Crypto World

Is a hidden hedge fund blowup behind bitcoin’s crash to $60,000?

Bitcoin’s plunge to nearly $60,000 on Thursday, a nearly 30% drop over 7 days, has got traders on X began floating theories that the selloff was not purely macro or risk-off, but various reasons that contributed to the asset’s worst single-day performance since FTX crashed in 2022.

Flood, a prominent crypto trader, called it in an X post the most vicious selling he’s seen in years and said it felt “forced” and “indiscriminate,” floating possibilities ranging from a sovereign dumping billions to an exchange balance sheet blowup.

Few theories: – Secret Sovereign dumping $10B+ (Saudi/UAE/Russia/China) – Exchange blowup, or Exchange that had tens of billions of dollars of Bitcoin on the balance sheet forced to sell for whatever reason.

Pantera Capital general partner Franklin Bi offered a more detailed theory. He suggested the seller could be a large Asia-based player with limited crypto-native counterparties, meaning the market would not “sniff them out” quickly.

My guess is that it’s not a crypto-focused trading firm but someone large outside of crypto, likely based in Asia, with very few crypto-native counterparties. hence why no one has sniffed them out on CT. comfortably leveraged & market-making on Binance –> JPY carry trade unwind –> 10/10 liquidity crisis –> ~90-day reprieve granted –> backfired attempt to recover on gold/silver trade –> desperate unwind this week.

In his view, the chain of events may have started with leverage on Binance, then worsened as carry trades unwound and liquidity evaporated, with a failed attempt to recover losses in gold and silver accelerating the forced unwind this week.

But the more unusual narrative emerging from the crash is not about leverage. It is about security.

Charles Edwards of Capriole argued that falling prices may finally force serious attention on bitcoin’s quantum security risks.

Edwards said he was “serious” when he warned last year that bitcoin might need to go lower to incentivize meaningful action, calling recent developments the first “promising progress” he has seen so far.

$50K not that far away now. I was serious when I said last year that price would need to go lower to incentivize proper attention to Bitcoin quantum security. This is the first promising progress we have seen to date. I genuinely hope Saylor is serious about establishing a well funded Bitcoin Security team.

He would have significant sway across the network in affecting change. I am concerned that his statement today is a false flag, to simply diminish mounting quantum fear without substantive action, but I would love for this to be wrong. We have a lot of work to do, and it needs to be done in 2026.

Parker White, COO and CIO at DeFi Development Corp., pointed to unusual activity in BlackRock’s spot bitcoin ETF (IBIT) as a possible culprit behind Thursday’s washout.

He noted IBIT posted its biggest-ever volume day at $10.7 billion, alongside a record $900 million in options premium, arguing the pattern fits a large options-driven liquidation rather than a typical crypto-native leverage unwind.

The last small piece of evidence I have is that I personally know a number of HK-based hedge funds that are holders of $DFDV, which had the worst single down day ever, with a meaningful mNAV decline. The mNAV had been holding steady surprisingly well throughout this pull back until today. One of these fund(s) could have been connected to the IBIT culprit, as I highly doubt a fund taking that large of a position in IBIT and using a single entity structure would only have the one fund.

Now, I could easily see how the fund(s) could have been running a levered options trade on IBIT (think way OTM calls = ultra high gamma) with borrowed capital in JPY. Oct 10th could very well have blown a hole in their balance sheet, that they tried to win back by adding leverage waiting for the “obvious” rebound. As that led to increased losses, coupled with increased funding costs in JPY, I could see how the fund(s) would have gotten more desperate and hopped on the Silver trade. When that blew up, things got dire and this last push in BTC finished them off.

“I have no hard evidence here, just some hunches and bread crumbs, but it does seem very plausible,” White wrote on X.

Bitcoin’s drop over the past week has been less about a slow grind lower and more about sudden air pockets, with sharp intraday swings replacing the orderly dip-buying seen earlier this year.

The move has dragged BTC back toward levels last traded in late 2024, while liquidity has looked thin across major venues. With altcoins under heavier pressure and sentiment collapsing to post-FTX style readings, traders are now treating each rebound as suspect until flows and positioning visibly reset.

