Crypto World

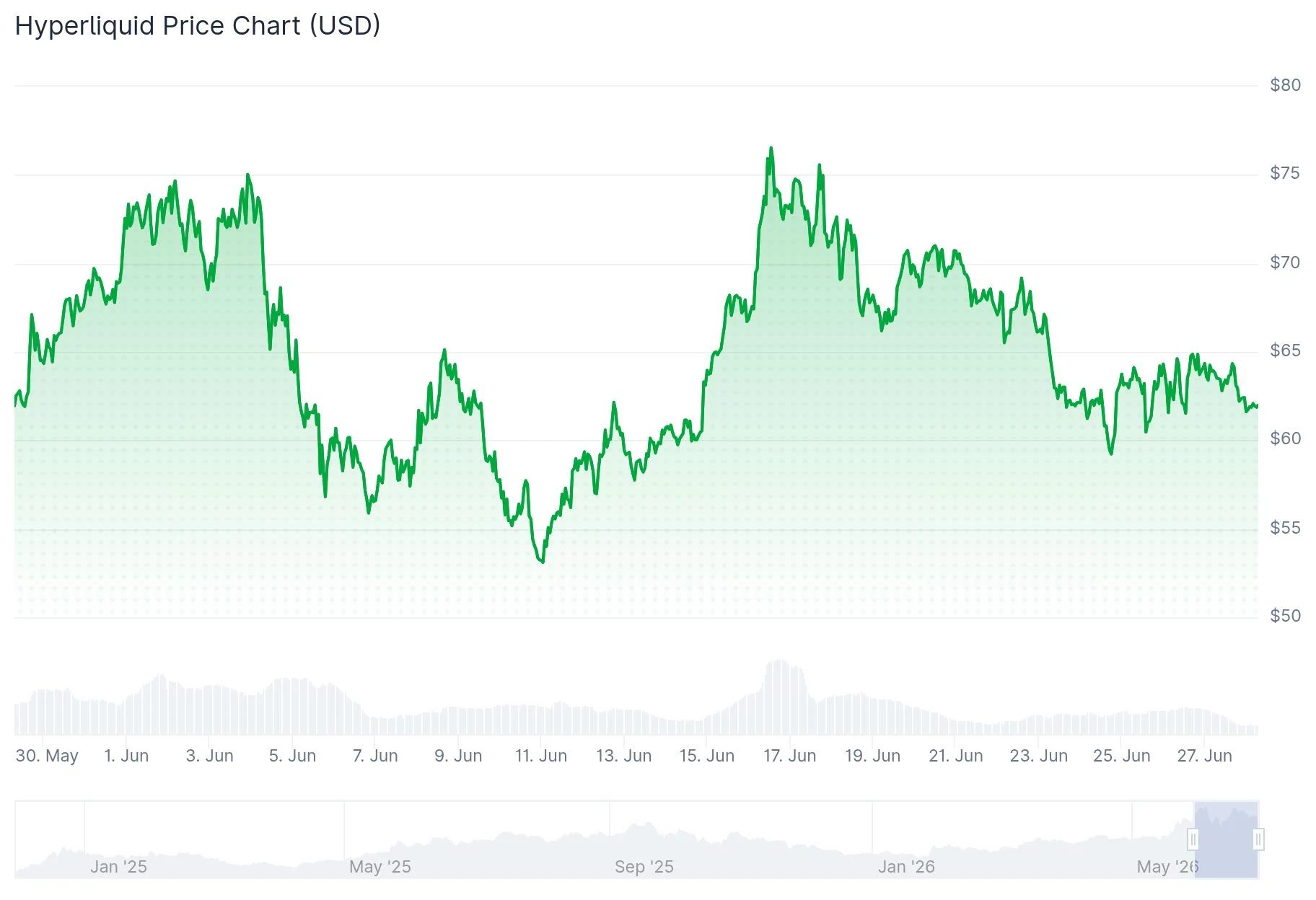

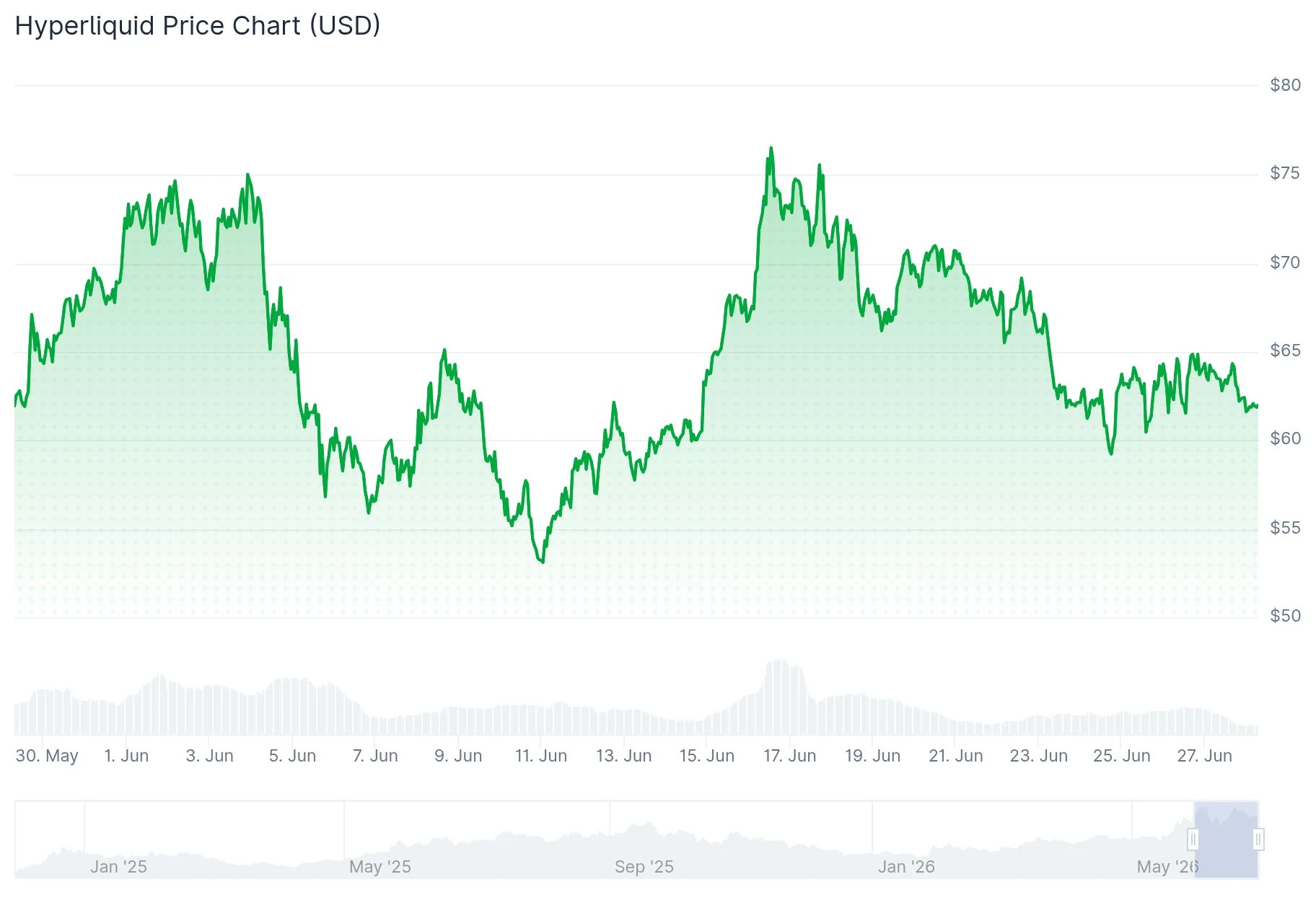

Hyperliquid (HYPE) 5-Year Price Forecast: Analyzing the Path to 2031

Key Takeaways

- HYPE is currently valued near $62 with a multi-billion dollar market capitalization

- Baseline scenario projects $100–$160, valuing HYPE as a decentralized exchange token

- Optimistic scenario envisions $250–$400 if Hyperliquid dominates on-chain derivatives trading

- Pessimistic scenario suggests $20–$35 amid competitive pressures, security incidents, and token dilution

- Weighted probability analysis points to approximately $145 by the year 2031

Hyperliquid stands out in a crowded cryptocurrency landscape by delivering tangible results. Unlike countless projects built purely on speculation, Hyperliquid has secured more than 40% of the decentralized perpetual futures market by mid-2026. This represents genuine market dominance backed by data.

