Crypto World

Ripple, JPMorgan settle a tokenized Treasury on XRPL

A redemption that used to take days cleared in about five seconds. The names in the room matter more than the speed, and the question for XRP holders is where the token actually sits in the flow.

Summary

- JPMorgan, Mastercard, Ondo, and Ripple tested tokenized Treasury redemption on the XRP Ledger.

- The settlement speed matters, but the institutional names matter more.

- XRP was not the asset being redeemed, but it can sit in fees, reserves, and routing.

- The long-term signal is utility; the near-term question is whether volume follows.

On June 12, JPMorgan, Mastercard, Ondo Finance, and Ripple completed a test that moved a tokenized United States Treasury through a full redemption on the XRP Ledger. The settlement finished in roughly five seconds.

The same operation on traditional rails takes three to five business days. crypto.news shared the result the day it happened, and within hours the XRP community had folded it into the familiar story: another institution, another marquee logo, another reason the token should be worth more than it is.

The speed is real and the participants are real. What deserves a closer look is the part the headlines skip, which is the exact role XRP the asset plays when a tokenized Treasury changes hands on its ledger.

That answer is more interesting than a simple win or loss. It sets the boundary on how much a holder should read into the news.

What actually happened on June 12

Strip the announcement down to its parts and the test looks like this. Ondo Finance issued a tokenized version of a short-dated United States Treasury instrument, the kind of product that wraps a real government bond into an on-chain token that pays the yield of the underlying paper.

Mastercard provided the link between the regulated money layer and the chain through its Multi-Token Network, the rails it has been building to let banks move tokenized deposits and settle against tokenized assets. JPMorgan brought its institutional settlement infrastructure to the bank side of the trade.

Ripple supplied the ledger and the surrounding tooling that let the redemption clear on the XRP Ledger instead of on a private bank network.

A redemption is the moment a holder hands the token back and receives cash value in return. In the legacy world, that round trip crawls through custodians, transfer agents, and settlement windows that only open on business days.

The test compressed that into a single near-instant on-chain event, with the cash leg and the asset leg settling together instead of days apart. Atomic settlement, where both sides of a trade move or neither does, removes the gap during which one party holds an asset and waits to be paid.

That gap is where counterparty risk lives, and closing it is the entire point of putting this kind of asset on a fast public ledger. So the result is a working proof that a tokenized Treasury can be issued, held, and redeemed across a chain that major financial firms were willing to touch.

That is not nothing. It is also not the same thing as production volume, and the difference is where careful readers should slow down.

The logos are the story, up to a point

Each name on the June 12 test carries weight, and the weight is worth spelling out because the market tends to treat any JPMorgan headline as a verdict.

JPMorgan has spent years building Kinexys, formerly Onyx, its blockchain settlement arm that already moves large daily volumes in tokenized deposits. When a bank of that size agrees to run a redemption across the XRP Ledger, even as a test, it signals that the ledger met its internal bar for security and controls.

Mastercard has been pushing its Multi-Token Network as the connective tissue between banks and tokenized assets, and its presence shows the test was built to plug into existing card-network plumbing instead of standing alone as a crypto experiment. Ondo is one of the larger issuers of tokenized Treasuries, and its OUSG product has become a reference point for the whole real-world-asset category.

Ripple sat at the center as the ledger host and the firm whose institutional features made the settlement possible. Put together, the group reads as a deliberate signal that tokenized Treasuries can settle on the XRP Ledger with names that compliance departments recognize.

The temptation is to draw a straight line from that signal to the XRP price. Before drawing it, look at what moved through the transaction and what did not.

Why tokenized Treasuries are the wedge asset

It is no accident that the test used a Treasury and not some exotic instrument. Among all the assets the industry has tried to move on-chain, short-dated government debt has become the wedge that opens the institutional door, and the reasons say a lot about why June 12 happened at all.

A Treasury bill is the simplest large asset to tokenize honestly. It has a known issuer, a known maturity, a yield that is easy to verify, and a price that barely moves day to day.

There is little argument about what it is worth, which means a token wrapped around it can be marked with confidence and redeemed without disputes. Compare that to tokenized real estate or private credit, where valuation is slow, subjective, and easy to challenge, and the appeal of starting with Treasuries becomes obvious.

The asset removes the hardest problem in tokenization, which is agreeing on value, so the experiment can focus on the plumbing. That is why tokenization as the real story keeps coming back to Treasuries: they are liquid, familiar, yield-bearing, and easy for institutions to understand.

The demand is also concrete. Crypto firms, trading desks, and treasuries sit on large idle dollar balances, often parked in stablecoins that pay them nothing.

A tokenized Treasury lets that cash earn the yield of real government paper while staying on-chain, available to move at any hour without leaving for the banking system. That single feature, on-chain dollars that earn a real yield, has turned tokenized Treasuries into one of the fastest-growing corners of the whole digital-asset market.

Ondo’s OUSG and a handful of competitors have pulled in billions because they answer a question every on-chain treasurer has, which is how to stop leaving money on the table.

So when Ripple wanted to prove the XRP Ledger could host serious institutional settlement, the Treasury was the natural choice. It is the asset most likely to move in real size, the one institutions most want on-chain, and the one with the fewest excuses for the test to fail.

Winning the Treasury-settlement business is the beachhead. Everything heavier, corporate bonds, funds, structured credit, follows the rail that first proves itself on the simple asset.

Where XRP actually sits in the transaction

Here is the part that gets lost. In the June 12 flow, the asset being moved was a tokenized Treasury. The cash leg most likely settled in a stablecoin or a tokenized deposit.

XRP, the native token of the ledger, was not the thing being bought, sold, or redeemed.

That sounds like bad news for the holder thesis, and read too quickly it would be. The reality is more layered.

XRP touches a settlement like this in three indirect ways, and each one is small per transaction but structural across millions of them.

First, every transaction on the XRP Ledger burns a tiny amount of XRP as a fee. The amounts are fractions of a cent, designed to stop spam, not to enrich anyone.

As transaction count rises, the burn rises with it, which slowly removes XRP from supply. Second, accounts and certain ledger objects require a reserve denominated in XRP, so a ledger that hosts more institutional activity locks up more XRP in reserves.

Third, and most important over time, XRP can serve as the auto-bridge asset when one currency or token needs to move into another inside the ledger’s exchange. In a redemption that converts a tokenized Treasury back into a chosen settlement currency, XRP can sit in the middle as the routing asset that connects the two sides.

None of those roles require XRP to be the headline asset in the trade. All three grow with usage, not with hype.

That is the honest frame: the June 12 test does not put XRP at the center of the transaction, but it does feed the machinery where XRP earns its keep. Whether that machinery turns fast enough to matter for price is a separate question, and the search history of XRP suggests patience is warranted.

This is also what the tokenized Treasury settlement means for XRP: the ledger can win serious institutional use before the token captures meaningful demand. The two are connected, but not identical.

The ledger features that made it possible

A redemption like this could not have run on the XRP Ledger of a few years ago. The capability is new, and it comes from a stack of institutional features Ripple and the wider XRPL developer community shipped across 2025 and into 2026.

Multi-Purpose Tokens, the MPT standard, let a token carry the metadata that a real financial instrument needs, things like maturity dates, transfer restrictions, and tranche information, without forcing developers to bolt on fragile smart contracts. Permissioned Domains and a permissioned version of the ledger’s decentralized exchange let regulated participants trade in gated environments where access depends on credentials such as know-your-customer checks.

RLUSD, Ripple’s dollar stablecoin, now settles on the ledger and gives institutions a compliant cash leg that lives on the same rail as the asset. The escrow feature was extended to support third-party tokens like RLUSD, which matters for structured settlement.

Layer the XLS-66 lending protocol on top, with its single-asset vaults that isolate credit risk one asset at a time, and the ledger starts to look less like a payments network and more like a settlement venue with a credit layer attached. The June 12 test is the visible output of that quieter build.

The features were the precondition. The redemption was the demonstration that they hold together under the eyes of firms that do not lend their names casually.

The competition for the same settlement business

The XRP Ledger is not the only chain courting this work, and the contest for institutional settlement is the backdrop that gives June 12 its real stakes.

