Lead Analyst, shares a brief technical outlook for EUR/USD.

“EUR/USD’s near-term technical outlook points to a bullish tilt. The Relative Strength Index (RSI) indicator on the daily chart climbed above 50 for the first time since the beginning of the US-Iran war and the pair broke above the two-month-old descending trend line.”

“The Fibonacci 50% retracement level of the February-April trend aligns as the next resistance level at 1.1730 ahead of 1.1800 (Fibonacci 61.8% retracement) and 1.1900 (Fibonacci 78.6% retracement). On the downside, the immediate support is located at 1.1650 (Fibonacci 38.2% retracement). In case this support fails, technical sellers could show interest, opening the door for an extended slide toward 1.1560 (Fibonacci 23.6% retracement) and 1.1500 (static level, round level).”

The post US CPI Inflation Set to Jump in March, Putting an End to Gradual Two-Year Decline appeared first on BeInCrypto.

MiCA introduced a unified European crypto market framework with one license valid across 27 countries. Large exchanges like Binance, Kraken, and Coinbase have successfully obtained MiCA licenses for all 27 EU countries.

For smaller companies, however, MiCA is proving to be a different kind of challenge. The regulation functions as a quality filter, but interpretations differ: some argue it removes bad actors, while others contend it disproportionately affects companies without deep capital reserves.

