Crypto World

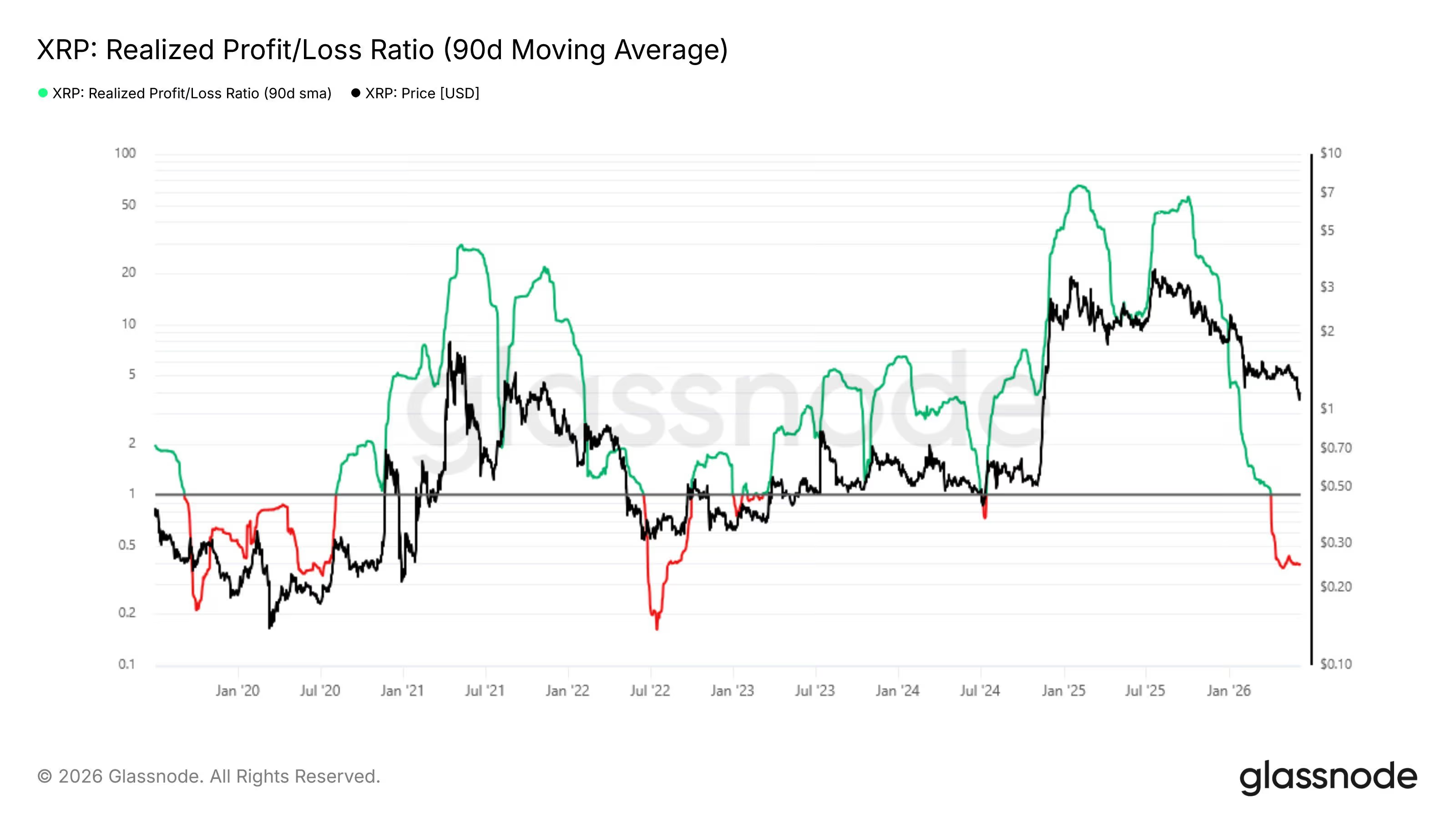

XRP market shows signs of capitulation as holders sell at loss

XRP holders are increasingly selling at a loss in a textbook sign of market capitulation.

The 90-day moving average of XRP’s realized profit-to-loss ratio has plunged to 0.38, according to data tracked by Glassnode.

That means for every $1 of losses investors are realizing right now, they are taking in just 38 cents in profit. Essentially, most of the coins trading on the blockchain are underwater.

The situation marks a reversal from the 2025 peak, when the ratio hit 50. At that time, profit-takers were overwhelming loss-sellers by a staggering 50-to-1.

A ratio this far below 1 is widely viewed as a hallmark of capitulation, a market phase where exhausted holders finally throw in the towel and sell, often after bearing the prolonged pain of holding coins in loss. It reflects intense fear or forced selling in the market.

While capitulation doesn’t always mark the exact bottom, it frequently appears near exhaustion points in downtrends. For XRP traders, this could mean that the bear market is in its final stages.

