Crypto World

Ripple IPO and XRP holders: what we know

Ripple’s CEO said the company might do “something special” for XRP holders if it ever goes public. The XRP community heard a promise. What he actually said was a maybe, attached to an IPO he calls a non-priority. Here is the real picture, separated from the hype.

Summary

- Ripple has not promised an IPO reward for XRP holders.

- Garlinghouse only left the door open to a possible future benefit.

- Ripple equity and XRP are separate assets with no automatic holder link.

- The real XRP case still depends on utility, regulation, adoption, and demand.

One sentence from Ripple’s chief executive set the XRP community alight. Asked on a podcast whether XRP holders might benefit if Ripple ever went public, Brad Garlinghouse said there could be a scenario where the company does “something special” for people who hold XRP, then immediately added that it was not something for the immediate term.

Within hours, the remark had been clipped, shared, and amplified into something close to a promise, with community members urging others to “hold accordingly.” But the gap between what Garlinghouse actually said and what the community heard is wide, and it matters.

The difference between a hinted-at maybe and a planned reward is the difference between a reasonable hope and a misplaced expectation. This piece separates the two, laying out exactly what was said, what it could mean, what stands in the way, and what an XRP holder should realistically take from it.

The subject sits at the intersection of two real questions: whether and when Ripple will go public, and whether holding XRP, which is a separate asset from Ripple equity, entitles you to any share of Ripple’s corporate success. These are questions the XRP community has debated for years, and Garlinghouse’s comments touched the nerve directly without resolving it.

This guide covers what Garlinghouse actually said and the precise wording that matters, the crucial distinction between Ripple the company and XRP the token, the theoretical mechanisms a holder benefit could take, why Ripple says an IPO is not a priority right now, the case that XRP holders already benefit indirectly, and what all of it adds up to for someone holding XRP today.

The goal is to give you the real picture, neither dismissing the possibility nor inflating it into the certainty the hype implied.

What Garlinghouse actually said

Precision matters here, because the entire community reaction hinges on a few words, and those words were more careful and more conditional than the excitement suggested.

Speaking with a journalist on a podcast, Garlinghouse was asked directly whether XRP holders could benefit from Ripple’s success if the company eventually launched an IPO. He did not deflect the question, but he did not commit to anything either.

His framing began with the indirect benefit Ripple already provides. He said he hopes XRP holders feel they are benefiting from Ripple’s existence through the work the company does to catalyze activity in the XRP ecosystem.

Then came the sentence that set off the excitement. Asked whether Ripple would do something specific for XRP holders if and when it goes public, he said, “Maybe. But I mean, that’s not in the immediate term.”

That is the entirety of the supposed promise: a maybe, explicitly qualified as not near-term, offered in response to a direct question, not volunteered as a plan.

The careful reading of those words reveals how conditional they are. Garlinghouse did not announce a program, describe a mechanism, or commit to any action.

He acknowledged a possibility, the way anyone might concede that something could happen without saying it will. He was explicit that it was not in the immediate term, and he attached it to an IPO that, as the next sections show, he describes as not a priority.

He also did not endorse any specific structure, declining when asked about a token buyback or another mechanism that would let holders share in Ripple’s wealth. Instead, he pointed to the indirect benefits Ripple already creates.

So the accurate summary is that Garlinghouse left a door open without walking through it. He acknowledged that a future, post-IPO benefit for XRP holders is possible while making clear it is neither planned nor imminent nor defined.

The community heard “Ripple will do something special for holders.” What Garlinghouse said was “maybe, someday, if we go public, which is not a priority.” Those are very different statements, and the difference is the whole story.

Ripple the company versus XRP the token

To understand why a holder benefit is even a question, you have to understand a distinction that confuses many people: Ripple and XRP are not the same thing, and owning one does not mean owning the other.

Ripple is a private technology company that builds payment and liquidity products, some of which use the XRP Ledger. XRP is a cryptocurrency, the native asset of the XRP Ledger, which is a decentralized, open-source blockchain that Ripple does not control.

When XRP was created, a large portion of the supply was allocated to Ripple to fund its development and promote adoption, which is why Ripple is closely associated with XRP and is in fact the largest single holder of the asset. But the association is not ownership in the corporate sense.

Holding XRP gives you a cryptocurrency, not equity in Ripple. It gives you no shares, no dividend rights, and no claim on the company’s profits or assets.

If Ripple goes public and its stock soars, that benefits Ripple’s shareholders, the holders of its equity. XRP holders are not automatically among them simply by holding the token.

This distinction is exactly why the “something special” question exists and why it is not trivially answered. Because XRP and Ripple equity are separate assets, there is no automatic, built-in mechanism by which Ripple’s corporate success, including a successful IPO, flows to XRP holders.

Any such benefit would have to be a deliberate corporate decision, a choice Ripple made to extend something to holders of a token that is legally distinct from its stock. There is no existing structure, no dividend, no buyback, and no holder-equity link that does this today.

This is what makes Garlinghouse’s maybe notable: it gestures at the possibility of Ripple voluntarily creating a link between its corporate success and XRP holders that does not currently exist and is not required to exist. The community’s hope is precisely that Ripple would choose to build such a bridge between the two separate assets.

The reality is that no such bridge exists, none is planned, and the entire question is whether Ripple might someday decide to construct one. That is a very different thing from a benefit that flows automatically.

What a holder benefit could theoretically look like

If Ripple ever did decide to do “something special,” what could it actually be? Several theoretical mechanisms have circulated, and walking through them clarifies both the possibilities and their limits.

The most discussed possibilities involve giving XRP holders some form of access to or stake in Ripple’s equity. One idea is early or preferential access to Ripple shares during an IPO, an allocation phase where verified long-term XRP holders could buy into the offering.

Another is a community-based reward structure tied to long-term XRP holding, rewarding holders who have held for a certain period. A third, more exotic idea is a tokenized representation of Ripple equity made available to eligible holders, using blockchain to give XRP holders some claim linked to Ripple stock.

Each of these would, in effect, create the bridge between Ripple equity and XRP holders that does not currently exist. It would extend a piece of the company’s success to token holders through a deliberately constructed mechanism.

These are the kinds of structures the community imagines when it hears “something special.” But they remain imagined structures, not announced ones.

The important caveat is that all of these are speculation, not plans, and each faces real practical and legal limits. Because Ripple equity and XRP are separate assets, any direct financial benefit to XRP holders would depend entirely on corporate decisions made during an IPO process that may never happen.

Such decisions carry legal, regulatory, and securities-law complications that make them far from straightforward. Linking a cryptocurrency’s holding to equity benefits raises exactly the kind of securities questions that XRP’s long legal history has been about, and Ripple would have to navigate those carefully.

Other, less direct possibilities are also floated, such as Ripple using IPO proceeds to fund ecosystem growth that indirectly benefits XRP through increased adoption and liquidity. That is closer to what Ripple already does.

