Crypto World

Why machine-to-machine payments are the new electricity for the digital age

We are moving toward an economic system in which software and devices transact with one another without human involvement.

Instead of simply executing transactions, machines will be able to make decisions, coordinate with each other and purchase whatever they need in real time. Sensors and satellites will sell data streams by the second. Factories will price power purchases in real-time based on supply and demand. Supply chains could even become completely autonomous — reordering materials, booking transport, paying customs fees and rerouting shipments without any human involvement.

But such an economy cannot be built on large infrequent payments. It needs to run on billions of tiny, continuous transactions, executed autonomously at machine speed. Just as electricity pricing enabled mass production, micro-transactions and machine-to-machine (M2M) payments will make full automation economically viable.

And if continuous M2M payments are the new electricity, then blockchains — the rails upon which these microtransactions will occur — must be seen as the new power grid. They’re a critical piece of infrastructure that unlocks new business models, new technologies and ultimately, this new machine economy.

How will these innovations develop? The electrical revolution has plenty of lessons to teach.

A new revolution

Before electrification, power was local, manual, inconsistent and expensive. Factories relied on steam engines or water wheels, which constrained where production could happen and how it could scale. Power was something you built into each operation.

Electricity changed that. Once power became standardized and always available, it stopped being a feature and became the substrate of modern industry.

Payments today still resemble the pre-electric era of power. They are episodic, usually processed in batches, and heavily mediated by humans and institutions. Even digital payments involve discrete events such as invoices, settlements, reconciliations or billing cycles.

But M2M payments (autonomous financial transactions between connected devices), when combined with micro-transactions (worth a few cents), turn value exchange into something ambient and infrastructure-like. Instead of stopping to pay, machines can simply operate continuously, exchanging value as they consume resources or provide services.

Tech leaders have discussed microtransactions since the early days of the Internet, but it was impossible to realize that vision with the current banking system. Now, blockchain technology enables sending value across the world instantly and at almost no cost. The crypto sector’s infrastructure is fundamental for the birth of continuous M2M payments.

And just as electricity enabled the creation of computers and the Internet, M2M payments and micro-transactions will allow a completely new economy to flourish.

How electricity changed the world

The continuous power provided by electricity enabled automation. Mass production did not happen because factories hired more workers, but because machines could run constantly and relatively independently.

Today’s machines are technically autonomous but economically constrained. An AI agent can make decisions, route traffic, or optimize logistics, but it cannot pay for compute on the fly. Economic friction forces human intervention in systems that are otherwise independent. But M2M payments, combined with micro-transactions, will provide continuous economic power in the same way electricity provides continuous mechanical power.

Also, electricity unlocked industries that simply could not exist before it. M2M payments will have the same property, providing economic infrastructure for industries that cannot function without fine-grained, real-time payments.

What does that look like? We could have autonomous supply chains, in which machines coordinate purchases and logistics continuously. Or we could see the emergence of AI services with pricing models that reflect milliseconds of inference time. Global data markets could depend on pay-per-byte access. Infrastructure itself — from roads to charging stations — could continuously and automatically price access.

It’s worth noting that shifting to usage-based pricing also transformed electricity’s business models. Paying per kilowatt-hour allowed firms to scale without renegotiating contracts or investing in fixed capacity. You paid for what you used when you used it. M2M payments will provide the same flexibility to 21st-century businesses.

Lessons from the electrical revolution

At the beginning of electrification, the focus was mostly on developing generators. However, that wasn’t the most important technological innovation. What mattered was transmission. Only once electricity could be delivered everywhere, cheaply and predictably, did it reshape industry and society.

The same lesson applies to M2M payments. The blockchain rails on which the payments will occur matter way more than the specific M2M payment application (like Coinbase’s x402 protocol) being used. The priority should therefore be to build the best blockchains possible — chains with near-zero fees, very low latency, and predictable performance. In other words, M2M payments hit the same frictions as ordinary stablecoin payments: they need the underlying infrastructure to be tip-top if they want to function properly.

Moreover, the blockchains used for machine payments need to be perceived as neutral infrastructure. They must be interoperable across vendors, jurisdictions and machines. After all, machines cannot negotiate bespoke payment systems any more than appliances can negotiate voltage standards. That means decentralization may play an important role in the growth of the machine economy. In that case, public blockchains could have the advantage over private alternatives.

If M2M payment rails achieve this neutrality, they become the coordination layer of autonomous systems, just as electricity is the coordination layer of physical power. At that point, innovation can safely shift to building entirely new machine-driven industries.

The machine economy will arrive when machines gain the ability to transact continuously, autonomously, and invisibly thanks to the power of blockchain. M2M payments are not just a feature of that future. They are its electricity.

Crypto World

Solana price confirms bearish flag pattern as ETFs break 6-week inflow streak, will it crash?

