Crypto World

Tokenization is becoming the financing layer for AI and robotics, Framework bets with $400 million fund

Traditional securitization markets struggle to package individual servers or computing equipment into investable products, Anderson said. Stablecoins — with more than $300 billion circulating onchain — create a new source of capital for asset-backed lending.

“We have the capital onchain to finance this industry,” he said.

The same thinking extends to energy. Framework has invested in Daylight, which finances residential solar projects through a distributed energy network, and Uranium Digital, which is building a tokenized marketplace for physical uranium.

A different generation

There’s also a notable shift in the profile of founders building today’s crypto companies, Anderson said.

Rather than anonymous crypto-native developers launching speculative protocols, Anderson said, many founders now come from traditional finance, energy or industrial technology, bringing deep expertise while using blockchain as the underlying financial infrastructure to solve real-world problems.

Framework’s recent investments already reflect that trend. They include TVL Capital, founded by former members of Morgan Stanley’s digital assets team; robotics startup Mecka AI, which supplies training data to frontier AI companies; and Plasma, a blockchain-based banking platform built around stablecoin payments.

The venture firm’s strategy mirrors a broader shift across the digital asset industry. Global banks and asset managers are increasingly using blockchain rails to issue, trade and settle traditional financial assets, while stablecoins are becoming part of cross-border payments and treasury operations as banks and fintechs look to modernize payment rails.

Pi Network lets tens of millions of people “mine” crypto by tapping a button on their phone once a day, with no hardware, no electricity bill, and no drained battery. That sounds too easy to be real mining, and in a sense it is not. Here is what Pi mining actually does, how the Stellar Consensus Protocol underneath it works, and what your daily tap really secures.

Summary

- Pi mining is not computational mining in the Bitcoin sense; it is a daily check-in that distributes PI tokens and feeds a trust graph the network uses to reach agreement.

- Pi runs on a version of the Stellar Consensus Protocol, a Federated Byzantine Agreement system that reaches consensus through overlapping groups of trusted participants instead of energy-intensive proof-of-work.

- Mobile users contribute their trust relationships through Security Circles, while the actual transaction validation runs on computer nodes, not on phones.

- There are four roles, Pioneer, Contributor, Ambassador, and Node, and the daily tap mainly proves you are a real human and keeps your token rewards flowing.

- The model trades the energy cost and hard security guarantees of proof-of-work for accessibility, and it depends on honest trust circles and a node network that is still maturing.

Pi mining is the process by which Pi Network distributes its PI tokens to users who confirm their participation through a mobile app and contribute trust relationships to the network, rather than by solving the energy-intensive computational puzzles that power Bitcoin mining. That distinction is the single most important thing to understand about Pi, because the word “mining” carries heavy baggage from Bitcoin, where it means racing thousands of specialized machines to solve cryptographic problems and consuming enormous amounts of electricity in the process. Pi uses the same word for something almost entirely different. A Pi user opens an app once every 24 hours, taps a button, and is credited with newly minted PI.

No puzzle is solved, no hardware is strained, and no meaningful electricity is consumed. This has made Pi one of the most-downloaded crypto apps in the world, with tens of millions of users, and also one of the most debated, because the obvious question is how something so effortless can be called mining at all, and what, if anything, the daily tap actually accomplishes. The answer lies in the consensus mechanism Pi is built on, a system called the Stellar Consensus Protocol, and in a reframing of what “mining” means. In Bitcoin, miners contribute energy and computation to secure the ledger, and they are rewarded for it; in Pi, the contribution is different.

Users supply trust relationships, vouching for people they know, and those relationships aggregate into a structure the network uses to agree on which transactions are valid. This guide explains how that works from the ground up. It covers why Pi rejected proof-of-work in the first place, how the Stellar Consensus Protocol reaches agreement without energy-intensive competition, what Security Circles are and how they feed the network, the four roles a participant can play, what the daily tap genuinely does as opposed to what users often assume, a worked example of how one person’s activity flows into consensus, why the mining rate falls over time, and the criticisms and limits that any honest account has to include. By the end you will understand both the clever idea at the heart of Pi and the real questions that surround it.

What Pi mining actually is

Begin by stripping the word “mining” of its Bitcoin associations, because they cause most of the confusion. In Bitcoin, mining is the work of validating transactions and securing the ledger by solving cryptographic puzzles, and the energy spent doing it is what makes the network hard to attack. Pi mining is not that. When a Pi user taps the lightning button in the app, the phone does not solve anything, does not validate transactions, and does not run any heavy computation.

What the tap does is twofold: it signals that the user is a real, active human participating in the network, and it keeps that user eligible to receive newly distributed PI tokens. In Pi’s own framing, mining is the act of making a contribution to the consensus algorithm in order to secure the ledger, in exchange for rewards, but the contribution a mobile user makes is not energy. It is trust. That is why Pi mining is better understood as a combination of two things: a distribution mechanism and a trust-gathering mechanism.

As a distribution mechanism, it is the way PI tokens are handed out fairly to a large population without requiring anyone to buy expensive equipment, which is the project’s central pitch of accessibility. As a trust-gathering mechanism, the daily check-in and the connections a user makes feed into the network’s way of telling real participants apart from bots, which matters because a system that gives away tokens to anyone who taps a button needs some defense against people creating thousands of fake accounts to farm rewards. The daily tap, and especially the trust relationships a user builds, serve that defense. This is why Pi places so much emphasis on identity verification and on the social connections between users: the whole model rests on being able to distinguish genuine humans from fake ones, and the “mining” activity is partly how it gathers the raw material to do that.

Calling it mining is a marketing choice that borrows Bitcoin’s vocabulary, but mechanically it is closer to a daily proof-of-participation than to anything involving computation. For readers comparing the two models, the model Pi rejected is proof-of-work, where miners expend computation and electricity to secure the chain. Pi’s design replaces that energy cost with a trust-based participation model. The tradeoff is accessibility on one side and a different set of security assumptions on the other.

Why Pi does not use proof-of-work

To understand why Pi works the way it does, you have to understand what it is reacting against. Bitcoin and similar cryptocurrencies use a consensus mechanism called proof-of-work, in which participants called miners compete to solve a difficult mathematical puzzle, and the first to solve it gets to add the next block of transactions and earn a reward. Proof-of-work is genuinely secure and has protected Bitcoin for over a decade, but it has two consequences that Pi’s founders saw as barriers. The first is energy: the global competition to solve puzzles consumes vast amounts of electricity, which is both an environmental concern and a cost.

The second is access: because the competition rewards raw computing power, serious mining requires specialized, expensive hardware and cheap electricity, which puts it out of reach of ordinary people and concentrates it among well-resourced operators. Pi Network was founded by two Stanford researchers, Nicolas Kokkalis and Chengdiao Fan, with the explicit goal of making cryptocurrency accessible to anyone with a smartphone, and proof-of-work was incompatible with that goal. A system that demands costly hardware and large electricity bills cannot, by design, be opened to billions of ordinary phone users. So Pi needed a fundamentally different way of reaching consensus, one that did not depend on burning energy or owning powerful machines, while still allowing the network to agree on a single, valid history of transactions without a central authority in charge.

That requirement led the project to a different family of consensus mechanisms, one built not on computational competition but on trust between participants. The choice it landed on was the Stellar Consensus Protocol, and understanding it is the key to understanding everything Pi does, because it is what allows a phone tap to stand in for the energy a Bitcoin miner would otherwise spend. Pi’s own explanation of mobile mining also frames the design this way, saying its consensus algorithm is adapted from SCP and Federated Byzantine Agreement rather than proof-of-work. The shift from work to trust is the core design decision behind Pi mining.

The Stellar Consensus Protocol, explained

The Stellar Consensus Protocol, usually shortened to SCP, is a way for a decentralized network to agree on the state of a shared ledger without proof-of-work, and it was created by David Mazières, a computer scientist associated with the Stellar blockchain. Its underlying model is called Federated Byzantine Agreement, and the core idea is a genuine departure from how Bitcoin works. Instead of every participant competing, or relying on a fixed, predetermined set of validators chosen by a central authority, each participant in an SCP network decides for itself which other participants it trusts. The set of validators that a given participant chooses to trust is called its quorum slice.