Currently trading near $62, HYPE’s valuation fundamentally depends on transaction volume, fee generation, and platform liquidity rather than empty promises.

The protocol handled transaction volumes in the hundreds of billions throughout the first quarter of 2026, with daily figures consistently reaching into the billions. These metrics mirror those of established centralized exchanges.

This performance explains why market observers increasingly compare HYPE’s valuation framework to traditional exchange tokens rather than standard Layer 1 blockchain assets.

Baseline Projection: $100 to $160 Range

The baseline forecast assumes Hyperliquid maintains its leadership position within decentralized perpetuals throughout the coming half-decade.

This scenario requires continued migration of traders toward on-chain platforms, sustained growth in cryptocurrency derivatives markets, and Hyperliquid’s ability to defend its market share. A valuation range of $100 to $160 would translate to a fully diluted market cap between $100 billion and $160 billion, calculated against the maximum token supply of 1 billion HYPE.

While ambitious, these valuations become reasonable if Hyperliquid evolves into essential infrastructure for cryptocurrency trading.

Reuters coverage indicates that cryptocurrency exchanges are positioning themselves for expanded U.S. perpetual futures offerings as regulatory frameworks crystallize. This regulatory shift could significantly expand Hyperliquid’s addressable market.

Optimistic and Pessimistic Scenarios

The optimistic projection places HYPE between $250 and $400. Achieving this requires Hyperliquid to dominate decentralized derivatives, successfully launch spot trading markets, attract significant institutional capital, and transform into a comprehensive on-chain financial infrastructure.

This scenario demands multiple favorable outcomes aligning simultaneously.

The pessimistic forecast settles between $20 and $35. Trading platform markets are intensely competitive. Centralized exchanges, dYdX, GMX, Solana ecosystem protocols, and emerging perpetual DEXs all compete for identical liquidity pools.

Security vulnerabilities represent substantial threats. The Financial Times documented a $280 million security breach at Drift, a rival decentralized derivatives platform. Such incidents can undermine confidence across the entire sector.

Token supply expansion creates additional downward pressure. The current circulating supply represents only a fraction of the 1 billion maximum HYPE tokens. Future unlock events occurring during periods of weak demand could significantly depress prices.

The probability-adjusted five-year projection estimates approximately $145 by 2031.

Hyperliquid commands over 40% of decentralized perpetual futures volume as of mid-2026, with daily trading consistently reaching billions of dollars.

Strategy is roughly $12 billion underwater on its Bitcoin, its stock has fallen below its net asset value, and its STRC preferred shares have crashed to a record discount as a law firm opens a fraud probe. Michael Saylor says nothing is wrong. The machine that bought 847,000 Bitcoin is being tested like never before. Here is what is actually happening.

Summary

- Strategy holds 847,363 Bitcoin, the largest corporate stockpile in the world, bought at an average cost near $75,650, leaving the position roughly $12 billion underwater with Bitcoin below $60,000.

- MSTR stock has fallen below $100 for the first time in about two years, trading at a discount to the Bitcoin it owns, which breaks the premium that powered its fundraising model.

- The sharpest stress is in STRC, Strategy’s preferred stock designed to trade near $100, which crashed to a record low near $74 as dividend obligations quadrupled to $1.2 billion and cash coverage collapsed from over seven years to about 14 months.

- A law firm has opened a securities-fraud investigation into Strategy and Saylor, and analysts including CryptoQuant have urged the company to stop buying Bitcoin and rebuild cash.

- Saylor says Strategy’s Bitcoin and cash exceed its debt by roughly $48 billion and points to surviving a worse 2022; the debate is whether this is a temporary confidence shock or a structural flaw in the model.

For five years, Michael Saylor’s company had one move, and it worked beautifully: issue securities, buy Bitcoin, watch the stock rise, repeat.

Strategy, the firm formerly known as MicroStrategy, rode that flywheel to a stockpile of 847,363 Bitcoin, roughly 4% of all the Bitcoin that will ever exist and the largest corporate hoard on earth.

The mechanism depended on a simple condition: that Bitcoin kept climbing and that Strategy’s stock traded at a premium to the Bitcoin on its balance sheet, so the company could sell shares to buy more coins on favorable terms.

In June 2026 that condition broke.

Bitcoin slid below $60,000, dragging Strategy’s position roughly $12 billion below what it paid for its coins. Its stock, MSTR, fell under $100 for the first time in about two years and is now trading at a discount to the very Bitcoin it holds.

And the company’s preferred stock, a security called STRC that was engineered to sit near $100, crashed to a record low around $74.

On top of the financial squeeze, a law firm has opened a securities-fraud investigation into the company and Saylor himself.

The flywheel that defined a half-decade of relentless accumulation is, for the first time, visibly spinning in reverse.

The question this raises is the one now dividing the market: is Strategy facing a temporary loss of confidence that a Bitcoin recovery would erase, or is something structurally broken in the model itself?

The stakes are large, because Strategy controls about 4% of all Bitcoin, and any sign that its machine is failing reverberates across a market already fragile from the June sell-off.

This piece works through what is actually happening, without either the doom that some critics project or the serenity that Saylor performs.

It explains the three interlocking pieces that make up Strategy’s structure and why they are straining at once, the specific crisis in the STRC preferred stock, the fraud investigation and the criticism from analysts, Saylor’s defense and the case that the company is fine, the genuinely difficult choices the company now faces, and what would resolve the question in either direction.

The aim is a clear, grounded picture of a financial machine under its sharpest stress in years, and an honest assessment of whether it is bending or breaking.

The three legs of the machine

To understand why Strategy is under pressure, you have to understand how its structure works, because the strain comes from three interdependent pieces leaning on one another and weakening at the same time.

The first leg is Bitcoin itself, the reserve asset, which Strategy holds in enormous quantity and treats as a permanent store of value that only grows over time.

The crucial feature of Bitcoin for this purpose is also its limitation: it produces no income. It pays no dividend and no interest, so while it can sit on the balance sheet appreciating, it generates none of the cash the company needs to meet its obligations.

That gap between a non-yielding reserve asset and cash obligations is the hinge on which the whole structure turns.

The second leg is MSTR, the common stock, which functions as the engine.

When MSTR trades above the value of the Bitcoin behind it, at a premium, Strategy can sell shares to buy more Bitcoin, and the premium makes that buying accretive, adding more Bitcoin per share than it dilutes.

This is the mechanics of the reversal that now matters. The same flywheel that works in a bull market starts to drag when the premium disappears.

The engine works in reverse when the premium disappears: raising $500 million at $500 a share takes 1 million shares, while raising the same amount at $50 takes 10 million shares.

That is the same cash for 10 times the dilution, which erodes the very reason to hold MSTR.

The third leg is STRC, the credit leg, a preferred stock with a stated value of $100 that pays a cash dividend, recently yielding around 11.5%.

STRC works only as long as investors trust that the dividend will keep coming, and Strategy can raise the rate to attract buyers when the price slips.

