Crypto World

The CLARITY Act quietly bans a US CBDC. What that actually means

Everyone is watching the CLARITY Act for what it does to crypto market structure. Buried inside it is a provision with a different target entirely: a ban on a US central bank digital currency. It is literally one of the bill’s three names. Here is what the anti-CBDC provision does, why it is there, and why it may matter more for stablecoins than for anything else.

Summary

- The CLARITY Act carries an anti-CBDC provision so central that it is one of the bill’s three official short titles, alongside the market-structure language that gets all the attention.

- The provision amends the Federal Reserve Act to bar the Fed from issuing a retail central bank digital currency directly or indirectly, and from using one to conduct monetary policy, without explicit approval from Congress.

- A central bank digital currency would be a direct liability of the Fed recorded on a government-controlled ledger, which supporters argue would hand the government real-time visibility into individual transactions.

- The biggest practical effect would be to remove the only potential government-backed competitor to private stablecoins, handing issuers of tokens like USDC, USDT, and Ripple’s RLUSD a durable structural advantage.

- The same CBDC ban is advancing on several tracks at once, including a four-year ban that already passed both chambers inside a housing bill, so the CLARITY provision is part of a broader, redundant Republican push.

Almost everyone watching the CLARITY Act is watching it for one reason: it would settle the long fight over whether crypto tokens are securities or commodities, reshaping how the entire digital-asset market is regulated. That is the headline, and it is a big one. But folded inside the same bill is a provision aimed at something completely different, a ban on a United States central bank digital currency, and it is not a minor footnote.

The anti-CBDC language is so integral to the legislation that it is one of the bill’s three official short titles: the same act is named the Digital Asset Market Clarity Act, the CLARITY Act, and the Anti-CBDC Surveillance State Act. In other words, stopping a government digital dollar is not a rider quietly attached to the bill; it is one of the bill’s stated purposes, written into its very name. Yet because the market-structure debate consumes nearly all the attention, the CBDC ban has traveled largely under the radar, which is exactly why it is worth examining on its own.

The reason this matters extends well beyond a technical change to the Federal Reserve Act. A ban on a US central bank digital currency touches some of the most charged questions in money today: financial privacy, government surveillance, the future of the dollar, and, most concretely for crypto, the competitive fate of private stablecoins. Removing the possibility of a government-issued digital dollar does not just settle a privacy debate; it clears the field of the one competitor that could have challenged the private stablecoins now becoming central to crypto and payments.

This piece explains what the anti-CBDC provision actually does, what a central bank digital currency is and why it generates such fierce opposition, the political case behind the ban, the bigger prize of a protected lane for private stablecoins, the several parallel tracks on which the ban is moving, the serious arguments against it, and what it all means for crypto holders. The market-structure fight may decide how crypto is regulated, but the CBDC provision could quietly shape who wins the payments future, which makes it one of the most consequential parts of the bill almost nobody is discussing.

What the provision actually does

Start with the mechanics, because the provision is specific. The anti-CBDC language amends the Federal Reserve Act to impose several related prohibitions on the central bank. It bars the Federal Reserve banks from offering certain products or services directly to individuals, which is the structural feature a retail digital dollar would require, since a true retail CBDC would mean ordinary people holding accounts or balances directly with the Fed.

It prohibits the Fed from issuing a central bank digital currency, or any digital asset substantially similar to one, directly to individuals or indirectly through financial institutions or other intermediaries. It prohibits the use of a central bank digital currency to conduct monetary policy. And in its fuller forms, the anti-CBDC framework also bars the Fed from even testing or developing a CBDC without explicit authorization from Congress.

The throughline of all these provisions is a single principle: the Federal Reserve should not be able to create a digital dollar for the general public on its own authority. Under the ban, any move toward a retail CBDC would require Congress to pass a law specifically authorizing it, rather than the Fed proceeding through its own rulemaking. This converts the question of a digital dollar from a decision the central bank could make into one that only elected legislators could make, which supporters see as a crucial check and critics see as an unnecessary handcuff.

Notably, the bans are generally written to protect private, dollar-denominated digital currencies that are open and preserve the privacy features of physical cash, meaning they target a government-issued CBDC specifically while leaving private stablecoins untouched. That carve-out is not incidental; as the later sections show, protecting private stablecoins while blocking a government one is arguably the whole point.

What a CBDC is, and why it draws such fire

To understand the intensity of the opposition, you have to understand what a central bank digital currency actually is, because it is easy to confuse with the digital money people already use. The dollars in an ordinary bank account are already digital, but they are a liability of a commercial bank, not the Federal Reserve, and they pass through the banking system with its existing layers of intermediation.

A retail central bank digital currency would be fundamentally different: it would be a direct liability of the Federal Reserve itself, a form of digital money issued and backed by the central bank, held by the public, and recorded on a ledger the government controls. In its retail form, it would be used by ordinary people for everyday transactions, the digital equivalent of cash but issued directly by the state, as distinct from a wholesale CBDC, which financial institutions would use to settle large transactions among themselves.

The objection that animates the ban is captured in the bill’s own framing as an anti-surveillance measure. Critics of CBDCs, including the lawmakers behind the provision, argue that because a retail CBDC would be recorded on a centralized, government-controlled ledger, it would give the issuing authority complete, real-time visibility into individual transactions, and potentially the power to control or restrict how people spend their own money.

To this way of thinking, a government digital currency is the antithesis of the privacy that cash and, in a different way, cryptocurrency provide, and it edges toward a system of financial surveillance incompatible with a free society. Supporters of the ban frame it as protecting Americans from government overreach into their financial lives.

This is why the provision carries the loaded name Anti-CBDC Surveillance State Act, and why the issue has become a rallying point: for its proponents, blocking a CBDC is about preventing a tool of state surveillance before it can be built, which is a far more emotive cause than the technical market-structure questions that surround it in the same bill.

The political case behind the ban

The anti-CBDC provision did not arrive by accident; it reflects a deliberate and long-standing political push, and understanding that context clarifies why it sits inside the CLARITY Act. Opposition to a US central bank digital currency has been a priority for many Republican lawmakers and for the current administration, framed around privacy and limited government.

The legislator most associated with the standalone anti-CBDC effort has described its purpose as codifying the President’s stated effort to prevent the development of a central bank digital currency and to keep the country’s digital-currency policy in the hands of the American people rather than what he called the administrative state.

The President signed an executive order opposing a CBDC early in the administration, and the Treasury Secretary has publicly stated that a digital dollar is off the table, with the government instead focusing its energy on passing crypto legislation like the CLARITY Act.

This alignment between the administration and congressional Republicans is why the anti-CBDC language has been pursued through multiple vehicles and why it found a home inside the CLARITY Act. For its proponents, the goal is not merely to stop a CBDC that might be built someday, but to write the prohibition into durable law so that no future administration could pursue a digital dollar without going back to Congress.

It is worth being precise that this is a contested, partisan framing rather than a neutral consensus: supporters present the ban as a vital privacy protection, while opponents, as a later section details, see it as solving a problem that does not exist and forfeiting a tool other countries are embracing.

But on the proponents’ side, the case is coherent and deeply felt: a retail CBDC represents, in their view, an unacceptable expansion of government power over individuals’ money, and banning it preemptively is a way to foreclose that risk for good. That conviction is what put an anti-surveillance measure into a crypto market-structure bill and made it one of the bill’s defining names.

The bigger prize: a moat for private stablecoins

Beyond the privacy argument, the anti-CBDC provision carries a commercial consequence that may matter more for crypto than the surveillance debate, and it concerns the booming market for private stablecoins. Stablecoins are privately issued digital tokens pegged to the dollar, and they have become central to crypto trading and increasingly to real-world payments, with the largest, such as Circle’s USDC and Tether’s USDT, accounting for the overwhelming majority of stablecoin volume, and newer entrants like Ripple’s RLUSD growing quickly.