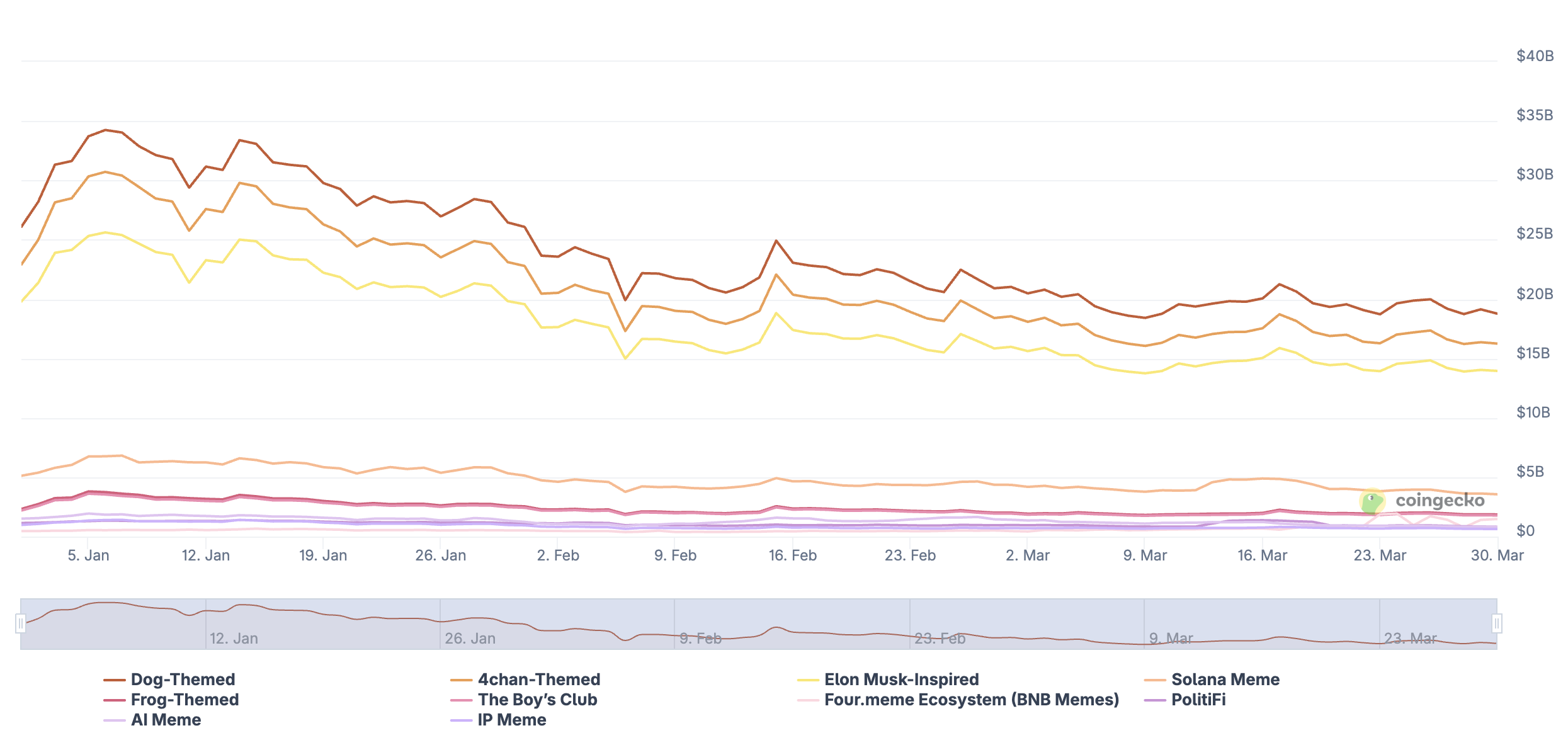

The total meme coin market capitalization has slipped to roughly $36 billion, with every major subsector posting year-to-date losses except one. Four converging signals suggest a recovery remains distant.

The first signal is the breadth of the decline. CoinGecko data paints a grim picture across meme coin categories.

Follow us on X to get the latest news as it happens

AI Meme tokens have been hit hardest, falling 46% year to date. Dog-themed, 4chan-themed, and Elon Musk-inspired tokens all dropped roughly 28% to 30% in lockstep.

The Boy’s Club and Frog-themed categories held up relatively better, each declining around 19% to 20%. The sole outlier is the Four.meme Ecosystem on BNB Chain, which has more than tripled since January.

The second signal is fading dominance. CryptoQuant data shows meme coin dominance within the altcoin market fell from 0.042 in mid-February to 0.034 in March. This suggests that capital is rotating away from meme tokens.

The third signal is collapsing participation. Solana, which served as the primary hub for memecoin speculation, has seen on-chain engagement collapse. Analyst Shah noted that the number of daily decentralized exchange (DEX) traders on Solana has hit their lowest levels on record.

“Participation is at all time lows, just a few thousand people are still active, so good coins that once had 100M–1B potential are stuck trading between 500k- 20M,” he wrote.

Analyst Capexbt described the chain as a “ghost town.”

The fourth signal is the macro backdrop. Escalating geopolitical tensions, particularly the US-Iran conflict, have kept the Crypto Fear and Greed Index in extreme fear territory.

Without fresh liquidity and renewed risk appetite, conditions for a meme coin rally remain absent.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post 4 Reasons Why Meme Coin Season Won’t Return Anytime Soon appeared first on BeInCrypto.

The GENIUS Act may have closed the door on interest-bearing payment stablecoins, but it has not ended the search for yield. It has simply pushed that search into new structures, where the return comes through DeFi design rather than through the stablecoin itself.

BeInCrypto asked two industry experts how the market is adapting.

Stefan Muehlbauer, Head of U.S. Government Affairs at CertiK, says the issue remains politically contested. He says”

“The question of yield is still facing strong opposition from banks, beyond the GENIUS Act, but also leading to discussions during the recent roadblock of the Senate’s version of the CLARITY Act market structure bill.”

In his view, the line now sits between products that resemble interest and products that present rewards differently.

“Banks are taking aim at yield that is earned as interest, while DeFi players are innovating around products that treat rewards more as a service fee through mechanisms such as staking,” Muehlbauer continues.

Anton Efimenko, co-founder at 8Blocks, sees the same divide. He notes:

“Under U.S. law, stablecoin issuers can’t issue stablecoins with passive yield accrual. Rebasing is basically banned. At the same time, “there’s nothing stopping those stablecoins from being used in DeFi products that generate yield through staking.”