Ethereum sits at the center of the tokenized-asset world today. Most tokenized Treasuries, including the largest funds from the biggest asset managers, launched on Ethereum or its layer-2 networks, where the deepest pool of developers and the most established custody and compliance tooling already live.

An institution choosing where to settle starts from a world in which Ethereum is the default, and the burden falls on every other chain to give a reason to look elsewhere. Solana has pushed hard on speed and cost and has won its own share of tokenization projects and corporate interest.

On top of the public chains, the banks are building private ones. JPMorgan’s own settlement network already moves enormous daily volumes inside a permissioned environment the bank controls end to end.

Against that field, the XRP Ledger’s pitch is specific. It offers settlement built for payments from the start, with the institutional features, the MPT standard, permissioned trading, credentials, baked into the base layer instead of bolted on through smart contracts that have to be audited one project at a time.

The argument is that a purpose-built settlement ledger carries less risk surface than a general-purpose smart-contract chain, because there is less custom code between an institution and a completed trade. June 12 is Ripple making that argument in public with partners who could have run the same test anywhere.

This is why the names matter more than the speed. Five-second settlement is achievable on several chains.

What the XRP Ledger needed to prove was that firms like JPMorgan and Mastercard would choose it for a real institutional flow when they had every other option available. The test does not win the war.

It wins the right to be in the room for the next one, which for a chain competing against Ethereum’s incumbency is the harder thing to secure.

Following one tokenized Treasury through the flow

Abstractions blur the stakes, so trace a single unit through the kind of cycle the test modeled.

Start with a short-dated United States Treasury bill sitting in a custodian’s account. Ondo, or an issuer like it, holds that bill and mints an on-chain token against it.

The token represents a claim on the bill and the yield it throws off. Call it one unit of a tokenized Treasury, and place it in the wallet of an institutional holder who wants short-term dollar yield without leaving the chain.

For weeks, the holder simply holds. The token accrues the bill’s yield.

When the holder decides to exit, the redemption begins. The holder submits the token back toward the issuer through the settlement arrangement that JPMorgan and Mastercard stand behind.

On the ledger, the asset leg and the cash leg are matched so they settle as one event. The token is retired.

A settlement currency, most likely RLUSD or a tokenized deposit, lands in the holder’s wallet in return. The fee for the ledger transactions is paid in XRP and burned.

If the chosen settlement currency differs from the currency the token was priced in, the ledger’s exchange can route through XRP as the bridge to complete the swap. Total elapsed time: around five seconds.

Compare that to the legacy path, where the same redemption would route through a transfer agent, wait for a settlement window, and clear across three to five business days while both sides carry risk. The end state is identical.

The holder is out of the Treasury and into cash. The path is what changed, and the path is the product.

Notice where XRP appeared in that walk. It paid the fee. It may have bridged the currencies. It backed the account reserves.

It was never the asset the holder set out to trade. That is the shape of XRP’s role in institutional settlement, and it explains why utility can climb for years while the token price moves sideways.

What institutions actually buy beyond the five seconds

The speed grabs the headline, but settlement time is not the only thing an institution gains, and the other gains explain why firms keep running these tests even when the token economics do not concern them.

The first gain is capital efficiency. In the legacy model, the days between trade and settlement are days during which capital sits frozen, posted as margin or held in reserve against the risk that the other side fails to deliver.

Collapse settlement to seconds and that frozen capital comes free, available to be deployed elsewhere. For a large trading desk, the value of unlocking capital that used to sit idle for three days at a time runs into real money across a year of activity.

The second gain is around-the-clock operation. Traditional settlement runs on banking hours and business days, so a Friday trade waits through the weekend.

An on-chain ledger settles at any hour, which matters more every year as markets globalize and the line between trading days blurs. The third gain is collateral mobility.

A tokenized Treasury that settles instantly can be moved, pledged, or redeemed the moment it is needed, which lets the same asset work harder as collateral across more uses.

These are the reasons a JPMorgan or a Mastercard cares about the test, and none of them depend on XRP the token doing anything. The institution is buying a better settlement process.

XRP earns its small dues in the background. Keeping those two things separate is the key to reading any announcement like this one without mistaking institutional interest in the ledger for institutional demand for the token.

The first is clearly growing. The second has to be inferred from on-chain flow, and the inference is where most of the disappointment in XRP’s price history has come from.

That is why Ripple’s IPO and XRP holders is part of the same broader lesson. Ripple’s success, XRPL adoption, and XRP holder value are related, but they do not automatically collapse into the same thing.

Does settlement volume reach the price?

This is the question every holder actually wants answered, and it deserves a straight treatment, not a number pulled from the air.

The bullish case runs through the indirect roles. If tokenized Treasuries and similar real-world assets move onto the XRP Ledger in size, transaction counts climb, fee burn climbs, reserves lock up more supply, and bridge routing pulls XRP into more flows.

Demand for the token then rises from use instead of from speculation, and demand that comes from use tends to be stickier. Ripple has framed exactly this flywheel in its institutional materials, and the logic holds on its own terms.

The sober case sits in the math. Fee burn on the XRP Ledger is deliberately tiny.

Even a large jump in institutional transactions removes a small fraction of supply against the tens of billions of XRP already in circulation and the monthly escrow releases that add to it. Bridge routing only pulls in XRP when a trade actually needs a currency conversion that the ledger chooses to route through XRP, and many institutional flows will settle stablecoin to stablecoin without ever touching the token.

Reserves lock supply but do not create buy pressure on their own. There is a supply side to weigh as well, and it cuts against the burn story in the near term.

Ripple releases up to one billion XRP from escrow at the start of each month, then re-locks most of it, but the net new supply that reaches the market still runs into the hundreds of millions of tokens monthly. For fee burn from institutional settlement to tighten supply in any meaningful way, the volume would have to grow large enough to offset that steady release, which is a high bar at current transaction levels.

A holder who pins hopes on burn alone is betting that on-chain activity climbs by orders of magnitude while the escrow schedule keeps running on its long-set path. That can happen over years. It does not happen because of one test.

The careful reading is that the June 12 test strengthens the long-term utility argument and does little for the short-term price argument. XRP spent most of 2026 trading near or below the one-dollar-and-change range while news exactly like this piled up, which is the market telling you that proofs of concept are priced as proofs of concept until volume follows.

A settlement test is a door opening. Walking through it at scale is a different event, and the token tends to wait for the second one.

What has to be true for this to matter

For the June 12 result to move from interesting to important, a few things need to happen, and naming them gives a holder a watchlist instead of a hope.

Production volume has to follow the test. One redemption proves the plumbing.

Recurring institutional flow, measured in real daily value rather than pilot transactions, is what feeds the burn-and-bridge machinery. Regulatory clarity has to land, because the CLARITY Act and the broader United States market-structure framework decide how freely regulated institutions can settle tokenized assets on public ledgers.

Until the rules set, much of this activity stays in the test-and-pilot stage where the June 12 work lives. That is why CLARITY’s XRP classification question matters: the technology can be ready before the legal framework gives the rest of Wall Street permission to use it.

Competing venues have to be held off, since Ethereum, Solana, and a wave of bank-built private chains are chasing the same tokenized-asset settlement business, and the XRP Ledger has to keep winning the names that make compliance teams comfortable.

If those line up, the indirect demand argument gets a real chance to show up in on-chain data, and from there in price. If they stall, June 12 joins the long list of XRP headlines that read well and changed little.

The token has taught its holders that lesson more than once. That is also why institutional positioning in XRP matters as a separate signal: ETFs show who wants exposure, while settlement flows show whether utility is becoming demand.

Reading the signal without inflating it

The clean takeaway is that Ripple, with JPMorgan, Mastercard, and Ondo alongside it, proved that a tokenized Treasury can be issued and redeemed on the XRP Ledger in seconds, with names that the institutional world takes seriously.

That is a meaningful step for the ledger as a settlement venue. For XRP the asset, it is a vote for the long-term utility thesis and a weak input to the near-term price, because the token sits in the fees, the reserves, and the bridge rather than at the center of the trade.

A holder who understands that distinction will not oversell the day and will not dismiss it either. The machinery that pays XRP its small, repeated dues got a high-profile workout.

