Crypto World

Nasdaq-Listed Riot Keeps Selling Bitcoin While Reinventing Its Business

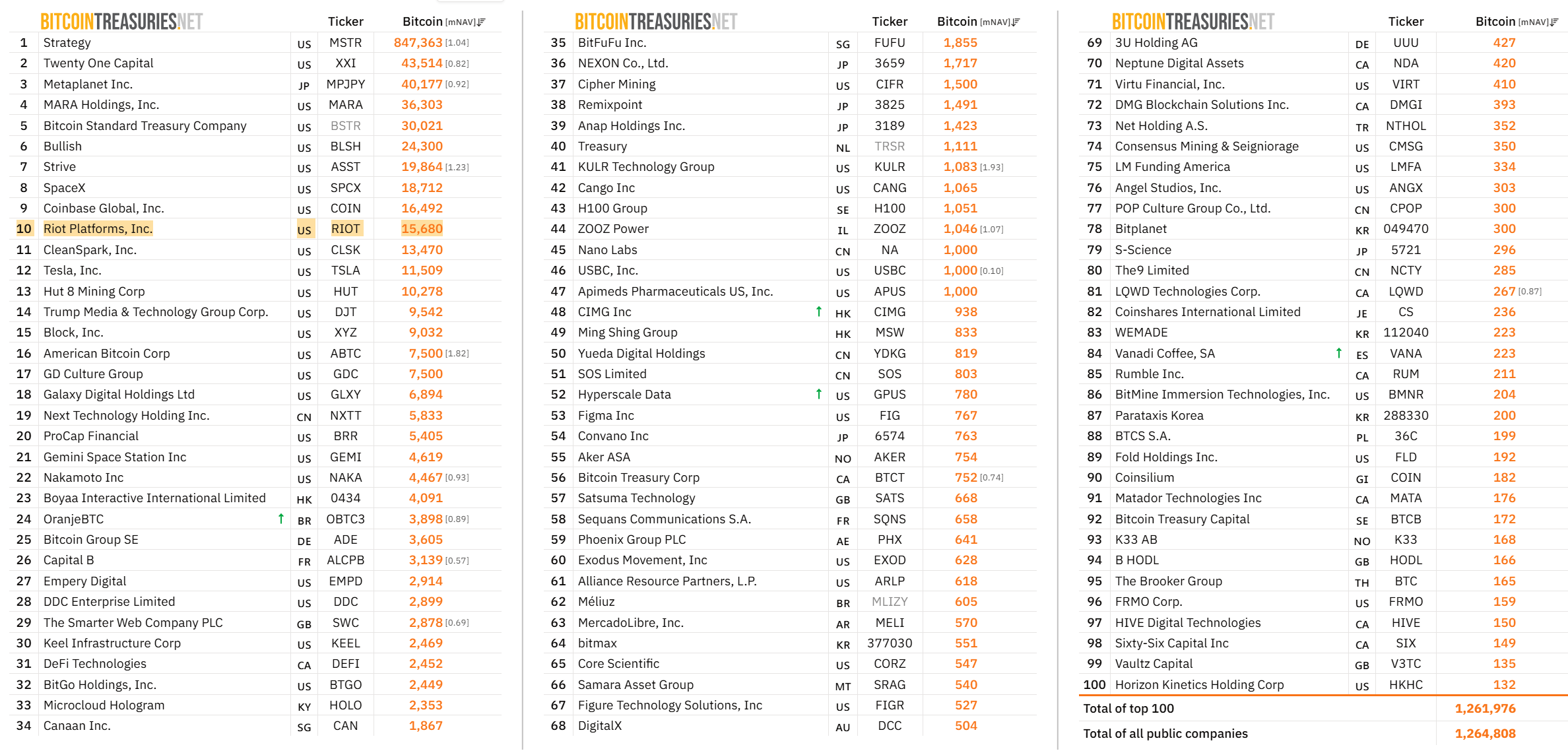

Bitcoin miner Riot Platforms (RIOT) has moved another 500 Bitcoin (BTC) to custody firm NYDIG, worth roughly $39 million, the latest move in a treasury strategy now funding its push beyond mining.

On-chain monitors spotted the deposit, which fits a familiar pattern. Riot has sold far more Bitcoin than it mines, converting its reserves into cash for a costly pivot into AI data centers.

A Familiar Pattern for Riot

Blockchain monitor Onchain Lens flagged the 500 BTC deposit on June 30. It mirrored a similar transfer that analytics firm Arkham tracked in early April. Such moves to custodians often precede sales.

The scale of the selling is striking. Riot disclosed selling 3,778 Bitcoin for $289.5 million last quarter, while mining just 1,473 coins. The first-quarter Bitcoin sell-off far outpaced production, draining the treasury.

Those sales cut holdings to about 15,680 BTC as of this writing, down 18% from a year earlier.

Other miners offloading Bitcoin have leaned on the same playbook. Rival MARA Holdings sold about $1.1 billion in Bitcoin this year, while Core Scientific began monetizing most of its coins.

Thinner margins since the 2024 halving have squeezed pure mining.

The Riot Bitcoin Sale Funds an AI Bet

The clearest link between the selling and the pivot came in January. Riot funded a $96 million land purchase at its Rockdale site in Texas entirely by selling about 1,080 Bitcoin.

That land now anchors a data center business. Anchor tenant AMD signed a 10-year lease worth about $311 million, then doubled its commitment to 50 megawatts last quarter. The segment brought in $33.2 million of revenue, its first contribution.

The economists explain the urgency. Once equipment depreciation is accounted for, Riot spent $96,283 to mine each Bitcoin last quarter, more than a Bitcoin was worth. It reported a net loss of about $500 million.

What the Sale Streak Signals

CEO Jason Les has cast the shift as a turning point rather than a retreat.

“The first quarter of 2026 marks a definitive inflection point for Riot, as we officially transitioned into an active, revenue-generating data center operator,” the miner’s CEO, Jason Les, said.

Follow us on X to get the latest news as it happens

Riot abandoned its long-standing hold-only policy in 2025 and now sells routinely. Still, the company has staked its future on tenants like AMD rather than on Bitcoin alone.

With Bitcoin trading near $58,700, Riot can still raise large sums from a shrinking treasury. The race for AI infrastructure has rewarded that bet, with miner stocks climbing even as mining margins fade.

The coming quarters will test whether data center income can replace what mining once delivered.

The post Nasdaq-Listed Riot Keeps Selling Bitcoin While Reinventing Its Business appeared first on BeInCrypto.

Hollywood director Carl Rinsch has been sentenced to two and a half years in prison for defrauding Netflix out of $11 million, which he spent on crypto, stocks and luxury goods.

A Manhattan federal court on Monday sentenced Rinsch, known for directing the 2013 film “47 Ronin,” starring Keanu Reeves, to 30 months in prison after he was convicted in December on charges including fraud and money laundering.

“Rinsch orchestrated a scheme to steal millions by seeking $11 million from a subscription streaming service, falsely claiming that money would be used to finance a television show that he was creating,” Manhattan US Attorney Jay Clayton said in a statement Monday.

“Instead of using the money to make the show, Rinsch made risky bets on highly speculative stock options and cryptocurrency, and spent millions of dollars on luxury goods for himself,” Clayton added. “Today’s sentence sends a deterrent message: fraud will not be tolerated.”

Rinsch’s sentence was far below the maximum possible prison time of 90 years he was facing for his seven total charges, to which he pleaded not guilty. His defense also argued that he suffered from mental health issues.

The sentence brings to a close a 15-month saga after Rinsch was arrested in March 2025 for defrauding what prosecutors referred to in court documents as “Streaming Company-1,” which multiple reports have identified as Netflix.

Source: US Attorney SDNY

Rinsch makes $27 million on Dogecoin bet

According to a March 2025 indictment and a November 2023 New York Times report on a confidential arbitration proceeding between Netflix and Rinsch, the company initially gave Rinsch $44 million for his sci-fi show “White Horse,” later renamed “Conquest,” but he asked for more funds to finish the show, prompting Netflix to wire an additional $11 million in March 2020.

Rinsch used $10.5 million from the fresh funding to gamble on the stock market and quickly lost about half of it in a few weeks by trading options on pharmaceutical companies and the S&P 500.

Rinsch transferred more than $4 million in remaining funds to crypto exchange Kraken and went all in on the memecoin Dogecoin (DOGE), a bet that ultimately generated around $27 million when he liquidated in May 2021, according to an account statement seen by The Times.

Carl Rinsch giving an interview in 2013 for his feature directorial debut film 47 Ronin. Source: YouTube

With the DOGE winnings, Rinsch then spent about $10 million on personal expenses and luxury goods, including $1.8 million on credit card bills, $1 million on lawyers to sue Netflix, $3.8 million on furniture and antiques, $2.4 million on five Rolls-Royces and a Ferrari, and $652,000 on watches and clothes, according to the indictment.

Related: Onchain, in court: What happened in crypto legal news this week

Rinsch never finished the show or returned the funds Netflix provided to complete it.

Prosecutors asked for five years

Rinsch was convicted of one count each of wire fraud and money laundering, each carrying a maximum sentence of 20 years in prison, along with five counts of making monetary transactions in property derived from unlawful activity, each carrying a maximum of 10 years.

Prosecutors asked the court in a mid-June sentencing memo to give Rinsch five years in prison after he argued for a sentence without prison time.

Rinsch’s defense said he suffered from mental health issues, with friends and family members writing to the court to say that his behavior changed around the time of the offenses. Keanu Reeves also wrote to the court in support of Rinsch.

In addition to his two-and-a-half-year prison term, Rinsch was sentenced to three years of supervised release, $11 million in forfeiture and $700 in mandatory special assessments.

Magazine: China’s 107 Bitcoin memory thief, Bithumb CEO booked: Asia Express

A $1,000 bet on the S&P 500 in July 2021 now beats the same bet on Bitcoin (BTC). Stocks won even though Bitcoin took the wilder ride.