Each leg holds up the others. Bitcoin is the collateral story that supports the stock, the stock is the engine that funds the buying, and the preferred is the credit instrument that raises cash.

When all three weaken at once, as they have, the question shifts from how much Bitcoin Strategy owns to whether it has the dollars to keep its word.

That shift is the heart of the current crisis.

The STRC crisis

The most acute stress is concentrated in STRC, and it is worth understanding in detail because it is where an abstract worry becomes a concrete problem.

STRC, formally a variable-rate perpetual preferred stock, was designed to trade near its $100 stated value, held there by a variable dividend mechanism that raises the payout to keep the price anchored.

Saylor has spent months explaining the structure publicly, framing STRC as part of Strategy’s broader Bitcoin-backed capital machine.

That design has failed under pressure.

STRC crashed to a record low, touching around $74 intraday before recovering somewhat, leaving it trading roughly a quarter below the par value it was engineered to hold.

A preferred stock trading that far below par is the market’s way of saying it demands far more yield before it will treat the instrument as sound, which is a vote of diminishing confidence in the dividend behind it.

The reason for that lost confidence is a squeeze coming from both directions at once.

As Strategy issued more and more STRC over the first half of 2026 to fund Bitcoin purchases, its annual dividend obligations ballooned from about $300 million at the start of the year to roughly $1.2 billion, a near fourfold increase in under six months.

At the same time, its cash reserves fell by 38% over the same period, drained in part by a $1.5 billion repurchase of convertible debt in May.

The result is a collapse in what analysts call dividend coverage, the measure of how long the company’s cash could keep funding the payouts: it fell from more than seven years to approximately 14 months.

A particularly unforgiving feature of STRC compounds the problem. Its dividends are cumulative, meaning any payment Strategy skips still has to be made up later.

So the company cannot simply switch the dividends off to conserve cash, and it is unlikely to suspend them anyway because doing so would shatter its credibility with the preferred holders it depends on.

CryptoQuant calculated that to restore a healthy 24 months of coverage and let STRC recover its peg, Strategy would need to rebuild its reserve to roughly $2.8 billion, against the roughly $1.4 billion it holds.

That is why CryptoQuant’s warning that Strategy should pause Bitcoin purchases and rebuild cash matters. The issue is not just the price of STRC; it is whether the cash behind the whole preferred-stock structure is thick enough to survive a prolonged Bitcoin drawdown.

STRC, in short, is the leg that is visibly cracking, and it is cracking because the cash behind its promises is running thinner while the promises themselves have multiplied.

The fraud probe and the analyst warnings

The financial squeeze has now drawn legal and analytical fire, which has intensified the pressure and the scrutiny.

A plaintiff law firm announced a securities-fraud investigation into Strategy and Michael Saylor, soliciting investors who bought the company’s securities and incurred losses, and saying it is examining whether the company may have issued materially misleading business information to the investing public.

The probe covers all five of Strategy’s publicly traded securities, the common stock and four series of preferred.

It is important to be precise about the status of this: an investigation announcement of this kind is common in volatile sectors, no class action has actually been filed, the allegations are unproven, and Strategy has not publicly responded.

It does not establish wrongdoing.

But it adds a layer of legal uncertainty and reputational pressure at the worst possible moment, and it has fed the narrative that something is wrong.

That narrative intensified because prominent critics have also tied the decline in MSTR and STRC to broader Bitcoin weakness, arguing that Strategy’s structure is no longer a harmless side story but a market stress point.

The analytical warnings have been sharper and more substantive than the legal noise.

CryptoQuant published a detailed report urging Strategy to stop buying Bitcoin and rebuild its cash position before resuming accumulation, laying out the collapse in dividend coverage and noting that the company sits on a large unrealized loss with every Bitcoin bought in 2024, 2025, and 2026 now underwater.

Its chief executive argued that a forced Bitcoin sale at current prices would crystallize those losses and destroy shareholder value.

He also separately observed that Strategy’s relentless buying had begun to look more like a liquidity sink than a price catalyst, absorbing capital without moving Bitcoin’s price upward.

Another firm suggested Strategy might eventually need to sell $3 billion to $4 billion of Bitcoin to ease the pressure on its capital structure, though it assigned that outcome only a modest probability and saw continued small stock sales as the likelier path.

Not all of the analysis was bearish. One firm rejected comparisons between STRC and the collapsed Terra stablecoin, arguing the funding engine had become less efficient rather than broken.

But the weight of the commentary converged on a single uncomfortable message: Strategy has overextended itself by buying too aggressively while its cash thinned, and the model needs to change, at least temporarily, to stabilize.

Saylor’s defense

Michael Saylor’s response to all of this has been characteristically defiant, and his arguments deserve a fair hearing because they are not without merit.

His central rebuttal, made in a public post, is one of scale: Strategy’s Bitcoin and cash reserves exceed its outstanding debt by roughly $48 billion, a cushion so large that talk of insolvency or forced selling, in his framing, misunderstands the company’s actual financial position.

He has emphasized that Strategy has raised more than $60 billion in additional capital since 2022 and invested it in Bitcoin, building the largest corporate stockpile in the world.

He points to that track record as evidence of a model that works through cycles rather than one on the verge of collapse.

His most pointed argument is historical.

Saylor has reminded the market that Strategy faced a far worse situation in the 2022 bear market, when Bitcoin fell below $16,000 and the company’s debt actually exceeded the combined value of its Bitcoin and cash reserves, with the stock falling roughly from the mid-$20s to the low teens on a split-adjusted basis.

Strategy survived that, he notes, by staying focused and continuing to execute its strategy, and went on to raise tens of billions more and add hundreds of thousands of Bitcoin.

The implication is clear: the company has been underwater before, in a deeper hole than today’s, and not only survived but expanded dramatically once Bitcoin recovered.

That makes the current stress, in Saylor’s framing, a familiar test rather than an existential threat.

Defenders have echoed and extended this case, with some arguing that Bitcoin’s market value cannot be pinned on any single individual and dismissing the comparisons between Strategy and collapsed crypto projects.

Others have praised STRC as a genuinely innovative instrument that strips volatility from Bitcoin exposure and could serve an enormous market.

Notably, Saylor has not publicly addressed the fraud investigation or the CryptoQuant warning directly, choosing instead to make the broad case for the company’s strength.

His defense, in essence, is that the fundamentals dwarf the fears, that the company has weathered worse, and that the panic reflects a temporary loss of confidence instead of a real flaw.

The hard choices

Whatever the rhetoric on either side, Strategy now faces a set of truly difficult choices, and laying them out shows why the situation is more than a passing scare even if it is not a collapse.

The company needs cash to fund STRC’s growing dividends and to rebuild the reserve that supports confidence in those dividends, and every available path to that cash carries a cost.

It can issue more common stock, but with MSTR trading below the value of its Bitcoin, doing so means heavy dilution that further erodes the reason to hold the stock, weakening the engine.

It can issue more preferred stock or raise STRC’s dividend rate to attract buyers, but more preferred means more dividend obligations and a higher rate deepens the cash drain, worsening the very problem it is trying to solve.

Each financing lever, in other words, tightens one part of the structure while loosening another.

That leaves the option the entire model was built to avoid: selling Bitcoin.

Selling would refill the reserve quickly and could even let Strategy buy back STRC below par, retiring a $100 claim for around $80, which on a spreadsheet is rational.

But it is precisely the move that would confirm the market’s deepest fear, because the whole proposition of the company is that its Bitcoin stack is permanent, a leveraged bet that never sells.

Strategy has already cracked that door open.

Earlier in June it sold 32 Bitcoin, a trivial amount against its holdings, to help fund preferred distributions, in what was its first net Bitcoin disposal since 2022.

The sale was tiny, but its symbolism was enormous, because it showed the treasury could become a funding source for the structure built on top of it, which reframes every future shortfall.