Solana price fell 13% over the past week after confirming a bearish pattern on the charts. Will it experience a steeper decline ahead as institutional investors seem to be backing away from the asset?

Summary

- Solana price dropped over 13% in a week after confirming a bearish flag pattern, signaling potential continuation of the downtrend.

- Institutional outflows from Solana ETFs and derivatives-driven liquidations have added to selling pressure, weakening investor sentiment.

- Technical indicators point to further downside risk toward $67, with a break below $80 likely to accelerate losses.

According to data from crypto.news, Solana (SOL) price fell 13.5% from its weekly high of $92.88 to $80.37 earlier on Monday before settling a little above at $84.07 at the time of writing.

Solana price fell as institutional investors began rotating capital away from the token, likely as they explored other options. Data from SoSoValue shows that spot Solana exchange-traded funds recorded $4.24 million in outflows over the past week, breaking a six-week weekly inflow streak that drew in nearly $127 million from the investment products.

While this recent cooling doesn’t necessarily mean that institutional investors will continue to back off from the asset in the weeks ahead, they have certainly spooked retail investors into a cautious state as they await clearer market signals.

Another major reason that has set back the token is the persistent liquidations across crypto derivatives markets. Over the past 24 hours, over $24 million in positions were liquidated from Solana alone, with the majority coming from long liquidations. As these positions were wiped out, the resulting selling pressure further accelerated the decline.

Meanwhile, the ongoing uncertainty around when the war between the U.S. and Iran would come to an end has also fostered a cautious environment for investors who are rotating to gold and other safe-haven assets that have historically protected capital during geopolitical crises.

On the daily chart, Solana price has confirmed a multi-month bearish flag pattern. Such a pattern is formed when an asset drops sharply downwards, forming a flagpole followed by some consolidation forming the flag part of the pattern.

A break from the lower trendline of the pattern confirms the bearish outlook and has often preceded a significant downward move.

Hence, Solana price is likely to visit its year-to-date low of $67.82 reached on Feb. 6. On the bearish side, if Solana price loses the $80 support level, the selloff could intensify quickly.

Technical indicators seem to support this bearish outlook. Notably, the Aroon Down stood at 92.86% while the Aroon Up was at 0%, a sign that the bears are in total control of the trend.

The Relative Strength Index, which shows the RSI at 44 slowly climbing back toward the neutral threshold, suggests that while the immediate panic has subsided, the overall momentum remains weak.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Prospects of interest rate rises are no longer just the U.S. story. Traders are now betting the Bank of Japan (BoJ) could tighten too as the resource-scarce nation faces inflation risks from the ongoing Iran war.

Traders see a roughly 69% chance of the BoJ raising its benchmark borrowing cost at the April 28 meeting, according to data tracked by Bloomberg. Action in options tied to U.S. interest rates shows traders expect the Fed to raise borrowing costs in the coming weeks.

BoJ’s policy meeting summary released Monday showed one member calling for a bigger rate hike in response to the conflict in the Middle East and its inflationary impact on Japanese society. Comments also noted that any move would factor in incoming economic data and anecdotal signals from the market.

The Fed’s tightening is a well-known headwind for risk assets, including bitcoin. The Bank of Japan can be just as impactful. Years of ultra-low rates encouraged traders to borrow in yen and invest in higher-yielding markets (the so-called carry trade), keeping borrowing costs suppressed globally and greasing rallies in risk assets.

So, a shift toward tighter policy in Tokyo could reverse these flows, sending ripples across markets and potentially deepening the crypto bear market. The BoJ has already raised its interest rate to 0.75% from -0.1% over the past two years while simultaneously ending its massive asset purchase program. Yet, rates in Japan remain significantly lower than the 3.5% seen in the U.S.

The bank, therefore, has plenty of room to hike if the Iran crisis worsens, potentially driving higher energy prices and imported inflation in Japan and other oil-dependent countries.

Easier said than done

Hiking rates, however, will be a challenging task given Japan’s strained fiscal situation. The country’s debt-to-GDP ratio stands at a staggering 240%, meaning higher rates could sharply increase borrowing costs and strain government finances.

Economists have said that Japan is caught between a rock and a hard place. If it hikes rates and allows government bond yields to rise, it could put Japan’s debt sustainability at risk. If it keeps rates low, the yen will likely depreciate significantly, adding to inflation concerns.

Strains are already evident in the FX market. The Japanese yen continues to weaken and is currently just around 160 per U.S. dollar, its weakest level since mid-2024. The JPY has depreciated by 54% since 2021.

South Korea’s Naver Financial has delayed plans for its share swap with crypto exchange Upbit’s parent firm Dunamu.

