Crypto World

3 Polymarket Traders Bet on US-Iran Ceasefire, Signaling Forecasts

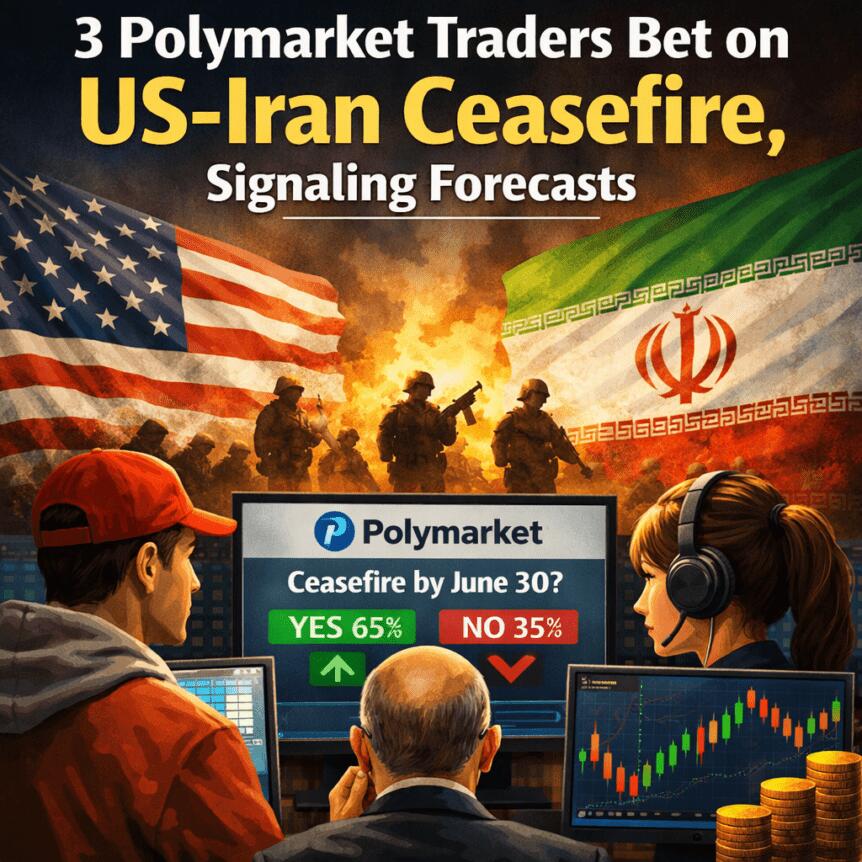

Fresh on-chain analytics show that three newly created wallets pocketed a combined $484,575 from Polymarket’s “US x Iran ceasefire by April 7” market, intensifying scrutiny over insider trading risks in prediction markets. Lookonchain highlighted that these wallets had no prior on-chain activity before placing their bets, suggesting rapid, opportunistic participation around a geopolitical event that drew intense attention.

Polymarket’s public activity feed confirms the three profits—$200,525, $158,600 and $125,450—were realized as trading continued during the period around the ceasefire news. The bets were placed at modest odds, with “yes” positions priced between roughly 2.9% and 10.3%. The payout occurred after the United States and Iran agreed to a two-week ceasefire on Tuesday, though both sides left room for the possibility of renewed action. The timing of the trades is notable: the earliest bet was placed at 1:59 pm UTC on Tuesday, roughly eight and a half hours before a Truth Social post by President Donald Trump at 10:32 pm UTC confirming a ceasefire. The other two positions opened at 10:01 am UTC on Tuesday and 8:50 pm UTC on Monday, according to blockchain-trace data.

The sequence of bets and the subsequent payout underscore a broader conversation about how prediction markets operate during geopolitical flux. As the market settled on a ceasefire timeline, participants with little or no on-chain history reportedly benefited significantly, prompting questions about information asymmetry, liquidity, and whether such patterns reflect legitimate hedging strategies or exploitative activity. While the event resolved into a temporary pause in hostilities, the underlying dynamics have sparked ongoing debate about how to monitor and regulate speculative markets tied to real-world events.

Prediction markets have emerged as a rapidly expanding niche within the crypto landscape. Industry observers note that prediction markets have become one of the fastest-growing uses for crypto, often surpassing $10 billion in monthly trading volume. The trend has drawn attention from policymakers who worry about insider trading and market manipulation that could undermine market integrity and consumer trust.

Key takeaways

- Three new Polymarket wallets earned a combined $484,575 from the US x Iran ceasefire by April 7 market, with wallets showing no prior on-chain activity before placing bets.

- The profits break down as $200,525, $158,600 and $125,450, with yes bets priced between 2.9% and 10.3% odds.

- One trader placed the first bet at 1:59 pm UTC on Tuesday—about eight and a half hours before the ceasefire confirmation—while the others opened at 10:01 am UTC Tuesday and 8:50 pm UTC Monday, according to on-chain records.

- Prediction markets continue to attract high volumes (often exceeding $10 billion per month), but they face increasing regulatory scrutiny and calls for stronger market-surveillance measures.

- Polymarket and Kalshi have started implementing safeguards to deter insider trading, including Kalshi’s independent advisory committee and a partnership with Solidus Labs for market abuse detection.

Geopolitics, markets and the regulatory glare

The episode sits at the intersection of rapid geopolitical news, crypto trading innovation and regulatory pushback. In January, U.S. lawmakers introduced a bill to curb officials from trading on prediction platforms after a Polymarket user reportedly profited more than $400,000 on a market tied to Nicolás Maduro. The proposal aims to reduce potential conflicts of interest and information leakage in sensitive bets, highlighting how policy makers view prediction markets as both open financial experiments and potential governance risks.

Meanwhile, international authorities have pursued legal action against traders seen as abusing information channels. In February, Israeli authorities arrested and indicted two individuals for allegedly using confidential information to place bets on a Polymarket event related to Israel’s potential strike on Iran, with one suspect reportedly connected to the Israeli military. These cases emphasize the stakes for traders and platforms alike, and they have spurred exchanges to bolster their surveillance and compliance programs.

To address the risk of market abuse, Polymarket has pursued ongoing improvements in oversight, while Kalshi has taken notable steps. Kalshi announced the formation of an independent advisory committee and a collaboration with Solidus Labs to enhance detection and investigation of market abuse. These measures are part of a broader push across prediction markets to balance innovation with responsible governance and user protection.

As coverage of these developments has shown, the debate over how to regulate prediction markets is shaping product design and market structure. Regulators are weighing how to preserve legitimate hedging and information discovery functions while curbing manipulation and unfair advantages. For traders and developers alike, the question now is how quickly platforms can operationalize robust surveillance without stifling legitimate participation or curtailing beneficial liquidity.

In the meantime, industry observers and investors will watch how policymakers translate sentiment into concrete guidance. The evolving regulatory backdrop, coupled with high-profile insider-trading concerns, could influence where liquidity flows, which markets gain credibility, and how quickly new participants ramp up their activity in this niche of crypto markets.

As the sector digests these developments, watchers should keep an eye on public disclosures from prediction-market platforms, updates to anti-manipulation tooling, and any new legislation or regulatory guidance that could shape how users access and interact with event-based markets in the months ahead.