If a small sale was acceptable once, a larger one is no longer unthinkable, and selling near current levels would also turn paper losses into realized ones.

Strategy appears to have absorbed the warnings to some degree, slowing its Bitcoin buying sharply and routing fresh stock-raise proceeds into its cash reserve instead of into more Bitcoin.

That is a sensible defensive move, but it is also an admission that the relentless accumulation defining the company has had to pause.

That is a meaningful change in posture for a firm whose identity is built on never stopping.

Is the model breaking?

So is Saylor’s model actually breaking, or merely being tested?

The honest answer is that it depends almost entirely on one variable the company does not control: the BTC price the model depends on.

Both the bull and bear readings are internally coherent.

The case that it is not breaking rests on Saylor’s strongest point: there is no immediate crisis.

Strategy is not required to sell Bitcoin, faces no margin call, and holds Bitcoin worth far more than its debt, with a cash reserve it has just moved to strengthen.

STRC holders cannot redeem their shares against the treasury, which removes the run-on-the-bank dynamic that destroys leveraged structures.

The company has survived a deeper hole before. And a Bitcoin recovery would reset the entire picture, lifting the value of the holdings, reviving the premium in MSTR, restoring confidence in STRC, and turning today’s stress into a footnote.

On this reading, the model is bending under a cyclical downturn, exactly as it is designed to, and will spring back when Bitcoin does.

The case that it is breaking, or at least structurally strained, is subtler and does not depend on imminent collapse.

It is that the model’s efficiency, not its solvency, is the real casualty.

The flywheel worked because of the premium and the perpetual buying, and both have been compromised: the premium has inverted into a discount, making new stock issuance dilutive instead of accretive, and the buying has had to pause.

Meanwhile the cost of maintaining the structure keeps rising, with dividend obligations that have quadrupled and a coverage cushion that has thinned to little more than a year.

That means the company must now spend real resources just to hold the structure together until Bitcoin recovers.

This is why how treasury firms are valued matters. A Bitcoin treasury company can look simple when its stock trades above NAV; it looks very different when the premium becomes a discount.

The deeper worry is reflexive: the cleanest fix for the cash problem, selling Bitcoin, is also the action that would most damage the premium and the narrative that the stack is permanent.

That leaves the company caught between a cash squeeze and an identity it cannot abandon without undermining itself.

In this reading, the machine does not break in a single dramatic event. It grinds less efficiently, costs more to run, and depends ever more heavily on a Bitcoin recovery that may or may not come on the needed timeline.

The truest synthesis is that Strategy is not facing insolvency but is facing the first serious test of whether its financing model can function when its core assumptions, a rising Bitcoin and a premium stock, both fail at once.

The answer will be written by Bitcoin’s price over the coming months.

Until then, the model is neither clearly broken nor clearly fine, but visibly, and for the first time in years, under genuine strain.

Frequently asked questions

How much is Strategy underwater on its Bitcoin?

Strategy holds 847,363 Bitcoin, bought for roughly $64 billion at an average cost near $75,650 per coin. With Bitcoin trading below $60,000, that position is underwater by approximately $12 billion, meaning the coins are worth that much less than the company paid. Every Bitcoin purchased in 2024, 2025, and 2026 is now below its purchase price. Importantly, this is an unrealized loss: it does not force Strategy to sell, does not trigger a margin call, and would only become a realized loss if the company actually sold coins at current prices. A Bitcoin recovery would reduce or erase it.

What is STRC and why is it crashing?

STRC is Strategy’s variable-rate perpetual preferred stock, designed to trade near its $100 stated value, held there by a variable dividend mechanism, recently yielding around 11.5%. It crashed to a record low near $74, roughly a quarter below par, because confidence in the dividend behind it has weakened. As Strategy issued more STRC to fund Bitcoin buying, its annual dividend obligations quadrupled to about $1.2 billion while its cash reserves fell 38%, causing dividend coverage to collapse from over seven years to about 14 months. A preferred stock trading far below par signals the market demands much more yield before trusting the instrument.

Is Strategy going bankrupt or being forced to sell Bitcoin?

Not imminently. Strategy holds Bitcoin worth far more than its debt, faces no margin call, is not required to sell, and recently moved to strengthen its cash reserve. Michael Saylor has said the company’s Bitcoin and cash exceed its debt by roughly $48 billion. STRC holders also cannot redeem their shares against the treasury, which removes the run-on-the-bank dynamic. The real pressure is not insolvency but the rising cost of maintaining the structure: funding growing dividends and rebuilding cash while its stock trades at a discount. Selling Bitcoin is one option the company has tested in tiny amounts, but it is not being forced into a large sale at this time.

What is the fraud investigation about?

A plaintiff law firm announced a securities-fraud investigation into Strategy and Michael Saylor, examining whether the company may have issued materially misleading business information to investors, covering all five of its publicly traded securities. It is important to be precise: this is an investigation announcement, not a lawsuit. No class action has been filed, the allegations are unproven, and Strategy has not publicly responded. Announcements like this are common in volatile sectors and do not establish wrongdoing. However, it adds legal uncertainty and reputational pressure at a difficult moment, and it has been amplified by critics suggesting Saylor may have crossed marketing rules in how he promoted the preferred stock.

What does Michael Saylor say about all this?

Saylor has been defiant, arguing the fears misunderstand the company’s position. His central points are that Strategy’s Bitcoin and cash exceed its debt by roughly $48 billion, that it has raised more than $60 billion since 2022 and built the largest corporate Bitcoin stockpile in the world, and that it survived a worse situation in the 2022 bear market. Back then, its debt briefly exceeded its Bitcoin and cash, but the company stayed focused and continued to execute. The implication is that the current stress is a familiar cyclical test instead of an existential threat. He has not directly addressed the fraud investigation or the analyst warnings, choosing instead to make the broad case for the company’s strength.

Is Saylor’s model actually breaking?

It depends heavily on Bitcoin’s price, and both readings are coherent. The case that it is fine: there is no immediate crisis, no forced selling, Bitcoin worth far more than the debt, and a Bitcoin recovery would reset everything, so the model is bending under a downturn as designed. The case that it is strained: the model’s efficiency has been compromised because the stock premium that made buying accretive has become a discount, the buying has paused, and the cost of maintaining the structure keeps rising. The cleanest cash fix, selling Bitcoin, would also damage the permanent-stack narrative the company is built on. The honest verdict is that the model is not broken but is facing its first serious test of whether it works when both a rising Bitcoin and a premium stock fail at once.

This article is information, not investment advice. Financial figures, securities prices, the status of legal investigations, and company actions reflect reporting available as of June 28, 2026, and can change quickly. The securities-fraud investigation referenced is unproven and has not resulted in a filed lawsuit. Nothing here is a recommendation to buy or sell MSTR, STRC, Bitcoin, or any security. Verify current details from primary sources and consider your own circumstances before making any decision.

Strategy is entering a tense stretch for its “digital credit” preferred stock STRC as the company weighs how to meet large cash obligations while continuing to manage its extensive Bitcoin holdings. In an X post on Saturday, Zach Pandl, head of research at Grayscale, said he hopes Strategy will sell at least $3 billion worth of Bitcoin to cover most of its cash commitments for the next two years.

Pandl’s commentary, however, points to a likely alternative outcome: he expects STRC’s dividend rate to rise by 50 basis points, which would add about $100 million in additional annual obligations over the next two years. For investors watching STRC trade below its $100 par value, that prospect may be less reassuring than a Bitcoin sale intended to stabilize Strategy’s capital structure.

Key takeaways

- Zach Pandl said he hopes Strategy sells at least $3 billion in Bitcoin over the next two years to meet most cash obligations.

- Pandl instead expects STRC’s dividend rate could increase by 50 basis points, adding roughly $100 million in annual obligations over two years.