Crucially, no central body assigns these trust relationships; each node selects its own, which is what makes the system both open and decentralized. Consensus then emerges from the overlap of these individual trust choices. When enough of the participants that a node trusts, and enough of the participants they in turn trust, all agree on a transaction or a block, that agreement propagates across the network until a global decision forms. In plainer terms, nodes reach agreement by exchanging messages and aligning with the peers they trust, and because trust relationships overlap and interlock across the whole network, a decision that begins locally spreads until the entire system converges on it.

There is no puzzle to solve and no energy to burn; the security comes from the structure of overlapping trust rather than from computational work. This is why the Stellar Consensus Protocol can run on modest hardware and reach agreement quickly with low energy use, which is exactly the property Pi needed. The protocol has well-studied properties of open membership, flexible trust, and fast, low-bandwidth messaging, and it is a real, respected approach to consensus, not something Pi invented. What Pi did was adapt SCP and layer on top of it a way to gather the trust relationships from a mass of ordinary mobile users, which is where Security Circles come in.

Security Circles and the global trust graph

The bridge between millions of phone users and the Stellar Consensus Protocol is a feature called the Security Circle. Each Pi user is encouraged to build a Security Circle by adding a small number of people, typically three to five, whom they personally know and trust. This is a deliberately human act: you are vouching for specific individuals, asserting that they are real people you have reason to trust. On its own, one person’s Security Circle is a tiny thing, a handful of trust links.

But Pi’s design aggregates every user’s Security Circle into a single, enormous structure called the global trust graph, a map of who trusts whom across the entire network of tens of millions of users. This global trust graph is what feeds Pi’s consensus mechanism, and it is the mobile user’s actual contribution. Where a Bitcoin miner contributes energy, a Pi mobile user contributes trust relationships and the active, daily confirmation of them. The individual Security Circles become the raw material from which the network builds its quorum slices, the overlapping trust sets that the Stellar Consensus Protocol uses to reach agreement.

The graph also serves a defensive purpose that is central to Pi’s whole proposition. Because the network distributes tokens to participants, it is a tempting target for people who would create armies of fake accounts to harvest rewards, an attack known as a Sybil attack. The trust graph is Pi’s main defense: if real humans only add other real humans they know to their circles, then fake accounts struggle to embed themselves in the web of genuine trust, and the network can prioritize the accounts that sit within dense, authentic trust relationships over isolated or suspicious ones. This is why the social dimension of Pi is not incidental but foundational, and why Pi’s identity-based design belongs in the broader debate about proving real humans in crypto.

The security of the whole system is meant to rest on the authenticity of the trust relationships that ordinary users build, which is also one of the model’s most debated features. If users build careful circles with people they genuinely know, the graph can become a useful Sybil-resistance layer. If users add strangers just to boost earnings, the quality of the graph weakens. That tension is central to understanding both Pi’s accessibility and its open questions.

The four roles: Pioneer, Contributor, Ambassador, and Node

Pi organizes participation into four roles, and understanding them clarifies who does what in the network. The most basic role is the Pioneer, which is simply a user who opens the app once every 24 hours and taps the button to confirm they are a real, active human and not a bot. Pioneers are the foundation of the user base, and the daily check-in is the minimum act of participation that keeps a user earning. The Pioneer role, on its own, does not validate transactions or secure the ledger in any direct technical sense; it confirms presence and keeps the rewards flowing.

The second role is the Contributor, which is a user who actively builds a Security Circle by adding trusted people. This is the role through which a user supplies the trust relationships that feed the global trust graph, so Contributors are the ones doing the work that actually matters for the consensus mechanism, even though that work consists of nothing more technical than choosing which people to vouch for. The third role is the Ambassador, a user who grows the network by referring new members, typically rewarded with a boost to their earning rate for doing so. Ambassadors expand the network’s reach, though, as critics point out, referral-based growth is also the feature that draws comparisons to multi-level marketing.

The fourth and most technically significant role is the Node. Node operators run Pi’s node software on a computer, not a phone, and it is these computer nodes that perform the heavy lifting of actually running the consensus algorithm and validating transactions, using the trust graph that all the mobile users have collectively built. The four roles together describe a division of labor: Pioneers prove they are real and keep earning, Contributors supply trust, Ambassadors grow the network, and Nodes do the actual computational work of reaching consensus. Recognizing that the validation happens at the Node level, not on phones, is essential to understanding what mobile “mining” really is.

What the daily tap really does

Here is the honest core of how Pi mining works, the part that promotional descriptions tend to blur. When you tap the button each day as a Pioneer, you are not validating transactions, you are not running the consensus algorithm, and you are not securing the ledger in the way a Bitcoin miner secures Bitcoin. What you are doing is two specific things. First, you are confirming that you are a real human who is actively present, which keeps your account in good standing and keeps you eligible to receive PI.

Second, through your Security Circle and your ongoing confirmation of those trust links, you are contributing to the global trust graph that the network’s computer nodes use to reach consensus. Your phone is a source of trust data, not a validator. The crucial point, in Pi’s own words, is that the heavy lifting of running the consensus algorithm based on the trust graph still falls to computer nodes. The mobile phones create and confirm the trust relationships; the nodes use those relationships to do the actual work of validating transactions and securing the ledger.

So when a Pi user says they are “mining,” what is really happening is that they are feeding the security model with trust and keeping their reward stream active, while the computational securing of the network happens elsewhere, on the node layer. This is not a criticism so much as a clarification, because it explains both why Pi mining can be so effortless and why it is so different from what most people picture when they hear the word mining. The effortlessness is real because the user truly is not doing computational work. The contribution is real too, but it is a contribution of trust and presence, not of energy or computation.

Understanding this distinction is the difference between thinking you are personally securing a blockchain with your phone and understanding that you are providing one input, trust, into a system whose actual validation happens on computers run by node operators. That is also why “mining” in Pi should not be evaluated with the same checklist as Bitcoin mining. The daily tap is closer to proof of participation and identity maintenance than to proof-of-work. The right question is not whether the phone solves blocks, because it does not, but whether the trust graph and node layer mature enough to secure a real network.

A worked example: how one Pioneer’s activity flows into consensus

To make this concrete, follow a single user through a day. Imagine a Pioneer named Maria who has had the Pi app for a few months. Each morning she opens the app and taps the lightning button, which starts a 24-hour earning cycle and credits her with PI at her current rate. That tap, on its own, simply tells the network that Maria is a real, active human and keeps her rewards flowing.

So far, nothing about the ledger has changed; Maria has only confirmed her presence. The part that feeds the network is Maria’s Security Circle. Some weeks ago, Maria added five people she knows personally, her sister, two close friends, a coworker, and a former classmate, to her Security Circle, vouching for each as a real, trustworthy person. Those five trust links are Maria’s contribution to the global trust graph.

When the network’s computer nodes run the Stellar Consensus Protocol to agree on the next set of transactions, they draw on the vast web of trust relationships that Maria and tens of millions of other users have built. Maria’s five links are a tiny but real part of the overlapping trust sets, the quorum slices, that the nodes use to reach agreement, and because Maria’s circle connects to her contacts’ circles, which connect to theirs, her small contribution is woven into the larger structure that lets the whole network converge on a shared, valid history. If Maria also chose to run node software on her computer, she would move into the Node role and take part directly in the validation work; as a Pioneer with a Security Circle, she instead supplies trust that the nodes consume. The reward she receives for her daily tap is, in effect, payment for her presence and her trust contribution.

This is the full loop of Pi mining at the level of one person: tap to prove presence and earn, build a circle to contribute trust, and let the node layer turn that aggregated trust into consensus. The example also shows why Pi’s model is both accessible and contested. Maria did not need an ASIC miner, a warehouse, or a power contract, which is the whole point. But the quality of her contribution depends on the authenticity of her trust choices, and the strength of the network depends on millions of similar choices being honest.

The mining rate and why it falls

A practical feature that surprises many new users is that the rate at which they earn PI is not fixed; it falls over time, by design. Pi built in a declining emission schedule loosely modeled on the way Bitcoin’s block reward halves over time, intended to create scarcity as the network grows. In Pi’s history, the base mining rate has dropped sharply at population milestones: it halved as the network crossed 1 million users, halved again at 10 million, and has continued to decline as the user base has grown into the tens of millions. A Pioneer today earns a small fraction of what early users earned for the same daily tap.