Now the only thing that turns that into price is the boring part, which is volume that shows up and keeps showing up. Watch the on-chain flow, watch the rules, and let the token follow the usage instead of the logos.

This article is information, not investment advice. Figures and partnership details reflect reporting available as of June 23, 2026, and corporate plans, test results, and market conditions can change.

Bitcoin can’t catch a break these days as the rejection from $67,200 at the beginning of the previous week continues to haunt it and push it south.

In alignment with Strategy’s stock price, the primary cryptocurrency has plummeted below the crucial support at $60,000.

It was just over a week ago that the overall sentiment in the crypto industry was much more positive, as U.S. President Donald Trump promised a deal with Iran that was supposed to be signed by June 19.

The actual confirmation didn’t arrive; instead, the two sides clashed again, and the POTUS made new threats over the weekend of further attacks.

Meanwhile, investor exodus from the spot Bitcoin ETFs continued as net outflows continue to dominate daily.

Fear Around MicroStrategy Mounts as Stock Price Plunges

Perhaps the most crucial part of the current market environment is Michael Saylor’s Strategy as the firm’s STRC shares still trade below their peg of $100.

FUD around the largest corporate BTC accumulator continues. Some analysts believe the company would have to sell at least 50,000 BTC in the next few years, while others urged Strategy to halt its bitcoin purchases for now.

The company has indeed begun announcing smaller BTC purchases while it focuses on rebuilding its USD reserves.

However, its main stock price has also taken a major beating, plunging by 10% daily to $93 as of press time. This marks a 2-year low.

With most alts following BTC on the way south, the total value of liquidated positions across derivatives markets is around $650 million, according to data from Coinglass.

The post Bitcoin Price Crashes Below $60K as Strategy’s MSTR Plunges 10% appeared first on CryptoPotato.

Crypto-aligned political action committees (PACs) helped fund several candidates across US House and Senate primaries held on Tuesday, with multiple backers securing nominations and positioning themselves for November general-election contests. The results highlight the growing role of digital-asset industry-aligned outside spending in US electoral processes, particularly in races where candidates’ views on crypto policy and regulation are expected to matter.

According to The New York Times, a combined total exceeding $8 million in media support—attributed by reporting to PACs including Fairshake and its affiliates—was directed toward candidates considered more likely to support digital-asset-friendly approaches in the next Congress. For compliance and institutional stakeholders, the practical implication is straightforward: political outcomes can shape the regulatory runway for stablecoin policy, exchange oversight, AML/KYC implementation, and enforcement priorities.

Key takeaways

- Fairshake and affiliated PACs reported more than $8 million in combined media expenditures supporting candidates in primaries across Utah, Maryland, and New York.

- In New York, Democrat Ritchie Torres won a primary for the 15th congressional district with 71.9% of the vote.

- In Utah, Republican Blake Moore won the 2nd district primary with 57.5% of the vote.

- Protect Progress, a Fairshake affiliate, reported $5.5 million in expenditures backing Adrian Boafo, who won Maryland’s 5th district Democratic primary with about 32%.

- Not all pro-crypto-aligned candidates won, underscoring that outside spending does not guarantee nomination outcomes.

Fairshake-backed wins and reported spending

Tuesday’s primary results included wins by candidates associated with positions that crypto-aligned donors reportedly view as favorable. Reporting indicates that the largest activity came from Fairshake and its affiliates, which have been linked by industry reporting to funding from major digital-asset firms such as Coinbase and Ripple Labs.

In New York, Democrat Ritchie Torres secured the nomination for the state’s 15th congressional district, capturing 71.9% of the vote. In Utah, Republican Blake Moore won the nomination for the 2nd district with 57.5% of the vote.

Maryland’s 5th district drew particular attention from Protect Progress, described as a Fairshake affiliate. Protect Progress reported $5.5 million in spending to support Adrian Boafo. Boafo won the Democratic primary with about 32% of the vote, defeating other candidates who opposed “spending from crypto billionaires,” according to the reporting.

Fairshake spokesperson Geoff Vetter said the PAC “went big and went early,” adding that its spending was intended to move Boafo from fifth place to the nomination. For institutions tracking policy risk, the immediate takeaway is less about campaign tactics and more about the fact that these PACs are deploying substantial resources into races that could influence legislative direction—especially in areas where Congress plays a central role alongside federal regulators.

Where crypto-aligned PACs fit in the US policy process

Crypto-aligned PACs have become a notable feature of the US political landscape as digital-asset regulation has intensified. Their spending is typically framed around advancing candidates perceived as more receptive to proposals affecting markets and compliance infrastructure, including the implementation of AML/KYC regimes, the future shape of broker-dealer and custody oversight, and the treatment of stablecoins across the banking and payments ecosystem.

Fairshake previously reported having “$150 million cash on hand” in June after spending in several US state primaries, as reported by Cointelegraph. The organization’s broader strategy—supporting candidates it characterizes as “pro-crypto”—suggests a long-running approach rather than isolated election-cycle expenditures.

Other crypto-aligned PACs reported spending on 2026 candidates as well. Reporting cited Fellowship, backed by Cantor Fitzgerald and Anchorage Digital, and the Blockchain Leadership Fund, described as a hybrid PAC backed by Anchorage and Chainlink Labs. These structures matter for compliance monitoring: different PAC types and backers can affect transparency timing, donor disclosure requirements, and how political spending intersects with lobbying and regulatory advocacy.

Unresolved questions: enforcement risk and electoral uncertainty

Tuesday’s outcomes also underscored that outside spending does not automatically determine results. In New York’s 12th district, Democrat Alex Bores lost the primary to Micah Lasher.

According to reporting, Bores faced criticism from Lasher during a June debate regarding whether Bores benefited from external support, including claimed funding by Ripple Labs co-founder Chris Larsen. While such allegations are common in political contests, they also reflect a recurring concern for institutions: the visibility of crypto-related political funding can heighten reputational and regulatory sensitivities, even when legal compliance requirements are met.

From a regulatory perspective, several practical uncertainties remain. Outside spending can influence legislative priorities, but it does not alter independent federal enforcement decisions. For regulated entities—exchanges, custodians, fintechs, and banks considering crypto integration—election outcomes may shift the direction of proposed bills, but implementation still depends on agency rulemaking, judicial interpretation, and enforcement posture. Cross-border firms face additional complexity, as US policy developments can interact with non-US frameworks such as the EU’s MiCA regime and other jurisdictional approaches to stablecoins, licensing, and market conduct.

What to watch next: Colorado and Arizona primaries

Attention is likely to move to upcoming primaries in Colorado and Arizona. Colorado is scheduled to hold its primary on June 30, while Arizona’s primary is set for July 21. As of Wednesday, reporting indicated Fairshake affiliates had not disclosed significant spending in those races.

Institutional observers may view this disclosure gap as informational rather than decisive. In earlier cycles, crypto-aligned PACs have invested heavily ahead of key contests. In 2024, Fairshake and its affiliates spent more than $10 million supporting Ruben Gallego’s Senate race in Arizona and $2.1 million for Democratic Representative Yadira Caraveo in Colorado’s 8th district. Gallego won, while Caraveo lost in the November 2024 election to Republican Gabe Evans.

For compliance and policy teams, the next phase to monitor is whether reported spending increases as the Colorado and Arizona primaries near, and whether candidates endorsed by these PACs introduce or align with legislative agendas relevant to digital-asset regulation, AML/KYC implementation, and stablecoin oversight. Electoral momentum may also affect how industry stakeholders plan lobbying and regulatory engagement during periods when Congress is poised to act.

Closing perspective: The Tuesday primaries reinforce that crypto-aligned outside groups can materially shape candidate slates in races with direct relevance to digital-asset policy. The key question for the next reporting cycle is whether similar levels of disclosed spending emerge in Colorado and Arizona, and how the resulting nominations may influence legislative negotiations and regulatory priorities ahead of the November election.

Stablecore, a digital asset infrastructure provider for financial institutions, has launched an early-access program for US credit unions, a move aimed at helping smaller lenders evaluate stablecoins and other blockchain-based financial services before broader adoption.