Many proponents of Bitcoin have pointed to the digital’s asset’s performance against traditional investment vehicles over the years. However, with Bitcoin now way below 50% of its all time high, more steady investments are overtaking.

The Numbers

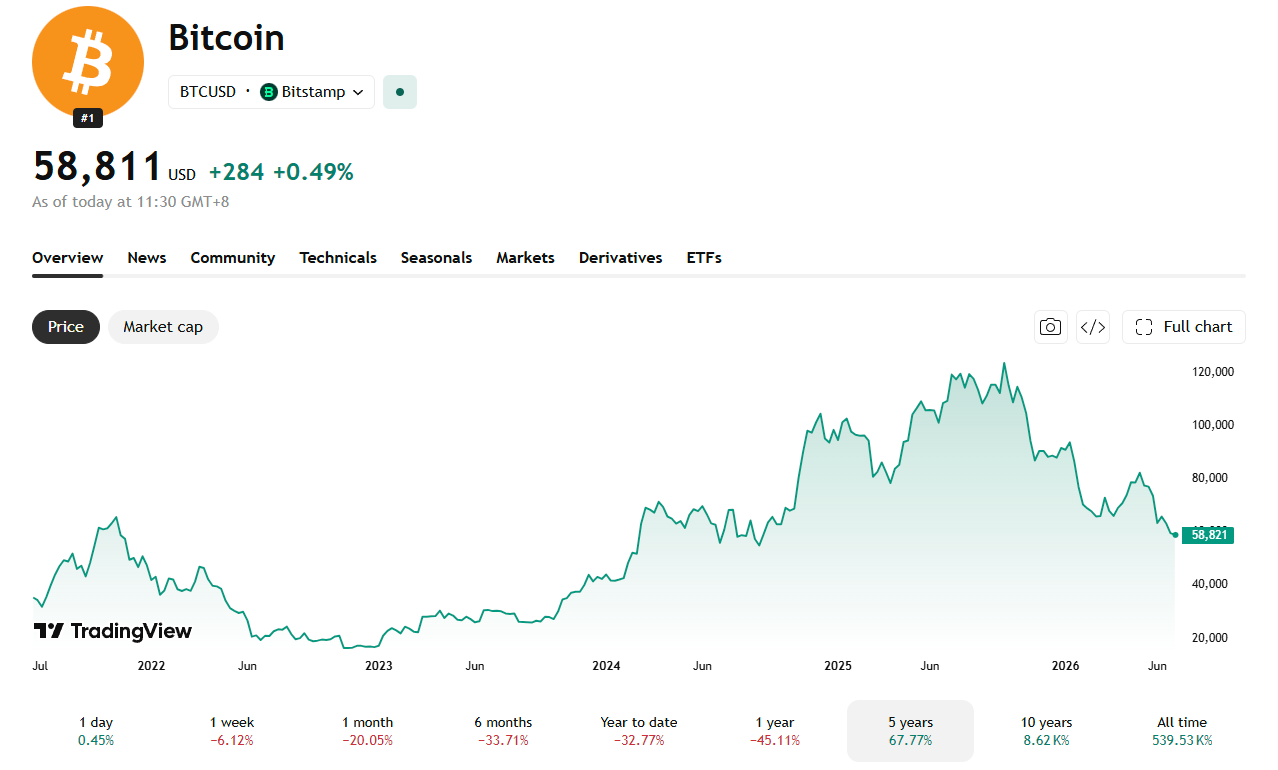

Bitcoin closed at $35,171 on July 1, 2021. It sits at around at $58,811 as of writing. That marks a gain of about 68%.

The S&P 500 closed at 4,319.94 on July 1, 2021. It closed at 7,499.36 on June 30, 2026. That marks a gain of about 74%.

A $1,000 stake in the S&P 500 grew to roughly $1,736. The same $1,000 in Bitcoin grew to roughly $1,676. Stocks came out around $60 ahead.

Stocks Won With a Much Smoother Ride

Bitcoin’s return looks unremarkable next to the risk it carried. Bitcoin rallied to nearly $69,000 in November 2021. It then crashed below $17,000 during the 2022 crypto winter. It surged past $120,000 in 2025 then slid back below $60,000 most recently.

The S&P 500 never came close to that kind of swing. Its worst drawdown in the same stretch hit about 25% in 2022, a fraction of Bitcoin’s peak-to-trough loss.

Bitcoin has beaten the index by far wider margins over longer stretches. Back in 2019, BeInCrypto reported a 250,000% Bitcoin gain since 2011, against a 147% gain for the S&P 500 over the same span.

This time, Bitcoin’s extra volatility didn’t pay off. Investors took on far more risk and still finished behind stocks.

The post $1,000 in Bitcoin or S&P 500 in 2021? Stocks Payout More Today appeared first on BeInCrypto.

The ETH/BTC ratio prices Ethereum in Bitcoin instead of dollars, stripping out the market-wide move so you can see which of the two is actually winning. Here is what the ratio measures, how to read it, what drives it, and why it has fallen to multi-year lows.

Summary

- The ETH/BTC ratio is the price of one ether expressed in bitcoin, a single number that shows whether Ethereum is outperforming or underperforming Bitcoin regardless of what the dollar price of either is doing.

- A rising ratio means ether is gaining on bitcoin, often a sign of risk appetite and a healthier environment for altcoins; a falling ratio means bitcoin is winning, usually a sign of caution and bitcoin dominance.

- As of mid-2026, the ratio sits near multi-year lows around 0.026, reflecting Ethereum’s deep underperformance against Bitcoin, down sharply from levels near 0.08 in 2021 and 0.15 in 2017.

- The ratio is driven by the tug-of-war between Ethereum-specific forces (ETF flows, staking, layer-2 activity, supply dynamics, competition from other chains) and Bitcoin-specific forces (halving cycles, ETF and treasury demand).

- It is a relative-strength gauge and a regime signal, not a price target, and it can stay depressed or elevated for years, so it should inform context rather than dictate trades.

The ETH/BTC ratio is the price of one ether (ETH) measured in bitcoin (BTC) rather than in dollars, and it is one of the most useful single numbers in crypto for understanding which of the two largest assets is actually winning. When you look at Ethereum’s price in dollars, you are seeing two things mixed together: how Ethereum is doing, and how the entire crypto market is doing, because almost everything in crypto moves loosely with Bitcoin and with the broad risk environment.

The ETH/BTC ratio removes the second factor. By pricing Ethereum directly in Bitcoin, it cancels out the market-wide move that both assets share and isolates Ethereum’s performance relative to Bitcoin alone. If both assets rise 20% in dollars, the ratio does not move, because neither outperformed the other. If Ethereum rises while Bitcoin is flat, the ratio rises, and you learn something the dollar chart obscured: capital is favoring Ethereum over Bitcoin right now.

That makes the ratio a lens, not just a number, and learning to read it changes how you see the market. This guide explains what the ETH/BTC ratio is and how it is calculated, why traders watch it, how to interpret a rising or falling ratio, what the ratio has done historically and where it sits now, the forces on each side that push it up or down, a worked example you can follow step by step, and how to use it sensibly without overreading it.

The aim is to give you a durable mental model rather than a snapshot, because the specific level will change, but the way the ratio works will not. None of this is trading advice; the ratio is an analytical tool, and like any tool, it can mislead if used in isolation. Used well, though, it is one of the clearest windows into the single most important relationship in the asset class, the one between its two dominant coins.

What the ratio actually measures

Start with the mechanics, because they are simple and the simplicity is the point. The ETH/BTC ratio is calculated by dividing the price of ether by the price of bitcoin, using the same currency for both, so the units cancel and you are left with a pure ratio. If ether trades at $1,550 and bitcoin trades at $60,000, the ratio is 1,550 divided by 60,000, which is about 0.0258, usually written as 0.026. That number tells you that one ether is currently worth about 2.6% of one bitcoin. You can read it directly: at a ratio of 0.026, it takes roughly 38 ether to equal one bitcoin in value.

Most charting platforms quote the pair as ETHBTC or ETH/BTC, and many crypto exchanges let you trade the pair directly, buying ether with bitcoin or the reverse, which is part of why the ratio is so closely watched, it is a live, tradable market, not just a derived statistic.

What the ratio measures, conceptually, is relative strength. It answers a question the dollar price cannot: between the two largest assets in crypto, which is the market choosing right now? Because Bitcoin and Ethereum share most of the same macro drivers, interest rates, risk appetite, regulatory news, dollar liquidity, comparing them to each other holds those shared factors roughly constant and exposes the difference that is specific to each asset. A dollar chart of Ethereum during a broad sell-off shows Ethereum falling, but it cannot tell you whether Ethereum fell more or less than Bitcoin.

The ratio can. If Ethereum fell harder than Bitcoin, the ratio dropped even as both went down, revealing that within the decline, capital preferred the relative safety of Bitcoin. That is the core value of the metric: it separates Ethereum’s own story from the market’s story, and in doing so it often reveals the direction of capital rotation that the dollar price hides.

Why traders watch it

The ratio matters because it functions as a regime indicator for the broader market, not just for Ethereum. In crypto, there is a long-observed pattern in which capital rotates in a rough sequence: money flows into Bitcoin first during the early, cautious phase of a rally, then rotates into Ethereum as confidence grows, and then spreads out into smaller altcoins as risk appetite peaks.

Because Ethereum sits in the middle of that sequence, the largest and most established asset after Bitcoin, the ETH/BTC ratio often acts as a barometer for where the market is in that cycle. A rising ratio, with Ethereum gaining on Bitcoin, frequently signals that risk appetite is building and that the environment is turning favorable for altcoins broadly, since Ethereum tends to lead the alt market. A falling ratio, with Bitcoin winning, usually signals the opposite: caution, a flight toward the relative safety of Bitcoin, and a harder environment for smaller tokens.

This is why traders treat the ratio as a piece of market-structure information instead of just a fact about two coins. When the ratio is trending up, many interpret it as confirmation of an “altcoin season” or “ETH season,” a period when capital is willing to move out the risk curve and non-Bitcoin assets outperform. When it is trending down, the read is “Bitcoin season” or rising “Bitcoin dominance,” a period when Bitcoin absorbs the market’s attention and capital while alts bleed against it. Portfolio decisions follow from this framing: a trader who believes the ratio is turning up might tilt toward Ethereum and altcoins, while one who sees it falling might rotate toward Bitcoin or cash.