A retail central bank digital currency would be the one thing capable of seriously challenging these private stablecoins, because a government-issued digital dollar would offer the public a sovereign, risk-free digital alternative to a privately issued token. If people could hold digital dollars directly from the Federal Reserve, the appeal of holding a private stablecoin would diminish for many uses.

By banning a US CBDC, the provision removes that competitor before it can exist, and this is where the privacy framing and the commercial reality converge. The ban forecloses the only credible government-backed rival to private stablecoins, effectively handing issuers a structural advantage that no amount of regulation or marketing could buy them: the absence of a sovereign competitor, guaranteed by law.

This is why the CLARITY Act and the stablecoin framework already signed into law are best understood as sequential pieces of the same strategy. The earlier law set up the licensing framework for private stablecoins, and the CLARITY Act, by blocking a CBDC, helps clear the competitive field on which those stablecoins will operate. The result is a deliberate tilt of the payments future toward private issuers and away from a government digital dollar.

For crypto, and for the stablecoin issuers in particular, this is arguably the most important practical effect of the anti-CBDC provision: not the abstract privacy principle, but the concrete removal of the one competitor that could have constrained the private stablecoin market just as it is becoming central to the industry. Holders of stablecoin-linked assets, including those in the XRP ecosystem given Ripple’s RLUSD, sit on the favorable side of that tilt.

The ban is moving on several tracks at once

An important nuance, often lost in coverage, is that the CLARITY Act is not the only vehicle carrying the CBDC ban, and appreciating the full picture prevents overstating the role of any single bill. The same anti-CBDC objective has been advancing through at least three parallel paths. First, the language lives inside the CLARITY Act itself as one of its named components.

Second, a standalone Anti-CBDC Surveillance State Act passed the House of Representatives as its own bill and went to the Senate separately, giving the prohibition an independent path. Third, and most strikingly, a four-year ban on a Federal Reserve CBDC, running through the end of 2030, was attached to an unrelated housing bill that passed the Senate by an overwhelming margin and cleared the House, putting it on the verge of becoming law.

That housing-bill ban illustrates both the momentum behind the anti-CBDC push and the political turbulence around it. The provision sailed through Congress with broad support, banning the Fed from issuing a CBDC directly or indirectly through intermediaries while explicitly protecting private stablecoins that are open and preserve cash-like privacy. But the bill’s signing was delayed when the President held it up over an unrelated demand on separate legislation, a reminder that even broadly supported measures can get caught in larger political standoffs, and that the delay consumed legislative time the CLARITY Act itself could ill afford.

The takeaway is that the CBDC ban is overdetermined: it is being pursued through redundant channels, so even if the CLARITY Act stalls, the prohibition may well become law through one of the other paths. For anyone trying to gauge the future of a US digital dollar, the honest assessment is that the political system has moved decisively against one, through multiple overlapping efforts, of which the CLARITY Act provision is one prominent part instead of the sole determinant.

The serious case against the ban

Evenhandedness requires taking the arguments against the CBDC ban seriously, because they are substantive and come from credible quarters, not just from would-be government surveillers. The most striking criticism is that the ban would make the United States a global outlier. A great many countries are actively developing or piloting central bank digital currencies, with China’s digital yuan among the most advanced and well over a hundred countries exploring the technology in some form.

Banning a CBDC outright would make the United States the only major economy to foreclose the option entirely, which critics argue cedes ground in the evolution of money and could, over time, weaken the dollar’s competitive position in a world moving toward digital sovereign currencies. The concern is not that a digital dollar is necessarily desirable, but that permanently banning even the ability to build one is a drastic and possibly shortsighted response.

A related criticism is that the ban could hamper legitimate central-bank work on the future of payments. The Federal Reserve participates in international efforts to modernize cross-border payments using tokenized central-bank money, and a sweeping prohibition could undercut that research and the United States’ role in shaping global standards. Critics also note a certain irony: the Federal Reserve was not actually building a retail CBDC, so the ban forecloses a project that did not exist, which they argue makes it more a symbolic and ideological act than a response to a real and present threat.

From this angle, the provision solves a hypothetical problem at the cost of real flexibility, while the privacy concerns it cites could in principle be addressed through design choices instead of an outright ban. Supporters answer that a preemptive, permanent ban is exactly the point, because it removes the temptation and the risk for good, and that the surveillance dangers are too serious to leave to future design promises. Both sides have a coherent case, and reasonable people land in different places, but the debate is real and should not be flattened into a simple privacy-versus-surveillance morality tale. The ban has genuine costs as well as the benefits its supporters emphasize.

What it means for crypto and XRP holders

For crypto holders trying to translate all this into something actionable, the anti-CBDC provision points in a fairly clear direction, even if its effects are more structural than immediate. The most direct consequence is favorable for private stablecoins and, by extension, for the parts of the crypto ecosystem built around them.

By removing the prospect of a government-issued digital dollar, the ban protects the competitive position of private stablecoins at exactly the moment they are becoming central to crypto payments and settlement. Issuers like Circle and Tether benefit from the absence of a sovereign rival, and so does Ripple’s RLUSD, which means holders in the XRP ecosystem have a stake in this outcome even though it sits in the regulatory weeds instead of the price charts. The broader thesis that private, on-chain dollars will carry an increasing share of payments gets a meaningful boost when the public-sector alternative is taken off the table by law.

The effects on the wider crypto market are more diffuse but still real. The anti-CBDC stance is part of the same policy posture that favors private digital assets and lighter-touch regulation, and its advance signals an environment broadly supportive of the industry. At the same time, holders should keep the provision in proportion. Because no US retail CBDC was actually being built, the ban changes the hypothetical future more than the present reality, and its largest effects are competitive and long-term instead of an immediate catalyst for any token’s price.

It is also worth remembering that the ban is moving through several vehicles, so its fate is not bound to the CLARITY Act alone, and that the privacy debate it embodies is genuinely contested, with credible arguments on both sides about whether foreclosing a CBDC serves or harms the country’s long-term interests. The clear-eyed reading for a holder is that the anti-CBDC provision is a quiet but meaningful tailwind for private stablecoins and the broader private-digital-money thesis, embedded in a bill whose market-structure provisions will likely matter more for prices in the near term, but whose CBDC language may shape the deeper question of who owns the future of digital payments.

Frequently Asked Questions

Does the CLARITY Act really ban a US CBDC?

Yes, the anti-CBDC provision is one of the bill’s three official short titles, alongside the Digital Asset Market Clarity Act and the CLARITY Act, the third being the Anti-CBDC Surveillance State Act. The language amends the Federal Reserve Act to bar the Fed from issuing a retail central bank digital currency directly to individuals or indirectly through intermediaries, from using a CBDC for monetary policy, and, in its fuller forms, from even testing one without explicit authorization from Congress. So blocking a government digital dollar is not a minor rider but one of the bill’s stated purposes, even though the market-structure provisions receive nearly all the public attention.

What is a central bank digital currency?

A central bank digital currency, or CBDC, is digital money issued and backed directly by a country’s central bank. A retail CBDC, the kind the ban targets, would be held by ordinary people and used for everyday transactions, making it a direct liability of the Federal Reserve recorded on a government-controlled ledger. This differs from the digital dollars already in bank accounts, which are liabilities of commercial banks, not the Fed. It also differs from a wholesale CBDC, which financial institutions would use to settle large transactions among themselves. The retail version is what generates the privacy concerns, because it would route everyday payments through a ledger the government controls.