Summary

- Naver Financial has delayed its share swap with Dunamu by nearly three months, with a shareholder vote set for Aug. 18 and completion now expected on Sept. 30.

- The deal remains subject to regulatory approvals and could face further delays or cancellation, with South Korea’s Digital Asset Basic Act also likely to influence the timeline.

According to a regulatory filing with the country’s Financial Supervisory Service, Naver said it will hold a shareholder vote on Aug. 18, following which it will complete the transaction on Sept. 30.

With the new timeline, the deal has now been delayed by nearly three months from earlier target dates of late May or early June.

While the company did not disclose the reason behind the delay, it said the deal remains subject to multiple regulatory approvals tied to changes in major shareholding and business combination review. It added that the transaction could be subject to further delays or cancellation depending upon how the approval process unfolds.

The deal may also be impacted by South Korea’s proposed Digital Asset Basic Act, which is expected to be implemented in the first half of 2026.

The planned legislation is the second phase of the country’s crypto regulatory framework and is set to expand beyond the current user protection regime to put in place a broader rulebook for the digital asset sector.

In the meantime, Dunamu has reported weaker operating performance, with its revenue and profit both falling in 2025 as market activity across the crypto market has slowed.

Per its annual filing, the company posted a 10% year-on-year decline in revenue, while its operating profit fell 26.7% and its net profit fell 27.9%.

Naver Financial first disclosed plans to acquire Dunamu last year, with local media reporting at the time that the company was preparing a share swap to bring the Upbit operator under its umbrella. The deal was subsequently confirmed in November as a roughly $10.3 billion all stock deal.

Around the same time, the company also announced plans to launch a stablecoin wallet service in collaboration with blockchain investment firm Hashed and the Busan digital exchange. As previously reported by crypto.news, the companies plan to develop a wallet named “Silk Pocket.”

Uniswap’s governance token is holding on and looking good. UNI crypto is now priced at $3.50, with a healthy 4.5% intraday gain. However, the real story is structural, with centralized exchanges clawing back relevance in a recovering market, and UNI sits at a critical technical junction that will define its next $1 move in either direction.

The CEX versus DEX debate has sharpened considerably in early 2026. Kraken’s anticipated IPO is positioning the exchange as the compliance gold standard, while Coinbase continues to dominate retail onboarding. Uniswap v4, meanwhile, is competing as a programmable liquidity layer rather than a simple swap venue, a pivot that changes its valuation calculus entirely.

The question now is whether crypto’s recovery provides a second attempt or whether UNI fades further.

Discover: The best crypto to diversify your portfolio with

Can UNI Crypto Price Reclaim $4 Before April?

UNI is consolidating inside a $3.10–$3.95 range, with moving averages stacked in mild bearish alignment. The 7-day SMA sits at $3.71, the 20-day at $3.83, and the 50-day at $3.68, all above the current price.

An analyst, Tony Kim, set a slightly more aggressive target earlier this month: “Potential move toward $4.22 resistance if current support levels hold through March.”

In a bull scenario, daily volume breaks above $5.2M, RSI pushes past 53, and UNI reclaims the $3.7 50-day SMA, opening a run toward $4.15.

However, the bear can argue that there could be an invalidation. A close below $3.3 flips short-term structure negative, potentially dragging price toward the $3.25 weekly low f

Discover: The best pre-launch token sales

LiquidChain Targets Early-Mover Upside as Uniswap Tests Key Levels

UNI at $3.50 offers a known asset at compressed valuation, but with the 200-day SMA at $5.85 as a realistic ceiling, the upside math is bounded. Early-stage infrastructure presales offer a different risk profile entirely.

LiquidChain is positioning itself as a Layer 3 cross-chain liquidity layer, fusing Bitcoin, Ethereum, and Solana liquidity into a single execution environment, a direct infrastructure play on the fragmentation problem that makes multi-chain trading expensive and slow.

A new layer emerges. Only a few see it first. — LiquidChain (@getliquidchain) March 24, 2026

The future is LiquidChain  ⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

The project’s Unified Liquidity Layer and Deploy-Once Architecture mean developers write once and access all three ecosystems simultaneously, reducing the bridging friction that has historically hemorrhaged value from DEX traders.

The presale is currently priced at $0.0144, with more than $600K raised to date. Liquid also offers a huge 1700% APY as staking rewards, and launched with a Certik audited contract.

This article is not financial advice. Crypto assets are highly volatile. Always conduct your own research before investing.

The post UNI Crypto Prediction: CEX Resurfaced as Crypto Recovers appeared first on Cryptonews.