The debate around centralized and decentralized exchanges has always generated more heat than clarity. CEX defenders point to DEX failures and declare the experiment incomplete. Proponents of self-custody treat centralized platforms as institutions to be dismantled. Both camps miss what actually matters: where the risk lives, and who agreed to carry it.

That is the real distinction between a CEX and a DEX. Not the technology, not the product surface, not the fee structure. It is a contract about responsibility.

The Trade-Off CEX Users Accept

When a user deposits on a centralized exchange, they are outsourcing operational complexity. The exchange handles custody, execution, fiat onboarding, and cross-chain access. You can deposit and withdraw through virtually any chain. Fiat flows in and out without requiring wallet management or on-chain knowledge. The friction inherent to crypto infrastructure largely disappears.

But the more significant transfer is less visible. By using a CEX, the user is also handing over accountability, and in doing so, gaining a kind of institutional caregiver. If a liquidation cascade wipes out positions and questions arise about how the platform performed, the exchange can choose to step in with bonuses, fee rebates, or direct compensation.

We have done this at Phemex, even during periods when the platform was operating at full capacity, when the pressure was highest and the easiest thing would have been to do nothing. That decision exists because there is a business that can make it, a team that can be held accountable, a relationship between platform and trader that goes beyond code.

Exchanges like Binance and Bitunix went down during those same events. We did not. On a centralized exchange, the user’s experience is something the business is personally invested in managing well.

That relationship does not exist on a DEX, by design. Rules are encoded and cannot be negotiated, adjusted for exceptional circumstances, or appealed to a support team. If you deposit to the wrong chain, the funds are gone. If a liquidation cascade hits and the protocol executes against you, no one will step in. The code ran. That is the final answer. There is no one to call, and that is exactly what the protocol’s users agreed to when they connected their wallet.

The Scope DEXs Unlock

The same conditions that remove the safety net also remove the intermediary, and for many users that is the point.

DEXs meaningfully expand what is possible in crypto. Liquidity provision, governance participation, and fee generation are all accessible to anyone willing to engage with the mechanics, not just to market makers or institutions.

A user who is not a trader can still participate in how markets function by providing liquidity to a pool. Someone holding an asset long-term can earn yield without trusting a third party with custody. When the tokenomics are structured well, users do not just trade on a protocol, they own part of it.

The counterweight is full responsibility. You manage your own wallet, you verify the chain before every transaction, and you accept the fixed parameters of the protocol regardless of whether those parameters favor you in a given situation. DEXs do not make exceptions, and that predictability is genuinely valuable.

But it demands a level of technical awareness and risk tolerance that is not realistic for every user in the market. Not all traders have traded on a DEX, and many have no interest in doing so because they simply do not want the burden of managing all of that themselves. That is a legitimate position, not a failure of ambition.

In my view, DEXs are a net positive for the ecosystem because they broaden the scope of what is possible by a lot. But users need to enter that environment with a clear understanding of what they are signing up for.

Where Centralized Exchanges Broke the Contract

Centralized exchanges have lost significant credibility over the past two years. FTX was the inflection point, but what came after made clear it was not an isolated failure. The pattern that emerged, platforms operating with backdoor arrangements, extracting value from users, managing reserves in ways that contradicted their public statements, damaged the confidence of retail participants in ways that have not fully recovered.

I have watched the sentiment shift in real time. Two or three years ago, the message of crypto was clear: alternative infrastructure, more freedom, more transparency, against institutions that resisted all of it. The adversary was traditional finance, the banks, the suits. That message has changed. What I see now is users against crypto scammers, honest participants against extractive ones. The adversary is no longer external. Platforms like Binance, which is now navigating a serious PR crisis of its own making, have become the entrenched incumbents that users are pushing back against. The very thing crypto was built to challenge, opaque institutions that operate in their own interest, has emerged inside the industry.

This is the responsibility that falls on those of us running centralized exchanges. The users who deposit on our platforms are making a specific bet: that the caregiver model is worth the trade-off, that handing over custody and self-sovereignty is worth the protection and the managed experience they get in return. When platforms violate that implicit agreement, they do not just hurt themselves. They push users toward self-custody and decentralized protocols, and given what some of those platforms did, that response is completely rational. The leaders of this industry failed to hold that trust. That is simply true.

The DEX market share relative to CEXs has grown month over month throughout 2025. Users are not moving to DEXs because on-chain execution suddenly became easier. They are moving because they stopped trusting the people running centralized platforms.

The Honest Framework

Neither model is inherently superior, and anyone telling you otherwise is trying to sell you something.

The question worth asking is much simpler: what kind of relationship does this user actually want with their trading environment? Someone who wants cross-chain deposits, fiat access, and a platform that takes responsibility when things go wrong will be better served on a centralized exchange like Phemex.

Someone who wants direct protocol interaction, self-custody, and participation in the underlying economics will be better served on a DEX, provided they understand the technical responsibility that comes with it.

These are different users making different choices about where risk should sit. The industry owes both of them honesty about the terms of that choice. Centralized exchanges cannot promise security while operating without transparency. Decentralized platforms cannot promise freedom while downplaying the responsibility users absorb in exchange.

What the next cycle requires from both sides is straightforward: say clearly what you are, deliver on it, and stop pretending the other model does not exist or does not serve a real purpose.

At Phemex, that is the standard we hold ourselves to. Not because it makes for a useful message. Because it is the only version of this business worth running.

The post CEXs and DEXs Are Not Competitors. They Are Different Contracts. appeared first on BeInCrypto.

Crypto World

Morgan Stanley’s bitcoin ETF opens today, giving BlackRock’s $55 billion IBIT fund its toughest rival yet

BlackRock’s most successful exchange-traded fund (ETF) is facing its clearest challenge yet, as Morgan Stanley rolls out a cheaper rival with direct access to trillions in client capital.

Morgan Stanley’s ETF, trading under MSBT, began trading Tuesday with a 0.14% expense ratio, below the iShares Bitcoin Trust’s (IBIT) 0.25%. The difference is narrow but lands in a market where price is one of the few levers investors can pull.

Each spot bitcoin ETF holds bitcoin and tracks its price. That leaves cost, liquidity and access as the main points of difference. IBIT has led on scale and trading activity since launch, becoming the most liquid vehicle for both shares and options tied to bitcoin ETFs with roughly $55 billion in assets-under-management.

That liquidity gives IBIT an edge that may be hard to replicate.

“The launch will impact things but it will be interesting to see if it can actually siphon assets from other funds,” said James Seyffart, ETF analyst at Bloomberg Intelligence. “IBIT is the most liquid ETF for trading and in the options market and it’s unlikely MSBT will ever compete with that. At least not anytime remotely soon.”

Still, Morgan Stanley’s entry changes the competitive balance.

The bank can tap its vast wealth management network, where advisors can shift client allocations with a single trade. In practice, that means new demand may be directed toward MSBT rather than existing funds like IBIT.

“Distribution is king in the ETF space, and Morgan Stanley has that in spades with its army of wealth managers,” said Nate Geraci, president of the ETF Store. “Combined with MSBT being the lowest-cost spot bitcoin ETF on the market, that’s a strong recipe for success.”

Geraci added that MSBT, which uses undercuts IBIT by 11 basis points, a gap large enough to draw attention from both investors and BlackRock.

