Business

Stock market gains mint new millionaires in 2025: UBS

The New York Stock Exchange on April 14, 2025.

View Press | Corbis News | Getty Images

A version of this article first appeared in CNBC’s Inside Wealth newsletter with Robert Frank, a weekly guide to the high-net-worth investor and consumer. Sign up to receive future editions, straight to your inbox.

Nearly 1 million people became millionaires in 2025, largely thanks to a thriving stock market, according to a new report by UBS.

The Swiss bank estimated that the United States is responsible for nearly half of these newly minted millionaires, adding an average of more than 1,200 new millionaires a day last year for an annual increase of about 441,000.

Stock market gains boosted global personal wealth by 10.8%, the biggest jump since 2017 and more than double the rate of 2024 and 2023, UBS found. However, this robust growth was belied by declines in median wealth in most of the 56 markets monitored by UBS, pointing to a growing wealth gap.

In the U.S., for example, median wealth per adult dropped nearly 20% from 2020 to 2025, while average wealth increased by about 10% over the same period of time, net of inflation, according to the bank’s data analysis.

UBS estimated that the world’s millionaire population, which the bank puts at 58 million, owns nearly half of the world’s wealth, or approximately $250.6 trillion.

UBS economist James Mazeau told CNBC that richer individuals reaped bigger gains compared with the broader population last year as they have more exposure to financial markets, noting that the U.S. stock market rose by approximately 18% in 2025.

“The higher you go in the wealth bands, the more wealth creation will tend to be linked to either the performance of your business or your investment portfolio — or both,” Mazeau said at a media conference.

These gains are also uneven among the ranks of millionaires. The bank estimated that the combined assets of so-called everyday millionaires, or individuals worth $1 million to $5 million, has jumped by 170%, net of inflation, since 2000. Over that same period, the collective fortune of richer peers soared by 343%.

As for the world’s billionaires, their collective net worth surged by nearly 25% in the year ended in April, according to UBS. However, the report noted that much of this rise was due to an increase in the number of billionaires, not just three-comma club members getting richer.

The depreciation of the U.S. dollar last year also contributed to discrepancies in global wealth creation as the bank tracks wealth in terms of USD. America’s millionaire population, while still the largest in the world, increased by a modest 1.9% in 2025, while most European and Middle Eastern markets saw higher percentage gains, including Turkey (6.4%) and the United Arab Emirates (3.5%). In terms of combined personal assets, the Americas’ growth rate was estimated at 8.5%, outranking the Asia-Pacific region at 5.9% but less than half of the 17.5% rate seen in Europe, the Middle East and Africa.

Mazeau said it is too early to predict how the Iran war will weigh on high-net-worth individuals in the Middle East. Asset allocation and currency trends are two of many factors that will determine the outcome.

“It will really depend on what share of international assets are held by these investors. If you are, let’s say, based in the Middle East, and most of your wealth is tied into U.S. stocks, and furthermore, you have a currency that’s pegged to the U.S. dollar, well, the currency moves really don’t matter at all,” he said. “Now, if you tend to diversify your holdings into other investments that tend to be in currencies that have appreciated versus the U.S. dollar, and if we measure things in U.S. dollars, then that will, for 2026 get a bit better outlook.”

He added that investors may have changed their portfolios as a result of the conflict.

“Will they diversify their holdings? Will they make more direct investments in the U.S.? How will the situation that unfolded change the investment landscape and the investment philosophy and asset allocation?” he said. “I don’t know yet.”

Form 4 Aehr Test Systems For: 2 July

Business

Palantir Stock Surges 3.5% Again Today After D.A. Davidson Upgrades to Buy, Cites Most Attractive Valuation

Palantir Technologies shares climbed further Thursday morning, adding to a string of daily gains as a fresh analyst upgrade from D.A. Davidson’s Gil Luria amplified momentum already building from a Nvidia partnership announcement, a U.S. government contract win and the partial retreat of one of the stock’s most prominent short sellers.

Shares of the Denver-based AI software and data analytics company were trading at $130.19 as of 10:47 a.m. EDT, up $4.46, or 3.55%, on the day, extending what has been a sharp recovery from the 52-week low of $106.37 the stock hit just two weeks ago. The multiple-day winning streak has now pushed the stock roughly 23% off that low, though shares remain approximately 37% below their 52-week high of $207.18 reached in late November 2025.

Thursday’s specific catalyst was D.A. Davidson analyst Gil Luria upgrading Palantir from Neutral to Buy and raising his 12-month price target to $175 from $165, implying upside of roughly 39% from Wednesday’s closing price. Palantir shares rose more than 3% in the immediate aftermath of the upgrade publication, with the stock continuing to add to those gains as the broader market also strengthened following the weaker-than-expected June nonfarm payrolls report.

