Business

Kaspi.kz ADR Jumps 7.88% as Strong Dividend Payout and Fintech Momentum Fuel Investor Optimism

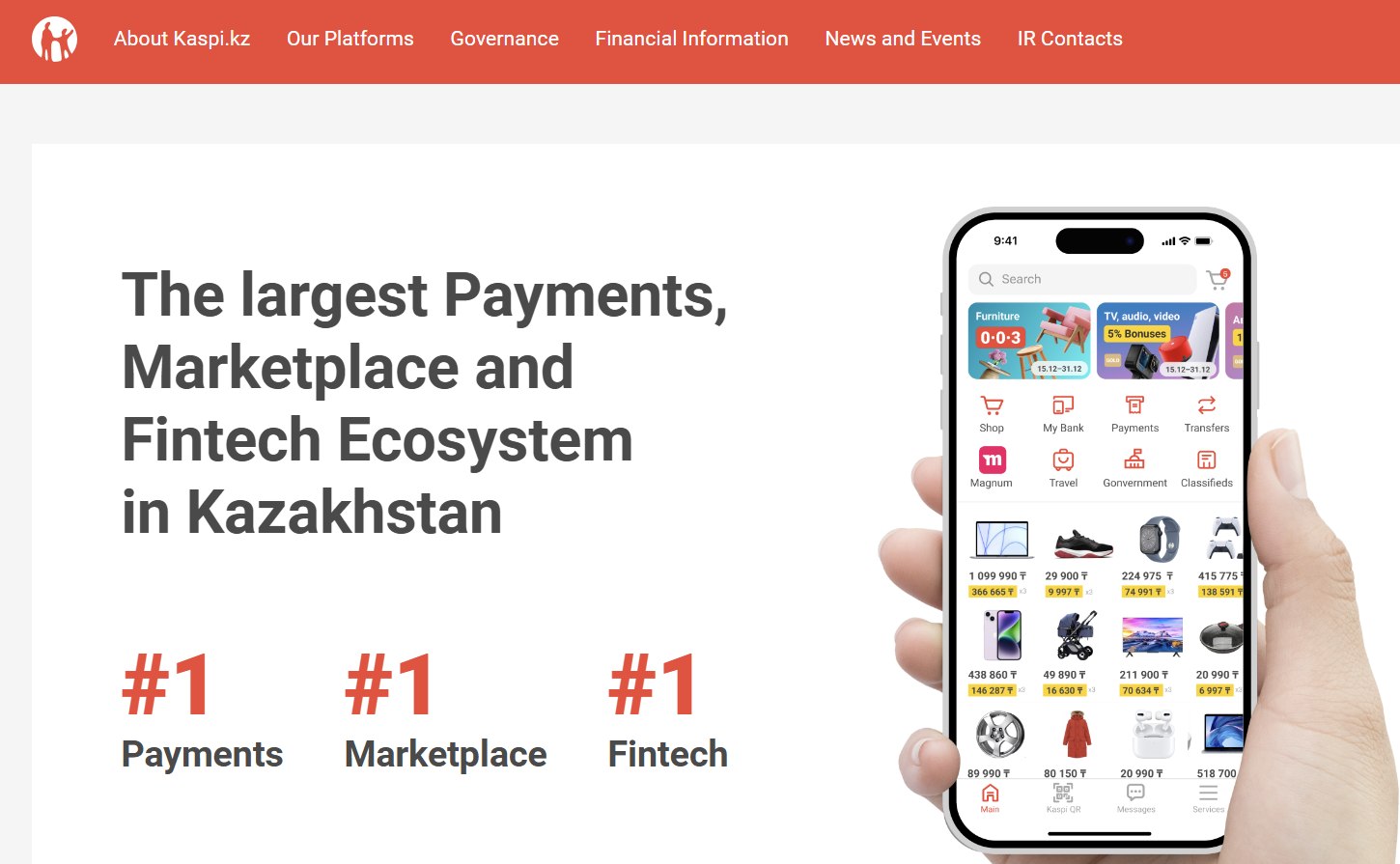

NEW YORK — Shares of Kaspi.kz JSC surged more than 7% in early Monday trading on April 20, 2026, rising $6.69 to $91.60 as investors cheered the Kazakh fintech giant’s recent approval of a substantial cash dividend and growing confidence in its super app ecosystem amid regional expansion.