Crypto World

Advanced Micro Devices (AMD) Stock: Aletheia Capital Projects 63% Rally on AI Infrastructure Boom

Key Highlights

- Aletheia Capital maintains Buy recommendation on AMD with $330 price objective

- Server CPU revenues expected to expand at 45% CAGR through 2028

- Data center business projected to surge from $17B in 2025 to $77B by 2028

- Company has evolved into comprehensive AI compute solutions provider

- CEO Lisa Su joins Trump administration’s science and technology advisory council

Advanced Micro Devices ($AMD) continues to attract bullish sentiment from Wall Street analysts, with Aletheia Capital maintaining its Buy recommendation and establishing a $330 price objective for the chipmaker. Trading at $201.99, the stock presents substantial appreciation potential based on the firm’s analysis.

Advanced Micro Devices, Inc., AMD

The investment case from Aletheia focuses heavily on AMD’s positioning within the emerging agentic AI landscape. The research firm contends that central processing units — rather than solely graphics processing units — represent the optimal semiconductor architecture for agent-based computational tasks, positioning AMD favorably to capitalize on this shift.

Aletheia’s financial projections anticipate AMD’s server CPU business will achieve a remarkable 45% compound annual growth rate spanning 2025 through 2028. This aggressive expansion forecast forms the foundation of the firm’s optimistic outlook.

Regarding data center operations, the analyst firm forecasts revenue climbing from $17 billion in 2025 to $58 billion by 2027, ultimately reaching $77 billion in 2028. This trajectory represents approximately 4.5-fold growth over a three-year period.

Aletheia employed a sum-of-the-parts methodology to derive its $330 valuation. For comparison, InvestingPro’s Fair Value analysis places AMD at $225.24, which still exceeds current trading levels.

The company delivered 34% revenue growth over the trailing twelve months. This performance validates the thesis that AMD is capturing increased market share within the AI computing sector.

Aletheia’s perspective on AMD has broadened beyond viewing the company as merely an alternative GPU supplier. The firm now characterizes AMD as a “comprehensive AI compute provider” — terminology that underscores the company’s strategic transformation.

However, the firm acknowledged several risk factors including end market demand volatility, execution challenges, and geopolitical uncertainties. These considerations carry significant weight given current macroeconomic conditions.

Wall Street Consensus Strengthens

Wolfe Research similarly maintains an Outperform stance on AMD with a $300 price objective. The firm emphasized AMD’s conviction in its AI accelerator development timeline and sustained server market traction.

Seaport analyst Jonathan Golub observed that semiconductor sector valuations, including AMD’s multiple, have contracted since July. He interprets this compression as creating attractive entry opportunities.

Corporate Updates and Strategic Moves

AMD and Celestica unveiled the Helios rack-scale AI platform designed for data center infrastructure applications. This collaboration capitalizes on Celestica’s engineering and production expertise.

The company also finalized a multi-year licensing arrangement with Adeia Inc. This agreement provides AMD access to Adeia’s semiconductor intellectual property library while settling all pending legal disputes between the parties.

CEO Lisa Su secured an appointment to President Trump’s Council of Advisors on Science and Technology. This role positions her among influential leaders guiding U.S. technology and scientific policy direction.

AMD communicated concerns regarding its client computing and gaming divisions due to escalating memory component costs. These segments have demonstrated weaker performance relative to the robust data center business.

InvestingPro designates AMD as a “prominent player in the Semiconductors & Semiconductor Equipment industry.” The stock declined 0.87% during the trading session at time of publication.

Brent crude oil just posted its biggest monthly price gain on record, 51% since the opening day of the month, and crypto traders are watching both the oil chart and their crypto positions simultaneously before making any prediction.

Bitcoin rebounded 2% intraday to $67,000 even as oil shockwaves rattled equities, raising a question active traders are increasingly asking: is the real opportunity in oil, crypto, or something built on top of both narratives? The answer depends heavily on what happens in the Strait of Hormuz over the next 72 hours.

Brent closed Friday at $112.57 per barrel, up from $72.48 on February 27, the day before the US-Israeli strike on Iran, and briefly tagged $119.50 intraday, its highest since June 2022. BloombergNEF estimates 9 million barrels per day have been knocked offline by the conflict, with Iran all but closing the Strait of Hormuz, through which roughly one-fifth of global oil and gas normally flows.

A coordinated 400-million-barrel emergency reserve release on March 11 barely dented the rally. Trump’s 10-day ultimatum to Iran to reopen the strait was met by a rising oil price and falling stock markets, not exactly the negotiating leverage the White House projected.

Total crypto market capitalization has reached $2.4 trillion despite the macro turbulence, suggesting digital assets are absorbing the geopolitical shock. The macro correlation between Treasury yields, risk assets, and crypto is tightening, and oil is now the single most consequential variable in that equation.

Discover: The best crypto to diversify your portfolio with

Oil Price Prediction: Will Oil Blast Pass $200?