- Strategy’s preferred stock STRC has been trading at a growing discount to its $100 par value, reflecting pressure on the “digital credit” segment.

- Strategy’s latest SEC filing shows it acquired 520 Bitcoin in mid-June while its cash reserve remains under closer scrutiny, with dividend coverage falling.

- CryptoQuant argues Strategy should pause new Bitcoin purchases and rebuild cash reserves, while others point to mechanisms that may defend STRC’s price without forcing sales.

Dividend math meets market pressure on STRC

Pandl’s remarks highlight a central tension in Strategy’s financing strategy: how to preserve liquidity and defend STRC’s credit profile without further weakening market confidence. He noted that Strategy faces an annual preferred dividend obligation of approximately $1.2 billion, driven primarily by STRC.

STRC is structured as a preferred stock designed to trade near its $100 par value, but it has been sliding for weeks. On Friday, STRC fell as low as $71.25—about a 28.75% discount to par—according to the figures cited in Pandl’s post. Strategy’s common stock, MSTR, also performed poorly; it closed Friday at $82.31, down 26.86% for the week.

Pandl acknowledged that a rate increase is likely if Strategy does not rely on asset sales. Yet he said the 50-basis-point dividend adjustment “probably does not help market confidence,” underscoring the challenge: higher dividends can increase total obligations, which may be read as a signal that liquidity needs are tighter than investors want to see.

SEC filing shows continued Bitcoin buying while cash cushion shrinks

Strategy remains the largest publicly listed corporate Bitcoin holder, with a reported 847,363 BTC stash. That scale means every financing decision—how much Bitcoin to hold, buy, or sell—carries added weight for markets watching corporate crypto exposure.

According to Strategy’s latest 8-K filing with the US Securities and Exchange Commission, the company acquired 520 Bitcoin for $34.9 million between June 15 and June 21. While that shows ongoing accumulation, other parts of the filing point to a thinner margin for error on cash management.

CryptoQuant, in a Tuesday report, argued Strategy should stop buying Bitcoin and instead focus on replenishing its cash reserve. The analytics firm said Strategy’s cash reserve is down 38% in 2026. In addition, the 8-K filing stated that Strategy increased its US dollar reserve by $300 million to $1.4 billion.

That reserve translates into about 14 months of dividend coverage, the filing indicated—down sharply from an earlier period when the company once had a seven-year cushion. Strategy’s own Monday post said it plans to keep replenishing cash reserves to support the credit quality of its “digital credit” securities, emphasizing the company’s intention to manage STRC through liquidity rather than letting credit fundamentals deteriorate.

Can STRC defend itself without selling Bitcoin?

CryptoQuant argued that Strategy has no direct obligation to sell Bitcoin to support STRC’s price. Instead, it suggested other tools could be used to defend the preferred stock, including raising the current dividend yield—citing the ability to adjust the yield (the report references an 11.5% dividend yield as a baseline) without liquidating Bitcoin.

Bitcoin advocate Samson Mow offered a different framing in a Monday X post, describing STRC as having a built-in “self-repairing mechanism.” His argument is that if STRC trades below its $100 reference price, Strategy halts new ATM issuance, reducing the supply of new shares. In parallel, a lower market price mechanically increases yield for new buyers relative to what they pay, which Mow said should attract demand and gradually pull the price back toward par.

In the same line of reasoning, this dynamic suggests that STRC’s discount could narrow over time even without Bitcoin sales—provided investors trust the market design and believe Strategy will prioritize liquidity management enough to sustain the dividend.

Still, the market reality reflected in STRC’s discount indicates that confidence is not automatic. Pandl’s comments add nuance: even if alternative defense mechanisms exist, investors may interpret a dividend-rate increase as a sign that more expensive capital or tighter resources are necessary.

What readers should watch next

With STRC trading far below its $100 reference price and dividend coverage reduced to roughly 14 months per Strategy’s filing, the next catalysts are likely to be any further announcements about dividend rate adjustments and whether Strategy changes its pace of Bitcoin buying in favor of liquidity replenishment, as CryptoQuant urged. Investors should track how quickly the company’s cash plan stabilizes credit expectations—because the market appears to be pricing not just Bitcoin exposure, but the near-term cost of maintaining “digital credit” obligations.

Ripple President Monica Long is set to appear at XRP Seoul 2026, adding a major company voice to one of Asia’s key XRP-focused events.

Summary

- Monica Long’s Seoul appearance comes as Korea remains one of XRP’s most active trading markets.

- XRP Seoul will connect holders, builders, and projects during Korea Blockchain Week on October 3.

- Ripple’s Korea ties now span custody, tokenized bonds, XRPL projects, and local developer programs.

The event will take place on October 3 during Korea Blockchain Week. It will bring together XRP holders, XRP Ledger builders, ecosystem projects, and companies working on blockchain finance.

Monica Long joins XRP Seoul lineup

The XRP Seoul account said it was “honored to welcome” Long to the event. The post described her as a leader across Ripple’s business, product, and engineering teams.

Long has worked at Ripple since 2013. The event page says she has helped build the company into a “one-stop shop to move, manage, hold and tokenize value.”

Her role gives the event added weight for XRP supporters. Ripple remains closely linked to XRP through its holdings, payments work, stablecoin strategy, custody services, and use of XRP Ledger infrastructure.

The appearance also comes as Korea Blockchain Week lists Long among its 2026 speaker lineup. The main KBW conference runs from September 30 to October 1 in Seoul.

Korea remains a major XRP market

South Korea has long been one of XRP’s most active retail markets. In a recent Korea and Japan trading review, XRP trading on Upbit and other Korean platforms stood out during several periods of strong market activity.

In May, XRP’s Korean won pair also led Upbit volumes after Hana Bank moved to buy a large stake in Dunamu, the operator of Upbit. As previously reported, XRP outpaced Bitcoin and Ethereum in 24-hour volume on the exchange at that time.

That trading pattern explains why Seoul is a key place for an XRP event. Korean traders often drive sharp moves in XRP volume during market cycles.

XRP Seoul 2026 says it will focus on XRP Ledger growth, institutional adoption, and real-world use cases. The official event site says it expects more than 3,000 attendees and over 100 companies.

XRPL activity expands in Korea

Ripple’s work in Korea goes beyond token trading. In May, Ripple Custody signed a deal with Kyobo Life Insurance to pilot near real-time settlement of tokenized Korean government bonds.

As previously reported, the pilot uses Ripple Custody to hold, transfer, and settle tokenized bonds. The project also explores stablecoin payment rails through RLUSD.

Local XRPL groups are also supporting developer activity. XRPL Korea lists the Korea Financial Innovation Program 2026 as a three-month path for teams building blockchain-based finance products.

That effort gives XRP Seoul a builder angle, not only a market angle. The event will likely give projects a stage to show how they use XRPL for payments, tokenization, custody, and other financial products.

XRP utility remains under debate

Long’s appearance comes as XRP holders continue to question how Ripple’s business growth connects to the token. Recent coverage has tracked Ripple’s moves toward banking, stablecoins, custody, and deeper ties with traditional finance.

A recent analysis of Ripple’s bank strategy said RLUSD may benefit first from a trust charter and Fed master account path. Another SWIFT strategy report noted that Ripple now appears more focused on working with bank messaging systems than replacing them.

That leaves XRP’s direct role under close review. Some holders want clearer proof that Ripple’s new deals create lasting demand for XRP, not only for Ripple products.

XRP Seoul gives Long a public stage to address that gap. Her comments may help show how Ripple sees XRP, RLUSD, custody, tokenized assets, and Korean market growth fitting into the same plan.

Coinbase CEO Brian Armstrong has responded after Zcash founder Zooko Wilcox criticized the exchange over alleged betting prompts inside the Coinbase app.