Luria’s upgrade framing was pointed and specific, centering on both valuation and a newly articulated competitive advantage argument tied to the ongoing friction between AI model providers and the U.S. government. He cited recent tensions between Anthropic and the Trump administration, which had placed restrictions on the company’s AI models, as evidence that customers who built their technology stacks on top of underlying AI models directly faced serious business disruption risk when those models became unavailable.

“Anthropic’s repeated choice to take a confrontational tact with the US government has resulted in the government placing restrictions on AI models and Anthropic pulling its own model from the market,” Luria said in a note to clients, adding that companies that built directly on those models risked catastrophic disruption. He contrasted that risk with Palantir’s orchestration model, where the company’s platform can swap underlying AI models without disrupting the broader solution it delivers to clients.

On valuation, Luria was equally direct.

“We believe Palantir’s valuation is the most attractive it has been in a while, especially in relation to other high growth software companies,” he said.

That argument resonates with a growing portion of the investment community that has been watching Palantir’s stock decline throughout 2026 while its underlying business has continued to accelerate. The company’s first-quarter results, the most recent available, showed revenue surging 85% year over year to $1.63 billion, beating estimates of $1.54 billion, while the company raised its full-year 2026 revenue guidance to approximately $7.65 billion. Operating margin for the first quarter reached 60% on an adjusted basis, and the company now counts more than 1,000 commercial customers, a milestone that underscores how broadly its AI platform has penetrated enterprise markets beyond its traditional government base.

Yet the stock had fallen approximately 29% year to date heading into the current recovery, a decline that reflected persistent investor concerns about competition from OpenAI, Anthropic and other AI tool providers that could eventually allow enterprise customers to replace dedicated data orchestration platforms like Palantir with more commodity-like AI services. Luria’s analysis suggests that very threat, and the political and regulatory complications that have accompanied it, may be creating demand for Palantir’s model rather than eroding it.

Palantir CEO Alex Karp also added to the week’s storyline Wednesday, when he used a public appearance to criticize what he called “tokenmaxxing,” a reference to AI providers who charge per token in ways that create what he characterized as a “wealth tax” on enterprise customers using AI tools at scale. Karp’s language was direct and provocative, positioning Palantir as a more efficient and accountable alternative to the per-token pricing models that have drawn increasing customer scrutiny as AI usage scales.

“Combining Palantir infrastructure with Nvidia’s AI and Nemotron models will allow the U.S. government to unleash the full power of LLMs while removing the underlying security risks,” Karp said in a statement accompanying the Nvidia partnership announcement earlier this week.

That Nvidia collaboration, announced Monday, involves embedding Nvidia’s Nemotron open-source AI models into Palantir’s core product stack, including its AIP, Foundry, Ontology and Apollo platforms, creating what the companies described as a secure, customizable environment for U.S. government agencies and critical infrastructure operators to train, customize and deploy large language models without exposing sensitive data to external model providers.

President Trump’s most recent financial disclosure added an unusual political dimension to the recovery. The U.S. Office of Government Ethics released Trump’s certified 2025 financial disclosure showing he owns at least $1 million in Palantir shares, a holding he reportedly added to in the period covered by the disclosure. While the filing does not establish any formal commercial relationship between the administration and the company, market observers noted it attracted renewed retail investor attention to the stock in the days immediately following its release.

“Big Short” investor Michael Burry, whose publicly disclosed short position against Palantir had been a recurring negative overhang on the stock throughout the spring, disclosed he had trimmed roughly half of that position, a partial retreat that some investors interpreted as a signal that even a prominent bear had decided the stock’s decline had run its course, at least for now.

According to data from 32 analysts tracked by Stock Analysis, the consensus rating on Palantir stands at “Buy,” with an average 12-month price target of $182.75, representing potential upside of more than 40% from Thursday’s trading levels. With the D.A. Davidson upgrade adding to that bullish chorus, investors now appear to be coalescing around the view that Palantir’s prolonged valuation compression has created the most attractive entry point the stock has offered since before its 2025 run to all-time highs, particularly given the acceleration in its underlying business metrics.