The payments-focused cryptocurrency traded at around $1.11 at press time, down nearly 40% for the year, according to CoinDesk data. Prices peaked above $3.60 last July.

White House crypto adviser Patrick Witt criticized banking leaders seeking tighter stablecoin reward restrictions as Senate delays pushed the CLARITY Act’s passage odds to a record low.

Summary

- 134 banking executives and leaders urged senators to expand restrictions on stablecoin rewards and incentives.

- Witt accused banks of opposing legislation that already prohibits stablecoin issuers from paying interest.

- Polymarket traders cut the bill’s 2026 passage odds to a record-low 27%.

- Senate scheduling decisions have narrowed the window for action before the Aug. 8 recess.

Patrick Witt challenges banks over CLARITY Act

Witt pushed back after 134 banking executives and industry leaders sent Senate lawmakers a letter seeking changes to Section 10404 of the CLARITY Act.

The section restricts issuers from paying interest or yield on payment stablecoins. Banking groups want lawmakers to extend the restriction to rewards, bonuses and other incentives offered by stablecoin firms or their partners.

Witt framed the request as inconsistent with the industry’s wider opposition to the market structure bill.

“Banks: We must ban the payment of interest on stablecoins to protect community bank lending!.”

He then noted that the CLARITY Act already bans interest payments before criticizing banks that still warn the bill could damage community lending.

His comments targeted the difference between banks’ support for an interest ban and their objections to other parts of the legislation. Bank representatives maintain that the existing language may leave room for stablecoin platforms to offer benefits with the same economic effect as interest.

Why banks want a wider stablecoin reward ban

Signatories included leaders tied to Bank of America, U.S. Bank, Zions Bank, First Hawaiian Bank, Bank of Hawaii, Hancock Whitney Bank, FNBO, Eastern Bank, Lake City Bank and Univest Financial Corporation.

The group said payment stablecoins should function as transaction tools rather than long-term savings products. It warned that rewards linked to a user’s balance or holding period could encourage customers to move money out of insured bank accounts.

Banking leaders claimed that large deposit outflows could reduce the funding available for lending to households, farmers, small businesses and local employers. They estimated that the effect could drain hundreds of billions of dollars from the traditional banking system.

Goldman Sachs CEO David Solomon has taken a different position by supporting the CLARITY Act. His stance separates the investment bank from groups demanding tighter stablecoin provisions before the Senate moves forward.

The debate has direct implications for US stablecoin users. Broader restrictions could limit the rewards that exchanges and other service providers offer, even when stablecoin issuers do not pay interest directly.

CLARITY Act odds fall to a record-low 27%

The banking dispute comes as the CLARITY Act faces a shrinking Senate calendar. Polymarket traders have reduced the probability that the legislation becomes law in 2026 to 27%, its lowest recorded level.

Galaxy Digital has separately lowered its passage estimate to 30% as negotiations extend deeper into the legislative year.

Senate Republicans recently released an updated 616-page draft combining texts from the Senate Banking and Agriculture committees. The framework would place digital commodity spot markets under the Commodity Futures Trading Commission while allowing the Securities and Exchange Commission to oversee investment contract assets.

It also includes protections for certain software developers, blockchain developers and decentralized networks that do not control customer assets. White House-backed ethics provisions would restrict digital asset issuance involving federal officials and their spouses.

Senate delay leaves little time before recess

Senate Majority Leader John Thune postponed CLARITY Act action while lawmakers considered federal nominees and the Lindsey O. Graham Sanctioning Russia Act of 2026. Senators voted on July 28 to advance the sanctions package, leaving fewer working days before the Aug. 8 recess.

Crypto industry participants have urged Thune to begin the cloture process before lawmakers leave Washington, even if a final vote cannot occur. A procedural vote would test whether the bill has enough bipartisan support to overcome Senate hurdles later in 2026.

Failure to begin that process would push the legislation further into an already crowded calendar. Stablecoin reward rules remain one of the issues lawmakers must resolve before the broader US crypto market structure framework can advance.

Crypto World

Federal Reserve holds rates steady, extending pause as markets await Warsh’s policy roadmap

The Federal Reserve left its benchmark fed funds rate range unchanged at 3.50%-3.75% on Wednesday, extending its pause for a sixth consecutive meeting as policymakers continue to grapple with stubborn inflation.

“Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy,” the policy statement read.

“Economic activity is expanding at a solid pace despite elevated uncertainty that owes, in part, to the conflict in the Middle East. Productivity growth and capital investment are strong,” the statement added. “Job gains have kept pace with the workforce, and the unemployment rate has changed little.”

There were three committee members dissenting, preferring to raise rates by 25 basis points. Nine voted to keep policy in place.

Bitcoin climbed to above $64,400 following the decision, up over 1% over the past 24 hours. The S&P 500 and Nasdaq bounced, trimming earlier declines. Gold also rose, up 1.2% through the day.