The logic is that rewarding early participants more generously bootstraps the network, while tapering rewards as it grows prevents the supply from expanding too fast and preserves some scarcity. On top of the declining base rate, a user’s actual earnings are shaped by multipliers tied to the roles described earlier. Building a Security Circle increases your rate, referring new users as an Ambassador adds a boost, engaging with apps in the ecosystem can contribute, and some users choose to lock up their PI for a period in exchange for a higher rate. So two users tapping on the same day can earn quite different amounts depending on how much they have contributed to the network’s trust and growth.

All of this sits against the backdrop of Pi’s very large maximum supply, on the order of 100 billion tokens, of which only a portion is currently in circulation. That large supply, combined with the way new tokens enter the market as users complete verification and move their balances onto the live network, is a structural factor that weighs on the token’s price, a dynamic worth keeping in mind alongside the mechanics of how the mining itself works. For readers following the market side, how mined Pi reaches the market explains why unlocks, migration, and supply absorption matter after tokens become transferable. The declining rate is, in part, the project’s attempt to manage that supply, rewarding participation while trying not to flood the market.

Risks, criticisms, and what mining really secures

An honest explanation of Pi mining has to address the genuine criticisms and limits, because they go to the heart of what the model is and is not. The most fundamental point, already noted, is that mobile “mining” does not secure the ledger the way proof-of-work does. The daily tap proves presence and feeds the trust graph, but the actual validation runs on computer nodes, and the security of the whole system rests on the trust graph being authentic and on the node network being sufficiently decentralized and robust. That leads directly to the central criticism: the trust-based security model is debated.

Its strength depends on real humans adding only other real humans to their circles, and skeptics question how reliably that holds at a scale of tens of millions of users, and how resistant the system truly is to manipulation if trust links can be gamed. Centralization is another recurring concern. For much of its life Pi has operated with significant control held by its founding team and foundation, including over key aspects of the network and the pace of its decentralization, which sits uneasily with the decentralized ideal that the consensus model is meant to embody. The node network that does the real validation is still maturing, and the degree to which it is truly decentralized is a fair question.

Critics also point to the referral mechanics, the Ambassador role and its rewards for recruiting new users, as resembling the structure of multi-level marketing, where growth is driven by recruitment, and they note that the long period during which Pi could be mined but not traded or used invited skepticism about whether the tokens would ever have real value. There are technical limits too, including questions about the network’s transaction throughput and its capacity to serve a user base of its claimed size. None of this means Pi is necessarily a scam, a charge its supporters reject by pointing to its real technical development and large verified community, but it does mean a clear-eyed user should understand exactly what their daily tap does and does not accomplish. You are not single-handedly securing a blockchain with your phone.

You are providing trust and presence to a system whose validation happens on a node network, in exchange for tokens whose ultimate value depends on the project delivering real utility and decentralization over time. That is the honest picture of what Pi mining secures, and what it does not. For price-focused readers, where the mined token trades is a separate question from how the mining mechanism works. For consensus comparisons, another way networks reach consensus shows how other systems use locked capital rather than proof-of-work or Pi’s trust graph.

Frequently asked questions

Is Pi mining real cryptocurrency mining?

Not in the way Bitcoin mining is. Bitcoin mining involves solving cryptographic puzzles with specialized hardware, consuming large amounts of energy, to validate transactions and secure the ledger. Pi mining involves tapping a button in an app once a day, which solves nothing and consumes no meaningful energy. What the tap does is prove you are a real, active human and keep you eligible for PI rewards, while the trust relationships you build feed the network’s consensus mechanism.

The actual transaction validation runs on computer nodes, not phones. So Pi uses the word mining, but mechanically it is closer to a daily proof-of-participation than to computational mining.

What is the Stellar Consensus Protocol?

The Stellar Consensus Protocol, or SCP, is a way for a decentralized network to agree on a shared ledger without proof-of-work, created by computer scientist David Mazières. It uses a model called Federated Byzantine Agreement, in which each participant chooses for itself which other participants it trusts, forming what is called a quorum slice. Consensus emerges when these overlapping trust choices align across the network, so a decision spreads until the whole system converges on it. Because security comes from the structure of overlapping trust rather than from computational work, SCP uses little energy and can run on modest hardware, which is why Pi adapted it for mobile use.

What does tapping the button actually do?

Two things. First, it confirms you are a real human who is actively present, which keeps your account in good standing and your PI rewards flowing. Second, combined with your Security Circle, it contributes to the global trust graph that the network’s computer nodes use to reach consensus. What it does not do is validate transactions or secure the ledger directly; your phone is a source of trust data, not a validator.

In Pi’s own description, the heavy lifting of running the consensus algorithm falls to computer nodes, while mobile users supply the trust relationships those nodes rely on. So the tap is about presence and trust, not computation.

What is a Security Circle?

A Security Circle is a small group of people, typically three to five, whom a Pi user personally knows and trusts and adds to their account, vouching for them as real, trustworthy individuals. On its own a Security Circle is just a few trust links, but Pi aggregates every user’s circle into a single global trust graph spanning the whole network. That graph is the mobile user’s real contribution: it feeds the consensus mechanism and serves as the network’s main defense against fake accounts, since genuine humans adding only other genuine humans makes it harder for bot armies to embed themselves in the web of authentic trust. The social authenticity of these circles is foundational to Pi’s security model.

Why does my Pi mining rate keep dropping?

By design. Pi built in a declining emission schedule, loosely modeled on Bitcoin’s halving, to create scarcity as the network grows. The base rate has halved at population milestones, dropping as the network passed 1 million and then 10 million users, and continuing to fall as it reached the tens of millions, so a Pioneer today earns a fraction of what early users earned. Your actual earnings also depend on multipliers from building a Security Circle, referring users, engaging with the ecosystem, and optional lockups.

The declining rate is partly an attempt to manage Pi’s very large maximum supply of around 100 billion tokens, rewarding early participation while trying to limit how fast new supply enters.

Is Pi Network legitimate, or is it a scam?

It is truly debated, and this guide does not resolve it. Supporters point to real technical development, the adaptation of a respected consensus protocol, and a large verified community as evidence that Pi is a serious project. Critics raise concerns about centralized control held by the founding team, the maturity and true decentralization of the node network, referral mechanics that resemble multi-level marketing, the long period when Pi could be mined but not used, and questions about the network’s technical capacity. A clear-eyed view is that Pi is a real project with real open questions, and that any user should understand exactly what their daily tap accomplishes and treat the token’s ultimate value as uncertain instead of assured.

This article is educational information, not financial advice. Details of Pi Network’s mechanics, mining rate, supply, and development reflect information available as of June 28, 2026, and can change. Pi Network is a debated project, and its token’s value and future remain uncertain. Verify current details from official sources and consider your own circumstances before participating or making any decision.

The past several months have not been kind to XRP. After it marked a new all-time high in mid-July 2025, it has been mostly downhill, losing over 70% of its value, dumping toward $1.00, being surpassed by BNB and USDC in terms of market cap, and registering six consecutive months in the red at one point.

Amid all of these adverse developments, some analysts have turned highly bearish on the asset. While the dominant belief is that XRP has reached its most crucial moment during this cycle, some, such as Ali Martinez, pointed to potential drops to the next crucial support levels at $0.80, $0.62, or $0.51 if the $1.00 floor gives in.

Glassnode warned that XRP token holders continue to realize more losses than profits, indicating intensifying selling pressure even among investors in the red. Even ChatGPT made some worrying predictions if the asset indeed flips $1.00 from support into resistance soon. But maybe such low sentiment is what is needed for XRP to turn things around.

Run Up Instead?

Paradoxically, history shows that the markets rarely reward such consensus. In fact, Warren Buffett has said it best, “Be fearful when others are greedy, and be greedy when others are fearful.”

Extreme pessimism has frequently appeared near important turning points across the crypto market. BTC, ETH, and XRP have all experienced periods where sentiment collapsed and remained there for a while before major recoveries began. This is generally possible when weak hands exited, and long-term investors quietly accumulated.

For XRP, this accumulation appears to be coming from ETF investors, as the funds tracking its performance have seen a green-only streak of eight consecutive weeks, while the BTC and ETH ETFs have bled out heavily.

The recent sell-off also pushed several on-chain and technical metrics into historically oversold territory. Some analysts argue that XRP may be approaching a zone where risk-reward begins to improve, even if short-term volatility persists.

History is indeed on XRP’s side. Recall that the asset’s sentiment had plunged to similar levels in mid-June but skyrocketed by double digits within 24 hours as the analytics company Santiment attributed that rally to the deteriorating investor behavior.

