Crypto World

Crypto Companies Have Spent $189M So Far on 2026 US Election Cycle: Report

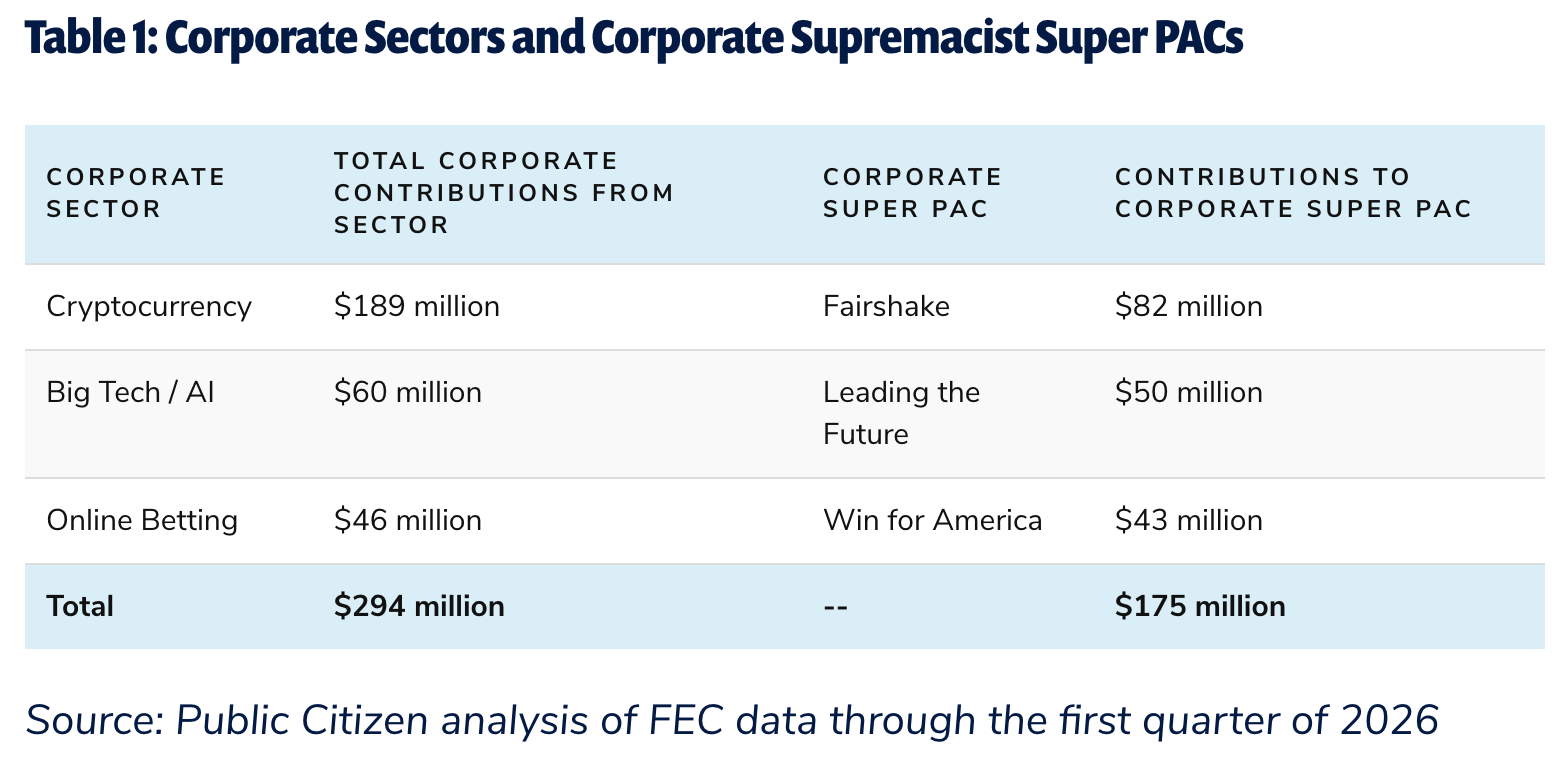

The US consumer advocacy group Public Citizen on Tuesday reported that the cryptocurrency industry had contributed $189 million toward the 2026 election cycle, following its 2024 playbook.

According to a report released Tuesday, the nonprofit organization said that about 37% of all corporate contributions in the 2026 US election cycle could be traced to crypto companies, totaling about $189 million so far, with more than four months until the November election.

While the watchdog group said that the crypto-aligned political action committee (PAC) Fairshake was responsible for spending more than $82 million so far, the MAGA Inc. Super PAC, largely backed by Crypto.com, had spent more than $56 million.

“These super PACs prioritize the interests of their business backers over either major political party or any candidate,” said Public Citizen. “Following the crypto playbook, they are set up to engage in both Democratic and Republican primaries and to support or attack candidates of either major party in the general election.”

Source: Public Citizen

Fairshake and its affiliates Defend American Jobs and Protect Progress are backed by cryptocurrency companies Coinbase and Ripple, and reported a $193 million war chest as of January. Entities aligning with industry interests have also been formed since 2024, including the Fellowship PAC backed by Cantor Fitzgerald.

Altogether, the PACs’ combined spending has already exceeded that in 2024, when companies contributed $170 million toward electing what it considered “pro-crypto” candidates to Congress.

Related: Senate leaders push for July passage of CLARITY Act

Cointelegraph reached out to a Fairshake spokesperson for a comment on the report but did not receive an immediate response.

Colorado primaries flush with crypto PAC cash

Colorado voters head to the polls today in primaries for Republican and Democratic candidates, with the state’s 8th congressional district potentially being influenced by crypto PAC spending.

The You Can Push Back Super PAC backed by Ripple Labs co-founder Chris Larsen reportedly spent $1 million on media to support Democrat Manny Rutinel. The committee’s last big bet — $3.3 million — was on Democrat Alex Bores in New York’s 12th Congressional District. He lost his primary last week to Micah Lasher, who had criticized Larsen’s involvement in the race.

Magazine: SBF will never get a pardon, Trump peace deal boosts Bitcoin: Hodlers Digest June 14-21

Taiwan has passed its Virtual Asset Service Act, giving crypto exchanges and stablecoin issuers a clear licensing path after years of legal uncertainty.

Summary

- Taiwan’s new crypto law requires exchanges and other virtual asset firms to obtain FSC licenses.

- Stablecoin issuers must secure central bank and FSC approval while keeping full reserve backing.

- Existing registered crypto firms get a transition period before the new licensing system fully applies.

Taiwan’s Legislative Yuan passed the Virtual Asset Service Act in its third reading on June 30, sending the bill to President Lai Ching-te for the next step. The Financial Supervisory Commission said the law moves Taiwan’s crypto oversight from anti-money laundering registration to wider supervision of operations, market order and customer protection.

The act creates rules for seven types of virtual asset service providers, including exchanges, trading platforms, transfer firms, custodians, underwriters and lending service providers. The law covers internal controls, cybersecurity, asset listing reviews, customer asset segregation, outsourcing, civil liability and financial reporting, according to the FSC statement.

Taiwan sets new licensing rules for crypto firms

Under the new law, crypto businesses must obtain approval from the FSC before operating. Existing firms that already completed anti-money laundering registration before the law takes effect will have 12 months to apply for approval and 21 months to obtain the required license, according to the FSC.

The law also gives firms a limited buffer if more time is needed. The FSC said the transition period may be extended by three months, but only once. Firms that fail to complete the process by the deadline will not be allowed to continue virtual asset business in Taiwan.

Stablecoins get central bank role

Stablecoin issuers will need approval from both Taiwan’s central bank and the FSC before issuing tokens in the country. The law requires issuers to maintain full reserve assets, place reserves in trust and carry out regular audits and public disclosures, according to the FSC.

As previously reported by crypto.news, Taiwan’s FSC had earlier planned a draft law that would allow local banks to issue stablecoins tied to the New Taiwan dollar. That plan gave the central bank a role in stablecoin oversight and placed local stablecoin approval under the FSC.

The final law also creates criminal penalties for unlicensed activity and market abuse. Focus Taiwan reported that illegal VASP operations or stablecoin issuance can bring up to seven years in prison and fines of up to NT$100 million, or about $3.14 million.

Fraud and market manipulation carry heavier penalties. Offenders can face three to 10 years in prison and fines from NT$10 million to NT$200 million, according to Focus Taiwan.

New rules end legal gray area

The law gives Taiwan’s crypto sector a formal legal base after a period where many businesses relied on anti-money laundering registration rather than a full license. The legislative document said the act aims to protect customers, support sector development and bring Taiwan closer to global standards used in markets such as the European Union, Japan and South Korea.

