Crypto World

MicroStrategy Explains What Happens First in a Bitcoin Collapse

MicroStrategy (Strategy) released its Q4 2025 earnings report and, along with it, disclosed an extreme downside scenario that would begin to strain its Bitcoin treasury model.

The CEO’s remarks provided rare insight into how far the market could fall before the company’s capital structure comes under serious pressure.

MicroStrategy Finally Reveals What Would Be Its Breaking Point as Bitcoin Price Drops

During its latest earnings discussion, MicroStrategy CEO Phong Le said that a 90% decline in Bitcoin’s price to roughly $8,000 would mark the point where the firm’s Bitcoin reserves roughly equal its net debt.

Sponsored

Sponsored

At that level, the company would likely be unable to repay convertible debt using its BTC holdings alone. As a result, it may need to consider restructuring, issuing new equity, or raising additional debt over time.

Leadership emphasized that such a scenario is viewed as highly improbable and would unfold over several years, giving the firm time to respond if markets deteriorated significantly.

“In the extreme downside, if we were to have a 90% decline in Bitcoin price to $8,000, which is pretty hard to imagine, that is the point at which our BTC reserve equals our net debt and we’ll not be able to then pay off of our convertibles using our Bitcoin reserve and we’d either look at restructuring, issuing additional equity, issuing an additional debt. And let me remind you: this is over the next five years. Right, So I’m not really worried at this point in time, even with Bitcoin drops,” said Le.

Meanwhile, it is worth noting that Le’s remarks come only months after the Strategy executive admitted a situation that would compell the firm would sell Bitcoin. As BeInCrypto reported, Phong Le cited a Bitcoin sale trigger tied to mNAV and liquidity stress.

Speaking on What Bitcoin Did, CEO Phong Le outlined the precise trigger that would force a Bitcoin sale:

- First, the company’s stock must trade below 1x mNAV, meaning the market capitalization falls below the value of its Bitcoin holdings.

- Second, MicroStrategy must be unable to raise new capital through equity or debt issuance. This would mean capital markets are closed or too expensive to access.

Therefore, the latest statement does not contradict Phong Le’s earlier position but adds another layer of risk.

Previously, a Bitcoin sale depended on stock trading below mNAV and capital markets’ closing. Now, he clarifies that in an extreme 90% crash, the immediate issue would be debt servicing, likely addressed first through restructuring or new financing—not necessarily selling Bitcoin.

Sponsored

Sponsored

Massive Bitcoin Exposure Comes with Large Losses

Strategy remains the world’s largest corporate holder of Bitcoin, reporting 713,502 BTC as of early February 2026. The company acquired the holdings at a total cost of about $54.26 billion, according to its fourth-quarter financial results.

However, Bitcoin’s decline during the final months of 2025 significantly impacted the balance sheet. The firm reported $17.4 billion in unrealized digital-asset losses for the quarter and a net loss of $12.4 billion. This highlights the sensitivity of its financial performance to market swings.

At the same time, Strategy continued to raise substantial capital. The company said it raised $25.3 billion in 2025, making it one of the largest equity issuers in the US.

Meanwhile, they also reportedly built a $2.25 billion USD reserve designed to cover roughly two and a half years of dividend and interest obligations.

Executives argue that these measures strengthen liquidity and provide flexibility, even during periods of market stress.

Sponsored

Sponsored

Bitcoin Volatility Brings the Risk Into Focus

The disclosure comes amid heightened volatility in crypto markets. Bitcoin traded near $70,000 in early February before extending successive legs lower to an intraday low of $60,000 on February 6. This shows how quickly price movements can reshape the outlook for highly leveraged treasury strategies.

Strategy’s capital structure relies heavily on debt, preferred equity, and convertible instruments used to accumulate Bitcoin over multiple years.

While this approach has amplified gains during bull markets, it also magnifies losses during downturns, drawing increasing scrutiny from investors and analysts.

However, the company’s leadership maintains that the long-dated nature of much of its debt provides time to manage through cycles. This, they say, reduces the risk of forced liquidations in the near term.

Saylor Doubles Down on Long-Term Thesis

Elsewhere, executive chair Michael Saylor reiterated his conviction in Bitcoin despite recent losses, describing it as the “digital transformation of capital” and urging investors to “HODL.”

Sponsored

Sponsored

Saylor and other executives argue that Bitcoin remains the hardest form of money and that the company’s long-term strategy is built around holding the asset indefinitely, rather than attempting to time market cycles.

The firm has also expanded its financial engineering efforts, including scaling its Digital Credit instruments and preferred equity offerings. According to management, these are designed to reduce volatility and diversify funding sources while continuing to accumulate Bitcoin.

Investors Split on the Risks Ahead

Market reaction to the earnings disclosures and downside scenario has been mixed. Supporters argue that Strategy’s massive Bitcoin reserves, ability to issue equity, and multi-year debt maturities provide sufficient flexibility to navigate even severe downturns.

Critics, however, warn that a prolonged bear market could still force difficult choices. Potential risks cited by investors include shareholder dilution, pressure on the capital structure, or the possibility of selling Bitcoin if funding conditions tighten.

“The company is currently facing a whopping -$7.3 billion loss on their Bitcoin investments,” said Jacob King.

For now, Strategy appears committed to its high-conviction approach. However, by acknowledging that its Bitcoin reserves would merely match its debt, the company has made clear that even the most aggressive corporate Bitcoin strategy still has a theoretical breaking point, one defined not just by market prices but by the limits of leverage itself.

Oil prices jumped more than 3% on Monday, pushing Brent crude above $116 a barrel. West Texas Intermediate (WTI), the US benchmark, climbed to roughly $102 per barrel.

The latest rise comes as the US-Israel war on Iran entered its fifth week with no signs of abating.

Oil Extends Its War-Fueled Rally

Several escalatory developments over the weekend fueled the surge. President Donald Trump told the Financial Times he could possibly seize Kharg Island, the terminal that handles roughly 90% of Iran’s crude exports.

Follow us on X to get the latest news as it happens

The US president struck a mixed tone on diplomacy with Iran, saying he was “pretty sure” of making a deal with Iran but conceding that talks could still collapse.

Meanwhile, Iran’s parliament speaker warned that Tehran would “set them on fire” when American forces arrived and promised consequences for US-allied nations in the region.

The oil price surge is far from over, according to market analysts, who warn that the prolonged closure of the Strait of Hormuz could drive crude even higher.

“A scenario in which the Strait remains closed for an additional month would be consistent with oil prices rising towards $150/bbl and constraints on industrial consumers of energy supply,” Bruce Kasman, global head of economics at JPMorgan, said.