He adds that the opportunity may extend even further. “If you think the structure through properly, a stablecoin issuer can also launch its own DeFi platform and distribute deposit yield through that layer.”

That leaves the U.S. stablecoin market in an unusual place. Yield remains one of the strongest product incentives in crypto, but in 2026, it has to be packaged with much more care.

Federal Charters Change the Balance of Power

Federal charters are where the balance of power changes most visibly. Crypto-native firms are already entering the U.S. financial system, and the focus now is how directly they can compete with the institutions that have controlled access to payments and settlement for decades.

Muehlbauer argues that this is where the biggest realignment is happening:

“The granting of national trust bank charters to crypto-native firms like Circle and Paxos has effectively dismantled the ‘walled garden’ that once protected legacy giants like JPMorgan Chase from outside tech competition.”

In his view, these licenses change who can operate with institutional standing inside the system. By securing federal charters, he says, digital asset issuers gain “the official federal imprimatur needed to compete directly for core payment and settlement services.” That gives them a path to “operational autonomy” rather than continued dependence on banking partners.

Fernando Lillo Aranda, Marketing Director at Zoomex, says the key change is that crypto-native firms no longer need to rely entirely on incumbent banks for legitimacy.

Aranda notes:

“Once a non-bank issuer can operate under a federal framework or an OCC-supervised charter, it is no longer just a technology company renting access to the banking system.”

In his view, that gives firms like Circle or Paxos clearer standing across payments, custody, and reserve management, turning them into directly regulated financial institutions rather than outside partners looking in.

At the same time, Lillo Aranda does not see this as a sudden reversal of bank dominance:

“That does not suddenly make JPMorgan weak – incumbents still dominate distribution, balance sheet depth, and client trust.”

But, he argues that the competitive gap has narrowed.

Where banks once held the regulatory advantage and crypto firms mainly moved faster on product design, some crypto-native issuers now have both. That shifts the contest away from basic market access and toward who can scale trust, distribution, and integration fastest.

Efimenko agrees that the market is opening up, but he does not think legacy finance has lost its edge.

“The U.S. stablecoin market is going to be highly competitive, but banks and asset managers will still hold the advantage,” he says. For him, the decisive factor is distribution.

“Crypto companies have to spend heavily on marketing to attract investors, while banks already have those investors on hand.”

Federal charters give crypto-native issuers more room to operate on their own terms, but banks still control the customer relationships that turn financial products into mass-market products.

Federal rules rise, but the states are still in the room

The GENIUS Act may have established a federal path for stablecoins, but it has not erased the state systems that helped define earlier phases of U.S. crypto regulation. What it has done is place them in a more constrained position.

Muehlbauer says the era of states acting as independent “laboratories of innovation” is largely over. In his view, the market is entering a period of “cooperative federalism” in which Washington sets the main rules for stablecoin oversight.

“Although the Wyoming Model and New York’s BitLicense endure, they are no longer autonomous,” Muehlbauer says. He argues that they now function within a federal framework that sets the minimum standards for capital and reserves.

He also points to a hard limit on how far a state-led route can go:

“Even successful state-chartered stablecoin issuers face a definitive ceiling. Once volume hits $10 billion, they must transition to primary federal oversight by the OCC.”

That leaves states with a role, but not the leading role they once claimed in crypto policy. They still influence licensing, supervision, and regional experimentation, though the center of gravity now sits in Washington.

CLARITY still has to solve the token question

Stablecoins may now have a federal framework, but the larger question of token classification remains unsettled. That is where the CLARITY Act comes into play.

Muehlbauer says the bill is designed to address what he calls the “security-forever” dilemma by updating how U.S. law treats tokens across their life cycle. He says:

“The Act isolates the ‘investment contract’ status by introducing ‘Ancillary Assets’, tokens whose value relies on the ‘entrepreneurial or managerial efforts’ of a central group, but only during their initial, centralized phase.”

In his telling, the bill creates a path for tokens to leave that category once a network develops beyond heavy reliance on a core team. Muehlbauer says:

“To provide a legal exit ramp, the Act establishes a ‘Maturity’ test, allowing tokens to graduate to Digital Commodities once the network becomes sufficiently decentralized.”

He says that originators would be able to certify that managerial efforts have become “nominal,” opening a 60-day window for the SEC to challenge that claim or allow the asset to proceed with a presumption of non-security status in secondary trading.

If that framework survives negotiations, it could bring the U.S. closer to a usable definition for utility tokens. Until then, stablecoins may have moved into a clearer legal era, while much of the rest of crypto still waits for its answer.

Final thoughts

The GENIUS Act has given the U.S. its clearest stablecoin framework yet, but it has also opened a new phase of competition. The debate now reaches beyond regulation itself and into who controls issuance, who captures the economics around digital dollars, and who gets direct access to the financial system.

Muehlbauer’s answers suggest that Washington has moved stablecoins into a more formal federal order, while leaving the next major fight unresolved around token classification and market structure.

Efimenko, meanwhile, points to the commercial reality behind that legal progress. Even with new charter opportunities and room for product innovation, crypto-native firms still have to compete with banks that already control distribution and client access.