The honest framing is that while several mechanisms are conceivable, ranging from share access to tokenized equity to ecosystem investment, none is announced, all face real hurdles, and the more direct and exciting versions are also the most legally complicated. The possibilities are real as possibilities. They are not, on any current evidence, plans.

Why Ripple says an IPO is not a priority

The “something special” was explicitly tied to Ripple going public, so the holder-benefit question is downstream of a prior question: will Ripple even have an IPO? And Garlinghouse has been clear that it is not a priority.

Garlinghouse stated plainly that Ripple has not prioritized going public, and he gave concrete reasons. He pointed to the recent underperformance of crypto-related public listings, citing companies whose stock has not done particularly well after going public and noting that another major exchange had reportedly delayed its own listing plans.

He also emphasized the benefits of staying private, joking that being private lets him speak freely without lawyers constraining every word. Beneath the humor was a real point about the disclosure burden and constraint that public-company status imposes.

The picture he painted was of a company that sees little reason to rush into public markets that have treated its peers poorly, and that values the flexibility of remaining private. An IPO, in his framing, is a distant possibility, not an imminent plan.

This matters enormously for the holder-benefit question, because it pushes the entire scenario further into the uncertain future. The “something special” was conditioned on Ripple going public, and Ripple going public is itself not a near-term priority.

So the holder benefit is a maybe contingent on an event that is itself a maybe. Stacking those conditionals, a possible benefit attached to a possible IPO that is explicitly not a priority and not near-term, shows how far the exciting headline is from anything concrete.

For an XRP holder, this means the “something special” should be understood as a distant, doubly conditional possibility, not as a catalyst to expect on any near horizon. Ripple may eventually go public, and if it does, it may eventually do something for holders.

But both halves of that sentence are uncertain and neither is imminent. That is a very different proposition from the one the hype implied. The IPO that the benefit depends on is not on the calendar.

The case that XRP holders already benefit

Set against the speculation about a future special benefit is Garlinghouse’s actual, stated position: that XRP holders already benefit from Ripple’s existence, indirectly but intentionally, and this argument deserves fair consideration.

Garlinghouse’s framing is that Ripple’s commercial activity is designed to benefit XRP even without any direct financial mechanism. He argues that Ripple is the most interested party in seeing XRP succeed, noting that the company remains the largest holder of XRP on the planet and therefore has the strongest economic incentive to increase the token’s value and adoption.

In his telling, Ripple’s strategy is built around making XRP the most useful, most liquid, and most trusted digital asset. Every acquisition, investment, and partnership the company pursues is evaluated partly through the lens of how it drives XRP adoption and utility.

The benefit to holders, on this view, is real but indirect. By growing the ecosystem, expanding XRP’s use in payments and settlement, and increasing its liquidity and trust, Ripple makes the XRP that holders own more valuable and more useful, which is a benefit even without any dividend or equity link.

This is where Ripple’s real-world strategy matters more than the IPO speculation. XRP’s long-term case is strongest when it is tied to actual institutional settlement, tokenization, liquidity, and demand, not to hopes of a future equity-linked reward.

This argument has genuine merit and should not be dismissed as spin. Because Ripple is the largest XRP holder, its incentives really are aligned with XRP holders in a meaningful way: Ripple profits when XRP rises, just as holders do, so the company has a built-in reason to drive the token’s value that does not require any special program.

Ripple’s actual activities, the partnerships, the payment integrations, and the institutional adoption work, do plausibly increase XRP’s utility and demand over time, which is a real if indirect benefit to anyone holding the token. That is also why XRP’s institutional catalysts matter: the strongest version of the XRP thesis comes from regulation, ETF demand, and utility aligning, not from IPO speculation alone.

The honest counterpoint is that this indirect benefit is exactly what the community finds insufficient, because it is diffuse and uncertain instead of a concrete share of Ripple’s specific corporate success. Garlinghouse’s maybe on direct benefits is precisely a response to that dissatisfaction.

But the indirect-alignment case is not nothing. It is a reasonable argument that holding XRP already ties you, loosely, to Ripple’s success through the company’s incentive to grow the token.

Whether that loose tie is enough is the debate, and it is one Garlinghouse’s comments intensified without settling.

Why the regulatory backdrop matters

The IPO question is speculative, but XRP’s regulatory backdrop is not, and it shapes why the community reacted so strongly to Garlinghouse’s remark.

XRP holders are not just hoping for a corporate reward. They are watching a year in which regulatory clarity, ETF inflows, tokenized settlement tests, and the CLARITY Act have all become part of the XRP investment story.

The CLARITY Act is especially important because it could turn XRP’s current regulatory position into a clearer statutory framework. That would matter more directly to XRP than any vague IPO benefit, because it could reduce the legal uncertainty that has constrained institutional adoption.

That does not mean the law guarantees price appreciation, and it does not mean Ripple’s IPO would automatically reward holders. But it explains why the community is primed to treat every Ripple-related signal as part of a broader XRP catalyst stack.

The problem is that not all catalysts are equal. CLARITY passage, ETF inflows, exchange-reserve changes, and real payment or settlement usage are observable market or regulatory developments.

A possible IPO reward is not. It is a speculative possibility attached to a corporate decision that has not been made.

This is why reading XRP signals carefully matters. Some signals describe actual supply, demand, usage, or regulation, while others describe hopes about what Ripple might one day decide to do.

For XRP holders, the discipline is to separate the two. The regulatory and institutional backdrop is real; the IPO reward remains hypothetical.

What it means for XRP holders

For someone holding XRP and watching this story, the practical question is what to actually make of it, and the answer is a matter of holding the possibility and its limits in proper proportion.

The realistic reading is that a direct XRP holder benefit from a Ripple IPO is a genuine possibility but a distant and unplanned one. It is contingent on an IPO that Ripple says is not a priority and structured through mechanisms that face real legal hurdles and do not currently exist.

An XRP holder should neither dismiss the idea entirely, since Garlinghouse did deliberately leave the door open and Ripple’s incentives are truly aligned with holders, nor treat it as a reason to expect a windfall. Nothing is planned, announced, or near-term, and the whole scenario depends on conditions that may not materialize.

Buying or holding XRP specifically in expectation of an IPO reward would be building on speculation about a maybe attached to a maybe, which is a weak foundation for any financial decision. The sensible stance is to regard a potential holder benefit as a possible future upside that is not to be counted on, instead of as a catalyst to position around.

The more grounded takeaway is to focus on what is actually known rather than on the speculation. What is known is that Ripple is closely tied to XRP, is the largest holder of the asset, and has strong incentives to grow its value, which provides a real if indirect benefit to holders.

What is known is that XRP and Ripple equity are separate, with no current mechanism linking the two. And what is known is that Garlinghouse acknowledged a possible future benefit while explicitly declining to plan or promise one, tied to an IPO he does not prioritize.

An XRP holder is better served evaluating the token on its actual merits: its use in payments and settlement, its regulatory position, its adoption trajectory, and institutional positioning in XRP. Those are measurable signals.