The decision came after one of the most uncertain pre-meeting setups in years. Futures markets had assigned roughly a 65% probability to a hold and 35% odds of a quarter-point increase, according to CME FedWatch data.

1inch has moved its Aqua liquidity protocol from developer preview to full public release, covering 13 EVM-compatible networks simultaneously, a scope that puts it in direct contact with most of the chains where professional market makers and retail liquidity providers already operate.

The launch addresses one of DeFi’s most persistent structural problems: capital that sits idle across fragmented pools on separate chains, earning suboptimal yields and forcing providers to manage positions across incompatible interfaces.

Discover: The Best Crypto to Diversify Your Portfolio

How Aqua’s Registry Model Differs from Standard AMMs

Aqua does not use conventional pool deposits. Instead, it operates on a registry-based allowance model: a liquidity provider registers a wallet balance as backing, and that balance can support multiple simultaneous quoted positions without the assets leaving custody.

A swap executes only when it matches the position’s stated terms, at which point the protocol pulls the required assets directly from the provider’s wallet.

Liquidity providers: it’s time to wake up. — 1inch (@1inch) July 28, 2026

Use 1inch Aqua to find more activity in more markets, without letting your tokens out of your wallet.

Risk-controlled execution meets full self-custody.

No, you aren’t dreaming.

Here’s how it works: pic.twitter.com/F7CJeikteJ

pic.twitter.com/F7CJeikteJ

The capital efficiency implication is significant in theory. According to the research context, 1inch has cited a scenario where a $100,000 wallet balance backs positions quoting a combined $300,000, but that figure reflects quoted inventory, not available capital.

Actual fill capacity is still constrained by whatever the wallet holds at execution time, so providers carrying concentrated positions or low on-chain balances will hit limits that the quoted figure obscures.

This custody-preserving design contrasts sharply with standard AMMs, where depositing into a pool transfers asset control to a smart contract and exposes the provider to impermanent loss on every price move.

Aqua’s model keeps the asset in the provider’s wallet, which is structurally cleaner for professional market makers who need balance-sheet flexibility, though execution still depends on verified counterparties and on-chain balance checks at fill time.

Chain Coverage and Incentive Structure at Launch

The public release covers Ethereum, Arbitrum, Base, BNB Chain, Optimism, Polygon, and Robinhood Chain, among seven others, all EVM-compatible.

That breadth matters because liquidity on EVM chains remains heavily fragmented, with meaningful depth concentrated on Ethereum mainnet and Arbitrum while newer chains struggle to attract professional providers without dedicated incentive programs.

To bootstrap depth across all 13 networks, 1inch is launching a parallel incentives program backed by 10 million 1INCH from the 1inch Foundation and 500,000 USDC from the 1inch DAO.

Rewards are distributed through Merkl and administered by Degensoft Ltd (BVI). The size of the package is meaningful, 10 million 1INCH at current market rates represents a real incentive floor, but the distribution mechanism and lockup terms will determine whether it attracts sticky liquidity or mercenary capital that exits once rewards dry up.

Trade Ripple XRP on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

The post Registry Model, 13 Chains: How 1inch Aqua Tackles DeFi’s Fragmented Liquidity appeared first on Cryptonews.

The Federal Reserve held interest rates steady on Wednesday, but three policymakers voted to raise them. Bitcoin and gold both climbed within minutes of the announcement.

The split vote is the most contested outcome of Kevin Warsh’s short tenure as chair. Interest rate swaps then pulled back from a fully priced September increase.

Why the Fed Rate Hold Split the Committee

The Federal Open Market Committee (FOMC) kept the federal funds target range at 3.50% to 3.75% by a vote of 9 to 3. Cleveland’s Beth Hammack, Minneapolis chief Neel Kashkari, and Dallas president Lorie Logan each wanted a quarter point increase.

Follow us on X to get the latest news as it happens

All three dissenters run regional reserve banks. Nobody on the Washington-based Board of Governors broke ranks with Warsh, which keeps the divide outside the Fed’s centre of power.

Warsh took over in May, and his first meeting in June produced a unanimous hold. Analysts had warned he might get a Fed family feud this time instead.

The statement itself barely moved. Policymakers again described activity as expanding solidly despite uncertainty tied to the conflict in the Middle East. They repeated that productivity growth and capital investment are strong.

Inflation, however, remains above the 2% goal. The Committee again blamed supply shocks in certain sectors, energy among them, and repeated its pledge that it “will deliver price stability.”

Traders had treated a hike as a live risk. CME FedWatch showed rare hike odds priced near 30% a day earlier, while Kalshi put the chance at roughly 23% on Wednesday morning.

Bitcoin and Gold Climb as Hike Bets Fade

Bitcoin (BTC) rose from about $63,700 to an intraday high near $64,700 in the quarter hour after the release. Bitcoin’s post-decision price action left it near $64,325, up 1.1% over 24 hours, with a market capitalization of $1.29 trillion.