IBIT’s position reflects how the market has evolved. Early inflows favored large, trusted issuers with deep liquidity. Over time, as more trusted names have entered the market, fee sensitivity has grown.

Morgan Stanley’s launch may speed up that shift, even if IBIT retains its lead in trading volume.

The result is a more defined split in the market. IBIT offers depth and liquidity for active traders.

Newer entrants like MSBT compete on cost and distribution. Morgan Stanley’s wealth management arm oversees trillions in client assets and has one of the largest adviser networks in the industry, giving the bank a steep advantage. As more capital moves through financial advisors rather than direct trading, that channel may carry increasing weight.

For now, IBIT remains the benchmark. But with fees falling and new entrants targeting its position, its grip on flows may face its first sustained test.

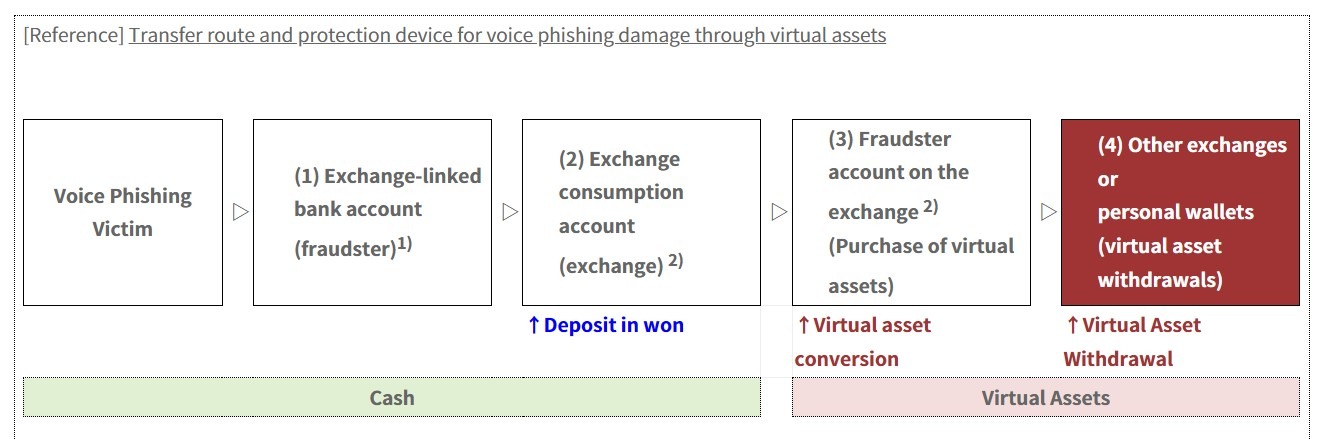

South Korea’s financial regulator said it will tighten the exception rules under crypto exchanges’ withdrawal-delay system after finding that scam-linked accounts granted exemptions accounted for most voice-phishing-related losses.

The Financial Services Commission (FSC) said Wednesday that the strengthened framework, developed with the Financial Supervisory Service (FSS) and the Digital Asset eXchange Alliance (DAXA), will impose unified standards on when users can bypass withdrawal delays.

The regulator said exchanges had been applying their own exception criteria with no clear minimum standard, creating loopholes that let bad actors quickly move funds if they meet easy requirements such as account age or trading history.

From June to September 2025, accounts granted withdrawal-delay exemptions made up 59% of fraudulent accounts and 75.5% of related losses at crypto exchanges, the FSC said.

The move follows a wider South Korean push to tighten crypto exchange controls after voice-phishing abuse and operational-control failures, including fresh reforms announced this week after Bithumb’s Bitcoin (BTC) payout error.

Unified rules aim to curb misuse of withdrawal-delay exemptions

The FSC said that under the new rules, exchanges must assess factors like trading frequency, account history and deposit and withdrawal amounts when determining whether a user qualifies for a withdrawal-delay exemption.

The regulator said the change is expected to reduce the number of users eligible for exemptions sharply. The FSC said a simulation showed the share of users eligible for exemptions would fall to around 1% under the new rules, but did not provide a baseline for comparison.

Related: South Korean brokerage Korea Investment & Securities eyes Coinone stake: Report

The FSC said it will also strengthen oversight of users granted exemptions through periodic checks, including verification of the source of funds, and by building systems to monitor suspicious withdrawal activity.

The regulator added that they will continue reviewing the rules to prevent new circumvention methods and adjust as needed.

The move adds to a broader push by South Korean regulators to tighten oversight of crypto exchanges following recent incidents.

On Tuesday, the FSC ordered exchanges to reconcile internal ledgers with actual asset holdings every five minutes after an inspection linked to the Bithumb payout error found gaps in internal controls and risk management systems.

On Jan. 29, South Korea expanded crypto licensing scrutiny to cover exchanges and major shareholders.

Magazine: ‘Phantom Bitcoin’ checks, Drift hack linked to North Korea: Asia Express

- Zcash surged above $336 after breaking key resistance as cryptocurrencies rose.

- The US-Iran ceasefire and fresh institutional interest have buoyed ZEC bulls.

- A potential short squeeze could catapult the ZEC price to above $500.

Zcash price has jumped 24% in the last 24 hours to $336, positioning ZEC as the top performer among the top 100 cryptocurrencies by market capitalization as of writing.

This sharp rally, which follows US President Donald Trump’s decision to abandon threats of military action against Iran in favour of a two-week ceasefire announcement, aligns with a pump across risk assets, including cryptocurrencies.

Zcash’s gains see it test the highest levels since late January 2026, and it currently sits 18th among the largest coins by market capitalization.

ZEC pumps amid crypto uptick

Zcash has pushed decisively beyond $300, delivering double-digit gains in 24 hours as its short-term outlook shifts bullish amid de-escalation in the US-Iran war.

The privacy-focused coin rose to intraday highs of $336, having cleared a major supply barrier as it tracked altcoins that echoed Bitcoin’s climb past $72,000.

ZEC traded at lows of $250 on Tuesday, and today’s uptick comes amid a 170% spike in daily volume.

Notably, geopolitical developments have added fuel to the upside spark of fresh institutional interest.

For instance, Foundry, operator of the world’s leading Bitcoin mining pool, has revealed plans to enter Zcash mining.

Also notable is the Zcash Open Development Lab’s unveiling of a $25 million ecosystem fund, with the initiative boasting the backing of global venture powerhouses like a16z crypto, Paradigm, and Coinbase Ventures.

Zcash price analysis

Zcash was holding above $330 on April 8, 2026, up on the day, as the broader near-term sentiment hints at bullish bias.

The positive picture aligns with the token’s powering through the convergence of its 100-day and 200-day Exponential Moving Averages (EMAs)

ZEC’s rebound means bulls can now eye the February 14 peak as a support level.

A firm close beyond this previous resistance-turned-support mark could unlock further upside, potentially triggering a short squeeze toward $500. Buyers now dominate as shorts suffer.

Leading into the breakout, Zcash had traced higher lows after a dip to a low of $193 on March 7, 2026.

Despite a long-term descending trendline, gains signal steady accumulation by investors. Momentum indicators back this recent outlook.