Business

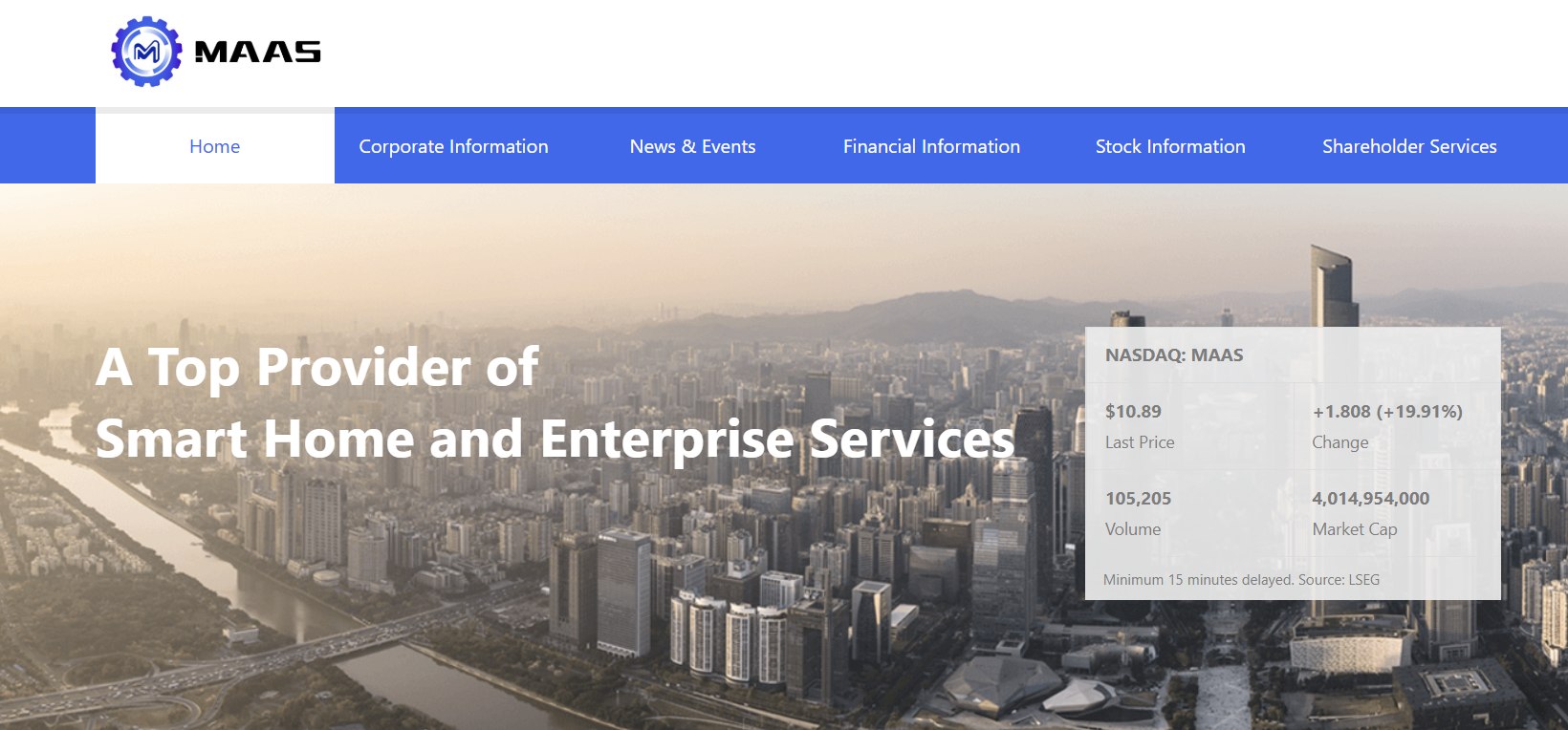

Maase Inc. Shares Rocket 20% on AI Computing Projects as Chinese Tech Pivot Ignites Small-Cap Rally

Maase Inc. shares surged nearly 20% to $18.70 in morning trading Thursday, continuing a remarkable run as the Chinese company advances multiple AI infrastructure initiatives following a series of strategic acquisitions.

The rapid re-rating of the former wealth management and insurance services firm reflects investor enthusiasm for its transformation into a full-stack AI operator focused on computing power, intelligent hardware and energy solutions. Maase has announced ambitious projects, including large-scale distributed intelligent computing centers, positioning it among a wave of smaller players chasing opportunities in China’s expanding AI sector.

Headquartered in Chengdu, Maase operates as an integrated provider of AI-centric digital systems. The company has completed several key acquisitions in recent months, including Huazhi Future and Times Good, aimed at building capabilities across computing infrastructure, algorithms and green energy applications.

In April, Maase announced the launch of the Stars Distributed Intelligent Computing Center Project with partners, outlining a planned investment of up to RMB5 billion. The initiative underscores ambitions to scale high-performance computing resources critical for AI training and deployment.

Subsidiary Huazhi Future has established a green energy infrastructure research team, designating 800VDC technology as a core focus. Additional collaborations explored with entities in Xinjiang and state-linked groups signal efforts to integrate sustainable power sources with AI computing demands.

Aggressive Acquisition Strategy

Maase’s pivot accelerated with the March completion of the Huazhi Group acquisition, described by the company as establishing “full-stack AI self-controllability.” Earlier deals targeted assets in new energy technologies and intelligent services.

The company, which began as Highest Performances Holdings, has methodically shifted its portfolio. Financial filings detail the integration of acquired businesses to create closed-loop solutions spanning hardware, software and deployment.