The True Cost of Compliance

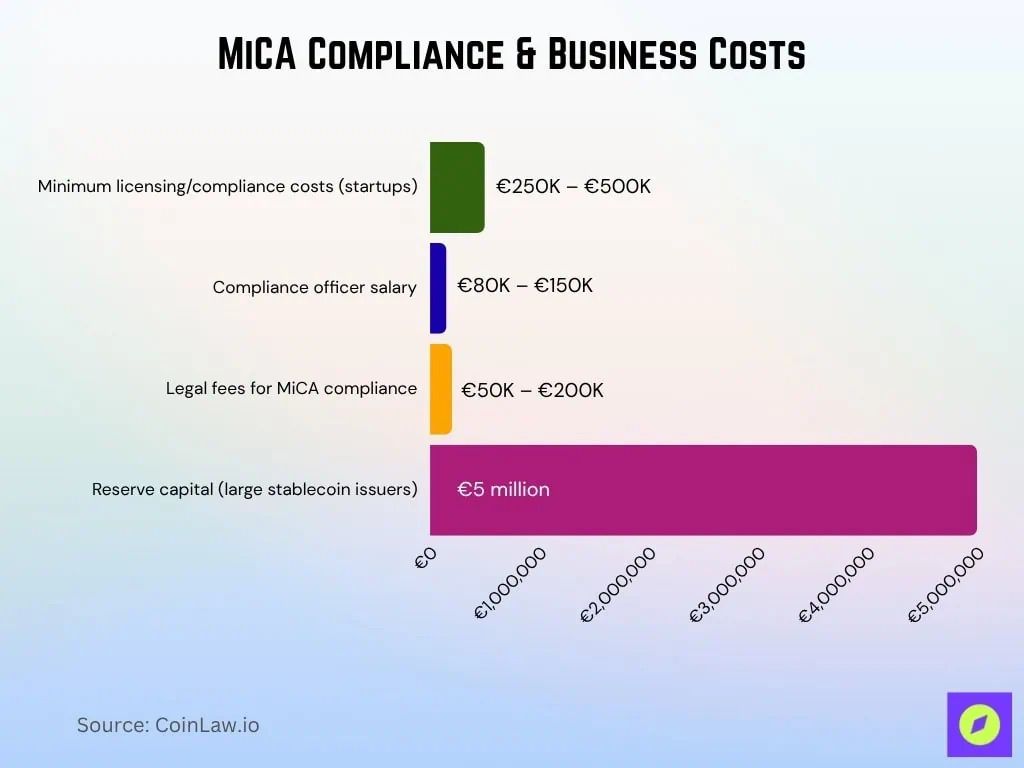

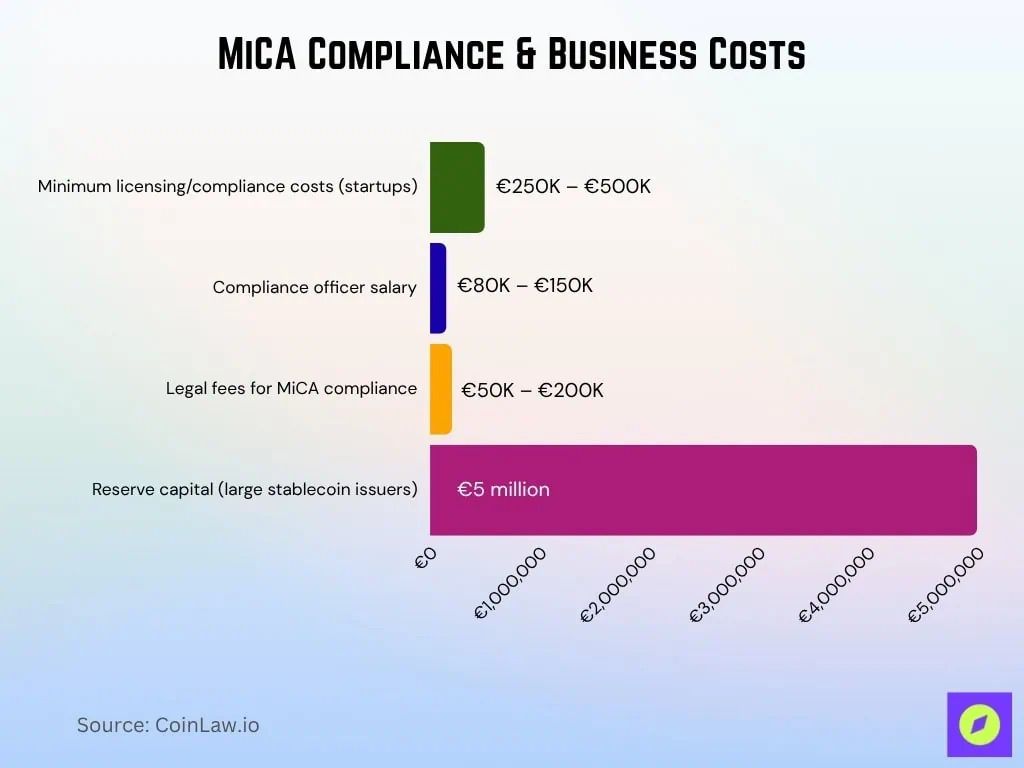

The cost breakdown reveals significant barriers to entry. Minimum licensing and compliance costs for crypto startups range from €250,000 to €500,000 for licensing alone, with additional expenses including compliance officer salaries (€80,000–€150,000 annually) and legal fees (€50,000–€200,000). Stablecoin issuers must also maintain a reserve capital of €5 million.

The impact varies considerably by company profile. Venture-backed exchanges treat these costs as manageable business expenses. Bootstrapped startups and small teams encounter substantially higher operational friction. The cumulative cost structure establishes a de facto market entry threshold that advantages capitalized players and disadvantages smaller entrants.

Holger Kuhlmann, speaking at the BeInCrypto expert council, articulated the operational pressure directly:

“A lot of companies are under pressure because they either do not have enough staff to handle the new rules properly or they need to hire more people and that quickly becomes expensive. Many companies have to make a decision between accepting more bureaucracy or taking on the cost and risk of relocation.”

This choice Kuhlmann describes is playing out across Europe. Industry data shows over 40% of crypto exchanges reported difficulty meeting MiCA’s reporting requirements specifically because of high compliance costs. At least 25% of exchanges that applied for MiCA licensing faced delays or rejections over incomplete AML documentation or other paperwork issues.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The Bureaucracy or Relocation Choice

For many smaller firms, relocation increasingly means Vienna. Austria’s Financial Market Authority offers licensing timelines under six months, significantly faster than German timelines. For companies that cannot afford to wait or to hire additional compliance staff, moving becomes the pragmatic economic choice despite the costs of relocation.