July Agrees

Current data show that XRP is on track to close June with a decline of over 20%, its worst monthly performance since February 2025. Data from CryptoRank suggests that this aligns with previous performances, as June has been a predominantly bearish month for the asset.

On the contrary stands July. XRP has closed each of the past six editions in the green, showing some impressive gains. Five out of the six have seen double-digit price increases, including massive 45%+ pumps in 2020 and 2023. The median gain for July stands at close to 11%.

The post Everyone Expects XRP to Crash Further: Is Ripple About to Surprise the Market? appeared first on CryptoPotato.

SBI Holdings is a financial services group with businesses spanning securities, banking, insurance, asset management and venture investing with a market capitalization of about $11 billion. The Tokyo-based company is one of Japan’s most active traditional-finance participants in digital assets, with stakes and partnerships across crypto trading, liquidity, tokenization, stablecoins and blockchain-based settlement.

Bitbank is one of the country’s largest licensed cryptocurrency exchanges, offering spot trading, custody and other digital-asset services to retail and institutional clients.

Cheaper, quicker to buy

Crypto mergers and acquisitions have remained brisk in 2026 as banks, payments firms and exchanges race to build regulated digital asset businesses rather than develop them in-house.

The industry has recorded 144 deals worth $11.8 billion so far this year, according to data from Architect Partners, with buyers increasingly targeting exchanges, custody providers, data firms and stablecoin infrastructure as regulatory clarity draws more institutional capital into the sector.

According to Payne, the Bitbank acquisition is about more than customer growth. The deal brings a Financial Services Agency-licensed exchange, one of Japan’s deepest altcoin liquidity pools and an institutional custody business, Japan Digital Asset Trust, giving SBI capabilities that would be far more costly and time-consuming to build internally.

The acquisition comes at a pivotal moment for Japan’s crypto industry. Legislation passed by the country’s lower house on June 11 would shift crypto assets under the Financial Instruments and Exchange Act, aligning them with securities regulation. The reforms lower the tax rate on crypto gains to a flat 20% and pave the way for spot bitcoin , ether (ETH) and XRP exchange-traded funds, while simultaneously imposing more stringent capital, custody and disclosure requirements on exchanges.

Mow is not the first to argue that bitcoin’s traditional four-year cycle has changed. After bitcoin climbed to a then-all-time high before the April 2024 halving, several analysts suggested growing institutional demand following the launch of U.S. spot bitcoin ETFs could alter the pattern that has historically followed each halving. Others, however, argued it was too early to conclude the cycle had changed.

$55,000 more likely

Not everyone agrees. Several analysts have recently argued that bitcoin is either close to a market bottom or still has further to fall, although they rely on different indicators and models.

CoinDesk market analyst Omkar Godbole recently wrote that if you were “wondering just how much lower bitcoin is likely to drop, the answer, at least according to one historically accurate contrarian indicator, is not much.”

That indicator is based on bitcoin’s 50-week and 100-week simple moving averages. The 50-week average, representing roughly one year, is very close to dropping below the 100-week line, forming what analysts call a “bear cross.” Historically, similar signals coincided with market bottoms, leading some analysts to see the pattern as bullish.

More recently, Markus Thielen, the founder of 10x Research, said he believes the bottom is more likely at $55,000 and not until somewhere between August and October. Arthur Hayes, the BitMex co-founder, took a more bearish position, saying bitcoin would bottom at around $40,000 within the next six months.

Michael Saylor shared a StrategyTracker chart on X this Sunday showing Strategy holds 847,363 bitcoin valued at $50.88 billion as of June 28, 2026, with 113 purchase events and an average cost basis of $75,653 per BTC.

That chart displays orange bubbles for MSTR’s buys overlaid on bitcoin price history, highlighting aggressive accumulation especially in 2024-2025 with the average purchase price line trending upward.

“We’re gonna need more charts” signals Saylor’s intent for continued bitcoin purchases, generating more data points as Strategy maintains its position as a leading corporate BTC holder.

Last week, Ripple CEO Brad Garlinghouse said he remains bullish on bitcoin but that Saylor’s approach to funding bitcoin purchases has damaged the wider cryptocurrency market, as the preferred stock at the center of Strategy’s model fell to a record low.

Strategy’s (MSTR) stock fell 8% lower Thursday to $86, amid concerns about its ability to meet dividend obligations. However, Saylor’s treasury still has 10 months of dollar reserves available to cover STRC’s dividend obligations. MSTR is currently priced at $82.31 following a further 3.54% drop. STRC hovers around $74.57 after a 1.48% increase on Sunday.

XRP is trading near $1.05 as buyers continue to defend the $1 level after a weak month.

Summary

- XRP trades near $1.05 after falling sharply over the past week and month.

- ETF inflows remain positive while Bitcoin and Ethereum funds continue showing heavy weekly outflows.

- Analysts watch $1 support, rising active addresses, and possible rebound signals toward the $1.30 zone.

The token is down more than 7% over the past week and about 19% over the past 30 days, while its 24-hour range sits between $1.04 and $1.07.

The price action remains weak, but several market signals show that XRP has not lost all support. ETF inflows remain positive, daily active addresses are rising, and some analysts now point to early reversal patterns on the daily chart.

XRP trades near $1 after sharp monthly decline

XRP holds a market rank of #6, with market capitalization near $65.4 billion. Its 24-hour trading volume stands above $1.1 billion, showing that activity remains strong even as price stays near recent lows.

The token remains far below its all-time high of $3.65 from July 2025. It has also fallen more than 50% over the past year and about 49% over the past 200 days, showing that the current weakness is part of a longer downtrend.

A recent XRP price prediction noted that XRP is trading near a 20-month low. The same report said $1 has become the key level to watch, with downside support near $0.85 and $0.70 if that area fails.

That makes the current setup simple. XRP needs to hold $1 to avoid a deeper technical breakdown. A strong move above $1.12 and then $1.27 would be needed before traders can argue that momentum is shifting back toward buyers.

ETF demand stays positive despite weak price

XRP fund flows continue to stand out against Bitcoin and Ethereum. On June 26, XRP ranked first in single-day net inflows at about $15.63 million, while spot Bitcoin ETFs saw about $444.51 million in outflows and Ethereum funds lost about $12.85 million.

The weekly trend also remains positive. XRP spot ETFs have now posted seven straight green weeks, with roughly $144.69 million in net inflows over that stretch, according to SoSoValue data.

This is not the same pattern seen in Bitcoin and Ethereum. Over the same seven-week stretch, Bitcoin ETFs recorded about $7.73 billion in outflows, while Ethereum ETFs lost around $1.18 billion.

A previous fund flow report showed XRP products had already beaten Bitcoin and Ethereum for five straight weeks. Another CLARITY Act analysis said XRP ETFs had drawn roughly $1.44 billion in cumulative inflows through six weeks of buying, even as price remained weak.

That contrast is important for the current XRP price analysis. It suggests that fund demand has not been enough to lift the token yet, but it may be helping to slow deeper losses near $1.

On-chain activity and chart signals improve

Analyst Ali Charts said XRP network activity has risen over the past two weeks. Daily active addresses climbed from about 23,000 on June 14 to nearly 39,500, pointing to higher on-chain participation.

Rising active addresses can show more users interacting with the network. It does not guarantee a price recovery, but it gives traders another data point at a time when price is testing a key support level.

Ali also pointed to two bullish reversal signals on the daily chart. He said the Tom DeMark Sequential indicator printed a “9” buy signal, which can sometimes appear before a short relief rebound lasting one to four daily candles.

He also said the past three daily sessions formed a Morning Star Doji pattern. That pattern is often used by technical traders to identify a local bottom after a downtrend.

If buying volume rises from here, Ali said XRP could move toward $1.30. That level also lines up with earlier resistance areas from recent price action.

A prior XRP technical report said traders were watching $1.20 as a recovery level, with $1.24 and $1.30 as the next zones if buyers pushed through resistance.