The ratio also serves as a sanity check on narratives. If commentators are loudly predicting an Ethereum breakout but the ETH/BTC ratio keeps falling, the market is voting against the narrative in the most direct way available, by pricing Ethereum lower against Bitcoin quarter after quarter. Watching the ratio keeps a trader honest about what is actually happening versus what is being talked about.

How to read a rising or falling ratio

Reading the ratio is mostly about direction and context instead of any single absolute level. A rising ETH/BTC ratio means ether is appreciating relative to bitcoin, whether because ether is rising faster than bitcoin, falling more slowly, or rising while bitcoin falls. In all of those cases the message is the same: on a relative basis, the market is favoring Ethereum.

Sustained increases in the ratio tend to coincide with periods of broad risk appetite, strong Ethereum-specific catalysts, and outperformance across the altcoin complex, since Ethereum often pulls the alts along with it. A falling ratio carries the opposite message: bitcoin is winning the relative contest, the market is leaning toward caution and Bitcoin dominance, and altcoins are generally struggling against bitcoin even if they are flat or rising in dollar terms.

The crucial discipline is to read the ratio in context instead of as a standalone buy or sell signal. The same ratio level can mean very different things depending on the trend and the backdrop. A ratio of 0.026 reached on the way down, after months of Ethereum underperformance, signals weakness and momentum against Ethereum. The same 0.026 reached on the way up, after a period of Ethereum gaining, would signal the opposite, recovering relative strength.

Direction and trend matter more than the absolute figure. It also helps to watch the ratio across multiple timeframes: a short-term bounce in the ratio within a long-term downtrend is a different and weaker signal than a multi-month trend change. And because the ratio is relative, it is silent about absolute price. The ratio can rise while both assets fall in dollars, if Ethereum falls less, which is relative outperformance during an absolute loss, useful to know but not the same as a gain. Reading the ratio well means always holding two questions at once: which asset is winning the relative contest, and what is the absolute market doing underneath that contest.

A worked example

Make it concrete with numbers you can follow. Suppose ether is trading at $1,550 and bitcoin at $60,000. Divide 1,550 by 60,000 and you get 0.0258, so the ETH/BTC ratio is about 0.026, and one ether is worth roughly 2.6% of one bitcoin, or equivalently it takes about 38 ether to equal one bitcoin. Now run three scenarios from that starting point to see how the ratio responds to relative moves.

In the first scenario, both assets rise 25% in dollars: ether to about $1,938 and bitcoin to $75,000. The ratio is 1,938 divided by 75,000, which is still about 0.0258. Despite a large dollar gain in both, the ratio did not move, because neither outperformed the other, exactly the information the dollar chart would have hidden.

In the second scenario, ether outperforms: ether doubles to $3,100 while bitcoin stays at $60,000. The ratio becomes 3,100 divided by 60,000, or about 0.052, a doubling of the ratio. This is the signature of Ethereum outperformance, and a trader watching only the ratio would see it climb from 0.026 to 0.052 and read a strong shift of capital toward Ethereum, the kind of move associated with an ETH-led alt rally. In the third scenario, the market falls but Ethereum falls harder: bitcoin drops to $48,000 (down 20%) while ether drops to $1,085 (down 30%).

The ratio is 1,085 divided by 48,000, or about 0.0226, a decline from 0.026. Here both assets lost money in dollars, but the ratio fell, telling you that within the sell-off, capital preferred bitcoin and Ethereum bore more of the damage. These three cases show the ratio’s whole purpose in miniature: it ignores the shared move and reports only the relative winner, which is the piece of information that dollar prices alone cannot give you.

Where the ratio has been, and where it is now

History gives the current level its meaning, and the history of ETH/BTC is a story of a long round trip. In Ethereum’s earlier years the ratio climbed dramatically as Ethereum established itself as the clear number-two asset and the home of smart contracts, decentralized finance, and much of crypto’s developer activity. It reached its highest levels around mid-2017, near 0.15, when one ether was worth about 15% of a bitcoin, a peak of Ethereum’s relative strength driven by the initial-coin-offering boom that ran on Ethereum.

The ratio then fell sharply, recovered into the 2021 cycle to peak around 0.08 as decentralized finance and non-fungible tokens drove enormous activity on Ethereum, and has since entered a prolonged decline. As of mid-2026, the ratio sits near multi-year lows around 0.026, with ether near $1,550 against bitcoin near $60,000, a level that reflects a sustained stretch of Ethereum underperforming Bitcoin.

The reasons for the long decline are worth understanding because they explain why the ratio is where it is instead of simply that it is low. Several forces have weighed on Ethereum’s relative strength. Bitcoin has captured an enormous wave of institutional demand through spot ETFs and corporate-treasury adoption, a clean, simple “digital gold” narrative that has pulled capital toward Bitcoin specifically. Ethereum, meanwhile, has faced intensifying competition from faster, cheaper chains, with much of the speculative and developer energy that once flowed to Ethereum moving to rivals, which has diluted the “Ethereum is the only smart-contract platform that matters” thesis that powered its earlier outperformance.

Ethereum’s own narrative has also been harder to summarize than Bitcoin’s, shifting across staking, scaling through layer-2 networks, and supply dynamics in ways that are powerful but complex, and complexity is a disadvantage in a market that rewards simple stories. The result is a ratio that has spent a long time grinding lower, which is the context any reader should hold when they see the current figure: it is not a momentary dip but the late stage of a multi-year trend, which is exactly why it is so closely watched for signs of a turn.

What drives the ratio up and down

To anticipate the ratio instead of just observe it, you have to understand the forces on each side, because the ratio is a tug-of-war between Ethereum-specific and Bitcoin-specific drivers. On the Ethereum side, the factors that tend to push the ratio up include strong inflows into Ethereum ETFs, which signal institutional demand specifically for ether; growth in staking, which locks up supply and can tighten the available float; rising activity on Ethereum and its layer-2 networks, which supports the case that the network is being used; and periods when Ethereum’s supply dynamics turn deflationary, reducing net issuance. Broadly, anything that strengthens Ethereum’s relative narrative or tightens its supply relative to Bitcoin tends to lift the ratio. When these forces are strong and Bitcoin lacks an equally strong catalyst, capital rotates toward Ethereum and the ratio climbs.

On the Bitcoin side, the factors that push the ratio down include the four-year halving cycle and its associated demand narratives, large institutional inflows into Bitcoin ETFs, corporate-treasury accumulation of Bitcoin, and any environment in which the market wants the relative safety and simplicity of Bitcoin over the complexity of Ethereum and altcoins. Risk-off conditions generally favor Bitcoin and pull the ratio down, because in a cautious market capital concentrates in the most established, most liquid, most narratively simple asset, which is Bitcoin.

The overall risk environment is the backdrop to both sides: in risk-on periods, capital is willing to move out the curve toward Ethereum and the ratio tends to rise, while in risk-off periods it retreats toward Bitcoin and the ratio tends to fall. This framework explains why the ratio has been weak: Bitcoin has enjoyed powerful, simple, institution-friendly catalysts in ETFs and treasuries, while Ethereum’s catalysts have been real but more diffuse, and much of the market has been in a cautious, Bitcoin-favoring posture. A durable turn in the ratio would require Ethereum-specific demand to outweigh Bitcoin’s, which is exactly what traders watch the ratio to detect.

How to use the ratio without overreading it

For all its usefulness, the ratio is easy to misuse, and using it well means respecting its limits. The most important discipline is to remember that the ratio is a relative-strength gauge, not a price target or a guaranteed mean-reverting signal. A common error is to look at a depressed ratio and assume it must bounce back toward old levels, treating the multi-year average as a magnet.

There is no rule that forces the ratio to revert. It can stay depressed for years if Ethereum continues to underperform, just as it can stay elevated during a strong Ethereum cycle, and betting on reversion simply because the ratio looks low has cost many traders dearly through long stretches of continued underperformance. The ratio describes the current balance of relative strength; it does not promise that the balance will swing back on any particular schedule.

The second discipline is to never trade the ratio in isolation. It is one input among many, most powerful when combined with an understanding of the absolute market environment, the specific catalysts on each side, and your own time horizon. The ratio tells you which asset is winning the relative contest, but it says nothing about whether the whole market is heading up or down in dollars, which is what actually determines whether you make or lose money in absolute terms.

A rising ratio in a collapsing market still means losses; a falling ratio in a soaring market can still mean gains. The ratio is best used to inform allocation tilts and to read market structure, for example to judge whether the environment favors Ethereum and alts or Bitcoin, instead of as a standalone entry or exit trigger. Treat it as a compass that shows direction of relative capital flow, not a clock that tells you when to act, and it becomes one of the more reliable instruments in a crypto analyst’s toolkit. Misread as a precise timing signal or a guaranteed reversion bet, it becomes a trap. The metric is honest; the overreading is the danger.

Frequently Asked Questions

What is a good ETH/BTC ratio?

There is no single “good” level, because the ratio is a relative measure whose meaning depends on trend and context instead of any fixed number. Historically the ratio has ranged from highs near 0.15 in 2017 and 0.08 in 2021 down to multi-year lows around 0.026 in 2026. A higher ratio reflects stronger Ethereum performance against Bitcoin, and a lower one reflects Bitcoin dominance, but neither is inherently “good” or “bad,” it depends on which asset you favor and where you are in the cycle. What matters more than the absolute level is the direction: a rising ratio signals Ethereum gaining, a falling ratio signals Bitcoin winning. Read the trend and the backdrop, not a target number.

How do you calculate the ETH/BTC ratio?