The program announced on Wednesday is in collaboration with Circuit, a credit union service organization (CUSO) focused on research and development, and Curql, a fintech investment collective representing more than 160 credit unions.

The initiative allows participating credit unions to test stablecoin and digital asset services, including stablecoin payments, tokenized deposits, Bitcoin (BTC), crypto on- and off-ramps and staking capabilities, before deciding whether to integrate them into their existing banking platforms.

The program builds on Stablecore’s broader effort to bring stablecoin and tokenized-asset services to US banks and credit unions through their existing core banking systems. In February, the company joined the Jack Henry Fintech Integration Network, operated by the eponymous core banking technology provider, giving Stablecore access to approximately 1,670 bank and credit union core clients.

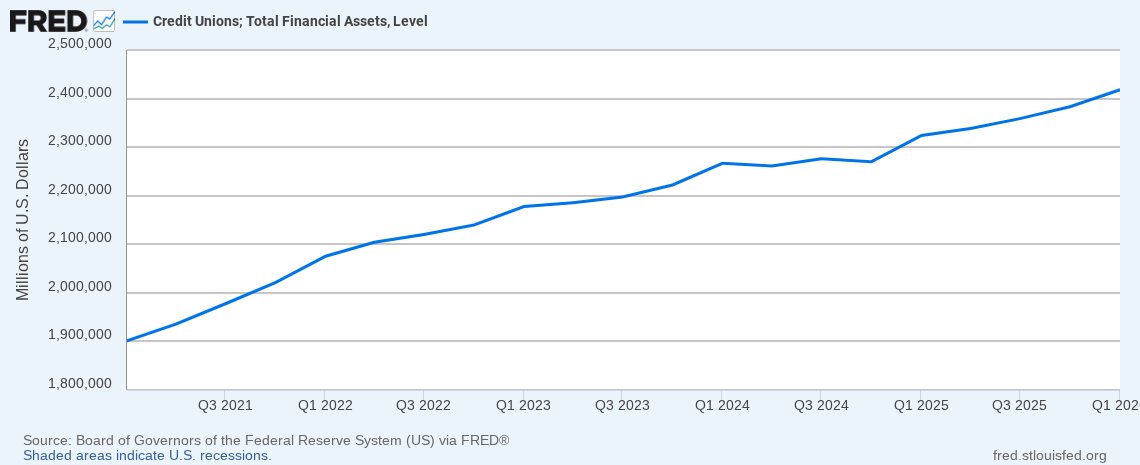

With the latest program, credit unions managing roughly $25 billion in combined assets will be able to explore stablecoin and digital asset services.

Credit unions remain a key pillar of the US financial system, with more than 4,200 federally insured institutions nationwide. Although their numbers have declined over the years, membership and total assets have continued to grow.

Total financial assets of US credit unions, as of Q1 2026. Source: FRED

Related: Chainlink joins European and Korean bank consortia to develop FX settlement network

Credit unions move to implement GENIUS Act stablecoin rules

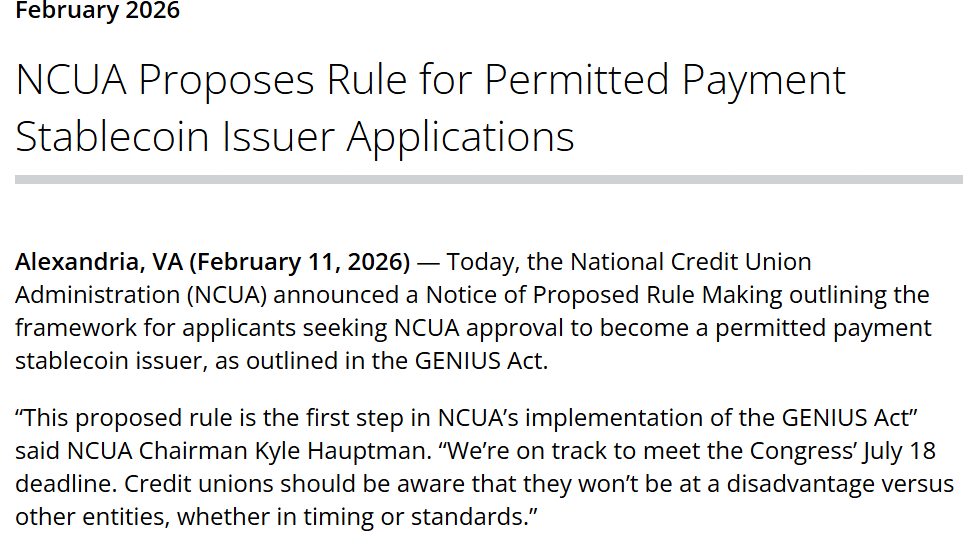

There are growing signs that US credit unions are increasingly preparing to adopt stablecoin services. In February, the National Credit Union Administration (NCUA), the federal regulator for federally insured credit unions, proposed a licensing framework for payment stablecoin issuers operating through credit union subsidiaries.

Under the proposal, any payment stablecoin issuer operating through a subsidiary of a federally insured credit union would be required to obtain an NCUA license before issuing stablecoins.

The proposal focuses on the licensing process and oversight framework, with additional rulemaking on reserve requirements, capital, liquidity and risk management expected at a later date. The proposed rules were open for public comment through April 13.

NCUA proposes licensing framework for stablecoin issuers operating through credit union subsidiaries. Source: NCUA

Related: CBOE weighs converting BTC, ETH continuous futures into perpetual futures: Report

Prediction markets company Kalshi has filed a lawsuit against state officials in Illinois over legislation it says “expressly bans sports event contracts” on its platform.

In a Tuesday filing in the US District Court for the Northern District of Illinois, Kalshi alleged that Illinois Governor JB Pritzker, Attorney General Kwame Raoul, and other officials on the state’s gaming board “usurped” the authority of the US Commodity Futures Trading Commission (CFTC) over prediction markets.

Specifically, the company alleged that legislation signed into law last week in Illinois, requiring prediction market platforms to be licensed in the state to offer sports event contracts, violated federal law. Kalshi claimed that it would be “irreparably harmed” when the law, Illinois Senate Bill 3019, takes effect on July 1.

“If Kalshi complies with the new state law by ceasing to offer its sports event contracts in Illinois, that would put Kalshi in violation of the CFTC’s uniformity requirements, harm Kalshi’s commercial interests, and require the company to implement complex and expensive technological solutions to limit access in Illinois — incurring costs that would not be recoverable when Kalshi ultimately prevails in the action,” said the complaint.

Source: PACER

The Illinois law, passed as part of a state budget package for the fiscal year 2027, included a 0.2% tax on crypto transactions and has already been heavily criticized by many in the industry.

The legislation amended the state’s definition of an “exchange wager” to include “an agreement, contract, transaction, or swap that is offered, traded, or executed on a prediction market or exchange tied to a sporting contest or sporting event,” making prediction market companies subject to the same rules as entities offering sports betting.

Related: Mark Zuckerberg ordered Meta staff to develop moneyless prediction market: NYT

“[…] Kalshi faces similar irreparable harms if it attempts to comply with SB 3019 by offering sports events contracts in compliance with Illinois’s costly and restrictive licensing and regulatory regime,” said the company. “Nor can Kalshi avoid these harms by simply disregarding the unlawful state requirements because an enforcement action by Illinois could subject Kalshi to criminal penalties.”

Legal fights eventually headed to the Supreme Court?

Kalshi’s lawsuit was the latest in a jurisdictional fight between federal and state authorities over sports betting on prediction markets.

The CFTC, headed by Commissioner Michael Selig, has claimed exclusive authority over the companies under the Commodity Exchange Act, arguing that the platform’s event contracts are “swaps” within its jurisdiction. The agency has filed several lawsuits against state authorities over this claim, most recently in response to Kentucky’s restrictions on prediction markets.

Some experts expect that the legal battles will end up at the US Supreme Court, given the opposing claims by federal regulators and state gaming officials.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Crypto-aligned political action committees (PACs) helped back multiple candidates in US congressional primaries on Tuesday, with several of those supported—spending more than $8 million in total on media in the races described—emerging as winners. The results set up new matchups for the November election and highlight how digital-asset interests are increasingly intersecting with mainstream electoral politics.