Why do supporters want to ban a CBDC?

Supporters frame it as a privacy and anti-surveillance measure. Their core argument is that a retail CBDC, recorded on a centralized government ledger, would give the state real-time visibility into individuals’ transactions and potentially the power to control how people spend their money, which they see as incompatible with financial freedom. The provision’s name, the Anti-CBDC Surveillance State Act, captures this framing. Proponents, including the administration and many Republican lawmakers, want to write the ban into durable law so no future administration could build a digital dollar without explicit congressional approval, foreclosing what they view as a serious surveillance risk before it can materialize.

How does banning a CBDC affect stablecoins?

It helps private stablecoins significantly. A government-issued digital dollar would be the one thing capable of seriously challenging private stablecoins like USDC, USDT, and Ripple’s RLUSD, because it would offer the public a sovereign, risk-free digital alternative. By banning a US CBDC, the provision removes that competitor before it can exist, handing private stablecoin issuers a structural advantage guaranteed by law. The bans are also typically written to protect private stablecoins explicitly while blocking the government one. This is arguably the most important practical effect of the provision, tilting the future of digital payments toward private issuers and away from a public digital dollar.

Is the CLARITY Act the only bill banning a CBDC?

No, and this is an important nuance. The same anti-CBDC objective is advancing through several parallel tracks. It exists inside the CLARITY Act as one of its named components, a standalone Anti-CBDC Surveillance State Act passed the House separately and went to the Senate, and a four-year CBDC ban running through 2030 was attached to an unrelated housing bill that passed both chambers and is near becoming law. So the prohibition is being pursued redundantly, which means it may become law through one of these paths even if the CLARITY Act stalls. The CLARITY provision is one prominent part of a broader push instead of the sole vehicle.

What are the arguments against banning a CBDC?

Critics make several serious points. A ban would make the United States the only major economy to foreclose a CBDC entirely, while many countries, including China with its digital yuan, are actively developing them, which critics argue cedes ground in the evolution of money and could weaken the dollar’s long-term position. They note the Fed was not actually building a retail CBDC, so the ban forecloses a project that did not exist, making it more symbolic than responsive to a real threat. They also warn it could hamper legitimate central-bank work on modernizing cross-border payments. Supporters counter that a permanent, preemptive ban is precisely the point, removing the risk for good. Both sides have coherent arguments

This article is information, not legal, financial, or investment advice. The status and contents of the CLARITY Act, the standalone anti-CBDC legislation, and related bills reflect reporting available as of June 27, 2026, and can change. The CBDC debate is politically contested, and this article presents the arguments of multiple sides instead of endorsing any. Nothing here is a recommendation regarding any token or security. Verify current details from primary sources and consider your own circumstances before making any decision.

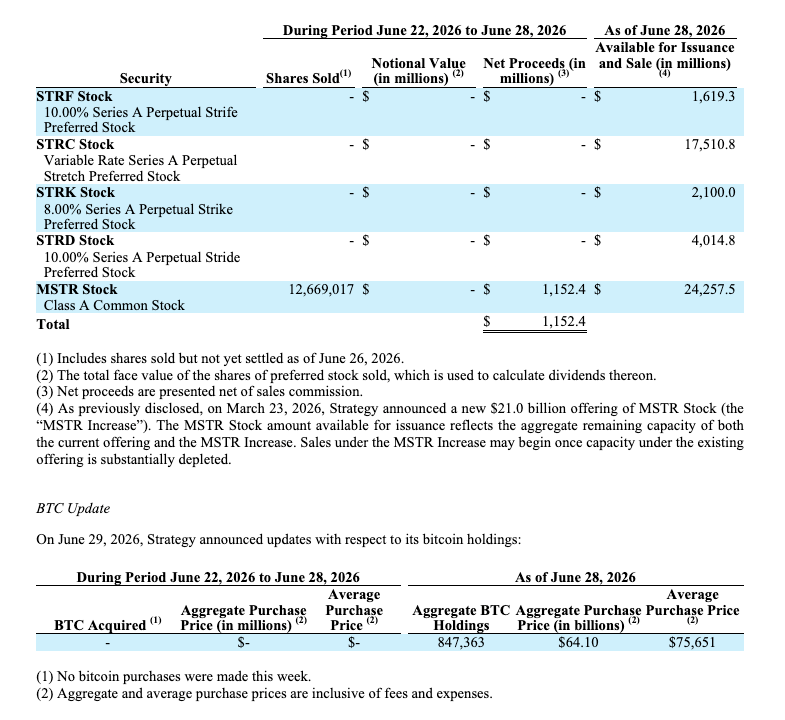

Strategy is adopting a new capital framework that allows it to monetize part of its Bitcoin holdings to fund dividends, build cash reserves and repurchase securities while maintaining its long-term Bitcoin strategy.

In a Monday 8-K filing with the US Securities and Exchange Commission, Strategy introduced its “Digital Credit Capital Framework,” which includes a Bitcoin monetization program and changes to its STRC preferred stock dividend policy.

The company has raised the STRC annual dividend rate to 12% from 11.5% and authorized separate buyback programs for preferred securities and its Class A MSTR common stock. Strategy said it may sell Bitcoin (BTC) to raise as much as $1.25 billion to increase its cash reserve, pay dividends and debt costs, as well as fund stock buybacks.

The filing comes amid a volatile stretch that has seen the value of MSTR shares slide almost 50% year-to-date while the price of STRC on Friday dropped as low as $71.25, a 28.75% discount to par, according to TradingView data. Grayscale’s research head Zach Pandl last week said Strategy should sell $3 billion in Bitcoin to cover its cash obligations.

Ahead of Monday’s Nasdaq open, investors had bid up MSTR share price more than 5.5%.

Strategy boosts cash reserve to $2.55 billion

A key part of the new framework is the company’s cash reserve, which it said has grown to $2.55 billion, or enough to cover about 17 months of preferred stock dividends and interest payments.

Under the new policy, the reserve can only be used for those payments and must be maintained at a minimum of 12 months unless the board approves otherwise.

Source: Michael Saylor

Strategy executive chairman Michael Saylor said the existing cash reserve, combined with the $1.25 billion Bitcoin monetization capacity, gives Strategy up to $3.8 billion in dividend coverage, or nearly 26 months.

Related: Grayscale’s Pandl says Strategy should sell $3B Bitcoin to restore confidence

“Strategy expects to remain disciplined in its use of MSTR issuance, particularly when the stock trades at or near 1x mNAV,” Saylor added.

No Bitcoin purchases as Strategy raises $1.15 billion

The biggest public Bitcoin treasury company also reported that it did not acquire any BTC during the week ended Sunday, leaving its holdings unchanged at 847,363 BTC purchased for a combined $64.1 billion, at an average of $75,651 apiece. At last look, traders were paying about $60,018 to buy the token.

The company has added a net 3,625 BTC so far in June after buying 3,657 BTC and selling 32 BTC earlier in the month.

Source: SEC

At the same time, the company disclosed raising around $1.15 billion in net proceeds by selling 12.67 million MSTR shares.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

The road from believing “crypto is a scam” to “Bitcoin is a legitimate asset class” is a long way to travel, fraught with many a twist and turn.

Yet against all the odds, a surprising number of high-profile skeptics have undertaken the journey unscathed and, perhaps more remarkably, without ever admitting they were wrong.

The very naysayers who once warned of a “crypto apocalypse” have begun preaching the virtues of blockchain rails and launching tokenized products of their own.

From Bitcoin exchange-traded funds to tokenized gold, here are five of the biggest crypto backflips.

