Crypto World

What are perpetual futures? Perps, funding rates, and liquidations explained

Perpetual futures, or perps, are the most traded instrument in crypto. They let you bet on price with leverage and never expire, held in line with the spot market by a clever fee called the funding rate. They are powerful, they are dangerous, and in 2026 they are finally arriving onshore in the United States.

Summary

- Perpetual futures let traders take leveraged long or short positions without an expiry date, using funding rates to keep prices aligned with the spot market.

- Funding payments flow between longs and shorts, while leverage and margin determine how quickly a position can be liquidated during adverse price moves.

- Crypto perps have begun entering regulated U.S. markets in 2026, bringing the industry’s most traded derivative product into a new regulatory framework.

A perpetual future, usually shortened to perp, is a derivative contract that lets a trader bet on the price of an asset with leverage and hold that bet open indefinitely, because unlike a traditional futures contract it has no expiration date. The price of a perp is kept tethered to the real spot price of the underlying asset by a recurring payment between traders called the funding rate, which nudges the contract back toward the market whenever it drifts.

Perps let you go long if you think the price will rise or short if you think it will fall, control a position far larger than the cash you put down, and never worry about a contract expiring out from under you. That combination has made perpetual futures the single most heavily traded product in all of crypto, and also one of the fastest ways to lose money in it.

This guide explains perpetual futures in plain English, with no derivatives background assumed. It covers what a perp actually is, the traditional futures contract it evolved from, the funding-rate mechanism that makes the whole thing work, how leverage and margin lead to liquidation, the difference between mark price and index price that decides when you get liquidated, where perps are traded and the major shift happening in the United States in 2026, the real risks that blow up accounts, and why this instrument came to dominate crypto trading.

By the end, you will understand not just how to read a perp but why it behaves the way it does, and why even regulators who now permit it call it a product to treat with respect.

What a perpetual future actually is

The name packs two ideas together. “Future” means it is a contract whose value is derived from the price of something else, a derivative, where you agree to gain or lose money based on how that price moves without necessarily owning the asset. “Perpetual” means the contract never expires, so you can hold the position open for as long as you like and your margin allows.

That second word is the whole innovation. A perp lets you take a leveraged bet on, say, Bitcoin, and simply keep it open, adjusting or closing whenever you choose, with no expiry forcing your hand. You can go long, profiting if the price rises, or short, profiting if it falls, and because the contract is leveraged, you can put down a fraction of the position’s value as collateral, called margin, and control the full size.

If you post one thousand dollars at ten times leverage, you control a ten-thousand-dollar position, so a ten percent move in your favor doubles your collateral, and a ten percent move against you wipes it out. The perp itself is settled in cash or a stablecoin, so you never have to take delivery of the underlying asset; you are trading the price, not the coin.

The product was invented by the crypto exchange BitMEX in 2016, and it spread because it fit crypto perfectly: traders wanted leverage, they wanted to bet in both directions, and they did not want the friction of contracts that expire and have to be rolled over. The perp gave them a single instrument that did all of that, and the rest of the market followed.

Futures first: the contract perps evolved from

To see what makes a perp special, it helps to understand the ordinary futures contract it grew out of, because the perp is essentially a futures contract with its biggest inconvenience removed.

A traditional futures contract is an agreement to buy or sell an asset at a set price on a specific future date. If you buy a Bitcoin futures contract expiring in three months, you are locking in a price now for settlement then, and when that date arrives, the contract expires and settles.

This is useful, and it is how commodities and financial futures have worked for a very long time, but it has an awkward feature for someone who simply wants ongoing leveraged exposure: the contract ends. If you want to keep your position past the expiry, you have to “roll” it, closing the expiring contract and opening a new one further out, paying costs and friction each time. Traditional futures also have a “basis,” a gap between the futures price and the spot price that opens and closes as expiry approaches, which adds complexity.

The perpetual future strips out the expiry entirely. There is no settlement date, so there is nothing to roll and no countdown forcing you to act. But removing the expiry creates a new problem. In a normal future, the looming settlement date is what drags the contract price toward the real spot price, because at expiry they must converge.

Take away the expiry, and you remove the very thing that keeps the contract honest. So the designers of the perp had to invent a replacement, a mechanism that would keep a never-expiring contract anchored to the spot price using market forces instead of a deadline. That mechanism is the funding rate, and it is the beating heart of every perp.

The funding rate: the mechanism that keeps perps honest

The funding rate is the single most important concept in perpetual trading, and it is the part beginners most often miss until it quietly costs them money.

Because a perp never expires, nothing automatically forces its price to match the spot price of the underlying asset. Left alone, a perp could drift well above or below the real market. The funding rate fixes this by creating a recurring payment, typically every eight hours, between the two sides of the market.

When the perp trades above the spot price, meaning demand to be long is too strong, the funding rate is positive, and longs pay shorts. When the perp trades below the spot price, meaning shorts are crowded, the funding rate is negative, and shorts pay longs. The payment is a small percentage of position value, and it flows directly between traders, not to the exchange.

The effect is elegant. If too many people are long and the perp price runs above spot, longs must keep paying a fee to shorts, which makes holding a long more expensive and encourages traders to close longs or open shorts, pushing the price back down toward spot. The mechanism is self-correcting: whichever side is crowded pays the other, and that cost pulls the contract back in line with the real market.

This is why a perp tracks spot closely without ever expiring. It also turns the funding rate into a live sentiment gauge, because a strongly positive rate tells you the market is aggressively long and paying for the privilege, while a negative rate tells you shorts dominate. Traders watch funding both as a cost they must pay or earn and as a signal of how the crowd is positioned. Even regulators who have studied perps note that funding rates, far from being a trick, perform roughly the same economic job as the costs of repeatedly rolling expiring futures, just packaged differently.

Leverage, margin, and the liquidation that follows

Leverage is what makes perps thrilling and what makes them lethal, so it is worth being precise about how it actually works and where it ends.

When you open a perp position, you post collateral, called margin, and the exchange lets you control a position several times larger. The multiple is your leverage. At five times leverage, a thousand dollars of margin controls five thousand dollars of exposure; at twenty times, it controls twenty thousand. Leverage magnifies both directions equally. A favorable move multiplies your gains against your small margin, and an unfavorable move multiplies your losses just as fast. The crucial consequence is that with leverage you do not need the price to go to zero to lose everything. You only need it to move against you by a fraction equal to your margin.