Divide the price of ether by the price of bitcoin, using the same currency for both so the units cancel. For example, if ether is $1,550 and bitcoin is $60,000, the ratio is 1,550 divided by 60,000, which equals about 0.0258, usually written as 0.026. That means one ether is worth roughly 2.6% of one bitcoin, or that it takes about 38 ether to equal one bitcoin. Most charting platforms display the pair directly as ETHBTC or ETH/BTC, so you rarely need to calculate it by hand, and many exchanges let you trade the pair directly, which is why it behaves as a live market instead of just a derived statistic.

What does a rising ETH/BTC ratio mean?

A rising ratio means ether is appreciating relative to bitcoin, whether because ether is rising faster, falling more slowly, or rising while bitcoin is flat or falling. The shared message is that the market is favoring Ethereum over Bitcoin on a relative basis. Sustained increases often coincide with broad risk appetite and outperformance across altcoins, since Ethereum tends to lead the alt market, which is why a rising ratio is frequently read as a signal of “ETH season” or a building altcoin rally. The key caveat is that a rising ratio describes relative strength only; it says nothing about whether the overall market is going up or down in dollar terms.

Why has the ETH/BTC ratio been falling?

The long decline reflects a tug-of-war that Bitcoin has been winning. Bitcoin has captured a powerful wave of institutional demand through spot ETFs and corporate treasuries, supported by a simple “digital gold” narrative. Ethereum has faced intensifying competition from faster, cheaper chains that drew away speculative and developer activity, while its own narrative, spanning staking, layer-2 scaling, and supply dynamics, has been harder to summarize than Bitcoin’s. A generally cautious, risk-off market has also favored Bitcoin’s relative safety. The combination pushed the ratio to multi-year lows near 0.026 by mid-2026. A durable turn would require Ethereum-specific demand to outweigh Bitcoin’s catalysts.

Can the ETH/BTC ratio predict altcoin season?

It is one of the more useful indicators for it, but not a precise predictor. Because Ethereum sits between Bitcoin and smaller altcoins in the typical rotation of capital, the ETH/BTC ratio often acts as a barometer: a rising ratio suggests capital is moving out the risk curve toward Ethereum and, by extension, toward altcoins, while a falling ratio suggests retreat toward Bitcoin. Many traders treat a sustained uptrend in the ratio as confirmation that an altcoin season is building. However, it is a relative-strength gauge, not a guarantee, and it should be combined with other signals and an understanding of the absolute market, instead of treated as a standalone forecast of when alts will run.

Should I trade based on the ETH/BTC ratio?

The ratio is best used as an analytical and allocation tool instead of a standalone trading trigger, and this is not trading advice. It is most valuable for understanding market structure, judging whether the environment favors Ethereum and altcoins or Bitcoin, and informing how you tilt a portfolio, instead of as a precise entry or exit signal. Two cautions matter most: do not assume a low ratio must revert to old highs, because it can stay depressed for years, and never read it in isolation, because it says nothing about whether the overall market is rising or falling in dollars. A rising ratio in a falling market still means losses. Use it as a compass for relative strength, combined with other analyses.

This article is educational information, not financial or investment advice. Price levels and ratio figures reflect approximate values as of June 2026 and change continuously. Cryptocurrency is volatile, and you can lose money. Do your own research and consult a qualified financial professional before making any investment decision.

MetaMask has launched Money Account, a self-custodial stablecoin account on Monad that combines automated yield of up to 4% variable APY, direct spending, and integrated trading through a single balance.

Summary

- MetaMask launched Money Account on Monad, combining automatic yield, spending, and trading through a single self custodial balance.

- Supported stablecoins can be converted into mUSD at one to one parity, with balances earning up to 4% variable APY after users opt in.

- The launch expands MetaMask beyond trading after its recent Agent Wallet rollout, adding everyday payments and savings features to the wallet.

According to a press release shared with crypto.news, the new product lets MetaMask users convert supported stablecoins into MetaMask’s mUSD stablecoin and begin earning returns immediately without staking, lockup periods, minimum balances, or manual fund transfers. The company said the service is available globally in eligible jurisdictions, excluding the UK and certain restricted regions.

Money Account brings together functions that previously required separate platforms. Users can earn yield through decentralized finance protocols, spend funds through the MetaMask Card, and access MetaMask’s trading tools, including swaps, perpetual futures, and prediction markets, without moving assets between different accounts.

Consensys said mUSD is backed one to one by U.S. dollars and short-term U.S. Treasury bills held in regulated custody by Bridge, a Stripe company, while the stablecoin runs on M0’s infrastructure. The company added that users retain control of their private keys, meaning MetaMask cannot freeze or move customer funds.

Money Account runs on Monad

Built on the Monad blockchain, Money Account uses sponsored gas fees, allowing users to manage balances, earn yield, and make payments without paying network transaction costs, according to the announcement. Consensys said Monad’s sub second finality and stable transaction costs support the product’s real time payment and settlement experience.

Supported stablecoins, including USDC, USDT, DAI, aUSDC, aUSDT, and aDAI on supported networks, can be converted into mUSD instantly at one-to-one parity without conversion fees. Users can also buy mUSD directly with debit cards, credit cards, or Apple Pay.

After users opt in, funds are allocated through third-party smart contract vaults managed by Veda and curated by Steakhouse Financial. Consensys said the launch version routes funds into Morpho, while Aave markets will be added later. The company stated that balances can earn up to 4% variable APY after fees, with returns updating continuously inside the account.

For payments, the Money Account connects directly to the MetaMask Card where available. Purchases settle automatically from the account balance without additional conversion steps, while eligible spending earns up to 3% cashback in mUSD that is deposited back into the account, according to Consensys.

“Money Account is what it looks like when self-custodial finance stops asking people to choose between control and convenience and starts delivering both. MetaMask is financial agency for everyone. Money Account makes financial agency even more powerful and valuable,” said Joe Lubin, Founder and CEO of Consensys and Co-Founder of Ethereum.

MetaMask expands beyond wallet features

The launch comes weeks after MetaMask introduced an early access version of Agent Wallet, a self custodial product that allows artificial intelligence agents to execute crypto transactions under user-defined permissions across Ethereum compatible networks and Hyperliquid.

At the time, Consensys said Agent Wallet was built with spending limits, transaction simulations, Blockaid security monitoring, and user approval controls to let AI agents perform tasks such as token swaps, perpetual futures trading, liquidity provision, and prediction market activity while keeping final authority with users.