Such transformations are common in China’s technology landscape, where policy support for AI and domestic innovation encourages rapid evolution. However, execution risks remain high for smaller firms navigating complex integration and capital requirements.

Maase reported ongoing financial challenges typical of growth-stage tech companies, with historical losses as it invests in new capabilities. Recent interim filings provide updates on post-acquisition performance, though full details on synergies are still emerging.

Market Reaction and Valuation

The stock’s volatility reflects its speculative appeal. Year-to-date gains have been substantial, with periodic pullbacks as profit-taking occurs amid thin trading and limited analyst coverage. Thursday’s advance added to momentum built on successive positive announcements.

Trading volumes have spiked during rallies, characteristic of retail-driven small-cap moves in AI-themed names. With a market capitalization in the billions despite modest revenue scale, the valuation incorporates significant expectations for future growth.

Analysts caution that many such pivots face hurdles in delivering sustainable profits. Capital intensity for data centers and computing projects requires substantial funding, potentially through partnerships, debt or equity raises that could dilute shareholders.

Maase’s focus on green AI computing aligns with broader industry efforts to address energy consumption concerns around large-scale artificial intelligence. Collaborations on power infrastructure could differentiate it if successfully executed.

Competitive Landscape in AI Infrastructure

China’s AI push receives strong government backing, with national strategies emphasizing technological self-reliance. Major state-backed and private players dominate core infrastructure, leaving opportunities for specialized or regional operators in distributed computing and edge applications.

Maase’s distributed computing center approach aims to provide flexible, scalable resources potentially serving enterprises across industries. Success depends on securing customers, maintaining technological competitiveness and managing operational complexities.

The company’s earlier roots in financial services provide some experience in customer-facing platforms, which it seeks to leverage in AI-enabled intelligent networks and commercial applications.

Broader market enthusiasm for AI has propelled numerous Chinese and U.S.-listed stocks, though sustainability varies. Sentiment can shift quickly on regulatory news, macroeconomic developments or competitive announcements.

Risks and Long-Term Outlook

Investors face elevated risks with Maase, including integration challenges from rapid acquisitions, execution on large projects and dependency on favorable policy and funding environments. Geopolitical tensions and export controls on advanced chips could impact technology access.

Financial metrics indicate the company continues investing heavily, with profitability potentially years away if AI initiatives scale as hoped. Dilution, debt levels and cash burn warrant monitoring in future reports.

Positive catalysts could include contract wins, project milestones or further strategic partnerships. Conversely, delays or disappointing financial updates might trigger sharp reversals given current valuations.

As a Nasdaq-listed entity with primary operations in China, Maase navigates cross-border regulatory considerations, including reporting requirements and audit standards for U.S. investors.

The company’s trajectory exemplifies the high-reward, high-risk nature of technology sector transformations. While AI infrastructure demand offers substantial addressable markets, realizing value requires disciplined execution amid intense competition.

Market watchers will track upcoming filings for progress on integration and project timelines. For now, Maase’s stock performance highlights how narrative shifts and acquisition news can drive significant repricing in small-cap technology plays.

Broader adoption of AI across Chinese industries could provide tailwinds if Maase establishes defensible positions in computing power and intelligent systems. Investors are betting on management’s ability to capitalize on the ongoing technological wave.

Check out what’s clicking on FoxBusiness.com.

The Food and Drug Administration has upgraded a recall of certain Utz Quality Foods potato chips to its highest risk classification, warning consumers ahead of the Fourth of July holiday that the products carry a reasonable probability of causing serious health consequences or death if contaminated with salmonella.

The FDA designated the recall as a Class I recall after Utz voluntarily recalled certain Zapp’s and Dirty brand potato chips sold nationwide in May. The products were pulled after the company learned a seasoning ingredient used during production contained dry milk powder that could potentially be contaminated with salmonella.

The timing comes as many Americans stock up on chips and other snacks for Independence Day cookouts and gatherings.

According to the FDA, a Class I recall is issued when there is a reasonable probability that using or being exposed to a product will cause serious adverse health consequences or death. It is the agency’s most serious recall classification.

CHECK YOUR AC: 13,000 UNITS RECALLED OVER FIRE RISK

Utz Quality Foods is recalling certain Zapp’s 1.5-oz. Bayou Blackened Ranch Potato Chips. (FDA / Fox News)

The recall covers select Zapp’s Bayou Blackened Ranch, Salt and Vinegar and Big Cheezy potato chips, along with Dirty brand Salt and Vinegar, Maui Onion and Sour Cream and Onion potato chips. The products were sold at retailers nationwide with “Best By” dates ranging from Aug. 3, 2026, through Aug. 31, 2026. No other Utz products are included in the recall.

When Utz announced the voluntary recall in May, the company told FOX Business that the seasoning used on the affected chips had initially tested negative for salmonella before production. It later learned from an ingredient supplier that the seasoning contained dry milk powder sourced from California Dairies Inc. through a third-party supplier that was subject to a separate recall.