As well as the RSI, the Awesome Oscillator (AO) has flipped positive with expanding green bars.

That said, the steep vertical advance over the past two days hints at short-term overextension, particularly with the RSI in overbought territory.

In any case, such explosive moves typically invite minor retracements or sideways action.

Zcash price could thus revisit the $250-$230 region, before resuming higher.

Global markets moved unevenly as geopolitical tensions intensified and energy prices climbed sharply. Oil prices surged above key levels while Bitcoin maintained stability despite pressure. Meanwhile, equities fluctuated as traders reacted to escalating rhetoric and uncertain diplomatic outcomes.

Oil Market Reacts to Supply Disruption

Oil prices climbed above $110 per barrel as supply concerns deepened across global markets. Brent crude traded near $110 while West Texas Intermediate hovered above $112 during volatile sessions. These levels marked the highest range since 2022 and reflected tightening supply conditions.

The Strait of Hormuz remained partially disrupted, which affected nearly one-fifth of global oil shipments. Tanker delays increased, and shipping insurance costs rose sharply as risks intensified across the region. As a result, energy markets experienced strong upward pressure and persistent volatility.

The crisis also raised concerns about inflation and economic stability across major economies. Higher energy costs pushed production expenses upward and strained supply chains globally. Consequently, policymakers faced increasing pressure as inflation risks expanded alongside slower growth expectations.

Bitcoin Shows Stability Amid Market Stress

Bitcoin traded around $68,400 and held firm despite broader financial market volatility. The digital asset showed resilience even as sentiment indicators reflected heightened fear across markets. This divergence highlighted strong underlying demand from long-term holders and institutions.

Institutional participation supported Bitcoin’s price as large entities accumulated significant volumes in recent weeks. Exchange-traded funds absorbed substantial inflows earlier, though recent sessions showed moderate outflows. Even so, the overall structure remained stable as buyers maintained key support levels.

Leverage activity contributed to recent price movements, yet Bitcoin avoided sharp declines seen in other risk assets. This stability positioned the asset as a potential hedge during geopolitical uncertainty. As a result, Bitcoin maintained relative strength while traditional markets showed mixed performance.

Equities Fluctuate as Geopolitical Pressure Builds

Equity markets posted mixed results as geopolitical developments shaped market direction throughout the session. Major indices moved between gains and losses before stabilizing near closing levels. This pattern reflected uncertainty around potential escalation and diplomatic efforts.

Energy-driven inflation concerns weighed on sentiment while economic data added further pressure. Reports showed weaker demand in key sectors, which increased concerns about slowing economic activity. At the same time, rising input costs signaled continued inflationary pressure across industries.

Late-session momentum improved after signs of possible diplomatic engagement emerged from international leaders. Markets responded positively to any indication of reduced tension and potential negotiation. However, uncertainty remained high as the situation continued to evolve.

Crypto World

DOJ Says Tornado Cash Developer Made 250 Changes to the Protocol: Is the Immutable Code Defense Dead?

The DOJ core legal theory in the Roman Storm crypto case has never been that writing code is a crime. It’s that exercising operational control over a platform that processes more than $1 billion in illicit funds – while explicitly declining to implement feasible anti-money-laundering controls – constitutes running a criminal business.

That distinction is the mechanism that makes this case matter far beyond Tornado Cash.

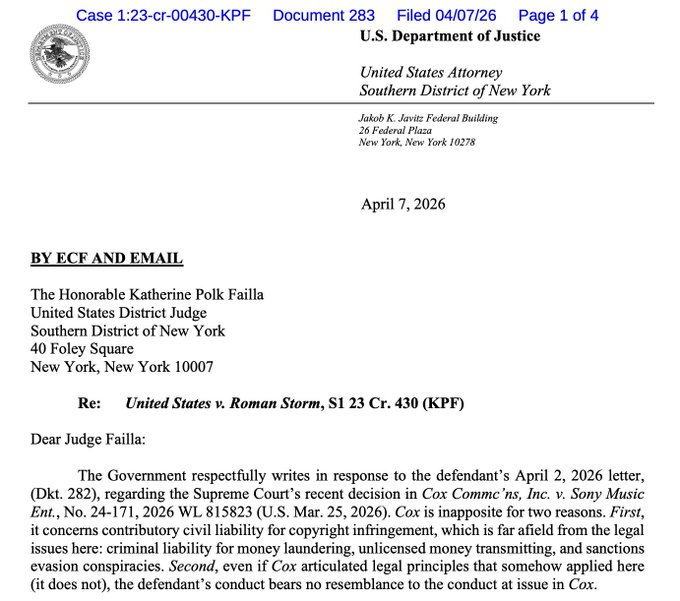

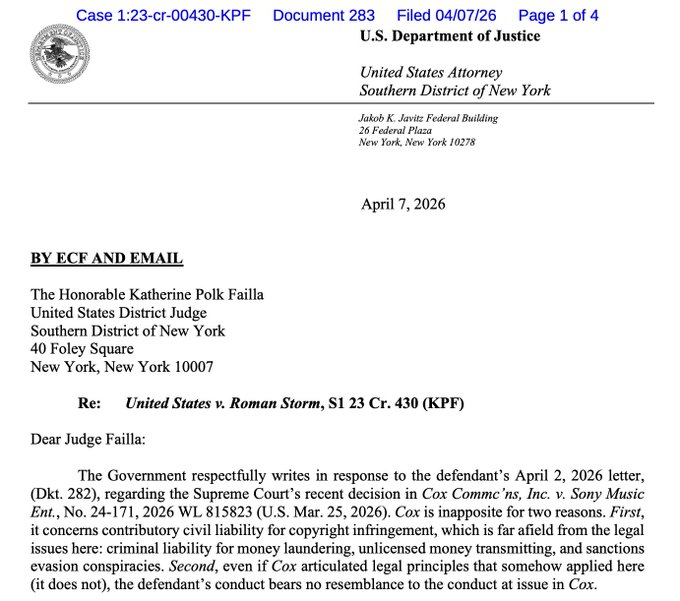

Prosecutors filed a letter Tuesday rejecting Storm’s attempt to leverage a March Supreme Court ruling in Sony Music v. Cox Communications as grounds for dismissal.

The DOJ called the analogy “inapposite” – and the reasoning behind that rejection defines exactly what level of developer involvement triggers federal criminal liability under the current enforcement framework.

The unresolved question: where is the legal floor for DeFi developers who upgrade protocols, manage governance, and selectively respond to compliance inquiries? After Tuesday’s filing, that floor is still undefined – and prosecutors are pushing to make Storm’s retrial the place where it gets drawn.

- The Dismissal Attempt: Storm’s attorneys cited the Supreme Court’s Cox ruling – which shielded the ISP from liability for users’ copyright infringement – as precedent for dismissing criminal charges. DOJ prosecutors rejected the parallel as inapplicable to Storm’s conduct.

- The Control Argument: Prosecutors documented over 250 changes made to the Tornado Cash infrastructure during the charged period, directly contradicting Storm’s defense that the protocol was immutable code beyond his control. That operational record is central to the money laundering conspiracy charge.

- The Partial Conviction: A jury in August 2025 convicted Storm on conspiracy to operate an unlicensed money-transmitting business but deadlocked on money laundering conspiracy and sanctions evasion – the two charges prosecutors now want retried in October 2026.