Moreover, the FSC released the draft Virtual Asset Service Act in March 2025 with licensing rules for crypto firms, stablecoin standards and investor protection measures. The new passage turns that draft direction into a law awaiting promulgation and an effective date from the cabinet.

Previously, crypto.news reported that Taiwan’s central bank and FSC were pushing tighter stablecoin rules while lawmakers debated the government’s seized crypto holdings. That earlier debate showed how digital assets had moved from a narrow compliance issue into a wider policy topic in Taiwan.

The FSC said it will continue drafting authorized sub-rules and will consult industry groups and other stakeholders. The next stage will decide how licensing standards, personnel rules, internal controls and stablecoin procedures work in practice.

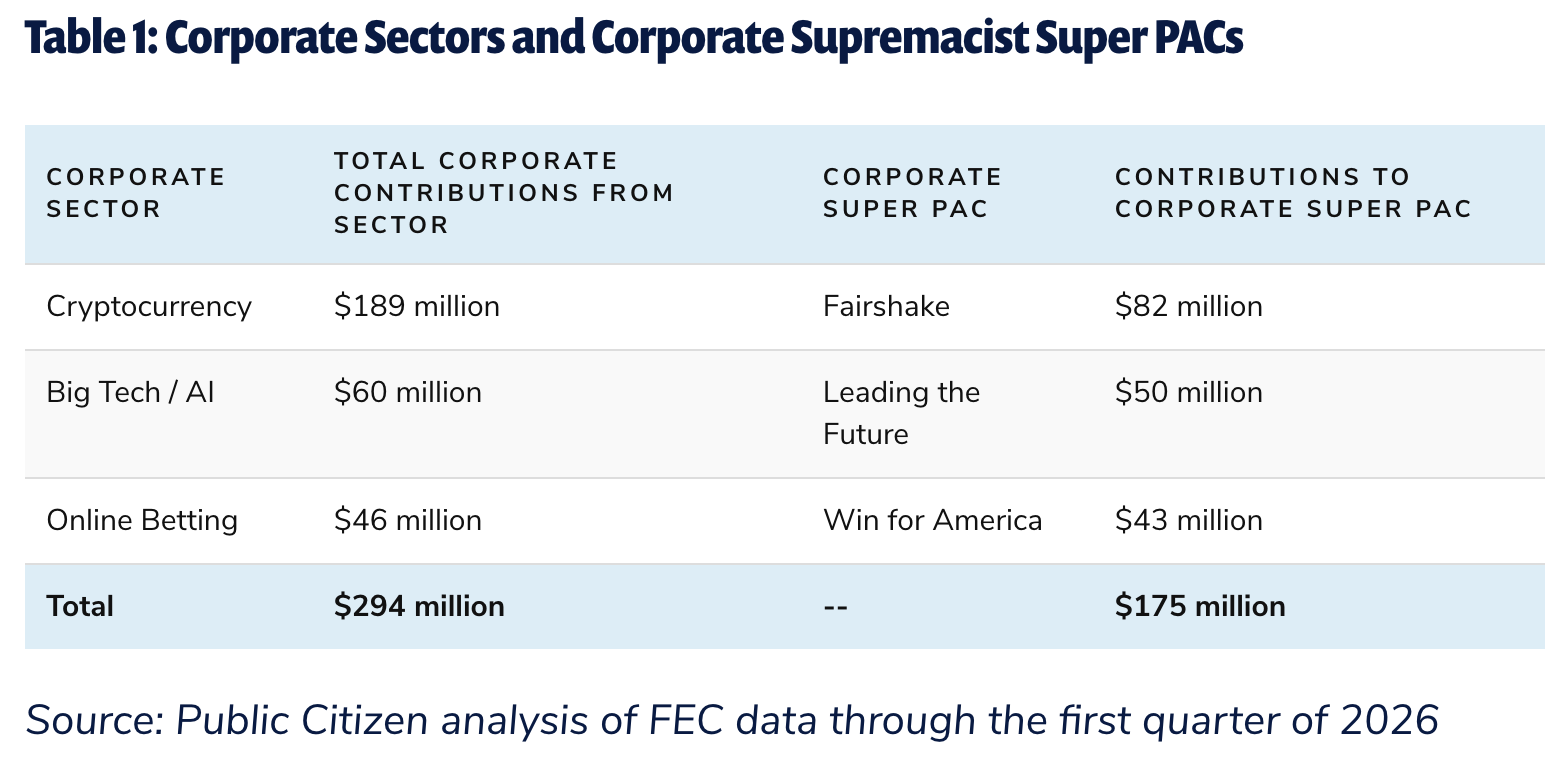

US-listed Bitcoin (BTC) exchange-traded funds (ETFs) recorded $4.5 billion in net outflows during June 2026. This was the worst monthly figure since the products launched in January 2024.

The redemptions coincided with a sharp price decline. Bitcoin fell 20.48% over the month, its steepest monthly drop since June 2022, when the asset shed 37.28% during that cycle’s collapse.

IBIT Leads the Institutional Retreat

June’s outflows broke the previous monthly record of $3.56 billion, set in February 2025 during an earlier stretch of market stress.

Follow us on X to get the latest news as it happens

BlackRock’s iShares Bitcoin Trust (IBIT) accounted for the bulk of the outflows. The fund alone shed $3.55 billion, close to 79% of the category’s total redemptions.

That concentration is striking. IBIT’s single-fund outflow nearly matched the entire category’s prior monthly record on its own.

The price data reinforces the pressure. Bitcoin closed four of 2026’s first six months in negative territory, with June’s 20.48% decline the deepest of the year.

How Crypto ETFs Performed in June 2026

The weakness extended beyond Bitcoin, though the scale varied across categories. Ethereum (ETH) ETFs posted $528.99 million in June outflows, SoSoValue data showed.

Solana (SOL) ETFs recorded net outflows of roughly $786,580. The figure is small, but it marks the first monthly outflow for Solana ETFs since their launch, ending a run of positive months.

Not every category turned negative. XRP (XRP) ETFs drew $59.46 million in net inflows during June, holding positive despite the broader downturn.

Hyperliquid (HYPE) ETFs led the group with $161.05 million in inflows, the strongest June showing across the products.

The split suggests capital rotated within crypto rather than exiting entirely. Newer altcoin products absorbed fresh money even as the two largest categories saw sustained redemptions.

Whether that rotation hardens will depend on how Bitcoin trades in July, since a price rebound could pull capital back toward the incumbents.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Bitcoin Spot ETFs Post Worst Month on Record With $4.5 Billion June Outflow appeared first on BeInCrypto.

A newly released federal financial disclosure has revealed that US President Donald Trump holds more than $50 million worth of Bitcoin in a cold wallet.

According to a 927-page document released by the US Office of Government Ethics, the Bitcoin is held under CIC Digital LLC as a “Cryptocurrency Wallet Virtual Bitcoin Key (held in cold wallet)” and is worth “Over $50,000,000,” the highest reporting category available on the form. Because the disclosure does not require an exact figure above that threshold, the actual value of the BTC holdings could be higher.

Trump’s BTC Stash

The filing shows that the Bitcoin is held in the Donald J. Trump Revocable Trust, with Trump listed as the sole beneficiary. The trust also controls his stake in Trump Media & Technology Group, the parent company of Truth Social.

Interestingly, the BTC is stored in cold storage, meaning the private keys are kept offline rather than on internet-connected systems or with a third-party exchange, a setup widely used to reduce online security risks.

The filing shows that Bitcoin is only one part of the digital assets held by CIC Digital LLC.

It also lists an Ethereum wallet, which is worth between $5 million and $25 million, a staked Ethereum position through a Coinbase staking agreement that generated $510,808 in validator rewards, a USDC stablecoin holding worth between $5 million and $25 million, and a smaller dollar-denominated wallet.

Based on the reported valuation ranges, the combined disclosed value of the Bitcoin and Ethereum holdings alone stands above $100 million. The same disclosure also reveals the scale of Trump’s crypto-related earnings during the reporting period. It states that World Liberty Financial (WLFI) generated more than $500 million from the sale of governance tokens and other crypto products, while CIC Digital LLC generated more than $635 million from sales of Trump-branded meme coins launched shortly before his inauguration.

Overall, Trump’s crypto earnings exceeded $1 billion during his first year back in office.

White House Rejects Conflict Claims

The disclosure has drawn significant scrutiny, to which White House spokesperson Anna Kelly responded that neither Trump nor his family has engaged in, nor will they engage in, conflicts of interest. She added,

“All actions by President Trump and his administration are taken in the best interest of the American people – and any so-called ‘reporters’ pushing otherwise are recycling the same, tired, false narrative that Democrats and the legacy media have been pushing for a decade”

The post New Federal Data Reveals Donald Trump Holds $50 Million in Bitcoin in Cold Wallet appeared first on CryptoPotato.