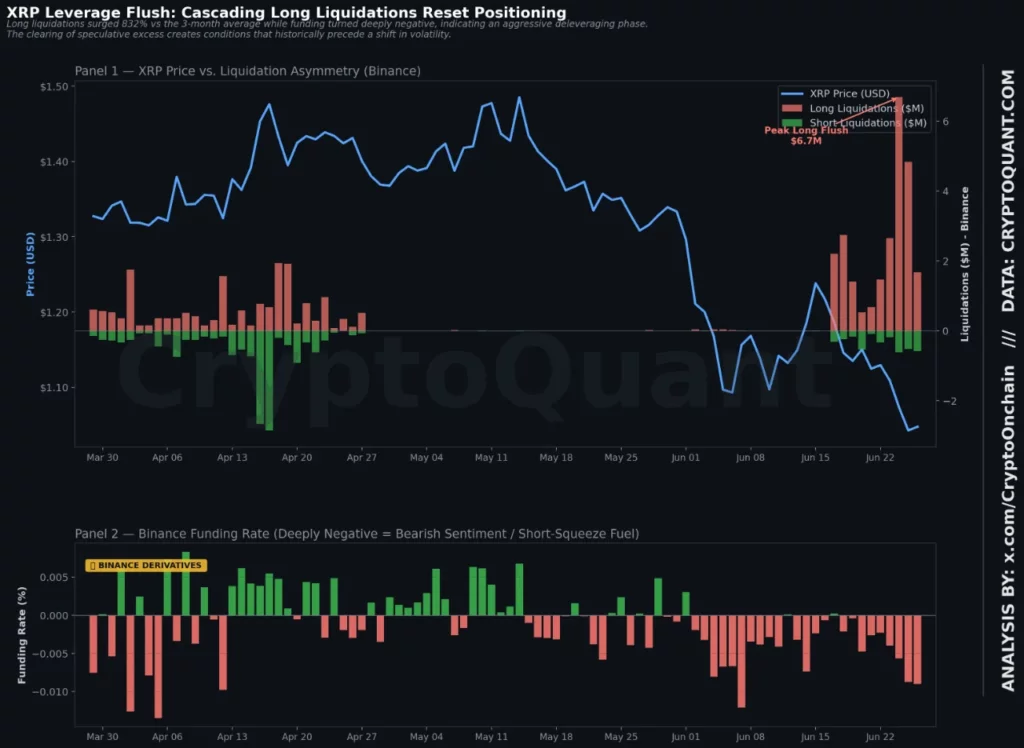

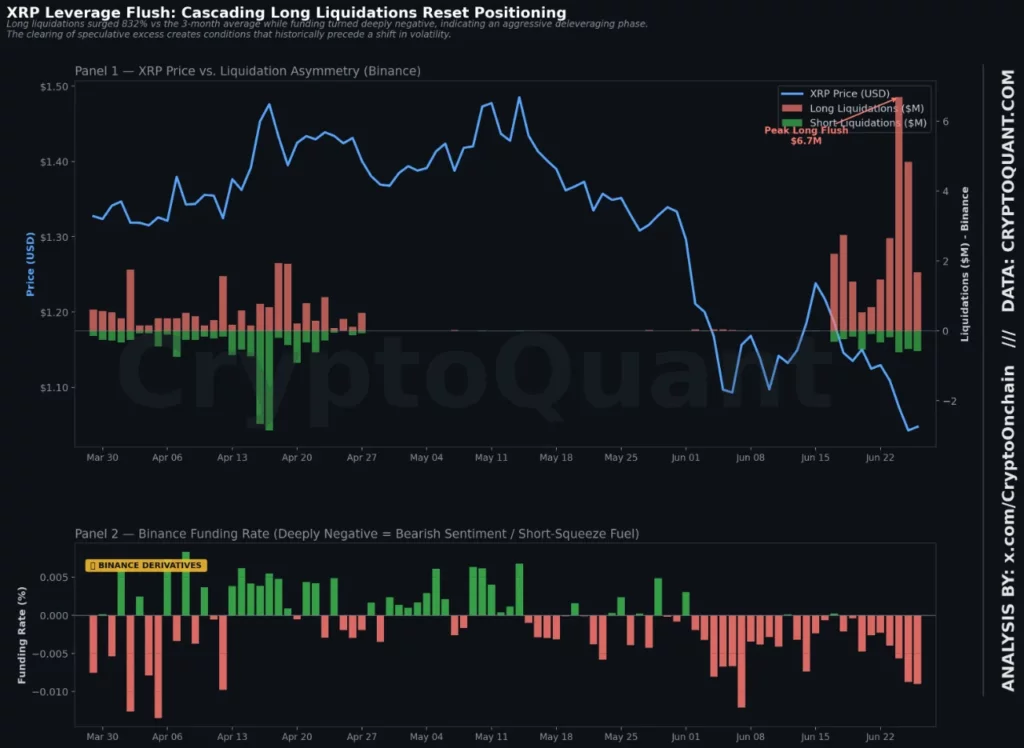

Derivatives reset may shape the next move

Acccording to CryptoOnchain, XRP derivatives have gone through a heavy deleveraging phase. Long liquidations jumped to nearly $3 million over the past week, up more than 800% from the prior month.

Open interest also fell from about $1.18 billion to roughly $1.04 billion. At the same time, funding rates turned deeply negative, showing that traders who were positioned for upside have been forced out.

That type of reset can cut speculative excess from the market. It can also create conditions for a sharp move if short sellers become crowded and spot buyers remain steady.

The spot side looks calmer than futures. Binance reserves were nearly flat over the week, suggesting holders are not rushing to move XRP to exchanges for immediate sale.

The next signal will come from open interest and funding rates. If open interest starts to recover while price holds $1, traders may read it as a healthier reset. If XRP loses $1 with rising volume, the market may shift back toward $0.85 and $0.70 support.

Ripple’s wider ecosystem also remains in focus after RLUSD became available in Japan through SBI VC Trade. The stablecoin launch gives Ripple a new regulated channel in Asia, though XRP’s short-term direction still depends on price action, fund flows, and whether buyers can defend the $1 level.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

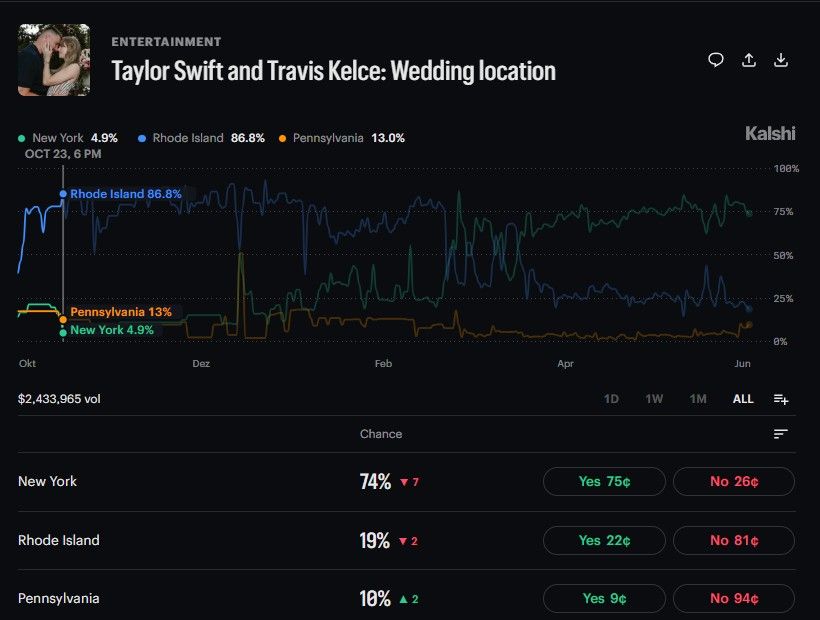

Taylor Swift and Travis Kelce’s unannounced wedding has already generated more than $4 million in trading volume on prediction platform Kalshi, with bettors wagering on the venue, the date, and even the bridesmaids.

According to Kalshi, entertainment trading grew from $43 million in 2024 to over $300 million in 2025. Music markets alone surpassed $400 million in Q1 2026, putting total 2026 entertainment volume on pace for $1 billion.

Location and Timing Drive the Biggest Bets

The location market has drawn $2.26 million in volume, making it Kalshi’s largest Swift-Kelce trading category. New York holds 80% odds, with Rhode Island trailing at 21%. Polymarket narrows the call further, placing Manhattan at 85%.

A street-closure permit filed near Madison Square Garden for July 3 has intensified speculation about the date. Neither Swift nor Kelce appears on the permit.

Kalshi gives 95.5% odds that the wedding will occur this year. Polymarket sets the chance of it occurring before August 31 at 96%. The permit reportedly calls for tenting outside the arena to accommodate between 500 and 999 guests.