Born-again crypto converts

Larry Fink: ‘Index of money laundering’ to ETF king

Larry Fink may be the archetypal born-again crypto convert. In 2017, the BlackRock chief executive cast Bitcoin as an “index of money laundering,” nicely capturing mainstream finance’s view at the time of a market they believed was dominated by wild speculation and dubious flows.

As a side note: people in glass houses shouldn’t throw stones. While money laundering in crypto was estimated at $82 billion in 2025, the United Nations Office on Drugs and Crime estimates that roughly $800 billion to $2 trillion is laundered the old fashioned way each year.

Related: BlackRock Bitcoin ETF sees near-record outflows as BTC dips below $75K

It’s not entirely clear why Fink decided to recalibrate but by 2020 he started acknowledging its potential, in 2023 he was actively defending BlackRock’s crypto push, and today BlackRock has become one of the most important institutional access points to Bitcoin via spot ETFs, helping pull the asset into the heart of the regulated investment universe.

In his annual shareholder letters, Fink now waxes lyrical about tokenization and writes impassioned OpEds about how it is set to transform the financial system.

Reluctant but will make money anyway

Jamie Dimon: still hates Bitcoin, loves the rails

If Fink is a born-again believer, Jamie Dimon sits squarely in the reluctant and still skeptical camp.

The JPMorgan chief has called Bitcoin a “fraud,” crypto investors “stupid,” and warned that BTC will blow up on more than one occasion, not to mention using Congressional hearings as a platform to reiterate his distaste for the asset.

But watch what he does, not what he says as JPMorgan has quietly become one of Wall Street’s biggest blockchain infrastructure providers.

The world’s largest bank has built out its Onyx division, rolled out JPM Coin, experimented with linking bank infrastructure to crypto wallets, and developed tokenized collateral platforms to move cash and securities around more efficiently.

Oh sure, Dimon still trashes Bitcoin in public, but JPMorgan now sells many of the rails that make institutional digital asset markets viable.

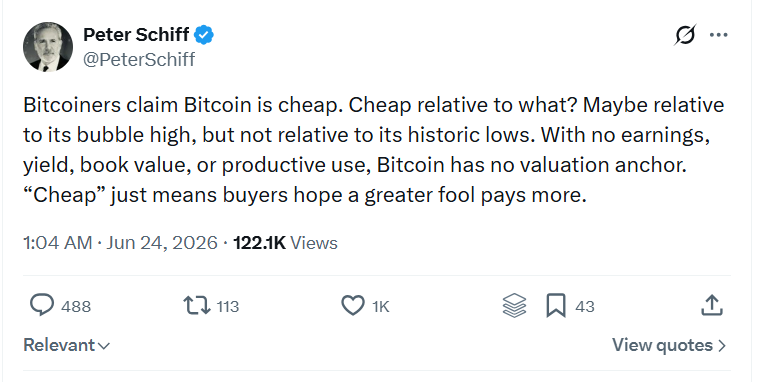

Peter Schiff: gold forever, but now onchain

Peter Schiff hasn’t softened his rhetoric as prices and adoption grow. If anything, each Bitcoin rally only amplifies his warnings about bubbles, “greater fools,” and inevitable collapse. It’s a highly effective form of advertising for Schiff’s beloved gold industry.

Peter Schiff’s infamous “greater fools” comment. Source: Peter Schiff

Yet even the perpetual goldbug has edged into the digital asset world by launching a tokenized gold platform, T-Gold.com, in December 2025, that uses blockchain to represent vaulted bullion as transferable tokens.

The product lets users buy physical gold and silver stored in segregated vaults and receive digital tokens representing specific quantities of the metals, with ownership recorded on a blockchain.

Related: Tucker Carlson presses Peter Schiff on Bitcoin as new global reserve currency

For Schiff, this is not apostasy but reinforcement: a way to tell crypto-native investors “you can keep the rails, but swap the asset for something with thousands of years of monetary history instead.”

Nouriel Roubini: Technodollars, not Bitcoin

Nouriel Roubini, once known in crypto circles as “Dr. Doom,” might seem like an unlikely candidate for any kind of crypto conversion.

He has spent years describing most digital assets as “useless,” warning of a “crypto apocalypse,” and cataloguing the sector’s governance failures, conflicts of interest, and investor harm.

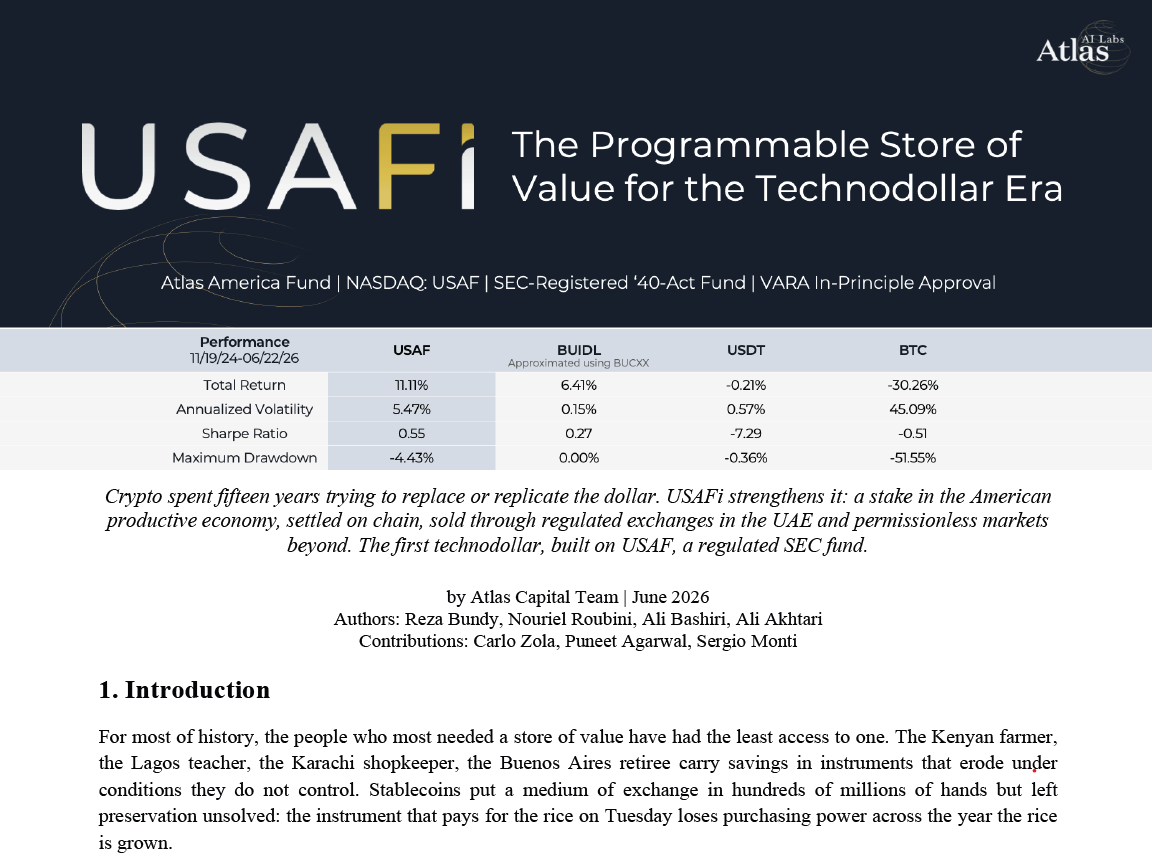

Yet this week, he published a whitepaper co-authored with Atlas Capital and announced USAFi, a tokenized instrument marketed as a regulated permissionless security, designed to embody what he calls the “Technodollar.”