According to Bloomberg, US officials and Wall Street analysts have also begun discussing the possibility of crude reaching $200 per barrel.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

Asian Stocks Tumble, Crypto Feels the Pressure

The energy shock rippled across Asia. Google Finance data showed that Japan’s Nikkei 225 fell over 4.5%, while South Korea’s KOSPI dropped more than 4.3% as import-dependent economies repriced risk.

The volatility has spread to crypto markets, with asset prices dipping early in the morning before rebounding.

“The market briefly crashed just now — ETH dropped below $1,940 and BTC fell below $65,000,” Lookonchain reported.

Oil above $100 per barrel continues to pressure risk assets by fueling inflation expectations and delaying anticipated Federal Reserve rate cuts.

The post Oil Rose 3% to Open the Week: Here’s What Moved the Market on Monday appeared first on BeInCrypto.

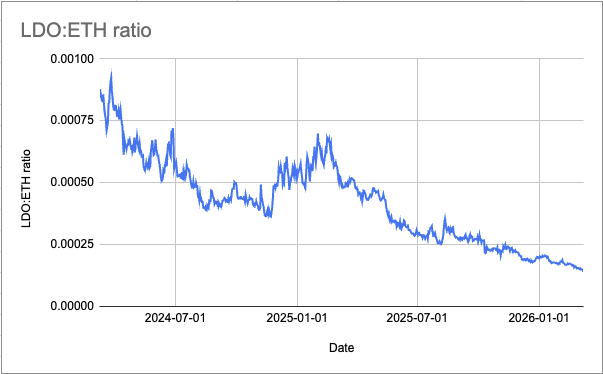

Lido’s decentralized autonomous organization is considering a one-off $20 million buyback of its governance token to address so-called price dislocation, which is at “historically depressed levels” relative to Ether, according to the DAO.

The proposal, submitted Friday, seeks permission to swap 10,000 Lido Staked Ether (stETH) tokens, currently worth $20 million from the DAO’s treasury for Lido DAO (LDO), arguing that LDO is undervalued.

“This is not a routine fluctuation. It represents one of the most significant dislocations between LDO’s market price and its underlying protocol fundamentals in the token’s history.”

A token buyback of this size could boost the price of the token, which has fallen roughly 96% from its all-time high. In November, a Lido DAO member pitched an automated buyback mechanism for LDO to improve the token’s price. However, that proposal hasn’t been implemented.

Lido DAO pointed out that LDO is trading at a steep discount to Ether (ETH) at a ratio of 0.00016, roughly 63% below its two-year median.

This is despite the protocol holding the top spot of the Ethereum liquid staking market, with a 23.2% share of staked Ether, according to Dune Analytics data. The protocol’s dominance has even been flagged as a centralization risk to the network in previous years.

Related: Ethereum builders propose ‘economic zone’ to tackle L2 fragmentation

LDO is currently trading at $0.30, down 95.9% from its $7.30 high set in August 2021, according to CoinGecko data. LDO’s $255 million market cap makes it the 141st largest token by value at the time of writing.

“That dislocation is not justified by a proportional deterioration in protocol performance,” Lido DAO said.

Lido DAO proposes buying stETH in batches

Lido DAO proposed buying up to 10,000 stETH in smaller batches of 1,000 to buy LDO.

Lido DAO said it would use limit orders or adopt a dollar-cost averaging strategy to avoid market volatility.

However, each batch would need approval and could be stopped by tokenholders.

After each batch, results would also need to be reported before continuing execution further.

The proposal also comes as Lido’s revenue fell 23% to 40.5 million in 2025, mostly due to staking fees falling 23% to $37.4 million.

Lido DAO argued the protocol’s fundamentals remain strong, noting that rewards declined just 20% amid the broader market pullback, costs improved 13% in 2025 compared with 2024 and Lido’s take rate rose from 5% to more than 6.1%, enhancing fee capture.

Take rate refers to the percentage of staked ETH rewards the protocol keeps as fees.

Magazine: Bitcoin’s ‘narrative vacuum,’ Ethereum now inevitable: Trade Secrets

Crypto World

Bitcoin’s Six-Month Losing Streak: What On-Chain Data Says About the Market’s Next Move

TLDR:

- Bitcoin may close March 2026 negative, marking six straight months of consecutive losses for the first time in years.

- SOPR data shows mild loss realization near the 1.0 level, but lacks the prolonged capitulation seen in the 2018 bear cycle.

- Declining exchange reserves suggest supply is being held off markets, yet weak ETF flows point to absent buyer demand.

- Analysts say recovering ETF inflows, a positive Coinbase Premium, and rising on-chain activity could spark a sharp BTC rebound.

Bitcoin is approaching a rare milestone that has historically preceded major market shifts. If March 2026 closes negative, it would mark six straight months of decline.

This pattern has appeared only a few times across crypto market history. Each instance was tied to a distinct structural event.

Analysts XWIN Research Japan studied this trend using CryptoQuant on-chain data. Their findings indicate the current cycle differs from past downturns in one key way.

Historical Comparisons Reveal Context for Bitcoin’s Extended Decline

Bitcoin’s 2014 four-month decline followed the collapse of the Mt. Gox exchange. That event damaged market trust and caused SOPR to become deeply unstable.

The data reflected a breakdown in market function itself, not a standard correction. It was a structural failure rooted in a single catastrophic exchange collapse.

The six-month decline from August 2018 to January 2019 followed the ICO bubble burst. SOPR stayed below 1 for a prolonged period, indicating widespread capitulation and forced selling.

The market underwent a full reset throughout that phase. A trend reversal followed as buying pressure eventually returned in early 2019.

Today’s SOPR reads near or slightly below 1, but sustained sub-1 behavior has not emerged. Loss realization is occurring, yet full capitulation has not taken place.

This separates the current phase from those earlier structural collapses. The market has not reached the same depth of distress seen in 2018.

In a post on Cryptoquant, analyst XWIN Research Japan noted that prior declines were driven by persistent selling pressure. The current downturn, however, is shaped by absent demand rather than forced exits.

That distinction changes how analysts should interpret this period. The framing of weakness matters when assessing potential recovery paths.

Demand, Absence, and On-Chain Signals Shape the Current Outlook

Exchange reserves are declining, which suggests supply is being held rather than actively sold. Yet weak Coinbase Premium data points to insufficient institutional buying interest in the market.

ETF flows have remained unstable, limiting new capital entry into the space. Together, these readings describe a market in pause rather than in freefall.

XWIN Research Japan noted that institutional infrastructure remains intact despite prolonged price weakness. Capital, however, has not returned in meaningful volume to the market.

Analysts describe this as a structural pause rather than a market breakdown. The market holds its footing but lacks the demand to move higher.

A sustained recovery would require ETF inflows to rebound and Coinbase Premium to turn positive. Rising on-chain activity would also need to accompany those developments.