That is where liquidation comes in. Every leveraged position has a liquidation price, the level at which your losses have eaten through your posted margin. If the market reaches that price, the exchange automatically closes your position to prevent your losses from exceeding your collateral, and your margin is gone. At ten times leverage, a roughly ten percent move against you is enough to trigger liquidation; at twenty-five times, about four percent will do it; at one hundred times, a one percent flicker can end the trade.

Offshore venues have historically offered enormous leverage, and the extreme figures sometimes quoted, fifty, one hundred, even more, are a hallmark of those unregulated platforms. Regulated perpetual products in the United States are subject to the same leverage limits as other regulated futures, which are far lower. High leverage does not make you more likely to be right; it only makes you more likely to be liquidated before you are proven right, and that distinction has emptied more accounts than any single price crash.

Mark price versus index price: why you actually get liquidated

A detail that confuses many new perp traders, and burns some of them, is that the price used to decide your liquidation is not always the last traded price on the exchange. Understanding this can be the difference between a survivable trade and an avoidable wipeout.

Exchanges track two prices. The index price is an average of the spot price across several major markets, a clean reading of what the asset is really worth right now. The mark price is a smoothed, fair value derived largely from that index, and it is the price the exchange uses to calculate your unrealized profit, your losses, and your liquidation.

Why not just use the last traded price on the perp itself? Because the last traded price on a single venue can spike or crash briefly during a moment of thin liquidity or a manipulation attempt, and if liquidations were based on that, a momentary wick could liquidate thousands of traders unfairly. By marking positions to a broad index-based fair value instead, the exchange protects traders from being liquidated by a fleeting, unrepresentative blip on one order book.

The practical lesson is that you are liquidated when the mark price, not necessarily the screaming candle on the chart, reaches your liquidation level. Most of the time, mark and last price are nearly identical, but in violent moments they can diverge, and knowing which one governs your position is part of trading perps without nasty surprises. It is also why checking your exact liquidation price before entering a trade, and giving yourself a wide margin of safety, matters far more than guessing where the price “should” go.

Where perps are traded, and the 2026 shift onshore

For most of their history, perps lived offshore, outside the reach of United States regulators, and that map is being redrawn right now in a way every trader should understand.

On centralized exchanges, perps are a flagship product, with venues such as Binance, Bybit, OKX, Deribit, and the original inventor BitMEX offering deep perpetual markets in hundreds of assets. A newer wave runs perps fully on-chain through decentralized exchanges, where trades settle on a blockchain, and users keep custody of their funds.

Hyperliquid has risen to dominate on-chain perpetual trading, alongside established names like dYdX and GMX, proving that a decentralized venue can match the speed and depth traders once thought only centralized platforms could provide. For years, United States traders were largely walled off from regulated crypto perps, pushing demand offshore.

That wall is now coming down. In May 2026, the Commodity Futures Trading Commission approved a Bitcoin perpetual futures contract from the prediction-market exchange Kalshi, the first regulated crypto perp cleared for United States traders, and Kalshi quickly expanded into perps tied to Ethereum, XRP, and others, reporting more than five billion dollars in trading volume within weeks. Coinbase secured its own regulated route to offer perpetual products domestically.

The arrival has not been smooth. The CME Group, the giant traditional derivatives exchange, sued the CFTC, arguing that perpetual futures should be regulated as swaps under the Dodd-Frank Act rather than as ordinary futures, and that the regulator bypassed proper procedure.

The CFTC’s chair has pushed back publicly, arguing that nothing in the law requires a futures contract to have a fixed expiration date, that regulated perps face the same leverage limits as other United States futures rather than the extreme offshore multiples, and that funding rates are a legitimate pricing mechanism. However that legal fight resolves, the direction is clear: the most popular instrument in crypto trading is moving from the offshore shadows into regulated American markets, and the rules for it are being written in real time.

The risks: why perps blow up accounts

Perps deserve their fearsome reputation, and an honest guide has to be blunt about why so many traders lose, because the dangers are structural, not just a matter of bad luck.

The first and largest risk is leverage itself. The same multiplication that makes a winning perp trade so satisfying makes a losing one fatal, and at high leverage a small, ordinary price move is enough to liquidate you entirely, which is why most accounts that chase big leverage do not last. The second is liquidation cascades.

When prices move sharply, waves of leveraged positions hit their liquidation prices at once, and the forced selling or buying pushes the price further in the same direction, triggering still more liquidations, a self-reinforcing spiral that can turn a modest move into a violent one and catch even careful traders. The third is funding cost. Holding a position on the crowded side of the market means paying funding every few hours, and over time that steady drain can quietly erode or erase a position that the price action alone would have left profitable.

The fourth is the psychological trap: perps are available around the clock, they encourage constant action, and the leverage makes every move feel urgent, which pushes traders toward overtrading, revenge trading after a loss, and holding losers too long. The fifth, on offshore venues especially, is platform and counterparty risk, because you are trusting the exchange’s solvency, its liquidation engine, and its honesty with your collateral.

The uncomfortable summary is that perps are a professional’s instrument that retail traders can access with one tap, and the gap between those two facts is where the damage happens. The product is not a scam, and the mechanics are sound, but the combination of high leverage, constant availability, and human emotion is genuinely hazardous, and that is true no matter how confident any individual trade feels.

A worked example: one long trade, from open to liquidation

Numbers make the danger concrete in a way definitions cannot, so walk through a single leveraged trade step by step, because every concept in this guide shows up in the life of one position.

You have one thousand dollars, and you are convinced Bitcoin is about to rise. You open a long perp at ten times leverage, so your one thousand dollars of margin now controls a ten thousand dollar position.

The exchange shows you a liquidation price roughly ten percent below where you entered, because a ten percent move against a ten-times position consumes your entire margin. You are also told the funding rate is positive, meaning longs are crowded, and you will pay a small fee to shorts every eight hours for as long as you hold. The trade is on.

Suppose Bitcoin rises five percent. Your position gained five percent of ten thousand dollars, or five hundred dollars, which is a fifty percent return on your one thousand dollar margin. This is the seduction of leverage: a modest move produced an outsized gain. Now suppose instead that Bitcoin falls.