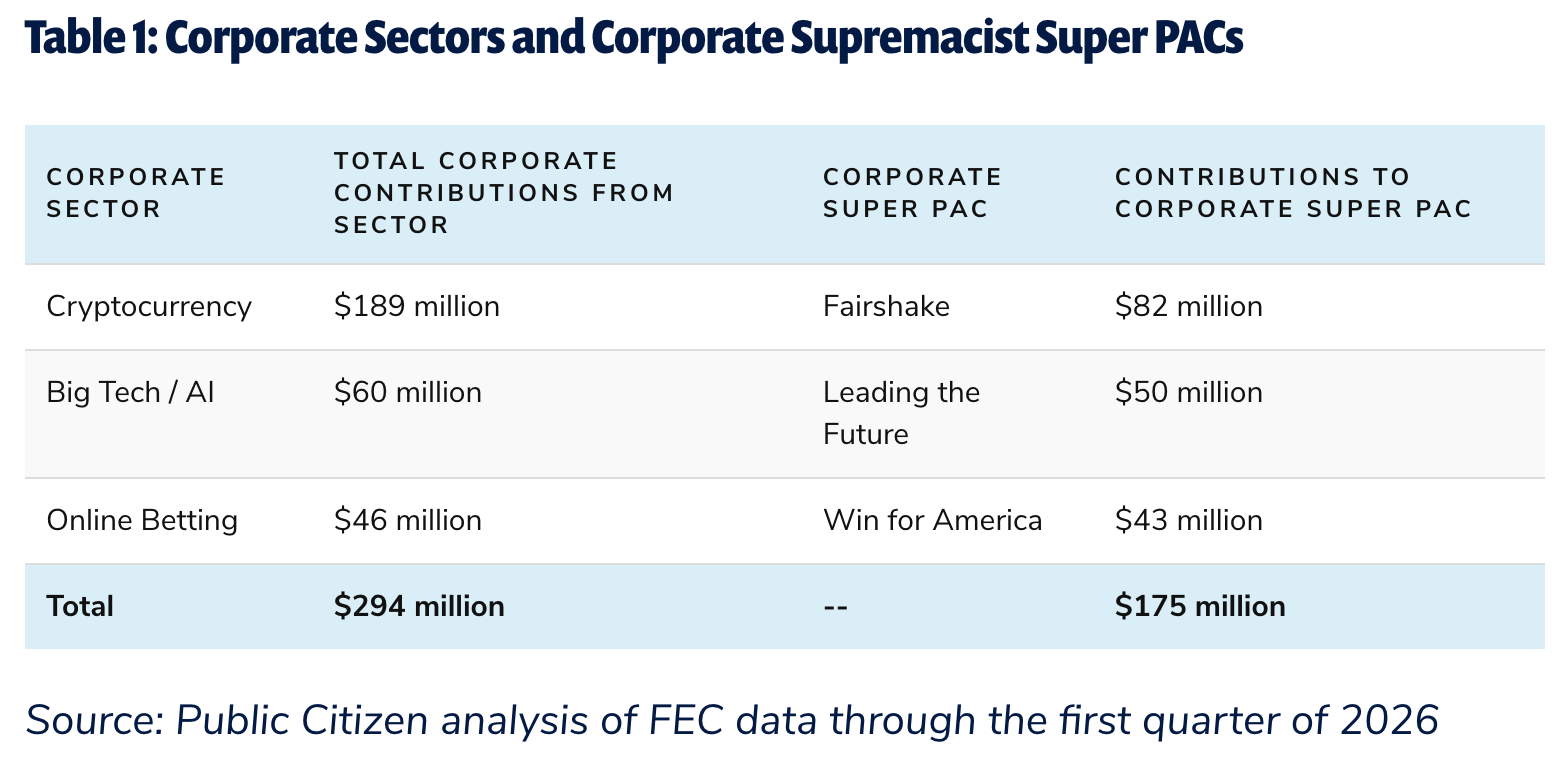

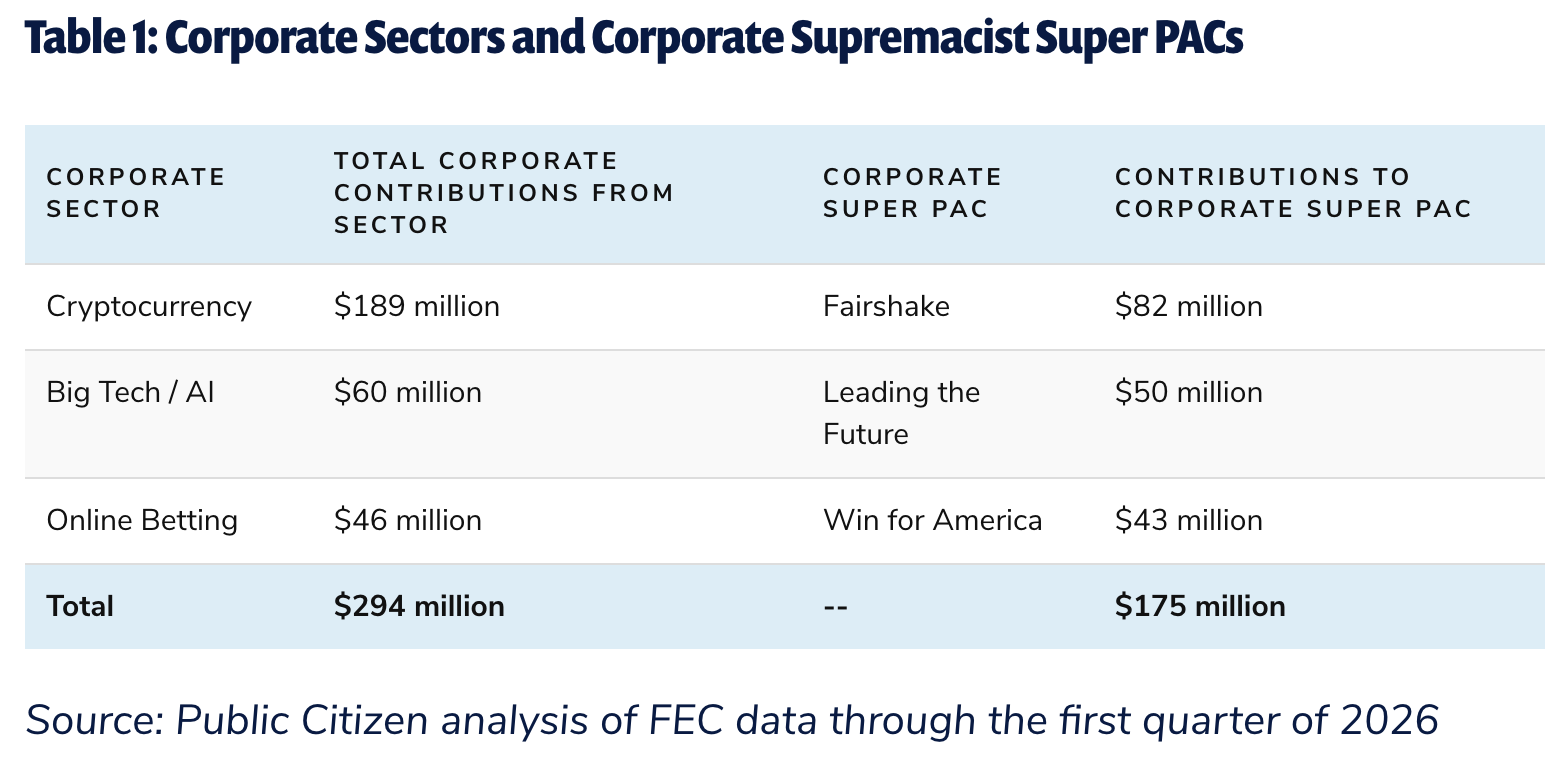

The US consumer advocacy group Public Citizen on Tuesday reported that the cryptocurrency industry had contributed $189 million toward the 2026 election cycle, following its 2024 playbook.

According to a report released Tuesday, the nonprofit organization said that about 37% of all corporate contributions in the 2026 US election cycle could be traced to crypto companies, totaling about $189 million so far, with more than four months until the November election.

While the watchdog group said that the crypto-aligned political action committee (PAC) Fairshake was responsible for spending more than $82 million so far, the MAGA Inc. Super PAC, largely backed by Crypto.com, had spent more than $56 million.

“These super PACs prioritize the interests of their business backers over either major political party or any candidate,” said Public Citizen. “Following the crypto playbook, they are set up to engage in both Democratic and Republican primaries and to support or attack candidates of either major party in the general election.”

Source: Public Citizen

Fairshake and its affiliates Defend American Jobs and Protect Progress are backed by cryptocurrency companies Coinbase and Ripple, and reported a $193 million war chest as of January. Entities aligning with industry interests have also been formed since 2024, including the Fellowship PAC backed by Cantor Fitzgerald.

Altogether, the PACs’ combined spending has already exceeded that in 2024, when companies contributed $170 million toward electing what it considered “pro-crypto” candidates to Congress.

Related: Senate leaders push for July passage of CLARITY Act

Cointelegraph reached out to a Fairshake spokesperson for a comment on the report but did not receive an immediate response.

Colorado primaries flush with crypto PAC cash

Colorado voters head to the polls today in primaries for Republican and Democratic candidates, with the state’s 8th congressional district potentially being influenced by crypto PAC spending.

The You Can Push Back Super PAC backed by Ripple Labs co-founder Chris Larsen reportedly spent $1 million on media to support Democrat Manny Rutinel. The committee’s last big bet — $3.3 million — was on Democrat Alex Bores in New York’s 12th Congressional District. He lost his primary last week to Micah Lasher, who had criticized Larsen’s involvement in the race.

Magazine: SBF will never get a pardon, Trump peace deal boosts Bitcoin: Hodlers Digest June 14-21

Nearly 1,700 investors in the United Kingdom have reportedly launched legal action against Binance and its founder, Changpeng Zhao, seeking £150 million (about $200 million). The claim alleges that Binance offered and sold crypto derivatives—including leverage tokens, futures contracts, and options—without the regulatory approval required under UK law.

According to the law firm KP Law, the case focuses on alleged violations of the Financial Services and Markets Act 2000 and on the continued availability of these products after the UK Financial Conduct Authority (FCA) banned them from being offered to retail customers in January 2021. Binance, for its part, says it will defend itself through the legal process and asserts it remains committed to operating in line with applicable law.

Key takeaways

- KP Law says almost 1,700 UK investors are pursuing a combined £150 million claim against Binance and Changpeng Zhao over crypto derivatives offerings.

- The lawsuit targets leverage tokens, futures, and options, alleging breaches of the Financial Services and Markets Act 2000.

- The case centers on alleged continued access after the FCA banned such products to UK retail customers in January 2021.

- Binance has denied wrongdoing and told Cointelegraph it will defend the claims in court.

- The complaint was reportedly filed in the London High Court, naming Binance-affiliated Nest Exchange and “persons unknown.”

What the lawsuit alleges

The investors are represented by KP Law, which states that Binance’s leverage tokens and derivatives offerings violated the Financial Services and Markets Act 2000. KP Law also argues that these products kept being offered to UK customers even after regulatory restrictions were issued.

In its statement, the law firm suggests there was “no effective barrier” preventing UK customers from accessing the products. While the precise mechanics of access are not detailed in the available reporting, the legal thrust is clear: the plaintiffs contend that the exchange’s products were distributed in a way that did not respect the regulatory prohibition for retail customers.

Reuters reported that multiple UK users lost “tens of thousands of pounds” through the affected products, underscoring that the suit is not framed as a purely technical regulatory dispute but as a remedy-seeking effort over financial losses.

Binance’s response and the legal posture

Binance told Cointelegraph it would “defend against these claims through the appropriate legal process.” The exchange also said it “remains committed to its obligations to users and to operating in accordance with applicable law.”

That stance positions the lawsuit squarely as a dispute over whether Binance’s derivative offerings were unlawfully provided to UK retail customers and whether the FCA’s January 2021 ban was effectively enforced in practice. As with any civil claim, the next steps—procedural rulings, discovery, and eventual merits arguments—will determine how those allegations are substantiated in court.

How this fits into Binance’s broader regulatory pressure

Lawyers and regulators are not acting in a vacuum. The filing adds to what Cointelegraph described as a growing list of legal and regulatory challenges for Binance, including compliance uncertainty linked to Europe’s Markets in Crypto-Assets (MiCA) framework.

Earlier coverage from Cointelegraph noted that Binance faced difficulty securing a MiCA-compliant license from an EU member state before a July 1 deadline. That type of licensing timeline matters to investors because MiCA was designed to create a clearer compliance structure across the EU—yet uncertainty around authorization and product restrictions can translate into uneven availability of services, shifting venue risk, and changes to how platforms present derivatives and related products.

In addition, Cointelegraph previously reported on allegations that Binance facilitated transactions tied to a sanctioned Iranian financier and that flowed to Iran’s Islamic Revolutionary Guard Corps. Binance strongly denied those allegations, and the case now reflects how regulatory scrutiny has spanned both market-structure compliance (derivatives access and retail suitability) and broader concerns around illicit finance and sanctions risk.

Who may be affected—and what changed for UK operations

The plaintiffs are said to be identifying the full scope of affected customers. KP Law said the precise number of UK customers affected is not publicly known, but argued that Binance’s global scale could mean a larger pool of exposure than the reported 1,700 claimants.

One individual described in coverage is Tomas Sutas, a financial controller who allegedly invested more than £100,000 into Binance’s derivatives products before the value was wiped out, the Financial Times reported. Reuters also described multiple UK users losing “tens of thousands of pounds.” While these accounts represent specific claim narratives rather than a verified aggregate loss figure for the full class, they help explain why the dispute has advanced as a high-stakes damages case.