The American Depositary Receipts of Kaspi.kz (NASDAQ: KSPI), which operates one of Central Asia’s most successful digital banking and e-commerce platforms, climbed on solid volume following last week’s annual general meeting where shareholders approved a KZT 850 per share dividend for 2025 results. The payout, which began on April 15, underscores the company’s commitment to returning capital while maintaining robust growth in payments, lending and marketplace services.

Kaspi.kz has transformed from a traditional bank into a dominant “super app” in Kazakhstan, serving more than 25 million consumers and nearly 900,000 merchants with integrated services ranging from mobile payments and installment loans to e-commerce and government services. The platform’s high user engagement has driven consistent revenue and profit expansion, making it one of the standout emerging market fintech stories since its Nasdaq listing in early 2024.

The latest dividend equates to a meaningful yield for ADR holders after currency conversion, reinforcing the stock’s appeal to income-focused investors. At the April 15 annual meeting in Almaty, shareholders also approved the 2025 audited financial statements and reappointed Deloitte as external auditor. The company set a record date of April 14 for common shares and April 16 for ADS holders, ensuring timely distribution of the cash dividend via wire transfers.

Analysts highlighted the payout as a positive signal of financial health and disciplined capital allocation. With Q1 2026 financial results scheduled for release on May 11, accompanied by a conference call and webcast at 8 a.m. ET, investors appear to be positioning ahead of what many expect will be another strong quarterly update showing continued loan growth, deposit inflows and marketplace transaction volume.

“Kaspi.kz continues to execute flawlessly in a challenging regional environment,” one emerging markets analyst noted. “The combination of a generous dividend, resilient core banking margins and successful diversification into e-commerce has supported premium valuations even as global fintech peers face headwinds.”

The company’s performance has benefited from Kazakhstan’s relatively stable macroeconomic backdrop compared to some neighboring markets, along with high smartphone penetration that has accelerated digital adoption. Kaspi’s super app model allows seamless switching between banking, shopping and utility payments within a single interface, creating strong network effects and customer stickiness.

Beyond its home market, Kaspi.kz has pursued strategic international moves, including a significant stake in Turkish e-commerce platform Hepsiburada. This exposure provides potential upside from Turkey’s larger consumer base while diversifying away from pure reliance on the Kazakh economy. Analysts have pointed to possible further expansion in Central Asia or adjacent regions as long-term growth drivers.

The stock’s 7.88% gain on Monday extended a solid year-to-date performance, though it has traded with volatility typical of emerging market names sensitive to commodity prices, currency fluctuations and geopolitical developments. Oil-rich Kazakhstan’s economy remains tied to energy exports, but Kaspi’s focus on consumer finance and digital services has provided a buffer against raw material cycles.

Short interest in the ADR had grown in recent months, creating potential for a squeeze as positive catalysts emerge. The dividend approval appears to have alleviated some concerns about capital returns, while the upcoming earnings will offer fresh insight into loan quality, asset growth and any updates on international initiatives.

Company leadership has emphasized technology investments and risk management as keys to sustained profitability. Kaspi maintains conservative underwriting standards in its lending business, which has helped keep non-performing loans low even during periods of economic uncertainty. Its payments segment benefits from low-cost digital infrastructure, supporting healthy net interest margins and fee income.

Wall Street coverage remains generally constructive, with consensus price targets clustering around $100, implying further upside from current levels. Some analysts maintain a “Hold” rating with targets near $87, while others see room for expansion if the company successfully scales its marketplace and cross-border ambitions. The wide range of forecasts — from the low $80s to above $140 in more bullish scenarios — reflects both enthusiasm for the business model and typical caution around emerging market risks.