New York City will simultaneously host July 4 celebrations and FIFA World Cup matches that weekend.

Separate markets track the wedding party. Jason Kelce leads the odds of being a groomsman at 89%, followed by Patrick Mahomes at 72%.

On the bridesmaid’s side, Abigail Anderson Berard holds 85% odds for maid of honor. Selena Gomez follows at 76%, with Gigi Hadid at 54%. Blake Lively and Brittany Mahomes, meanwhile, have both fallen to 8% odds.

Celebrity Markets Break Records as Kalshi Eyes $40 Billion

The Swift-Kelce surge arrives as prediction markets post record monthly transactions. Monthly active users reached 865,411 in March 2026, up 118% from the prior year. Monthly notional volume hit $23.89 billion, a 1,107% year-over-year increase.

The sector grew from roughly $1.2 billion in monthly volume in April 2025. By March 2026, that figure had exceeded $25 billion. Kalshi is targeting a $40 billion valuation in an ongoing funding round, up from $22 billion a month earlier.

The platform has also expanded through a World Cup prediction partnership, broadening its market categories.

Female Traders Reshape the Prediction Market Audience

Kalshi reports the share of female traders on its platform has doubled over the past year. That shift suggests celebrity-focused markets attract users well beyond the typical trading audience. Research also shows US voters consult prediction markets alongside conventional polling.

A bill seeking to ban prediction markets has circulated in Congress, though it has yet to clear both chambers. Despite that, Kalshi’s reach across sports, politics, and pop culture continues to grow.

The post Swifties Storm Prediction Markets: Over $4 Million Wagered on Taylor Swift’s Wedding appeared first on BeInCrypto.

Whether a token is a security or a commodity decides almost everything about how it can be traded, listed, and held in the U.S. In March 2026 regulators called sixteen major tokens “digital commodities,” but only on interpretive footing a future administration could undo. The CLARITY Act would turn that label into law. Here is what a digital commodity actually is, and how the bill would reclassify crypto.

Summary

- A digital commodity is a crypto asset whose value comes from the workings of a functional blockchain and from supply and demand, not from the expectation of profit from a company’s managerial efforts.

- The distinction matters enormously: a security falls under the securities regulator’s heavy registration and disclosure regime, while a commodity falls under the commodities regulator’s lighter-touch oversight.

- In March 2026 the SEC and CFTC jointly classified sixteen major tokens, including Bitcoin, Ethereum, XRP, and Solana, as digital commodities, but that was an interpretation, not a law, and a future administration could reverse it.

- The CLARITY Act would write the digital-commodity category into federal statute, making the classification durable, and create a maturity test that lets a token move from security to commodity as its network decentralizes.

- Reclassification changes what products can be built, especially exchange-traded funds, how exchanges list assets, how institutions hold them, and how much investor protection applies.

A digital commodity is a crypto asset whose value comes from the workings of its blockchain and from supply and demand, rather than from the promised efforts of a company or team, which is the legal distinction that places it under the lighter-touch oversight of the commodities regulator instead of the heavier hand of the securities regulator. That sentence contains the entire stakes of one of the most consequential questions in crypto: for any given token, is it a security or a commodity. The answer determines which federal agency has authority over it, what financial products can be built around it, how exchanges can list it, whether large institutions can comfortably hold it, and how aggressively the government can act against the people who issue and trade it. For more than a decade, the U.S. had no clear way to answer that question for most tokens, leaving the entire industry in a gray zone, and the fight over how to draw the line, and who gets to draw it, has shaped the regulation of crypto in America more than any other issue.

In 2026 that long-running question reached a turning point on two fronts at once, and understanding both is essential to understanding what a digital commodity is and why it matters. On the regulatory front, the two relevant agencies, the securities regulator and the commodities regulator, took the unprecedented step of jointly declaring sixteen major tokens to be digital commodities, ending years of ambiguity for those specific assets. On the legislative front, Congress has been working on the CLARITY Act, a bill that would take the digital-commodity concept and write it into permanent federal law, with a mechanism for deciding which tokens qualify and how a token can move from one category to another over time. This guide explains what a digital commodity actually is, why the security-versus-commodity distinction decides so much, the test at the heart of classification, what the 2026 regulatory interpretation did and why it was not enough on its own, how the CLARITY Act would reclassify crypto by statute, the clever maturity mechanism that lets a token change categories, what reclassification practically changes, and the real limits and risks that remain.

What a digital commodity actually is

Start with the precise definition, because the legal language is doing specific work. A digital commodity, in the formulation regulators have adopted, is a crypto asset that is intrinsically linked to and derives its value from the programmatic operation of a functional crypto system, as well as from supply and demand dynamics, rather than from the expectation of profits from the essential managerial efforts of others. That is a dense sentence, so it helps to unpack it: the key idea is the source of the asset’s value. A digital commodity is valuable because of how its blockchain works and because of ordinary market forces of supply and demand, not because some company is promising to do work that will make the token go up.

Crucially, regulators have added that a digital commodity does not carry intrinsic economic rights such as generating a passive yield or conveying a claim on the future income, profits, or assets of a business, which is exactly the kind of feature that would make something look like a security. The contrast that makes this concrete is the traditional commodity. Think of oil, wheat, or gold: these are produced by many different parties around the world, not issued by a single company to raise money for itself, and one unit is interchangeable with another, so one barrel of a given grade of oil is worth the same as any other. Their value comes from supply and demand and from their inherent usefulness, not from anyone’s promise of profit.

Regulators have long treated Bitcoin the same way, reasoning that it is produced by many disparate miners around the world, is fungible, and has no central issuer making promises, which makes it commodity-like rather than security-like. The digital-commodity category extends that logic to other tokens whose networks are sufficiently decentralized and functional that no central enterprise is driving their value through promised efforts. A digital commodity, then, is the crypto equivalent of gold or oil instead of the crypto equivalent of a company’s stock. That single distinction is what determines how it is regulated.

Security or commodity: the question that decides everything

To see why this classification carries such weight, you have to understand how differently the two categories are regulated. Securities, which include stocks and bonds, fall under the securities regulator, whose regime is built around investor protection through heavy obligations: companies issuing securities must register their offerings, provide extensive ongoing disclosures, and operate within a tightly controlled system of registered broker-dealers and exchanges, all backed by the threat of enforcement for non-compliance. The logic is that when people invest money expecting profit from someone else’s efforts, they need protection and information, so the law imposes a demanding framework. Commodities, by contrast, fall under the commodities regulator, whose regime is far lighter.

The commodities regulator oversees the derivatives markets for commodities, such as futures and options, and can pursue fraud and manipulation, but it does not impose the same registration-and-disclosure burden on the underlying asset. It also has limited direct authority over spot markets where commodities are bought and sold for immediate delivery, which is why the jurisdictional split codified by the CLARITY Act matters so much. The practical consequences of which bucket a token lands in are enormous, which is why the industry has fought over classification for years. If a token is a security, its issuer faces registration and disclosure requirements, the exchanges listing it face securities-law obligations, and institutions weighing whether to hold it confront the heavier compliance and restrictions that come with securities.

If the same token is a commodity, those burdens largely lift: listing is easier, compliance is lighter, and the path to building products around it, especially exchange-traded funds, becomes far more direct. Classification also determines which regulator writes the rules, who pays which fees, how custody is handled, and how much room institutions have to participate. Calling a token a security or a commodity is not a technicality; it is a decision that shapes whether a project can operate smoothly in the U.S. or faces a wall of regulatory friction. It also influences the token’s accessibility to the institutional capital that can move its price, which is why the definition of a digital commodity, and the process for deciding which tokens qualify, became one of the central battles in crypto policy.

The Howey test and the efforts of others

At the heart of the security-versus-commodity question sits a legal test that has governed it for decades: the Howey test. Derived from a Supreme Court case, the Howey test defines an investment contract, which is a type of security, as an investment of money in a common enterprise with an expectation of profits derived from the efforts of others. That last phrase, the efforts of others, is the crux. If you buy a token primarily because you expect a company or team to do work that will increase its value, the arrangement looks like a security, because your profit depends on their efforts.

If, instead, the token’s value comes from a decentralized network and market forces with no central party whose efforts you are relying on, it looks more like a commodity. The Howey test is why the same token can be treated differently depending on how it is sold and how mature its network is. This is also where one of the most important and confusing features of crypto classification comes from: a token’s status is not necessarily permanent. The Howey analysis depends on facts that can change as a project evolves.