Lillo Aranda sharpens that point: federal charters may have narrowed the old moat around legacy finance, but they have not erased the incumbents’ advantage in scale, trust, and customer ownership.

Stablecoins are entering a more defined legal era, but the balance of power between crypto firms, banks, regulators, and token issuers is still being contested in real time.

The post The American Pivot and Wall Street 2.0 appeared first on BeInCrypto.

Ethereum’s Ether (ETH) could slip toward the $1,200 region in the coming weeks, as a fractal-driven setup highlighted by trader Leshka.eth points to a potential deeper pullback if key support gives way. The analyst emphasizes a daily Supertrend pattern that has preceded outsized declines when bearish flips have failed to hold.

Historically, the pattern produced notable reversals: bullish flips that failed to sustain gains in October 2025 and January 2026 culminated in sharp drops of roughly 45% and 48%, respectively. The current formation forms near $1,990, and the trader warned that a break below that level could open the path toward the $1,200 zone. As Leshka.eth put it: “If that level breaks, the next target is the $1,200 zone.”

The narrative sits alongside a broader chart look that ties the bearish setup to a measured downside target from a bear-flag pattern on ETH’s daily chart, signaling a test of lower levels if momentum remains negative. The Ethereum price context has shifted as the market contends with a softer macro backdrop and a tug-of-war between risk appetite and liquidity considerations.

On the price action front, ETH has erased more than 17% from its monthly high in a little over two weeks. The pullback comes as Ether futures and spot sentiment loosen, with Ether ETFs reportedly registering net outflows of about $300 million in that span. Market observers describe the demand for Ethereum as having cooled to one of its weakest levels in 16 months, adding to the headwinds for a near-term recovery.

In the broader market backdrop, macro forces are not supportive of an immediate rebound. Risk appetite has waned amid geopolitical headwinds and recession concerns, while bond traders have pushed back expectations for Federal Reserve rate cuts beyond December 2027, according to probabilities tracked by CME’s FedWatch tool. The combination of softer macro signals and cleaner liquidity dynamics has kept ETH in a fragile zone even as short-term liquidity remains plentiful in some pockets of the market.

Key takeaways

- Bearish fractal setup on ETH’s daily chart points to a possible drop to $1,200 if the near-term level around $1,990 is breached, reaffirming a risk of deeper downside rather than a quick bounce.

- Historical occurrences where similar bullish flips failed have preceded sharp declines of roughly 45% to 50%, underscoring the difficulty of a sustained reversal in this pattern.

- On-chain demand signals show weak conviction among large and mid-size holders, with mega-whales (>10,000 ETH) flattening and mid-tier cohorts not reaccumulating decisively, suggesting limited downside protection from holders at present.

- The macro environment and ETF flows temper near-term momentum, with outflows and recession concerns weighing on Ethereum’s immediate prospects even as staking activity and exchange-supply dynamics offer a more complex longer-term picture.

Bearish fractal signals and price structure

The proposed bearish path hinges on a Supertrend-based pattern observed on ETH’s daily chart. The Supertrend, a trend-following indicator that changes color to mark direction, has previously produced brief bullish flips that did not stick. In the two notable prior instances—October 2025 and January 2026—the price rose briefly above the upper band only to fail and slide aggressively once the band’s support failed to hold. The current setup centers near $1,990, with the implication that a break below that crumb could activate the next leg lower toward the $1,200 zone. This aligns with a broader bear-flag interpretation that yields a measured downside target consistent with a sharper decline if support fails.

Trading-view charts referenced by the analyst illustrate a pattern where the price dropped decisively after the upper-band break and the subsequent loss of support, reinforcing the risk of a renewed downtrend if the current formation cannot sustain upward momentum. While such fractals do not guarantee outcomes, they provide a framework for assessing risk in a market dominated by macro uncertainty and shifting liquidity conditions.

On-chain behavior and holder conviction

Beyond price patterns, on-chain metrics paint a mixed picture of ETH demand. Glassnode data show that accumulation signals remain tepid across major wallet cohorts. For instance, mega-whale addresses holding more than 10,000 ETH have flattened after peaking in late 2025, and the 30-day change across this cohort has moved back toward neutral after extended declines. That pattern suggests that the biggest holders have not been stepping in with renewed aggression to back a sustained rally.

The story is similar for smaller but meaningful cohorts. Ethereum wallets holding between 1,000 and 10,000 ETH remain well below their late-2025 highs, with the 30-day change hovering around flat to marginally negative levels. Likewise, addresses in the 100–1,000 ETH bracket continue to trend below last year’s peaks, indicating a broad lack of renewed buying conviction among mid-sized to mid-tier holders. Taken together, the on-chain picture points to distribution pressures rather than broad-based accumulation, reinforcing the risk of a continued slide if the $1,990 zone gives way.

Despite the overall cautious stance from holders, there are some glimmers of potential longer-term support. Market observers note that on-chain activity around Ether staking has been rising, while the amount of Ethereum available on exchanges has fallen to ten-year lows. This combination signals that some holders are choosing to stake rather than liquidate, a dynamic that could eventually bolster Ethereum’s supply-side stability and reduce immediate selling pressure if demand improves. Still, these factors have not yet outweighed the current headwinds reflected in price action and investor sentiment.