USAFi whitepaper. Source: Atlas AI Labs

Roubini insists this is “not a reversal,” telling Cointelegraph he “remains skeptical of unbacked crypto assets whose value depends primarily on speculation rather than fundamentals.”

The Technodollar, he argued, is about “modernizing the financial system through regulated, asset-backed digital instruments that can be trusted by institutions and individuals alike.”

He added that he still believes most crypto assets “suffer from excessive speculation, weak governance, conflicts of interest, and insufficient investor protections.”

Don’t understand it, but happy to cash in

Donald Trump: vibes over whitepapers

Perhaps unsurprisingly, Donald Trump belongs in a category of his own. The same politician who once said Bitcoin “seems like a scam” and warned that it could undermine dollar hegemony later rebranded himself as the “crypto president.”

Trump has flirted with nonfungible token drops, launched his own meme coin and one for his wife, and pitched himself as the defender of domestic crypto innovation against overreaching regulators (all while reportedly pocketing over $2.3 billion from his various crypto endeavors since 2024).

Trump promised to end Joe Biden’s war on crypto. Source: Vivek Ramaswamy

He may not be able to tell you the difference between proof-of-work and proof-of-stake, but he does understand his constituencies.

Related: Trump crypto company’s USD1 stablecoins backing UFC event bonuses

The crypto industry has matured into an important voting bloc, and its donors are increasingly strategic. What matters is the ability to read a room full of HODLers and say the right words about freedom, innovation, and firing Gary Gensler.

What changed: faith, incentives, or both?

Born-again converts like Fink have reframed crypto and tokenization as extensions of their existing mission, encouraged by clear demand and the opportunity to graft new fee streams onto enormous asset management franchises.

The reluctant skeptics, on the other hand, have tried to draw bright lines between “bad crypto” and “good digital finance,” and the opportunists, well, they’ve learned that even a shallow embrace of digital assets can unlock both support and riches.

Of course, whether these moves represent genuine intellectual evolution or a simple instinct to follow the money remains to be seen. But perhaps the bigger question is: which crypto skeptic will be the next to see the light? Is it too much to hope that Warren Buffett will review his famed opinion about Bitcoin that it is “rat poison squared?”

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

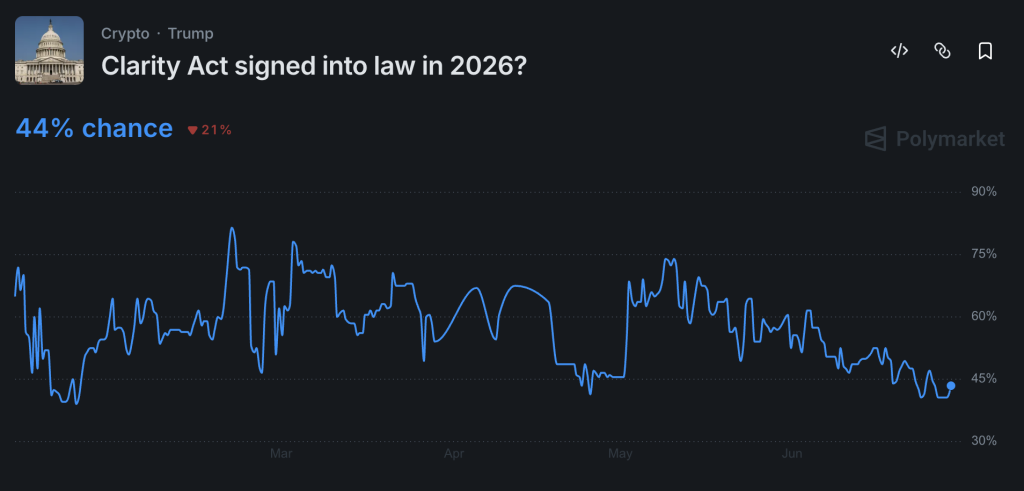

Galaxy Digital’s Head of Firmwide Research Alex Thorn cut the firm’s estimated probability of CLARITY Act passage in 2026 from 60% to 50% on June 26, citing a narrowing Senate calendar and intensifying competition for floor time, not unresolved policy disputes.

The downgrade marks the second directional cut in weeks, pulling the odds back to levels last seen in April after a brief surge to 75% following the Senate Banking Committee markup in May.

The context matters for anyone tracking crypto regulation and market structure legislation heading into the second half of 2026. A bill that passed the House 294-134 on July 17, 2025, with 78 Democrats crossing the aisle, is now stalling not on substance but on scheduling, and the window is closing fast.

Thorn’s note framed the issue plainly: the shortening calendar and growing competition for floor time are the primary drivers, with a July vote still possible but the path to 60 Senate votes increasingly unclear.

Discover: The Best Token Presales

Clarity ACT: Senate Adjourned Until July 13, Leaving Weeks Before the August Recess

The structural constraint is straightforward. The US Senate adjourned until July 13, and the August recess creates a hard backstop that compresses meaningful floor time to roughly two to three weeks. Senate Majority Leader John Thune secured unanimous consent for the adjournment with no objection, meaning the chamber has already consumed time that the CLARITY Act needed.

The Banking Committee and Agriculture Committee have not yet released a merged bill text, a prerequisite for any floor vote. Until a unified Senate draft is published, Thune cannot schedule floor consideration, and without an early July scheduling commitment, the bill slides to September.

That is not a soft deadline; September puts crypto legislation 2026 directly into midterm election season, where bipartisan cooperation on complex market structure bills has historically collapsed.

The Senate requires 60 votes for CLARITY Act passage, a threshold that demands meaningful Democratic buy-in. Competing priorities, FISA legislation, the National Defense Authorization Act, Trump’s housing bill tied to the SAVE Act, and a backlog of nominations, are all positioned ahead of crypto market structure in the queue.

Galaxy’s scenario framework is specific. If a unified Senate text is published around July 4, as Senator Cynthia Lummis has indicated is the target, and Thune commits to a floor vote before the recess, Thorn said odds could move back above 60%. The policy building blocks are largely in place: the bill establishes SEC/CFTC jurisdictional boundaries, introduces a mature blockchain test for securities classification, and extends federal AML obligations to digital commodity intermediaries for the first time.

If neither a merged text nor a scheduling commitment materializes before mid-July, Galaxy’s framework points to another downgrade. Ethics provisions, specifically conflict-of-interest rules for government officials’ crypto holdings, remain unsettled after a Van Hollen amendment failed 11-13 in committee, and Senators Ruben Gallego and Cory Booker have both treated enforceable ethics rules as a condition for their support. That is not resolved; it is deferred.

Parallel regulatory timelines in 2026 have consistently shown that prediction markets reprice faster than institutional analysts when legislative momentum stalls.

Polymarket traders currently put CLARITY Act passage at 41%, nine points below Galaxy’s 50%, having fallen from 82% in February as the Senate calendar deteriorated. That gap does not invalidate Thorn’s estimate, but it reflects how sharply informed public sentiment has moved against the July timeline.

The divergence is worth holding. Galaxy is pricing in the possibility that Lummis’s July 4 text target holds and leadership acts; Polymarket is pricing in the base rate of Senate inaction on complex legislation under a compressed calendar.

The CLARITY Act’s failure to clear the Senate this year would not be a minor procedural setback. Senator Lummis has warned that a miss in 2026 risks pushing market structure legislation to 2030 or beyond, given the probability of a changed chamber composition after November.

For institutional participants waiting on the SEC/CFTC jurisdictional split the bill codifies, each week of delay extends compliance uncertainty across the digital asset intermediary sector. The next hard signal to watch: publication of the merged Senate text. Its presence or absence in the first two weeks of July will determine whether Galaxy’s 50% holds or gets cut again.