Kaspi.kz faces competition from traditional banks and newer digital entrants, but its first-mover advantage and ecosystem lock-in have proven difficult to replicate. Regulatory oversight in Kazakhstan has been supportive of fintech innovation, though any tightening of consumer lending rules could pose a headwind. Currency risk, with the tenge’s movements against the dollar, also influences ADR performance for U.S. investors.

The broader context for Monday’s trading included mixed global markets, with energy prices rising on geopolitical developments in the Middle East. Kaspi’s resilience in such an environment highlights the defensive qualities of its diversified digital revenue streams.

Looking ahead, the May 11 earnings release will be closely watched for metrics on active users, transaction volumes, loan origination growth and any commentary on margin trends or expansion plans. Management is expected to address the integration of recent investments and the trajectory of its Turkish exposure through Hepsiburada.

For retail and institutional investors alike, Kaspi.kz represents a rare pure-play exposure to high-growth digital finance in Central Asia. The combination of strong dividends — projected by some observers to offer yields approaching 9% in certain scenarios — and organic business expansion has attracted long-term holders seeking both income and capital appreciation.

The ADR’s performance on April 20 reflected renewed buying interest after the dividend went ex and as traders anticipated positive momentum into the earnings period. While not every session will deliver double-digit percentage moves, the underlying fundamentals suggest continued investor interest in a company that has consistently delivered on its promises since going public.

As Kaspi.kz prepares its first-quarter update, the market appears to be pricing in sustained leadership in Kazakhstan’s fintech landscape and measured progress on international fronts. Whether the upcoming results confirm or exceed expectations will likely set the tone for the stock through the remainder of 2026.

With a market position that blends banking stability with tech-driven innovation, Kaspi.kz continues to stand out among global fintech names. Monday’s 7.88% advance served as a reminder of the company’s ability to reward shareholders through both operational excellence and attractive capital returns.

Check out what’s clicking on FoxBusiness.com.

Apple’s senior vice president of Hardware Engineering, John Ternus, is set to take over as the tech manufacturer’s CEO later this year after current chief executive Tim Cook announced on Monday that he would be stepping down.

Cook will transition to executive chairman of the company’s board of directors. The company said the transition followed a “thoughtful, long-term succession planning process” and was unanimously approved by the board of directors.

“It has been the greatest privilege of my life to be the CEO of Apple and to have been trusted to lead such an extraordinary company,” Cook said in a statement.

“I love Apple with all of my being, and I am so grateful to have had the opportunity to work with a team of such ingenious, innovative, creative, and deeply caring people who have been unwavering in their dedication to enriching the lives of our customers and creating the best products and services in the world,” he added.

APPLE CEO TIM COOK TO STEP DOWN IN MAJOR LEADERSHIP SHAKEUP, SUCCESSOR NAMED

John Ternus will become Apple CEO on September 1, 2026, as Tim Cook transitions to Apple Executive Chairman. (Reuters / Reuters)

The leadership shakeup marks the first change in the company’s chief executive in 15 years, when Cook replaced Apple co-founder Steve Jobs.

Ternus will take over as CEO on Sept. 1, leading the company into its next phase of innovation. He will also join the board of directors upon assuming the role.

“I am profoundly grateful for this opportunity to carry Apple’s mission forward,” Ternus said in a statement. “Having spent almost my entire career at Apple, I have been lucky to have worked under Steve Jobs and to have had Tim Cook as my mentor. It has been a privilege to help shape the products and experiences that have changed so much of how we interact with the world and with one another.”

He joined Apple’s product design team in 2001 and became vice president of Hardware Engineering in 2013. Eight years later, he joined the executive team as senior vice president of Hardware Engineering, where he has overseen work on many of the company’s flagship products across iPhone, Mac, iPad, AirPods and Apple Watch.

Ternus also recently led the team behind the new MacBook Neo and the redesigned iPhone 17 lineup. Apple credits his leadership with driving advancements in AirPods, including active noise cancellation and capabilities that enable them to function as an all-in-one hearing health system, including over-the-counter hearing aid features.

Additionally, he has led efforts focused on durability, materials innovation, and sustainability, including the use of recycled aluminum and new manufacturing techniques. Ternus has also played a key role in Apple’s transition to in-house silicon.