If these signals align, analysts anticipate a sharp Bitcoin price recovery could follow. The timing of that convergence remains the central question for market participants.

Bitcoin now sits between structural resilience and cyclical weakness. Without full capitulation, further price consolidation is possible in the near term.

However, conditions for a reversal exist if demand returns. Monitoring on-chain data closely will be essential to tracking when the next directional move begins.

A new collaborative framework proposed by developers from Gnosis and Zisk, with support from the Ethereum Foundation, aims to knit Ethereum’s sprawling layer-2 ecosystem into a more cohesive execution fabric. The initiative, dubbed the Ethereum Economic Zone (EEZ), envisions cross-rollup interactions that would allow smart contracts on different rollups to run in lockstep with one another and settle back to Ethereum in a single transaction—without the need for traditional bridges.

Presented in an announcement shared with Cointelegraph, the EEZ would mitigate a central tension in Ethereum’s scaling approach: dozens of rollups have increased throughput, but liquidity, infrastructure, and user activity remain fragmented across separate networks. If realized, the framework could enable shared infrastructure across rollups and streamline settlement to Ethereum, reducing duplication and the burden of cross-chain transfers for developers and users alike.

The effort positions Ethereum researchers and a broader ecosystem behind a formal standard for interoperable rollups, with Gnosis and Zisk among the early contributors. The project also signals a broader push to move beyond isolated scaling layers toward a more unified execution layer architecture. Early participants include infrastructure providers and DeFi protocols exploring a common standard for interoperable rollups.

Key takeaways

- EEZ would allow cross-rollup smart-contract execution to occur synchronously, bypassing bridges and settlement bottlenecks.

- The proposal targets liquidity fragmentation by enabling shared infrastructure and cohesive interaction among rollups and Ethereum mainnet.

- The EEZ Alliance has been formed to coordinate standards and push adoption as Ethereum’s scaling landscape evolves.

- Gnosis and Zisk anchor the initiative, with involvement from Ethereum researchers and other industry actors; Jordi Baylina (Zisk) cites zero-knowledge proving expertise as a key component.

- Technical details and performance benchmarks are slated for release in the coming weeks as the framework moves from concept to design and potential deployment.

Interoperability in the spotlight as scaling debate intensifies

The EEZ proposal arrives amid a long-running discussion within the Ethereum community about the trade-offs of a rollup-centric scaling path. Rollups have pushed throughput higher than base Ethereum, but the field has grown into a tapestry of separate ecosystems, each with its own liquidity and user base. Data from L2BEAT indicates there are more than 20 active layer-2 networks with collectively close to $40 billion in total value locked, distributed across networks like Arbitrum, Base, and Optimism. The outcome has been a parallelized execution environment rather than a single, consolidated scaling layer.

Industry voices have recently highlighted concerns about the architecture of some L2s. Vitalik Buterin suggested in a February X post that the original vision for L2s and their role in Ethereum may require a rethink, pointing to potential weak points in centralized sequencers and trusted bridges. The ensuing discussion among L2 builders underscored a spectrum of views on whether scaling alone remains the priority or if interoperability and unified settlement should take a more central role in the network’s evolution.

Karl Floersch, co-founder of Optimism, has acknowledged the need for L2s to evolve beyond simple scaling mechanics, citing ongoing technical hurdles. Steven Goldfeder, co-founder of Offchain Labs (the team behind Arbitrum), emphasized that scaling remains a core function as rollups continue to handle higher transaction throughput than Ethereum itself. The EEZ concept could be seen as a response to these ongoing debates, offering a pathway to reduce cross-network friction while preserving the performance advantages of rollups.

What changes with EEZ—and what remains uncertain

If the EEZ framework progresses, it would potentially enable applications to share infrastructure across multiple rollups and settle their state to Ethereum in a coordinated fashion. This would reduce duplication of validators, data availability resources, and bridging overhead, while preserving rollups’ high throughput. The defining feature would be a synchronized execution model that subscribes to a common standard, enabling more seamless inter-rollup communication and a more unified user experience.

Several questions remain as the project moves from concept to design. How would a cross-rollup execution model handle security guarantees across diverse rollups with different trust assumptions? What governance and standardization processes would be needed to ensure broad acceptance across the ecosystem? And crucially, what would adoption look like in practice—how quickly would developers and users pivot to a shared framework, and what incentives would drive this transition?

Early work emphasizes collaboration among major ecosystem players, with the EEZ Alliance positioned to coordinate development, testing, and eventual rollout. While concrete technical specifications are not yet public, the timeline anticipates forthcoming detail on implementation strategies, performance benchmarks, and compatibility assurances across major rollups.

What to watch next

Developers expect a more detailed technical outline in the weeks ahead, accompanied by benchmarks illustrating how cross-rollup synchronization would perform under realistic workloads. The EEZ Alliance’s progress will also be a key indicator of whether the broader ecosystem is ready to adopt a shared standard that could reduce cross-network friction while maintaining or enhancing security, reliability, and user experience.

Investors and builders should monitor how the EEZ concept interacts with ongoing efforts to modularize Ethereum’s scaling stack, including cross-layer collaboration, data availability solutions, and zk-based tooling. The question of whether a unified cross-rollup framework can gain rapid traction remains open, but the proposal clearly signals a deliberate shift toward interoperability as a central pillar of Ethereum’s long-term scaling strategy.

As Ethereum’s scaling architecture continues to evolve, the next few quarters could reveal whether the EEZ Alliance becomes a conventional standard, or whether the path toward a truly cohesive rollup economy will require alternative approaches. For now, the industry is watching a select group of core contributors test a bold idea: how to turn multiple high-throughput networks into a single, more efficient ecosystem without surrendering the strengths that have driven their rapid growth.

Readers should stay tuned for technical disclosures and real-world experimentation that would demonstrate the practicality of cross-rollup synchronization and the feasibility of shared infrastructure across rollups—an outcome that could reshape how developers build and users interact with Ethereum’s scaling frontier.

TLDR:

- Brent crude consolidating at $100.66 places 30% of global oil supply under critical logistical risk at the Strait of Hormuz.

- Institutions moved $11.574 billion in Bitcoin through OTC desks, locking supply as a strategic reserve amid cost-push inflation fears.

- Bitcoin’s $65K–$70K structural support zone holds a 65% survival probability, contingent on no global credit market capitulation.

- A systemic stress scenario tied to April 6th liquidity risk could push Bitcoin toward a corrective low of $54,000 per coin.

The ghost of 1973 is back, and oil at $100 is forcing a reckoning across global markets. Brent crude has consolidated at $100.66 per barrel as the Strait of Hormuz faces active geopolitical tension.

Roughly 30% of the world’s oil supply now sits under critical logistical risk. Bitcoin, priced at $66,339.88 after a 3.45% weekly decline, is caught in the crossfire.