At a four percent drop, you are down four hundred dollars and nervous. At a move near ten percent against you, the mark price reaches your liquidation level, the exchange automatically closes the position, and your one thousand dollars is gone. Notice what did not happen: Bitcoin did not crash, it did not go to zero, it simply moved ten percent, an ordinary day in crypto, and your account was wiped out.

Had you used two times leverage instead of ten, the same ten percent drop would have cost you two hundred dollars, painful but survivable. Had you used one hundred times leverage, a one percent flicker would have ended you.

Layer in the funding cost and the picture sharpens further. If you held that crowded long for several days, you paid funding every eight hours the whole time, a steady drain that eats into gains and deepens losses. And if the market dropped sharply, your liquidation might have been one of thousands firing at once, the forced selling pushing the price down faster and triggering still more liquidations around you. One trade, and you have lived through leverage, margin, the liquidation price, the mark price, funding cost, and a liquidation cascade. That is why experienced traders obsess over position size and liquidation distance before they ever think about where the price is going.

Why perps took over crypto trading

For all the danger, perps did not come to dominate by accident, and understanding why explains a great deal about how crypto markets actually function. A perp gives a trader almost everything they could want in a single instrument: leverage to amplify a view, the ability to profit in both rising and falling markets, no expiry to manage, a price kept honest by funding, and deep liquidity that makes entering and exiting easy. For speculators, it is the sharpest tool available. For sophisticated participants it is also a hedging instrument, a way to offset the risk of a spot holding or to manage exposure without buying or selling the underlying coin. That versatility is why perpetual futures now account for the large majority of all crypto trading volume, dwarfing the spot market most newcomers assume is the main event.

The instrument that BitMEX dreamed up in 2016 has become the center of gravity of crypto markets, and in 2026 it is crossing from the unregulated fringe into the regulated mainstream, with traditional exchanges fighting over how it should be classified. That trajectory tells you something important: perps are not a passing fad but a durable financial innovation that traditional finance is now scrambling to adopt and contain. The right way to approach them is with respect. Understand the funding rate, know your liquidation price, treat leverage as the dangerous tool it is, and never confuse the thrill of a leveraged win with skill. The traders who survive perps are the ones who understand the machinery before they ever pull the lever.

Frequently Asked Questions

What is a perpetual future in simple terms?

A perpetual future, or perp, is a contract that lets you bet on the price of an asset with leverage and hold the bet open with no expiration date. You can go long if you think the price will rise or short if you think it will fall, and you post a fraction of the position’s value as collateral, called margin, to control a much larger position. The perp’s price is kept close to the real spot price by a recurring payment between traders called the funding rate. It settles in cash, so you never own the underlying asset.

How does the funding rate work?

Because a perp never expires, nothing automatically keeps its price matched to the spot market, so the funding rate does that job. Roughly every eight hours, a payment flows between longs and shorts. When the perp trades above spot, longs pay shorts, which makes being long costlier and pushes the price back down. When it trades below spot, shorts pay longs. The payment goes between traders, not to the exchange, and it both keeps the perp anchored to spot and signals which side of the market is crowded.

What is liquidation in perpetual trading?

Liquidation is when the exchange automatically closes your leveraged position because your losses have consumed your posted margin. Every leveraged position has a liquidation price, and if the market reaches it, your collateral is gone. The higher your leverage, the smaller the move needed to liquidate you: at ten times leverage about a ten percent move against you is enough, and at one hundred times around one percent will do it. Liquidations are usually triggered by the mark price, a fair value based on a broad index, not the last traded price on a single venue.

Why are perps so risky?

The core risk is leverage, which multiplies losses as fast as gains, so a small price move can wipe out a highly leveraged account. Liquidation cascades can make sharp moves worse, as forced closures push the price further and trigger more liquidations. Funding costs can quietly erode a position held on the crowded side of the market. Perps are also available around the clock and encourage emotional overtrading, and on offshore venues you take on the platform’s solvency and honesty as additional risks.

Where can you trade perpetual futures?

Perps trade on centralized exchanges such as Binance, Bybit, OKX, Deribit, and BitMEX, and increasingly on decentralized exchanges that settle on-chain, where Hyperliquid, dYdX, and GMX are leading venues. For years, United States traders were largely excluded from regulated crypto perps, but that changed in 2026 when the CFTC approved a Bitcoin perpetual contract from Kalshi, and Coinbase gained a regulated route, bringing perps onshore even as exchanges like CME dispute how they should be classified.

Who invented perpetual futures?

The perpetual swap was created by the crypto exchange BitMEX in 2016. It caught on quickly because it suited crypto traders perfectly: it offered leverage, allowed betting in both directions, and removed the expiry and rollover hassle of traditional futures, all in a single instrument anchored to spot by the funding rate. The design spread across the industry, and perpetual futures now account for the majority of all crypto trading volume.

This article is educational and does not constitute financial or investment advice. Perpetual futures are high-risk leveraged products, and the rules governing them, especially in the United States, are changing quickly. As of June 22, 2026, verify current product details, leverage limits, and regulatory status with official sources, and never trade with money you cannot afford to lose.