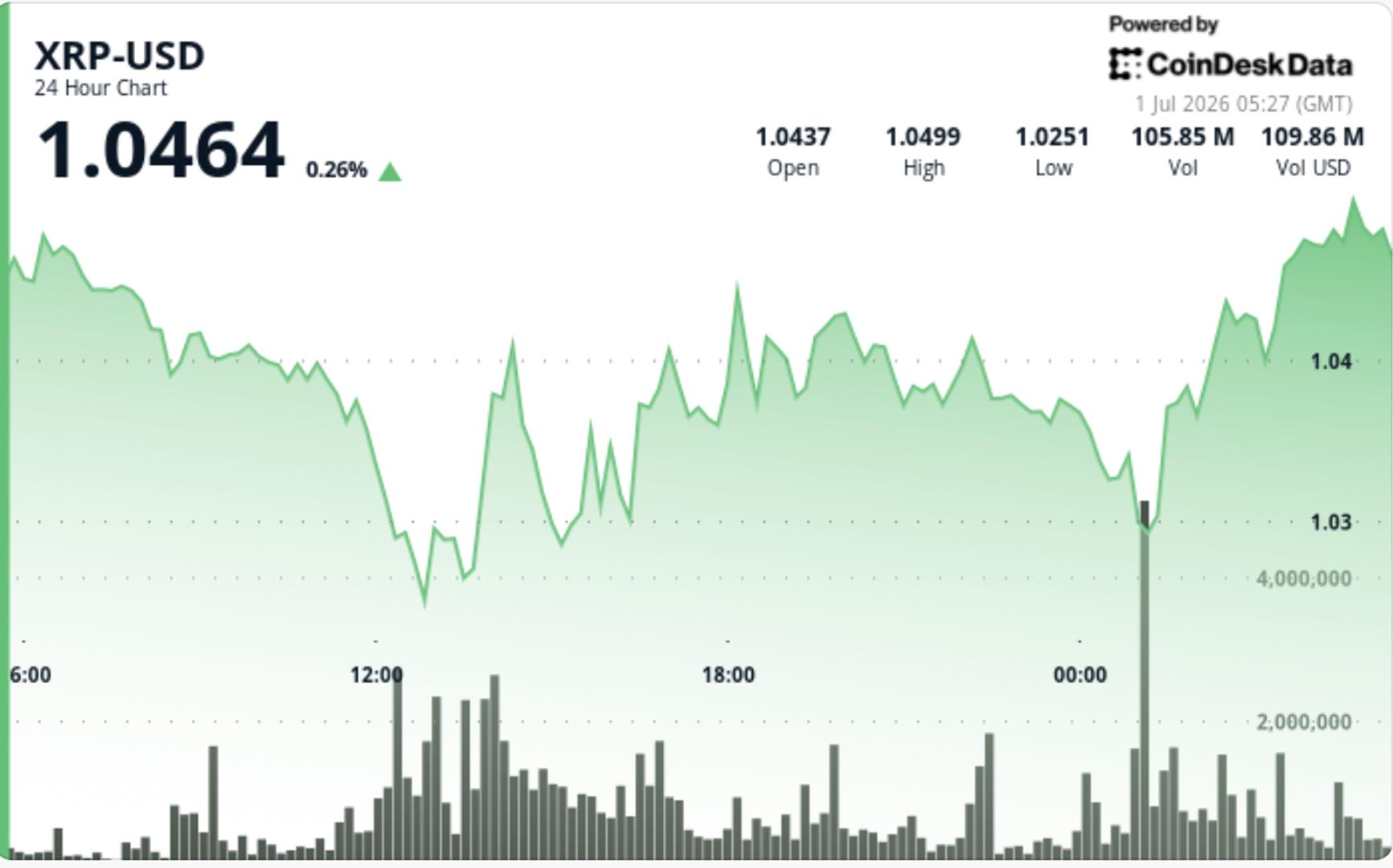

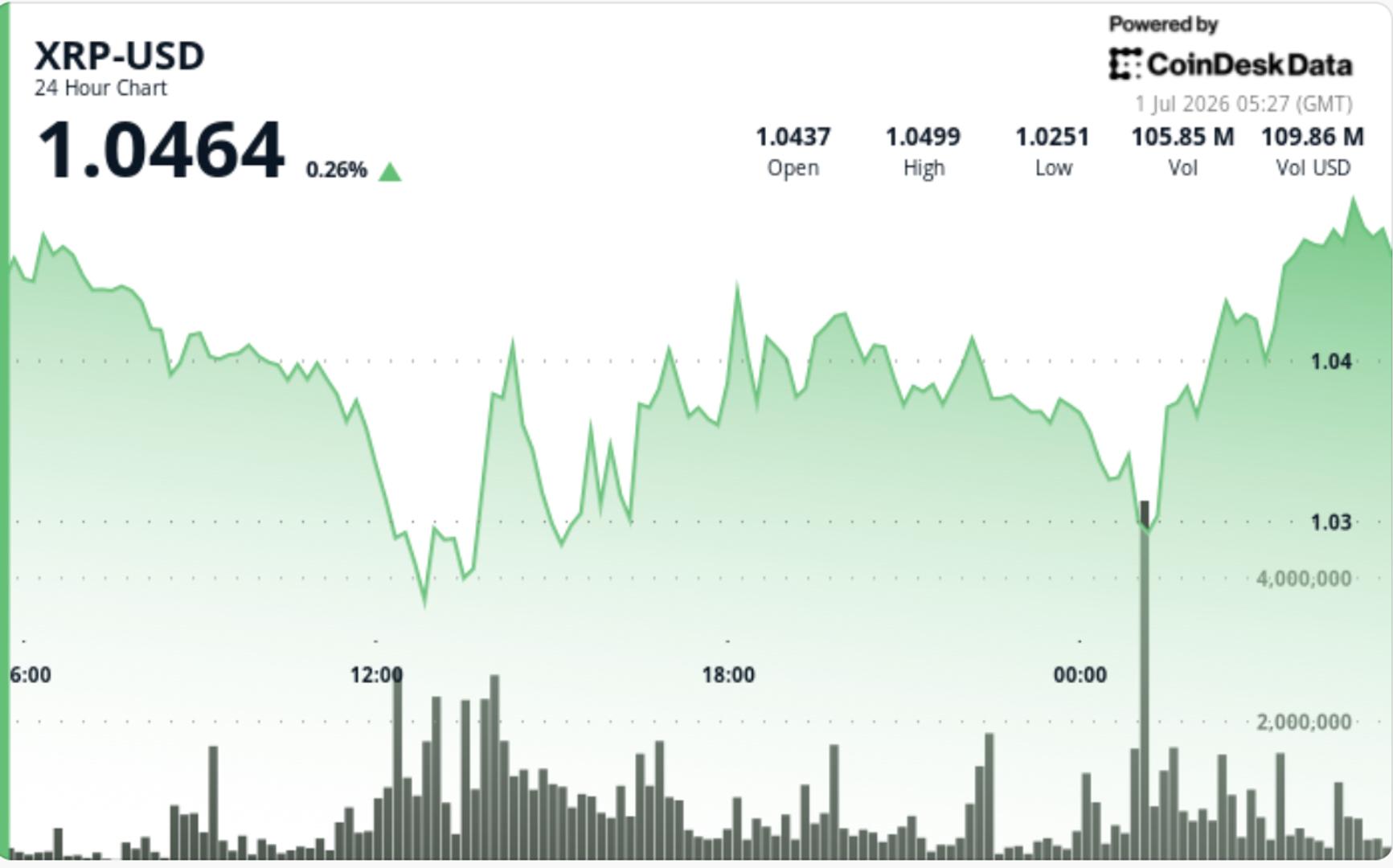

• Selling pressure broke support near $1.0350 during the June 30 session before XRP tested $1.0249 and stabilized.

• Buyers stepped in near the lows, with volume rising to 92.73 million XRP at 01:00 UTC, about 134% above the 24-hour average.

• A late rebound pushed XRP from $1.024 to $1.038, with volume spiking to 3.88 million during the break above $1.032 resistance.

Technical Analysis

• The key development is that XRP continues to defend the $1.00 area even as sentiment across crypto remains weak.

• The leverage reset improves the short-term setup. Open interest has collapsed, funding rates have turned negative and forced liquidations have cleared out crowded long positions.

• The bounce from $1.02 showed buyers are still active near support, but the move has not yet reclaimed the levels needed to shift momentum higher.

• XRP remains below major moving averages, with the 20-day EMA near $1.11, the 50-day near $1.20, the 100-day near $1.31 and the 200-day near $1.52.