Cointelegraph also pointed to earlier restrictions affecting Binance in the UK. Binance’s operations in the region reportedly became heavily constrained in June 2021, when the FCA informed Binance Markets Limited that it could not operate without written consent. That timeline is central to how the plaintiffs frame causation: the argument is that regulatory action came earlier, but access to the relevant derivatives continued.

Reuters reported that the lawsuit was filed in the London High Court. The defendants reportedly include the Binance-affiliated Nest Exchange as well as “persons unknown,” a formulation often used when claimants cannot yet identify all involved parties or when seeking broader injunctive and compensatory relief. KP Law said the firm is still working to determine the full set of impacted customers.

For UK-based investors and traders, the practical takeaway is that product availability can become a long-term legal issue, not just a short-lived trading restriction. Even when regulators impose bans, the continuing question—central to this lawsuit—is whether platforms effectively prevent retail access and how that is assessed under the relevant financial services framework.

As the case moves through the UK courts, readers should watch for early procedural developments, including how the court interprets the FCA ban’s reach and whether plaintiffs can demonstrate that the alleged access after January 2021 was sufficiently direct and attributable to Binance’s offerings. Beyond the outcome, the litigation could influence how exchanges design and enforce geo- and user-level controls for derivatives and other complex products in jurisdictions with active retail restrictions.

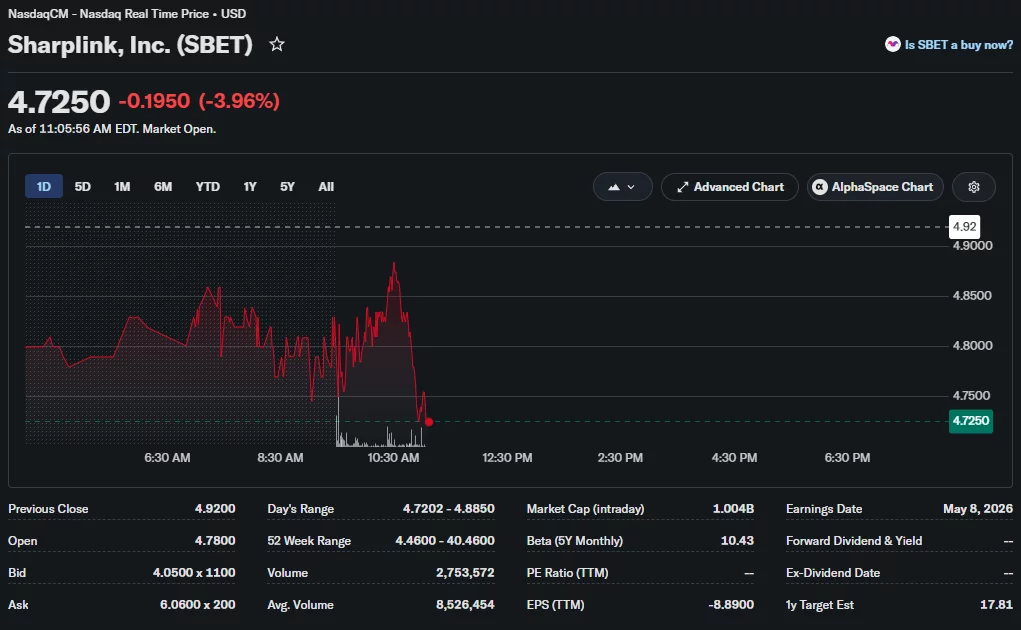

SharpLink has expanded its Ethereum treasury with another 10,000 ETH purchase even as the cryptocurrency has remained on course for its third consecutive quarterly decline.

Summary

- SharpLink bought another 10,000 ETH for $16.1 million, increasing its Ethereum holdings to 886,725 ETH.

- Ethereum is on track for its first-ever third consecutive quarterly loss despite continued treasury accumulation.

- Bitmine now holds more than 5.7 million ETH, adding to institutional buying as analysts watch the $1,500 support level.

According to a company press release, SharpLink acquired the latest 10,000 ETH at an average price of $1,611 per token, spending approximately $16.1 million on the purchase.

The transaction increases the company’s total Ethereum holdings to 886,725 ETH and follows a $75 million capital raise completed through a registered stock offering.

SharpLink continues building its Ethereum treasury

Alongside the latest crypto purchase, SharpLink stepped up its capital management efforts by repurchasing more than 2.13 million shares of its common stock, SBET, at an average price of $4.69 per share.

The company said it has now bought back over 4.07 million shares since August 2025. Despite those moves, SBET shares were trading around $4.72 at the time of writing, down nearly 4% on the day.

Recent corporate developments have also added to the company’s profile. Earlier this week, SharpLink joined the Russell 2000 and Russell 3000 indexes, extending its presence in major U.S. equity benchmarks while continuing to increase its Ethereum reserves.

SharpLink is not the only listed company expanding its exposure to Ethereum. As crypto.news reported on Monday, Ethereum treasury firm Bitmine purchased another 27,084 ETH during the past week, lifting its holdings to more than 5.7 million ETH.

Based on the company’s figures, those reserves now account for about 4.7% of Ethereum’s estimated circulating supply of 120.7 million ETH, bringing Bitmine closer to its previously stated target of holding 5% of the network’s supply.

Earlier this month, crypto.news also examined the implications of treasury companies accumulating increasingly large portions of Ethereum. The report noted that sustained buying could reduce the amount of ETH available for trading, although concentrated ownership may create additional risks if companies later need to fund operations through debt, equity issuance, or asset sales during weaker market conditions.

Ethereum remains under pressure despite corporate buying

Even as treasury companies continue adding to their holdings, Ethereum (ETH) has struggled to regain upward momentum. At the time of writing, ETH traded near $1,560, down about 1% on the day and roughly 25% for the quarter.

Current market performance also places Ethereum on track to record its third straight quarterly loss, a result that would be the first such streak in the asset’s history if the quarter closes at current levels.

Some analysts nevertheless see the recent weakness as a key technical test rather than a definitive breakdown. According to crypto analyst Ted Pillows, Ethereum could stage a relief rally next month if it manages to hold support around $1,500.

The analyst’s chart also outlined the downside risk if that level fails. Under that scenario, Ted Pillows said Ethereum could fall toward $1,400 or lower, underscoring that price direction in the coming weeks may depend on whether buyers continue defending the current support zone despite ongoing accumulation by treasury firms.