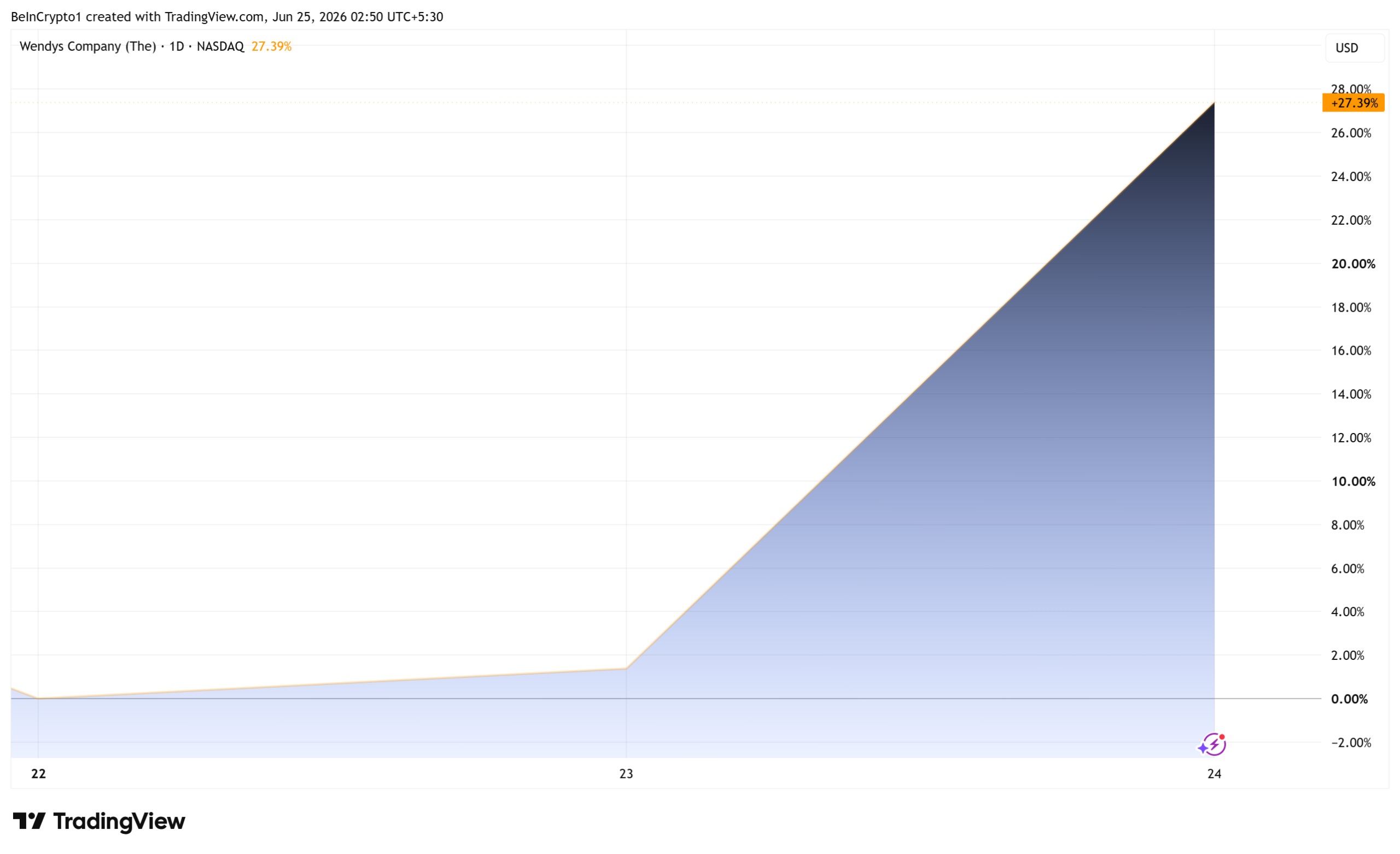

Wendy’s stock climbed almost 30% on Wednesday after traders on Reddit’s WallStreetBets forum rallied behind the struggling burger chain, reviving the meme-stock playbook that powered GameStop in 2021.

The rally lifted Wendy’s shares (WEN) to an intraday high near $8.89 and triggered at least one volatility halt, even as sales keep sliding.

Why Wendy’s Stock Drew a Short Squeeze

The move started with a since-deleted WallStreetBets post that urged members to rescue the chain before it collapsed. Copycat posts showing share and options purchases quickly followed.

“Save Wendy’s before it’s too late,” the post read.

Follow us on X to get the latest news as it happens

Volume confirmed the frenzy. More than 202 million shares changed hands, over 15 times the recent average.

The stock logged its biggest single-day gain since March 2020, CNBC reported. Wendy’s had ended the prior session near $6.26, not far from a multiyear low.

The squeeze setup is real but far smaller than 2021. About 23% of Wendy’s float was sold short before the rally, according to S3 Partners. The same firm put GameStop’s short interest above 140% of its float ahead of the 2021 squeeze.

Rising prices can still force shorts to buy back stock, which pushes prices higher. That pattern drove the AMC and GameStop squeeze, and it resurfaced this year during the GameStop meme stock frenzy.

A CFO Hire Gives Bulls a Story

Sentiment had a fundamental hook too. Wendy’s named Steve Cirulis chief financial officer on June 23, succeeding Ken Cook, according to a regulatory filing.

Cirulis ran finance at Potbelly alongside Bob Wright, now Wendy’s CEO. The company credits the pair with a more than 500% gain in Potbelly’s share price during their tenure.

That record gave retail buyers a turnaround story to chase, a familiar driver of meme driven market moves. The hire builds on a recovery plan the company calls Project Fresh.

Fundamentals Still Point Down

The business behind the rally remains weak. US same-restaurant sales fell 7.8% in the first quarter, and net income slid to $22.7 million.

Quarterly earnings still beat reduced forecasts, yet the rally rests on sentiment rather than results.

Wendy’s has been here before. A June 2021 Reddit post hailed Wendy’s as the perfect WallStreetBets stock and briefly drove shares up 26%. That rally faded within weeks because almost none of the stock was sold short.

This time a crowded short base gives the move real fuel. Still, most names lifted by Reddit traders and markets eventually gave back their gains.

Wendy’s gains holding may depend on how long the crowd stays interested.

The post Wendy’s Stock Climbs 30% as WallStreetBets Targets a GameStop Repeat appeared first on BeInCrypto.

![]()

Kalshi is seeking to raise fresh capital at a valuation of about $40 billion, nearly doubling the $22 billion valuation it targeted in its previous funding round, according to a Financial Times report citing people familiar with the matter.

The prediction markets platform could close the fundraising as soon as the third quarter of this year, FT said.

If completed, the deal would widen Kalshi’s valuation lead over rival Polymarket, which was last reported to be seeking funding at $15 billion. The two platforms have emerged as the dominant names in the prediction markets sector, while many other entrants have increased the industry’s competitive landscape.

Kalshi’s previous funding round, which valued the company at $22 billion, attracted a roster of high-profile investors including Philippe Laffont’s Coatue Management, Sequoia Capital, Andreessen Horowitz and Morgan Stanley.

Competition in the sector has intensified as firms race to capture users and expand product offerings.

Kalshi operates as a federally regulated exchange in the United States, a distinction that has helped it attract mainstream investors and institutional backing. Meanwhile, Polymarket, which uses blockchain infrastructure and cryptocurrency-based settlement, has gained popularity among crypto traders and has become widely followed during recent election cycles.