On-chain data tracked by GugaOnChain reveals $12.3351 billion in institutional movement reshaping how the market absorbs this pressure.

Oil’s 1973 Echo Puts Bitcoin’s Neutral Infrastructure Under the Spotlight

The 1973 oil crisis repriced nearly every asset class as supply disruptions spread across global economies. Today’s energy shock carries a structurally similar fingerprint, with physical logistics facing blockade-level risk at a critical shipping corridor. Unlike oil, Bitcoin moves without ships, pipelines, or territorial dependencies.

GugaOnChain described Bitcoin as a liquidity rail that operates outside physical blockades entirely. This framing positions the asset differently from commodities that rely on geographic infrastructure to settle and clear. When oil freezes at a chokepoint, Bitcoin settlement continues at the same pace.

Source: Crptoquant

That distinction becomes relevant as cost-push inflation pressures mount from rising energy prices. Institutions appear to be responding to this dynamic through heavy over-the-counter accumulation.

Of the $12.3351 billion tracked on-chain, 93.83%—approximately $11.574 billion—flowed through OTC desks away from public exchanges.

This volume signals a deliberate strategy to lock Bitcoin as a strategic reserve during the current macro disruption. Smart money is absorbing mobile supply during the panic rather than exiting.

The 1973 parallel holds here too — those who held hard assets through the energy crisis largely preserved purchasing power.

Bitcoin’s $65K–$70K Support Zone Faces a Systemic Stress Test

The $65,000–$70,000 range now serves as a structural support zone anchored by Bitcoin’s realized price. GugaOnChain estimates a 65% probability that this zone holds through the current volatility cycle. That probability, however, depends on global credit markets avoiding a full capitulation event.

The probability of a broader liquidity crunch in traditional markets currently sits between 45% and 50%. Such an event would trigger margin calls across leveraged positions, forcing temporary liquidations even where demand remains fundamentally strong. The shallow exchange order book raises the risk of moves exceeding 8% to above 70% on any geopolitical trigger.

GugaOnChain flagged April 6th as a concentrated risk window, calling it a global liquidity solvency test. A systemic stress scenario during this period could drive a corrective move toward $54,000. Derivative hedges are recommended as active protection around this specific date for exposed portfolios.

The overall asymmetry remains neutral-to-positive given the supply lock-up through OTC channels. Forced scarcity from institutional accumulation creates a structural floor even as downside scenarios remain on the table.

Bitcoin’s trial by fire, much like 1973, will ultimately determine whether the asset earns its place as a credible reserve in an energy-disrupted world.

Ethereum’s effort to reclaim the market’s No. 2 spot is facing a different obstacle this year: a booming stablecoin economy. While Bitcoin remains the dominant benchmark, the faster-growing sector of dollar-denominated crypto assets is reshaping how capital flows through the space, with USDT leading the charge and pulling liquidity away from ETH at the margins.

Five-year data show a striking divergence in growth patterns. ETH’s market capitalization rose by about 11.75% over the past five years to roughly $240 billion, but USDT tallied a far larger ascent, expanding by approximately 622.5% to more than $184 billion in market cap. XRP and USD Coin have also outpaced ETH in growth over the same horizon. That dynamic helps explain traders’ evolving bets on whether ETH can hold or reclaim its No. 2 ranking in 2026. On Polymarket, more than 59% of wagers are currently predicting ETH will drop from the No. 2 position in 2026, up from around 17% at the start of the year, signaling a shift in sentiment as the stablecoin economy strengthens.

Key takeaways

- Stablecoins are reshaping market leadership: ETH’s five-year market-cap growth trails USDT, XRP, and USDC, signaling a broader reallocation of capital away from ETH toward dollar-pegged assets.

- USDT dominates the stablecoin landscape: the total stablecoin market sits near $310 billion, with Tether controlling about 58% of that share.

- Weak ETH demand from institutions: US spot Ethereum ETFs have seen assets under management fall about 65% year-to-date, dipping to roughly $11.76 billion in March from $31.86 billion in October last year.

- Market fragility and risk-off dynamics: macro headwinds—from tariffs to geopolitical tensions and shifting expectations for rate cuts—have amplified demand for liquidity and safety, benefiting stablecoins.

- Technical setup points to potential near-term downside: Ether is forming a bear-flag pattern, with a measured downside target around $1,250 if the breakdown persists into mid-2026.

Why stablecoins are pulling the rug from under ETH

ETH’s price dynamics have historically benefited when risk appetite was broad and capital flowed into sustained growth narratives around decentralized finance and smart-contract infrastructure. But the current macro environment has encouraged more conservative positioning and a preference for liquidity and capital preservation. Stablecoins—crypto dollars designed to maintain peg to the U.S. dollar—serve as a ready-made conduit for capital during risk-off phases. This dynamic helps explain why USDT’s market capitalization has surged while ETH’s growth has lagged behind some of its peers.

Market data show the broader stablecoin sector has grown to about $310 billion, a level that reflects deep liquidity and the willingness of traders and institutions to park cash in a familiar, compliant asset rather than chase the latest DeFi yield. With USDT accounting for the lion’s share of this market, investors gain access to rapid risk management, arbitrage opportunities, and flexibility in a choppy macro backdrop. In contrast, ETH’s value creation remains tethered to the crypto cycle and the willingness of market participants to take on price risk for longer-term network fundamentals.

These forces help explain why ETH’s market cap expansion has not kept pace with the sheer scale and velocity of stablecoins. For traders and builders, the implication is clear: even as Ethereum remains foundational to DeFi and smart contracts, it faces structural headwinds when overall risk sentiment cools and liquidity seeking behavior drives inflows into dollar-pegged assets.

Institutional demand for ETH cools as stablecoins flourish

The narrative around Ethereum ETFs has also shifted. Data tracked by Glassnode show that US spot Ethereum ETF balances have declined sharply, with assets under management sliding from about $31.86 billion in October last year to roughly $11.76 billion in March—a drop of around 65%. This trend underscores how institutional appetite for ETH, whether through spot structures or related products, has cooled in the face of competing liquidity instruments and a more cautious macro environment.

Industry observers point to a few contributing factors: hedging and liquidity preferences during a risk-off cycle, evolving regulatory expectations around ETF products, and a general rotation of capital toward assets with visible liquidity profiles in volatile markets. While Ethereum remains a core infrastructure asset for many users and developers, the near-term flow dynamics suggest that institutional catalysts for a sustained ETH price breakout may be harder to come by without broader risk-on momentum.