John Ternus will take over as CEO of Apple on Sept. 1 (Adam Gray/Bloomberg via Getty Images / Getty Images)

“I am filled with optimism about what we can achieve in the years to come, and I am so happy to know that the most talented people on earth are here at Apple, determined to be part of something bigger than any one of us,” he said. “I am humbled to step into this role, and I promise to lead with the values and vision that have come to define this special place for half a century.”

Before joining Apple, Ternus worked as a mechanical engineer at Virtual Research Systems. He graduated with a bachelor’s degree in Mechanical Engineering from the University of Pennsylvania.

Cook praised Ternus as having “the mind of an engineer, the soul of an innovator, and the heart to lead with integrity and with honor.”

“He is a visionary whose contributions to Apple over 25 years are already too numerous to count, and he is without question the right person to lead Apple into the future,” Cook said. “I could not be more confident in his abilities and his character, and I look forward to working closely with him on this transition and in my new role as executive chairman.”

Apple shares dipped slightly—less than 1%— in after-hours trading following the news of the leadership shakeup, which some analysts said was not surprising.

“This transition shouldn’t come as a shock, as Cook is at retirement age and Ternus has long been rumored as the successor,” Jacob Bourne, a technology analyst at EMARKETER, told Reuters. “Cook staying on as CEO through September before continuing as executive chairman should provide some degree of reassurance to investors even as markets react negatively to the near-term uncertainty.”

LEADERSHIP CHANGE AT APPLE SPARKS INDUSTRY AND WALL STREET REACTIONS AS COOK TRANSITIONS ROLES

Tim Cook said it “has been the greatest privilege of my life to be the CEO of Apple.” (David Paul Morris/Bloomberg via Getty Images / Getty Images)

GET FOX BUSINESS ON THE GO BY CLICKING HERE

Rick Meckler, a partner at Cherry Lane Investments, told the outlet he is “not surprised that the initial reaction is for the stock to be a little bit lower.”

B. Riley Wealth chief market strategist Art Hogan also said Cook “would never leave if the numbers were going to be bad, so I think that that’s the important thing.”

“They’re about to report numbers, and you know they’re going to be good,” he added. “You know the guidance is going to be positive. And you know we’re going to start hearing more about how they are going to use artificial intelligence to improve their products.”

Ternus will take over Apple at a time when it faces antitrust scrutiny around the world. This includes a landmark case brought by the U.S. Department of Justice and more than a dozen states, alleging that Apple has maintained an illegal monopoly by using its control over the iPhone to stifle competition. European and Asian governments have also sought to penalize Apple for allegedly exploiting its dominant position in the industry.

ICICI Bank gained 0.7% to close at ₹1,356.2, while HDFC Bank fell 0.6% to ₹795.45. The Nifty 50 ended little changed at 24,364.85.

near-term investor views diverge But most analysts say shares of the private banking leaders are poised to make further gains

Analysts remain positive on both. Bloomberg consensus implies an average upside of about 33% for HDFC Bank and 24% for ICICI Bank.

HDFC Bank’s 12-month average target price was trimmed to ₹1,056.3 from ₹1,100.72, even as HSBC, JP Morgan and Nomura raised their estimates post-results, while Citi lowered its target but retained a ‘Buy’. ICICI Bank’s average target edged up to ₹1,680.02.

All analysts covering HDFC Bank have a ‘Buy’ rating, while 96% of those on ICICI Bank recommend the stock, according to Bloomberg data.

Tariff refund system launches as thousands of companies file claims

In the NSE list of stocks with a market cap over Rs 10,000 crore, eight stocks’ close prices crossed above their 200 DMA (Daily Moving Averages) on April 20, according to stockedge.com’s technical scan data. The 200-day daily moving average (DMA) is used as a key indicator by traders for determining the overall trend in a particular stock. As long as the stock is priced above the 200-day SMA on the daily time frame, it is generally considered to be an overall uptrend. Take a look:

Business

Middle East Turmoil Drives Prolonged Natural Gas Surge, Keeping Electricity Costs High for 2+ Years

The Middle East conflict has sharply increased LNG prices by disrupting supply, especially from Qatar, driving up global and Thai electricity costs. Thailand should adopt flexible tariffs, boost clean energy, and improve efficiency.