Discover: The Best Crypto to Diversify Your Portfolio

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Here’s Why Galaxy Just Slashed Clarity Act Odds In Half appeared first on Cryptonews.

Crypto World

Prediction market consolidation could spark wave of M&A across sports betting, Bernstein says

The rapid consolidation of the prediction market technology stack is raising the odds of a new wave of mergers and acquisitions across sports betting and financial markets, according to Wall Street broker Bernstein.

Over the past eight months, every major consumer-facing prediction platform has moved to own both customer distribution and exchange infrastructure, the report said.

“Kalshi and Polymarket own the stack but trail on distribution, which leaves each as plausibly a target as an acquirer,” analysts led by Ian Moore said in the Monday report.

The analysts noted that DraftKings acquired Railbird to launch its DKeX exchange, Robinhood partnered with Susquehanna to build Rothera, Coinbase acquired The Clearing Company shortly after launching event contracts, and Flutter established a dual-FCM structure to preserve access to multiple exchanges.

The trend reflects Bernstein’s view that prediction markets are converging with sports betting and consumer finance into a single competitive landscape, opening the door to combinations that previously seemed unlikely, including sportsbooks buying exchanges, exchanges buying sportsbooks, and consolidation among sportsbook operators themselves.

Despite growing criticism and online FUD, Saylor’s brainchild Strategy continues to focus on BTC, but the new move is quite different.

Instead of announcing a new bitcoin purchase, the firm’s former CEO noted on X that the company has launched the Digital Credit Capital Framework to strengthen its digital credit, enhance liquidity, preserve long-term BTC exposure, and support long-term value creation.

DCCF Launched

Saylor’s first message reassured the public that the company has increased its USD reserve to $2.55 billion, which should cover the dividend payments for 17.4 months. The greenback stash can be used only for dividends and interest expense, and “will be maintained at a minimum of 12 months.”

Strategy has also established a BTC Monetization Program, which allows it to sell bitcoin to fund the USD reserve (with a cap of $1.25 billion), dividends and interest expenses, or to repurchase Digital Credit securities and MSTR under the applicable programs. If it indeed sells more bitcoin, then its dividend coverage rises to $3.8 billion – or 25.9 months of such payments.

Strategy has also established repurchase programs for its Digital Credit securities of up to $1 billion of MSTR.

“This will create flexibility to accretively buy back securities during market dislocations. Repurchases will not be funded from the USD reserve,” said Saylor.

In addition, STRC’s dividend rate has been increased by 50 bps to 12%, effective for the July 2026 record date. Saylor said the company will continue to evaluate the rate monthly, as its corporate objective for Stretch remains to trade at $99-$100. Recall that STRC plummeted by 25% under its par value in the past few weeks.

The Growing FUD

Recall that Strategy and particularly its STRC stock have come under a lot of fire in recent weeks. The company sold a tiny portion of its BTC holdings by the end of May, and even though it has accumulated a lot more since, market observers claim that the firm has rattled the industry.

Critics have continuously attacked Saylor and his company, warning that they might have to sell over 50,000 BTC in the next couple of years to cover some expenses or dividend payments.

CryptoQuant analysts suggested that Strategy should halt its BTC purchases in favor of rebuilding its USD reserve. Although the company has not listened entirely to this advice, the last two announcements were more focused on the USD reserve rather than the BTC stockpile.

The post Saylor’s Strategy Responds to Critics With New Plan to Protect BTC Exposure appeared first on CryptoPotato.

The former major bitcoin miner has expanded its Ethereum treasury once again during a week in which the asset slumped by over 8% and dived to a multi-month low of $1,500 before it found some support.

Bitmine Immersion Technologies now holds just over 5.7 million tokens, equivalent to approximately 4.7% of Ethereum’s total circulating supply of 120.7 million coins.

Bitmine Buys Again

Based on an ETH price of $1,570 as of June 28, the company’s total crypto, cash, and investment holdings stand at roughly $10 billion. The firm has reinforced its position as the world’s largest corporate holder of ETH and the second-largest public crypto treasury behind Strategy, which announced a new initiative this week, not a new BTC purchase.

Chairman and long-term ETH bull Tom Lee acknowledged the recent weakness across the entire market but maintained that Bitmine’s long-term outlook remains unchanged.

“This past week was a challenging one for crypto investors as ETH fell by 8%, even as Ethereum witnessed notable positive developments such as the creation of Ethlabs, and even the Bank of England softened its stance around stablecoins. We are nearing quarter-end for June, and it is not surprising to see ‘window dressing’ leading to investors reducing their holdings in assets which have fallen in the past 3 months,” added Lee.

He doubled down on his belief that Ethereum will eventually benefit from Wall Street’s migration toward blockchain-based financial infrastructure and the emergence of agentic AI payment systems operating on crypto rails.

The press release shared by the firm also noted that Bitmine has staked almost 4.9 million tokens (over 85% of its total holdings) through its own institutional staking platform, MAVAN. The current staking yield of 2.75% means that its annualized revenue will be around $211 million.

SharpLink’s Return

Although Bitmine remains the undisputed leader in terms of ETH accumulation, the second-in-line SharpLink returned last week with several major purchases. After spending eight months on the sidelines, the Joe Lubin-chaired firm bought 5,000 ETH on Friday and kept accumulating more over the weekend.

In total, the company spent more than $62 million to acquire a total of 39,196 ETH, which is actually more than the amount purchased by Bitmine within the same period. However, the gap between the two is still too wide.

The post Bitmine Buys Another 27,000 ETH Despite Market Slump, Nears 5% of Ethereum Supply appeared first on CryptoPotato.

Crypto World

EBC12 Brings Europe’s Leading Digital Asset Leaders Together in Barcelona This September