The IPO story is worth knowing, but it is a speculative possibility at the edge of the picture, not the center of any sound reason to hold XRP. That is the price reality behind the hope: bullish narratives only matter when the market can connect them to actual token demand.

None of this is investment advice; it is a frame for reading a piece of news that the community has inflated well beyond what was actually said.

A maybe, not a promise

The story that “Ripple will do something special for XRP holders when it goes public” is, on close inspection, a story about a carefully hedged maybe.

Garlinghouse, asked directly, acknowledged that a post-IPO benefit for XRP holders was possible while immediately adding that it was not in the immediate term. He declined to describe any mechanism and pointed instead to the indirect benefits Ripple already provides.

The community heard a promise. What was actually offered was a conditional acknowledgment of a possibility, attached to an IPO that Ripple says is not a priority, structured through mechanisms that do not exist and would face real legal hurdles.

The gap between those two readings is the entire substance of the story.

The grounding facts cut through the excitement. Ripple and XRP are separate assets, so no benefit flows automatically; any link would be a deliberate, unplanned corporate choice.

The IPO that a benefit depends on is itself not near-term by Ripple’s own account. And the benefit that does exist today is the indirect one Garlinghouse emphasized: Ripple, as the largest XRP holder, has genuine incentives to grow the token’s value, which loosely aligns the company’s success with holders’ even without any special program.

For an XRP holder, the honest conclusion is that a direct IPO reward is a distant possibility worth knowing about but not worth counting on. It is a maybe at the edge of the picture rather than a catalyst at its center.

The door Garlinghouse left open is real, but it is just a door left open, not a path being walked. The difference is exactly the difference between a reasonable hope and the windfall the hype imagined.

Frequently asked questions

Did Ripple promise to reward XRP holders if it goes public?

No. Ripple CEO Brad Garlinghouse, asked whether XRP holders could benefit from a Ripple IPO, said the company might do something special but immediately added that it was not in the immediate term. He did not announce a program, describe a mechanism, or commit to anything; he acknowledged a possibility in response to a direct question. The community amplified this into a promise, but what was actually said was a carefully hedged maybe, attached to an IPO Ripple says is not a priority.

Are Ripple and XRP the same thing?

No, and the distinction is crucial. Ripple is a private technology company that builds payment products, some using the XRP Ledger. XRP is a cryptocurrency, the native asset of the decentralized XRP Ledger, which Ripple does not control. Holding XRP gives you a cryptocurrency, not equity in Ripple, no shares, dividends, or claim on company profits. Ripple is the largest single holder of XRP, but that association is not ownership. That is why a holder benefit would require a deliberate corporate decision.

What could a holder benefit theoretically look like?

Several speculative mechanisms have circulated: early or preferential access to Ripple shares during an IPO allocation, a reward structure tied to long-term XRP holding, or a tokenized representation of Ripple equity for eligible holders. Ripple could also use IPO proceeds to fund ecosystem growth that indirectly benefits XRP. All of these are speculation, not plans, and the more direct versions face real legal and securities-law hurdles, since linking a cryptocurrency to equity benefits raises exactly the questions XRP’s legal history has been about.

Is Ripple going to have an IPO soon?

Not according to Garlinghouse, who said going public is not a priority for Ripple. He cited the underperformance of recent crypto-related public listings as evidence the environment is unfavorable, and emphasized the benefits of staying private. Since the something special was tied to an IPO, and the IPO itself is not near-term, the holder benefit is a possibility contingent on an event that is itself uncertain and not imminent. That pushes the whole scenario into the distant and doubly conditional future.

Do XRP holders benefit from Ripple’s success at all?

Indirectly, yes, by Garlinghouse’s argument. Ripple is the largest XRP holder, so its incentives are genuinely aligned with holders; it profits when XRP rises, just as they do. Ripple’s strategy aims to make XRP the most useful, liquid, and trusted digital asset, and its partnerships and adoption work plausibly increase XRP’s value over time. This indirect benefit is real, though the community finds it insufficient compared to a concrete share of Ripple’s corporate success, which is the dissatisfaction Garlinghouse’s maybe was responding to.

Should I hold XRP because of a possible IPO reward?

A possible IPO reward is a weak basis for a financial decision, because it is a maybe attached to a maybe: an unplanned, undefined benefit contingent on an IPO Ripple does not prioritize. It is better regarded as a distant possible upside not to be counted on than as a catalyst to position around. An XRP holder is better served evaluating the token on its actual merits, its use in payments, its regulatory position, and its adoption, than on speculation about an IPO reward that exists only as a hedged maybe. This is not investment advice.

As of June 21, 2026. Statements and corporate plans can change; this concerns speculative, unannounced possibilities. This article is information, not investment advice.

Worldcoin has fallen nearly 12% while Robinhood has added the token to its trading platform, bringing fresh attention to the project as allegations linked to co-founder Sam Altman continue to weigh on sentiment.

Summary

- Robinhood has added Worldcoin to its crypto trading platform as WLD falls nearly 12%.

- Allegations involving Sam Altman-linked Orb have added fresh pressure on investor sentiment.

- WLD is testing key support near $0.53 ahead of a planned reduction in token unlocks next month.

According to a June 23 X announcement by Robinhood, users of the brokerage platform can now trade Worldcoin (WLD), giving the token exposure to a broader retail investor base despite ongoing market turbulence.

The listing arrives during a difficult period for the project. At the time of writing, Worldcoin (WLD) was trading around $0.53 after dropping almost 15% over the past 24 hours.

Although listings on major exchanges and brokerages often improve liquidity and visibility, traders appeared reluctant to chase the news. The token remains well below its recent June peak near $0.70 despite gaining access to Robinhood’s customer base.

Selling pressure persists despite Robinhood listing

Market attention has increasingly turned toward allegations involving Altman and entities connected to the Worldcoin ecosystem.

A report highlighted by podcaster Katie Miller said internal investigations at Orb, a startup associated with Worldcoin, examined payments allegedly approved by company leadership to a foreign entity. According to the report, those payments were intended to influence the market performance of the WLD token.

The allegations have added another layer of uncertainty around a project that has already faced criticism over its biometric identity verification system and token distribution model.

Earlier this month, Worldcoin also drew attention after BitMEX co-founder Arthur Hayes disclosed that he had sold his WLD holdings. His exit added to concerns among traders already navigating increased volatility across the token.

Token unlock reduction approaches in July

At the same time, Worldcoin is preparing for a change in its token issuance schedule. According to project details, Worldcoin is expected to reduce its token unlock rate beginning on July 24, 2026. Lower unlock rates typically slow the pace at which new tokens enter circulation and can reduce selling pressure from newly released supply.

The planned adjustment has prompted discussion among traders because supply-related changes have historically influenced price action in crypto markets. Yet recent trading suggests investors remain more focused on the controversy surrounding the project than on upcoming tokenomics changes.

Separately, renewed discussion about a potential future public listing of OpenAI has brought additional attention to Altman-linked ventures, including Worldcoin. While no direct connection exists between OpenAI’s corporate plans and Worldcoin’s token economics, the heightened visibility has kept the project in market conversations.