Summary

- Coinbase CEO backs user choice but warns high-risk products need careful in-app promotion rules.

- Zooko’s complaint turned Coinbase prediction markets into a debate over vulnerable users and app design.

- Coinbase’s broader product push adds betting-style markets while regulators argue over sports event contracts nationwide.

The exchange chief defended user choice, but said platforms should treat high-risk products with care when serving less experienced users.

Zooko criticizes betting prompts

Zooko said on X that he had spoken with a young and financially vulnerable Coinbase user. He claimed the app had started prompting that user to bet on sports and the price of Bitcoin.

He said the situation made him “ashamed” to be part of the crypto industry. His post quickly turned into a wider debate about how large crypto apps should promote prediction markets and similar products.

The criticism comes as Coinbase expands beyond spot crypto trading. Recent coverage of Coinbase’s pre-IPO perpetual futures described the firm’s push to combine crypto, stocks, prediction markets and futures inside one account.

That wider product strategy gives users more ways to trade. It also raises questions about how trading apps present risk, especially when products look simple inside a mobile interface.

Armstrong says adults should choose

Armstrong replied that he is “pro-freedom” and believes adults should be able to use their money as they choose, as long as they do not harm others. He also said there is no perfect line between investing and gambling.

The Coinbase CEO added that buying early Bitcoin, Zcash or stocks could also be described as gambling by some people. His point was that risk depends on the product, the user and the context.

Still, Armstrong agreed with part of Zooko’s concern. He said it does not feel right to “aggressively promote high-risk products to unsophisticated users.”

He also said there is a difference between making a product available and making it the main focus of an app. That distinction now sits at the center of the debate.

Prediction markets face regulatory pressure

Coinbase’s sports prediction markets page says the products are offered through Coinbase Financial Markets, a registered futures commission merchant. The page also warns that prediction contracts involve high risk and may lead to the loss of the full investment.

Sports event contracts remain a disputed area in the U.S. In related coverage, Kentucky sued Kalshi, Polymarket and partners tied to Coinbase, Robinhood and Webull, saying the products looked like sports wagering under state law.

The CFTC took the opposite view and argued that Kalshi and Polymarket fall under federal oversight as designated contract markets. The dispute now centers on whether sports contracts belong under federal derivatives rules or state gambling laws.

Former CFTC Chair Gary Gensler also weighed in through a court filing, saying sports prediction contracts do not qualify as swaps under U.S. derivatives law. That filing added another layer to the legal debate.

Coinbase weighs access and safety

Armstrong suggested that Coinbase could use clearer disclosures, AI-based financial literacy tools and more personal app settings. He said users could choose whether to enable or disable certain product groups during onboarding.

That approach would let users decide what they see without removing access for everyone. It would also give Coinbase a way to answer concerns about younger or less experienced users seeing betting-style prompts.

The debate shows how fast crypto apps are changing. Platforms no longer offer only coins and tokens. Many now offer event contracts, derivatives and other products that behave more like financial bets.

For Coinbase, the issue is not only whether users can access these markets. The next question is how strongly the app should promote them and what safeguards should appear before users place trades.

SecondFi says it remains on track to recover user assets after a Cardano wallet exploit drained about $2.4 million in ADA.

Summary

- SecondFi says its recovery plan remains on track while engineers test several secure return methods.

- The exploit drained 16 million ADA from 374 addresses through flawed wallet generation software code.

- Users now face fresh scam risks as fake recovery accounts target affected Cardano wallet holders.

The latest update comes as users wait for a wallet check tool and clear steps to move assets safely.

SecondFi says recovery work remains on track

SecondFi said its recovery process is still moving within the estimated two-week timeline. The team said engineers are working on several technical routes at the same time to choose the safest recovery method for affected users.

The project said it plans to release a tool by early next week that will let users check whether their wallet was affected. It also said it will later share a secure process that lets users move assets out of the platform.

SecondFi warned that no recovery step needing user action has started. It told users to leave wallets untouched until official instructions arrive and said it will never ask for private keys, seed phrases, wallet credentials or asset transfers.

The latest notice followed another warning about rising scam activity. SecondFi said fake accounts and impersonators have been targeting users after the exploit. It also told users not to deposit more funds into existing SecondFi wallets until further notice.

Exploit drained 16 million ADA from 374 addresses

The case began after attackers drained about 16 million ADA from 374 addresses between June 21 and June 23. The value stood near $2.4 million at the time of the reported theft.

SecondFi has linked the issue to its own Cardano wallet generation software. As crypto.news reported, the project said the problem was limited to its native Cardano web wallet generation software and that affected services had been paused.

EMURGO CEO Phillip Pon later said the company had completed a forensic review, checked wallet balances and found what he called a “clear recovery solution.” The company expects one week to build the recovery system and another week to test it before returns begin.

SecondFi also moved about 129 million ADA to an independent third-party custodian as an emergency measure. The company said it took that step to keep more assets away from attackers while it reviewed the breach.

Outside report questions wallet code

A report from Tibane Labs gave a more detailed account of the possible technical fault. The firm said the breach came from an unaudited third-party SDK that replaced EMURGO’s audited signing code on June 8.

Security researcher Taylor Monahan also criticized the wallet code, saying SecondFi “rolled their own crypto.” The comment added pressure on the project because Yoroi, now SecondFi, had served Cardano users for years before the rebrand.

The full cause still needs an official technical report from EMURGO or SecondFi. Until then, users only have public updates, outside analysis and the project’s recovery notices to follow.

Users wait for wallet checker and safe exit steps

SecondFi’s next key step is the wallet check mechanism expected by early next week. That tool should help users know whether they are part of the affected group before any recovery action begins.

The project has asked users to use only official channels and support tickets. That warning matters because wallet hacks often attract fake recovery links, phishing forms and accounts asking for seed phrases.

For now, affected users should not sign new transactions or move assets without official guidance. SecondFi says the recovery depends on the current state of compromised wallets, so early action may create more risk.

The case now tests whether SecondFi can return funds safely while explaining what failed. It also adds fresh concern for Cardano users as ADA trades near multi-year lows and wallet security remains under review.

Base has explained why its mainnet stopped producing blocks twice in two days.

Summary

- Base’s latest postmortem shows one sequencer bug caused two mainnet halts within two straight days.

- Funds stayed safe, but transaction queues overflowed as Base stopped producing new L2 blocks temporarily.

- The team plans stronger fuzz tests, load tests, monitoring, and recovery tools after the outage.

The Coinbase-backed Ethereum layer-2 network said both outages came from the same bug in its sequencer block-building logic.

The first outage began on June 25 and lasted about 116 minutes. The second began on June 26 and lasted about 20 minutes. Base said funds stayed safe during both incidents.

Sequencer bug stopped block production

In its official postmortem, Base said an invalid transaction failed during execution, as expected. The issue came after that failure, when stale journal state remained inside the block builder.

That stale state included accounts and storage slots touched by the failed transaction. When a valid transaction came next, the system used the wrong journal state and charged gas incorrectly.

This created a block with an invalid state transition. Other nodes could not accept the block, so the chain stopped producing new L2 blocks.

“The integrity of the chain was not compromised and all funds on Base were safe,” Base said.

The team added that block production resumed safely after mitigation.

Transactions queued during the halt

During the outages, users could not get new transactions included onchain. Base said transactions queued in the mempool while the chain waited for block production to recover.

The transaction pool later grew beyond what it could store. As a result, new eth_sendRawTransaction requests returned errors during the outage window.

The halt also affected sequencer and validator progress. Base said these nodes could not move beyond the invalid block until sequencing returned.

As previously reported, Base first flagged unhealthy block production on June 25 before engineers isolated a consensus problem tied to an invalid block.