What to watch next: price structure and market sentiment

From a technical standpoint, Ether appears to be navigating a bear-flag formation on shorter timeframes. A breakdown below the structure’s lower trendline would, in this reading, increase the probability of a corrective move toward the low-$1,000s region. A commonly cited target sits near $1,250 by June, should the pattern play out as anticipated. Of course, chart-based forecasts carry uncertainty, and headlines—ranging from regulatory developments to macro policy shifts—can alter the trajectory quickly.

Beyond price, the evolving balance between ETH and stablecoins in market liquidity is a critical barometer. If risk appetite improves and demand for ETH returns, the relative performance gap could narrow as DeFi activity, NFT markets, and institutional participation regain steam. Conversely, further strength in the stablecoin market and continued preference for cash-like liquidity could keep ETH price gains muted even as the broader crypto ecosystem remains active in pockets of use and development.

Key signals to watch include: changes in stablecoin issuance and redemption trends, ETF inflows or outflows for ETH-related products, and macro developments that alter risk sentiment or the expected pace of Federal Reserve policy. If the bear-case scenario unfolds, investors will want to monitor whether ETH can anchor a bottom while stablecoins continue to absorb a large share of new liquidity in the crypto space.

Ultimately, the question for 2026 remains partly about ETH’s fundamental resilience and partly about the broader appetite for dollar-denominated liquidity in a volatile market. As the ecosystem evolves, investors, traders, and builders will need to weigh ETH’s role as infrastructure against the advantages that stablecoins offer in terms of liquidity, risk management, and cross-asset flexibility.

Readers should keep an eye on ETF flow patterns, the pace of stablecoin growth, and the macro signals that drive risk-on versus risk-off dynamics. Those factors will help determine whether ETH can reverse the current trajectory or whether stablecoins will continue to crowd out its price drivers in the near term.

TLDR:

- Russia’s monthly oil revenue doubled to $24 billion as Brent crude surpassed $100 per barrel.

- Ukraine’s drone strikes have taken roughly 40 percent of Russian export refining capacity offline.

- Iran’s attack on Ras Laffan removed 17 percent of global LNG and 33 percent of helium supply.

- Western sanctions capped Russian oil at $60 per barrel, but the dual-war supply shock made it void.

Russia’s oil revenue has surged sharply as two concurrent conflicts disrupt global energy supply chains. Ukrainian drone strikes have degraded roughly 40 percent of Russian export refining capacity in recent weeks.

At the same time, Iran’s strikes on Gulf infrastructure pushed Brent crude above $100 per barrel. Russia’s Foreign Minister Lavrov and President Putin have both publicly forecast oil reaching $150 per barrel. Russia appears financially positioned to benefit from both conflicts running simultaneously.

Russia Benefits as Iran’s Gulf Strikes Push Oil Above $100

Russia supplied Shahed drone technology and design upgrades to Iran’s Islamic Revolutionary Guard Corps over recent years. Those drones, combined with Chinese BeiDou-guided ballistic missiles, struck the Ras Laffan complex in Qatar.

The attack removed 17 percent of global LNG export capacity and 33 percent of global helium supply. The energy shock from those strikes quickly pushed Brent crude above $100 per barrel.

Russia’s monthly oil revenue consequently doubled to $24 billion as crude prices climbed. The Western sanctions price cap of $60 per barrel has since become functionally irrelevant at current market levels.

Sanctions were designed to target Russian oil pricing, but both conflicts have instead targeted global supply directly. Supply disruptions have overpowered the sanctions framework that was originally built to limit Russian earnings.

On March 27, Lavrov publicly warned of what he called “the most severe energy crisis in human history.” Putin followed by openly forecasting oil at $150 per barrel shortly after.

Both leaders are stating a price target that enriches Russia with every dollar crude rises above current levels. Social media analyst Shanaka Anslem Perera described it as a self-amplifying feedback loop that continuously benefits Russia.

Perera wrote: “Russia arms Iran. Iran closes Hormuz. Hormuz closure spikes oil. Oil spike enriches Russia.” He further noted that Russia needs neither Hormuz reopened nor its own refineries fully operational.

Russia needs both disruptions to persist so their combined effect drives oil toward $150. The compound supply shock, as a result, overwhelms a sanctions architecture never designed for this dual-war scenario.

Ukraine Retaliates Against Russian Refineries and Builds New Alliances

Ukraine struck the Tuapse refinery complex, one of Russia’s largest, setting it ablaze with precision drones. Combined with weather damage and maintenance backlogs, approximately 40 percent of Russian export refining capacity is now offline.

Each barrel of Russian refined product removed from markets tightens global supply further. Every tightening, in turn, pushes oil closer to the $150 target Russia has publicly forecast.

That same week, Ukrainian President Zelensky traveled to Saudi Arabia for high-level diplomatic engagements. Ukraine offered its battle-tested anti-drone expertise to protect Gulf LNG and helium infrastructure directly.

Ukrainian technology has already proven effective against the same Shahed variants Iran deploys in the broader region. This opened an unexpected military technology export market for Ukraine among the world’s wealthiest nations.

The OECD revised US inflation projections upward to 4.2 percent, directly linking the change to the Iran-driven energy shock. BlackRock CEO Larry Fink stated publicly that $150 oil would likely trigger a global recession.

Ukraine’s strikes on Russian refineries and Iran’s pressure on Gulf supplies are tightening markets from opposite directions.

Russia, however, continues collecting elevated revenue from price premiums generated by both disruptions running at once.

Perera closed his widely shared analysis with a sharp observation: “Two wars. One price. One beneficiary. The arsonist is selling fire insurance.”

The feedback loop connecting both conflicts shows no sign of breaking under current conditions. Russia’s oil earnings continue to grow beyond what any sanctions cap was structured to contain.

As long as both wars persist, Russia’s financial position remains stronger than at any prior point since invading Ukraine.

TLDR:

- Dogecoin is printing a consistent accumulation-markup-pullback cycle near $0.09, signaling structured price behavior.

- Analysts note shallow pullbacks and tight consolidation zones that point to underlying demand supporting DOGE price.

- A long-term MACD crossover is forming on macro timeframes, a signal that has historically preceded DOGE rallies.

- The $0.05 support level remains critical, as a hold with MACD confirmation could trigger a broader bullish reversal.

Dogecoin is once again following a recurring cycle pattern that analysts say could fuel fresh rally expectations. The token has been trading near $0.09, where chart structures show a consistent sequence of accumulation, markup, and pullback phases.

Adding to the outlook, a long-term MACD signal is now forming on macro timeframes. These two developments are drawing close attention from traders watching for the next directional move in DOGE.

Recurring Accumulation Cycle Points to Potential Markup Phase

Dogecoin has been printing a recognizable cycle structure that technical analysts describe as methodical. Crypto analyst Bitcoinsensus recently outlined the pattern, noting three repeating phases: accumulation, markup, and pullback. The consistency of this structure across multiple cycles is what separates it from typical sideways price action.