For now, technical indicators suggest traders are becoming increasingly cautious despite Robinhood’s listing. On the daily chart, WLD has retreated to the 61.8% Fibonacci retracement level near $0.53 after failing to hold above $0.60, while the MACD has produced a bearish crossover and its histogram has slipped below zero.

The relative strength index has also fallen sharply from recent highs, signaling fading buying pressure following the token’s rally to nearly $0.70 earlier this month.

A sustained move below $0.53 could open the door for a deeper retracement toward $0.48 and potentially $0.42, whereas a recovery above $0.62 would be needed to ease immediate downside pressure.

The crypto market has been quite unstable (to say the least) lately, with the past 24 hours delivering another substantial correction. Bitcoin (BTC) briefly tumbled below $62,000, while numerous altcoins also entered red territory.

However, DeXe (DEXE) defied the bearish conditions, soaring by double digits over the last day. While several analysts expect further short-term increases, one key technical indicator suggests it might be time for a pullback.

New ATH Soon?

The lesser-known altcoin is currently worth around $23 (per CoinGecko), representing a whopping 50% spike from yesterday’s figure. Its market capitalization has surpassed the psychological $1 billion threshold, making DEXE the 65th-largest cryptocurrency.

Perhaps one of the main catalysts for the rally is MEXC’s support. The prominent crypto exchange included DEXE in its futures trading section, allowing adjustable leverage up to 50x.

The analyst, using the X moniker “The Boss,” claimed that the token “is showing one of the strongest structures” among altcoins, noting buyers’ quick reaction after every pullback. The market observer paid close attention to the $24 resistance level, arguing that if bulls turn it into support, the uptrend could continue to as high as $39. DEXE has been on the market since late 2020 and reached an all-time high of almost $30 the following year, meaning a rise of that magnitude would mark a new historic peak.

OxNeena also chipped in. According to the analyst, DEXE is breaking out of a bullish Cup & Handle formation that could push the price above $27 in the near future.

Time to Short?

Contrary to prevailing optimism, some industry participants anticipate an upcoming correction. Crypto with Haris ₿, for instance, opened a $40,000 short position on DEXE, describing the $22.80-$23.30 area as “very important.”

“If buyers were still fully in control, price should have already reclaimed the recent highs. Instead, DEXE is struggling below resistance while volume is cooling down. That usually happens when a trend starts losing strength,” the analyst explained.

They further predicted that a plunge below $22 could drop the price to as low as $18.

DEXE’s Relative Strength Index (RSI) should also serve as a warning. Its ratio has climbed to 87, meaning that the coin has entered extreme overbought territory and could be due for a pullback. The RSI ranges from 0 to 100; anything below 30 is considered a buying opportunity.

The post DeXe (DEXE) Explodes 50% Despite Crypto Bloodbath: What Comes Next? appeared first on CryptoPotato.

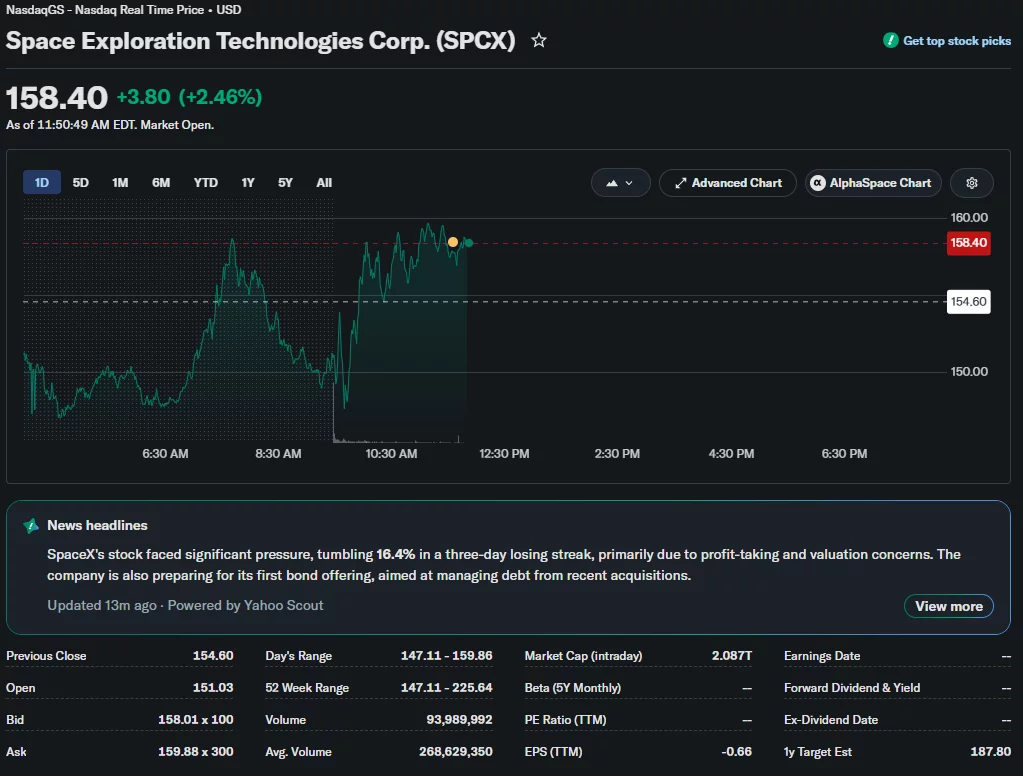

SpaceX stock has remained under pressure after Susquehanna initiated coverage with a $170 price target while warning that the company’s valuation depends on aggressive growth assumptions.

Summary

- Susquehanna initiated SpaceX coverage with a neutral rating and a $170 price target.

- The brokerage warned that the stock’s valuation relies on aggressive revenue and EBITDA growth forecasts.

- Peter Schiff flagged a potential surge in share supply, while ARK Invest continued buying the recent dip.

According to a research note from Susquehanna, the brokerage assigned SpaceX a neutral rating and set a $170 target for the stock as shares continue trading below their $150 debut price following a sharp post-listing rally and subsequent pullback.

The firm projects SpaceX revenue to grow at an 81% compound annual growth rate between 2025 and 2028, while adjusted EBITDA is expected to expand at a 76% CAGR during the same period. Even with those forecasts, Susquehanna cautioned that the stock’s current valuation requires premium multiples and leaves room for multiple outcomes as several of the company’s businesses operate in markets that remain relatively untested.

At current levels, the brokerage said it would prefer to wait for a more attractive entry point before becoming more constructive on the stock.

Analysts point to growth drivers but remain cautious

In its coverage report, Susquehanna highlighted four factors supporting the company’s long-term case. The first was SpaceX’s leading position in the rocket launch industry, which continues to provide a competitive advantage over rivals.

