Crypto World

Viral Meme Coin Challenges Shiba Inu (SHIB) After Exploding 80% Daily: Details

The cryptocurrency market has staged an evident rebound over the past 24 hours, with Bitcoin (BTC) rising by 4% and Solana (SOL) surging by 9%.

MemeCore (M), though, has outperformed all top 100 digital assets by skyrocketing 80% in a single day. Following the rally, it has become the third-biggest meme coin and could soon overtake Shiba Inu (SHIB) if it maintains momentum.

Is the Rally Sustainable?

The meme coin is currently worth around $1.50 and has a market capitalization of just under $2 billion, making it the 40th-largest cryptocurrency (according to CoinGecko). It is important to note that the major revival comes just days after M crashed by 76% following allegations of manipulation.

Just hours ago, the team behind the meme coin addressed the issue and informed that following “a comprehensive internal and on-chain review,” it has not found anything suspicious related to the matter.

“Our review confirms:

– No issues affecting the protocol or infrastructure.

– All core systems continue to operate normally.

– No token sales were conducted by the MemeCore Foundation.

– No unusual activity has been identified regarding the Foundation’s treasury or project operations,” the announcement reads.

Perhaps this has become the primary catalyst driving M’s price higher today (July 2). Despite the evident jump, many analysts remain skeptical of the token, warning investors to be extremely cautious.

X user Suf claimed that the price climbed “not because of bullish buyers, but from the traders who shorted, being forced to buy.” For his part, CryptoBuffett said he will short M “to infinity.”

“I will DCA all the way up to $3 and beyond. My whole reputation and net worth will go into shorting this manipulative team and coin to ZERO. It’s worth ZERO; they want to rug you twice. If you’re buying, you will be REKT,” he added.

Additional Red Signals

MemeCore’s Relative Strength Index (RSI) also suggests the price might head south soon. The ratio has risen to 82, representing an extreme overbought condition, which is often a precursor of an impending pullback.

The token has been labeled a scam by numerous well-known analysts in recent months. In April, lockchain investigator ZachXBT openly questioned MemeCore’s valuation and token distribution, claiming that insiders control more than 90% of its supply.

The post Viral Meme Coin Challenges Shiba Inu (SHIB) After Exploding 80% Daily: Details appeared first on CryptoPotato.

Bitcoin rises amid Fed inflation talks: Bull trap or $65K next?

Bitcoin (BTC) reacted positively to US Federal Reserve Chair Kevin Warsh’s remarks on stubborn inflation. Despite the gains on Wednesday, traders fear that incentives for fixed-income investments and strong earnings momentum in tech stocks will continue to pressure non-yield-bearing assets like cryptocurrencies.

The US five-year Treasury yield jumped to 4.22%, meaning traders demanded higher returns to hold government bonds. Even as inflation eventually eases and WTI crude oil prices fell to a 4-month low, investors anticipate monetary expansion.

Regardless of how the Fed manages interest rates and its balance sheet, the US Treasury dictates debt issuance trends.

Bitcoin bounces off 21-month low, but leverage data signals caution: Was $57K the bottom?

Bitcoin (BTC) is trading at around $61,490 at the time of publication after falling to a 21-month low of $57,737 earlier on Wednesday.

Ether (ETH) and Solana (SOL) also gained, up 3% and 4.85%, respectively.

The bounce took place amid deep investor caution, with sentiment trackers gauging the balance of fear and greed in crypto markets currently reading around 11 out of 100, which is in “Extreme Fear” territory. Despite the rebound from the yearly low, Bitcoin remains down roughly a third since the start of the year.

Investors’ cautious stance shows up clearly in the institutional products. US spot Bitcoin exchange-traded funds (ETFs) have hemorrhaged funds in recent weeks, including a reported $4.5 billion total outflow in June, the largest since the ETFs launched.

Related: Bitcoin price taps new July high above $62K on weak US jobs data

Analyst warns BTC could drop further after worst June since 2022

Bitcoin could face further downside pressure after ending June below its 200-week moving average while still trading above its realized price, a combination that crypto analyst PlanB says suggests the market has yet to reach a bear market bottom.

Bitcoin fell 20.5% in June to close the month at $58,526 — its worst monthly performance since June 2022 — below its 200-week moving average of $62,000 but above its realized price of $52,000.