Each accumulation phase begins with a contraction in volatility. Price trades within a tight range as buyers absorb available supply at lower levels. This compression phase tends to persist until a liquidity event triggers the next move upward.

The markup phase that follows is typically sharp and measured. Bitcoinsensus noted that these moves often begin with stop hunts, clearing out weak hands before price advances. Rather than forming a sustained trend, these bursts reflect structured participation, likely algorithmic in nature.

After each markup, Dogecoin enters a shallow pullback that respects prior breakout zones. These retracements hold above key support areas, reinforcing the presence of underlying demand. If the current consolidation near $0.09 maintains this structure, the next markup phase could be forming.

MACD Signal on Macro Chart Strengthens Rally Expectations

Beyond the micro-cycle structure, a broader technical signal is now building on Dogecoin’s macro chart. Crypto Logic Lab flagged a developing MACD crossover forming on longer-term timeframes, not the daily, but higher macro charts. This type of signal has historically preceded sustained rallies in DOGE.

Bears are currently targeting the $0.05 level as a key zone to test before the crossover confirms. The strategy involves pushing price lower to shake out long positions and trigger stop losses. Both sides of the market are watching this level, making it the central battleground for this cycle.

Crypto Logic Lab noted that the MACD signal is forming ahead of any price breakout, which represents the optimal positioning window.

A hold at $0.05 combined with MACD confirmation would strengthen the case for a reversal and a broader rally. A breakdown below that level, however, would cancel the bullish setup entirely.

The convergence of the recurring cycle pattern and the developing macro MACD signal gives rally expectations a stronger technical foundation.

Traders are watching for a breakout above the recent local high as confirmation. Until then, the $0.05 support zone remains the critical level to monitor for directional clarity.

The crypto market is buzzing again, are you watching closely or missing out? With Bitcoin showing renewed strength and Solana gaining momentum from recent ecosystem growth, investors are actively hunting for the best altcoins to invest before the next breakout wave hits.

While Bitcoin holds dominance and Solana continues scaling with faster transactions, a new contender is quietly building explosive potential. Enter APEMARS ($APRZ), currently in presale and already generating serious buzz. As major coins make headlines, smart investors are positioning early in projects like APEMARS that could deliver life-changing returns before hitting exchanges.

APEMARS: The Best Altcoins To Invest Before The Next Surge

If you’re searching for the best altcoins to invest, timing is everything, and APEMARS is right at that sweet spot. Still in presale, it offers a rare early-entry opportunity that most investors only wish they had with projects like Solana or even Bitcoin in their early days.

APEMARS is currently in Stage 14 (Drift King) of its presale, priced at $0.00017238, with a projected listing price of $0.0055. That’s a massive 3,090% ROI potential from this stage alone. With over 1,505 holders, $345K+ raised, and 22.84 billion tokens sold, the momentum is undeniable. The numbers aren’t just stats, they signal growing demand and shrinking opportunity.

Staking System Powering Long-Term Growth

One of the strongest features of APEMARS is its staking system, known as the APE Yield Station. Offering an impressive 63% APY, it allows investors to grow their holdings passively. Inspired by Mars’ extreme conditions, this mechanism isn’t just creative, it’s strategic. With a mandatory 2-month lock post-launch, it helps stabilize early trading and reduces sell pressure, giving the project a stronger foundation right out of the gate.

Orbital Boost Referral System Driving Viral Expansion

APEMARS also introduces a powerful referral system called the Orbital Boost System. Once you contribute at least $22, you unlock the ability to earn 9.34% rewards for both you and your referrals. This creates a community-driven growth engine where users are incentivized to spread the word, fueling organic expansion and increasing demand as the presale progresses.

How To Buy APEMARS

Getting started with APEMARS is simple:

- Visit the official presale platform

- Connect your crypto wallet (like MetaMask)

- Choose your investment amount

- Confirm the transaction

- Secure your tokens before the next stage price increase

Turn $2,000 Into A Massive Win: APEMARS ROI Breakdown

Let’s talk real numbers, because this is where things get exciting.

If you invest $2,000 today at Stage 14 price ($0.00017238), you’ll receive approximately 11.6 million tokens.

- At launch price ($0.0055): Your $2,000 becomes approximately $63,800

- If APEMARS reaches $1: Your investment skyrockets to $11.6 million

- At $5: You’re looking at a jaw-dropping $58 million+

This is why early investors hunt presales. While others chase trends, you position yourself before the wave hits. If you’ve ever regretted missing early Bitcoin or Solana, this is your second chance.

Solana Surges With Ecosystem Growth And Institutional Attention

Solana has recently been gaining traction again, fueled by increased developer activity and institutional interest. Faster transaction speeds and lower fees continue to make it a strong competitor in the smart contract space.

With growing adoption in DeFi and NFTs, Solana is proving its resilience after past challenges. Many analysts are optimistic about its future, and it often appears in discussions around Bitcoin price prediction and broader altcoin market movements. However, while Solana offers stability, its explosive growth phase may already be partially priced in.

Bitcoin Holds Strong As Market Confidence Returns

Bitcoin remains the backbone of the crypto market. Recent bullish sentiment, ETF developments, and macroeconomic factors have helped it maintain strong price support.

As always, Bitcoin is seen as a safer long-term hold, especially during uncertain times. But for investors seeking exponential returns rather than steady growth, Bitcoin’s size limits its upside compared to emerging projects. It sets the tone for the market, but smaller caps like APEMARS create the real wealth opportunities.

Conclusion

The search for the best altcoins to invest often leads investors to established names like Bitcoin and Solana, but the biggest gains usually come from getting in early. APEMARS is still in its presale phase, offering a rare opportunity to enter before exchange listings drive prices higher. With strong tokenomics, staking rewards, and viral growth mechanisms, it’s designed for momentum.

If you’re serious about finding the best crypto to buy now, APEMARS stands out as a high-potential contender. Opportunities like this don’t stay open forever. As stages progress and prices rise, early access disappears. Don’t wait until it trends, position yourself now and be part of the journey before the masses arrive.

Using the information curated by best crypto to buy now, this analysis presents an overview of crypto rankings and growth opportunities.

For More Information:

Website: Visit the Official APEMARS Website

Telegram: Join the APEMARS Telegram Channel

Twitter: Follow APEMARS ON X (Formerly Twitter)

Frequently Asked Questions About Best Altcoins To Invest

What Are The Best Altcoins To Invest In 2026?

The best altcoins to invest include emerging presale projects like APEMARS, alongside established coins. Early-stage investments often provide higher ROI potential compared to already matured cryptocurrencies.

Is APEMARS ($APRZ) A Good Investment?