WTI crude surged above $110 per barrel on March 9 and has held elevated since, with 10-year futures still pricing around $57 per barrel, a signal that markets expect eventual normalization but have no timeline for it.

Bitcoin is currently trading in a defined $62,000–$73,000 channel. Resistance sits at $73,000, tested and rejected recently; support is intact at $62,000. The brief touch of $74,000 before the pullback signals buyers are present at highs, but conviction is thin.

Rising import prices, up 1.3% in February, combined with oil above $110, are the inputs feeding that rate-hike probability. Watch Tuesday’s API Crude Oil Stocks and ADP Employment data as the next directional catalysts.

Once the Strait of Hormuz opens for business, oil will likely start to normalize. Is this the time to long oil? The answer lies more in geopolitics right now, not much in chart structure.

Discover: The best pre-launch token sales

Bitcoin Hyper is Targeting A movement Similar to Oil

BTC at $67,000 inside a known range is a respectable position, but at this market cap, the asymmetric upside that early crypto cycles delivered is structurally compressed.

The Iran deadline extension is already weighing on risk assets, and spot BTC traders are essentially betting on a macro resolution they cannot control. For traders hunting for leverage on the Bitcoin ecosystem without the channel ceiling, the infrastructure layer is where some rotation is happening.

Bitcoin Hyper ($HYPER) is positioning as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, combining Bitcoin’s security model with sub-Solana-speed execution and low-cost smart contracts.

The presale has raised $32 million at a current price of just $0.0136, with 36% staking rewards live for early participants. The core pitch: Bitcoin’s programmability problem (slow transactions, high fees, no native smart contracts) gets a direct fix, while the security layer stays intact.

Research Bitcoin Hyper before the presale window closes.

This article is not financial advice. Crypto assets are highly volatile. Do your own research before investing.

The post Oil Price Prediction: Trading Oil With Crypto? Is It Time to Long Oil? appeared first on Cryptonews.

Bitcoin (BTC) buyers made a tepid comeback on Monday, pushing BTC price to its intraday high of $67,860. Analysts said that Bitcoin remains in a bear market, with several metrics pointing to a potential bottom below $50,000.

Key takeaways:

-

Bitcoin price turns $70,000 into resistance, clearing the path for a deeper correction.

-

Bitcoin’s short-term holder realized price bands moved lower, with a potential bottom around $46,000.

-

Historical retracement levels and a bear flag breakdown point to $39,000–$41,000 as the final low for BTC price this cycle.

Bitcoin’s “path of least resistance” is downward

Data from TradingView captured ongoing BTC price gains, up 1.5% on the day to trade at $67,750, as $69,000-$70,000 became new resistance.

Analyzing Bitcoin’s price action on lower time frames, Telegram trading resource Technical Crypto Analyst said losing the $68,000-$69,000 support “confirms short-term bearish momentum,” adding:

“Unless price quickly reclaims $69K–$70K, the path of least resistance remains downward toward the $65K demand zone.”

Related: Worst six months since 2018? Five things to know in Bitcoin this week

“Great bounce upwards, but nothing confirmed as of yet on Bitcoin,” MN Capital founder Michael van de Poppe said in a Monday post on X.

It “all depends on macroeconomic events; however, I’d rather see a breakout above $71K for confirmation,” he added.

“On the other hand, a classic little sweep to $65K just before the push upwards would signal that we’re going to get that momentum.”

Analyst Kyle Chassé said that with the Fear and Greed index still in the “extreme fear zone” and the order books showing more shorts than longs, the market leans “towards more downside.”

Where will the Bitcoin price bottom?

Bitcoin’s 46% drawdown from its $126,000 all-time high has seen the cost basis of short-term holders (STH) — the average price of entities who have held BTC for less than 155 days — drop from $113,500 to $83,200.

“This is a sign that the pricing for a potential bottom has also moved lower,” said CEO and founder at Alphractal Joao Wedson in an X post on Monday.

Similarly, the lower line of the STH realized pricing bands (blue line) has also moved “even lower, which could confirm that Bitcoin may form a bottom around $50K or slightly below,” Wedson added.

The chart below shows that Bitcoin bottomed out just below the lower band of the STH realized price during the 2022 bear market.

Analyst Willy Woo said that the bear market bottom for Bitcoin could be between its realized price, currently at $54,000, and the Cumulative Value-Days Destroyed (CVDD), now at $45,500.

“Old school onchain models suggest a BTC bottom between $46K-54K. ”

The CVDD measures the cumulative value of “Coin Days Destroyed” (long-term holders selling) relative to the market’s age, creating a rising “floor” price during bear markets.

Crypto analyst Crypto Jelle said Bitcoin’s bear market lows have historically formed between the 0.618 and the 0.786 retracement levels, which are at $57,600 and $39,000, respectively.