For readers tracking the narrative, the balance of signals suggests that the immediate trajectory will hinge on whether ETH can defend the $1,990 threshold. A break lower would align with the fractal-driven downside scenario and the bear-flag target discussed by analysts, potentially amplifying the downside risks in the near term.

What to watch next

Investors should monitor a few key developments in the days ahead. First, whether ETH can sustain a move back above $1,990 or whether sellers regain control and push the price toward the $1,200 zone. Second, on-chain data—especially the behavior of mega-whales and the flow of Ether into staking pools—will be crucial for gauging whether demand may crystallize later in the year. Finally, macro momentum, including Fed expectations and risk appetite in relation to geopolitical developments, will continue to shape ETH’s risk premium and potential recovery path.

The market’s path remains uncertain, but the combination of a fragile macro backdrop, cooling on-chain demand, and fragile price patterns suggests a cautious stance for ETH in the near term as traders weigh the potential for further downside against the lure of long-term staking and shrinking exchange supply.

Crypto World

Ethereum Price Prediction: Prediction Market Bettors Think ETH Will Slide From Second Biggest Crypto

Ethereum price is trading at $2,052, with its second-place ranking now genuinely in question in a fast-moving prediction market. Prediction market data assigns a 59% probability that ETH loses its number-two spot by 2026, a dramatic surge from just 17% earlier this year.

The pressure is coming from an unlikely direction: stablecoins. Tether’s market cap has reached approximately $184 billion, narrowing the gap with Ethereum’s $243 billion valuation to a margin that once seemed untouchable.

The broader stablecoin sector now tops $310 billion, up from roughly $5 billion in 2020, driven by surging demand for liquidity, payments, and cross-border settlement rather than price speculation. Prediction markets have been under scrutiny lately, but these odds are hard to dismiss.

Unlike Ethereum, USDT doesn’t need a bull market to grow. That asymmetry is what makes this threat structurally different from past competitive cycles.

Discover: The best pre-launch token sales

Ethereum Price Must Hold Above $2,000 or Prediction Market Odds Can Come Into Fruition

ETH is currently trading at $2,052, clinging to a psychologically significant level after a brutal drawdown. The asset peaked near $4,900 in October 2025 before collapsing to under $2,000 last week, a decline exceeding 50%. The recovery since then has been tentative at best.

$2,000 is now the line in the sand. A sustained break below that level opens the path back toward the $1,700–$1,800 range, where longer-term structural support clusters. Momentum indicators remain weak. Price is trading below key moving averages, and volume on recovery attempts has been unconvincing.

Three scenarios shape the near-term outlook:

- Bull case: ETH reclaims and holds above $2,200, momentum shifts, and the $2,500–$2,700 range becomes the next target.

- Base case: ETH consolidates between $1,900 and $2,200 through Q2, with no decisive directional move. Ranking risk persists but doesn’t crystallize immediately.

- Bear case: A close below $1,900 on elevated volume invalidates the recovery thesis entirely.

The bearish pressure below $2,000 has been well-documented. What’s new is the structural narrative layered on top of a weak technical picture, and that combination tends to attract sustained selling pressure rather than dip-buyers.

Discover: The best crypto to diversify your portfolio with

Bitcoin Hyper Eyes Early-Mover Positioning as Ethereum Tests Critical Support

Ethereum’s stall at current levels, down more than 50% from its peak, with ranking risk now quantified at 59%, is prompting a segment of active traders to rotate toward earlier-stage infrastructure plays where asymmetric upside still exists. At $2,052, ETH’s market cap of $243 billion leaves limited room for the kind of multiples that defined its earlier cycles.

One project drawing attention in that rotation is Bitcoin Hyper ($HYPER), a Bitcoin Layer 2 integrating the Solana Virtual Machine, positioning it as the first-ever SVM-powered Bitcoin L2. The pitch: Solana-grade speed and programmability, secured by Bitcoin’s trust layer.

The presale has raised more than $32 million at a current price of just $0.0136, with staking available at high APY for early participants. The rise has accelerated in recent weeks alongside broader Bitcoin ecosystem momentum.

Key features include sub-second transaction finality, a decentralized canonical bridge for BTC transfers, and low-cost smart contract execution, targeting the gap between Bitcoin’s security and Ethereum’s programmability.

Those researching early-stage infrastructure plays can review Bitcoin Hyper’s presale details here.

This article is for informational purposes only and does not constitute financial advice. Crypto assets are highly volatile. Always do your own research before investing.

The post Ethereum Price Prediction: Prediction Market Bettors Think ETH Will Slide From Second Biggest Crypto appeared first on Cryptonews.

The first week of April brings a cluster of catalysts that could move select altcoins sharply in either direction. Token unlocks, protocol upgrades, and new mining integrations are converging within days of each other.

In line with the same, BeInCrypto has analysed three such altcoins that the investors should watch as April and Q2 2026 begin.

Dogecoin (DOGE)

Dogecoin (DOGE) is trading at $0.09315, up 2.99% on the day, consolidating just above the 0.618 Fibonacci level at $0.08807. DOGE is within a descending channel visible since late January. The Chaikin Money Flow (CMF) is reading exactly 0.00, signaling neither accumulation nor distribution, as price hovers near the lower boundary.