- The Privacy Protocols Precedent: DOJ’s framing – that developers who implement changes and knowingly forgo compliance measures are operators, not bystanders – applies directly to any upgradeable DeFi protocol with identified founders or core teams.

- The Exposure: Storm faces up to 40–45 years in prison if convicted on all counts. The retrial scope covers the two deadlocked charges; the money transmitting conviction stands.

- What to Watch: The conference between Storm’s defense and Judge Katherine Polk Failla’s court will determine whether October 2026 becomes a firm retrial date – the specific scheduling order is the next legal trigger that confirms or compresses the timeline.

Explore: The best pre-launch token sales with asymmetric upside potential

What the DOJ’s Cox Rejection Actually Establishes – and Why the ‘Immutable Code’ Defense Is Running Out of Road

Storm’s legal team drew a specific parallel: the Supreme Court found Cox Communications shouldn’t be held liable for its users’ infringing activity because Cox had a robust, 98%-effective termination policy for repeat infringers.

The argument was that Storm, like Cox, was a neutral infrastructure provider. Prosecutors dismantled that comparison in a single filing.

The DOJ’s letter to Judge Failla emphasized that Cox actively discouraged the illegal conduct occurring on its network – while Storm and his co-conspirators at Tornado Cash did the opposite.

Prosecutors stated that Storm “actively lied in response to inquiries from victims, telling them he had little control over the protocol when in fact he and his co-conspirators implemented over 250 changes to Tornado Cash infrastructure during the charged time period and explicitly discussed – but forwent – feasible measures to curb criminality on their platform.”

That last clause is the legal weight-bearing element. Under the money laundering and unlicensed money transmission statutes at issue, the question isn’t whether a developer wrote code – it’s whether they operated a system they knew was being used for money laundering, had the capacity to limit that use, and chose not to.

The Bank Secrecy Act’s anti-money-laundering compliance obligations attach to operators, not passive bystanders. Prosecutors’ position is that Storm was an operator by every functional measure.

“In short, the defendant’s reaction to criminal use of his company was window dressing at best and outright misdirection at worst” – prosecutors’ letter to Judge Failla, filed Tuesday.

The August 2025 jury conviction on the unlicensed money transmission count already rejected Storm’s passive-developer framing once.

The October 2026 retrial targets the money laundering conspiracy and sanctions evasion charges directly – the counts where the jury deadlocked, not where it acquitted. That distinction matters: deadlock means twelve jurors couldn’t reach unanimity, not that the evidence was insufficient to convict.

Discover: The Best Crypto Presales Live Right Now

The post DOJ Says Tornado Cash Developer Made 250 Changes to the Protocol: Is the Immutable Code Defense Dead? appeared first on Cryptonews.

Evernorth has moved its XRPN merger plan forward with a fresh SEC filing. The amended S-4 keeps the company on course for a Nasdaq market debut. The transaction would combine Evernorth with Armada Acquisition Corp. II.

The move follows the SPAC route rather than a standard IPO. It gives the market another formal step in the listing process. If the deal closes, stock investors could access Evernorth’s XRP-focused strategy through a public company. For now, the filing serves as a process update, not a final approval.

Evernorth Advances Merger Process With Amended S-4 Filing

On April 7, 2026, Evernorth filed “Amendment No. 1” to its “Form S-4” with the SEC. The filing relates to its proposed merger with Armada Acquisition Corp. II. Armada already trades on Nasdaq under the ticker XRPN. The amendment keeps the registration path active.

A Form S-4 is used in business combinations that involve new securities. In this case, Evernorth is using a SPAC structure. That route differs from a traditional IPO. It links the market debut to the merger close.

The amended filing adds to earlier paperwork in the same transaction. It may include revised terms, updated disclosures, or responses to Sec comment. Such changes are common during review. They also give the market a clearer record before any shareholder vote.

The filing does not mean the merger is complete. The SEC review must continue, and other approvals may still be needed. Shareholders may also need to vote on the transaction. Closing terms remain part of the process.

XRPN Route Gives Evernorth a Public Market Path

XRPN is the current Nasdaq ticker for Armada Acquisition Corp. II. Evernorth plans to reach the market through that listed vehicle. If the transaction closes, the combined company would gain public market access. That is the core purpose of the merger.

The company has drawn attention because of its focus on XRP. Evernorth has described a business model tied to XRP exposure and treasury strategy. That approach differs from most recent SPAC deals. It also connects the transaction to digital asset markets.

Market attention has grown because few public companies center their strategy on XRP. No official filing text provided here confirms a direct partnership with Ripple. Even so, the company’s XRP focus remains central to the deal story. That keeps the merger in view across crypto markets.

For some investors, a listed stock can be simpler than direct token ownership. Shares can be bought through standard brokerage accounts. That structure may widen access for investors who avoid crypto custody. It may also increase attention on future treasury disclosures.

Next Steps Remain Before Any Nasdaq Debut

The next stage will center on SEC review and deal approvals. The parties may need to answer more staff comments. They may also need to update risk factors and financial details. Those steps are normal in a SPAC merger.

Market watchers are also tracking potential fundraising around the transaction. Reports have said Evernorth may seek more than $1 billion. Public confirmation on the final amount remains limited. Future filings may provide clearer numbers.

Reports have also mentioned interest from crypto-focused firms. However, the terms and participants remain unconfirmed in the provided details. Investors usually wait for named commitments in official documents.

Apple’s outlook looks materially different from the one traders were pricing a year ago. After delivering $416.2 billion in FY2025 net sales and a record $143.8 billion revenue in fiscal 2026 1Q, AAPL enters mid-2026 tied to three themes: whether the foldable iPhone expands the addressable market, whether Apple Intelligence translates into measurable Services growth, and whether a 29x forward multiple holds up if macro conditions weaken.

Analytical Apple Stock Price Prediction: Quick Answer

AAPL trades near $260 as of 6th April 2026, somewhat below its all-time high of $288.62 made in December 2025. The 12-month analyst consensus averages $304.40 across 24 analysts tracked by TipRanks, with targets ranging from $248 (Barclays) to $350 (Wedbush). MarketBeat’s average sits at $297.58.

The stock trades at approximately 29x forward earnings on consensus FY2026 EPS of $8.60–$8.80, which assumes that continued Services momentum, a full iPhone 18 and foldable launch cycle and no major tariff escalation further support AAPL’s price trajectory.

Recent Price History of AAPL

AAPL traded in a wide range over the past twelve months, swinging from around $169 near its April 2025 low to an all-time high of $288.62 in early December 2025. That represents a move of roughly 70% from trough to peak. As of 6th April 2026, AAPL is priced at around $260, having oscillated between $243 and $280 since the start of the year.

Several catalysts drove the rally. A 90-day tariff pause in April 2025 triggered an immediate bounce. Strong quarterly earnings through mid-2025 kept momentum building, and the iPhone 17 launch in September added fresh demand. Apple’s $100 billion US investment pledge in August also lifted sentiment.

The sharp swings reflected how sensitive AAPL had become to trade policy and macro headlines. In early April 2025, the stock lost over $770 billion in market capitalisation across four sessions. The recovery was equally aggressive once tariff fears eased and earnings came through.