Bitcoin is down 8.80% over the past 30 days. (CoinMarketCap)

“ALL previous bear market bottoms were below realized price,” said PlanB, the creator of the stock-to-flow pricing model. He added in a separate post that Bitcoin could drop to $52,000.

Ether treasury Sharplink bought $16M ETH last week

Crypto treasury company Sharplink, which resumed buying Ether last week after an eight-month pause, has bought a total of $16 million worth of Ether since June 25.

Onchain data from Arkham shows that after Sharplink bought 5,000 ETH on June 25, it bought another 5,000 ETH (worth $8.5 million) on June 26.

Ether is down 10.73% over the past 30 days. (CoinMarketCap)

The company confirmed the ETH purchases in an announcement, adding it bought it at an average price of $1,611 per ETH.

The two-day buying spree adds to evidence that Sharplink has revived its active Ether accumulation strategy, with its total Ether holdings now at 866,725 ETH. The crypto treasury company was once a close competitor to Bitmine as the world’s largest ETH treasury company, but has fallen far behind.

“The Company’s ETH purchases reflect its continued commitment to growing its ETH treasury as a long-term reserve asset,” it said in a statement on Tuesday.

Crypto enters Q3 with thinner liquidity but less leverage after Q2 reset: Talos

Cryptocurrency markets entered the third quarter of 2026 with less leverage but thinner liquidity after a wave of liquidations cleared speculative positions while major sources of demand weakened during the second quarter.

According to a market update from institutional data provider Talos, Bitcoin (BTC) and Ether (ETH) long liquidations totaled $8.35 billion in Q2. The data provider pointed out that the deleveraging coincided with spot Bitcoin exchange-traded fund (ETF) outflows, reduced Bitcoin buying by Strategy and a contraction in stablecoin supply.

While the reset left the market more stable heading into Q3, Talos said reduced order-book depth weakened its ability to absorb renewed selling pressure. This means the market could be less vulnerable to a chain reaction of forced selling, but prices may still swing sharply because there’s less trading activity to absorb large orders.

Features: Has Strategy’s capital overhaul put an end to ‘death spiral’ fears?

Stablecoin supply contracted in the second quarter of 2026, undoing almost three years of consistent quarterly growth and underscoring a growing split between crypto-native yield products and offerings backed by traditional reserves. According to a Q2 2026 stablecoin report published by crypto exchange CEX.IO, the category fell 15% in Q2—by more than $3.5 billion—marking the first quarterly decline since Q3 2023.

The shift was driven by reductions in yield-bearing, crypto-issued tokens, even as treasury-backed stablecoin yield products gained ground. CEX.IO’s figures point to a total stablecoin supply of $312 billion in Q2 and an adjusted transaction volume decline of 5.5%, alongside meaningful weakness in overall transaction counts.

Key takeaways

- Stablecoin supply fell more than $3.5 billion in Q2 2026, according to CEX.IO’s Q2 report, reversing nearly three years of quarterly growth.

- Crypto-native yield stablecoins shrank sharply: Ethena’s sUSDe supply dropped 52% (nearly $2 billion) and Sky’s sUSDS declined 16%.

- Treasury-backed products expanded while crypto-native contraction accelerated, including BlackRock’s BUIDL (+2%), Circle’s USYC (nearly +16%), and Ondo Finance’s USDY (up over 66%).

- Activity deteriorated at the transaction-count level: CEX.IO reports stablecoin transaction counts fell by 530 million to 4.48 billion, the largest quarterly drop on record.

- Smaller transfers looked relatively more resilient: transfers under $250 rose 5% to $19.39 billion, even as overall usage weakened.

Crypto-native yield tokens lose traction

CEX.IO’s report centers on a clear divergence in the stablecoin yield landscape. During Q2, yield-bearing stablecoin supply declined significantly as crypto-native products contracted. Ethena’s sUSDe stood out as the largest contributor to the downturn, losing 52% of its supply—shedding nearly $2 billion. Sky’s sUSDS also declined, down 16% over the same period.

The implication for users is straightforward: when demand for crypto-native yield strategies weakens, supply can retract quickly because these products are tightly linked to onchain activity and the availability of capital within crypto trading and hedging structures. In practice, that means stablecoin “yield” is not a uniform category—different issuers and reserve models can experience very different supply dynamics in the same quarter.