Gold moved in step. Spot prices climbed from roughly $4,000 to a high above $4,084 before easing back toward $4,076, according to OANDA data.

Rate markets did the rest. Swaps no longer fully price a September hike, which eases some of the strain that had lifted global bond yields to their highest levels since 2008.

Oil remains the swing factor. Brent fell sharply after Washington paused its strikes on Iran, though oil markets moved again on Wednesday as tensions resurfaced.

What Comes Next for Rates and Crypto

Bank of America told clients a July increase would have been without precedent. The bank noted the Fed has not hiked since 1994 with less than 60% odds priced in.

JPMorgan had modeled a hawkish hold as its base case at 50%, with a quarter point hike at 20%. Three dissents hand that hawkish reading more weight than an unchanged rate implies.

Attention now shifts to Warsh’s press conference and to September. Should oil turn higher again, the dissenters regain the argument they lost on Wednesday.

The post Bitcoin and Gold Jump After Fed Rate Hold Splits FOMC 9 to 3 appeared first on BeInCrypto.

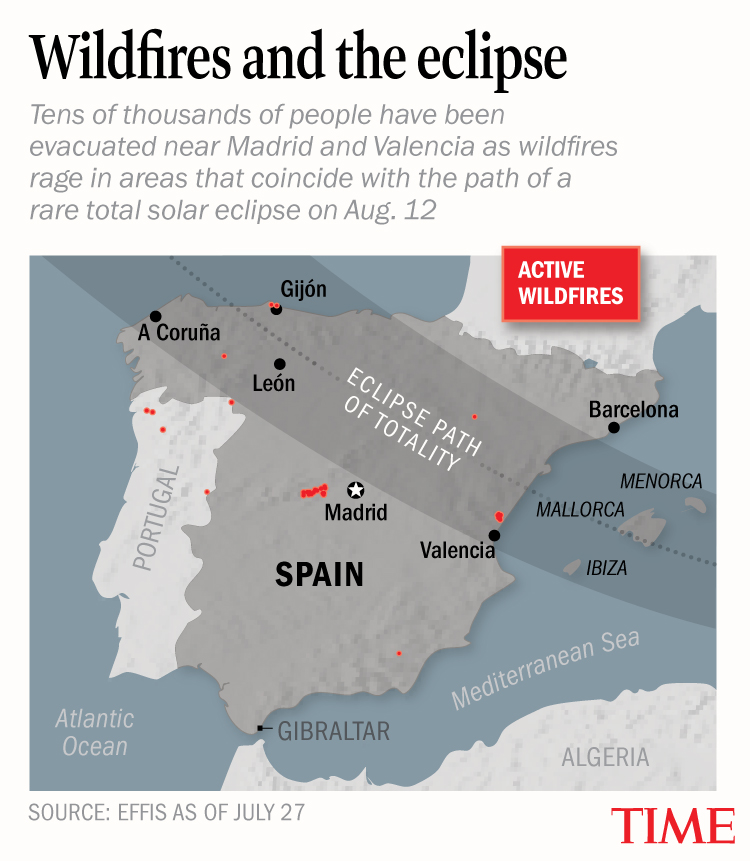

Spain will be in the path of totality for a solar eclipse on Aug. 12. Not only is it the first time this type of celestial event has been visible to the mainland since 1905—it is also taking place during Europe’s peak tourism season, which runs from June to August. Millions of people live within the 190-mile-wide eclipse path, which reaches 36 of the nation’s 50 provinces, while hundreds of thousands of international travelers are also expected to visit for the occasion.

Tourists are expected to flock to cities and towns along the path of totality—including parts of Aragón, Castilla y León, Castilla-La Mancha, and Valencia—as well as nearby hubs, where a deep partial eclipse will be visible, like the capital city of Madrid.

But with multiple wildfires raging amid a particularly hot and dry summer, the rare experience of observing a total solar eclipse may be disrupted by evacuations and widespread smoke.

Read More: What to Know About the Deadly Wildfires in Western Europe

What are the fire conditions leading up to the eclipse?

While Spain is used to wildfires, record-breaking heat in June created a tinderbox in Western Europe, prompting two catastrophic fires: one that broke out on July 24, in the Guadalajara province just northeast of Madrid, devastating over 32,000 hectares (79,000 acres), and another in Ávila, which is in central Spain, that has burned more than 50,000 hectares (123,500 acres) since July 22. The Ávila fire is now the “largest forest fire in our country’s recent history” according to a statement on Sunday from the minister of ecological transition, Sara Aageson.

Together with numerous other fires across the country, they put Spain on track for its worst wildfire season in over three decades. Over 150,000 hectares (370,600 acres) have burned since January, according to Prime Minister Pedro Sánchez—which is six times the area destroyed during the same period last year. Prior to 2025, the worst wildfire year for the country was 1994.