Michelle Bond, the wife of Ryan Salame—former co-CEO of FTX Digital Markets—has been scheduled for trial in November following delays tied to motions connected to Salame’s plea agreement. The proceeding comes as prosecutors pursue remaining criminal accountability related to the 2022 collapse of FTX, an episode that has since reshaped regulatory scrutiny of crypto-linked political activity and financial crime controls.

On Wednesday, U.S. District Judge George Daniels of the Southern District of New York set Bond’s trial to begin on Nov. 9. Bond faces four charges alleging violations of U.S. campaign finance law, stemming from prosecutors’ claims that FTX-related money was used to improperly support a 2022 congressional bid.

Key takeaways

- Judge George Daniels ordered Michelle Bond’s criminal trial to start on Nov. 9 in the Southern District of New York.

- Bond is charged with four offenses related to alleged campaign finance violations connected to the 2022 U.S. House race in New York’s 1st district.

- Prosecutors alleged that Ryan Salame used FTX funds in a “sham” payment arrangement, which they said violated campaign finance rules.

- The case is part of the final criminal track arising from FTX’s 2022 bankruptcy, following convictions and prison sentences for other key figures.

Bond’s trial date set amid motion-related delays

Bond’s schedule reflects procedural disputes that have continued since the charges were brought. A week earlier, Judge Daniels denied a motion by Bond seeking dismissal of the indictment. According to reporting by Cointelegraph, the defense argued that prosecutors had promised Salame he would not be charged if he pleaded guilty—an issue that, if accepted, could have materially affected Bond’s exposure.

With the dismissal attempt rejected, the court moved forward to establish a firm trial start date. For compliance and legal teams, the decision is significant because it underscores how plea negotiations and alleged assurances can become contested topics in later proceedings involving related defendants, even when one defendant has already resolved the matter through a plea agreement.

Alleged campaign finance conduct tied to the FTX collapse

Bond’s case is anchored in an August 2024 indictment. Prosecutors alleged that Bond and Salame “illegally funded” Salame’s political activity by using FTX resources to support a 2022 campaign for the U.S. House of Representatives.

The government’s allegations include that Salame used $400,000 of FTX funds as part of a “sham” payment intended to comply on paper while violating campaign finance laws in substance. Bond reportedly ran as a Republican in New York’s 1st congressional district, though she lost in the primary to Nicholas LaLota.

From an institutional perspective, the case illustrates a recurring enforcement theme: where crypto-related business failures intersect with political contributions, prosecutors may pursue campaign finance statutes in addition to financial fraud and related offenses. That creates additional compliance expectations for crypto firms and their leadership regarding the provenance of funds, controls around payments, and documentation that can withstand scrutiny across regulatory regimes.

How the plea deal with Salame shaped the remaining proceedings

Ryan Salame pleaded guilty and ultimately received a 7.5-year prison sentence, concluding his own criminal case. Authorities alleged that, as part of a conspiracy to make unlawful political contributions, Salame and others used money linked to FTX to support political activity. Salame later attempted to vacate his plea, arguing that prosecutors had misled him regarding whether Bond would face charges. Ultimately, he reported to prison in October 2024, leaving the dispute to continue within his wife’s case.

Bond’s trial therefore sits at the end of a broader U.S. prosecution landscape stemming from FTX’s collapse and its aftermath. The government’s pursuit of multiple individuals tied to FTX has included defendants who received prison time, as well as cooperation outcomes that reduced sentences for some witnesses.

In addition to Bond’s expected trial, the FTX criminal docket has largely reached resolution for several other participants. Sam “SBF” Bankman-Fried and Caroline Ellison—former Alameda Research CEO—were convicted or sentenced in separate proceedings. Two other former executives, Nishad Singh and Gary Wang, were given time served after testifying against Bankman-Fried at trial, reflecting the structure of cooperation-driven outcomes.

Parallel litigation: Bankman-Fried’s appeal and pardon bid

While Bond’s matter moves toward trial, Sam Bankman-Fried remains at a different procedural stage. Authorities convicted him on seven felony charges and sentenced him to 25 years in prison in 2024. Although Bankman-Fried sought to appeal his conviction and sentence, the Second Circuit recently rejected his appeal, leaving limited avenues for relief.

Separately, Bankman-Fried has pursued clemency routes, including applying for a presidential pardon from Donald Trump. However, as the appellate process has narrowed, the practical pathway to freedom is now tied either to further legal escalation to the U.S. Supreme Court or to executive action via pardon—an uncertainty that continues to shape the political and legal discourse around the case.

For institutional observers, this matters less because it affects crypto markets directly and more because it highlights how high-profile crypto fraud enforcement can diverge into distinct tracks: courtroom adjudication, sentencing appeals, and executive clemency. These overlapping tracks can influence how defense strategies and prosecutorial positions are evaluated in future cases with similar fact patterns involving financial wrongdoing and political or public-facing conduct.

Closing perspective

Bond’s Nov. 9 trial date sets a clear procedural next step, but unresolved questions around the indictment’s dismissal arguments—and how courts treat alleged assurances connected to plea deals—could still be consequential if litigated through motions and pretrial rulings. As the remaining FTX-related prosecutions narrow toward final outcomes, compliance professionals should watch how courts evaluate links between crypto-linked funding flows and regulated activity outside the financial sector, including campaign finance rules.

Crypto World

Ethereum Holds Near $1,600 as Whale Activity and Stablecoin Data Hint at a Potential Trend Reversal

TLDR:

- Ethereum is trading near $1,600, approximately 21% below its 30-day peak amid sustained market weakness.

- Two whale wallets withdrew $58.83M in ETH from Kraken and Bitgo, matching prior Bitmine purchase patterns.

- Binance stablecoin reserves and netflows have shifted to neutral, signaling a pause in aggressive capital flight.

- The bullish regime shift probability has climbed to 45%, but confirmation signals are still needed before acting.

Ethereum is trading around $1,600, roughly 21% below its 30-day peak, as on-chain data and whale activity draw renewed attention.

A quantitative regime model currently enforces a highly defensive stance, limiting market exposure to just 15%. Yet underlying metrics are shifting, with the probability of a bullish regime transition climbing to 45%.