Beyond launch services, the analysts identified Starlink as a major source of future growth. The report also pointed to the company’s early-stage artificial intelligence initiatives and its ability to build large-scale AI infrastructure. Completing the list was CEO Elon Musk, whom Susquehanna described as a proven operator with a record of building and scaling businesses.

Even so, the brokerage argued that much of the expected growth may already be reflected in the current valuation.

As crypto.news reported, analysts at KeyBanc adopted a similar stance on Monday, initiating coverage of SpaceX with a neutral rating. The cautious outlook from both firms has emerged as the company reportedly seeks to raise up to $20 billion through its first bond offering.

Investor attention has also turned to how other high-profile private-market assets have traded after gaining broader access to retail participants. Anthropic pre-IPO futures, for example, have fallen as much as 9% since their Coinbase debut despite the artificial intelligence company announcing a partnership with Micron Technology. The decline suggested traders remained focused on future valuation risks rather than recent business developments.

Supply concerns add to pressure on shares

Elsewhere, economist Peter Schiff raised concerns about the stock’s future supply dynamics in a June 23 X post.

Schiff argued that the relatively small public float helped fuel SpaceX’s explosive first-day gains. However, he warned that the number of shares available for trading could increase substantially over time. According to Schiff, the float may expand from roughly 640 million shares to 7.5 billion shares by Dec. 8, representing an increase of nearly twelvefold.

“That’s a massive supply overhang for a stock priced for perfection and already falling.”

Despite those concerns, some institutional investors have continued adding exposure. As previously reported by crypto.news, ARK Invest purchased over 210,000 SpaceX shares worth nearly $32.5 million after the recent decline.

SpaceX stock fell below its $150 debut price earlier in the session before recovering. Data from Yahoo Finance showed that the shares changed hands around $158.40 at press time, up 2.4% on the day but still down more than 17% over the past five trading sessions.

Crypto World

Specialist Agency Kooc Media Opens Up Dedicated PR Packages for the AI Productivity and Automation Sector

Kooc Media, a PR distribution agency with a track record spanning more than seven years in specialist tech sectors, is now accepting clients from the AI productivity tools and business automation software space. The agency has built out a dedicated service for companies in this category, covering everything from press release writing and guaranteed article placements to full newswire syndication across hundreds of outlets worldwide.

The business case for AI productivity tools has never been stronger. Enterprises are actively investing in automation software that cuts time spent on repetitive tasks, speeds up decision-making and reduces operational overhead. AI agents, workflow automation platforms, intelligent scheduling tools, document processing software and AI-powered communication tools are all seeing strong demand. But demand alone does not guarantee that any single product gets noticed. In a market with this many players, media visibility is what separates the companies that grow quickly from those that struggle to gain traction.

Kooc Media exists to solve that problem.

Why AI Tool Companies Need a Specialist PR Agency

Most PR agencies are generalists. They handle a wide range of clients across many industries and apply a broadly similar approach to all of them. That can work fine for some sectors, but it tends to fall short for AI and automation companies, where the product story requires a degree of technical literacy and the target audience spans both technical evaluators and senior business decision-makers.

A PR agency for AI productivity tools needs to understand what workflow automation actually means to a business, why AI agents are different from traditional software bots, and how to frame a product announcement so it lands with a CTO, a procurement team and a technology journalist all at the same time. That requires focus and experience in the sector — not a generic press release template.

Kooc Media’s editorial team has that focus. The agency produces press release content that describes AI products clearly and accurately, avoiding the kind of empty language that experienced readers tune out immediately. Whether the client is launching a new AI productivity platform, announcing a major enterprise integration, closing a funding round or expanding into a new market, the content is written to inform and persuade the audiences that matter most.

“Companies building AI productivity tools are operating in one of the most competitive software markets in the world right now,” said Michelle De Gouveia, spokesperson for Kooc Media. “Good PR in this space is not about sounding impressive — it is about being credible and being visible to the right people. That is what we focus on delivering for every client.”

Owned Publications and a Wide Distribution Network

Kooc Media’s distribution model is built on two foundations. The first is its own network of established online publications, which includes Blockonomi, CoinCentral, MoneyCheck, Parameter, Beanstalk and Computing. These are real, active websites with indexed content and genuine readerships across finance, technology and business sectors. Clients receive guaranteed placements across these sites as a core part of every package — confirmed published articles, not outreach attempts.

The full network of Kooc Media’s owned publications can be found at kooc.co.uk/sites.

The second foundation is Kooc Media’s partner distribution network, which reaches hundreds of partner websites and thousands of syndicated outlets. For clients that need broader reach, premium packages include distribution to major global platforms. Press releases can be picked up and published on sites including Business Insider, Bloomberg, Benzinga, MarketWatch, USA Today and through Dow Jones news feeds. For an AI automation company building its brand or preparing for a funding raise, that level of coverage builds the kind of third-party credibility that is difficult to achieve through owned channels alone.

All campaigns include complete reporting with live links to every placement secured, so clients always have a clear record of exactly what coverage was delivered.

Free Inclusion in the AgentLocker AI Tools Directory

Every Kooc Media client also receives a complimentary listing in AgentLocker.ai, the AI tools and agents directory owned and operated by Kooc Media. AgentLocker is a dedicated resource for people researching, comparing and selecting AI productivity tools and automation platforms. It covers a broad range of categories including AI writing tools, business process automation, AI agents, enterprise AI software, scheduling tools and more.

Unlike general software directories, AgentLocker is built specifically around AI tools and attracts an audience that is actively looking to adopt or switch AI solutions. Getting listed here puts a client’s product in front of people at exactly the point they are making buying decisions.

This inclusion comes at no additional cost. Every PR client is featured in the directory as a standard part of their campaign, adding a persistent, searchable listing to complement the time-sensitive media coverage generated through press release distribution. For AI productivity companies focused on building long-term discoverability, it is a meaningful benefit.

A Proven Model Applied to a Growing Sector

Kooc Media built its reputation running PR campaigns for crypto and blockchain companies and iGaming operators — two sectors where media presence, speed to market and audience targeting are directly tied to commercial results. The same distribution infrastructure, editorial processes and reporting standards that serve those clients now underpin Kooc Media’s AI PR services.

For AI productivity and business automation companies, this means working with an agency that has already figured out how to deliver consistent, high-quality PR at scale in demanding markets.

About Kooc Media

Kooc Media is a specialist PR distribution agency founded in 2017, serving clients in the crypto, fintech, AI, technology and iGaming industries. The agency operates its own network of online publications and distributes content through a partner network reaching hundreds of outlets globally. Services include press release writing, guaranteed placements, sponsored content and full newswire syndication.

Website: https://kooc.co.uk

AI Directory: https://agentlocker.a

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Ripple has secured preliminary Crypto Asset Service Provider approval from the Luxembourg CSSF under the EU’s MiCA regulation, and XRP dropped 3% on the news. The token is trading at $1.10, down 5% over 24 hours, with the crypto market providing no cover.

The regulatory milestone is real, but was, sadly, not an XRP catalyst. Ripple framed the approval entirely around RLUSD and Ripple Payments infrastructure, with XRP appearing only as something that “underpins” those solutions, a footnote in Ripple’s own announcement about its own network’s native token.