Key Drivers Behind the Apple Stock Forecast in 2026

Several factors are driving expectations for Apple in 2026.

Services Growth

Services is now Apple’s second-largest revenue stream and its highest-margin segment. In FY2025, Services revenue set a new record of ~$109.16 billion, growing approximately 13.5%-14% year-over-year. iPhone revenue grew 4% to $209.6 billion. Fiscal Q1 2026 pushed Services to a quarterly record of $30.0 billion. Advertising, payments and cloud all set new highs. CFO Kevan Parekh has guided FY2026 Services growth at a similar rate to FY2025, pointing towards roughly $123 billion for the full year.

Greater China, Tariffs and Supply Chain Diversification

Greater China remained a pressure point in FY2025, with net sales down 4% year on year, while Europe, Japan and Rest of Asia Pacific all grew. However, Q1 FY2026 saw a sharp reversal: Greater China revenue jumped 38% to $25.5 billion. On tariffs, the US Supreme Court struck down IEEPA tariffs in February 2026, though a 10% Section 122 surcharge remains in place.

iPhone Upgrade Cycle

The iPhone 17 drove Q1 FY2026 iPhone revenue up 23% to $85.3 billion. Morgan Stanley estimates around 550 million active iPhones cannot run Apple Intelligence, highlighting a sizable installed base that may require hardware upgrades over time, potentially supporting future iPhone demand. A foldable iPhone is expected in late 2026, priced between $1,800 and $2,500.

Apple Intelligence

Apple Intelligence is live across 16+ languages on iPhone 15 Pro and newer devices. The full conversational Siri overhaul, powered by Google’s Gemini AI model, remains delayed, with a phased rollout now expected through late 2026.

Capital Returns

Apple authorised an additional $100 billion repurchase programme in May 2025 and bought back $90.7 billion of common stock during FY2025. Buybacks reduce the share count and directly support diluted EPS, which rose 19% to $2.84 in Q1 FY2026 on revenue of $143.8 billion.

Traders may keep up to date with AAPL CFD price movements in FXOpen’s TickTrader platform.

Analytical Bull, Base and Bear Scenarios for AAPL (12-Month Outlook)

In a base case, Apple keeps expanding Services, protects margins and posts steady EPS growth, supporting a gradual re-rating. In a bull case, the foldable iPhone, Apple Intelligence adoption and Greater China momentum lift the revenue mix and justify a richer multiple. In a bear case, softer consumer spending, tariff escalation and slower AI execution cap earnings.

These Apple target prices for 2026 are based on publicly available analyst consensus data from TipRanks, accessed April 2026 (24 analysts). Published values: average $304.40, high $350.00, low $248.00.

Other aggregators, including MarketBeat (average $297.58) and Ticker Nerd (median $300.00 across 77 analysts), show a broadly similar range, although exact figures vary due to differences in analyst coverage, sample windows and update frequency.

Analytical Long-Term Outlook for AAPL (2027–2030)

Projecting precise Apple stock forecasts for 2027 and beyond is difficult, especially given its 30x+ forward earnings. A more practical approach is to identify what would need to happen for AAPL to move materially higher or lower from current levels.

New Device Categories and Form Factors

The foldable iPhone, expected in late 2026, opens a price tier Apple has never occupied. If it succeeds, it adds a $1,800–$2,500 product to the lineup and lifts average selling prices. Beyond that, smart glasses (rumoured for 2027) and AI-enabled wearables could create new revenue streams. Vision Pro has underperformed commercially, so execution here is not guaranteed to lift Apple stock price predictions in 2027 and later.

AI Platform Maturity

Apple Intelligence needs to evolve from a feature set into a genuine platform by 2027–2028. If on-device AI drives measurably higher engagement, App Store spending and Services attach rates, it supports both revenue growth and a premium multiple. If Siri remains behind other voice assistants, the narrative weakens.

Regulatory Pressure on Services Economics

The EU Digital Markets Act, US DOJ antitrust trial (expected 2027), and ongoing App Store commission disputes pose structural risk to Services margins. A forced reduction in commission rates from 30% to 20% or lower would compress the segment’s contribution meaningfully over this period.

Valuation Sustainability

AAPL’s current forward P/E of roughly 29x assumes continued double-digit EPS growth. If earnings were to compound between 10% and 12% annually through 2030, the stock could continue to rate higher. If growth slows to mid-single digits, multiple compression pulls it back. Buybacks will continue to support per-share metrics, but they cannot offset a fundamental slowdown indefinitely.

How Traders Can Evaluate the Apple Stock Outlook

Traders typically break an AAPL analysis into a few core steps.

- Starting with earnings and valuation, traders check the trailing and forward P/E ratio against Apple’s five-year average and the broader S&P 500. If the premium is widening without a corresponding acceleration in EPS growth, the risk/reward shifts.

- Tracking Services momentum. Services revenue and its growth rate are the clearest signal of whether Apple is becoming a higher-margin business or staying hardware-dependent. Quarterly earnings releases break this out directly.

- Monitoring the product cycle calendar. iPhone launch quarters consistently drive the largest revenue beats. Traders check when new models ship and whether supply chain reports suggest strong or constrained demand.

- Watching macro and trade policy. AAPL’s sensitivity to tariff headlines and consumer confidence was on full display in 2025. Interest rate direction and trade policy shifts remain key swing factors.

Risks That Could Cap the Upside

China Exposure

Greater China accounts for roughly 15% of Apple’s revenue. A renewed demand slowdown or market share gains from Huawei could reverse the Q1 FY2026 recovery quickly. Geopolitical tensions add an unpredictable layer.

Valuation Compression

AAPL trades at around 29x forward earnings. That multiple leaves little room for disappointment. Any earnings miss or guidance cut would likely trigger a sharper drawdown than for a stock on a lower multiple.

Macro and Consumer Weakness

US consumer confidence sits near recessionary levels. If household spending weakens further or rate cuts stall, demand for premium devices softens. Launching a $2,000+ foldable into that environment carries timing risk.

AI Execution Gap

Google, Samsung, and Meta are shipping competitive AI features now. If the delayed Siri overhaul underwhelms when it arrives, the AI premium embedded in the stock fades and AAPL loses a key part of the upgrade narrative.

Regulatory Drag on Services

The EU DMA review report lands in May 2026 and the US DOJ antitrust trial is expected in 2027. Forced commission cuts or sideloading mandates would directly compress Apple’s margins.

Final Thoughts

Apple’s financial performance heading into 2026 is strong by any measure. Record revenue, accelerating Services growth and a large upgrade base give the stock a solid fundamental floor. But the valuation already reflects much of that strength. The path for Apple’s stock in 5 years depends on whether Apple Intelligence delivers real differentiation, whether the foldable iPhone expands the addressable market and whether macro conditions hold up.

Traders looking to explore AAPL and other stock CFDs may consider opening an FXOpen account and using the TickTrader platform for charting and analysis.

FAQ

What Is the Apple Stock Forecast for 2026?

The Apple stock prediction 2026 consensus averages $304.40 across 24 analysts on TipRanks, with a low of $248.00 and a high of $350.00. MarketBeat puts the average at $297.58, while Ticker Nerd‘s median across 77 analysts is $300.00. The spread reflects ongoing disagreement over AI execution, tariff risk, and the foldable iPhone’s impact.