• The 14-day RSI has recovered to about 33, showing selling pressure has eased, but momentum remains weak and below neutral levels.

• Bollinger Bands have narrowed after June’s selloff, pointing to lower volatility, but XRP still needs to reclaim the middle band near $1.12 to show a stronger recovery.

Zero-knowledge scaling company StarkWare has released a quantum-resistant roadmap for Starknet, arguing that other chains will remain exposed if the industry is “too stubborn or stupid” to act.

In an announcement on Tuesday, Starknet framed its three-phased quantum-resistant roadmap as evidence that the crypto industry has no excuse for remaining vulnerable to future quantum computing attacks.

“The tried-and-tested cryptography exists to secure every crypto key in the world, if necessary changes are made, and the only reason anyone will remain vulnerable is if heads remain buried in the sand,” said Eli Ben-Sasson, CEO at StarkWare.

Efforts to quantum-proof blockchains are accelerating as some researchers warn that quantum computing could outpace blockchain’s defenses and cryptographically relevant quantum machines could be ready before 2030.

The Bitcoin community remains divided on how to approach securing old coins against the quantum threat, while other networks are forging ahead with quantum roadmaps.

Ben-Sasson said Starknet can become resistant to quantum attacks by “seizing on its architecture advantage,” pointing to its zero-knowledge STARK (Scalable Transparent Argument of Knowledge) proofs, which are “inherently post-quantum safe.”

“There’s an awful irony in the notion that a young industry born from rejecting the way things have always been done is stalling and procrastinating about making changes for quantum security.”

Speaking to Cointelegraph, Ben-Sasson said that “we are currently in a position where the necessary cryptographic tools to secure our future actually exist.”

We aren’t waiting for a miracle invention; we have the solutions. It is legitimate for people to hesitate before taking on the human coordination required. That concern is real and valid. But the issue is that if we don’t address this, we will have missed the chance.

Related: Trump signs orders for quantum computer, cryptography upgrades

He added that crypto has an “elliptical illusion,” distorting reality around elliptic-curve cryptography, the current standard for securing blockchains.

Believing that this will be quantum resistant is “false confidence” that is leaving the industry “dangerously complacent,” he said.

“The migration paths we’re discussing are objectively difficult,” he said. “There are hard technical trade-offs, complex governance decisions, and a massive amount of human coordination involved. The changes needed are definitely not trivial, and I fully acknowledge the scale of the task ahead.”

“The crypto industry shouldn’t need wake-up calls from the White House or anyone else. We should all be acting and seizing on the best cryptography that exists.”

Starknet’s three-phase roadmap

The first phase involves swapping out some of its current security math (Pedersen hashing) for quantum-resistant versions and adding quantum-resistant signatures.

Phase two focuses on migration tooling that quietly upgrades existing smart contracts to the new quantum-safe standard, without forcing developers to manually rebuild apps.

Phase three covers dependencies that Starknet cannot resolve alone, which largely depend on Ethereum’s quantum upgrade roadmap.

Circle, Ethereum, Solana, Tezos and Algorand have all proposed quantum-proof roadmaps, while the Bitcoin community remains at loggerheads.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Crypto World

Taiwan passes key crypto law, raising the bar with with licensing, reserve mandates, and tough penalties

Taiwan has taken a major step forward in overseeing its digital asset sector by enacting comprehensive new regulations for cryptocurrency operations.

On Tuesday, lawmakers in the Legislative Yuan approved the Virtual Asset Service Act during its third reading, forwarding it to President Lai Ching-te for formal signing, which is anticipated within the next ten days.

Once signed, the Executive Yuan will set the official start date for the rules.

The legislation requires all virtual asset service providers, including cryptocurrency exchanges and platforms, to secure explicit licensing from the Financial Supervisory Commission (FSC) before they can legally operate in the country.

It also brings in tougher standards around cybersecurity protections, keeping customer funds separate from company assets, and strengthening internal governance and risk management.

Platforms that are already registered for anti-money laundering compliance will receive a 12-month grace period to submit license applications and up to 21 months in total to obtain full FSC approval and any other required permits. Until now, crypto businesses operating in Taiwan only needed to register for anti-money laundering compliance.

Wedbush initiated coverage of SpaceX (SPCX) with an Outperform rating and a $190 price target. The firm called SpaceX an artificial intelligence infrastructure play, not a traditional space business.

Wedbush’s Global Head of Tech Research, Dan Ives, made the case on CNBC’s Fast Money. He argued SpaceX’s AI compute business could make it one of the market’s top long-term hyperscaler bets.

Ives Builds His SpaceX Bull Case

The $190 target implies about an 11% upside from SPCX’s close on Tuesday at $170.86. Wedbush values SpaceX with a sum of the parts model. AI compute forms a major piece of that long-term thesis.

“It’s much more of an AI play, and that’s our whole view from a data perspective.”

Dan Ives, CNBC

Ives admitted the stock looks expensive against current revenue. He said execution over the next two to three years could make SpaceX one of the market’s best AI plays.

SpaceX is heading toward Nasdaq 100 inclusion. Shares recently tested a critical support level after the company’s record IPO. A later bond sale prompted some bubble warnings.

Starlink Still Anchors the SpaceX Bull Case

Starlink remains SpaceX’s real engine. The satellite broadband unit brought in roughly $11.4 billion in revenue last year, about 61% of the company’s total, and turned a solid operating profit even as SpaceX posted a net loss overall.

Wedbush’s $190 target leans heavily on Starlink’s recurring subscriber revenue and expanding margins, with the launch business and the newer AI unit layered on top.

Launch is the strategic moat, not the profit driver. Falcon 9 dominates the global launch market, and Starship aims to cut costs further by carrying more satellites per flight. But the segment brings in far less revenue than Starlink, and most of its launches simply deploy SpaceX’s own satellites rather than generate outside sales.

That breakdown is why investors are watching Starlink’s subscriber growth and margins so closely. If that business keeps scaling, it can carry a large share of SpaceX’s valuation on its own, with AI infrastructure adding upside rather than shouldering the entire bull case.

The post SpaceX Is ‘Much More Of An AI Play,’ Wedbush’s Dan Ives Says appeared first on BeInCrypto.

A community takeover, or CTO, is when the holders of an abandoned token band together and run it themselves after the original developer walks away. It is one of the defining rituals of Solana memecoin culture. Here is how a CTO works, why most fail, and what separates the rare survivor from the rest.

Summary

- A community takeover (CTO) is when the holders or broader community of a token take over running it, marketing, socials, and coordination, after the original developers abandon the project, walk away, or lose credibility.

- CTOs are most common with Solana memecoins, where tokens are fully liquid from launch, so the token keeps trading on a decentralized exchange even after the creator leaves.

- The mechanics involve the community seizing the social accounts, organizing on Telegram and X, sometimes getting listing trackers to relabel the token as a CTO, and rallying new marketing and momentum.

- The appeal is an underdog, level-playing-field narrative: with the original developer gone and no insider advantage, holders feel they finally own the project outright.

- The hard reality is that most CTOs fail and the token stays near zero, because a new logo and a Telegram group do not create real demand, and the same speculative dynamics that sank the project remain.

A community takeover, almost always shortened to CTO, is what happens when the people who hold a token decide to take over and run the project themselves after its original developers abandon it, walk away, or lose the community’s trust. It is one of the most distinctive rituals of memecoin culture, particularly on Solana, where the fast, cheap, fully liquid nature of token launches makes both abandonment and revival routine events. In a typical CTO, the founding developer of a memecoin disappears, sells their holdings, or is exposed as untrustworthy, and the token, which would normally just collapse to nothing, instead gets a second life when a group of remaining holders bands together to keep it alive.

They take over the project’s social media accounts, organize themselves in group chats, raise money for marketing, and try to generate fresh momentum around a token that technically has no team behind it anymore. The contract on the blockchain stays the same; what changes is who is steering the narrative and the community around it. The holders, in effect, seize the wheel of a car the driver has jumped out of.

Understanding the CTO is essential to understanding how the memecoin trenches actually work, because abandonment and revival are not edge cases there but core features of the landscape. This guide explains what a community takeover is and why it is possible at all, the mechanics of how a CTO unfolds step by step, why these takeovers happen so often on Solana specifically, a worked example tracing a typical CTO from abandonment to revival attempt, what separates the rare CTO that succeeds from the many that fail, and an honest look at why most CTOs go to zero and how to think about the risks.

The aim is to give you a clear and unromantic picture of a phenomenon that memecoin culture often wraps in heroic, underdog language, because the narrative of a community heroically rescuing an abandoned token is emotionally powerful and frequently used to draw in buyers, and the reality is far more sobering than the story.

This is educational material, not investment advice, and the memecoin environment it describes is among the riskiest corners of crypto.