Qubic’s Dogecoin mining mainnet, targeting April 1, adds a new demand narrative for DOGE. If the catalyst drives a breakout above the descending channel upper trendline, currently converging toward $0.09933, a push toward the 0.382 Fibonacci level becomes viable. The channel compression means the resolution is approaching fast.

A daily close below $0.08807 would confirm bears remain in control inside the descending structure. The 0.786 level at $0.08005 then becomes the next meaningful downside reference. A sustained CMF drop below zero on rising volume would reinforce the bearish case heading into April.

Celo (CELO)

Celo (CELO) is trading at $0.0757, up 3.70% on the day, sitting below the 0.382 Fibonacci level at $0.0773 with the EMA sloping downward at $0.0785. Price has been oscillating between $0.0741 and $0.0825 for weeks, unable to reclaim the 0.618 level and trading dangerously close to the all-time low at $0.0689.

The Jovian Hardfork going live on March 31 brings gas mechanic upgrades and a buyback-and-burn tokenomics proposal to CELO. A successful upgrade that sparks buying could push the price through $0.0773 and toward the 0.618 Fibonacci resistance at $0.0825. Here, the green horizontal level on the chart has capped multiple recovery attempts.

Failure to hold above the 0.236 level at $0.0741 would be a bearish signal. This would suggest that the event is already priced in. Below there, the all-time low at $0.0689 becomes the only remaining technical reference point on the chart.

Sui (SUI)

Sui (SUI) is trading at $0.8714, up 2.91% on the day, sitting inside a broadening wedge with price pressing against the lower trendline. The Bollinger Bands show the middle band at $0.9552 and the lower band at $0.8381. The Money Flow Index (MFI) has dropped to 32.70, approaching oversold territory after peaking near 80 in mid-March.

The 42.94 million SUI unlock on April 1 is the dominant near-term catalyst. If the market absorbs the supply and MFI bounces from 32.70, a recovery toward the $0.8814 becomes plausible. A close above $0.9687 would shift the short-term structure back in favor of buyers.

A failure to hold the lower wedge trendline and a close below $0.8222 would invalidate any recovery thesis. Below there, $0.7609 is the next visible support on the chart. MFI sliding further without a bounce would confirm sustained selling pressure through the unlock event.

The post 3 Altcoins To Watch In The First Week Of April 2026 appeared first on BeInCrypto.

The Ethereum Foundation has staked over $46 million worth of ether in its largest single-day allocation, while continuing to rotate parts of its treasury through sales.

Summary

- Ethereum Foundation has staked 22,517 ETH worth over $46 million in its largest single-day deposit into the Beacon Chain.

- The move has followed a 2025 treasury strategy to deploy holdings for yield.

On-chain data from Arkham Intelligence shows the foundation transferred 22,517 ETH (ETH) to the Ethereum Beacon Deposit Contract at around 1:38 a.m. ET on Monday.

The contract is used to lock ETH into the network’s proof-of-stake system, where it helps validate transactions and secure the chain. The move marks the foundation’s biggest recorded staking transaction so far.

The latest deposit builds on a broader shift in treasury management that began last month, when the nonprofit first staked 2,016 ETH following a 2025 policy update outlining plans to actively deploy treasury assets to generate returns while supporting the network’s long-term development.

According to the foundation, this approach allows it to both strengthen Ethereum’s security and fund core operations, including protocol research and development, ecosystem growth initiatives, and community grants.

The increase in staking activity comes shortly after the foundation also executed a separate treasury transaction, selling 5,000 ETH in an over-the-counter deal worth just over $10.2 million to BitMine Immersion Technologies.

It marked the second instance of the foundation directly selling ETH to a corporate treasury firm, following a 10,000 ETH sale to SharpLink Gaming in July last year. The foundation has maintained that periodically selling assets across market cycles allows it to sustain development efforts without relying solely on external funding.

At the time of writing, ETH price was trading above $2,057, up more than 2.5% over the past 24 hours, with gains extending across both weekly and monthly timeframes.

Bitcoin price is trading at $67,500, up 1.5% in the last 24 hours, a soft jump that, on its own, means little, especially for those believing at 200K prediction. But combine it with radio silence from Michael Saylor’s Strategy and suddenly the question writes itself.

Has the most aggressive institutional buyer in crypto history finally tapped out?

— That Martini Guy ₿ (@MartiniGuyYT) March 29, 2026

LATEST

LATEST

MICHAEL SAYLOR HAS NOT POSTED THE SAYLOR TRACKER TODAY

IT SUGGESTS STRATEGY BOUGHT NO BITCOIN AFTER 13 STRAIGHT WEEKS OF BUYING pic.twitter.com/wpjUrVq39e

No fresh Strategy purchase announcement has emerged in the last 48 hours, an unusual silence from a firm that conditioned markets to expect near-weekly BTC accumulation disclosures. Profit-taking talk has intensified alongside it.

Still, with U.S. economic data releases imminent and ETF flow reports due, the next 72 hours carry outsized weight. Recent BTC price action analysis suggests the market is coiled, not broken.

Discover: The best crypto to diversify your portfolio with

Bitcoin Price Prediction: Can BTC USD Break $72,000 Resistance This Week?

Bitcoin’s current technical picture is a study in controlled tension. Price sits at just above $67,000, wedged between primary support at $65,000 (recent swing lows) and immediate resistance at $72,000 as the “now” ceiling.