Treasury-backed products pick up share

While crypto-native yield tokens shrank, treasury-backed offerings moved in the opposite direction. CEX.IO reported that BlackRock’s BUIDL rose 2% in Q2, Circle’s USYC increased by nearly 16%, and Ondo Finance’s USDY climbed by more than 66%. Taken together, the data suggests investors may have shifted toward products perceived as more directly tied to traditional reserve mechanisms rather than crypto activity.

For market participants, this matters because treasury-backed expansion can stabilize parts of the stablecoin ecosystem even when broader crypto-native demand softens. However, the data also highlights an unresolved question: whether treasury-backed growth will fully offset crypto-native contraction, or whether the overall decline in supply signals that stablecoin usage itself is cooling.

First quarterly contraction since late 2023

CEX.IO frames Q2 as a turning point. The category recorded its first quarterly contraction since Q3 2023, with total stablecoin supply reaching $312 billion. The report also notes that adjusted transaction volume declined by 5.5%—a sign that not only did supply shrink, but the underlying flow of stablecoin-related activity also moderated.

Transaction data adds further detail on what changed. CEX.IO said total stablecoin transaction counts fell by 530 million to 4.48 billion, described in the report as the largest quarterly decline on record. At the same time, the report found that smaller transfers—below $250—rose 5% to $19.39 billion. That combination suggests that smaller peer-to-peer or retail-style use may be holding up better than transaction-heavy activity associated with larger automated or trading flows.

It’s an important nuance for traders and builders: the headline supply decline doesn’t necessarily mean everyday transfers disappeared. Rather, the weakness appears concentrated in higher-frequency, larger-dollar, or more automation-dependent segments of stablecoin utilization.

Weaker signals in Q1 preceded the Q2 drop

The slowdown didn’t arrive without warning. In Q1 2026, stablecoin supply still increased by about $8 billion to a record $315 billion, according to reporting referenced by CEX.IO. However, the report also points to earlier signs that organic demand was softening.

During Q1, retail-sized transfers declined by 16%, while automated activity made up roughly 76% of stablecoin transaction volume. By Q2, these patterns were more pronounced: transaction counts fell sharply, yet sub-$250 transfers increased. Together, the data suggests a market where the “type” of stablecoin activity shifted—away from larger, automation-heavy usage and toward smaller transfers, even as overall activity and supply eventually contracted.

Broader crypto demand concerns weigh on stablecoin dynamics

Stablecoin contraction in Q2 also aligns with concerns about weaker momentum across broader crypto markets. Earlier in the week, institutional data provider Talos identified declining stablecoin supply alongside spot Bitcoin ETF outflows and slower Bitcoin purchases by Strategy as three demand channels that weakened in Q2.

In comments relayed to Cointelegraph, Talos’s Tanay Ved argued that a recovery in stablecoin supply would be a useful signal of “fresh capital coming back into the ecosystem more broadly,” potentially supporting onchain liquidity. Ved also emphasized that spot ETF flows remain among the most important channels to watch, since they tend to reflect more durable shifts in institutional appetite.

Crucially, Ved noted that ETF flows, corporate Bitcoin purchases, and stablecoin supply often move together when market momentum changes. That observation frames stablecoins as more than a settlement tool: when capital rotates out of crypto exposure, stablecoin issuance and onchain usage can weaken as well—especially in segments dependent on active trading and capital deployment.

For readers tracking the next phase, the key question is whether Q2’s contraction represents a temporary reset or the start of a longer decline. CEX.IO’s data shows a sharp internal reshuffle—crypto-native yield tokens losing supply while treasury-backed products gain—so investors should watch both overall stablecoin issuance trends and the relative growth of different reserve models as new quarterly figures arrive.