Analysts and market observers are watching closely for confirmation signals before adjusting their positioning.

Defensive Model Meets Stabilizing Liquidity

Ethereum’s current price decline reflects a broader period of caution across crypto markets. The systematic regime model relies on multiple data layers, not price action alone.

It factors in Bitcoin’s structural cycles, derivative flows, and stablecoin dynamics on major exchanges like Binance.

Trend filters remain weak, with a moving average death cross showing a spread of -18.8%. That reading keeps the model in a highly defensive mode, reducing exposure significantly. However, momentum indicators tell a different story at the margin.

MACD histograms are contracting positively, suggesting that selling pressure may be running out of steam. This divergence between long-term trend weakness and short-term momentum stabilization is a key feature of the current setup.

Crucially, stablecoin data on Binance adds another layer of nuance. Stablecoin reserves registered a z-score of -0.32σ, while netflows came in at +0.20σ, both now in neutral territory.

This suggests the aggressive capital flight seen during deep corrections has paused, and exchange liquidity is no longer actively draining.

Whale Withdrawals Add a Bullish Variable

On-chain intelligence firm Arkham flagged notable activity from two fresh whale addresses this week. The wallets withdrew a combined $58.83 million worth of Ethereum from Kraken and Bitgo within hours.

Arkham noted that the purchase patterns matched prior observed activity linked to Bitmine, raising speculation about institutional accumulation.

Arkham posted on X: “Is Tom Lee stacking ETH this week?” referencing Bitmine chairman Tom Lee, known for public bullish stances on digital assets. The withdrawal pattern drew attention because it occurred against a backdrop of broader price weakness.

Ethereum recorded a 2.94% decline over the past 24 hours and a 7.43% drop over the past seven days, with 24-hour trading volume reaching $13.08 billion. Despite that, large-wallet behavior suggests some participants are positioning ahead of a potential reversal.

A decisive shift in Binance stablecoin netflows toward positive territory could serve as an early signal of returning risk appetite.

Until that confirmation arrives, the data supports patience rather than conviction in either direction. Ethereum’s next move may depend on whether these liquidity and behavioral signals continue to align.

Crypto World

Ethlabs Will Overlap with the Ethereum Foundation and Draw Its 'Densest Talent,' Funders Say

Ethlabs, a new Ethereum research lab backed by the network's two largest corporate holders, launched this week with a pitch to complement the Ethereum Foundation. Its own funders concede it will also compete as Ethlabs is “playing to win.” "I think they will be complementary," Joseph Chalom, chief… Read the full story at The Defiant

Kalshi has entered talks to raise fresh capital at a valuation of about $40 billion, an 82% jump from the $22 billion valuation it secured less than two months ago.

Summary

- Kalshi is reportedly seeking new funding at a $40 billion valuation, up 82% from May.

- The company processed over $17 billion in monthly trading volume and recently expanded crypto perpetuals.

- Legal disputes with CME Group and several U.S. states continue as Kalshi grows its product lineup.

According to a Financial Times report citing people familiar with the discussions, Kalshi is seeking a new funding round that could value the prediction market operator at roughly $40 billion, with the financing potentially closing as early as the third quarter.

The proposed valuation would represent another sharp increase for the company, which was valued at $22 billion during a $1 billion funding round completed in May. Earlier in 2025, Kalshi carried a valuation of about $5 billion, while its December valuation stood at $11 billion before doubling in the latest raise.

Investors in the previous financing included Coatue, Sequoia Capital, Andreessen Horowitz, and Morgan Stanley. If completed, the new round would push Kalshi’s valuation to eight times the level recorded at the beginning of the year.

Trading growth has supported investor interest

Financial Times reported that Kalshi’s rapid expansion has been driven by rising activity across prediction markets tied to sports, politics, financial markets, and entertainment.

Company figures show that Kalshi processed more than $17 billion in trading volume last month, up from less than $5 billion during the same period a year earlier. During its May fundraising announcement, the company said annualized trading volume had reached $178 billion, more than three times the level recorded six months before.

Sports-related contracts remain the platform’s largest category, accounting for about 65% of total volume, according to company data. Multi-outcome combination contracts introduced last year have also become one of Kalshi’s fastest-growing products.

Recent product launches have extended the company’s reach beyond event markets. Earlier on June 24, Kalshi expanded its Commodity Futures Trading Commission-regulated crypto perpetual futures lineup by adding contracts tied to Zcash, Near Protocol, and Shiba Inu. The additions increased the number of supported digital assets to 13, with the contracts operating without expiration dates under a structure approved by the CFTC.

Legal disputes continue across multiple fronts

While pursuing new funding, Kalshi remains involved in several legal and regulatory battles linked to its products.

A recent dispute emerged after the company launched cryptocurrency perpetual futures following approval from the CFTC. CME Group subsequently sued the regulator, arguing that the products should be classified as swaps and subjected to a different regulatory review process.

Elsewhere, state-level challenges continue to target Kalshi’s event contracts. Arizona filed criminal charges against the company in March, alleging that it operated without a gambling license and offered prohibited election-related contracts.

Separately, a Massachusetts judge ordered Kalshi to stop offering sports-related contracts in the state unless it obtains a local gaming license.

Kalshi has contested those actions and maintains that its event contracts fall under the exclusive jurisdiction of the federal derivatives regulator. As the company seeks another major funding round, the ongoing court cases are unfolding alongside its push into new markets and the rapid growth of its trading business.

Key takeaways:

- Cooling oil prices and a multi-month high for the US dollar are keeping intense pressure on non yield-bearing assets.

- Spot Bitcoin ETF outflows paired with Strategy’s slowest buying pace in 18 months signal short-term downside risks.

Bitcoin (BTC) traded down to $59,060 on Wednesday despite the sharp retreat in oil prices. Inflationary pressures eased following a memorandum of understanding between the US and Iran, which temporarily reopened the Strait of Hormuz. Bitcoin traders fear that the bounce back to $60,000 might not last long as the US dollar strengthened.

US dollar strength index (left) vs. Bitcoin/USD (right). Source: TradingView

The US dollar jumped to its highest level against a basket of foreign currencies in 13 months, indicating growing confidence in the US economy. Typically, this metric shows a negative correlation with Bitcoin’s price, as some investors view the cryptocurrency as a hedge against inflationary pressures traditionally driven by high oil prices.