The yearly trend remains bearish at 17% drop, and the 30-day base has held without a serious test. March opened at $65,000 leve; before staging the run, which was invalidated last week.

Three scenarios deserve equal attention right now:

- Volume returns, Strategy resumes buying (or another institutional name steps in), and BTC clears $72,000 on a daily close, opening a path toward the $75,000 area.

- Consolidation persists between $65,000 and $72,000 through early April as markets digest U.S. macro data; no breakdown, no breakout, just accumulation.

- A confirmed close below $65,000, however, would shift momentum, with $63,000 the next meaningful floor.

The Saylor silence is worth watching. GameStop’s recent 4,710 BTC treasury move hints corporate demand hasn’t evaporated; it may simply be rotating to new buyers. If ETF flow data due this week confirms continued institutional inflows, the $72,000 resistance test looks more likely than not.

Discover: The best pre-launch token sales

Bitcoin Hyper Targets Early Mover Upside as Bitcoin Tests Key Levels

Here’s the uncomfortable truth for late-cycle BTC buyers: at $67K, the asymmetric upside that early institutional adopters captured simply doesn’t exist anymore. Bitcoin’s risk-reward at current levels demands patience, possibly years of it. For traders who want Bitcoin-ecosystem exposure with early-stage return potential, the calculus looks different.

Bitcoin Hyper ($HYPER) is making a credible case for attention. It’s positioned as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, a genuinely novel architecture that is faster transaction performance than Solana itself while preserving Bitcoin’s security layer.

The presale has raised over $32 million at a current price of $0.0136, with high-APY staking already live for participants.

This article is not financial advice. Crypto investments carry significant risk. Always conduct your own research before investing.

The post Bitcoin Price Prediction: Michael Saylor Strategy Stops Buying? appeared first on Cryptonews.

The final week of March is shaping up to be a volatile one, with the FTX Recovery Trust set to distribute $2.2 billion to creditors on Tuesday and the key U.S. monthly nonfarm payrolls statistic due Friday, when many equity markets worldwide will be closed for Good Friday.

The war in the Middle East, now in its fifth week, is also critical. The conflict has disrupted major energy infrastructure and transport in the region, in turn leading to higher inflation expectations and a meaningful shift in monetary policy expectations, Luke Deans, a senior research associate at Bitwise, told CoinDesk.

“Bitcoin, a highly reflexive and liquidity-sensitive asset, typically responds earlier to shifts in risk appetite and has repriced lower since October 2025,” Deans said. “This suggests that digital assets began reflecting tighter financial conditions ahead of many traditional risk assets.”

Global macro forces, he added, remain the primary drivers of risk sentiment. While liquidity will certainly play a role, the market backdrop remains fragile given the ongoing geopolitical uncertainty.

What to Watch

(All times ET)

- Crypto

- Macro

- March 30, 9:30 p.m.: China NBS Manufacturing PMI for March (Prev. 49.0); Non-Manufacturing PMI (Prev. 49.5)

- March 31, 5:00 a.m.: Eurozone Inflation Rate YoY Flash for March (Prev. 1.9%); Core (Prev. 2.4%)

- March 31, 9:00 a.m.: U.S. S&P/Case-Shiller Composite-20 Home Price Index YoY for January (Prev. 1.4%)

- March 31, 9:45 a.m.: U.S. Chicago PMI for March (Prev. 57.7)

- March 31, 10:00 a.m.: U.S. Conference Board Consumer Confidence for March (Prev. 91.2)

- March 31, 10:00 a.m.: U.S. JOLTS job openings for February (Prev. 6.946M)

- March 31, 07:50 p.m.: Japan Tankan Large Manufacturing Index for Q1 (Prev. 15)

- April 1, 8:15 a.m.: U.S. ADP Employment Change for March (Prev. 63K)

- April 1, 10:00 a.m.: U.S. ISM Manufacturing PMI for March (Prev. 52.4)

- April 2, 8:30 a.m.: U.S. Initial Jobless Claims for week ending March 28 (Prev. 210K)

- April 3, 8:30 a.m.: U.S. Nonfarm Payrolls for March est. 48K (Prev. -92K)

- April 3, 8:30 a.m.: U.S. Unemployment Rate for March est. 4.5% (Prev. 4.4%)

- April 3, 10:00 a.m.: U.S. ISM Services PMI for March (Prev. 56.1)

- Earnings (Estimates based on FactSet data)

- March 30: Nano Labs (NA), pre-market

Token Events

- Governance Votes & Calls

- Stake DAO CRV and BAL are voting on their bi-weekly gauge to allocate CRV and BAL inflation across various liquidity pools. Voting ends March 31.

- SuperRare DAO is voting to consolidate its treasury management under the RareDAO Foundation by migrating remaining balances and officially concluding its legacy Network Engagement and Grants programs. Voting ends March 31.

- Aventus DAO is voting to simplify AVT emissions to a flat daily rate, increase the node staking requirement, and replace ongoing fees with an upfront appchain token allocation. Voting ends March 31.

- Unlock DAO is voting to transfer 3 ETH to its Base multisig to swap for USDC to cover current and future operational expenses. Voting ends April 2.