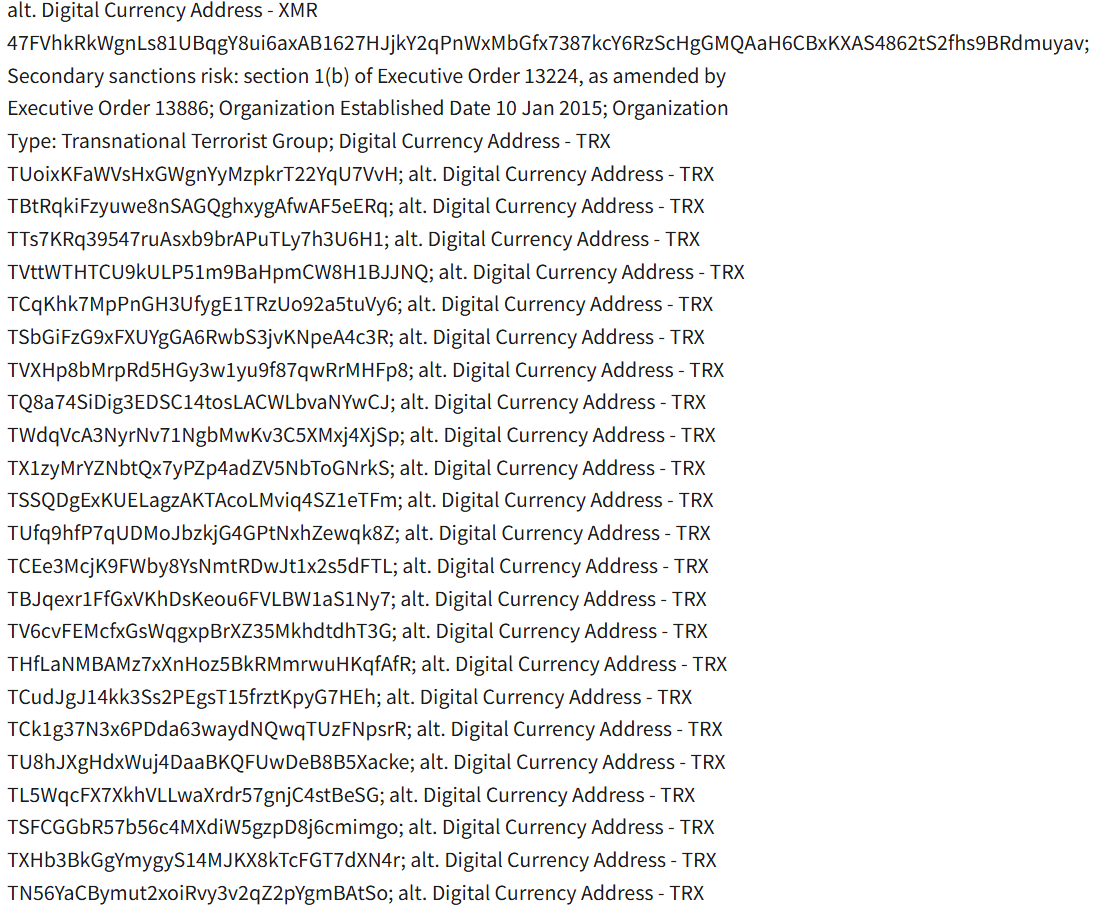

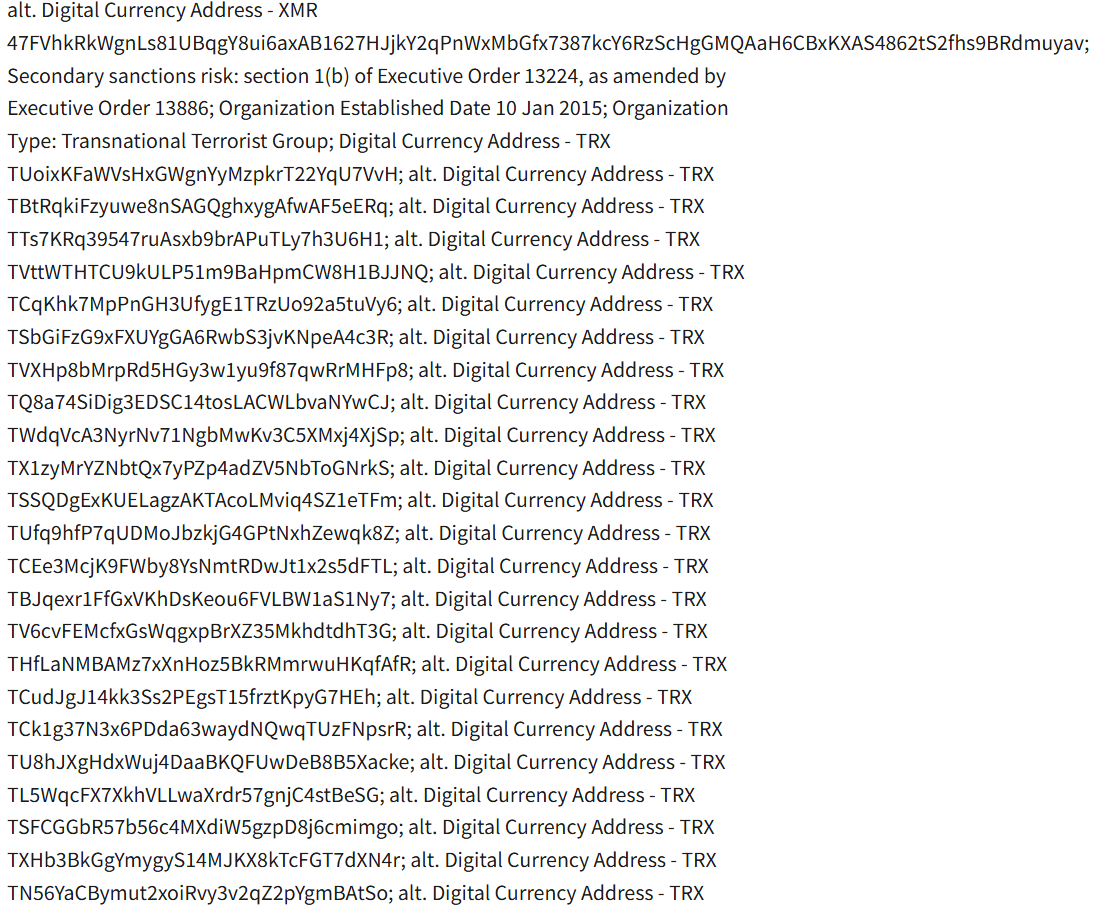

The US Department of the Treasury’s Office of Foreign Assets Control (OFAC) sanctioned 134 cryptocurrency wallet addresses identified as belonging to ISIS-Khorasan (ISIS-K), which has been a Specially Designated Global Terrorist since September 2015.

The wallet addresses were added to the OFAC’s Specially Designated Nationals (SDN) list on Wednesday, which includes individuals, entities and digital asset addresses linked to terrorism, narcotics trafficking and other illicit activity.

Stablecoin issuer Tether has frozen the balances associated with 131 Tron addresses, while the remaining three sanctioned addresses were on the Monero network, blockchain forensics company Chainalysis said in a Wednesday report.

The development comes over a week after the OFAC’s previous round of sanctions against ISIS-supporting financiers using cryptocurrency. On June 22, the OFAC sanctioned three individuals and six entities across Europe, the Middle East and West Africa, including Syria-based MSB Bitcoin Xchange and Turkish MSB Spider.

OFAC said the previous round of sanctions targeted “key facilitators who enable ISIS to move funds among its regional affiliates.”