Gold (left) vs. Brent Crude oil, USD. Source: TradingView

Gold prices fell below $4,000 for the first time in 7 months as Brent crude oil plummeted below $74, nearing levels seen prior to the conflict in Iran. Investors signaled lower demand for scarce assets despite moderate anxiety about tech-sector cash flows amid increased capital expenditure by AI hyperscalers.

Bitcoin investment thesis weakened by reduced inflation perspectives and AI sector growth

Inflation will take time to cool down to the US Federal Reserve (Fed) target of 2%, leading traders to anticipate interest rates remaining higher for longer, which ultimately favors fixed-income investments. The latest US Labor Department unemployment benefit claims data fell by 4,000 from the prior week, further confirming that the economy is not slowing.

US expanded Monetary Base (M2), USD. Source: Fed St Louis

Regardless of investors’ risk assessments of the profitability of AI infrastructure investments, US government debt has been driving up liquidity over the past 3 years. Data released on Tuesday revealed that the US expanded Monetary Base (M2) increased to $23.05 trillion in May, up from $22.8 trillion the prior month.

Related: Lyn Alden tips Bitcoin outperforming gold over next ‘two to three years’

While there is no short-term correlation between the amount of money in circulation and Bitcoin’s price, investors will eventually seek gains elsewhere if higher demand for fixed income causes diminished yields. For now, the tech sector remains investors’ largest bet, weakening the case for alternative scarce assets such as Bitcoin.

Micron (MU US), the computer memory and data storage manufacturer, reported strong quarterly earnings on Wednesday. Micron’s market capitalization has grown to $1.16 trillion, following a 265% gain over 6 months. More impressively, chipmakers SK Hynix and Samsung now account for 40% of the entire South Korean stock market, according to CNBC.

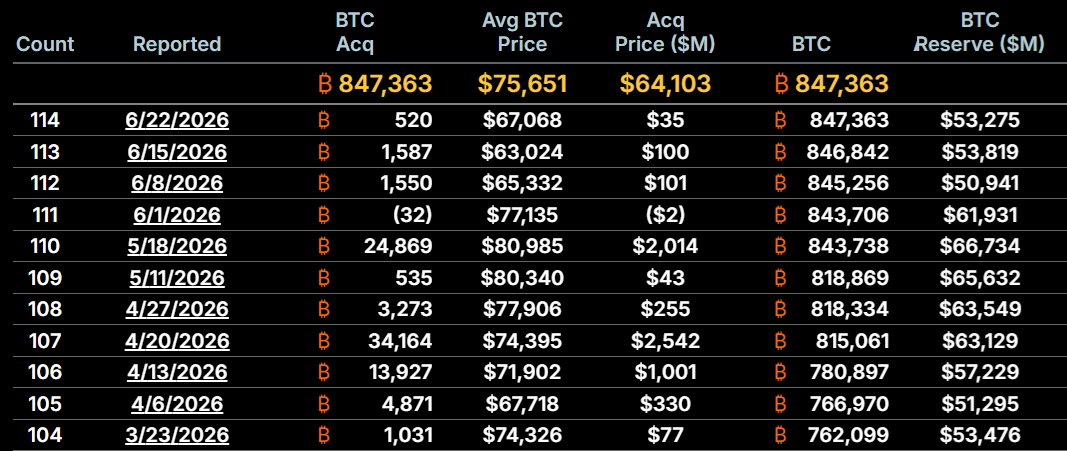

Strategy (MSTR US) Bitcoin reserve changes, BTC. Source: Strategy

The slowdown in Strategy’s Bitcoin acquisition pace has likely contributed to the weaker market sentiment. The company, led by Michael Saylor, reported adding 520 BTC during the week ending June 21, marking its lowest weekly intake in 18 months. Moreover, $300 million of the net proceeds from MSTR’s stock issuance during the period were used to replenish its cash position.

Bitcoin’s negative performance on Wednesday partly reflects macroeconomic conditions, with gold prices also affected. However, heavy net outflows from spot Bitcoin exchange-traded funds (ETFs) and disappointment that Strategy’s stock trades below its Bitcoin reserve acquisition cost have added significant pressure. Thus, further downside from the $59,000 level should not be ruled out.

Coatue Management founder Philippe Laffont says artificial intelligence (AI) and space now offer clearer bets than Bitcoin (BTC). He told CNBC he is increasingly unsure what to make of the asset.

The billionaire investor argued that picking a future $10 trillion company is easier than predicting Bitcoin’s path. He sees that debate as more solvable than Bitcoin’s long-run role.

Why the Coatue Founder Is Cooling on Bitcoin

Laffont built Coatue in 1999 after training under Julian Robertson at Tiger Management. That pedigree gives his cooling stance added weight.

Speaking on CNBC, he said scarce IPOs once funneled speculative money into Bitcoin. That is changing. Fresh listings and a fast-growing stablecoin payments boom now offer rival outlets for risk.

The timing stings. Bitcoin trades near $60,000, about half its record high near $126,000, while AI and space valuations climb.

“I don’t know what to think about Bitcoin anymore,” Philippe Laffont said in the interview.

Follow us on X to get the latest news as it happens

The Case for a $10 Trillion Company

Laffont’s math is simple. He said global market value could grow from about $120 trillion to $200 trillion. A single company at a 5% share would then be worth $10 trillion.

The candidates are forming. Nvidia (NVDA), the chip maker driving the AI boom, sits near $5 trillion. SpaceX priced the biggest IPO on record this month at $1.77 trillion, and its shares jumped 19% on debut.

Privately held Anthropic is valued at $965 billion, and OpenAI at $852 billion. Each is closing in on the roughly $1.2 trillion value of all Bitcoin.

This is not idle talk. Coatue and his brother Thomas led an earlier Anthropic round worth $380 billion and joined its latest raise. The fund also backs OpenAI.

The comments land as Wall Street continues to debate where capital flows next. Some buyers still argue that Bitcoin remains too small for institutions.

Not everyone shares his caution. BlackRock, the world’s largest asset manager, still recommends a small Bitcoin allocation for diversification.

Bitcoin’s ability to hold its value proposition while money chases AI and space is now the open question. For now, Laffont says he would rather bet elsewhere.