- Aavegotchi DAO is voting to elect nine multi-sig signers, maintain a 5-of-9 signature threshold, and set their quarterly compensation at $1,000 paid in GHST. Voting ends April 2.

- Arbitrum DAO is voting across two proposals to transition its Code of Conduct and Procedures into living documents managed by OpCo, and to upgrade to ArbOS 60 Elara. Voting ends April 2.

- SSV Network DAO is voting across two proposals to integrate ENS names for core protocol contracts to enhance security against phishing, and to establish a soft fee floor for public operators to ensure economic sustainability. Voting ends April 3.

- Lisk DAO is voting to test the Degov.ai governance platform ahead of Tally’s shutdown by executing a 0 LSK transfer. Voting ends April 7.

- Unlocks

- Token Launches

Conferences

Decentralized lending protocol Aave has officially launched on Ethereum layer 2 X Layer.

Summary

- Aave has launched on X Layer, enabling OKX Wallet users to lend, borrow, and earn yield directly on the network without bridging assets.

- X Layer, developed by OKX, has seen limited growth so far, with about $25 million in total value locked.

According to the official announcement, the launch will allow OKX Wallet users and DeFi participants to directly supply assets, borrow against collateral, and earn yield on the network without having to use a separate wallet or bridge assets across chains.

X Layer was developed by OKX and launched in 2024, but network growth has been relatively slow so far, with the chain holding only about $25 million in total value locked as of press time.

Onboarding Aave could significantly strengthen liquidity and expand the network’s DeFi capabilities.

“With a multi-year track record across more than a dozen blockchain networks and a 60% market share of DeFi lending, Aave is the largest and most trusted onchain lending network, with over $46 billion in supply & borrow. Its arrival on X Layer brings that same battle-tested infrastructure to OKX’s L2 ecosystem, permissionless, non-custodial, and accessible directly from OKX Wallet,” OKX said.

As part of the expansion, users can supply assets including USDT0, USDG, GHO, xBTC, xETH, xSOL, xBETH, and xOKSOL to earn yield that compounds automatically while retaining custody of their tokens.

Further, users will be able to borrow assets such as USDT0, USDG, GHO, xBTC, xETH, and xSOL against their collateral without any credit check or intermediary.

To access the service, OKX Wallet users just need to open the wallet, navigate to Aave through the DApps section, and connect to the X Layer network.

The latest expansion follows the launch of Orbit, a social trading platform that the crypto exchange introduced earlier this month.

As previously covered, Orbit is designed to combine social media-style interaction with trading tools, allowing users to share strategies, discuss market developments, and follow experienced traders in real time.

Around the same time, OKX disclosed a strategic investment from Intercontinental Exchange, with the deal set to give ICE a seat on the company’s board.

The Ripple research team has published a paper on adding transaction privacy to the XRP Ledger (XRPL).

The paper introduces Confidential Transfers for Multi-Purpose Tokens (Confidential MPTs). The goal is to enable institutional and regulated use cases, with issuer controls such as freezing and clawbacks.

Follow us on X to get the latest news as it happens

The paper is authored by Murat Cenk, Aanchal Malhotra, and Joseph Ayo Akinyele. The Confidential MPTs would be a cryptographic extension of the XLS-33 token standard, which went live on the XRPL mainnet in October 2025.

The protocol replaces plaintext per-account balances with EC-ElGamal ciphertexts. Furthermore, it uses non-interactive zero-knowledge proofs to enforce transfer correctness and balance sufficiency without requiring decryption by validators.

Meanwhile, sender and receiver identities remain visible, preserving XRPL’s account-based model.

“To accommodate regulatory and institutional requirements, Confidential MPTs provide cryptographic auditability through an on-chain selective-disclosure model based on multi-ciphertext balance representations and equality proofs, while remaining compatible with simpler issuer-mediated audit models,” the abstract reads.

The timing aligns with shifting regulatory attitudes toward on-chain privacy. In a recent report submitted to Congress in early March, the US Treasury Department acknowledged that lawful users of digital assets may rely on mixers when transacting on public blockchains.

The privacy paper arrives as Ripple simultaneously strengthens the network’s security foundation. The firm recently outlined an AI-driven security strategy for XRPL.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Ripple Researchers Propose Privacy-Preserving Transfers for XRPL Multi-Purpose Tokens appeared first on BeInCrypto.

4 Reasons Why Meme Coin Season Won’t Return Anytime Soon

Poll: MAHA wants more. They may turn to Democrats to get it.

Best teams for Honkai Star Rail 4.1 Pure Fiction (Virtual Made Manifest)

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos4 days ago

News Videos4 days agoParliament publishes latest register of MPs’ financial interests

-

Sports7 days ago

Sports7 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Sports7 days ago

Sports7 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat3 days ago

NewsBeat3 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

News Videos7 days ago

News Videos7 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Entertainment7 days ago

Entertainment7 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment1 day ago

Entertainment1 day agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

Fashion7 days ago

Fashion7 days agoFringe Bags for the Season

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

NewsBeat6 days ago

NewsBeat6 days agoEntrepreneurs Forum survey reveals optimism in North East

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

-

Politics6 days ago

Politics6 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

Crypto World6 days ago

Crypto World6 days agoBTC gives up $70,000 level as markets mull higher interest rates

You must be logged in to post a comment Login