The company said it initiated the recall out of an abundance of caution and had not received any reports of illness linked to the affected products.

“We are working in coordination with the U.S. Food and Drug Administration on this recall,” Utz said in a statement at the time.

POPULAR POTATO CHIPS RECALLED DUE TO SALMONELLA FEARS

Utz Quality Foods is recalling Dirty brand Salt and Vinegar Potato Chips. (FDA / Fox News)

The potato chips are among dozens of products recalled after being linked to the contaminated dry milk ingredient, which has also prompted recalls involving other snack foods and seasonings.

| Ticker | Security | Last | Change | Change % |

|---|---|---|---|---|

| UTZ | UTZ BRANDS INC | 8.27 | +0.08 | +0.98% |

CLICK HERE TO GET FOX BUSINESS ON THE GO

Consumers who purchased the affected chips should not eat them and should discard the products.

According to the Centers for Disease Control and Prevention, salmonella can cause fever, diarrhea, nausea, vomiting and abdominal pain. While most healthy people recover without treatment, infections can become severe or even life-threatening for young children, older adults and people with weakened immune systems. In rare cases, the bacteria can spread to the bloodstream and cause more serious complications.

FOX Business’ Matthew Kazin also contributed to this report.

Oracle Corp. shares traded modestly higher Thursday near $143 as investors digested the software giant’s strong fiscal 2026 results, marked by explosive growth in cloud infrastructure and artificial intelligence workloads even as capital spending soared to support expansion.

The database and enterprise software leader posted record full-year revenue of $67.4 billion, up 17% from the prior year, with cloud services driving much of the acceleration. Fiscal fourth-quarter revenue reached $19.18 billion, exceeding expectations, while cloud infrastructure revenue nearly doubled.

Oracle’s transformation into a major cloud and AI infrastructure provider has gained momentum, with significant contracts from leading technology companies seeking computing capacity for large-scale AI models. The company delivered over 1.2 gigawatts of data center capacity during the fiscal year, with delivery pace accelerating into fiscal 2027.

Chief executives have highlighted robust demand. In prepared remarks and filings, Oracle leadership pointed to a massive remaining performance obligation backlog, underscoring committed future revenue from AI-related deals.

The results come as Oracle navigates leadership transitions, with new co-CEOs overseeing day-to-day operations amid continued strategic direction from Chairman Larry Ellison. Heavy investments in data centers have pressured free cash flow in the short term but are viewed as essential for capturing market share in the competitive cloud sector.

Cloud and AI Momentum Accelerates

Oracle Cloud Infrastructure (OCI) posted standout growth, with revenue surging 93% in the fourth quarter to approximately $5.8 billion. Overall cloud revenue climbed 47% to nearly $10 billion in the period, reflecting broad adoption across enterprise customers.

Multicloud strategies, including partnerships with major hyperscalers, have expanded Oracle’s reach. The company has emphasized its ability to provide high-performance computing environments optimized for AI training and inference, differentiating through database integration and enterprise-grade security.

Fiscal 2026 marked a pivotal year as AI workloads drove demand for both infrastructure and applications. Oracle reported signing substantial contracts with prominent AI developers and technology firms, contributing to a remaining performance obligation approaching record levels.

Analysts have noted Oracle’s unique position at the intersection of traditional enterprise software and modern cloud infrastructure. Its database business, a long-time strength, benefits from AI-driven data management needs, with multicloud database revenue showing triple-digit growth in prior periods.

Capital expenditures totaled tens of billions for the year, reflecting aggressive data center buildout. While this has led to negative free cash flow in some metrics, management maintains that such spending positions the company for sustained high-teens revenue growth.

Oracle guided for continued strong performance, with expectations for fiscal 2027 revenue expansion in the mid- to high-teens percentage range, supported by backlog conversion and new customer wins.

Leadership and Strategic Direction

Following Safra Catz’s tenure as CEO, Oracle has implemented a co-CEO structure with executives Mike Sicilia and Clay Magouyrk taking operational leadership. Ellison remains actively involved as chairman and chief technology officer, providing strategic vision particularly around AI and cloud technologies.

The leadership evolution coincides with Oracle’s heaviest period of investment. Executives have stressed a commitment to chip neutrality, partnering with multiple vendors including Nvidia while optimizing for customer preferences.

Oracle’s applications business, including ERP, HCM and CX suites, posted steady growth with AI enhancements helping drive adoption. New AI agents for finance, HR and other functions aim to automate enterprise processes, expanding the total addressable market.

The company’s healthcare offerings, bolstered by Cerner, are expected to benefit from AI integrations in patient care and operational efficiency.