APEMARS ($APRZ) offers strong presale metrics, staking rewards, and referral incentives. Its early entry price and structured growth model make it appealing for high-risk, high-reward investors.

How Does Bitcoin Price Prediction Affect Altcoins?

Bitcoin price prediction often reflects broader market sentiment. When XRP and major altcoins rise, it signals bullish momentum that can positively impact smaller projects like APEMARS.

Can APEMARS Compete With Solana And Bitcoin?

While Solana and Bitcoin are established, APEMARS has higher growth potential due to its early stage. It targets exponential returns rather than stability.

When Is The Best Time To Buy APEMARS?

The best time is during presale stages like Stage 14, where prices are still low. Early participation increases potential ROI before exchange listings.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

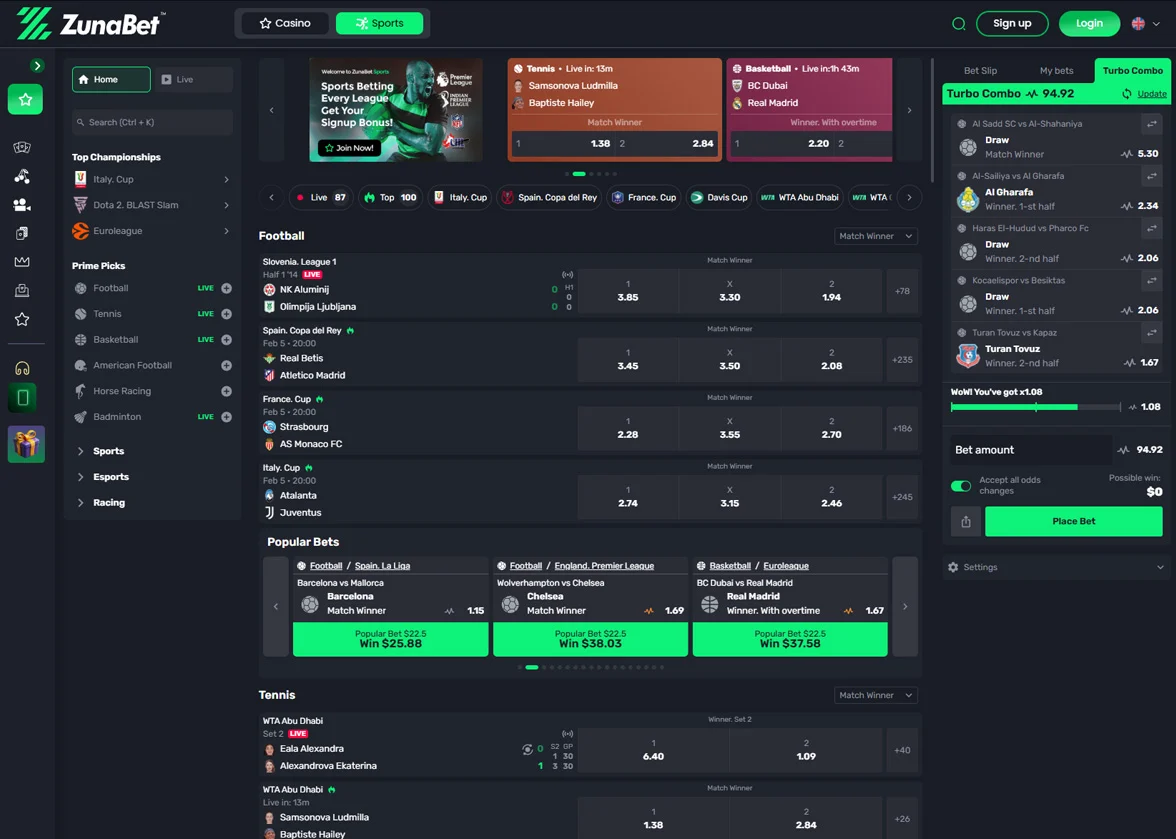

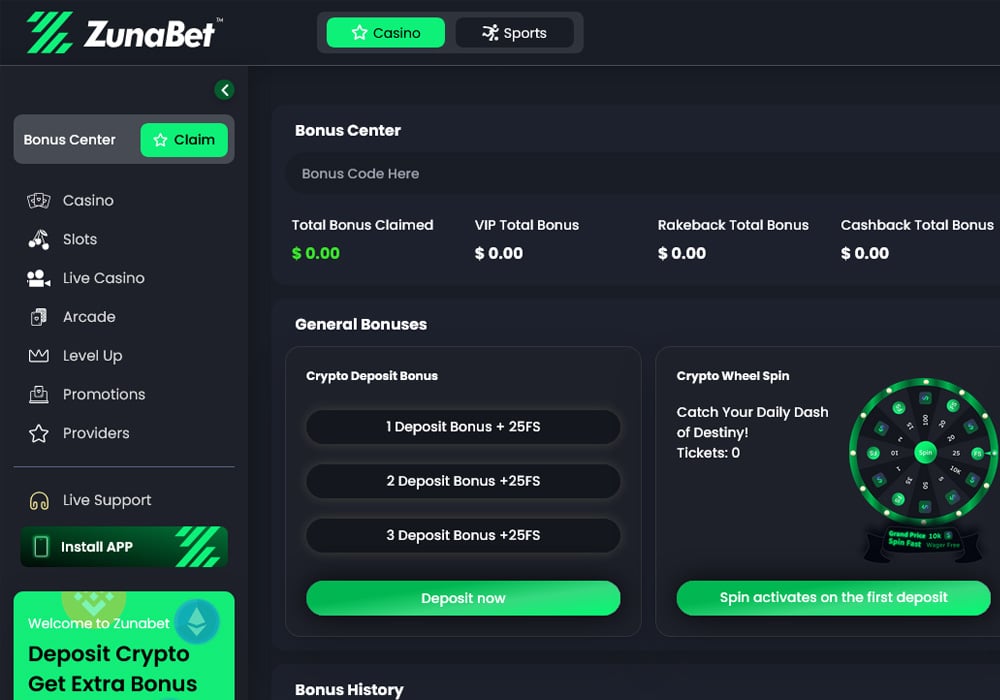

Crypto gambling has grown steadily over the past few years, and 2026 has brought more competition to the space than ever. Stake.com remains one of the biggest names in the industry, but it is no longer the only platform drawing serious attention. ZunaBet entered the market this year and has quickly become a talking point among crypto gamblers. This comparison looks at both platforms across bonuses, game selection, loyalty rewards, and overall value.

What Stake.com Brings to the Table

Stake.com has been around since 2017. It operates under a Curaçao license and has grown into one of the most visited crypto gambling sites in the world. The platform covers both casino games and sports betting, with support for Bitcoin, Ethereum, Litecoin, Dogecoin, and several other cryptocurrencies.