A token might begin its life as a security, sold by a founding team to raise money for a network that does not yet exist, where buyers are clearly relying on the team’s efforts. Over time, if the network becomes genuinely functional and decentralized, with no central team driving its value, the same token can stop looking like a security and start looking like a commodity, because the efforts-of-others element fades away. This transition is the key conceptual move that everything else builds on, and it explains why regulators and lawmakers have struggled to draw clean lines: the line itself moves as a project matures. The 2026 regulatory interpretation adjusted the Howey analysis for crypto by requiring that an issuer affirmatively make representations or promises about its essential managerial efforts for there to be an investment contract, which sharpened the test in a way favorable to treating mature, decentralized tokens as commodities.

The March 2026 interpretation: a label, not a law

In March 2026 the security-versus-commodity question got its most significant answer yet, though an incomplete one. The securities regulator and the commodities regulator, which had spent years disagreeing over jurisdiction, jointly issued a formal interpretation that, for the first time, set out an agreed framework for classifying crypto assets. The interpretation sorted crypto into a taxonomy of categories, most of which are not securities: digital commodities, digital collectibles such as certain non-fungible tokens, digital tools that perform a utility function like membership or access, stablecoins, which sit in their own lane governed by separate stablecoin legislation, and digital securities, the one category that clearly is a security. Within that framework, the agencies named sixteen major tokens as examples of digital commodities, including Bitcoin, Ethereum, Solana, and XRP, alongside others such as Cardano, Litecoin, and even some memecoins, explicitly declaring that these assets are not securities and that their spot trading falls primarily under the commodities regulator.

This was a landmark moment, the first time the two top financial regulators agreed in writing on how to treat these assets, and it brought real clarity to the named tokens. But it carried a critical limitation that defines why the story does not end there. The interpretation is exactly that, an interpretation: a statement of how the agencies read existing law, binding on the agencies themselves in how they administer the law, but not a new statute passed by Congress. That distinction matters enormously, because an interpretation issued by agencies can be modified or reversed by those same agencies under a future administration.

The clarity it provides is real but conditional, resting on the current regulators’ chosen reading instead of on durable law. This is precisely why, even as the industry welcomed the interpretation, many participants, and even one of the regulators involved, called for Congress to act, because only legislation can turn a reversible interpretation into permanent law. Stablecoins sit in their own separate lane, which is why the law governing the stablecoin category matters alongside the CLARITY Act rather than inside the same commodity bucket. Digital securities, meanwhile, remain a separate class, and the rise of the digital-securities category shows why not every on-chain asset belongs under commodity-style treatment.

How the CLARITY Act reclassifies crypto

The CLARITY Act, formally the Digital Asset Market Clarity Act, is the legislative effort to take the digital-commodity concept and write it into federal statute, giving it the permanence the 2026 interpretation lacks. The bill would create a statutory framework that sorts digital assets into categories and assigns them to regulators, with digital commodities placed under the commodities regulator and securities remaining with the securities regulator. In doing so, it would codify the jurisdictional split that the interpretation expressed, so that the division of authority between the two agencies rests on law instead of on an agreement that could be undone. A companion measure moving through the agriculture committee, sometimes called the Digital Commodity Intermediaries Act, would give the commodities regulator formal jurisdiction over the spot markets for digital commodities, addressing the long-standing gap in which that regulator could oversee derivatives but had limited authority over everyday spot trading.

The conceptual heart of how the CLARITY Act reclassifies crypto is a principle of separating the asset from the way it is offered and sold. Under this approach, the act recognizes that a token can be sold in a transaction that is an investment contract, and therefore a security at the point of that sale, while the underlying token itself can be a digital commodity. This separation is what allows the law to handle the awkward reality that the same token can look like a security in one context and a commodity in another. It means the securities regulator retains authority over primary-market fundraising, when a project first sells tokens to raise capital and buyers are relying on the team’s efforts, as well as over assets that truly function as investment contracts, while the commodities regulator takes over the secondary-market trading of digital commodities once a token’s network is mature.

By writing this structure into statute, the CLARITY Act would replace the case-by-case, lawsuit-driven approach of the past, in which classification was fought out one enforcement action at a time, with a predictable framework that issuers and exchanges can read in advance. That shift, from regulation by enforcement to regulation by clear rule, is what the industry treats as the bill’s central promise. It is also why the bill’s contested path matters so much: until the bill becomes law, the digital-commodity framework remains partly dependent on agency interpretation rather than statutory permanence. The category may now be easier to understand, but it still needs Congress to make it durable.

The maturity test: how a token moves from security to commodity

The cleverest and most important mechanism in the CLARITY Act is the one that lets a token change categories as its network matures, because it directly addresses the moving-line problem that Howey created. The bill creates a maturity test, a set of criteria for determining when a blockchain system has become decentralized and functional enough that its token should be treated as a digital commodity instead of as part of a securities offering. The underlying idea follows directly from the efforts-of-others principle: a token sold early in a project’s life, when a central team is building the network and buyers are betting on that team’s success, fits the securities framework. Once the network is truly up and running and no longer dependent on a central group’s managerial efforts, the justification for securities treatment fades, and the token can graduate to commodity status.

This creates what is sometimes called a maturity on-ramp, a path by which a token can begin under securities oversight and, as its network decentralizes and meets the maturity criteria, transition to commodity oversight. The criteria for maturity center on decentralization: roughly, whether the system operates without any single person or affiliated group exercising outsized control over the network or its value, whether it is functional, and whether its governance and operation are truly distributed. A blockchain that meets the test is treated as mature, and its native token is treated as a digital commodity. This mechanism is what makes the CLARITY Act more sophisticated than a simple fixed list of which tokens are commodities.

Instead of freezing classifications in place, it provides a rule for how a token earns commodity status by becoming the kind of decentralized network that commodity treatment is meant for. It is also, as the limits section notes, one of the most contested parts of the bill, because deciding exactly how decentralized is decentralized enough is truly difficult, and the definition the bill uses has been criticized from multiple directions. But the basic design, a test that lets status follow the reality of a network’s maturity instead of being fixed at launch, is the conceptual engine of how the CLARITY Act would reclassify crypto. It gives projects a legal path from fundraising-stage oversight to mature-network treatment, rather than forcing every dispute into the courts.

What reclassification actually changes

For everyday holders and for the market, the abstract question of classification translates into concrete consequences, so it is worth being specific about what changes when a token is treated as a digital commodity. The most immediate effect is on financial products, above all exchange-traded funds. An asset classified as a commodity follows a far more direct regulatory path to a spot ETF than a security does, which is why the digital-commodity designation has been linked to a surge of pending ETF applications across many tokens. For an investor, this matters because spot ETFs are often the most convenient and trusted way for both retail and institutional money to gain exposure to an asset, so commodity status can widen access and bring in new demand.

Reclassification also eases how exchanges list a token, since listing a commodity does not carry the securities-law obligations that listing a security does, and it lowers the compliance burden across the board. The change extends to institutions and to specific crypto activities. Large institutions, including asset managers and pension funds, generally face fewer restrictions holding commodity-classified assets than security-classified ones, so commodity status can unlock institutional participation that securities treatment would discourage. The 2026 interpretation also clarified that certain activities long shadowed by securities-law uncertainty, including protocol staking and the wrapping of tokens, are not in themselves securities transactions when conducted within defined boundaries, which removed legal risk that had pushed some platforms to suspend staking services.

To make the journey concrete, consider a token’s path under this framework: it might launch through a sale that is an investment contract, a security at that moment, with its issuer subject to securities obligations. Then, as its network grows decentralized and functional and meets the maturity test, the token itself comes to be treated as a digital commodity, its spot trading moves under the commodities regulator, exchanges can list it more easily, an ETF becomes feasible, and institutions grow more comfortable holding it. That arc, from security at birth to commodity at maturity, is the practical shape of what the CLARITY Act’s reclassification is designed to enable. It is why the industry views statutory clarity as the gateway to the next phase of adoption.

Limits, risks, and what is still unsettled

For all its significance, the digital-commodity framework comes with real limits and unresolved tensions that an honest account must address. The first and most important is the gap between interpretation and law. The 2026 classification of sixteen tokens as digital commodities is an agency interpretation, binding on the agencies but reversible by a future administration, which means the clarity it provides is conditional instead of permanent until Congress acts. And the legislation meant to make it durable, the CLARITY Act, has not become law; it has advanced through the House and a Senate committee but still faces a contested path, so the statutory permanence the industry wants is not yet secured.