Market Position and Challenges

Oracle competes with Amazon Web Services, Microsoft Azure and Google Cloud in infrastructure, while maintaining leadership in enterprise applications. Its differentiated approach — combining cloud with proven database and middleware technologies — appeals to large organizations wary of full rip-and-replace migrations.

Heavy capex has drawn scrutiny, with some investors questioning the return timeline amid intense competition. Oracle has responded by highlighting high utilization rates in new capacity and strong renewal trends among GPU customers.

Stock performance has been volatile, with shares pulling back from highs earlier in 2026 despite fundamental progress. Analysts cite concerns over valuation and spending levels, though many maintain positive outlooks based on backlog visibility and AI tailwinds.

Oracle’s fiscal year ends in May, providing a full-year view of progress under accelerated cloud investments. The company plans to raise additional capital through equity and debt offerings to fund ongoing expansion without compromising financial flexibility.

Outlook and Industry Trends

Demand for AI infrastructure remains robust globally, with enterprises and technology providers racing to secure capacity. Oracle’s ability to deliver at scale while integrating with existing enterprise environments positions it favorably for multiyear contracts.

Broader technology spending trends, including digital transformation and data analytics, support Oracle’s core businesses. Potential economic slowdowns could temper growth, but AI investments have shown resilience.

Regulatory scrutiny of big tech and data centers, along with energy availability, represent external risks. Oracle has emphasized sustainable practices and efficiency in its infrastructure plans.

For the current quarter, Oracle is expected to report continued momentum when it releases fiscal first-quarter 2027 results in September. Guidance will be closely watched for updates on capex trajectory and cloud growth rates.

Oracle’s evolution from database pioneer to cloud and AI powerhouse demonstrates adaptability in a rapidly changing industry. While short-term financial metrics reflect investment costs, the strategic foundation appears solid amid strong secular demand.

Investors will continue balancing enthusiasm for AI growth against near-term cash flow pressures and competitive dynamics. Oracle’s track record of execution in enterprise technology suggests potential to translate backlog into sustained revenue acceleration.

Two of the world’s most powerful advertising and artificial intelligence businesses are heading into the second half of 2026 in very different positions than where they started the year, and the question of which one to buy has become considerably more complex and more interesting than it was six months ago.

Meta Platforms surged more than 7% on Wednesday alone after Bloomberg reported the company plans to enter the cloud computing business by selling its excess AI computing capacity to external customers, pushing the stock above $600 for the first time in weeks and adding an entirely new revenue dimension to the investment case. Alphabet, meanwhile, joined the Dow Jones Industrial Average last week, was reclassified as a pure growth stock by FTSE Russell, and closed out the first half of 2026 as the undisputed favorite among institutional investors hunting for value in the megacap technology space.

Understanding which stock makes more sense for an individual investor in 2026 requires separating the narrative from the numbers, and the numbers from the trajectory.

Revenue and Growth: Meta Leads But Alphabet Is More Diversified

Meta’s first-quarter 2026 results, reported on April 29, showed advertising revenue reaching $55.02 billion, up 33% year over year, with ad impressions rising 19% and price per ad climbing 12%, both powered by AI-driven targeting improvements that have made Meta’s advertising products more effective and therefore more expensive per impression.

Meta chief executive Mark Zuckerberg called the performance “a milestone quarter” tied to the first model from Meta Superintelligence Labs, the AI research division the company has been building at enormous cost. But Reality Labs, the division responsible for virtual and augmented reality development including Meta’s AI glasses and the broader metaverse initiative, posted a $4.03 billion operating loss on only $402 million in revenue for the quarter, a drag that has persistently overshadowed the core advertising business’s strength.

Alphabet’s own first-quarter results showed total revenue of $109.9 billion, up 22% year over year, with Google Search still delivering 19% growth and Google Cloud delivering the standout performance, with revenue surging 63% to $20 billion and a record contracted backlog approaching $460 billion. Gemini Enterprise paid users grew 40% quarter over quarter, and Gemini APIs processed 16 billion tokens per minute, up 60%, signaling that Alphabet is converting its AI investment into actual paying customers at a meaningful scale.

AI Strategy: Different Bets on Different Timelines

The most fundamental difference between the two companies in 2026 is how they are converting AI infrastructure spending into near-term financial results. Alphabet is monetizing AI through cloud customers, subscription products and enterprise software, with Google Cloud’s 63% revenue growth representing real, booked revenue from companies paying for Gemini-powered services and computing capacity. Waymo, Alphabet’s autonomous driving unit, crossed 500,000 autonomous rides per week, adding a long-term optionality layer that Meta has no equivalent of.

Meta’s AI strategy centers on using artificial intelligence to improve the targeting and creative effectiveness of its advertising products, a bet that appears to be paying off given the strong ad revenue numbers, and on developing a future consumer hardware business through AI glasses and, longer term, more advanced mixed reality devices. The cloud business announcement Wednesday adds a third front: monetizing the enormous computing capacity Meta has been building without directing all of it exclusively toward internal use. That announcement, if it materializes into an actual competitive cloud service, could transform the way investors value Meta’s capital expenditures over the next several years.