As Cointelegraph reported, the current “last stages” of the bear market are producing predictions of as low as $41,000, based on a bear flag breakdown.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Morgan Stanley is preparing to launch a Bitcoin ETF with a 0.14% fee, undercutting major competitors. The fund aims to compete directly with BlackRock’s IBIT dominance. The listing progress suggests a likely April debut as competition intensifies.

Key Highlights

- Morgan Stanley sets 0.14% fee to rival BlackRock’s Bitcoin ETF dominance

- MSBT filing signals aggressive pricing strategy ahead of April launch

- Low-cost structure may attract both advisors and external capital flows

- ETF approval progress points to imminent debut on NYSE Arca exchange

- Bank expands crypto push with filings for Ethereum and Solana ETFs

🚨LATEST:

$1.9 trillion Morgan Stanley to offer Bitcoin ETF with 0.14% fee, cheapest in the market if approved. pic.twitter.com/8h5XLiMSAO

— CryptoGoos (@cryptogoos) March 28, 2026

Bitcoin ETF Pricing War Intensifies

Bitcoin traded near $67,000 during the latest session, reflecting ongoing market volatility and uneven ETF flows. Morgan Stanley positioned its ETF with a 0.14% management fee, placing it below most competitors in the current market.

The fee undercuts BlackRock’s IBIT, which charges 0.25%, and slightly beats Grayscale’s Mini Bitcoin Trust. As a result, the pricing strategy signals a direct challenge to established leaders. It also reinforces growing competition among issuers seeking market share.

Bloomberg analyst Eric Balchunas described the move as strategic and timely. He noted that lower fees could remove internal friction among advisors. Additionally, the structure could attract external allocations due to cost efficiency.

Morgan Stanley Expands Crypto Strategy

Morgan Stanley has steadily increased its exposure to digital asset products in recent years. The firm already allows client allocations to Bitcoin related funds through advisory channels. This ETF marks its first direct issuance in the spot Bitcoin ETF market.

The bank manages trillions in advisory assets and maintains a large network of financial advisors. Therefore, the ETF launch could unlock significant distribution potential. It also positions the firm as a direct competitor rather than a facilitator.

James Seyffart highlighted the broader implications of the pricing decision. He suggested that similar fee reductions could apply to future products. The firm has already filed for Ethereum and Solana ETFs, signaling continued expansion.

Launch Timeline and Market Context

The ETF has secured a listing on NYSE Arca, which often signals an imminent launch window. Current expectations point to a debut within weeks, possibly in April. This timeline aligns with regulatory progress and final preparation stages.

Bitcoin ETF flows have shown mixed patterns amid recent price weakness. Some funds have recorded outflows, while others maintain steady inflows. Despite this trend, new entrants continue to pursue market share through aggressive pricing.

Morgan Stanley’s entry stands out due to its scale and distribution reach. The firm operates a large advisor network managing substantial client assets. Consequently, its ETF could influence allocation trends within traditional wealth channels.

The broader ETF market has evolved rapidly since initial approvals earlier in the year. Large asset managers have dominated early inflows, led by BlackRock. However, new issuers now compete through differentiation, mainly via fees.

Morgan Stanley’s approach reflects this shift toward cost leadership and accessibility. Lower fees reduce barriers for adoption and improve long term competitiveness. This strategy may reshape pricing standards across future crypto ETFs.

South Korea’s Naver Financial has pushed back the timeline for its planned share swap with Dunamu, the operator of crypto exchange Upbit, according to a regulatory filing posted on Monday.

In a filing with the Financial Supervisory Service (FSS), the company said it expects to hold a shareholder vote on Aug. 18 and complete the transaction on Sept. 30, marking a roughly three-month delay from earlier target dates of late May or early June.

Naver Financial’s plans to acquire Dunamu were first revealed in September 2025, as local news agencies Yonhap and Chosun reported the company was preparing a share swap to bring the Upbit operator under its umbrella. The company later confirmed the transaction in a Nov. 26 regulatory filing, outlining a roughly $10.3 billion all-stock deal.

The transaction is part of Naver Financial’s plan to bring Dunamu under its umbrella as a wholly owned subsidiary. The transaction would combine one of South Korea’s biggest fintech platforms with the operator of its biggest crypto exchange, making it one of the country’s most consequential crypto-finance tie-ups.

Digital Asset Basic Act could affect the deal’s outcome

Naver Financial’s FSS filing also outlined that the deal remains subject to multiple regulatory approvals tied to changes in major shareholding and business combination review.

Naver said the transaction could be delayed further or even canceled depending on the progress of approvals.

It also said ongoing discussions around South Korea’s proposed Digital Asset Basic Act could affect the timeline or outcome once the legislation is enacted.