The post AI and Space Offer Better Bets Than Bitcoin, Billionaire Philippe Laffont Says appeared first on BeInCrypto.

Michelle Bond, the wife of former FTX Digital Markets co-CEO Ryan Salame, who is serving a 7.5-year prison sentence after reaching a plea agreement with prosecutors, is scheduled to stand trial in November following delays stemming from motions related to her husband’s plea deal.

On Wednesday, Judge George Daniels in the US District Court for the Southern District of New York ordered a trial start date of Nov. 9 for Bond, who faces four charges related to campaign finance law violations. The proceedings came a week after the judge denied Bond’s motion to dismiss the indictment, based on claims that prosecutors had promised Salame she would not be charged if she pleaded guilty.

Bond’s case is one of the final criminal proceedings related to the collapse of cryptocurrency exchange FTX, which filed for bankruptcy in 2022. The event led to criminal charges for Salame and other executives, including former CEO Sam “SBF” Bankman-Fried and former Alameda Research CEO Caroline Ellison.

In an August 2024 indictment, prosecutors alleged that Bond and Salame “illegally funded” the former’s 2022 campaign for the US House of Representatives. Salame allegedly used $400,000 of FTX funds as part of a “sham” payment in violation of campaign finance laws. Bond ran as a Republican in New York’s 1st congressional district but lost in the primary to Nicholas LaLota.

2022 campaign post on X (then Twitter) Source: Michelle Bond

Salame, charged in 2022 along with Bankman-Fried and others, was sentenced to 90 months in prison in 2024 after pleading guilty to conspiracy to make unlawful political contributions. He initially attempted to vacate his plea after claiming that prosecutors misled him over charging Bond, but ultimately reported to prison in October 2024 and left the matter to his wife’s case.

Bankman-Fried, angling for a presidential pardon, loses appeal

Salame, Bankman-Fried and Ellison were the only three people tied to FTX to receive prison time. Two other executives, Nishad Singh and Gary Wang, were given time served after testifying against SBF at trial. Ellison, meanwhile, was released early in January after serving less than her two-year sentence.

Related: US lawmakers warn against presidential pardon for Sam Bankman-Fried

Aside from Bond’s expected trial, Bankman-Fried was the only one connected to the crypto exchange to have his day in court. He was found guilty on seven felony charges and sentenced to 25 years in prison in 2024.

Although Bankman-Fried filed to appeal his conviction and sentence, he also recently applied for a presidential pardon from Donald Trump. The Second Circuit Court of Appeals rejected SBF’s appeal earlier this month, leaving the US Supreme Court or a presidential pardon as his only likely path to freedom over the next 20 years.

Magazine: AI is banking the unbanked in Africa… faster than crypto

TLDR:

- Binance’s Greek license bid collapsed, leaving the exchange one week to secure an alternative EU authorization.

- Regulators in Greece, Ireland, and Latvia all pushed back against Binance’s MiCA license application.

- Binance Head of Europe Gillian Lynch confirmed the firm is actively seeking a new EU licensing jurisdiction.

- Officials cited past money laundering penalties and Binance’s complex structure as key concerns during review.

Binance Europe operations remain intact for now, but the world’s largest crypto exchange faces a critical deadline after its bid to secure a regulatory license in Greece collapsed. Gillian Lynch, Binance’s Head of Europe and the UK, confirmed the company is not withdrawing from the region.

She said the exchange is actively exploring alternative authorization pathways. The development puts Binance in a tense position with European regulators as its current operating permission nears expiry.

Binance Faces Regulatory Resistance Across Multiple EU Countries

Binance approached regulators in Greece, Ireland, and Latvia in search of a MiCA-compliant license. According to sources familiar with the process, all three countries pushed back against the application.

Officials raised concerns about the exchange’s prior money laundering penalties and its complex international structure. Regulators also pointed to what they described as a risk-taking internal culture.

Lynch stated that Binance had contacted four or five regulators in total but submitted only one formal application, to Greece.

She told Reuters, “Binance is not leaving Europe,” and added, “We may just have a different pathway to being authorised.”

The company was previously under the impression that Greece would approve the license. However, the bid collapsed without a clear explanation from the Greek regulator.

The exchange has roughly one week to obtain a new license before its current EU operating permission expires. If no authorization is granted in time, Binance would be required to wind down its European operations.

That outcome would affect millions of users across the bloc. Lynch made clear the company intends to find another route to compliance before the deadline.

Binance is pushing back against the narrative that it is a non-compliant operator. Lynch noted the exchange employs approximately 1,500 compliance staff and has invested heavily in internal controls.

She said Binance has no outstanding issues related to the application. The company maintains it has fully addressed the concerns tied to its past regulatory penalties.

Binance Europe Strategy Shifts Toward Alternative Authorization Path

With Greece off the table, Binance is reassessing which EU member state could serve as its licensing jurisdiction. Lynch said, “If it is not Greece, I’m looking at other alternatives,” signaling the search is already underway.

No specific country has been named as the next target. The timeline, however, remains extremely tight given the approaching deadline.

The situation reflects the broader difficulty major crypto firms face in navigating MiCA’s compliance requirements. Binance’s international structure and past legal history have complicated its regulatory standing across Europe.

Other exchanges with cleaner compliance records have moved through the process with fewer obstacles. For Binance, the path forward requires rebuilding trust with skeptical national regulators.

A resolution before the deadline would require a regulator to move quickly on a new application. That is considered unlikely given the resistance Binance has encountered so far.

The exchange may face a temporary operational gap in Europe while it pursues authorization. Lynch has not ruled out any specific country as a potential licensing jurisdiction.

Binance’s continued presence in Europe matters to a large retail and institutional user base. The exchange offers crypto trading and related services to users across the EU.

Any forced wind-down, even temporary, would disrupt access for those customers. The company is clearly treating this as a solvable problem rather than a permanent setback.

Meta Pauses Employee-Tracking Program Following Internal Data Leak

Switzerland beats Canada 2-1 at World Cup, wins Group B

Micron: Q3 Proved Me Wrong (Rating Upgrade)

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports1 day ago

Sports1 day agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World19 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World16 hours ago

Crypto World16 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business22 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World5 days ago

Crypto World5 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World4 days ago

Crypto World4 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Business6 days ago

Business6 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

You must be logged in to post a comment Login