Beyond the interpretation-versus-statute problem, several substantive concerns persist. The definition of decentralization at the core of the maturity test is truly hard to pin down, and critics argue the version in play is too narrow or too vague, which could lead to inconsistent or contestable classifications. There is a meaningful investor-protection tradeoff: moving an asset out of the securities regime and into the commodity regime means lighter disclosure requirements and fewer of the protections securities law provides, which supporters see as appropriate for decentralized assets but critics warn could leave holders more exposed, particularly because crypto can be more susceptible to manipulation than registered securities and direct crypto holdings do not carry the same regulatory safeguards. Classification can also remain context-dependent: even a token treated as a commodity in secondary trading could be part of a securities transaction if it is later sold subject to an investment-contract arrangement promising profits.

The whole area remains politically contested, with the CLARITY Act facing objections over its decentralized-finance provisions, its treatment of stablecoin yield, and ethics questions, any of which could reshape or stall it. The honest summary is that the digital-commodity category represents real and welcome progress toward clarity, but it currently stands on reversible interpretive ground, depends on legislation that has not passed, relies on a maturity test that is hard to define, and carries genuine investor-protection tradeoffs. It is a meaningful step in defining how crypto is regulated, not a finished or settled answer.

Frequently asked questions

What is a digital commodity in simple terms?

A digital commodity is a crypto asset whose value comes from how its blockchain works and from ordinary supply and demand, instead of from a company promising to do work that makes the token go up. That makes it the crypto equivalent of gold or oil instead of a company’s stock. Because no central enterprise is driving its value through promised efforts, it is treated like a commodity under the lighter-touch commodities regulator instead of as a security under the heavier securities regulator. Regulators have long treated Bitcoin this way and, in 2026, extended the label to other sufficiently decentralized tokens such as Ethereum, XRP, and Solana.

Why does it matter whether a token is a security or a commodity?

Because the two are regulated completely differently, and the difference shapes nearly everything. A security falls under the securities regulator’s heavy regime of registration, disclosure, and trading restrictions designed to protect investors. A commodity falls under the commodities regulator’s far lighter regime, which oversees derivatives and pursues fraud but imposes much less burden on the underlying asset. Commodity status makes a token easier to list, lighter to comply with, more accessible to institutions, and far closer to qualifying for a spot exchange-traded fund.

Which cryptocurrencies are digital commodities?

In March 2026 the securities and commodities regulators jointly named sixteen major tokens as examples of digital commodities, including Bitcoin, Ethereum, Solana, and XRP, along with others such as Cardano, Litecoin, Stellar, and some memecoins. The list was described as not closed, meaning other assets could qualify. The common thread is that these tokens derive their value from decentralized, functional networks instead of from a central team’s promised efforts. It is important to note this came from an agency interpretation instead of a law, so while it gave real clarity to those tokens, the classification rests on interpretive footing that could change until Congress passes durable legislation.

How does the CLARITY Act reclassify crypto?

The CLARITY Act would write the digital-commodity category into federal statute, placing digital commodities under the commodities regulator and securities under the securities regulator, codifying the jurisdictional split so it rests on law instead of a reversible interpretation. Its key mechanism is separating the asset from how it is sold: a token can be sold in a securities transaction while the underlying token is a digital commodity. The securities regulator keeps authority over fundraising and genuine investment contracts, while the commodities regulator takes over secondary trading of mature digital commodities. This replaces the old case-by-case enforcement approach with a predictable, statutory framework.

What is the maturity test?

The maturity test is the CLARITY Act’s mechanism for letting a token move from security to commodity as its network matures. The idea follows from the principle that a token sold early, when a central team is building the network and buyers rely on that team’s efforts, fits the securities framework, but once the network is truly decentralized and functional, no longer dependent on a central group, the token can graduate to digital-commodity status. The criteria center on decentralization: whether any single person or group exercises outsized control, whether the system is functional, and whether its operation is truly distributed. It creates a maturity on-ramp instead of freezing a token’s status at launch, though defining decentralization precisely remains contested.

Is a digital commodity safer or less regulated than a security?

It is less heavily regulated, which cuts both ways. Commodity status means lighter compliance, easier listing, and broader access, which the industry views as appropriate for decentralized assets and a driver of adoption. But it also means fewer of the disclosure requirements and investor protections that securities law provides, so holders may be more exposed, particularly because crypto can be more susceptible to manipulation than registered securities and direct crypto holdings lack the same safeguards. Commodity status is also not a permanent, blanket shield, since a token could still be part of a securities transaction if later sold with profit promises.

This article is educational information, not legal, financial, or tax advice. The classification of crypto assets, the status of the 2026 regulatory interpretation, and the progress of the CLARITY Act reflect information available as of June 28, 2026, and can change. Regulatory classifications can be modified, and the legal treatment of any specific token may differ by context and jurisdiction. Verify current details from primary sources and consult a qualified professional before making any decision.

Tether is expanding the use of Tether Gold as crypto lender Ledn adds support for XAU₮.

Summary

- Tether is expanding XAU₮ utility by bringing tokenized gold into Ledn’s lending platform this year.

- XAU₮ holders will be able to borrow against gold without selling the underlying tokenized bullion.

- The move follows Tether’s wider shift toward gold, Bitcoin mining, AI, and infrastructure assets.

The move will let users hold and trade tokenized gold on Ledn, with gold-backed loans expected later this year.

The plan extends Tether’s wider gold strategy at a time when tokenized bullion is gaining more use in crypto markets. Each XAU₮ token represents one fine troy ounce of physical gold stored in Swiss vaults.

XAU₮ joins Ledn’s lending platform

Ledn said it has added support for XAU₮ alongside Bitcoin, USD₮ and USA₮. The platform said users can now hold and trade XAU₮, while borrowing against the tokenized gold product will come later in 2026.

The product follows the same structure Ledn has used for Bitcoin-backed loans. Users can access liquidity while keeping exposure to the underlying asset instead of selling it for cash.

Ledn said client collateral remains held 1:1 and is not lent out or used to generate yield. That point matters after the 2022 crypto lending failures, when weak risk controls and rehypothecation hurt many customers.

The company said demand is growing for services that combine long-term asset ownership with financial flexibility.

“As digital assets become an increasingly important part of the global economy, demand is growing for solutions that combine long-term ownership with financial flexibility,” Tether CEO Paolo Ardoino said.

Tether expands its gold strategy

Tether Gold has grown sharply over the past year as demand for tokenized gold increased. Tether said XAU₮ reserves reached 707,747.139 fine troy ounces by March 31, 2026.

That was up from 520,089.350 fine troy ounces at the end of 2025. Tether said XAU₮’s market value rose from about $2.25 billion to more than $3.3 billion during the first quarter.

The wider $23 billion gold figure refers to Tether’s broader bullion position across its products. Reuters reported that Tether held about 132 metric tons of gold for USDT reserves at the end of March, valued near $19.8 billion, while XAU₮ accounted for about 22 tons.

Tether has also moved to focus more on XAU₮ after closing Alloy and aUSDT. As previously reported, users can redeem aUSDT and recover XAU₮ until Sept. 17 before Alloy support ends.

Gold-backed loans mirror Bitcoin lending

Gold-backed lending is not new in traditional finance. Banks, bullion dealers and large financial firms have long used physical gold as collateral.

Tether and Ledn are trying to bring that model into digital asset markets. Tokenized gold can move on blockchain rails while still tracking ownership of physical bullion held in custody.

This setup may appeal to users who want to keep gold exposure but still need liquidity. A borrower could use XAU₮ as collateral and receive stablecoins without selling the gold-backed asset.

The model also gives Tether another way to add use cases around XAU₮. Instead of acting only as a tokenized gold holding, XAU₮ could become collateral inside crypto lending markets.

Tokenized gold push widens

The Ledn plan follows other recent moves around Tether Gold. Tether and Fasset launched a Visa card with XAU₮ rewards, allowing eligible users to spend through the card and earn up to 6% cashback in tokenized gold.

That product placed XAU₮ closer to everyday payments. It also showed how Tether is testing uses for tokenized gold beyond storage and trading.

The company has also invested beyond stablecoins. Tether has backed Bitcoin mining, renewable energy projects, AI infrastructure, Gold.com and Antalpha as part of a wider technology and infrastructure push.