Sánchez said over the weekend that the “scale of the disaster we are living through is very hard to accept.” More than 90,000 tourists and residents have been evacuated or placed under shelter at home orders across central Spain, in parts of Madrid, Toledo, and Ávila. Spanish authorities said at least two people were killed in the eastern provinces of Castellón and Valencia

Sánchez also expressed concern about the weather conditions this week, which brings peak temperatures of nearly 40°C (104°F). Extreme heat makes it difficult to fight existing fires and adds the threat of new ones, which would challenge Spain’s already-stretched resources.

With additional factors such as gusting winds and a lack of recent rainfall, the fire danger conditions in the country have been classified as “very extreme,” according to the European Forest Fires Information System (EFFIS).

And those conditions are not likely to improve ahead of the solar eclipse, according to Jason Nicholls, senior meteorologist at AccuWeather.

“There’s a heat wave going on right now, which carries into the weekend,” he tells TIME. “It may ease back a little bit, but then tries to come back again as we get into the week of August 10.”

“I don’t see a lot of significant rain coming into Spain over the next two weeks, so drought conditions will continue to not improve, or even worsen,” he continues, explaining that “wildfire risk will remain extreme across a whole lot of Spain” in the days leading up to the solar eclipse.

How the wildfires could impact eclipse viewers

The wildfires will likely affect both visibility and air quality for eclipse viewers in the country, Becky Wagner, air quality and climate researcher at the University of Sheffield, tells TIME.

The smoke from the fires contains “particulate matter” consisting of burnt material, she explains.

“Firstly, that can affect visibility because these particles can reflect the sunlight and just create a haze and a sort of a cloud that is really hard to see through,” Wagner says.

But there is also the question of air quality, which could hinder viewers’ ability to safely stand outside and observe the eclipse.

“There’s high levels of this smoke, and high levels of the particulate matter within the smoke, which is really harmful to human health, as these particles are really small,” Wagner says, referring to a type of fine air pollutant known as PM2.5, which has been linked to lung cancer and heart disease. “They can be breathed in, and it can affect people’s health, particularly vulnerable populations with respiratory and cardiovascular problems.”

Totality occurs when the moon passes exactly between the sun and the Earth, blocking out the daylight and casting impacted areas into complete darkness for about three minutes. While the experience of totality is brief, breathing in wildfire smoke can make people sick “right away,” leading to coughing and headaches, among other symptoms, according to the United States Centers for Disease Control and Prevention.

And many eclipse-chasers will seek to observe the phenomenon beyond the moments of totality. Observation often begins as soon as the moon is visible in front of the sun, and lasts until it has completely passed by, meaning that the complete experience of a solar eclipse can span some two to three hours.

But it’s hard to predict how current conditions might impact the air quality in mid-August, Wagner says, especially as wildfires can often create their own mini weather conditions.

Particles “can last in the atmosphere for days to weeks, and they can be transported a really long distance, depending on sort of wind direction and wind speed,” Wagner says.

Aside from Spain’s progress in quelling the fires this week, there are still active fires in France to consider, since the particulate matter could continue drifting across large portions of its neighboring nation. Wagner points to the wildfires in Canada earlier this month that drifted thousands of miles into the United States, worsening air quality in cities from Detroit to Manhattan.

“So fires in one region of Spain, or one region of Europe, could end up affecting different parts of the country or different countries,” she explains.

Still, Nicholls says that residents in Spain should be able to experience and enjoy the eclipse—with the proper precautions. He recommends wearing a mask when outdoors to avoid inhaling dangerous smoke, as well as limiting exposure to it.

“Maybe hang around inside, and as you get closer to the eclipse, maybe come outside and maybe have a mask on,” he recommends. Then “get back inside to get away from the harmful smoke and poor air quality.”

Read More: Photos Show the Destruction in France and Spain From Ferocious European Wildfires

What are the potential economic repercussions for Spain?

Access to viewing locations could also be impacted by the fires. One of the larger outbreaks is near Valencia—Spain’s third-largest city, which is situated along the Mediterranean. Last month, Space.com said that its beaches will be one of the easiest places to catch a glimpse of the eclipse. But local wildfires could potentially inhibit access to the beaches and other prime viewing spots. Such restrictions could be especially detrimental in light of the surge of tourists Spain is expecting next week—and might even have economic repercussions.

According to Spain’s Ministry of Tourism, the country continues to see an increase in international travelers year over year. And, despite the fires, the ministry is expecting a larger-than-usual boost in tourism next month, with dedicated umbraphiles—or eclipse chasers—traveling just for the occasion.

“Between August 10 and 16, Spain will welcome 446,000 additional visitors due to the total solar eclipse,” the government said in a statement to TIME, citing an economic impact report from the Ministry of Economy, Trade, and Business. “A 7.9% increase in scheduled airline seats is projected, compared to the same period in 2025, as well as a 17.8% rise in hotel reservations for August, compared to the same month last year.”