OFAC update to SDN list, new wallets included. Source: OFAC

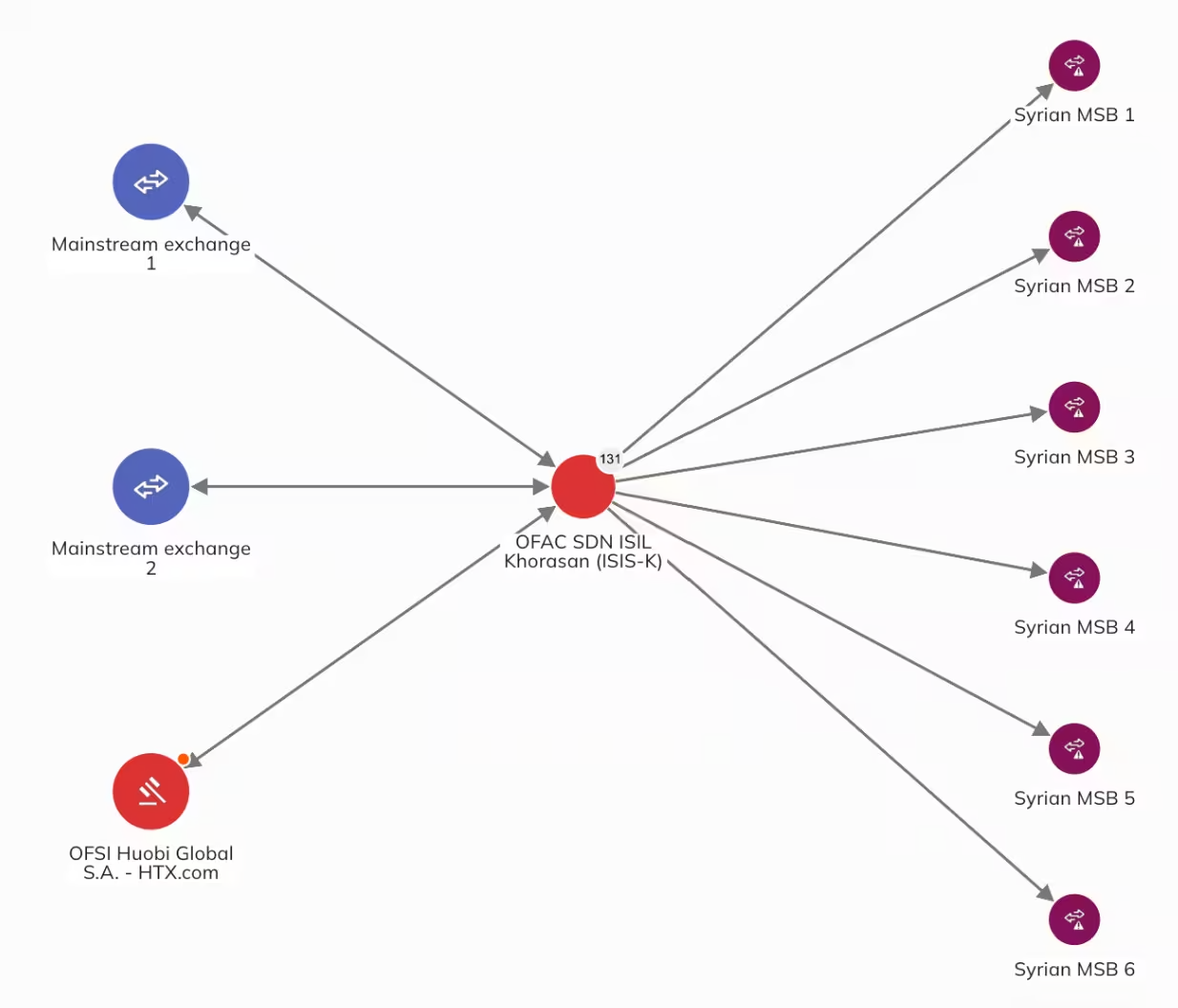

131 wallets linked to ISIS-K received $1.4 million in donations

ISIS-K has historically solicited crypto through donation campaigns on various websites and messaging platforms, Chainalysis said.

The report said that the 131 Tron addresses in the latest round of sanctions received over $1.4 million in crypto donations since 2023 and sent over $880,000.

Network of ISIS-K funding entities sanctioned by OFAC. Source: Chainalysis

Chainalysis identified multiple such donation addresses used by the group on Tron, Monero and the Bitcoin network. It found significant exposure to mainstream services, including some wallets that sent funds to Syria-based cryptocurrency exchanges.

Related: US sanctions Sinaloa cartel-linked Ethereum addresses

Blockchain analytics tools are playing an increasingly prominent role in financial sanctions targeting illicit activity.

Earlier in April, blockchain intelligence company TRM Labs said that onchain evidence was key to securing the conviction of three individuals for terrorism financing in Indonesia in 2024 and 2025.

“Indonesian courts have demonstrated that cryptocurrency evidence — wallet addresses, transaction histories, on-chain flows — is not only admissible but can anchor a terrorism financing prosecution,” TRM said in a statement.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

In 2011, $2.7 billion of inflows sent Bitcoin up more than 55,000%. This cycle, $697 billion produced 689%. A leading analyst says the math has changed so much that the next parabolic run needs a trillion dollars. Here is the case, and the case against.

Summary

- CryptoQuant chief executive Ki Young Ju argued on July 1 that Bitcoin’s capital efficiency is collapsing, so each cycle needs far more money to produce far smaller percentage gains.

- His headline figures: in 2011, roughly $2.7 billion of net inflows drove a gain of more than 55,000%, while this cycle, about $697 billion produced a return of around 689%.

- Ju still expects one more parabolic run, but says it likely requires Bitcoin to absorb more than $1 trillion in realized capitalization and to become a core macro asset rather than a retail-driven ETF trade.

- The bull reading is that declining capital efficiency is normal maturation, and that gold’s roughly $27 trillion market value shows enormous headroom for institutional adoption that is still early.

- The bear reading is that a trillion-dollar requirement is an enormous ask in a market bleeding ETF flows to stocks and gold, and that collapsing efficiency signals the era of outsized returns is ending.