Fairshake and its affiliates were among the most active, according to disclosures referenced in the reporting. The PAC network, largely backed by major crypto companies including Coinbase and Ripple Labs, reported combined media spending of about $8 million to support candidates considered favorable to digital asset policy priorities in the next congressional session.

Key takeaways

- In New York, Democrat Ritchie Torres won the 15th district primary with 71.9% of the vote.

- In Utah, Republican Blake Moore won the 2nd district primary with 57.5% of the vote.

- Fairshake affiliate Protect Progress backed Maryland’s 5th district candidate Adrian Boafo, who won the Democratic primary with 32%.

- Not all “pro-crypto” backed candidates won, including Alex Bores in New York’s 12th district.

- Next statewide primary focus is expected to shift toward Colorado and Arizona, though no major additional spending by affiliates had been disclosed as of Wednesday.

Crypto-linked PAC spending shows up in primary results

Tuesday’s primaries for select US House and Senate races in Utah, Maryland, and New York produced wins for candidates aligned with crypto industry policy interests. One of the central players in the effort was Fairshake, a PAC and network of affiliates that has positioned itself as a key political vehicle for digital asset priorities.

According to the figures cited, the crypto-aligned PACs spent about $8 million on media across the relevant races. In New York, Ritchie Torres—supported by the described crypto-aligned efforts—secured victory in the state’s 15th congressional district primary, taking 71.9% of the vote. In Utah, Blake Moore won the Republican primary for the 2nd district with 57.5%.

Maryland offered a more closely contested outcome among the cited races. Protect Progress, a Fairshake affiliate, reported $5.5 million in expenditures supporting Adrian Boafo, who won the Democratic primary for Maryland’s 5th district with 32% against other candidates described as opposed to “spending from crypto billionaires.”

Fairshake spokesperson Geoff Vetter said the group “went big and we went early,” adding that the campaign aimed to move Boafo “from fifth place to the halls of Congress.”

Reporting also notes that Fairshake previously described having “$150 million cash on hand” in June, after earlier spending connected to state primary efforts. That prior activity included a separate round of spending referenced in earlier coverage by Cointelegraph, underscoring the PAC’s pattern of deploying resources well before election deadlines.

Where the money could matter most

The primary results matter for more than just individual contests. They reflect a strategy: using targeted advertising to shape which candidates advance to November in districts where crypto policy could become a campaign issue. PACs such as Fairshake have framed their efforts around sending lawmakers viewed as “pro-crypto,” aiming to influence legislative direction in the next Congress.

In addition to Fairshake and Protect Progress, other crypto-aligned PACs referenced as having reported support for 2026 candidates included Fellowship—backed by Cantor Fitzgerald and Anchorage Digital—and the Blockchain Leadership Fund, described as a hybrid PAC backed by Anchorage and Chainlink Labs. Together, these groups illustrate that crypto political spending is not concentrated in a single committee.

The June cash figure cited for Fairshake suggests the network has continued financial capacity to remain active beyond a single election cycle, and Tuesday’s wins may encourage further investment in competitive contests.

Some backed candidates still fell short

While several candidates aligned with crypto industry interests won Tuesday’s primaries, the picture was not uniform. Alex Bores, a Democrat running in New York’s 12th district, lost the primary to Micah Lasher.

According to the reporting, Bores faced criticism from Lasher during a June debate. Lasher alleged that Bores may have benefited from Ripple Labs co-founder Chris Larsen spending $3.5 million to support his campaign. That exchange illustrates a political tension often found in high-spending races: even when PAC-aligned candidates are competitive, opponents may attempt to shift the narrative toward donor influence and away from policy substance.

For voters, these dynamics can become a decisive factor in how campaigns are framed—especially when digital asset-related money is already in the spotlight.

Looking ahead to Colorado and Arizona primaries

Attention is expected to move to upcoming primaries in Colorado and Arizona. The reporting indicates that Colorado is scheduled for June 30 and Arizona for July 21. Fairshake affiliates had not disclosed significant spending in any races as of Wednesday, according to the account.

That timing is important. It suggests that crypto-aligned PACs may be pacing their media spending to target later or more competitive windows—or waiting for clearer signals about which candidates need reinforcement. Still, the absence of disclosed spending so far does not rule out later investment closer to those dates.

The report also contextualizes Fairshake’s prior activity in those states. In 2024, the PAC and affiliates reportedly spent more than $10 million in Arizona to support Ruben Gallego’s Senate race, and about $2.1 million to support Democratic Representative Yadira Caraveo in Colorado’s 8th district. Gallego ultimately won, while Caraveo lost in the November 2024 election to Republican Gabe Evans.

With that background, upcoming Colorado and Arizona primaries may serve as a test of whether earlier spending patterns translate into similar success—or whether PAC strategy shifts in response to local dynamics and candidate field changes.

As the next primary dates approach, readers should watch for new disclosures of PAC expenditures and for how candidates in Colorado and Arizona respond to crypto-related campaign narratives—particularly whether the same “early and aggressive” ad strategy credited in Tuesday’s races repeats or evolves.

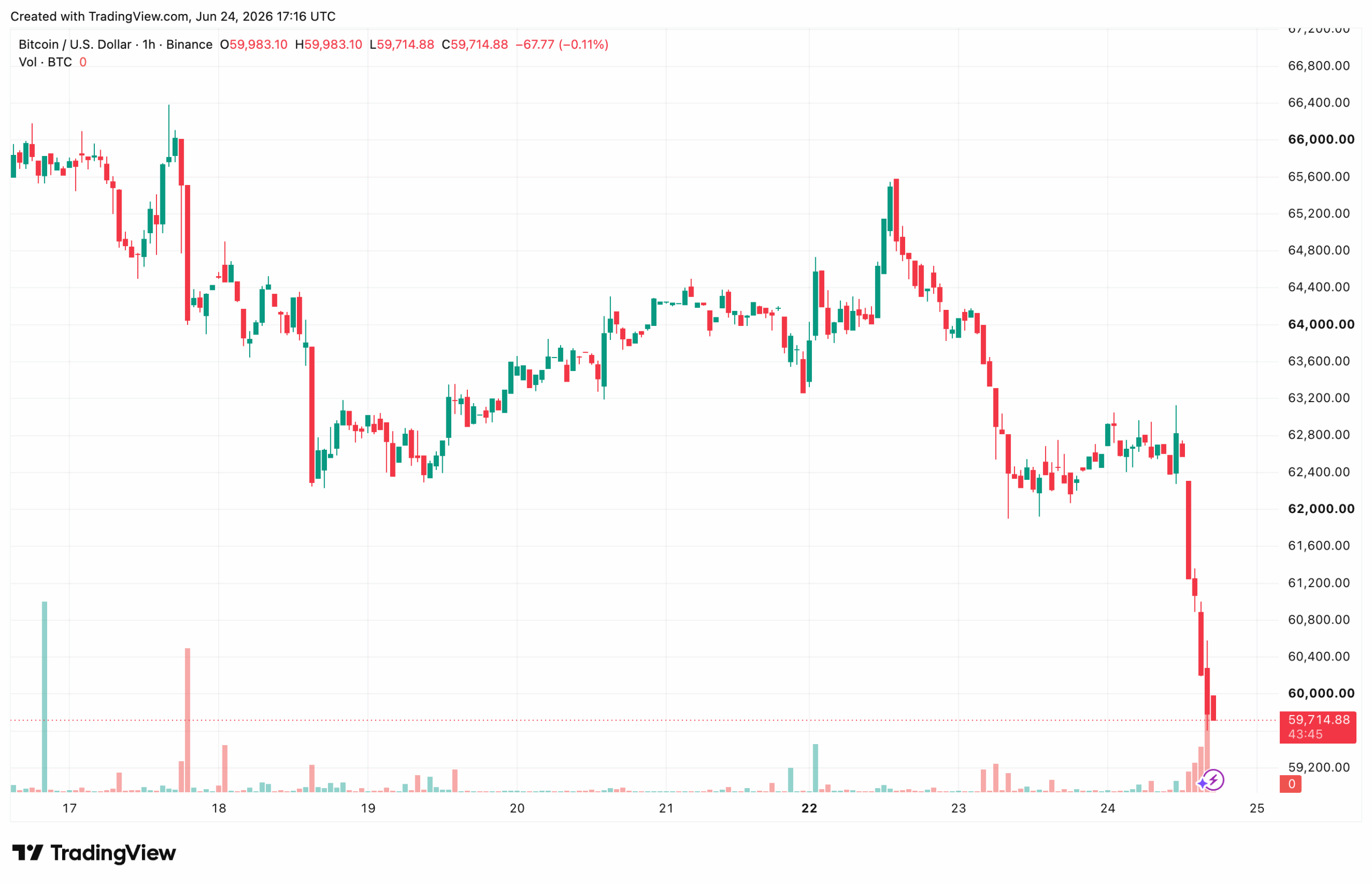

Bitcoin (BTC) has fallen 3% over the past 24 hours, trading into a dense buy-side liquidity zone after slipping below $61,000. More than $525 million in buy bids initially stacked between $60,500 and $61,500 created a key area of demand as liquidation risk builds on both sides of the market.