Impact of Middle East Conflict on LNG Prices

The Middle East conflict has caused liquefied natural gas (LNG) prices to surge by over 91%, rising from USD 10.7 to USD 20.5 per million BTU between February and April. This spike was triggered by supply disruptions, particularly damage to Qatar’s Ras Laffan gas field, which accounts for 17% of its capacity, reducing global LNG supply by 3%. Recovery of this supply is expected to take 3–5 years. Persistent disruptions and high demand in Asia and Europe will keep LNG prices elevated, though increased U.S. production and alternative energy adoption should help balance supply and demand after two years.

Rising Electricity Costs and Tariff Implications

Thailand faces higher electricity generation costs due to increased LNG prices and supply disruptions. Imported natural gas costs push electricity prices up to around THB 4.9 per unit by the end of 2026. However, maintaining EGAT’s debt at THB 36 billion could moderate tariff rises to approximately THB 4.0 per unit in 2026–2027. Prolonged conflict or further damage could drive LNG prices to USD 36.1 per million BTU and tariffs near THB 5.7 per unit. Flexible tariff adjustments and energy management will be crucial to controlling costs.

Recommendations for Government and Consumers

The government should implement both short- and long-term strategies to manage electricity costs, including gradually adjusting tariffs, increasing energy imports, enhancing renewable energy capacity, and exploring small modular nuclear reactors. Public communication about energy costs is essential. Households and businesses must improve electricity efficiency by using energy-saving devices, avoiding peak usage, and investing in rooftop solar systems. These efforts will help reduce dependence on LNG and strengthen Thailand’s energy security sustainably.

Other People are Reading

Chinese President Xi Jinping has made a rare comment about the Strait of Hormuz.

Xi emphasized the need to open the Strait of Hormuz, explaining that this will be the most beneficial decision for all.

Xi Jinping Comments on Strait of Hormuz

According to 9News, the state news agency of China reported that Xi has spoken to Saudi Crown Prince Mohammad Bin Salman.

“The Strait of Hormuz should remain open to normal passage, as this serves the common interests of regional countries and the international community,” Xi reportedly said.

Xi also stressed that China supported all peace efforts. He likewise said that the conflict between the US and Iran must be resolved through dialogue.

JD Vance to Head Delegation Should Iran Agree to Talks

While Iran has remained firm thus far that it is no longer open to any peace talks, US Vice President JD Vance will still fly to Pakistan to lead the US diplomatic delegation.

Alongside Vance, Donald Trump’s special envoy Steve Witkoff and Jared Kushner will also be part of the delegation, according to The Guardian. Kushner is Trump’s son-in-law.

Should Iran agree to peace talks, its delegation will reportedly be once again headed by parliamentary speaker Mohammad Bagher Ghalibaf.

Ghalibaf had accused Trump of turning this negotiating table – in his own imagination – into a table of surrender or to justify renewed warmongering.”

South Korea’s Lee says claim that minister leaked classified intel is ’absurd’

ValuEngine.com (VE) is a stock valuation and forecasting service founded by Ivy League finance academics. VE utilizes the most advanced quantitative techniques and analysis available.

Our research team continues to develop, test, and improve the VE Stock Recommendation, Valuation and Forecast Models related to stock price movement. This research is updated daily and applied to more than 4,200 US Stocks, 600 plus US ETFs, over 1,000 Canadian stocks, and all sector and industry groups.

Business

ETMarkets Smart Talk | Financials, industrials, healthcare top picks for FY27: Nimesh Chandan

In this environment, Nimesh Chandan, Chief Investment Officer, Bajaj Finserv Asset Management Limited believes that while short-term headwinds may weigh on earnings and sentiment, the broader structural story of the Indian economy remains firmly intact.

In an interaction with Kshitij Anand of ETMarkets, Chandan highlights that current market corrections have brought valuations closer to fair levels, creating opportunities for long-term investors willing to look beyond near-term noise.