South Korea’s proposed Digital Asset Basic Act is a planned second-phase crypto law meant to go beyond the current user-protection regime and create a broader rulebook for digital assets. The legislation is expected to be rolled out in the first half of 2026.

Related: Upbit hit with $36M Solana hot wallet breach day after $10B Naver deal

Dunamu profit declines as crypto trading volumes fall

The pushed-back timeline comes as Dunamu reported a decline in operating performance, with revenue and profit both falling in 2025 amid weaker activity in the crypto market.

According to its annual report filed with the FSS, the company posted revenue of about 1.56 trillion won (around $1 billion), down 10% year-on-year. Operating profit fell 26.7% to 869.3 billion won (around $573.3 million), while net profit fell 27.9% to 708.9 billion won (around $467 million).

The company attributed the decline to reduced trading volumes during a broader slowdown in the crypto market.

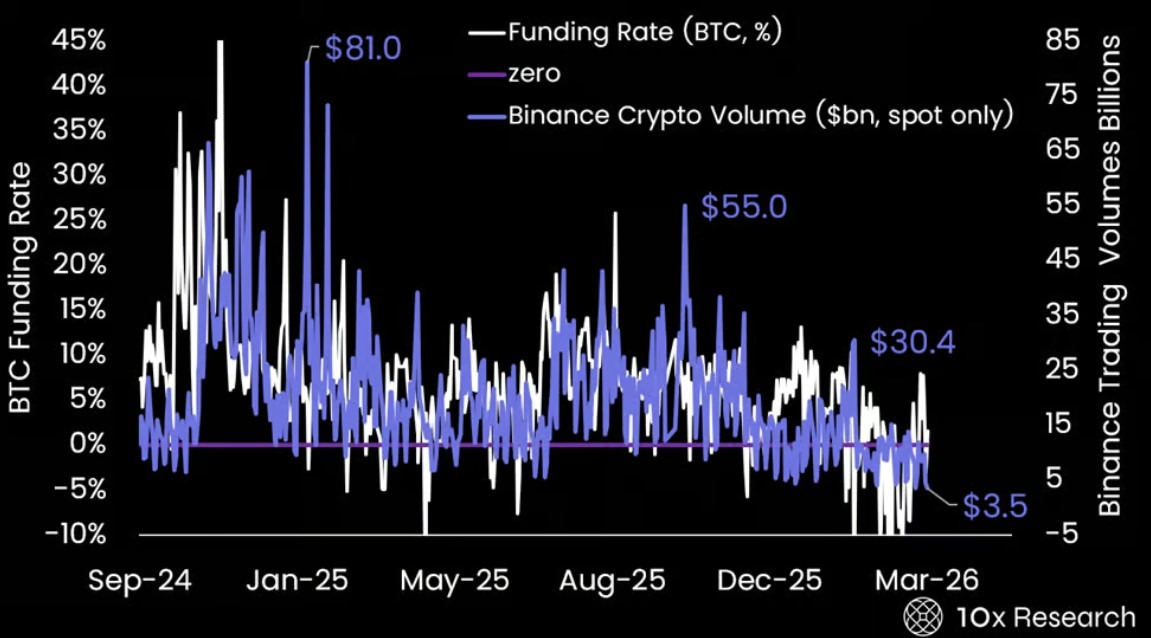

According to research firm 10x Research, trading volumes recently fell to their lowest levels since 2022, with total weekly volume down about 7% from average and network usage indicators such as Ethereum fees signaling subdued demand.

Magazine: Hong Kong isn’t the loophole Chinese crypto firms think it is

The decentralized finance (DeFi) revolution promised a financial system without banks, borders, or gatekeepers. And to be fair, it delivered. Today, anyone with an internet connection can lend, borrow, trade, and earn yield through blockchain-based protocols.

But here’s the uncomfortable truth: most of DeFi ended up optimizing for profit… not purpose.

Enter ImpactFi—the evolution of DeFi that merges financial returns with real-world social and environmental impact. It’s not just about making money anymore; it’s about making money matter.

What Is ImpactFi?

ImpactFi sits at the intersection of DeFi and impact investing.

Impact investing itself focuses on generating measurable social or environmental benefits alongside financial returns.

Now combine that with blockchain—and you get a transparent, programmable, and decentralized system that aligns capital with global impact.

In simple terms:

ImpactFi = DeFi + Purpose

Instead of yield farming for pure profit, users can now earn while funding renewable energy, education, healthcare, or climate initiatives.

Why Traditional Finance Fell Short

Before ImpactFi, impact investing faced several bottlenecks:

- High entry barriers (big money only)

- Slow decision-making

- Lack of transparency

- Limited community involvement

Even with trillions flowing into the sector, capital distribution remained inefficient and often disconnected from the communities it aimed to serve.

ImpactFi fixes this—with code.