What a CTO is and why it is possible

Start with why a community takeover can happen at all, because the answer reveals something fundamental about how memecoins are structured. When a memecoin launches on a platform like those common on Solana, the token is created with its liquidity placed in a pool on a decentralized exchange, which means the token can be bought and sold by anyone the moment it exists, with no central party required to keep the market running. The developer who launched it does not control the trading; the market lives on-chain, in a liquidity pool that functions independently of whether the creator is still involved.

This is the structural fact that makes a CTO possible. Even if the original developer completely abandons the project, sells everything, and deletes the social accounts, the token itself keeps existing on the blockchain and keeps trading on the exchange, because the liquidity pool and the contract do not depend on the creator’s presence. The project as a social and marketing entity may be dead, but the token as a tradable asset survives.

This separation between the token and its creator is what gives the community something to take over. In traditional contexts, if a company’s founders walk away, the company often simply ceases to function. But a memecoin is not a company; it is a freely trading token with a community attached, and the community can continue even when the founder does not. A community takeover is the act of that community formally adopting the orphaned token, declaring that they will now run the things the developer used to run, the social media presence, the marketing, the coordination, the narrative, and attempting to carry the project forward on collective effort alone.

Crucially, a CTO does not change the underlying token or its contract; the holders cannot rewrite the code or mint themselves new control. What they take over is everything around the token: the story, the channels, the momentum. The token is the same; the stewardship is new. This is why a CTO is sometimes described as the community inheriting a project rather than acquiring it, they take possession of an asset that was left behind, with all its existing properties intact, good and bad.

How a CTO unfolds

The mechanics of a community takeover follow a recognizable sequence, even though the details vary from case to case. It begins with the trigger: the original developer abandons the project. This can take several forms. The developer might pull the liquidity or sell their entire holding in a rug pull, crashing the price and signaling they have given up; they might quietly disappear, going silent on social media and ceasing all activity; or they might be exposed as having acted in bad faith, destroying the community’s trust even if they have not formally left. Whatever the form, the result is a token with no active team, a collapsed or collapsing price, and a community of holders sitting on losses and a decision: walk away, or try to save it.

If enough holders choose to try, the takeover organizes itself. A core group, often the most committed remaining holders, coordinates through group chats on Telegram and through posts on X, rallying the community around the idea of continuing without the developer. They take over or recreate the social media accounts, establishing new official channels under community control, since the original accounts may have been deleted or abandoned.

They frequently seek to have the token’s listing on price-tracking sites relabeled to reflect the takeover, since major trackers have processes for marking a token as community-run when the original team is gone, which updates the project’s public information to point at the new community channels. The community then tries to do the work a team would normally do: organizing marketing pushes, raising funds for promotion, sometimes coordinating to provide or lock liquidity, and generating social momentum to attract new buyers.

In the best cases, the community also pushes for transparency about who is now leading and takes steps to reassure potential buyers, such as confirming that the liquidity is locked or burned so it cannot be pulled again. The whole effort is a bet that collective enthusiasm can substitute for a founding team and breathe new life into a token the market had written off.

Why CTOs happen so often on Solana

Community takeovers are not unique to Solana, but they are far more common there than anywhere else, and the reasons are structural to how the Solana memecoin ecosystem works. The first reason is the sheer volume of memecoin launches. Solana’s low fees and fast transactions, combined with launch platforms that make creating a token nearly effortless, have produced an enormous number of memecoins, far more than could ever succeed, which means abandonment is constant and the raw material for CTOs, orphaned tokens, is abundant.

Where thousands of tokens launch and the overwhelming majority fail or are abandoned, there is a steady supply of projects a community could potentially take over. The second reason is that Solana memecoins are fully liquid from day one, trading freely on decentralized exchanges, so an abandoned token does not vanish; it keeps trading, which is the precondition for any takeover.

The third reason is cultural and narrative. The Solana memecoin scene has developed a powerful underdog mythology around the CTO, in which a community rescuing a token abandoned by a faithless developer is framed as a triumph of the people over insiders. This narrative has real emotional force in a market where traders are acutely aware that many tokens are stacked in favor of developers and early insiders. When the developer leaves, the community feels it is finally operating on a level playing field, with no insider dumping on them and no hidden team allocation, just the holders and the token.

That underdog framing, the sense of a genuine community reclaiming something and proving the doubters wrong, turns a failed launch into a movement, at least in the storytelling, and movements attract attention and buyers. The combination of constant abandonment, full liquidity, and a culture that celebrates the takeover as a heroic act makes Solana uniquely fertile ground for CTOs. It is worth being clear-eyed that this same narrative is also a marketing device, deployed precisely because it is effective at drawing in new money, which is part of why the romance of the CTO deserves scrutiny rather than acceptance.

A worked example

Trace a representative case to see how a CTO actually plays out, using an illustrative example rather than any specific real token. Picture a memecoin that launches with an appealing theme and a charismatic developer who builds an early community. The token runs up quickly as buyers pile in, reaching a meaningful market value within days. Then the developer, having accumulated a large position at launch, sells their entire holding into the buying, crashing the price by most of its value in minutes, and goes silent, deleting the project’s social accounts. The remaining holders are left with a token that has lost the vast majority of its value, no team, and no official channels. By the normal logic of memecoins, this token is dead, and most would simply go to zero from here.

But a group of holders decides to attempt a community takeover. They form a new Telegram group, recreate the project’s presence on X under community control, and begin coordinating. They publicize that the original developer is gone and frame the situation as an opportunity: the insider who was dumping on everyone has left, the liquidity that remains is now locked so it cannot be pulled again, and the token is in the hands of the community. They petition the major price-tracking sites to relabel the token as a community takeover, updating its public listing to point at the new channels.

They organize a marketing push, pooling funds to pay for promotion and rallying members to post about the revival. For a while, this can work: the CTO narrative attracts fresh attention, new buyers come in drawn by the underdog story and the apparent absence of an insider threat, and the token’s price recovers some ground on the renewed momentum. Whether this recovery lasts is the crucial question, and in the great majority of cases it does not, because, as the next section explains, enthusiasm and a new logo do not generate the durable demand a token needs to hold value. The example shows the mechanism clearly; it does not imply the mechanism usually succeeds.

What separates a rare success from the many failures

Among the flood of community takeovers, a small number achieve a real and lasting revival while most fade, and the differences between them, though they do not guarantee anything, are instructive. The first factor is transparent and credible new leadership. A CTO led by identifiable, communicative people who articulate a clear plan and follow through tends to fare better than one run anonymously with vague promises, because trust is the scarce resource in a project that has already betrayed its community once.

The second factor is the state of the liquidity. A takeover where the remaining liquidity is verifiably locked or burned, so it cannot be pulled out from under buyers again, removes one of the biggest risks and gives new participants a reason to believe the rug cannot happen twice. Checking whether liquidity-provider tokens have been burned or locked is one of the most important pieces of due diligence in any CTO.

The third factor is the distribution of holdings. A CTO where the token supply is spread across many holders is healthier than one where a few large wallets dominate, because concentrated holdings mean a small number of people can crash the price by selling, recreating the very dynamic the takeover was supposed to escape. A diversified holder base gives a revival a more stable foundation. The fourth factor, the hardest and least common, is genuine sustained effort and some reason for the token to attract ongoing attention, real marketing, real community activity, sometimes an attempt to build something beyond pure speculation.

Even with all of these factors present, success is rare, and it is essential to understand that these are markers that improve the odds at the margin, not formulas that produce a winner. The base rate is failure. The point of knowing the success factors is not to identify guaranteed revivals, which do not exist, but to recognize the warning signs in their absence: anonymous leadership, unlocked liquidity, and concentrated holdings are signals that a CTO is especially likely to fail, and their presence should make anyone considering participation far more cautious. The factors are a filter for avoiding the worst, not a recipe for finding the best.

The hard truth about CTOs and how to think about the risk

The unromantic reality, which the heroic CTO narrative tends to obscure, is that the overwhelming majority of community takeovers fail, and the token settles at or near zero regardless of the community’s effort. This is not a cynical exaggeration but the base rate of the phenomenon, and understanding why is essential. A community takeover changes the stewardship of a token, but it does not change the fundamental problem that sank the project in the first place: a memecoin has no inherent product, revenue, or utility, and its price depends entirely on continued speculative demand.

A new Telegram group, a recovered social account, and a wave of marketing can generate a burst of renewed attention, but attention is not the same as durable demand, and once the initial CTO excitement fades, the token is left exactly where it was, a speculative asset with nothing underneath it, now without even the novelty of a fresh launch. The community can work tirelessly and still fail, because the thing they are trying to revive never had a foundation to stand on.