What Could Push AAPL Higher?

A foldable iPhone super-cycle, faster-than-expected Apple Intelligence adoption, continued Services growth, and sustained Greater China recovery are seen as the primary upside drivers.

How Much Will Apple Stock Be Worth in 10 Years?

Analytical Apple stock predictions in 10 years are highly uncertain. The outcome depends on revenue growth, margin trajectory, new product categories and the broader market environment. Apple’s track record of compounding earnings is strong, but past returns do not guarantee future performance.

What Will Apple Stock Be Worth in 2030?

Rather than target a specific analytical Apple stock forecast for 2030, traders typically focus on what would need to go right or wrong. Sustained 10%–12% annual EPS growth and new device categories would support a higher share price. Slower growth, regulatory headwinds or multiple compression would cap analytical Apple stock price predictions for 2030.

Will Apple Stock Ever Reach $1,000?

Reaching $1,000 from roughly $255 would require a near-fourfold increase. At 12% annual EPS growth with a steady multiple, that could take well over a decade. A stock split, new revenue streams or a structural re-rating could shorten this Apple stock forecast to 5 years or more, but less than 10.

How High is Apple Stock Expected to Go?

The current Street-high 12-month target is $350, set by Wedbush analyst Dan Ives. Beyond that, longer-range projections vary widely and carry low reliability. Most analysts anchor their outlook to earnings visibility one to two years ahead.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