He identifies Financials, Industrials, and Healthcare as key sectors poised to benefit from India’s ongoing economic and credit cycle upturn, supported by improving earnings visibility and reasonable valuations.

He also advises investors to stay disciplined—either deploying lump sum capital if they can absorb volatility or adopting a staggered approach via SIPs or STPs—while maintaining a minimum three-year investment horizon. Edited Excerpts –

Q) Thanks for taking the time out. We have entered FY27 on a volatile note amid geopolitical concerns, rising oil prices, possibility of rise in interest rates etc. Where do you see markets headed?

A) Unfortunately, we seem to have hit a speed bump in an otherwise strong growth year. Due to the geopolitical concerns and rising oil prices, there is a possibility that there could be some slowdown in economic growth and profit growth in the first half.

A small cut in earnings cannot be ruled out if this crisis continues for a bit longer. If this war in West Asia resolves quickly, as is widely expected right now with the ceasefire, there is a possibility that there is no significant earnings cut for FY27.

Our base remains that Indian economy, business cycle and the credit cycle are on an upturn. We have a positive stance on the earnings growth for FY27 and FY28. We are currently trading below intrinsic value for the Nifty 50 Index.

Q) What should investors do who are planning to put fresh money say Rs 10 lakh in markets? What should be the sectoral allocation?

A) Investors who can handle near-term volatility can put a lumpsum amount right now. Valuations are fair, but because of the geopolitical crisis, there could be near-term volatility. Other investors may stagger their investment through STP (Systematic Transfer Plan) or SIP (Systematic Investment Plan) as a route.

However, they should have at least three-year view when they are investing in the equity markets. From a sectoral perspective, we like Financials, Materials, Industrials, Healthcare and Consumer Discretionary. We believe large private banks as a category are available at good valuations.

We have been positive on pharma, specifically CRAMS (Contract Research & Manufacturing Services) and hospitals. We are equal-weighted on consumer discretionary as we are positive on long term prospects of the sector.

However, we are selective in this sector, evaluating companies on the potential impact of high energy and material prices on them. Within Industrials, we prefer Defence and Power.

Q) FIIs have remained net sellers in Indian equity markets withdrawing Rs 1.6 lakh cr. What will reverse the flows?

A) The India–US trade agreement earlier helped stem the FPI outflows that India had been witnessing over the past year. However, the recent escalation in geopolitical tensions in the Middle East has triggered a renewed phase of outflows.

Given India’s heavy dependence on imported crude oil, rising oil price uncertainties tend to weigh on investor sentiment in the near term.

That said, we view this as a transitory phase. As the geopolitical situation stabilizes and recovery gains traction, India’s relative valuation attractiveness compared to other emerging markets should support a revival in FPI inflows.

The key variables to monitor remain the evolution of the West Asia crisis and a moderation in crude oil prices.

Q) How do you see the currency moving in the next few months?

A) The INR has seen a sharp correction, first due to tariffs, FPI outflows and now crude spike and higher gold prices. We are the world’s largest importers of gold and most of our crude requirements are imported. These exert a lot of pressure on the INR.

If the geopolitical crisis abates and the crude cools off, we believe the pressure on the INR could ease at these levels. Falling INR is also an opportunity. A contrarian view we hold is that, this depreciation of currency will create huge export opportunity for Indian manufacturing sector.

Q) You have seen many market cycles and I am sure this one is no different. Things which one should avoid doing at current juncture?

A) Clearly, investors should avoid getting fearful in these equity markets. We did a very simple analysis at Bajaj Finserv AMC. We observed that the markets correct every time crude prices have crossed $100 per barrel.

The investors who have used that correction to invest have made healthy returns in almost all cases over the next three to five years.

Hence, the only thing the investors should not do right now is panic, be fearful, or be very myopic. This is a good opportunity from an equity investor’s perspective because of the corrections in valuation. Investors should focus on fundamentals, be patient, and stick to their asset allocation plan.

Q) How do you see Gold and Silver moving in FY27?