Germany’s strict interpretation of MiCA amplifies this pressure considerably. While most EU countries kept the full 18-month transition window that MiCA allowed, Germany shortened its deadline to just 12 months. Less time to prepare means higher costs, more pressure on limited resources, and more companies reaching the conclusion that relocation is preferable to compliance within the German framework.

This pattern has real consequences. Germany’s crypto hub status, as detailed in related analysis on the crypto hub question, depends partly on retaining startup ecosystems. Yet the compliance burden is precisely what pushes those startups elsewhere.

Winners and Losers Under MiCA

The data reveals a stark divide. MiCA-compliant businesses saw a 45% increase in institutional investments compared to non-compliant platforms. Large exchanges with existing institutional relationships, capital reserves, and compliance infrastructure have used MiCA as a moat against smaller competitors.

Binance, Kraken, and Coinbase secured MiCA licenses for all 27 EU countries. For them, MiCA functions as intended: it unified the market and removed uncertainty. The regulation brought legitimacy and enabled them to deepen institutional relationships.

Chris Pliessnig, whose firm Tirox navigated the MiCA transition for multiple clients, acknowledged both sides of the impact: “It opened up the product offering, the service offering, and it brought it to a new level.” That elevation happened—but only for companies with sufficient resources to reach the new level.

The Structural Shift

Germany granted over 30 MiCA licenses, but most went to traditional banks entering crypto for the first time. The startups that once made Berlin and Frankfurt attractive crypto destinations are licensing elsewhere, often in Vienna. The effect is a hollowing out of the startup ecosystem that originally built Germany’s reputation for innovation in digital assets.

One expert observed that Germany risks losing its status as a crypto hub not because of MiCA itself, but because of how strictly it applies the rules. The regulation is uniform across the EU, but enforcement strictness is not.

The Path Forward Remains Unclear

Smaller companies must navigate three constrained options: absorb compliance costs while accepting thinner margins and slower growth, relocate to Vienna or Lisbon and forgo existing customer relationships and German market access, or exit the market entirely.

This outcome diverges substantially from MiCA’s regulatory design intent. Experts interviewed for this analysis agreed that rather than creating market unification, the regulation has produced market consolidation favoring large, well-capitalized players. The barrier to entry for smaller competitors is now substantially higher. Some experts characterize this as necessary quality control; others view it as an unintended regulatory burden. The relocation patterns, however, indicate that companies themselves have already decided.

The post Why Smaller Crypto Companies Are Struggling Under MICA appeared first on BeInCrypto.

The Liquidation of Lebanon

McLaughlin: How BYU Could Benefit From a 5-Year Rule

OPPO F33 Series to Launch With IP69K Rating and 7,000mAh Battery

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports6 days ago

Sports6 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Tech3 days ago

Tech3 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

Business5 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion4 days ago

Fashion4 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion3 days ago

Fashion3 days agoLet’s Discuss: DEI in 2026

-

Politics7 days ago

Wings Over Scotland | The quality of mercy

-

Crypto World2 days ago

Crypto World2 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Crypto World22 hours ago

Crypto World22 hours agoCanary Capital Files SEC Registration for PEPE ETF

-

Fashion7 days ago

Fashion7 days agoFrugal Friday’s Workwear Report: Hammered Metallic Button Sweater Vest

-

Politics6 days ago

Politics6 days agoThe UK should not pay a penny in slavery reparations

-

Tech4 days ago

Tech4 days agoSamsung just gave up on its own Messages app

-

Tech4 days ago

Tech4 days agoHaier is betting big that your next TV purchase will be one of these

-

Fashion7 days ago

Fashion7 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

-

Fashion7 days ago

Fashion7 days agoWeekly News Update, 4.3.26 – Corporette.com

-

NewsBeat7 days ago

NewsBeat7 days agoKemi Badenoch talks ‘spring cleaning’ Reform defections

-

Tech4 days ago

Tech4 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

You must be logged in to post a comment Login