The Core Pillars of ImpactFi

1. Transparency Through Blockchain

Every transaction, allocation, and outcome is recorded on-chain.

No more vague “impact reports.”

No more “trust us” fund managers.

With blockchain:

- You can verify where funds go

- Track outcomes in real time

- Audit impact metrics transparently

This solves one of the biggest issues in traditional impact investing—accountability.

2. Smart Contracts = Automated Impact

Smart contracts power DeFi by executing agreements without intermediaries. ImpactFi takes this further.

For example:

- A portion of the yield is automatically redirected to climate projects

- Donations are triggered by on-chain events

- Funds are released only when impact milestones are met

This creates programmable philanthropy—no human bias, no delays.

3. Community Governance via DAOs

ImpactFi platforms often use DAOs (Decentralized Autonomous Organizations).

Instead of a centralized fund manager:

- Investors, communities, and stakeholders vote on decisions

- Governance tokens give real influence

- Funding decisions are democratized

This flips the script:

The people affected by investments finally have a say in them.

4. Impact Yield Farming

A standout innovation is impact yield farming.

Traditionally:

- You stake → you earn rewards

In ImpactFi:

- You stake → you earn and fund real-world impact

Some protocols even split yields:

- Part goes to the user

- Part goes to social/environmental causes via smart contracts

It’s like earning passive income… with a conscience.

5. Financial Inclusion at Scale

DeFi already removes intermediaries, making finance accessible globally.

ImpactFi extends this by:

- Funding underserved communities

- Supporting microfinance through decentralized systems

- Enabling grassroots participation in investment decisions

This is where things get powerful:

ImpactFi doesn’t just redistribute wealth—it redistributes opportunity.

How ImpactFi Is Changing DeFi Itself

ImpactFi isn’t just a niche—it’s reshaping the entire DeFi narrative.

From Speculation → Sustainability

DeFi has often been criticized for being overly speculative. ImpactFi introduces long-term, mission-driven capital allocation.

From Whales → Communities

Governance is shifting from large token holders to broader stakeholder groups via DAO models.

From Yield → Purpose

Yield is no longer the only KPI. Now we measure:

- Carbon offset

- Social impact

- Community development

Real-World Use Cases

ImpactFi is already being applied in:

- 🌱 Climate finance (carbon credits, reforestation)

- 🏥 Healthcare funding in underserved regions

- 📚 Education access through decentralized grants

- 🌍 Local economic development via community DAOs

Blockchain even enables faster capital flow by simplifying the verification and tracking of outcomes.

Challenges (Because Nothing Is Perfect)

Let’s not pretend this is all sunshine and green candles:

- Impact measurement is still evolving

- Regulatory uncertainty remains

- Greenwashing risk exists (yes, even on-chain)

- User experience is still… very crypto

But compared to traditional systems?

ImpactFi is already leagues ahead in transparency and efficiency.

The Future of ImpactFi

The impact investing market is projected to grow massively in the coming years, and decentralized models are accelerating that shift.

We’re heading toward a world where:

- Every transaction has a traceable impact

- Capital allocation is community-driven

- Financial systems are aligned with global sustainability goals

In other words:

Finance stops being neutral—and starts being intentional.

Conclusive

ImpactFi is what happens when DeFi grows up.

It keeps the best parts—permissionless access, transparency, automation—and adds something DeFi desperately needed:

a reason beyond profit.

And if DeFi was about removing middlemen…

ImpactFi is about removing meaninglessness.

REQUEST AN ARTICLE

Form 424B5 Trio Petroleum Corp For: 30 March

Solana price confirms bearish flag pattern as ETFs break 6-week inflow streak, will it crash?

3 Behaviours Split Those Who Live Long From Those Who Don’t

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos4 days ago

News Videos4 days agoParliament publishes latest register of MPs’ financial interests

-

NewsBeat3 days ago

NewsBeat3 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Entertainment7 days ago

Entertainment7 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment2 days ago

Entertainment2 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

NewsBeat7 days ago

NewsBeat7 days agoColombian military plane with 110 soldiers onboard crashes following takeoff

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

NewsBeat6 days ago

NewsBeat6 days agoEntrepreneurs Forum survey reveals optimism in North East

-

Politics7 days ago

Politics7 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

Crypto World6 days ago

Crypto World6 days agoBTC gives up $70,000 level as markets mull higher interest rates

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

Fashion6 days ago

Fashion6 days agoCoffee Break: Korean Skincare Set

-

Fashion6 days ago

Fashion6 days agoAlthea Mink: Patrice Taylor’s Atlanta Couture Brand Built on Legacy, Resilience, and Architectural Glamour

-

Tech5 days ago

Tech5 days agoUS FCC Prohibits Approval Of New Foreign-Made Consumer Routers

You must be logged in to post a comment Login