BTC’s orderbook data shows concentrated liquidity pockets below $60,500 and near $65,000, placing liquidity flows at the center of Bitcoin’s short-term price action.

Bitcoin momentum weakens below $63,000

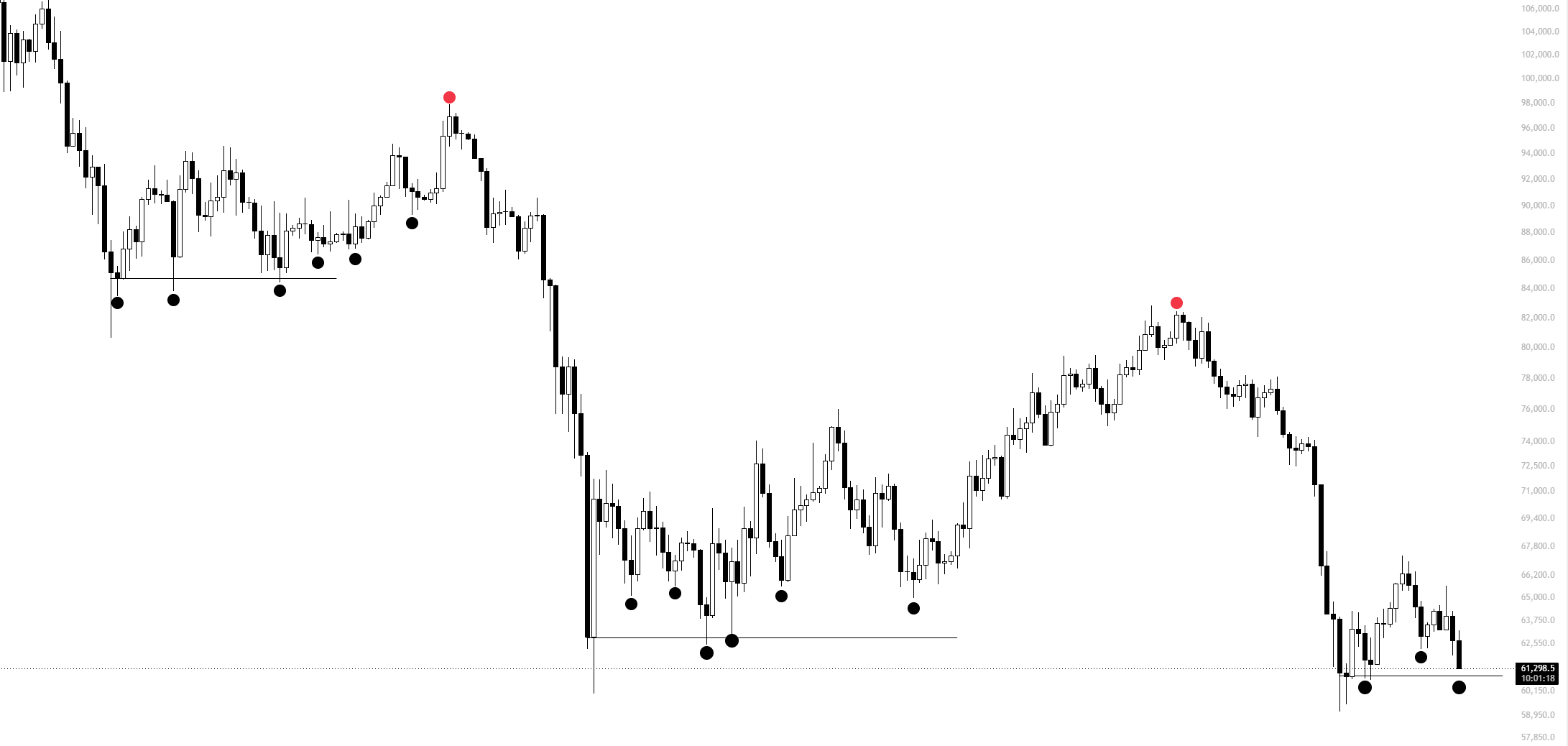

Bitcoin closed at $62,700 on Tuesday, its lowest daily candle close since June 10. The move also produced a bearish engulfing candle against Monday’s range, erasing the prior day’s gains and signaling weaker short-term momentum.

BTC/USDT, one-day chart. Source: Cointelegraph/TradingView

The price has since consolidated beneath $63,000 after losing that level as support. The one-hour chart shows a series of lower highs following the rejection near $66,000 earlier this week. The momentum indicator, or relative strength index (RSI), has cooled from recent overbought levels, while Bitcoin continues to trade above the June range low near $60,500.

BTC/USD, one-hour chart. Source: Cointelegraph/TradingView

Crypto trader Lennaert Snyder called for caution and expected BTC to test the lower liquidity before considering long exposure. The trader said,

“Bitcoin started a little bounce, but I’m not convinced and not buying in yet,” Snyder wrote in a recent market update.

The trader identified $61,500 and $60,500 as the primary levels to watch for bullish reactions. On the upside, he pointed to $63,500 and $64,000 as potential areas where liquidity could attract price before another move lower.

$530 million in BTC buy bids sit below $61,000

Data from Velo shows that BTC traders initially added 8,366 BTC to bid liquidity between $61,500 and $60,500. At the time of writing, Bitcoin has traded through a significant portion of that range, triggering roughly $270 million worth of buy orders as the price dipped below $61,000.

The remaining bids remain near the lower end of the liquidity cluster, where traders are attempting to absorb the latest wave of selling pressure.