Compounding this, the same dynamics that make memecoins dangerous in the first place persist through a takeover. The people coordinating a CTO are often the same speculators who bought in originally, with the same incentives to sell into any strength, so a price recovery driven by the CTO narrative can itself become an exit opportunity for early holders at the expense of the new buyers the narrative attracted. The underdog story that draws fresh money into a CTO is, viewed coldly, sometimes a mechanism for transferring losses from the people who held through the crash to the people who buy the revival. There are also coordination and trust problems inherent in running anything by committee with anonymous participants and no formal structure.

For anyone weighing involvement in a CTO, the honest framework is this: treat it as among the highest-risk activities in crypto, assume the base rate is failure, do the specific due diligence that can at least rule out the worst cases, checking that liquidity is locked or burned, researching who is now leading, examining whether holdings are concentrated, and never commit money you cannot afford to lose entirely, because losing it entirely is the most common outcome. The CTO is a real and fascinating feature of memecoin culture, and it occasionally produces a genuine revival, but it is a casino bet dressed in the language of community heroism, and seeing it clearly means holding both the appeal and the brutal odds in view at once.

Frequently Asked Questions

What does CTO mean in crypto?

CTO stands for community takeover. It refers to a situation where the holders or broader community of a token take over running the project after its original developers abandon it, walk away, or lose the community’s trust. The community assumes the roles a team would normally fill, controlling the social media accounts, organizing marketing, coordinating through group chats, and trying to generate fresh momentum, even though there is no longer an official team behind the token. CTOs are most common with memecoins, especially on Solana, where tokens trade freely on decentralized exchanges and so keep existing even after the creator leaves. A CTO changes who steers the project’s narrative and community, but it does not change the underlying token or its contract.

How does a community takeover work?

It usually starts when the original developer abandons the project, by selling out in a rug pull, going silent, or being exposed as untrustworthy, leaving a token with a collapsed price and no team. A core group of committed holders then coordinates, typically through Telegram and X, to keep the token alive. They take over or recreate the social accounts under community control, often get price-tracking sites to relabel the token as a community takeover, and organize marketing and fundraising to attract new attention. They may also confirm that the remaining liquidity is locked or burned to reassure buyers. The goal is to substitute collective community effort for the missing team and revive a token the market had written off. The token’s code itself does not change.

Why do community takeovers happen on Solana?

Three structural reasons. First, Solana’s low fees and easy launch platforms have produced an enormous volume of memecoins, the vast majority of which fail or are abandoned, creating a constant supply of orphaned tokens that communities could take over. Second, Solana memecoins are fully liquid from launch, trading on decentralized exchanges, so an abandoned token keeps trading instead of vanishing, which is the precondition for any takeover. Third, the culture has built a powerful underdog narrative around the CTO, framing a community rescuing an abandoned token as a triumph over faithless insiders, which has emotional force and attracts attention. The combination of abundant abandonment, full liquidity, and a celebratory culture makes Solana uniquely fertile ground for community takeovers.

Do community takeovers succeed?

Rarely. The overwhelming majority of CTOs fail, and the token settles at or near zero despite the community’s effort. The reason is that a takeover changes who runs the project but not the underlying problem: a memecoin has no inherent product, revenue, or utility, and depends entirely on speculative demand. A new social account and a marketing push can create a burst of attention, but attention is not durable demand, and once the excitement fades the token is left as a speculative asset with nothing underneath it. A small number of CTOs do achieve real revivals, usually those with transparent leadership, locked or burned liquidity, and a diversified holder base, but these are exceptions. The base rate is failure.

How can I tell if a CTO is legitimate?

There is no way to be certain, but several checks can rule out the worst cases. First, examine the new leadership: transparent, identifiable, communicative people with a clear plan are a better sign than anonymous accounts making vague promises, because the project has already betrayed its community once. Second, verify the liquidity: check whether the liquidity-provider tokens have been burned or locked, which prevents another rug pull and is one of the most important pieces of due diligence. Third, look at the holder distribution: a supply spread across many wallets is healthier than one where a few large holders could crash the price. These checks improve your odds of avoiding disasters, but they cannot identify a guaranteed winner, because most CTOs fail regardless.

Is buying into a CTO a good investment?

It is among the highest-risk activities in crypto, and this is not investment advice. The honest framework is to assume the base rate is failure, because most community takeovers end with the token near zero. The underdog narrative that draws money into a CTO can itself be a mechanism for early holders to exit at the expense of new buyers, transferring losses to the people the story attracted. The same speculative dynamics and trust problems that sank the original project usually persist. If you choose to participate anyway, do the due diligence that can rule out the worst cases, locked or burned liquidity, transparent leadership, diversified holdings, and never commit money you cannot afford to lose entirely, because total loss is the most common outcome.

This article is educational information, not financial or investment advice. Memecoins and community takeovers are among the highest-risk activities in crypto, and most result in total loss. Examples are illustrative and not references to specific tokens. Nothing here is a recommendation to buy or participate in any project. Do your own research and never risk money you cannot afford to lose.

A Manhattan federal judge sentenced Carl Erik Rinsch to 30 months in prison in an $11 million fraud case tied to an unfinished Netflix science-fiction series.

Summary

- Rinsch got 30 months after prosecutors said Netflix production funds fueled crypto and luxury spending.

- His Dogecoin trade reportedly turned about $4 million into $27 million before the case widened.

- Prosecutors sought five years, but the court imposed prison, supervised release, forfeiture and mandatory assessments.

According to the U.S. Attorney’s Office for the Southern District of New York, Rinsch was also sentenced to three years of supervised release, $11 million in forfeiture and $700 in mandatory special assessments.

Rinsch, known for directing the 2013 film “47 Ronin,” was convicted in December 2025 after a one-week trial. The case centered on funds he received to complete a streaming series called “White Horse,” which was later renamed “Conquest,” according to federal prosecutors and court records.

U.S. Attorney Jay Clayton said Rinsch sought $11 million from a subscription streaming service by falsely claiming the money would be used to finance the television show he was creating.

“Instead of using the money to make the show, Rinsch made risky bets on highly speculative stock options and cryptocurrency, and spent millions of dollars on luxury goods for himself,” said Clayton.

Production money moved into trading

Federal prosecutors said the streaming company had already paid Rinsch about $44 million between 2018 and 2019 before sending another $11 million in March 2020. The added funds were meant to complete the show, but prosecutors said Rinsch moved the money through several accounts and into a personal brokerage account.

According to the original indictment, Rinsch used the funds to trade stock options and lost more than half of the $11 million in less than two months. Prosecutors said he placed trades tied to pharmaceutical companies and the S&P 500 before moving remaining funds into cryptocurrency.

The government said Rinsch later used the money for personal expenses and luxury goods. The spending included credit card bills, legal fees, furniture, antiques, mattresses, watches, clothes, five Rolls-Royces and a Ferrari, according to the case filings.

Dogecoin profit did not end the case

As previously reported by crypto.news, Rinsch was arrested in March 2025 after prosecutors accused him of using Netflix production funds for crypto and stock bets. The case named the company as “Streaming Company-1,” but several reports identified it as Netflix.

Previously, crypto.news reported that Rinsch allegedly turned about $4 million in Dogecoin into roughly $27 million. Prosecutors said the crypto gains did not change the source of the funds, which had been provided for production work.

The Dogecoin trade became one of the most watched parts of the case. However, the court focused on whether Rinsch obtained the extra production money through false claims and used it outside the agreed purpose. Rinsch never finished the show or returned the added funds.

Prosecutors sought five years

Rinsch was convicted of one count of wire fraud, one count of money laundering and five counts of engaging in monetary transactions in property derived from unlawful activity. Wire fraud and money laundering each carried a maximum sentence of 20 years in prison, while the five other counts each carried a maximum of 10 years.

Prosecutors asked the court to sentence Rinsch to five years in prison, according to sentencing filings. His defense sought a sentence without prison time and argued that he had mental health issues, with friends and family writing to the court about changes in his behavior.

Actor Keanu Reeves, who starred in “47 Ronin,” also wrote to the court in support of Rinsch, according to AP News. The court imposed a prison sentence below the five years requested by prosecutors, but still ordered prison time, forfeiture and supervised release.

The sentence closed a case that began with Rinsch’s March 2025 arrest and continued through his December 2025 conviction. The U.S. Attorney’s Office also announced the sentencing in a post on X, saying the director had been sentenced for an $11 million production fraud.

A bridge asset is a cryptocurrency used as a neutral middle step to move value between two different currencies without pre-funding accounts in each one. XRP and XLM were both built for this job. Here is how a bridge asset works, the problem it solves, and the hard question of whether being a bridge makes a token valuable.