Valuation: The Argument That Decides Most Debates

Valuation has been the central dividing line between analysts who favor Meta and those who prefer Alphabet. Meta trades at approximately 20 to 23 times forward earnings, while Alphabet, despite its higher absolute stock price, trades at roughly 16 to 28 times depending on the valuation methodology and metric used. GuruFocus gave Meta a perfect GF Score of 100 out of 100, suggesting the stock is undervalued by approximately 10%, while Alphabet’s GF Score of 93 still reflected strong fundamentals but at a more expensive entry point.

The analyst consensus on Meta stands at Strong Buy with an average 12-month price target around $826 to $840, implying upside of more than 30% from recent trading levels, with some high estimates reaching $1,015. Alphabet carries a Moderate Buy to Buy consensus across 38 to 54 analysts, with average price targets between $373 and $413, reflecting more modest single-digit to low double-digit implied upside.

Since both companies reported first-quarter results on April 29, Alphabet’s shares have outperformed, gaining approximately 10.8%, while Meta’s stock has been essentially flat or slightly lower through the subsequent weeks, reflecting investor enthusiasm for Google Cloud’s growth versus continued concern about Meta’s capital spending trajectory and Reality Labs losses.

The Core Trade-Off

The debate ultimately reduces to two different types of investment propositions. Meta offers faster top-line growth, a lower valuation relative to that growth rate, and the possibility of outsized returns if either its AI glasses product line gains mainstream adoption or its new cloud business succeeds in capturing enterprise customers from established cloud providers. The downside risks include continued Reality Labs losses, the capital spending uncertainty highlighted by the raised guidance to between $125 billion and $145 billion in 2026 capital expenditures, and the regulatory exposure that comes with operating three of the world’s most widely used social media platforms.

Alphabet offers a more diversified business with a proven second revenue engine in Google Cloud that is already generating tens of billions of dollars annually and growing faster than any comparable cloud segment. Its lower price-to-earnings multiple, now close to 16 on some estimates, represents the kind of valuation analysts have historically described as cheap for the quality of business on offer. The downside risks include ongoing antitrust scrutiny, a $4.1 billion European antitrust fine upheld by a court this week, and uncertainty about whether AI will strengthen or threaten Google Search’s long-term dominance as the entry point for online queries.

As with any individual investment decision, the right choice depends entirely on each investor’s own risk tolerance, time horizon and portfolio composition rather than any single analyst’s view. Neither stock is a sell, and both remain among the most financially sound businesses in the world.

Jonathan Weber holds an engineering degree and has been active in the stock market and as a freelance analyst for many years. He has been sharing his research on Seeking Alpha since 2014. Jonathan’s primary focus is on value and income stocks but he covers growth occasionally. He is a contributing author for the investing group Cash Flow Club where along with Darren McCammon, they focus on company cash flows and their access to capital. Core features include: access to the leader’s personal income portfolio targeting 6%+ yield, community chat, the “Best Opportunities” List, coverage of energy midstream, commercial mREITs, BDCs, and shipping sectors,, and transparency on performance. Learn More.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of AVGO, NVDA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Business

Science Explains Why 39-Year-Old Messi Still Dominates at the World Cup Despite Being Old, Short and Slow

MIAMI — He is 39 years old. He stands 1.70 metres tall, shorter than virtually every defender he faces. He was never a sprinter, and he is slower now than he has ever been. None of that has stopped Lionel Messi from being the most dangerous player at the 2026 World Cup, co-leading the tournament in goals with six alongside France’s Kylian Mbappé, and continuing to confound everyone who watches him with the simple question: how?

The answer, according to researchers who have spent more than a decade studying elite soccer cognition, has almost nothing to do with what happens when Messi touches the ball. It has everything to do with what happens in the seconds before the ball arrives.

The explanation lies in a behavior that cameras rarely linger on and commentators rarely mention: scanning. The constant, deliberate movement of Messi’s head in the moments before he receives a pass, gathering information about the positions of defenders, teammates and open space that other players have not yet obtained or have not yet processed. By the time the ball reaches his feet, the decision has already been made. The touch, the turn, the pass that splits a defense open, those are, as researchers describe them, the easy part. The hard part happened earlier and mostly invisibly.

Johan Cruyff, the Dutch soccer philosopher and one of the most perceptive analytical voices the sport has ever produced, identified the principle behind this decades ago, even without the data to quantify it.

“What is speed? The sports press often confuses speed with insight,” Cruyff said. “If I start running slightly earlier than someone else, I seem faster.”

That observation, dismissed at the time by some as poetic misdirection, has since been validated in peer-reviewed research. Scientists who study visual cognition in elite sports have consistently found that what appears to be physical quickness in the game’s best players is frequently something different and more subtle: a head start bought by earlier and better perception.