“It is clear that this event will have a very positive impact on our economy,” the Ministry of Tourism wrote, saying that it is expected to bring in 347.5 million euros ($395 million). The government has not revised its projections due to the wildfires; however, it says that the consequences to tourism are not its primary focus.

“The priority is to address the emergency posed by these fires, protect human lives, preserve the natural surroundings, and minimize the impact on the environment,” the statement said.

But the government’s statement also acknowledged that it has “a Special Security Plan and a Specific Civil Protection Plan” in place for the eclipse, which addresses wildfire prevention in particular, as well as increasing the response capacity of public services in preparations for the large gatherings that are anticipated for the special event.

Spain has yet to issue any travel advisories in response to the fires, but the United Kingdom last week began warning its residents—who make up nearly 20% of annual travelers to Spain—to take precautions if traveling through affected areas of Madrid and Ávila.

Bitcoin and other major cryptocurrencies barely moved after the Federal Reserve left interest rates unchanged, suggesting traders had largely prepared for the decision.

Summary

- Bitcoin traded near $64,100, gaining only 0.3% over the previous 24 hours.

- Gold and silver ETF proxies rose 1.25% and 2.52%, respectively.

- Crypto-linked stocks diverged as Strategy gained 2%, while major Bitcoin miners fell about 6%.

- The CLARITY Act’s 28% passage odds make U.S. crypto policy the next industry-specific catalyst.

Fed keeps interest rates unchanged

Federal Reserve officials maintained the federal funds rate at between 3.5% and 3.75% following Chair Kevin Warsh’s second Federal Open Market Committee meeting.

Policymakers voted 9–3 for the decision, with the presidents of the Cleveland, Dallas and Minneapolis regional Federal Reserve banks preferring a quarter-point increase. Markets had assigned roughly a one-in-three chance to a hike before the announcement.

The Fed described economic activity as “expanding at a solid pace,” citing stable unemployment and job growth that has broadly kept up with changes in the workforce. However, it also acknowledged that inflation remained above its 2% target.

Warsh has avoided giving detailed guidance on future policy and has instead focused on current economic data. He has also created five task forces to examine the Fed’s communications, balance sheet, inflation framework, productivity, and labor-market analysis.

The widely expected hold removed the immediate risk of a surprise hike. However, the three dissents and persistent inflation mean uncertainty has shifted toward the September meeting rather than disappeared.

Bitcoin and top cryptocurrencies barely move

Bitcoin traded at about $64,129 after the announcement, up only 0.3% over 24 hours, according to CoinGecko. Ethereum changed hands near $1,911 after gaining 0.6%.

Other large cryptocurrencies also recorded limited moves. BNB rose 0.4%, XRP gained 1.3%, Solana advanced 0.9%, and TRON added 0.6%. Hyperliquid and Dogecoin were up 1.4% and 1%, respectively.

Total cryptocurrency market capitalization increased just 0.4% to approximately $2.27 trillion. The narrow price changes suggest the rate hold had been largely reflected in crypto valuations before the announcement.

Sentiment nevertheless remained cautious. The daily Crypto Fear & Greed Index stood at 29, within the “Fear” category, on July 29.

Bitcoin’s Coinbase Premium also remained negative. A negative reading means Bitcoin trades at a discount on Coinbase relative to Binance, pointing to weaker U.S. spot demand compared with offshore markets.

Gold rises as crypto-linked stocks diverge

Safe-haven assets outperformed cryptocurrencies during the session. SPDR Gold Shares rose 1.25%, while the iShares Silver Trust gained 2.52% shortly after the Fed announcement.

Their performance showed that investors continued to seek defensive exposure amid inflation concerns and renewed Middle East tensions, even as the expected rate decision produced little direct volatility.

Crypto-linked equities delivered mixed results. Strategy gained approximately 2.1%, while Coinbase fell about 1%. Robinhood declined 1.7%.

Bitcoin miners suffered larger losses. MARA Holdings, Riot Platforms and CleanSpark each dropped roughly 6% on the day. However, these declines had started before the Fed announcement and therefore cannot be attributed solely to the interest-rate decision.

Broader U.S. stock-market proxies moved less sharply. The SPDR S&P 500 ETF, Invesco QQQ and iShares Russell 2000 ETF were each down about 0.4% shortly after the decision. Earlier pressure had come from rising oil prices, Middle East tensions and weakness among semiconductor stocks.

CLARITY Act becomes the next crypto policy test

With the FOMC decision producing no major crypto move, investors may now turn toward the CLARITY Act as the largest U.S. crypto-specific policy catalyst.

Polymarket traders currently give the legislation a 27% probability of becoming law during 2026. The prediction market has generated about $3 million in volume.

Senate negotiations remain divided over political ethics provisions and whether crypto companies should be allowed to offer rewards tied to stablecoin balances. Banking groups argue that such rewards could pull deposits away from traditional lenders.