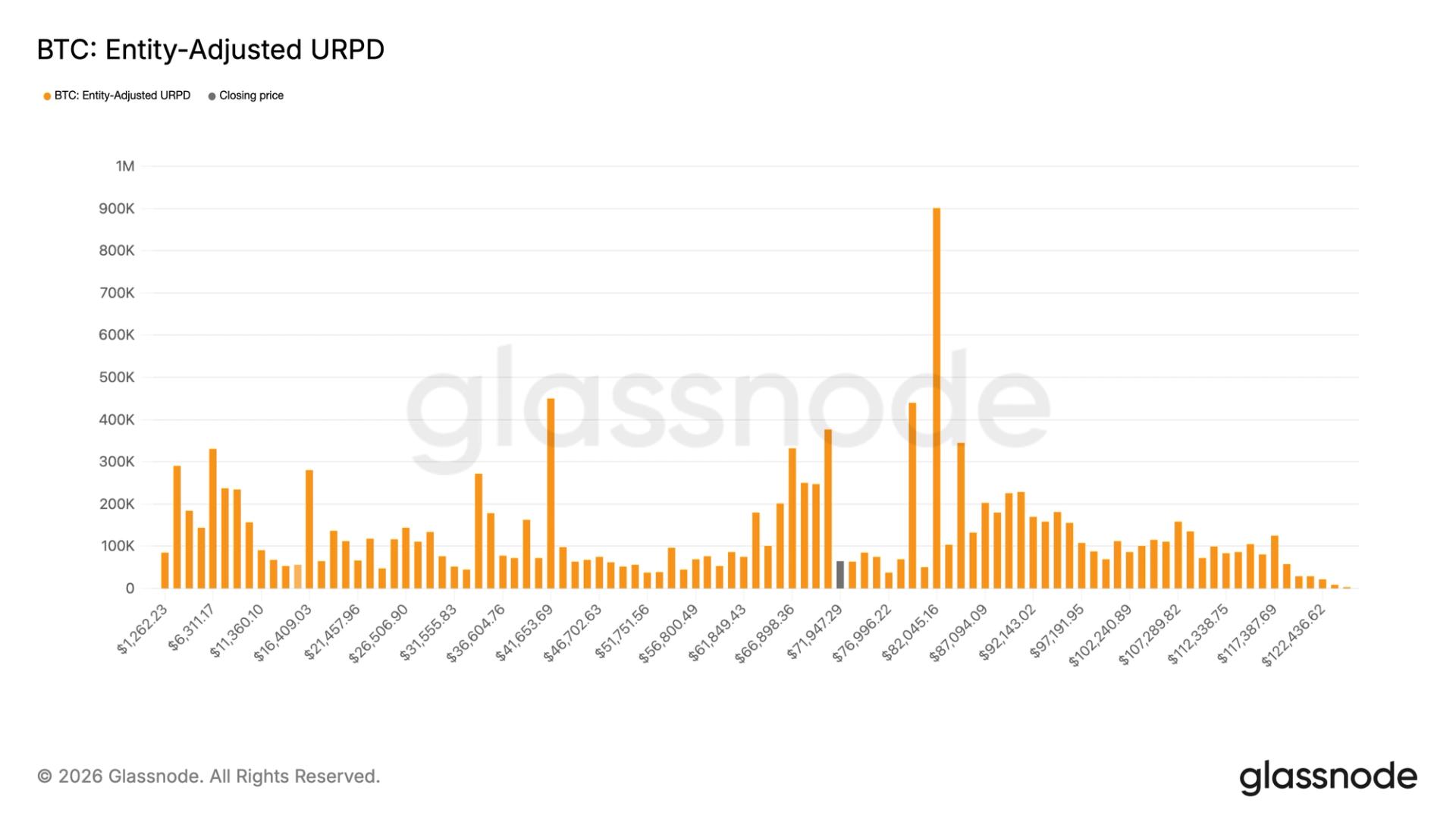

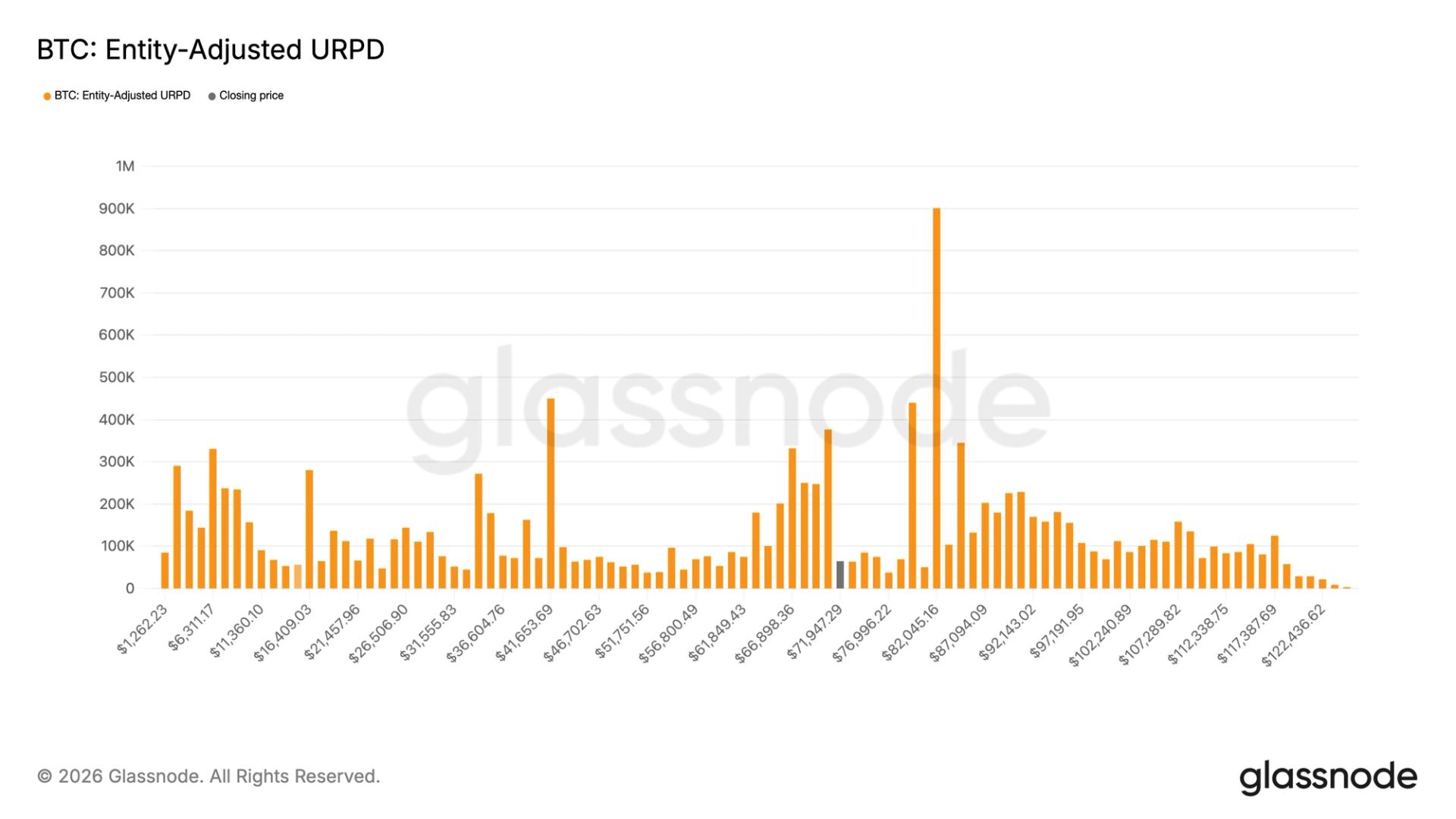

Bitcoin may have recently looked choppy under $70,000, but a ton of BTC was traded then, in a sign of strong dip demand.

That’s evident from blockchain data, which shows the total amount of BTC that last moved on-chain in the $60,000-$70,000 range now stands at 1,845,766 BTC, up from 1,001,491 BTC on Jan. 1, according to data source Glassnode. This increase of 844,275 BTC indicates that some market participants aggressively bought the dip below $70,000.

More importantly, that 1.84 million BTC figure accounts for about 9.23% of bitcoin’s circulating supply. It means valuations below $70,000 could act as a floor because a lot of coins are “anchored” there and sellers might be reluctant to sell below it.

These numbers are derived from Glassnode’s Realized Price Distribution (URPD) metric, which shows the price levels where the current set of bitcoin UTXOs – basically, individual chunks of bitcoin in wallets – were last moved. Each bar, as seen in the feature image, represents how much bitcoin is held at a given price. This version is entity-adjusted, meaning coins held by the same owner are grouped together based on the average price they were acquired at.

While the $60,000 to $70,000 range has seen heavy activity, $70,000 to $80,000 looks relatively thin, according to Glassnode. Just 400,000 BTC sit in this range, which is nearly half of the amount transacted below $70,000.

Bitcoin has bounced back above $70,000 following the temporary ceasefire between the U.S. and Iran. The cryptocurrency spent a better part of the past five weeks or so trading back and forth below $70,000. Yet, it remained resilient relative to traditional risk assets, such as stocks, which wilted as Iran war lifted per barrel oil prices above $100.

SEC Case Count Falls as Agency Resets Enforcement Approach

The US Securities and Exchange Commission reported a sharp drop in enforcement activity for fiscal 2025. The agency said it brought 456 enforcement actions through September. That was down from 583 actions in the prior year.

The news comes as the SEC changes its enforcement approach under Chairman Paul Atkins. The agency said it now wants fewer volume-driven cases. It said the focus is on fraud, market manipulation, and abuses of trust.

Penalty Totals Rise on Old Ponzi Case While Core Remedies Fall

The SEC said its latest annual report reflects a different way to judge enforcement work. The agency said past resources were often used to raise case counts. It said that method created the wrong standard for effective enforcement.

The SEC also said its annual totals did not include 1,095 matters that were investigated and later closed. Some of those matters involved practices that were fixed without formal charges. The agency used that point to explain its new reporting frame.

Atkins described the new direction in the agency statement. He said, “We have redirected resources toward the types of misconduct that inflict the greatest harm.” He added that the SEC is moving away from approaches centered on volume and record penalties.

The decline was also shaped by timing. SEC data showed that nearly half of the 456 actions were filed before January 2025. That means activity slowed further after the Trump administration began.

Crypto Cases and Staff Losses Add to the Shift

The policy change has also reached the crypto sector. Under current leadership, the SEC has dismissed several high-profile cases against crypto firms and executives. That move matters for digital asset markets because the agency had pursued the sector aggressively in earlier years.

For crypto readers, the new report signals a softer enforcement posture in some areas. Still, the SEC said fraud and market manipulation remain top priorities. That means crypto-related conduct can still draw action when investor losses are clear.

The enforcement division also faced internal strain during the year. Its enforcement director resigned suddenly last month. At the same time, the division lost 18% of its staff in fiscal 2025, according to a recent government report.

Staff losses and leadership turnover often slow enforcement work during transition periods. Experts have noted that such slowdowns are common after a change in administration. In 2025, however, the drop in SEC activity also reflects a clear reset in how the agency defines enforcement success.

CEXs and DEXs Are Not Competitors. They Are Different Contracts.

Patriots’ Mike Vrabel, Dianna Russini React to Hotel Photos

Moti chain mota paisa #pawansahu #naturalbodybilding #money

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Moti chain mota paisa #pawansahu #naturalbodybilding #money

These 6 simple rules can change your financial future #MoneyRules #FinancialFreedom #MoneyManagement

FASILITAS NUKLIR IRAN DISERANG! #trading #kriptodump #trader #forex #crypcurrencey #bitcoin #kripto

-

NewsBeat6 days ago

NewsBeat6 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business6 days ago

Business6 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World7 days ago

Crypto World7 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business3 days ago

Business3 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business4 days ago

Business4 days agoExpert Picks for Every Need

-

Sports4 days ago

Sports4 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech15 hours ago

Tech15 hours agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business3 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Tech6 days ago

Tech6 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Fashion2 days ago

Fashion2 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World7 days ago

Crypto World7 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Tech7 days ago

Tech7 days agoDrawing Tablet Controls Laser In Real-Time

-

Crypto World7 days ago

Crypto World7 days agoWhy It’s Partnering, Not Issuing

-

Politics5 days ago

Wings Over Scotland | The quality of mercy

-

Sports7 days ago

Sports7 days agoSteal Gary Woodland’s subtle power move for longer drives

-

Tech7 days ago

Tech7 days agoBattery Tester Outperforms Cheaper Options

-

Business4 days ago

Business4 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion20 hours ago

Fashion20 hours agoLet’s Discuss: DEI in 2026

You must be logged in to post a comment Login