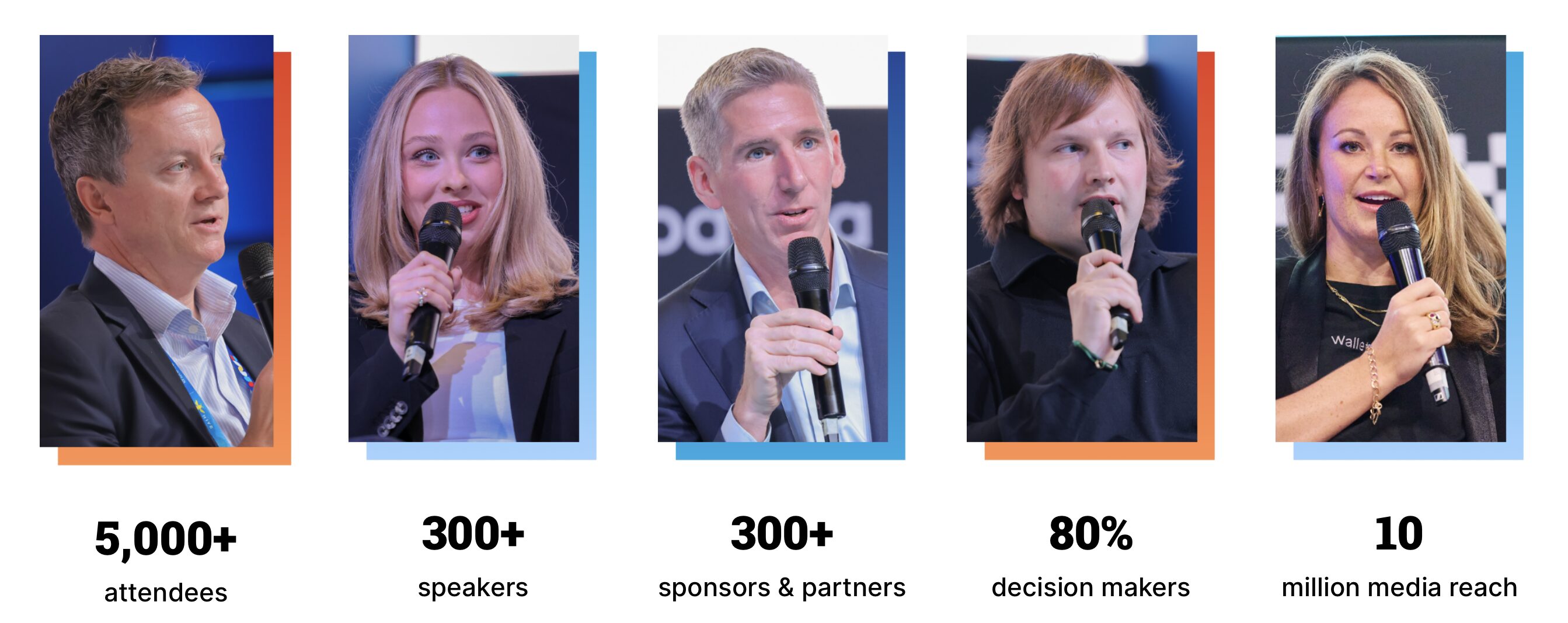

Institutional interest in digital assets continues to accelerate, and this September the industry’s key decision-makers will gather in Barcelona for the 12th European Blockchain Convention (EBC12).

Taking place on September 16–17, 2026, EBC12 will host 6,000+ attendees, 300+ speakers, and participants from more than 70 countries, creating one of Europe’s largest meeting points for blockchain, digital finance, and institutional crypto.

As an official media partner, we’re happy to share an exclusive 15% ticket discount. Register using the promo code SLR_15.

The Marketplace for Europe’s Digital Asset Economy

Rather than simply being another blockchain conference, EBC12 positions itself as the place where Europe’s fragmented digital asset ecosystem comes together.

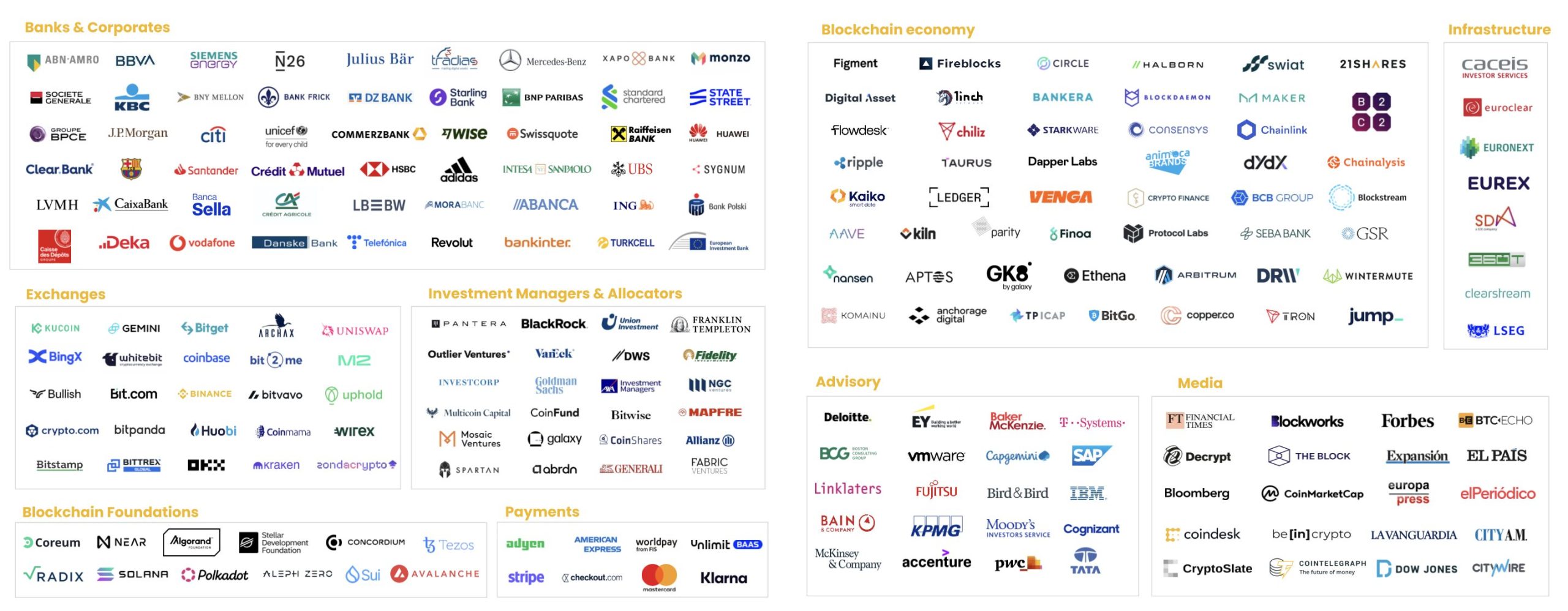

Banks, asset managers, venture capital firms, exchanges, custody providers, blockchain protocols, fintech companies, regulators, and institutional investors will meet to discuss the next stage of market development.

The conference comes at a pivotal moment following regulatory progress across Europe, increasing institutional participation, and growing adoption of tokenized financial products.

Key Themes for 2026

EBC12’s program explores the issues that matter most to institutional participants, including:

- Market infrastructure for institutional adoption

- Tokenization of real-world assets

- Stablecoin ecosystems and payment innovation

- MiCA and global regulatory developments

- AI-powered financial services

- Investment strategies for digital assets

- Cross-border market collaboration

The speaker lineup includes representatives from organizations such as BlackRock, Cardano, WisdomTree, Bitwise, Baillie Gifford, Zodia Custody, Hilbert Capital, Midchains, Caisse des Dépôts, and many more.

Why Attend?

Europe remains one of the world’s most dynamic digital asset markets, but opportunities are spread across multiple jurisdictions.

EBC12 creates a single venue where investors, institutions, entrepreneurs, and policymakers can build partnerships, explore investment opportunities, and stay ahead of industry developments.

Whether you’re raising capital, expanding internationally, or looking for strategic partners, Barcelona becomes the industry’s meeting point this September.

Secure your ticket today and receive 15% off with promo code SLR_15.

Learn more: https://eblockchainconvention.com/european-blockchain-convention-12/

Tickets: https://www.tickettailor.com/events/europeanblockchainconvention/1927550

Censorship of crypto assets has become so popular that a new dashboard is tallying the number of times companies have frozen tokens.

According to new tracker, stables.rip, two companies have frozen 3.7 billion stablecoins.

Although BTC as good as created the crypto industry as a protest against trusted intermediaries, stablecoins are more than twice as popular as BTC by trading volume.

By this measure, trusted intermediaries still maintain a majority share of power over most crypto transactions.

Despite crypto users being vaguely aware of these censorship practices as something nebulous, few could quantify its precise scope. This new tracker has helped turn an abstract reality into a specific quantity.

Alex Gladstein at the Human Rights Foundation pushed the headline into social media’s timeline on Friday, calling it a “Good reminder that while stables have utility they are not freedom money.”

Matt Odell remarked, “Two billion frozen in two years. Wild.”

Another widely shared comment contrasted stablecoin censorship with censorship-resistant BTC.

More crypto censorship than ever

The numbers behind the outrage are real.

Over the past six years, two stablecoin issuers have frozen approximately 3.7 billion coins on the Ethereum and Tron blockchains, censoring the power of those coins’ keyholders from moving them on-chain.