A big part of Stake’s identity is its library of original games. Titles like Plinko, Crash, Mines, and Dice are provably fair and have developed a loyal following. Outside of originals, Stake carries slots and live dealer tables from well-known providers including Pragmatic Play, Hacksaw Gaming, and Evolution.

The sportsbook side covers major leagues and sports globally, including football, basketball, tennis, MMA, and a solid esports section. Stake has earned a reputation for sharp odds and a straightforward betting experience.

Where Stake stands apart from most competitors is its approach to bonuses. There is no welcome bonus. No deposit match, no free spins for signing up. Instead, Stake operates an invite-only VIP program where rewards are unlocked based on wagering volume over time. Benefits at higher tiers include rakeback, weekly and monthly bonuses, and tailored offers. This setup favors players who are already planning to bet frequently and in larger amounts.

What ZunaBet Offers as a Newcomer

ZunaBet went live in 2026 under the ownership of Strathvale Group Ltd. It holds an Anjouan gaming license and was built by a team with more than 20 years of combined experience in online gambling. The platform was designed from the ground up as crypto-first, meaning crypto is the primary way to deposit and withdraw rather than a secondary option bolted onto a fiat system.

The game library is hard to ignore. ZunaBet lists over 11,000 games from 63 different providers. That roster includes Pragmatic Play, Hacksaw Gaming, Yggdrasil, BGaming, and Evolution, covering slots, table games, and live dealer options. With 60+ providers feeding into one platform, the variety is among the widest available in the crypto casino market right now.

Sports betting is fully integrated. The sportsbook covers football, basketball, tennis, NHL, and combat sports, along with esports markets for CS2, Dota 2, League of Legends, and Valorant. Virtual sports are included too. Everything sits under one account, so switching between casino and sports is seamless.

ZunaBet supports more than 20 cryptocurrencies. The list includes BTC, ETH, USDT on multiple chains, SOL, DOGE, ADA, XRP, and others. The platform charges no processing fees on its end, and withdrawals are built to process quickly. Apps are available for iOS, Android, Windows, and MacOS, and live chat support runs around the clock.

Welcome Bonus: A Clear Split

The most obvious difference between these two platforms is what happens when you first sign up.

Stake gives you nothing upfront. There is no deposit match and no free spins. You start playing, and if you wager enough over time, you may eventually get invited into the VIP program. That works for a certain type of player, but it asks for commitment before giving anything back.

ZunaBet goes in the other direction with a welcome package worth up to $5,000 plus 75 free spins. It breaks down like this: the first deposit is matched at 100% up to $2,000 with 25 free spins, the second deposit is matched at 50% up to $1,500 with 25 spins, and the third deposit is matched at 100% up to $1,500 with another 25 spins. Spreading the bonus across three deposits keeps players coming back rather than dumping everything into one session.

For anyone who wants value from day one, ZunaBet has the clear edge here. A $5,000 bonus ceiling gives players real room to explore the library and sportsbook with extra funds backing them up.

Loyalty Rewards: Open vs Invite-Only

Stake runs a closed VIP system. Players are invited based on their activity, and the exact thresholds are not publicly listed. Once you are in, the rewards — rakeback, reload bonuses, and personalized offers — can be significant. But if you are a casual or mid-level player, you may never see the inside of that program.

ZunaBet handles loyalty differently. Its system is themed around dragon evolution and has six named tiers: Squire, Warden, Champion, Divine, Knight, and Ultimate. Rakeback starts at 1% at the lowest level and climbs to 20% at the top. Other perks include up to 1,000 free spins depending on tier, VIP club access, double wheel spins, and a gamified experience built around a dragon mascot called Zuno.

The important distinction is that ZunaBet’s system is transparent and open to everyone from the start. You can see the tiers, see the rewards, and track your own progress. There is no guessing about whether you qualify or waiting for an invitation that may not come. For most players, that openness is more motivating than a mystery system operating behind the scenes.

The Crypto Advantage Over Traditional Operators

Both Stake and ZunaBet sit firmly in the crypto camp, which already separates them from traditional operators like DraftKings, BetMGM, FanDuel, and Caesars. Those platforms were built around bank transfers, credit cards, and regulated fiat currencies. Withdrawals can take days. Fees add up. Payment options are limited by region.

Crypto platforms skip most of that. Transactions are faster, fees are lower, and players have more control over their funds. ZunaBet pushes this further with support for 20+ coins and zero platform processing fees. For players who already live in the crypto world, this is how they expect a gambling platform to work.

Traditional platforms still hold advantages in terms of regulatory trust and brand recognition in markets like the US and UK. But for players outside those tightly regulated markets, or for anyone who simply prefers crypto, platforms like Stake and ZunaBet are the more practical choice.

Where Things Stand

Stake.com has years of trust built up. It has a massive user base, a recognizable brand, and a VIP system that delivers real value to its most active players. If you already know you are going to wager heavily and consistently, Stake rewards that over time.

ZunaBet is making a pitch to everyone else — and doing it well. A generous welcome bonus, a game library with over 11,000 titles, broad crypto support, and a loyalty program that does not hide behind an invite wall add up to a compelling package. It feels built for the current moment, designed for players who grew up with crypto and expect their gambling platform to reflect that.

Stake set the standard for crypto casinos. ZunaBet is showing what the next version of that standard could look like — more games, better upfront value, and a rewards system that treats every player like they matter from the first deposit. For anyone shopping for a new platform in 2026, ZunaBet is the one generating the most buzz right now.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Real day you’re supposed to eat your Easter eggs as many Brits tuck in too early

Bluesky Introduces Agentic AI ‘Attie’ That Delivers Custom Feeds Based on Preferences

Southend colt chases 2026 Champagne Stakes after Baillieu win

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

“This time it’s yo’ money”: Trump’s signature to be added to U.S. paper currency

How and WHAT to invest in! #investing #stockmarket #money #finance #recession #inflation #wallstreet

This Machine Turns Paper into Money! #moneytips #gadgetsshorts #artshorts

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos4 days ago

News Videos4 days agoParliament publishes latest register of MPs’ financial interests

-

Sports7 days ago

Sports7 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Sports7 days ago

Sports7 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat2 days ago

NewsBeat2 days agoThe Story hosts event on Durham’s historic registers

-

News Videos7 days ago

News Videos7 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Business3 days ago

Business3 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Entertainment7 days ago

Entertainment7 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech6 days ago

Tech6 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment1 day ago

Entertainment1 day agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Fashion5 days ago

Fashion5 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

Fashion7 days ago

Fashion7 days agoFringe Bags for the Season

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

NewsBeat5 days ago

NewsBeat5 days agoEntrepreneurs Forum survey reveals optimism in North East

-

Politics6 days ago

Politics6 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

You must be logged in to post a comment Login