Summary

- A bridge asset is a cryptocurrency used as a neutral intermediary to convert one currency into another, source currency into bridge asset into destination currency, without holding pre-funded accounts in every currency.

- The problem it solves is the cost of traditional cross-border payments, where banks must lock up capital in pre-funded accounts around the world; a bridge asset frees that capital by settling in seconds.

- XRP and XLM are the two most prominent bridge assets, designed respectively for Ripple’s payment network and the Stellar network, both aiming to move value between currencies quickly and cheaply.

- The hard question is whether serving as a bridge creates lasting demand for the token, because a bridge asset is held only momentarily during a transfer, a tension known as the velocity problem.

- Stablecoins increasingly compete as bridge instruments, offering price stability that a volatile bridge token cannot, which complicates the long-term value case for bridge assets.

A bridge asset is a cryptocurrency that serves as a neutral intermediary for moving value between two different currencies, allowing a sender to convert from one currency into the bridge asset and then out into another currency, without needing to hold pre-funded balances in each currency along the way. The idea sits at the heart of one of crypto’s oldest and most practical use cases, cross-border payments, and it is the design purpose behind two of the largest cryptocurrencies by market value, XRP and XLM.

In a world where moving money across borders is slow, expensive, and capital-intensive, a bridge asset promises a faster and cheaper path: instead of a bank needing accounts pre-funded with local currency in every country it pays into, it can convert the source currency into a bridge asset, send that asset across a blockchain in seconds, and convert it into the destination currency on the other side. The bridge asset is the universal middle step, the common denominator that connects any currency to any other without requiring a direct relationship between them.

Understanding the bridge-asset concept is the key to understanding what XRP and XLM were actually built to do, and also to understanding the central debate about whether that role makes them valuable. This guide explains what a bridge asset is and the specific problem it solves, how the mechanics work step by step, how XRP and XLM each implement the idea, a worked example of a cross-border payment, the crucial difference between a bridge asset and a cross-chain bridge, and then the hard part: the unresolved question of whether being a bridge asset creates sustained demand for a token, including the velocity problem and the growing competition from stablecoins.

The aim is to give you both the clear mechanical picture and the honest analytical debate, because the bridge-asset story is genuinely useful technology wrapped around a genuinely contested investment thesis, and you cannot understand one without the other. This is educational material, not investment advice.

The problem a bridge asset solves

To see why a bridge asset is useful, you have to understand the problem with how cross-border payments traditionally work, because the bridge asset is an answer to a specific and expensive inefficiency. When money moves across borders through the conventional banking system, it travels through a network of correspondent banks, each holding accounts with the others. To pay out in a foreign currency, a bank typically needs a pre-funded account in that currency, sitting in a bank in the destination country, a setup known in the industry as nostro and vostro accounts.

The bank fills these accounts in advance with the local currency so that when a payment needs to be made, the money is already there to send. Multiply this across every currency and every corridor a large bank operates in, and the result is enormous amounts of capital locked up around the world, sitting idle in pre-funded accounts purely so that payments can be made when needed. That trapped capital has a cost, and it is one of the reasons cross-border payments are expensive, slow, and inaccessible to smaller players.

A bridge asset attacks this problem directly by eliminating the need for pre-funding. Instead of holding local currency in an account in the destination country, an institution can convert the source currency into the bridge asset at the moment of payment, send the bridge asset across a blockchain to the destination in a matter of seconds, and convert it into the local currency there, where it is paid out. Because the whole round trip happens almost instantly, there is no need to keep capital parked in advance; the liquidity is sourced and settled on demand. This is the core promise of a bridge asset: it replaces pre-funded, idle capital with just-in-time conversion, freeing up the money that would otherwise be locked in nostro accounts and making cross-border settlement faster and cheaper.

A neutral bridge asset is especially powerful because it does not belong to any one country or currency, so it can connect any pair of currencies without requiring a direct trading relationship between them. Rather than maintaining liquidity between every possible pair of currencies, which grows impossibly complex as you add currencies, institutions only need liquidity between each currency and the single common bridge. The bridge asset becomes the hub that every spoke connects to.

How the mechanics work

The mechanics of a bridge-asset payment follow a consistent pattern regardless of which asset is used, and walking through the steps shows why speed is everything. The process begins when a sender wants to move value from a source currency to a destination currency.

First, the source currency is converted into the bridge asset, typically on an exchange or liquidity venue in the source market, turning, say, dollars into the bridge token at the current market rate.

Second, the bridge asset is transferred across its blockchain from the source side to the destination side, a step that takes seconds on the networks designed for this purpose.

Third, on the destination side, the bridge asset is converted into the local currency at a liquidity venue in that market, turning the token into, say, pesos or euros, which are then paid out to the recipient.

The entire sequence, convert in, transfer, convert out, completes in seconds rather than the days a traditional cross-border transfer can take. The reason speed matters so much is that it is what makes pre-funding unnecessary, and it also limits the risk of holding the bridge asset. Because the bridge token is only held for the few seconds between conversion in and conversion out, the parties are exposed to its price for only a moment, which limits the risk that the token’s volatility moves against them during the transfer. This is essential, because bridge assets like XRP and XLM are themselves volatile cryptocurrencies, and no institution would want to hold a volatile asset for long simply to make a payment.

The design solves this by minimizing the holding time to near zero. It also depends on deep liquidity at both ends: there must be enough of a market to convert the source currency into the bridge asset, and the bridge asset into the destination currency, without large price slippage, which is why bridge-asset systems concentrate on building liquidity in the corridors they serve. When liquidity is deep and the transfer is fast, the bridge-asset path can be cheaper and faster than the correspondent-banking alternative. When liquidity is thin, the conversions become expensive and the advantage erodes, which is one of the practical limits of the model and one reason adoption has concentrated in specific corridors rather than spreading evenly everywhere.

How XRP and XLM implement the idea

XRP and XLM are the two most prominent bridge assets, and although they share the core concept, they come from related but distinct lineages. XRP is the native asset of the XRP Ledger and is the bridge asset used by Ripple’s cross-border payment offering, where it functions as the intermediary for sourcing liquidity on demand instead of pre-funding destination accounts. Ripple’s branded implementation of this, its on-demand liquidity service, is the productized version of using XRP as a bridge between currencies for institutional payments, and it is the clearest real-world deployment of the bridge-asset concept at scale.

The XRP Ledger settles transactions in a few seconds with very low fees, which are the properties a bridge asset needs, and XRP’s entire original design rationale was to serve as this neutral settlement intermediary between currencies. When people describe XRP as a “bridge currency,” this is what they mean: an asset meant to sit in the middle of cross-border value transfers, converted in and out within seconds.

XLM, the native asset of the Stellar network, was designed with a closely related purpose, and Stellar’s architecture makes the bridge role especially explicit. Stellar was built to move money between currencies cheaply, with a particular focus on payments, remittances, and financial inclusion. On Stellar, institutions called anchors issue tokens that represent fiat currencies, backed by reserves, and the network includes a built-in decentralized exchange and a feature called path payments that automatically finds the cheapest route to convert one asset into another. XLM serves as a bridge in this system, a neutral asset that can connect currency pairs that lack a direct market, and it is also used to pay the network’s small transaction fees.

So both assets are built around the same fundamental idea, a fast, cheap, neutral intermediary for moving value between currencies, but XRP is most associated with institutional, bank-facing cross-border payments through Ripple, while XLM is most associated with a more open, anchor-based network oriented toward payments and financial inclusion. Both illustrate the bridge-asset concept in production, and both face the same hard question about whether the role translates into lasting token value.

A worked example

Trace a single payment to make the concept concrete. Imagine a business in the United States needs to pay a supplier in Mexico the equivalent of $10,000, and consider how this works with and without a bridge asset. In the traditional model, the US business’s bank would rely on having a pre-funded account holding Mexican pesos at a bank in Mexico, or on a chain of correspondent banks that do. The payment instruction passes through this chain, the pesos are paid out from the pre-funded account, and the whole process can take one to several business days, with fees taken at multiple points and a large amount of peso liquidity sitting idle in that account at all times to make such payments possible. The cost of that idle capital, plus the intermediary fees, is what makes the traditional transfer expensive.

In the bridge-asset model, the same payment takes a different path. The $10,000 is converted into a bridge asset, say XRP or XLM, on a liquidity venue in the United States, turning dollars into the token at the current rate. The bridge asset is then sent across its blockchain to Mexico in a matter of seconds. On the Mexican side, the bridge asset is immediately converted into pesos on a local liquidity venue, and the pesos are paid out to the supplier.