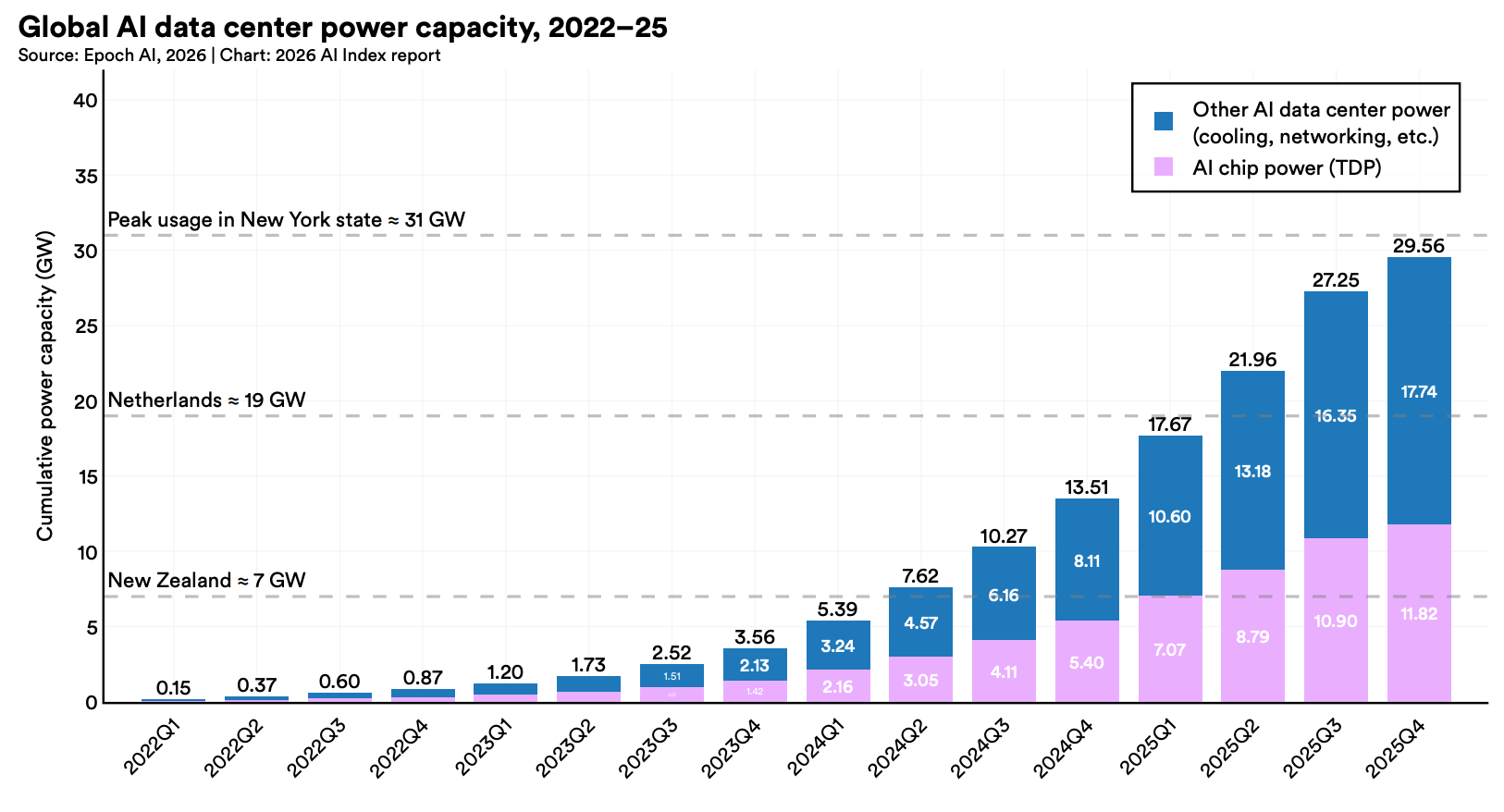

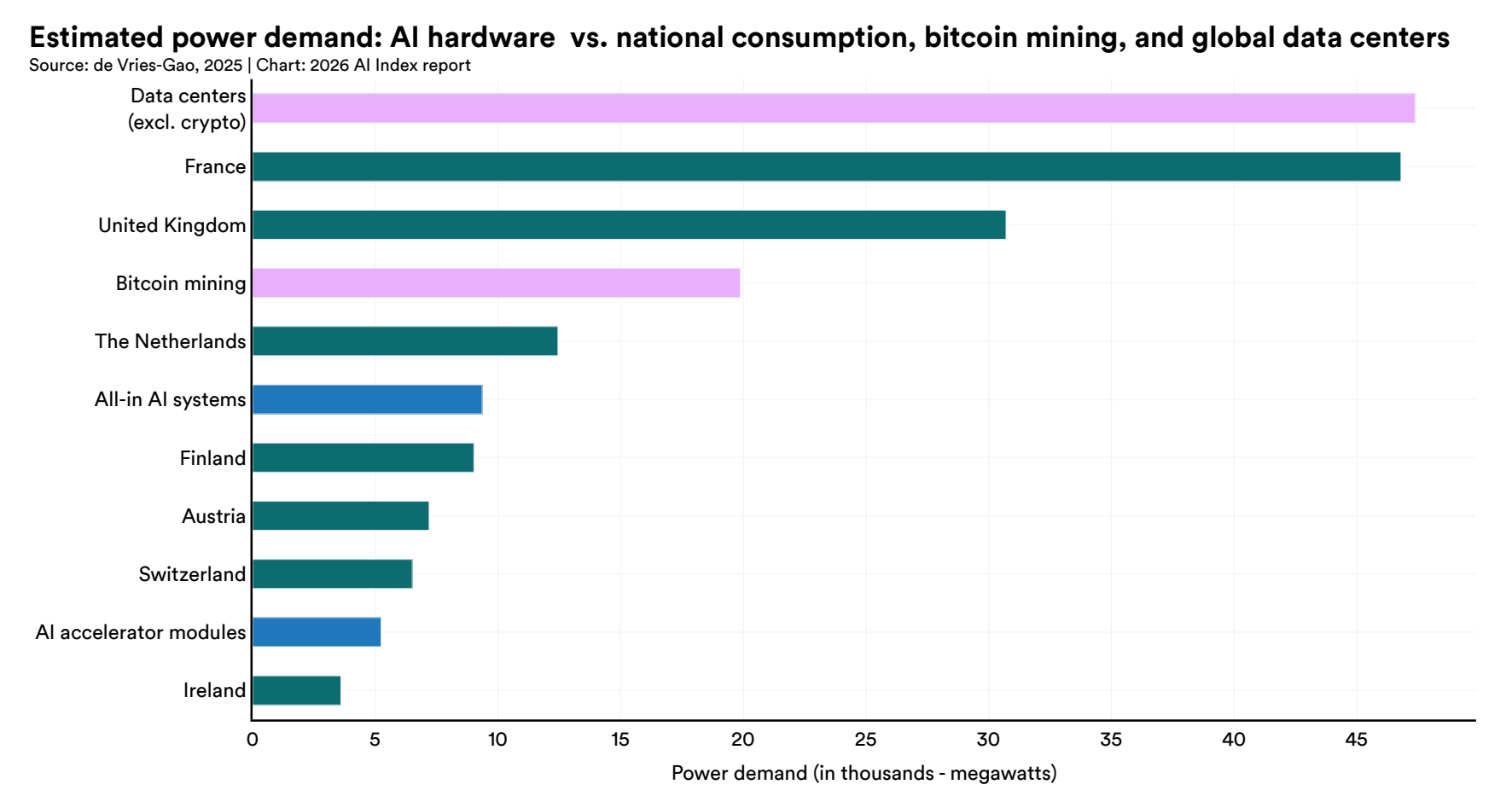

By the end of 2025, the power capacity tied to artificial intelligence data centers worldwide had reached about 29.6 gigawatts (GW), enough to run all of New York state at peak demand, according to Stanford University’s annual report on the AI industry.

The report, released in April, suggests that compute itself is abundant and getting cheaper. Permitted, grid-connected, ready-to-draw electricity is in high demand, but the sources to power it are much harder to come by. One industry has spent the past decade quietly building exactly that infrastructure for a different reason: Bitcoin mining.

AI data center power capacity reached about 29.6 GW by the end of 2025, comparable to New York state at peak demand. Source: Stanford University

Chips get more efficient, but total demand rises

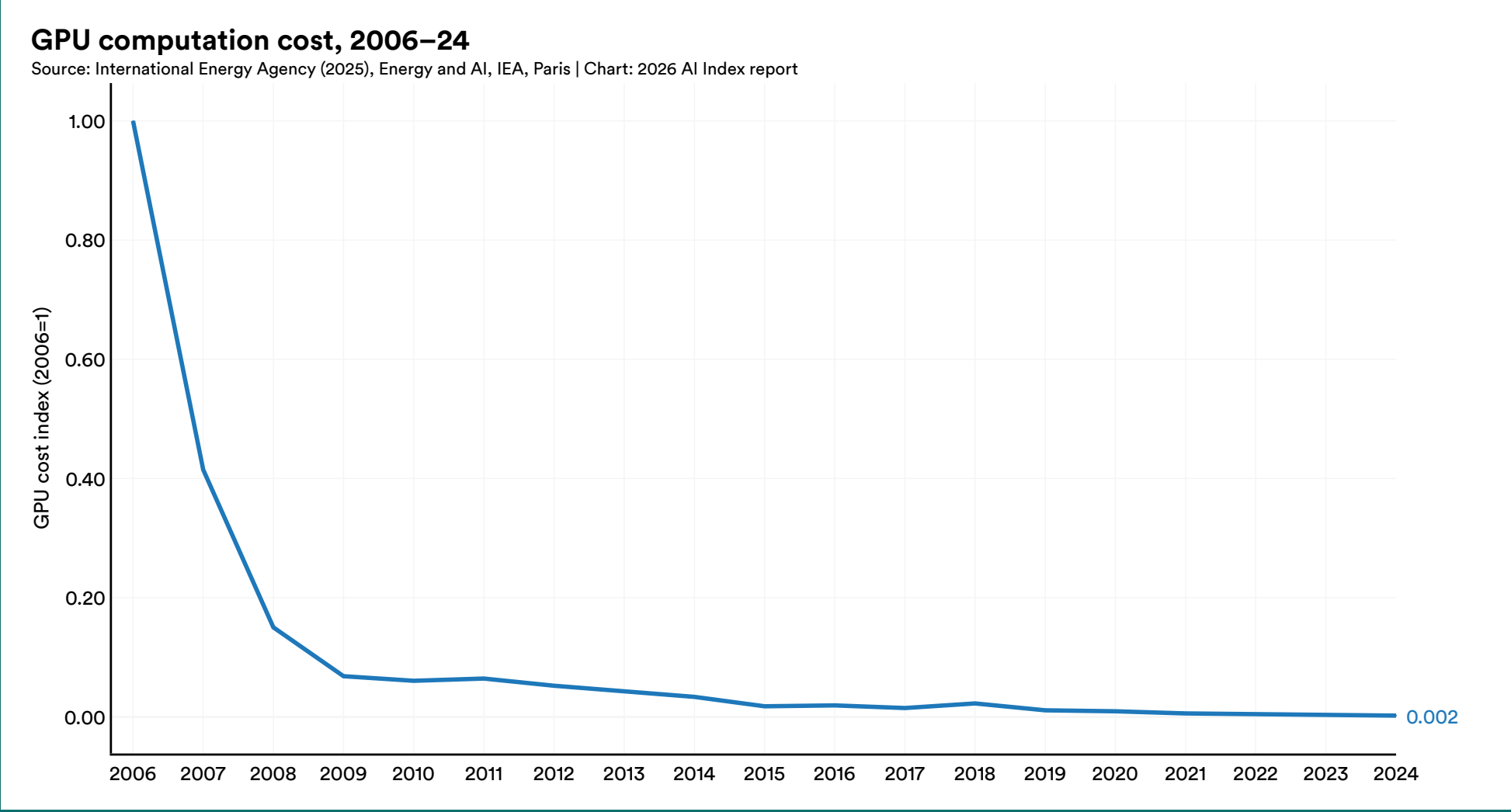

The economics of chips are moving in the opposite direction. Stanford said the cost of GPU computation has dropped more than 99% since 2006, while leading chips now perform far more work per watt than they did a decade ago. But efficiency gains have not reduced total demand. They are instead poured back into larger models rather than banked as savings, keeping the pressure on the power grid.

The cost of GPU computation has fallen more than 99% since 2006, even as total power draw climbed. Source: Stanford University

Stanford estimates that the most demanding training runs, including for systems such as Llama 4 Behemoth, have pulled upward of 100 megawatts (MW), comparable to a small power plant. Capacity dedicated to AI has risen some 200-fold in three years, from under a gigawatt in 2022, and data center electricity use is projected to keep rising through 2030.

The squeeze is geographic as much as numerical. The United States hosts 5,427 data centers, more than 10 times any other country, according to Stanford.

Chips can be ordered and delivered in months, but energizing a site, with its substation, interconnection approval and cooling, takes years.

Counted across full systems rather than the accelerators alone, AI’s cumulative power demand through 2024 reached an estimated 9.4 GW, close to the national electricity use of Switzerland or Austria and about half the estimated draw of Bitcoin mining.

Estimated all-in AI power demand (through 2024) sits near half of Bitcoin mining’s. Source: de Vries-Gao, Stanford University

The asset was never the hardware

But Bitcoin miners cannot just hand their machines to an AI lab. Mining ASICs (the chips that solve Bitcoin calculations) do one narrow job and are useless for training or inference. What does transfer is everything around the chips, such as the energized sites, power contracts, grid hookups and the shells to cool dense racks.