A) Gold and silver have already witnessed a strong rally, and from here, returns are likely to be more measured rather than sharply bullish. These assets should be viewed primarily as portfolio hedges rather than return-chasing opportunities.

Gold is expected to continue playing its role as a key diversifier, especially amid ongoing global uncertainties.

Silver, on the other hand, may remain relatively more volatile due to its higher linkage to global growth and industrial demand.

At this stage, investors should avoid chasing the rally in precious metals and instead use them strategically within portfolios for diversification rather than for aggressive return expectations.

Q) After the recent correction, do you see Indian markets trading at reasonable valuations vs developed or emerging markets?

A) From 2021 till Sept 2024, Indian markets outperformed other emerging markets by 70-80%. Since then, Indian has underperformed by more than 40%. This has brought valuations closer to fair value at an aggregate level.

Growth is recovering, interest rates are lower and hence in many pockets of the market, valuations are attractive.

From a global perspective, India continues to command a premium over both developed and emerging markets. This premium reflects strong growth visibility and better capital efficiency of corporate India.

Q) Which sectors are likely to hog the limelight in FY27 after the recent fall?

A) In the current environment, investors should avoid crowded trades and instead focus on sectors offering earnings visibility alongside reasonable valuations. Domestic cyclicals such as capital goods, manufacturing, and infrastructure are well-positioned to benefit from India’s ongoing capex cycle.

Financials, including banks and select NBFCs, should continue to see steady support from credit growth and overall economic momentum.

Within consumption, opportunities exist but are selective in nature, with a preference for segments where demand visibility remains strong. Information Technology may hog the limelight but due to worries on the US economy and developments in AI.

(Disclaimer: Recommendations, suggestions, views, and opinions given by experts are their own. These do not represent the views of the Economic Times)

Hello. I am a graduate from Bocconi University with a degree in Economics and a concentration in Quantitative Economics. I am currently working at a management consultancy, with aspirations of working as an investment analyst.I primarily invest in growth stocks, with a focus on highly innovative sectors, particularly tech and energy. My portfolio consists of mainly high-conviction growth plays – ranging from large-cap tech to speculative early-stage ventures. I aim to provide sound, quantitative analysis through deep fundamental insights on target companies within the context of the sector they operate in & broader macro conditions.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ALM either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

World Snooker Championship: Jones targets title at the Crucible

Philips Baristina Milk Frother review: perfectly frothed milk every time, including non-dairy alternatives.

Doctor Amir Khan urges Brits to do 1 thing before bed to aid sleep each night

-

NewsBeat7 days ago

NewsBeat7 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Theodora Dress

-

News Videos6 days ago

News Videos6 days agoSecure crypto trading starts with an FIU-registered

-

Sports4 days ago

Sports4 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World7 days ago

Crypto World7 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business2 days ago

Business2 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Crypto World3 days ago

Crypto World3 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics8 hours ago

Politics8 hours agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Politics3 days ago

Politics3 days agoPalestine barred from entering Canada for FIFA Congress

-

Business4 days ago

Business4 days agoCreo Medical agree sale of its manufacturing operation

-

Politics2 days ago

Politics2 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Crypto World3 days ago

Crypto World3 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Tech2 days ago

Tech2 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Tech5 days ago

Tech5 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

-

Tech6 days ago

Tech6 days agoMicrosoft adds Windows protections for malicious Remote Desktop files

-

Crypto World6 days ago

Crypto World6 days agoX Launches New Cashtag Feature for Stocks and Crypto: X

-

Sports7 days ago

Sports7 days agoYounger Than Sachin Tendulkar: Vaibhav Sooryavanshi Set To Make Historic India Debut

-

Entertainment6 days ago

Entertainment6 days agoPrince Carter Brings Fans Front Row and Backstage at Boys 4 Life Tour

-

Entertainment6 days ago

Entertainment6 days agoDave Portnoy Slams Dianna Russini: ‘Makes Zero Sense’

-

Sports5 days ago

Sports5 days agoBritish climbers complete new route in Swiss Alps

You must be logged in to post a comment Login