Worse, the trend has accelerated substantially. Of that six-year total, 2.8 billion tokens, or 75%, froze within the past two years.

Although the number and value of coins is known, it’s impossible to determine how many transactions were unilaterally prevented.

The two most popular stablecoins, for example, trade over $40 trillion annually in on- and off-chain trades against other assets, according to CoinMarketCap.

Tether and Circle, the respective issuers of USDT and USDC, maintain privileged administrative control over their own smart contracts.

At any time, they may add any wallet to a blacklist, forcing the tokens sitting in that wallet to stop moving until they lift the freeze.

Tether even goes a step further with a function named destroyBlackFunds, which lets it burn tokens outright.

Indeed, in 2025 alone, it incinerated $698 million of the $1.26 billion it froze that year.

Many other stablecoins, including the Trump family’s USD1, have similar powers to remotely freeze tokens.

Read more: Justin Sun represents 99.9% of blacklisted World Liberty tokens

Your keys, your coins, that someone else can censor

Stablecoin companies often justify their censorship due to governmental pressures, such as complying with a court order. They claim to be stopping money laundering or human trafficking.

Regardless, the point is that stablecoin companies simply have the power to decide on their own accord.

When the US Treasury sanctioned the privacy tool Tornado Cash in August 2022, Circle immediately froze roughly 75,000 USDC tokens to comply.

Tether, however, declined to follow suit, saying it wouldn’t act without a law enforcement order.

Its defiance didn’t last. By late 2023, Tether made a strategic bargain to onboard the US Secret Service and FBI, earning regulatory goodwill by freezing batches of addresses at their law enforcement officers’ requests.

In all, the power to censor stablecoin transactions is too useful and tempting to forego.

Tether’s USDT is worth $186 billion and Circle’s USDC about $74 billion, and these tokens transact by the tens of trillions annually.

The utility of stablecoins isn’t so much their permissionlessness as much as their selective permissiveness.

Mistakenly, many people believe crypto assets to be trustless and censorship resistant.

In stark contrast, 3.7 billion tokens have been remotely frozen by companies, with three-quarters of these censored tokens locked within the last two years.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

European Blockchain Convention 12 Returns to Barcelona as Europe’s Digital Asset Marketplace

The European Blockchain Convention (EBC12) returns to Barcelona on September 16–17, 2026, bringing together the institutions, investors, founders, and infrastructure providers shaping the future of digital assets.

Recognized as Europe’s Digital Asset Marketplace, EBC12 will welcome more than 6,000 attendees from over 70 countries, alongside 300+ speakers representing leading financial institutions, blockchain companies, investment firms, and regulators. The event offers a unique opportunity to meet the people driving the next phase of institutional crypto adoption—all under one roof.

As a media partner of EBC12, we’re pleased to offer our community an exclusive 15% discount on tickets. Use the code SLR_15 during registration.

Where Europe’s Digital Asset Industry Meets

The digital asset landscape has entered a new era. Following the approval of spot Bitcoin and Ethereum ETFs, the implementation of MiCA across the European Union, and growing institutional allocations to digital assets, the industry’s focus has shifted from adoption to execution.

EBC12 is designed to bring together the market participants making those decisions, including asset managers, banks, custodians, exchanges, blockchain protocols, venture capital firms, and policymakers.

What to Expect at EBC12

This year’s agenda focuses on the topics currently shaping global digital finance:

- Institutional investment strategies

- Digital asset regulation and MiCA implementation

- Real-world asset tokenization

- Stablecoins and CBDCs

- Institutional custody and market infrastructure

- AI applications across digital finance

- Capital allocation and market structure

Attendees will also have access to networking sessions, business meetings, exhibitions, startup showcases, and discussions with industry leaders from organizations including BlackRock, Cardano, Bitwise, WisdomTree, Baillie Gifford, Zodia Custody, Hilbert Capital, Midchains, and many others.

One Place. Two Days. Unlimited Opportunities.

Europe’s digital asset market remains highly fragmented across multiple financial centers. EBC12 bridges those markets by creating one environment where investors, founders, infrastructure providers, regulators, and institutions can connect efficiently.

What often requires months of meetings across different countries can happen over two productive days in Barcelona.

Register today and save 15% with the code SLR_15.

Registration: https://eblockchainconvention.com/european-blockchain-convention-12/

Ticket Discount: https://www.tickettailor.com/events/europeanblockchainconvention/1927550

The year 2026 has so far been an unforgiving one for gold. XAU/USD is down approximately 7% since the start of the year, and roughly 28% from the late-January peak — a significant correction, though a physiologically natural one following the sustained bullish rally of recent years.

Fundamental Picture

Several factors have converged to weigh on the precious metal. The Federal Reserve has maintained its restrictive stance, keeping interest rates elevated and reducing the appeal of a non-yielding asset like gold. Simultaneously, institutional portfolio rotation has forced financial players to liquidate a portion of the long positions accumulated during the bull run, amplifying selling pressure. Notably, even the US-Iran geopolitical tension — a scenario that would typically act as a tailwind for gold in its role as a so-called safe-haven asset — has failed to provide meaningful support, with the broader macro environment overriding the flight-to-safety narrative.

Technical Analysis of XAU/USD

Gold is currently navigating a bearish structure in the short-to-medium term, with price consistently reacting to a descending trendline drawn from the highs of early March, forming a clear sequence of lower highs and lower lows on the daily chart.

Price has now arrived at a technically and psychologically significant area: the $4,000 per ounce. This zone has demonstrated its relevance on multiple occasions in the past, and Thursday’s session (25 June) offered the first tentative signs of a reaction, with the daily candle closing in positive territory.

→ Bullish scenario: A sustained reaction from the $4,000 zone, accompanied by a confirmed break above the descending trendline — which converges with resistance in the $4,300–$4,380 area — would establish a new sequence of higher highs and open the door to a broader bullish recovery.

→ Bearish scenario: A decisive break below $4,000, followed by a retest and breach of recent lows, would confirm the continuation of the medium-term downtrend, potentially exposing the $3,400–$3,500 zone — a former major resistance that now acts as structural support.

Both scenarios remain open. Price action on the H4 and H1 timeframes will be key to determining gold’s next directional move in the sessions ahead.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Strategy Unveils Bitcoin Framework With $2.55B Cash Reserve

Riding wave of stellar starting pitching, Giants visit struggling D-backs

Are Michelin Wiper Blades Any Good? Here’s What Users Say

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Blockchain.com files with SEC for U.S. IPO

Brian Armstrong on Bitcoin, Anthropic Drops Fable 5 & Mythos 5, NewLimit’s $435M Age-Reversal | 264

Scharmine L Baker – Fraud Fumble – Financial Advisor Reacts

Financial Management | Class 12th | Business Studies | Part-2 | Easy Explanation |

-

Sports6 days ago

Sports6 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics3 days ago

Politics3 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics3 days ago

Politics3 days agoPotential 2028er World Cup attendee leaderboard

-

Business3 days ago

Business3 days agoAsia stock markets slide as tech shares slump

-

Tech4 days ago

Tech4 days agoA Look At A Gaggle Of Transputer Boards

-

News Videos19 hours ago

News Videos19 hours agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Crypto World5 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World4 days ago

Crypto World4 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World2 days ago

Crypto World2 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World2 days ago

Crypto World2 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Sports3 days ago

Sports3 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World3 days ago

Crypto World3 days agoRTX holders must register wallets before token distribution begins

-

Crypto World3 days ago

Crypto World3 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech2 days ago

Tech2 days agoRussian hackers now target Signal backup recovery keys

-

Sports4 days ago

Sports4 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Crypto World3 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

You must be logged in to post a comment Login