A Bitcon miner that already has a grid connection has infrastructure ready to fill the gaps for the AI developers, and renting that capacity beats starting over. Miners also tend to sit where AI wants to be anyway, in cheap-power US states like Texas and the Gulf Coast.

Mining economics is itself a numbers-crunching game. JPMorgan recently estimated Bitcoin’s all-in production cost at about $78,000 per coin, well above BTC’s market price of around $53,400 at the time of writing, down by more than 34% year-to-date, according to CoinGecko.

Bitcoin is down by around 34% in 2026. Source: CoinGecko

Cointelegraph previously reported that hashprice had fallen below breakeven for many miners, putting about 20% of the industry in unprofitable territory.

Some major contracts between miners and AI infrastructure operators followed. In November 2025, Iren signed a five-year GPU cloud deal with Microsoft worth about $9.7 billion, served from a 750-megawatt campus in Childress, Texas. In December, Bitcoin miner Hut 8 signed a 15-year, $7 billion lease with Fluidstack for 245 megawatts at its River Bend site in Louisiana, with the payments backstopped by Google.

TeraWulf reported $12.8 billion in contracted high-performance computing (HPC) revenue and now earns more from leasing than mining. Core Scientific has expanded its CoreWeave agreement to $10.2 billion over 12-year terms. Across the listed miner sector, CoinShares counts more than $70 billion in announced AI and HPC contracts, but much of the value is years out. Hut 8’s River Bend site, for example, is not due to start commissioning until the second quarter of 2027.

Related: TeraWulf doubles AI revenue but posts $427M quarterly loss as mining income declines

Investors have nonetheless rewarded the shift. Hut 8 stock jumped about 20% in premarket trading the day its lease was announced, Reuters reported, and across the sector, valuations are increasingly tied to compute pipelines rather than the Bitcoin price alone. Indeed, CoinShares said the miners with HPC contracts were trading at 12.3 times the value of their 12-month revenue vs 5.9 times for pure play miners. CoinShares’ projects listed miners could derive as much as 70% of revenue from AI by the end of 2026, up from roughly 30% in Q1.

Why it is not a free pivot

However, the conversion is far from cheap, and is not just a matter of plug-and-play. CoinShares estimates that mining infrastructure costs about $700,000 to $1 million per MW, while AI-grade, liquid-cooled infrastructure can cost $8 million to $15 million per MW. Hyperscalers also demand power density, redundancy and uptime guarantees that many mining facilities were never designed to provide.

Related: Celsius-linked Bitcoin miner Ionic Digital seeks Nasdaq direct listing amid AI pivot

Miners are covering that gap with debt and new capital raises. Iren had already disclosed about $3.75 billion in convertible note debt at the end of March, then raised another $3 billion through a new convertible note sale in May.

The sector is also leaning on a small group of hyperscalers and AI infrastructure buyers. If demand cools, customers renegotiate or projects slip, miners that have torn out ASICs may have fewer options to fall back on.

Whether that shift away from BTC mining pays off remains an open question. Signing multibillion-dollar AI contracts is one thing, but delivering the earnings investors expect is another.

For now, the market is placing a premium on miners making the transformation rather than those that simply produce new BTC. If AI demand continues to outpace electricity supply, those assets could prove more valuable than the machines they were originally built to support. If not, some of today’s biggest AI plans could prove to be costly bets, rather than real second acts for former Bitcoin miners.

Magazine: Bitcoin miners are pivoting to AI, so why is the hashrate near ATHs?

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

An XRP Power user shares a story of financial recovery, encouraging users to explore its platform and AI-powered digital asset services.

On a winter night, the temperature on the streets of New York dropped to freezing. A ragged man huddled on a bench near a subway station, his only old coat wrapped tightly around his body. At that time, he had no job, no fixed address, only a few coins in his pocket, and he didn’t even know if he would have a hot meal the next day.

Few passersby stopped, and no one would have imagined that this seemingly insignificant homeless man would, a few months later, achieve financial freedom and own a million-dollar fortune.

The low point of life

Before becoming homeless, he lived an ordinary life, with a family, a job, and expectations for the future. But all of this was quickly shattered by reality, bit by bit.

His marriage ran into problems, and the breakdown of his family plunged him into both emotional and financial hardship. Not long after, his company laid off employees, and he lost his only stable source of income.

To get back on his feet, he decided to start his own business, investing all his meager savings. However, due to inexperience and an unfavorable market environment, the business quickly failed. Instead of recovering, he was burdened with debt.

When all possible avenues were exhausted, he lost his home and was forced to move between shelters, his car, and the streets. During that time, he truly experienced for the first time what it meant to have “no way out.”

Turning point

During his most difficult time, a chance encounter changed circumstances.

Through a former colleague, he saw discussions and introductions about XRP Power in the Global Times. This caught his attention. Hiscolleague had been with XRP Power for some time and had earned a considerable amount of money there, but when he told him, he didn’t have the funds to risk investing.

For the next two months, he focused primarily on observation and understanding, gradually familiarizing himself with the platform’s operation and only making very small trial investments.

After confirming the basics, he officially joined. Although the earnings weren’t high, during his most difficult time, he successfully withdrew $100 for the first time, enough to support his basic living expenses for several days.

From then on, he gradually increased his investment while continuing to learn and adjust his strategies.

In the following months, his income began to stabilize, his life gradually emerged from its lowest point, and a real turning point began to appear.

The process

After gradually seeing a glimmer of hope, he began to plan each step more cautiously.

Initially, he only used a small amount of about $100 to try it out, mainly to familiarize himself with the rules and control risk, rather than pursuing a complete change in his situation.

After things stabilized somewhat, he gradually increased hisinvestment to about $5,000, then $50,000, and only later, when he felt more confident, did he gradually moved to the $100,000 level. Throughout this process, he maintained a phased and controlled pace, rather than a one-time investment.

In this process, he learned to adjust his strategy according to different stages, making his financial arrangements more stable, rather than chasing short-term fluctuations.

From the initial cautious attempts to the gradual expansion, he was more focused on managing his own rhythm than simply pursuing results.

Looking back, the real change wasn’t a single investment, but rather long-term adjustments and perseverance.

In conclusion

Looking back on this experience, he has returned to a stable life from living on the streets.

For him, this isn’t a story of “sudden success,” but rather the result of taking it one step at a time. The low point taught me to calmly face reality and made him understand the importance of perseverance and making the right choices.

He says, the hardest thing in life isn’t falling down, but whether someone can start over after falling down.

From homelessness to regaining his footing, there were no shortcuts, only continuous attempts and adjustments.

What truly changes your destiny isn’t the starting point, but the step taken forward even at someone’s lowest point.

Join XRP Power achieve a better life and be the starting point for financial freedom.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Bitcoin Core has released version 31.1rc1, fixing a privacy flaw in PrivateBroadcast while introducing software, wallet, and validation improvements ahead of the next stable mainnet release.

Summary

- Bitcoin Core 31.1rc1 fixes a privacy flaw that could expose users’ IP addresses during PrivateBroadcast.

- The release also improves blockchain validation, wallet accuracy, networking, and MuSig2 security.

- Developers are encouraging community testing before the stable version is released.

According to the Bitcoin Core development team, version 31.1rc1 is now available as a release candidate, giving users, node operators, and developers an opportunity to test nearly finished software before the official production release. The developers said the testing period is intended to uncover any remaining issues that may not have appeared during internal development.

The most notable change addresses a privacy issue affecting the PrivateBroadcast feature. According to the release notes, certain network conditions could expose a user’s internet address by allowing a connection outside the intended privacy network. The updated software removes that behavior, making transaction broadcasting more consistent for users who rely on privacy-focused network configurations.

Privacy protections and node performance receive upgrades

Alongside the privacy fix, the Bitcoin Core developers introduced several changes to improve blockchain validation and long-term node performance. According to the project documentation, the software now manages transaction-related data more efficiently while maintaining a leaner blockchain database, a change designed to reduce unnecessary storage growth and improve performance as the chain expands.

Networking behavior has also been refined. The developers said Bitcoin Core now handles proxy settings and PrivateBroadcast connections more intelligently, providing more predictable behavior for users routing traffic through privacy tools such as proxy networks.

Wallet functionality received additional maintenance updates as well. According to the release notes, migration checks have been improved, and transaction input size estimation has been refined, allowing wallet operations to calculate transaction data more accurately behind the scenes without changing the user experience.

Security improvements extend to signatures and developer tools

Security-related updates also include additional safeguards for MuSig2, the signature aggregation protocol supported by Bitcoin Core. According to the developers, the software now rejects empty public key lists that contain invalid public keys, preventing incorrect signature aggregation and improving validation during multi-signature operations.

Several changes were introduced for developers maintaining or building software around Bitcoin Core. The release notes state that testing utilities have been cleaned up, race conditions have been removed, fuzz testing has been expanded, and build systems have been updated to improve software reliability during development.

Configuration handling has also been strengthened. Before saving important settings, Bitcoin Core now performs checks for failed write operations, a safeguard the developers said can help prevent configuration errors caused by unsuccessful disk writes.

Version 31.1rc1 is available for current versions of Linux, macOS, and Windows. According to the Bitcoin Core team, users running recent software versions can upgrade directly, although systems upgrading from much older releases may require additional time to migrate existing blockchain data.

Because version 31.1rc1 remains a release candidate rather than the final production version, the developers are encouraging the community to install the software in test environments, verify its behavior under real-world conditions, and report any bugs before the stable release reaches the Bitcoin network. The project said feedback collected during this testing phase will help identify remaining issues before the software is finalized.

Devin Haney given 20 day deadline to strike a deal with mandatory challenger or risk losing title

The 5 Most Affordable Riding Lawn Mowers You Can Buy In 2026 (So Far)

XRP TO $0.16?! THIS WOULD SHOCK EVERY HOLDER

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World1 day ago

Crypto World1 day agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business1 day ago

Business1 day agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

-

Business1 day ago

Business1 day agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login