The entire round trip completes in seconds, and at no point did anyone need to keep pesos pre-funded in advance, because the liquidity was sourced on demand at the moment of payment. The business’s bank did not need idle peso capital sitting in Mexico; it converted exactly what it needed, exactly when it needed it. If the liquidity on both ends is deep, the total cost of the two conversions plus the tiny network fee can be lower than the traditional route, and the settlement is far faster. This is the bridge asset doing its job: replacing days and pre-funded capital with seconds and just-in-time conversion. The token was held for only the few seconds of the transfer, which is the whole point of the design, and also, as the next sections explain, the source of the central debate about its value.

Bridge asset versus cross-chain bridge

A crucial point of confusion deserves its own section, because the word “bridge” is used in two very different ways in crypto and conflating them leads to real misunderstanding. The bridge asset described in this guide is about moving value between currencies, an asset used as a neutral intermediary to convert one currency into another in a payment. A cross-chain bridge, by contrast, is about moving tokens between blockchains, a piece of infrastructure that lets you take a token on one blockchain and represent or transfer it onto a different blockchain, for example moving an asset from Ethereum to another network. These are entirely different concepts that happen to share a word. A bridge asset is a currency playing a role in a payment; a cross-chain bridge is software connecting two blockchains, often by locking a token on one chain and minting a wrapped version on another.

The distinction matters for several reasons. First, the risks are completely different. Cross-chain bridges have been among the most exploited pieces of infrastructure in crypto, with several large hacks resulting from vulnerabilities in the smart contracts that lock and mint tokens across chains, so “bridge risk” in that context refers to the security of that connecting infrastructure. A bridge asset used in a payment carries different risks, mainly the price volatility of the token during the brief moment it is held and the depth of liquidity on each side, not smart-contract exploit risk of a chain-connecting bridge.

Second, the purpose is different: a bridge asset answers “how do I move value from one currency to another,” while a cross-chain bridge answers “how do I move a token from one blockchain to another.” When you read about XRP or XLM as bridge assets, the meaning is the currency-to-currency payments sense, not the chain-to-chain infrastructure sense. Keeping the two ideas separate is essential to understanding both the technology and the risks, because a discussion that mixes them will mislead on both. The shared word is an unfortunate accident of terminology, and the careful reader learns to ask which kind of bridge is meant.

Does being a bridge asset make a token valuable?

Now the hard question, the one that turns a clean technical story into a truly contested investment debate: does serving as a bridge asset actually create lasting demand for the token, and therefore support its value? The intuitive answer is yes, surely a token used to move large volumes of cross-border payments must capture value from that usage. But the reality is more complicated, and the complication has a name: the velocity problem.

A bridge asset, by design, is held for only the few seconds of a transfer. It is bought, used, and sold almost instantly, never accumulated. High transaction volume through a bridge asset therefore does not necessarily translate into sustained holding demand, because the same units of the token can be reused over and over for many transfers without anyone needing to hold a growing stockpile. A token can process enormous payment volume while generating little persistent demand to own it, because payments require the token to flow through, not to be held. This is the core tension in the bridge-asset value thesis, and it is why critics argue that network usage and token price can diverge: the network can be busy while the token is weak.

There is a serious counterargument, and the honest treatment gives it weight. Proponents contend that very large and growing payment volume does require deeper liquidity pools at every conversion point, and that maintaining those pools effectively takes a meaningful float of the token out of circulation, creating a baseline of demand that scales with usage. They argue that if a bridge asset became the settlement layer for a significant share of global cross-border value, the liquidity required to support that volume without slippage would be substantial and persistent, supporting the token’s value even if no individual holder keeps it for long.

The debate, then, is between the velocity critique, which says payments flow through without creating holding demand, and the liquidity-depth argument, which says sufficient scale forces a persistent float. Layered on top is a growing competitive threat: stablecoins. A stablecoin pegged to a currency can serve as a bridge instrument too, moving value between parties quickly, and it offers something a volatile bridge token cannot, price stability, so neither sender nor receiver bears volatility risk during the transfer.

As regulated stablecoins proliferate, including ones issued by the very companies behind bridge-asset networks, some of the cross-border settlement role that bridge tokens were meant to fill may flow to stablecoins instead, which would weaken the demand case for the volatile bridge asset. None of this is settled, and a careful reader should hold all of it at once: the bridge-asset technology is real and useful, the velocity problem is a genuine challenge to the token-value thesis, the liquidity-depth rebuttal is a legitimate counter, and stablecoin competition is a real and growing complication. The mechanism works; whether it makes the token valuable is the open question.

Frequently Asked Questions

What is a bridge asset in crypto?

A bridge asset is a cryptocurrency used as a neutral intermediary to move value between two different currencies. Instead of converting one currency directly into another, or keeping pre-funded accounts in every currency, a sender converts the source currency into the bridge asset, sends that asset across a blockchain in seconds, and converts it into the destination currency on the other side. The bridge asset is the common middle step that can connect any currency to any other without a direct relationship between them. XRP and XLM are the two most prominent examples, both designed to make cross-border payments faster and cheaper by replacing idle pre-funded capital with just-in-time conversion through the bridge token.

How is XRP used as a bridge asset?

XRP is the native asset of the XRP Ledger and serves as the bridge in Ripple’s cross-border payment system. Instead of a bank pre-funding accounts with local currency in every destination country, it can convert the source currency into XRP, send the XRP across the ledger in a few seconds at very low cost, and convert it into the destination currency on arrival. Ripple’s branded version of this is its on-demand liquidity service, the productized use of XRP as a settlement bridge for institutional payments. XRP’s original design purpose was exactly this neutral-intermediary role, which is why it is described as a bridge currency: an asset meant to sit briefly in the middle of cross-border value transfers.

Is XLM the same as XRP?

They share the same core idea but are distinct assets on distinct networks. XLM is the native asset of the Stellar network, which was built to move money between currencies cheaply with a focus on payments, remittances, and financial inclusion. On Stellar, institutions called anchors issue fiat-backed tokens, and the network’s built-in exchange and path-payment feature find the cheapest route to convert one asset into another, with XLM serving as a bridge between pairs that lack a direct market and paying the network’s small fees. XRP, by contrast, is most associated with institutional, bank-facing cross-border payments through Ripple. Both are bridge assets built around fast, cheap, neutral settlement, but they come from different networks with different emphases.

What problem does a bridge asset solve?

It solves the cost and slowness of traditional cross-border payments, specifically the need to pre-fund accounts. In the conventional system, a bank must keep accounts filled in advance with local currency in every country it pays into, known as nostro and vostro accounts, which locks up enormous amounts of capital sitting idle around the world. A bridge asset removes this need by sourcing liquidity on demand: the institution converts into the bridge asset and out into the destination currency at the moment of payment, in seconds, so no capital has to sit pre-funded. This frees up trapped liquidity and can make cross-border settlement faster and cheaper, which is the central promise of the bridge-asset model.

Does high payment volume make a bridge asset valuable?

Not necessarily, and this is the central debate. A bridge asset is held for only the few seconds of a transfer, so it is bought, used, and sold almost instantly instead of accumulated. This means high payment volume does not automatically create sustained demand to hold the token, because the same units can be reused for many transfers, a tension known as the velocity problem. Proponents counter that very large volume requires deeper liquidity pools, which take a meaningful float out of circulation and create demand that scales with usage. The question is unresolved, and it is complicated further by stablecoins, which can serve as bridge instruments too while offering price stability a volatile token cannot.

Is a bridge asset the same as a cross-chain bridge?

No, and confusing them is a common error. A bridge asset is a currency used to move value between two different currencies in a payment. A cross-chain bridge is infrastructure that moves tokens between two different blockchains, often by locking a token on one chain and minting a wrapped version on another. They share the word “bridge” but are entirely different concepts with different risks. Cross-chain bridges have been frequently exploited through smart-contract vulnerabilities, so their risk is about infrastructure security, while a bridge asset’s risks are mainly the token’s price volatility during the brief holding period and the depth of liquidity on each side. When XRP or XLM are called bridge assets, the meaning is the currency-to-currency payments sense.

This article is educational information, not financial or investment advice. Descriptions of XRP, XLM, and their networks reflect their design and general operation as understood in mid-2026 and can change. Nothing here is a recommendation about any asset, and the question of whether bridge assets accrue value is truly contested. Cryptocurrency is volatile, and you can lose money. Do your own research and consult a qualified professional before making any decision.

Men reveal how often they really think about ‘the one that got away’

Abivax Stock Soars 34% Today as New Trial Data Eases Cancer Fears Over Bowel Disease Drug Obefazimod

Taiwan passes crypto law for exchanges and stablecoins

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World1 day ago

Crypto World1 day agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business1 day ago

Business1 day agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Tech1 day ago

Tech1 day agoAnonymous researcher drops 0-day ‘exploitarium’ repo

You must be logged in to post a comment Login