The bill would establish clearer responsibilities for the Securities and Exchange Commission and Commodity Futures Trading Commission. Failure to advance it before the Senate’s August recess could further narrow its path during the midterm election cycle.

Investors will also watch upcoming inflation and employment figures for signs that the Fed may raise rates in September. Those releases, alongside the CLARITY Act negotiations, could determine whether Bitcoin breaks out of its current range or continues consolidating near $64,000.

XRP has come under renewed selling pressure after failing to sustain its previous rebound, sending the price back toward a key support region. Although buyers have stepped in to defend the latest decline, the broader technical picture still favors caution as the asset trades below major resistance levels.

XRP Price Analysis: The Daily Chart

The daily chart continues to reflect a bearish market structure, with the cross-border token trading inside a long-term descending channel while remaining below both the 100-day and 200-day moving averages. The recent rejection from the upper portion of the range reinforces that sellers are still controlling the broader trend.

The $1.02 to $1.04 demand zone once again attracted buyers, triggering the latest rebound. However, the recovery remains vulnerable as long as the price stays beneath the descending trendline and the major resistance area around $1.24 to $1.28, where the moving averages also converge. A successful reclaim of this region would be the first meaningful sign that momentum is shifting in favor of the bulls.

On the downside, losing the $1.02 to $1.04 support would expose the broader demand zone around $0.89 and extend the prevailing bearish trend.

XRP/USDT 4-Hour Chart

The 4-hour timeframe highlights the recent breakdown below the yellow ascending trendline, confirming that buyers have lost short-term control after failing to defend the series of higher lows. That breakdown led to a sharp decline into the $1.02 to $1.04 demand zone, where buying interest quickly emerged.

The current rebound has pushed XRP back toward the $1.08 to $1.09 resistance area, which previously acted as support before the breakdown. This makes the current rally an important retest of former support turned resistance. As long as the price remains below this zone, the recent bounce could simply represent a corrective recovery within the broader downtrend.

A rejection from the current resistance would increase the probability of another move toward the $1.02 to $1.04 demand zone. Conversely, a decisive reclaim of the $1.08 to $1.09 region would improve the short-term outlook and open the door for a recovery toward the larger supply zone around $1.16 to $1.18.

The post Ripple Price Analysis: XRP Risks Falling Below $1 Unless It Breaks This Barrier appeared first on CryptoPotato.

But then, those mechanics—along with loads of elaborately fake-looking special effects, which now, rather than being dazzling, are just business as usual—are the hallmarks of all Marvel movies. It seems you can’t build one without them. You also can’t really explain the plot of Brand New Day without giving away the arrival of a surprise character, but here, roughly, is how it goes: Sad Peter Parker goes through the motions of being Spider-Man for four long years, as MJ and Ned study hard at MIT, the college the three of them were supposed to attend together. After graduation, MJ and Ned return to New York; Peter spies on them wistfully, and when he finally does get up the guts to talk to them, his face draws blank stares. He regularly leaves fresh flowers at Aunt May’s grave. The rest of his days are spent foiling workaday crimes, until some weird events shake the city: an unseen force capable of taking control of people’s bodies and brains has begun to wreak mayhem. Meanwhile, Spider-Man’s web-shooting capabilities have gone awry. His know-it-all AI assistant E.V.I.E. informs him that this is due to a massive increase in “arachnid hormones,” which is also causing him to be more aggressive. In other words, he’s angry and stressed out, and he has no idea how to handle his rage.

Although there was some uncertainty about the monetary direction the United States Federal Reserve will take following the July FOMC meeting, the central bank approved with a 9-3 vote to maintain the interest rates at 3.50% to 3.75%.

All eyes have turned to the incoming press conference by the new Fed Chair, Kevin Warsh, as investors anticipate which way he will lean.

“The Committee decided to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent, in support of the Federal Reserve’s dual mandate. The Committee is continuing its policy of maintaining ample reserves in the banking system,” reads the statement.

As reported earlier today, this meeting was described as the most unpredictable since the COVID-19 pandemic broke out in March 2020. The reason for this is that all meetings since then had a 99% agreement about the outcome ahead of their conclusion.

In contrast, futures markets and prediction platforms had assigned a 30%-38% probability for a rate hike for today’s meeting.

Investors apparently had de-risked from more volatile assets like bitcoin ahead of the event today, as the asset slumped by $3,000 yesterday. It rebounded to $64,500 today, where it was rejected and slipped to under $63,800 before the meeting.

Its minor volatility returned after the announcement, pumping above $64,000 as of now. However, it’s likely that the Warsh speech will impact it even more, especially if the new Fed chair hints at what the central bank will do next – a rate hike or another pause.

The post Bitcoin Volatility Returns After Fed Holds Interest Rates Steady appeared first on CryptoPotato.