The CASP green light enables regulated crypto-asset services across all 30 countries of the European Economic Area. It does not create a direct demand mechanism for XRP.

Discover: The Best Token Presales

Ripple MiCA Win Is Infrastructure Plumbing, Not an XRP Demand Catalyst

The CSSF’s green light is a “Green Light Letter,” preliminary approval that remains subject to final conditions before full MiCA compliance is conferred. Ripple said that upon full approval, the CASP license, combined with its existing EU Electronic Money Institution (EMI) license, also issued out of Luxembourg, would make it fully MiCA-compliant.

What the approval actually covers is Ripple Payments and RLUSD distribution infrastructure. The commercial pitch is that European banks, fintechs, and corporates can run collection, exchange, and payout through a single Ripple integration across the entire EEA.

There is an additional nuance that the announcement does not resolve. A CASP license authorizes crypto-asset services, but it is structurally distinct from the separate authorization a stablecoin requires to be issued as a MiCA e-money token. Ripple’s announcement touts stablecoin payments infrastructure without clarifying RLUSD’s own standing under MiCA’s non-euro token regime, which caps dollar-pegged stablecoins’ use as a means of exchange in the bloc.

Tether’s USDT, on the other hand, was effectively pushed out of Europe ahead of MiCA’s implementation. Circle, however, brought USDC and EURC into compliance through its EMI. Where RLUSD sits on that spectrum is precisely what institutions will want answered before committing to the integration.

Ripple is also arriving at this milestone late relative to peers. MiCA became fully applicable to crypto-asset service providers in December 2024. Circle secured its approval in April 2025, and B2C2 obtained a CASP license from the Luxembourg CSSF in May 2025. OKX, Coinbase, and Kraken were cleared through the course of 2025.

— Coin Bureau (@coinbureau) June 15, 2026

EU TO DELIST TETHER'S $175 BILLION USDT FROM LICENSED EXCHANGES

EU TO DELIST TETHER'S $175 BILLION USDT FROM LICENSED EXCHANGES

Major exchanges including Binance, Coinbase, Kraken, and Crypto .com have removed USDT for EU users after Tether chose not to seek approval under Europe's MiCA regulations.

Meanwhile, Circle's USDC has secured… pic.twitter.com/HAVrClNkTq

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Ripple’s differentiating argument is the combined EMI-plus-CASP full stack, “one regulated rail for the entire payments flow” backed by over $100 billion in Ripple Payments volume across 60-plus markets and more than 75 licenses globally. That is a credible enterprise pitch. It does not route revenue or demand through XRP.

This pattern is not new. The XRP community publicly pushed back on Ripple’s Swell 2026 agenda last week for prioritizing RLUSD development while the token underperformed. RLUSD’s regulatory queue extends beyond Europe as well, with a California DFAL filing deadline adding another stablecoin-focused regulatory hurdle to the list.

It’s the truth that every major Ripple announcement this cycle has landed as confirmation of the same thesis: the company is building a compliant payments infrastructure in which RLUSD is the product, and XRP is background infrastructure. The MiCA green light has not been priced in just yet – because, structurally, there is nothing in it for XRP to price in.

Discover: The Best Crypto to Diversify Your Portfolio

The post Ripple MiCA Approval Boosts RLUSD, Leaves XRP at $1.10 Support appeared first on Cryptonews.

The US dollar’s rise to a 13-month high is weighing on metals. That has changed the debate around gold, silver, and copper heading into the end of 2026. The key question is which metal can withstand the pressure best.

Because these commodities are priced in dollars, a stronger greenback makes them more expensive outside the US. That puts gold, silver, and copper under the same pressure. The real separation now shows up in the ratios, weekly charts, and bank forecasts for year-end prices.

The Rising US Dollar Index is Pressing Commodities

The starting point for every metal right now is the dollar. The US Dollar Index (DXY), which measures the dollar against a basket of major currencies, has pushed above 100 to a 13-month high.

A stronger dollar makes dollar-priced commodities costlier for the rest of the world, which weighs on gold, silver, and copper. The same force has cooled risk appetite across crypto and stocks.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

The driver is the rate path. With the Federal Reserve seen holding rather than cutting in 2026, real yields stay firm, and the dollar stays bid, which is the headwind behind the recent metals pullback.

With the DXY chart looking strong (bullish rising channel) and rate hikes back on the table, the case for a weaker dollar near term looks thin. That headwind affects the entire metals complex, bringing the focus back to which one holds up best.

The Metals Move as One, So Leadership Is the Real Question

The three metals are pulling in the same direction. Over the past six months, gold (XAU/USD) and silver (XAG/USD) show a correlation of 0.83; silver and copper, 0.72; and gold and copper, 0.61.

Correlation measures how closely two assets move together, where 1.0 is lockstep, and 0 is no link. Readings this high mean one shared trade, not three separate bets.

So the gold, silver, and copper forecast comes down to relative strength inside the complex, not to calling one metal up and another down. The ratios and the weekly charts decide it.

Gold sets the tone for the group, so it is the place to start.

Gold Holds a Falling Channel With Banks Far Apart

(XAU/USD) has traded inside a falling channel since late January, when it peaked near $5,608. A falling channel is a downward drift between two parallel trendlines. Price tried to rebound on March 23, pushed higher, then rolled over again.

On the weekly chart, the line that matters is $4,027. Gold should hold above it. A weekly close under $4,027 opens the door toward $3,249, the prior breakout shelf.

To rebuild strength, gold needs to reclaim $4,400, and a move back above $5,004 would turn the weekly trend constructive again.

The bank split is wide. Goldman Sachs analysts Lina Thomas and Daan Struyven cut their year-end target to $4,900 on June 19, on the view that the Federal Reserve may not cut rates in 2026. JPMorgan sees $6,000 by year end despite the crowded bearish positioning.

Silver shares gold’s bearish pattern, but its chart hides a second setup.

Silver Tracks Gold but Builds a Double Bottom

(XAG/USD) sits in the same falling channel, which the high correlation supports. Underneath it, a double bottom is taking shape, a pattern where price carves two similar lows and hints at a base.

The first hurdle is $66.53, which has already been rejected once. The level that matters is $75.36. A weekly move above the $75 zone would break the falling channel and turn the bias bullish.

The downside is clear if it fails. Under $59.40, the next stops are $52.27 and then $42.12. A larger trigger sits at $89.62, which would complete the double bottom and project a move of roughly 46%, though that is far off.

The fundamentals are supportive. The Silver Institute forecasts a sixth straight annual market deficit in 2026, near 215 million ounces, and the largest on record. Six straight years of deficit means the market is leaning on above-ground stock to fill the gap, a slow squeeze that supports silver over time.

Copper is the other half of silver’s story, the industrial pull, and right now, copper is the AI trade.