Patch fixed stale state issue

Base said it fixed the main bug by applying a sequencer patch. The patch ensures journal state updates properly during execution after a failed transaction.

The team also found a second issue during recovery. Base said mitigation took longer because a race condition in the engine reset feature stopped sequencers from catching up after restart.

That second issue helped explain why the incident returned the next day. Base said the problem affected sequencers, not validator nodes, but it still slowed recovery.

The Base status page showed sequencing resumed on June 25. It also told ecosystem node operators to restart Base nodes if they were still stuck.

Testing and recovery changes planned

Base said it will strengthen protocol fuzz testing and load testing. These methods help teams find strange transaction patterns that may expose hidden bugs.

The team also plans better monitoring and operational checks. It said these changes should help engineers detect similar problems earlier and respond faster.

Base also wants to add graceful recovery to base-consensus. That change would make it easier for validator nodes to continue syncing after similar failures.

The outage came during a busy week for the network. Base also moved forward with its Beryl upgrade, which adds the B20 token standard and cuts the standard Base-to-Ethereum withdrawal period from seven days to five days.

The incident gives developers and users a clearer view of the weak point. Base has now named the bug, released a patch, and listed the tests it plans to improve.

Taiko says it is ready to bring its Ethereum layer-2 network back online after a June 21 security breach.

Summary

- Taiko says the attack path is closed after outside experts reviewed its latest security fixes.

- The restart plan will restore chain activity before reopening the bridge under withdrawal quotas.

- Recent bridge attacks show why projects now face close scrutiny over proof validation controls.

The project says the attack path is now closed, outside security experts have reviewed the fixes, and users will not lose funds.

The update marks a shift from emergency response to staged recovery. Taiko plans to restore the chain, back the bridge assets, reopen network activity and then unpause bridge operations under limits.

Taiko says attack path is closed

Taiko said the June 21 attack path has been closed after a review by independent security experts. The team said it now has a staged plan to restore the chain while protecting user funds and network stability.

The project said the first step will deploy the fixes and confirm the chain’s finalized state. Taiko also said the review must confirm there are no forged checkpoints or attacker claims still reachable.

The update follows an earlier warning after Taiko confirmed a compromise of its chain-state verification mechanism. As previously reported, the project had urged users to withdraw bridge funds and asked exchanges to pause TAIKO deposits while the team contained the issue.

Blockaid had linked the attack to flawed source-signal proof checks. The security firm said crafted message proofs were accepted on Ethereum without matching valid events on Taiko, allowing unauthorized releases from the ERC20 Vault.

Bridge backing comes before full access

Taiko said the second step will replenish the bridge so every L2 asset is backed 1:1. The team said users will be able to verify the backing on-chain.

This step matters because bridge users rely on the claim that assets on the L2 match assets held or locked elsewhere. If backing becomes weak after an exploit, users may lose trust in wrapped or bridged balances.

Taiko said the Security Council will handle key restart actions. The council will also submit the proposal that unpauses the bridge once the chain finalizes properly and the network remains stable.

The team said it will reopen the bridge with conservative withdrawal quotas. Taiko said it does not expect the limits to stop users from moving assets, but it will use them as an extra safety guard.

Network activity returns in stages

After the fixes and bridge backing steps, Taiko plans to bring network functions back online. Transfers, swaps and trading on L2 will return before the bridge fully opens.

That order gives the team time to watch the chain under normal activity before allowing free movement to and from the bridge. It also lowers the risk of a rushed restart after a security breach.

Taiko said, “No user will lose funds.” The team also warned users that there is no claim site and that the project will never contact users first through direct messages.

That warning targets phishing risks that often follow crypto exploits. Fake recovery links, support accounts and claim pages can lead users into signing harmful transactions or exposing wallet details.

Bridge security remains under pressure

The Taiko breach adds to a series of recent bridge security failures. A Verus Protocol bridge exploit drained more than $11.5 million after attackers used forged cross-chain transfer messages.

Axelar also disabled Secret Network bridge routes after a $4.7 million exploit. Aztec Connect later lost about $2.1 million after an old contract suffered a verification mismatch.

A separate report said cross-chain bridge exploits caused $28.6 million in May losses, or about 42% of the monthly total. That figure shows why bridge proof checks and recovery plans now face close review.

Taiko’s next test is execution. The project must restore activity, prove 1:1 backing, reopen withdrawals safely and keep users away from scam recovery channels.

Grayscale’s research head Zach Pandl says he expects Strategy (the publicly listed corporate Bitcoin holder) will likely have to raise the dividend rate on its flagship “digital credit” preferred stock, STRC, to meet near-term cash obligations. In an X post on Saturday, Pandl also argued that a Bitcoin sale—rather than dividend hikes—could help restore confidence in Strategy’s capital structure.

Still, Pandl’s own base case is unfavorable for investors focused on STRC’s stability: he projected a 50-basis-point increase that would add roughly $100 million in annual obligations over the next two years. The dispute comes as STRC continues trading far below its $100 par reference level, with Strategy’s broader financing choices now under heightened scrutiny.

Key takeaways

- Zach Pandl said he hopes Strategy sells at least $3 billion in Bitcoin to cover most cash obligations over the next two years, but he expects a STRC dividend increase instead.

- Pandl projected a 50-basis-point rise in STRC’s dividend rate, which he said would add about $100 million in annual obligations over two years.

- Strategy’s preferred dividend burden is about $1.2 billion per year, and STRC has recently traded materially below its $100 par value.

- An SEC 8-K filing shows Strategy bought 520 BTC for $34.9 million between June 15 and June 21, while cash reserves increased by $300 million to $1.4 billion.

- CryptoQuant argued Strategy should pause new Bitcoin purchases and focus on rebuilding cash reserves; Samson Mow countered that STRC has a “self-repairing mechanism” once the stock falls.

Dividend pressures collide with STRC’s discount

Pandl, head of research at Grayscale, said Strategy may need to adjust its approach to satisfy cash requirements tied to STRC. In his view, selling Bitcoin could cover most obligations over the next two years and potentially strengthen confidence in the company’s capital structure.

However, Pandl said he expects the opposite outcome. He predicted a 50-basis-point increase to STRC’s dividend rate—an adjustment he estimated would add approximately $100 million in annual obligations over two years. Pandl added that this scenario “probably does not help market confidence,” highlighting a key tension: even if the dividend is supported, the market may still interpret the change as further proof that cash needs are intensifying.

Strategy’s preferred dividend obligation is cited as approximately $1.2 billion annually, driven primarily by STRC. STRC is designed to trade near its $100 par value, but it has been sliding for weeks; on Friday it dropped as low as $71.25, a 28.75% discount to par. Strategy’s common stock, MSTR, also declined over the same period, closing Friday at $82.31, down 26.86% for the trading week.

What the SEC filing and cash math suggest

Strategy remains the largest publicly listed corporate Bitcoin holder, with its Bitcoin and financing activities closely watched by markets. According to Strategy’s latest 8-K filing with the US Securities and Exchange Commission, the company acquired 520 Bitcoin for $34.9 million between June 15 and June 21.

In the same filing, Strategy increased its US dollar reserve by $300 million to $1.4 billion. That figure implies roughly 14 months of dividend coverage, according to the reporting referenced in the article—down sharply from an earlier “seven-year cushion” that investors had previously pointed to as providing insulation.

CryptoQuant argued in a report released this week that Strategy should stop or pause further Bitcoin purchases and instead prioritize rebuilding cash reserves. The report also noted that cash reserves are down 38% in 2026, framing the current posture as increasingly stretched.

Strategy, for its part, said on Monday that it plans to continue replenishing its cash reserves to support the credit quality of its “digital credit” securities, suggesting the company views reserve maintenance as central to its financing strategy.