BTC buy bids analysis. Source: Velo Chart

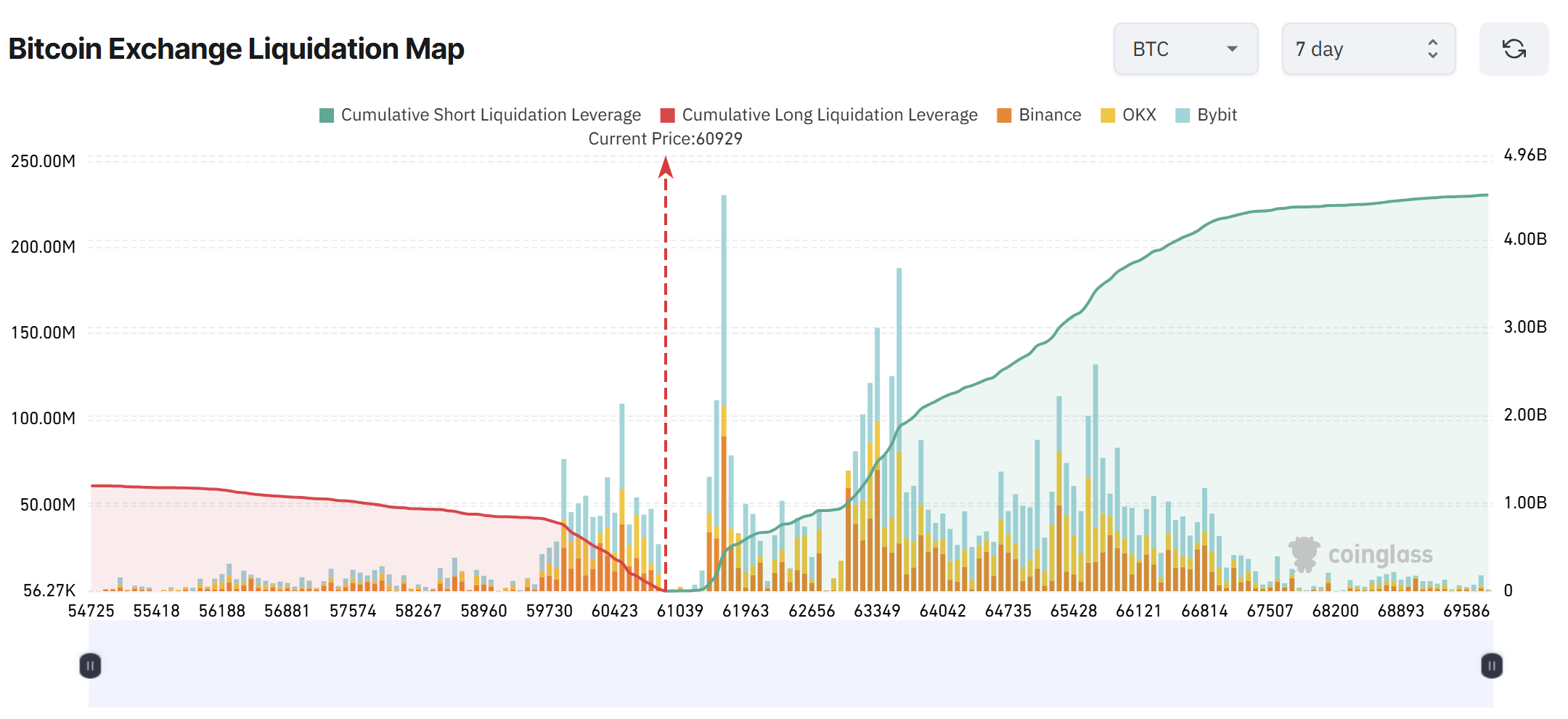

The move below $61,000 has already flushed a significant portion of the leveraged long positions clustered around $61,500. CoinGlass data shows more than $125 million in long liquidations over the past hour, reducing downside liquidation pressure near the current price.

With much of the nearby long-side leverage cleared out, the liquidation map now shows a growing imbalance toward short positions positioned above spot price.

Now, more than $1.2 billion in short positions sit near $63,500. A stabilization in the remaining bid liquidity around $60,500-$61,000 may shift attention toward those positions, especially as the downside liquidation pools become less concentrated following the latest flush.

Bitcoin liquidation map. Source: CoinGlass

The next major concentration of liquidation risk sits near $65,000, where more than $2.4 billion in short positions are vulnerable. Such setups often trigger fast moves as liquidations fuel additional buying. For now, the largest liquidity concentrations remain near $60,500, where both spot demand and leveraged exposure remain heavily stacked.

Related: BTC price four-year trend calls for $76K as analysis says Bitcoin ‘not broken’

Key Points

-

Presidential postponement leaves Federal Reserve digital currency prohibition uncertain.

-

Legislation would prevent Fed-issued digital dollar implementation until 2030.

-

Presidential signature contingent on passage of voter registration requirements.

-

Private stablecoin exemptions preserved within housing legislation framework.

-

Senate cryptocurrency regulatory proposals encounter additional legislative complications.

President Donald Trump has put a federal prohibition on central bank digital currencies in jeopardy after canceling Wednesday’s anticipated signing ceremony for a comprehensive bipartisan housing reform package. The measure would prevent the Federal Reserve from launching a retail central bank digital currency until the end of 2030. Trump’s decision ties the legislation’s fate to separate voter identification requirements.

Presidential Approval Conditional on Election Reform Measure

Through his Truth Social platform, Trump announced the ceremony cancellation moments before its scheduled commencement at the White House. He stipulated that congressional lawmakers must first approve the SAVE America Act, legislation mandating citizenship verification during federal voter registration. This maneuver threw both the housing reform package and its embedded CBDC prohibition into sudden legislative limbo.

The SAVE America Act mandates documentary proof of United States citizenship for individuals registering to participate in federal elections. Proponents characterize this requirement as essential election integrity infrastructure, while critics contend it creates unnecessary obstacles for legitimate voters. Trump has urged Republican senators to expedite the proposal despite minimal Democratic backing.

The housing legislation sailed through the House of Representatives with 358 affirmative votes against 32 negative votes, following Senate passage by an 85-to-5 margin. The bill consequently arrived at the executive branch with extraordinary bipartisan consensus. Trump nevertheless suspended the ceremony despite widespread support from congressional leadership in both chambers.

Digital Currency Prohibition Embedded Within Housing Reform

The 21st Century ROAD to Housing Act principally addresses housing inventory expansion, affordability challenges, mortgage lending protocols, and construction regulatory obstacles. Congressional negotiators, however, inserted provisions barring the Federal Reserve from developing or deploying a retail CBDC. This prohibition would maintain force through December 31, 2030.

The language additionally encompasses digital instruments exhibiting characteristics substantially similar to central bank digital currencies. Critically, it carves out private dollar-denominated assets functioning through transparent, permissionless, and decentralized infrastructure. This exclusion safeguards eligible stablecoins from the federal restriction.

Trump has previously issued executive guidance prohibiting federal agencies from establishing, deploying, or advocating for a United States CBDC absent explicit statutory authority. While the Federal Reserve has conducted exploratory research into digital currency possibilities, no digital dollar has been introduced. The congressional language would therefore codify existing executive policy through statutory law.

Legislative Postponement Complicates Cryptocurrency Regulatory Agenda

Trump retains the option to sign the housing package following congressional advancement of his preferred election legislation. Constitutional procedures also permit the measure to achieve legal status without presidential signature. Timing will depend on formal legislative presentation protocols and congressional scheduling dynamics.

This postponement may generate additional uncertainty surrounding the Digital Asset Market Clarity Act currently pending. That legislation would establish jurisdictional boundaries for digital asset oversight and allocate regulatory responsibilities among federal agencies. Trump has previously expressed support for establishing comprehensive market structure frameworks for the cryptocurrency industry.

The CLARITY Act awaits Senate floor deliberations, potential amendments, and conclusive voting. Simultaneously, legislators continue negotiating ethical guidelines concerning political figures’ participation in digital asset enterprises. The housing legislation dispute now injects another political prerequisite into an already congested Senate legislative schedule.

Trump has not issued explicit veto threats regarding the market structure legislation or other pending cryptocurrency proposals. Nevertheless, his refusal to advance unconnected measures may decelerate congressional progress across multiple policy domains. The CBDC prohibition consequently remains entangled with broader controversies involving housing policy, electoral procedures, and digital asset regulatory frameworks.

Crypto World

The Death of the Petrodollar: Nouriel Roubini Outlines Shift to AI-Backed ‘Technodollars’

Economist Nouriel Roubini has declared the “death of the petrodollar” and backed a new tokenized reserve asset called ‘Technodollar’ tied to US productive assets, marking his first formal move into digital assets after years as one of crypto’s most prominent critics.

Speaking on the Expert Council podcast this week, Roubini said stablecoins fail to protect investors from the same inflation and debasement risks that affect traditional fiat currencies.

He argued that the next reserve asset should be linked to technology, artificial intelligence, defense, semiconductors, and other parts of the US economy.

The comments came as Atlas Capital Team launched USAFi, a tokenized reserve asset issued in Dubai under the Virtual Assets Regulatory Authority’s Asset-Referenced Virtual Asset framework.

Atlas says USAFi introduces a new category of regulated digital reserve infrastructure. The token is structured as a permissionless ERC-20 asset and is directly collateralized by the Atlas America Fund, an SEC-registered, actively managed ETF listed on Nasdaq under the ticker USAF.

The Illusion of On-Chain Safety

For years, crypto investors have treated dollar-pegged stablecoins such as USDT and USDC as safe places to park capital during market stress.

Roubini said that view misses a larger problem. Stablecoins may help with payments, but they still track a fiat currency that can lose purchasing power during inflationary periods.