AI Trade Highlights Copper, Its Strengths and Problems

Copper has been in a rising channel since 2024. It came close to breaking above that channel on May 11 and again on June 1, where a double top is now forming, a pattern of two failed highs that warns of exhaustion.

The structural case is the AI build-out. Goldman Sachs Research expects data-center power demand to rise about 165% by 2030, and sees grid and power infrastructure driving more than 60% of copper demand growth this decade, at roughly 6 to 8 tonnes of copper per megawatt of capacity.

So why has copper stalled just under its breakout? The AI trade has wobbled, and data-center policy risk has taken some heat out of the ascent. It shows up in the targets. Bank targets now straddle copper’s record price.

JPMorgan’s full-year 2026 average near $12,075 a tonne sits just below it, Goldman recently lifted its year-end call to about $13,735, and Citi is the highest near $15,000.

On the chart, copper needs to hold $6.12. Under it, expect a slip toward $6.04. A weekly break above $6.47 brings $6.68 and then $7.02 into play. The $6.68 level would confirm the real breakout.

In the per-pound terms the chart uses, the targets straddle copper’s current $6.16. JPMorgan’s 2026 average near $5.48 sits below it, Goldman’s raised year-end call near $6.23 is right at it, and Citi is the highest near $6.80, just above the $6.68 breakout.

The ratios between the metals show how this tension is resolving.

The Ratios Tell You Who Is Leading

Three ratios frame the macro tape. The gold-silver ratio has climbed from about 44 in January to 66 now. That is a risk-off tilt favoring gold, though 66 is not yet extreme enough to scream silver is cheap.

The gold-oil ratio has risen from about 41 on May 19 to 56, a stress reading where gold is strong and oil is weak.

The silver-copper ratio cuts the other way. It has fallen from about 19 in January to 10, with copper leading, a classic industrial-demand signal.

That is the core tension. Gold and oil say risk-off, silver and copper say industrial growth, and silver gets squeezed between the two regimes.

Put together, the three charts point to a clear pecking order into year-end.

The Gold, Silver, and Copper Forecast Into End-2026

Copper is the structural leader. The AI and grid demand story is the strongest multi-year case of the three, but the chart has stalled at a double top, and most 2026 bank targets imply a near-term pullback from record levels.

Gold is the macro anchor. It carries the widest bank disagreement, a $1,100 gap between Goldman at $4,900 and JPMorgan at $6,000, and it leads only if stress and rate cuts dominate.

Silver is the high-beta wildcard. It lags both, yet a record supply deficit and a building double bottom give it the most catch-up room if either the macro or the industrial bid strengthens.

The dollar is the switch. So while the DXY holds above 100, the complex stays capped, and copper’s $6.12 is the line that separates a fresh AI-led leg higher from a double-top unwind that pulls silver and gold down too. All thanks to the positive correlation between the three.

The post Gold, Silver or Copper: Which Commodity Looks Best Heading into the End of 2026? appeared first on BeInCrypto.

The House Financial Services Committee has scheduled back-to-back hearings on July 14 and July 17, one covering Federal Reserve monetary policy, the other focused directly on the CLARITY Act. This is giving supporters of comprehensive crypto regulation their highest-profile platform yet as the pre-recess window narrows.

As of today, the bill has cleared the Senate Banking Committee, been placed on the Senate legislative calendar, and attracted a House fast-track commitment if the Senate moves first. None of that changes the core arithmetic: the CLARITY Act needs 60 votes on the Senate floor, and Republicans currently hold 53 seats.

Senator Cynthia Lummis, the Wyoming Republican leading the Senate push, has set the end of July as a hard deadline. She also warns explicitly that missing the pre-recess window could delay enforceable digital asset market structure rules until 2030.

Discover: The Best Crypto to Diversify Your Portfolio

The 60-Vote Clarity Act Problem

The gap between “placed on the Senate legislative calendar” and “signed into law” runs through a specific procedural bottleneck. Invoking cloture to cut off debate requires 60 votes; with a 53-seat Republican majority, the CLARITY Act needs at least seven Democratic crossovers. The Senate Banking Committee vote on May 14 produced only two Democratic votes from Ruben Gallego and Angela Alsobrooks, and it is leaving five or more additional Democratic senators to be secured before a floor vote can succeed.

A bipartisan ethics provision in the bill has been fracturing Democratic support further, and Fox Business reporter Eleanor Terrett described the original White House target of July 4 as “logistically impossible” before the date even arrived. Galaxy Research has pegged passage odds at roughly 60% and notes that the window “effectively closes” once the August recess begins.

Even if the Senate floor vote clears 60, the bill would then require reconciliation with the version the House passed in July 2025 by 294–134. Rep. Dusty Johnson pledged on June 18 that the House would act “swiftly” on any Senate text, compressing that step, but reconciliation differences still have to be resolved before the bill reaches the president’s desk.

If this misses the pre-recess window, the next viable legislative opening is 2027 at the earliest, with some analysts pointing further out. The same credible basis for Lummis’s 2030 warning.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

July 14 and July 17: What To Expect?

The July 14 session before the House Financial Services Committee is formally structured around the Federal Reserve’s semi-annual Monetary Policy Report. However, its market significance extends further. It is reported that Kevin Warsh will deliver his first congressional testimony as Fed Chair, making it the first opportunity for lawmakers to publicly interrogate the new leadership’s posture on rate policy, dollar strength, and the regulatory perimeter around financial innovation.

For crypto markets, Warsh’s framing of digital assets, whether he treats them as a monetary policy variable or a separate regulatory question, will carry weight heading into the CLARITY Act hearing three days later.

The July 17 hearing moves the focus explicitly to the CLARITY Act and digital-asset innovation, with the notable detail that it is being held in New York rather than Washington. That venue choice is deliberate: New York is the largest U.S. financial center, and holding the hearing there anchors the bill’s stakes to institutional finance rather than abstract legislative process. Exchanges, custody providers, and capital markets participants concentrated in the city represent the economic constituency that regulatory uncertainty is actively costing.

Together, the two hearings give the bill’s backers a sequenced argument: monetary policy context on the 14th, market-structure specifics on the 17th. The CFTC’s expanded role under the bill, and the digital asset market structure framework it would codify, will be front and center at the New York session. The hearing is a narrative event. The execution event is the floor vote that has to follow it.

Discover: The Best Token Presales

The post Senate’s 60-Vote Gap Looms Over CLARITY Act Before August Recess appeared first on Cryptonews.

The European Parliament has advanced legislation for a digital euro, bringing the EU closer to launching a central bank digital currency, while the U.S. moves to restrict similar efforts.

Summary

- EU lawmakers backed digital euro legislation, moving the ECB closer to a potential 2029 launch.

- The ECB says the digital euro would complement cash and reduce reliance on foreign payment networks.

- Meanwhile, the U.S. Senate approved a bill that would block the Federal Reserve from issuing a CBDC until 2030.

According to a June 23 decision by the European Parliament’s Economic and Monetary Affairs Committee, lawmakers backed the proposed framework for a digital euro, a key step in the legislative process that could pave the way for a launch by 2029.