Credit default swap (CDS) demand is surging throughout the AI industry. Five years of default protection on $10 million of Nvidia debt now costs about $82,000 a year — double since the start of July when it cost roughly $40,000.

CDS spreads are deteriorating rapidly across mega-cap AI stocks including Alphabet, Amazon, Meta, Broadcom, and SpaceX, which all hit record spreads this week.

Alphabet CDS contracts traded up to 67 basis points days after reporting its first negative quarterly free cash flow since its 2004 listing.

Investors refer to the “price” of a CDS by its basis point spread above the notional amount of debt it guarantees.

A basis point is one hundredth of a percentage point, and the higher they “spread” above the notional quantity of debt, the more investors have to pay as a de facto insurance premium.

Companies want their CDS contracts to be cheap. When basis points are low, investors aren’t bidding extra for the right to receive a payout in the event of a credit default. Low basis points on CDS contracts — or even better, no CDS demand at all — indicate confidence that the company will service its debt on-time and in full.

Insurance premium doubles to protect Nvidia credit

Unfortunately, Nvidia’s five-year CDS contracts reached a record 82 basis points on Monday.

Monday’s jump of roughly 14 basis points was the largest single-day move since those Nvidia CDS contracts began trading in November 2025, ICE Data Services reported.

The $330 billion AI company Oracle carries an even worse premium. Its five-year CDSs traded above 215 basis points this week, up from 145 at the end of last year.

S&P Global cut the company’s creditworthiness rating to BBB- earlier this month, the lowest rung of its investment grade band.

Oracle’s bonds that mature in 2056 and pay 6.7% interest widened eight basis points on Monday to 263 basis points over US Treasuries. Not good.

Even worse, CoreWeave topped 855 basis points on Tuesday. A popular CDS pricing model reads that as roughly a 50% chance of default within five years.

Disturbingly, the instruments themselves have become an unfortunate growth market for Wall Street.

CDS for AI stocks shouldn’t be a growth sector

AI companies and tech stocks accounted for nearly $650 million of second-quarter corporate CDS trading, DTCC data shows. That is up 20% on the first quarter and almost 600% year on year.

The spike in CDS spreads this week followed a Bloomberg report that Nvidia is preparing AI commitments potentially worth more than $750 billion.

Those include a partnership with SK Group valued above $500 billion and talks over a guarantee of as much as $250 billion to help OpenAI lease computing capacity.

Doubt about its ability to service that debt sent CDS rates higher.

Read more: South Korea’s KOSPI has erased more than Bitcoin’s market cap in 29 days

CDS trader Michael Burry posted, “There is a reason Nvidia’s five-year credit default swaps are going parabolic.”

The short-seller blamed circular spending, i.e. companies buying services from one another in order to manufacture higher revenue for fundraising purposes.

Credit ratings agency Moody’s has already warned that unprecedented AI spending threatens the credit quality of Microsoft, Amazon, Alphabet, Meta, Oracle and CoreWeave.

Direct debt across those six names is worth roughly $460 billion. Land, office, and data center lease commitments add another $1.2 trillion.

The six largest tech stocks now account for 8.6% of duration times spread risk among US high-grade corporate bonds, per Barclays.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Kyverna Therapeutics: 'Strong Buy' On ElevateBio Manufacturing Deal And RA Program Advancement

Patrick Witt hits back at 134 bank leaders over CLARITY Act

Danny DeVito parties, gets married, and ‘human traffics’ in first look at “It’s Always Sunny” season 18

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

How Billionaires Teach the Value of Money | Ft. Rizwan Sajan | #SanjayKathuriaPodcast

*AFTER PATCH* EASY SOLO MONEY GLITCH IN GTA ONLINE! 20 MILLION PER HOUR! (UNLIMITED MONEY GLITCH)

Bitcoin Hit by a Massive Global Sell-Off

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Brooks Brothers

-

Sports3 days ago

Sports3 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Tech3 days ago

Tech3 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World7 days ago

Crypto World7 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics2 days ago

Politics2 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World4 days ago

Crypto World4 days agoRipple bought a bank in pieces. The $4 billion audit

-

Entertainment5 days ago

Entertainment5 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos3 days ago

News Videos3 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Sports6 days ago

Sports6 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Politics1 day ago

Politics1 day agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Fashion6 days ago

Fashion6 days ago16 Dresses for the High Summer Event

-

News Videos6 days ago

News Videos6 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Business14 hours ago

Business14 hours agoMajor shareholder moves on Canyon

-

Politics3 days ago

Politics3 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Crypto World3 days ago

Crypto World3 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Crypto World6 days ago

Crypto World6 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Entertainment1 day ago

Entertainment1 day ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Tech5 days ago

Tech5 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Crypto World7 days ago

SEC Agrees to Overhaul Recordkeeping After Settling Coinbase Lawsuit Over Gensler’s Lost Texts

-

Entertainment4 days ago

Entertainment4 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

You must be logged in to post a comment Login