“Stablecoins are going to be useful as a means of payment… but if the critique of cryptocurrency was the risk of debasement that comes from inflation, then something that is not interest bearing, like a stablecoin, just a digital dollar with zero interest rate, is subject to the same kind of a debasement risk as a fiat,” Roubini said. “Stablecoins are a very imperfect way of providing this hedging. Highly imperfect is essentially a digital version of the fiat currency with all the problems of fiat currencies.”

His argument is simple. A token that only tracks the dollar does not solve the dollar’s weakness. It moves that weakness onto the blockchain.

That matters more in an economy facing persistent inflation, geopolitical shocks, and climate-related risks. In that environment, Roubini argues that investors need exposure to assets that can preserve real value, rather than digital cash that earns no yield.

From Petrodollars to Technodollars

Atlas framed USAFi around a larger shift in the global reserve system.

In a whitepaper published alongside the launch, the firm said the world has moved from the gold standard of 1944 to 1971, then to the energy-backed petrodollar from the 1970s onward. It now sees a new phase built around what it calls the “technodollar.”

The thesis is that US economic power is increasingly driven by technology rather than oil. Atlas says a reserve asset backed by AI-linked equities, semiconductors, defense technology, cyber infrastructure, short-duration Treasuries, gold, and climate-resilient real estate offers a better hedge for the modern economy.

USAFi’s collateral comes through the Atlas America Fund, which is custodied at BNY Mellon. Atlas says the fund uses machine learning to manage risk across its portfolio.

“The machines do the homework and the people on the investment committee, which Nouriel chairs, make the call,” said Reza Bundy, Atlas Capital CEO and Chairman.

Bringing the Asset On-Chain

Atlas partnered with Securitize to bring the asset onto public blockchains. Securitize is the tokenization platform behind several institutional real-world asset products, including BlackRock’s tokenized fund infrastructure.

The goal is to make USAFi usable as on-chain collateral, rather than keeping it inside a closed institutional environment.

“We think that the tokenized version of it could actually be a very good fit as working as a reserve asset for DeFi collateral,” said Carlos Domingo, founder and CEO of Securitize.

The launch also reflects a broader shift in real-world asset tokenization. Tokenized Treasuries and money market products have already gained traction, but Atlas is pitching USAFi as a more adaptive reserve asset for periods of inflation and macro stress.

For Roubini, the core point is that digital assets cannot rely only on fiat replicas. If investors want protection from debasement, he argues, the collateral itself must change.

USAFi is his first major test of that idea.

The post The Death of the Petrodollar: Nouriel Roubini Outlines Shift to AI-Backed ‘Technodollars’ appeared first on BeInCrypto.

Bitcoin (BTC) hit new two-week lows at Wednesday’s Wall Street open as traders predicted a rally to a “poor” lower high.

Key points:

- Bitcoin price action edges closer to range lows, which traders still see holding.

- A relief bounce should enter soon, they say, with targets closer to $70,000.

- US-Iran peace progress has little bullish impact on risk assets, with US stocks flat at the open.

BTC price nears range lows: Is $70,000 next?

Data from TradingView showed BTC price action dropping below $60,000 for the first time since June 10.

BTC/USD four-hour chart. Source: Cointelegraph/TradingView

Traders had warned of increasing short interest with rising funding rates, boosting the odds of a capitulatory move lower.

“It’s time to start bouncing soon on the LTF,” trader Killa wrote in ongoing commentary on X, referring to low time frames.

“Range bound till proven otherwise.”

BTC/USD chart segment. Source: Killa/X

Killa uploaded a further chart showing a relief bounce toward $70,000, being due following the bounce.

BTC/USD chart segment. Source: Killa/X

Fellow trader RektProof had a broadly similar forecast, seeing BTC/USD trading in a range with $60,000 as its floor “for the rest of the month.”

“Overall, a move to supply and back down to the EQ lows before forming back to poor highs + 70k,” he added.

BTC/USDT one-hour chart. Source: RektProof/X

Stocks tread water as Hormuz oil transit progresses

On a macro level, US stocks appeared to have already priced in relief from the US-Iran peace deal.

Related: BTC price four-year trend calls for $76K as analysis says Bitcoin ‘not broken’

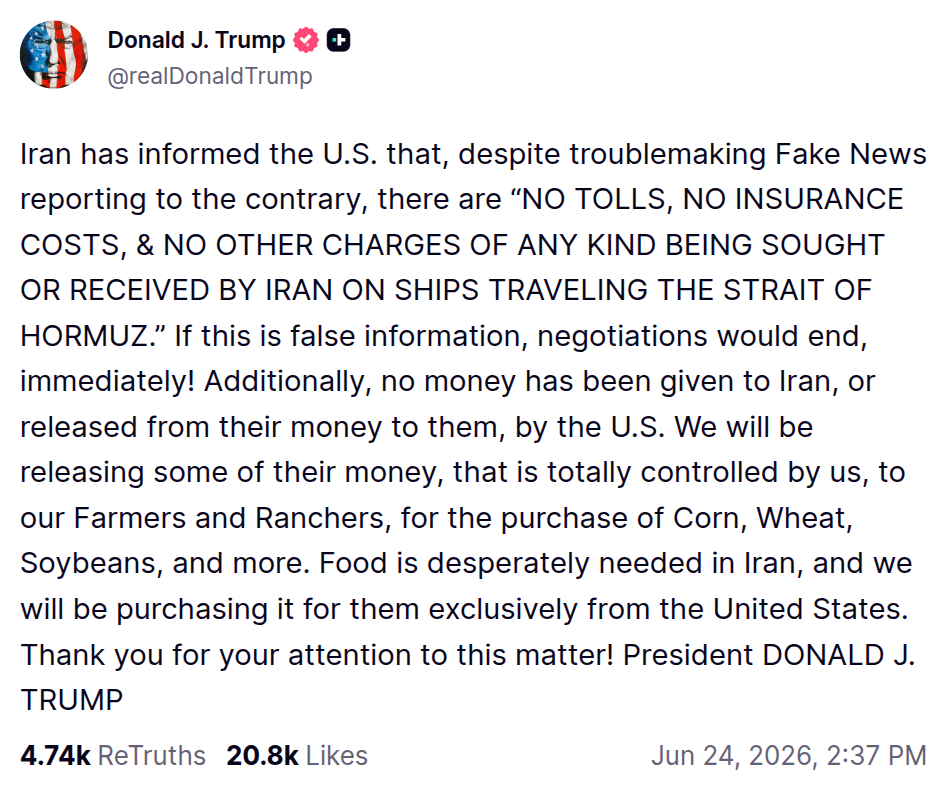

Upside was limited at the open despite US President Donald Trump offering further details of mutual cooperation between the two sides.

Trump specifically made reference to the Strait of Hormuz oil transit route, writing in a post on Truth Social that there would be “no tolls, no insurance costs, & no other charges of any kind being sought or received by Iran on ships traveling” via the route.

Source: Truth Social

The S&P 500 traded up 0.4% at the time of writing, while the Nasdaq Composite Index even turned slightly negative on the day.

Earlier, Cointelegraph reported on several factors keeping risk-asset enthusiasm in check, including forward earnings guidance by tech giant Micron Technologies and the May print of the Personal Consumption Expenditures (PCE) index, due out on Wednesday and Thursday, respectively.

Crypto World

Strategy Stock Falls Below $100 for First Time in Two Years as Analysts Pick Apart Its Bitcoin Bet

Shares of Strategy, the largest corporate holder of Bitcoin, fell below $100 on Wednesday for the first time since March 2024, leaving the company trading at a discount to the Bitcoin on its balance sheet and turning investor attention to which layer of its capital structure is still worth owning…. Read the full story at The Defiant

Houses will stay cool during the heatwave with 6 ‘super effective’ tips

U.S. banks can withstand $708B in losses

Bitcoin Price Crashes Below $60K as Strategy’s MSTR Plunges 10%

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports1 day ago

Sports1 day agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Crypto World16 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World13 hours ago

Crypto World13 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business19 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoAndy Burnham and the meaning of Makerfield

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Crypto World4 days ago

Crypto World4 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World4 days ago

Crypto World4 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Business6 days ago

Business6 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

You must be logged in to post a comment Login