The vote arrives as European policymakers examine the region’s dependence on foreign payment infrastructure. Data cited by the European Central Bank shows that Visa and Mastercard handle 61% of card payments in the euro area and nearly all cross-border card transactions.

European officials have argued that a digital euro could strengthen the bloc’s payment system by providing a public digital payment option issued directly by the ECB. Under the proposal, consumers would hold digital euros in dedicated wallets, while banks and payment providers would offer services connected to the system.

The digital euro remains under development

Within the proposed framework, the ECB would operate the core infrastructure while financial institutions would manage customer-facing services. According to the proposal, the system could support both online and offline payments and include privacy safeguards for users.

Holding limits for digital euro wallets have not yet been finalized and remain part of ongoing negotiations among European institutions.

European authorities have repeatedly stated that the digital euro is intended to complement physical cash rather than replace it. Following the committee vote, the ECB welcomed the outcome, stating that the European Parliament’s position supports both the preservation of euro cash as legal tender and the development of a digital version of the currency.

Although the ECB has warned that stablecoins could create risks for the financial system, the central bank has continued to support the digital euro project as part of its long-term payments strategy.

Elsewhere in Asia, central banks are also exploring digital finance initiatives. As reported by crypto.news, Bank of Korea Governor Shin Hyun-song said in his inaugural speech in April that the central bank would support innovation in blockchain-based finance while maintaining the stability of South Korea’s payment and settlement systems. He added that the bank would work to strengthen the role of the Korean won in an increasingly digital financial environment.

U.S. lawmakers take the opposite route

While Europe advances work on a central bank-issued digital currency, policymakers in the U.S. are pursuing a different approach.

The U.S. Senate recently approved the 21st Century ROAD to Housing Act in an 85-5 vote. Included in the legislation is a provision that would prevent the Federal Reserve from creating a CBDC or a similar asset before the end of 2030.

The Senate’s position aligns with President Donald Trump’s support for privately issued stablecoins rather than a Federal Reserve-backed digital currency.

At the same time, U.S. lawmakers continue to work on crypto-specific legislation. The CLARITY Act, which seeks to establish a clearer regulatory framework for digital assets, remains under consideration as Congress debates the future structure of the country’s crypto market.

The U.S. Senate has approved a sweeping bipartisan housing bill that bans the Federal Reserve from issuing a CBDC until 2030.

The bill passed by a strong 85-5 vote and awaits action in the House, where leadership and committee members reportedly plan to advance it quickly.

CBDC Ban Advances Through Housing Package

The housing package is designed to make homes more affordable and reduce competition from corporate firms. Interestingly, one of its provisions prevents the Fed from issuing a U.S. central bank digital currency (CBDC) for up to 4 years.

“Agreed to, 85-5: Motion to concur in the House amendment to the Senate amendment to H.R.6644, 21st Century ROAD to Housing Act,” wrote the Senate.

Lawmakers were said to be considering a fast track that could see the bill signed into law as early as Tuesday, with House Financial Services Committee Chairman French Hill saying he “looks forward to the House moving quickly to advance this bill to President Trump’s desk.”

Senate Chair Tim Scott added that it is time for the American people to get real relief, and Ranking Member Elizabeth Warren called it the biggest housing bill in over 30 years.

The latest development follows months of negotiation, during which the Senate first added the anti-CBDC provision in March, after which the House cleared the amended version in May.

President Donald Trump signed an executive order in January 2025 banning his administration from creating a CBDC, citing concerns that it would threaten the U.S. financial system and individual privacy. However, because this would only apply under his tenure, his allies in Congress pushed to include the restriction in the unrelated housing bill.

House Schedules July CLARITY Act Hearing

As lawmakers prepare for key meetings over the next few weeks, momentum is building around the CLARITY Act. The House Financial Services Committee said it will hold a hearing in New York on July 17 to look at the impact the legislation will have on financial innovation.

Senator Cynthia Lummis has been one of the biggest supporters of the proposal, often taking to social media to urge lawmakers to act faster. In her latest commentary, the Republican warned that regulatory uncertainty has driven talented developers overseas.

But there have been serious repercussions for others, like Tornado Cash developer Roman Storm, who was found guilty of knowingly transmitting more than $1 billion in criminal proceeds. The DOJ also pushed for a retrial after the jury deadlocked on charges of money laundering and sanctions violations.

The post US Senate Clears Housing Bill That Also Halts CBDC Push appeared first on CryptoPotato.

But Slavin said firms appear reluctant to wait. “Even though the regulations and the rails aren’t fully ready yet, they want to get products out,” he said.

Wall Street believes that blockchain networks could eventually become a new distribution channel for traditional investment products. Tokenized funds could allow investors to hold and transfer fund shares around the clock, potentially reducing settlement times and expanding access to global investors.

One concern emerging for fund issuers, according to Slavin, is that tokenized versions of well-known ETFs are already trading on platforms outside traditional financial markets, often without direct involvement from the fund sponsors themselves.

“There are ETFs, like hundreds of them, that are trading in unregulated markets around the world,” he said.

Because anyone can theoretically create a tokenized representation of a publicly traded fund, issuers face the prospect of products bearing their names circulating beyond their oversight.

“It’s opaque,” he said. “It effectively creates a reputation risk, even though it’s not at all affiliated, frankly, with the asset manager.”

That dynamic has become a growing topic of discussion among BNY’s asset-management clients as they evaluate their own tokenization strategies. Similar to the early days of bitcoin and crypto trading, the technology is evolving faster than the rules governing it.

Clear Blue Technologies International Inc. (CBLU:CA) Q4 2025 Earnings Call Transcript

Robinhood lists Worldcoin as Sam Altman faces fresh scrutiny

Most Hated Fast And Furious Movie Is A Streaming Megahit On Peacock

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Miami – Corporette.com

-

Tech7 days ago

Tech7 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Entertainment3 days ago

Entertainment3 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech1 day ago

Tech1 day agoMicrosoft accidentally kills epic Outlook email threads

-

Business3 days ago

Business3 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics5 days ago

Politics5 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Business4 days ago

Business4 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Tech5 days ago

Tech5 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World4 days ago

Crypto World4 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Politics3 days ago

Politics3 days agoAndy Burnham and the meaning of Makerfield

-

Crypto World3 days ago

Crypto World3 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World3 days ago

Crypto World3 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech22 hours ago

Tech22 hours agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Sports5 days ago

Sports5 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

-

Business5 days ago

Business5 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Business3 days ago

Business3 days agoMHP SE 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MHPSY) 2026-06-20

-

Tech2 days ago

Tech2 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

NewsBeat4 days ago

NewsBeat4 days agoKeir Starmer Allies Question His Chances For No 10

-

Entertainment4 days ago

Entertainment4 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Crypto World5 days ago

Crypto World5 days agoAnthropic’s Dario Amodei Urged AI Unity at G7, Even as US Banned His Models

You must be logged in to post a comment Login