Calls to sell Bitcoin vs. “self-repairing” stock mechanics

CryptoQuant further suggested that Strategy does not have a direct obligation to sell Bitcoin to defend STRC’s market price. The analytics firm pointed to alternatives such as raising the dividend yield—an approach that could attract incremental demand while spreading the cash burden through a higher return on STRC for new buyers.

Samson Mow, a prominent Bitcoin advocate, took the opposite tack in an X post on Monday, arguing that STRC has a built-in “self-repairing mechanism.” His thesis is tied to Strategy’s financing behavior: once STRC trades below its $100 reference price, Strategy would halt new ATM (at-the-market) issuance, limiting the supply of new shares. In parallel, a lower stock price mechanically increases the yield for buyers relative to what they pay, which Mow said could draw in fresh demand and gradually pull the price back toward par.

Taken together, the debate frames a broader question for STRC investors: is the market discount primarily a cash-coverage issue that must be resolved with reserve rebuilding or asset sales, or is it a pricing mechanism that can correct without selling Bitcoin? The answer matters because dividend adjustments and cash actions affect not only yield, but also how markets interpret the credit durability of Strategy’s digital credit structure.

Why this dispute matters for investors right now

With STRC trading well below par and Strategy’s dividend burden running at roughly $1.2 billion per year, investor attention is shifting from long-term Bitcoin accumulation narratives to short- and medium-term capital structure credibility. Pandl’s comment that a dividend hike may not restore market confidence underscores why the market reaction to cash actions could be as important as the actions themselves.

Meanwhile, the SEC filing confirms Strategy is still buying Bitcoin while cash reserves are being replenished—an approach that may reassure some investors focused on the company’s operating plans, but also fuels skepticism from analysts who argue that cash reserve strength is slipping.

Readers should watch what Strategy does next with its reserve strategy and whether STRC’s discount narrows or widens alongside any dividend policy expectations. The key uncertainty is whether the company will lean more heavily on cash rebuilding and yield adjustments—or accelerate Bitcoin sales—before the next coverage milestone tightens further.

It almost feels inevitable at this point. It was hard to imagine 11 months ago, even 6 weeks ago, but the current landscape appears mostly dominated by the bears, and the psychological $1.00 level has come into focus.

Remember how XRP stood at $3.65 last July? Even the subsequent rejections and corrections that managed to drive it below $3.00 and eventually $2.00 seemed bad enough, but a breakdown below $1.00 was almost out of the question. However, such a probability is highly anticipated now, with BTC seemingly losing the $60,000 support.

XRP dumped to $1.01 on Thursday when the entire market crashed. The question is, and we asked ChatGPT about it, how low can the token go if that coveted support breaks?

Might Not Stop Soon

The popular AI solution warned that if $1.00 falls cleanly by the end of June or in July, it “may not stop at $0.99.” Instead, a decisively daily close below the round-numbered support will likely turn that level into resistance. If that’s the case, then the first downside target sits between $0.96 and $0.94. Although this could mark the “first wave of damage,” it won’t necessarily mean it’s the bottom.

The actual danger, though, comes if XRP loses $0.94. ChatGPT warned that the asset’s path to $0.90 will be wide open. If panic accelerates, the next precise downside zones are $0.87, $0.82, and $0.78, which align with some popular analysts’ views on the token’s potential bottom.

The worst-case scenario for XRP in July would be a crash to $0.65, ChatGPT said.

“That level matters because it sits far enough below obvious support to flush late buyers, liquidate leveraged longs, and reset sentiment completely. It would represent a 35% collapse from $1.00 and a nearly 40% drop from the current $1.05 area.”

On the Contrary

OpenAI’s solution outlined a different scenario in which the XRP bulls defend the $1.00 support and the broader market’s environment improves, or at least doesn’t deteriorate further. Ripple’s token would need to reclaim the first major resistance levels at $1.08 and $1.10 before it can receive some breathing room, as such a rebound would invalidate the bearish thesis of a plunge below $1.00.

However, until XRP indeed goes beyond $1.10 and closes above it, every bounce will appear less like recovery and “more like another chance for sellers to reload” and push it south to under $1.00 territory.

The post How Low Can XRP Go in July if $1 Support Falls? ChatGPT’s Worrisome Predictions appeared first on CryptoPotato.

Peter Schiff warned that a MicroStrategy collapse would damage Bitcoin far more than the FTX fallout.

The veteran gold advocate argued that Michael Saylor could end up remembered as a bigger villain than Sam Bankman-Fried. Schiff framed Strategy as a far more consequential test case than FTX.

Strategy’s Fall Could Dwarf the FTX Collapse

Schiff made the remarks on X. He said Strategy’s (formerly MicroStrategy) collapse portends consequences for Bitcoin far worse than those of FTX’s fall.

He added that anyone who defended Saylor publicly would have “a lot of explaining to do.”

Still, the comparison carries weight. FTX’s 2022 collapse wiped billions in customer funds and triggered a broad market selloff. Strategy’s exposure is larger and more direct.

The company holds more than 843,000 Bitcoin (BTC), roughly 76% of all BTC on public company balance sheets.

Strategy has faced serious pressure in 2026. Bitcoin price action has been unkind, with BTC trading well off its prior highs. The firm has accumulated roughly $14 billion in unrealized losses.

Strategy’s legal pressure has also intensified. The Rosen Law Firm is now probing whether executives made materially misleading statements across five linked securities.

Saylor Defends the Model

Additionally, Strategy’s preferred stock coverage window has shrunk from over seven years to roughly 14 months. Some analysts now question whether its debt-heavy model can survive a prolonged downturn.

Saylor has pushed back against such concerns. He has argued that liquidation risk does not appear until Bitcoin drops to $8,000. Saylor has pledged to refinance debt rather than sell BTC. Still, that position has not calmed critics who point to narrowing financial buffers.

Other prominent voices have echoed similar doubts. Billionaire Jeremy Grantham has used sharp language to describe Bitcoin as a speculative bubble with no fundamental anchor.

Schiff himself had predicted a death spiral in Strategy’s preferred stock structure months before these latest warnings.

Schiff Dismisses Bitcoin’s Proof-of-Work Argument

Schiff also challenged a claim on CNBC’s Squawk Box that Bitcoin derives value from proof of work. He rejected it as a logical fallacy, arguing that effort alone does not generate value.

He contrasted Bitcoin mining with gold mining. In his view, Bitcoin mining produces nothing tangible. Gold mining, by contrast, yields a physical commodity with direct industrial and commercial applications.

The post MicroStrategy’s Saylor Could Become a Bigger Villain Than FTX’s Sam Bankman-Fried? appeared first on BeInCrypto.

Strategy $12B underwater, STRC cracks: model breaking?

World Cup 2026: What does next Scotland head coach look like as ‘monster job’ awaits?

Make Your Own Loudspeaker From Scratch

-

Sports5 days ago

Sports5 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech6 days ago

Tech6 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics2 days ago

Politics2 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics2 days ago

Politics2 days agoPotential 2028er World Cup attendee leaderboard

-

Business2 days ago

Business2 days agoAsia stock markets slide as tech shares slump

-

Tech3 days ago

Tech3 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World4 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business4 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World1 day ago

Crypto World1 day agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports2 days ago

Sports2 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World2 days ago

Crypto World2 days agoRTX holders must register wallets before token distribution begins

-

Crypto World2 days ago

Crypto World2 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Sports3 days ago

Sports3 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech7 days ago

Tech7 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World2 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

-

Crypto World3 days ago

Crypto World3 days agoStrategy (MSTR) has a 10-month cash runway for dividends, but retail investors are losing faith

-

Crypto World2 days ago

Crypto World2 days agoAAVE price tests 9-month trendline after 17% rebound as breakout hopes build

You must be logged in to post a comment Login