Researchers studying how soccer players gather visual information before receiving the ball fitted small motion sensors to the backs of athletes’ heads, from youth academy players to senior professionals, recording how frequently and how widely players turned to look around during live match conditions. They were measuring what the field calls visual exploration, or, more plainly, scanning, and asking a straightforward question: does the frequency and quality of a player’s environmental awareness before the ball arrives actually change what they are able to do once it does?

The findings were consistent across subjects and settings. Players who scanned more frequently in the seconds before receiving a pass were measurably faster to release their next pass, more likely to turn forward with the ball rather than playing it safely back the way it came, and more likely to deliver a forward pass that created a genuine threat to the opposition. The information gathered before ball contact directly shaped the quality of decision-making once contact occurred.

The research separates scanning into two distinct functions. The first, which the researchers call orientation, is the broader, earlier phase of looking around to understand what the entire field is offering in a given moment: what options exist, where threats are developing, which spaces might open. The second, called specification, is the finer, later visual work that guides the actual execution of a pass or movement once a course of action has been chosen.

Orientation is the phase that tends to be overlooked, because it happens away from the ball at moments when nothing dramatic is visually occurring. Yet it is also the foundation. Without it, even technically gifted players are forced to make decisions with incomplete information, reacting to what they find when the ball arrives rather than acting on what they already knew.

Cruyff described the same concept in different language.

“There is only one moment in which you can arrive in time,” Cruyff said. “If you are not there, you are either too early or too late.”

Messi’s scanning behavior is, by any observable measure, among the most continuous and comprehensive in professional soccer. Watching him for 30 seconds when the ball is not near him reveals a pattern of constant, small head movements: a check left, a check right, a glance at the player on the ball, a scan behind. None of it looks especially significant in isolation. In aggregate, it means that by the time a pass arrives, Messi has assembled a mental map of everything happening around him that his marker, almost certainly taller and faster in a physical sense, has not finished constructing.

This is why the puzzle of Messi at 39, the question of how someone physically limited by every conventional athletic metric can still be the best player on the field at the most important soccer tournament in the world, resolves cleanly once you look at the right variable. He is not racing defenders. He has arranged, through earlier and better information-gathering, to never need to race anyone. He has already arrived.

The broader implication of this research extends well beyond understanding a single extraordinary player. Scanning frequency and quality are trainable skills. Data consistently shows that the habit of visually exploring the environment before the ball arrives can be developed deliberately and systematically in young players, from an early age, regardless of their physical dimensions or raw athletic capacity. The phrase coaches shout on training pitches everywhere, “check your shoulder,” is an intuitive, low-tech version of exactly this principle. The research suggests it should be formalized and made central rather than incidental to player development.

That matters at the population level because most players will never have Messi’s technique or his touch, but some of what makes him dominant is not genetic genius or exceptional physical gifting. It is habit. Perception is not a fixed attribute. It responds to practice, the same way passing does or first touch does, and coaches who train it systematically in young players may find they produce players who make better decisions even if they never make the physical charts.

For now, the immediate practical conclusion is simpler. The next time someone watches Messi at this World Cup and struggles to explain how a 39-year-old, standing shorter than virtually everyone else on the pitch, in his sixth and almost certainly final World Cup, is still doing what he is doing, the explanation is not in his feet. It has never been in his feet. Watch his head. That is where it all begins.

The Sunday Investor is focused exclusively on U.S. Equity ETFs. He has a strong analytical background, has received a Certificate of Advanced Investment Advice from the Canadian Securities Institute, and has completed all the educational requirements for the Chartered Investment Manager designation.Having covered hundreds of ETFs on Seeking Alpha, The Sunday Investor has developed a complex, proprietary ETF Rankings system which he shares on his website, etf-rankings.com. Nearly 1,000 ETFs receive individual factor scores covering costs, liquidity, risk, size, value, dividends, growth, quality, momentum, and sentiment, which feed into an easy-to-understand composite score from 1-10. The Sunday Investor is always active in the comments section in his articles – please don’t hesitate to reach out via comment in any article or by visiting etf-rankings.com. Happy Investing!

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CGDV, SPY either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

As Go The Peace Talks, So Goes The Economy

New Shed Seven album – and band say it’s ‘our best yet’

Form 4 Aehr Test Systems For: 2 July

Ripple Co-Founder Backs Venture by US Senator’s Son, Report Says

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics7 days ago

Politics7 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics7 days ago

Politics7 days agoPotential 2028er World Cup attendee leaderboard

-

Business7 days ago

Business7 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World7 days ago

Crypto World7 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Crypto World7 days ago

Crypto World7 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Sports1 day ago

Sports1 day agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Tech5 days ago

Tech5 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

You must be logged in to post a comment Login