Bitcoin just posted the worst month in the history of its exchange-traded funds, bounced modestly into July, and is trading more than 50% below its October 2025 record. Into that gloom, one of the most-watched analysts in crypto dropped a statistic that reframes the entire debate about where Bitcoin goes next.

On July 1, CryptoQuant chief executive Ki Young Ju laid out the numbers behind a claim that is now spreading fast: Bitcoin’s next parabolic bull run may require it to absorb more than $1 trillion of fresh capital. That is not a price target; it is a statement about how much harder it now is to move Bitcoin at all.

This piece breaks down the number behind the claim, what Ju is really arguing, and the serious case on both sides of whether a trillion-dollar bull run is a bullish invitation or a bearish warning.

The number behind the claim

The heart of Ju’s argument is a single, striking comparison of how much money it has taken to move Bitcoin across cycles. In 2011, in Bitcoin’s earliest days, roughly $2.7 billion of net capital inflows drove a price increase of more than 55,000%. In the current cycle, by contrast, about $697 billion of inflows produced a return of only around 689%.

Put those side by side, and the ratio of dollars in to price gain has compressed by something on the order of 80x across the life of the asset. Each successive cycle has demanded far more capital to generate far smaller percentage moves.

The metric underneath this is realized capitalization, which measures the total capital actually invested in Bitcoin by valuing every coin at the price it last moved on-chain, instead of at today’s market price.

Realized cap is the closest thing Bitcoin has to a measure of real money committed to it, and Ju frames the whole question in those terms: the next parabolic run, he argues, likely requires Bitcoin to absorb more than $1 trillion of new realized cap. That is the concrete threshold behind the headline, and it is why the claim is about capital absorbed, not about a price level reached.

This is not a doom call from a permabear. Ju has spent much of the past year as one of the more constructive voices among top analysts, and his July 1 post explicitly says Bitcoin likely has another parabolic cycle ahead of it. The trillion-dollar figure is his estimate of the price of admission for that run, not a declaration that it cannot happen.

Understanding that distinction is essential, because the same numbers can be read as a reason for optimism or a reason for caution, and the rest of the debate flows from which reading you find more convincing.

What Ki Young Ju is actually arguing

Ju’s full thesis is more nuanced than the headline stat suggests, and it rests on a claim about what kind of asset Bitcoin needs to become. In his telling, the shrinking capital efficiency is a symptom of Bitcoin outgrowing its old drivers. The retail-led, exchange-traded-fund-driven demand that has powered recent moves is, he argues, not enough to fuel another parabolic run at Bitcoin’s current size.

For that, Bitcoin needs to graduate into a core macro asset held by institutions and allocators as a serious portfolio holding, not traded as a speculative vehicle by retail investors chasing momentum.

That shift, Ju stresses, is still in its early stages and has not been invalidated by the current downturn. He points to the gap that still exists between Bitcoin and the assets it aspires to sit alongside: gold carries a market value of roughly $27 trillion, dwarfing Bitcoin’s, which leaves enormous room for growth if institutional and macro capital genuinely rotates in.

If Bitcoin can absorb more than $1 trillion in realized cap, he argues, another parabolic bull run remains firmly on the table. The trillion dollars, in this framing, is not an impossible barrier but the scale of adoption required to prove Bitcoin has become what its supporters say it is.

So the argument is really two claims bundled together. The first is descriptive: capital efficiency is declining, and it now takes vastly more money to move Bitcoin than it once did. The second is conditional and hopeful: if the right kind of capital, deep institutional and macro allocation, shows up at sufficient scale, the next parabolic run can still happen. The disagreement in the market is not mostly about the first claim, which the numbers support, but about the second, about whether that $1 trillion is realistically coming, and about what it means for Bitcoin if it does or does not.

Why the math changes as Bitcoin grows

To weigh the claim, it helps to understand why capital efficiency declines in the first place, because the mechanism is not mysterious. It is a straightforward consequence of Bitcoin getting bigger. When Bitcoin was a tiny, obscure asset in 2011, a small amount of new money represented an enormous percentage of its total value, so modest inflows produced explosive percentage gains.

As the asset has grown into the hundreds of billions and, at its peak, past $2 trillion in market value, the same percentage move requires vastly more absolute capital. Moving a large asset by a given percentage simply costs more than moving a small one.

A second force compounds this: the pool of holders willing to sell cheaply keeps shrinking. Over time, a growing share of Bitcoin has moved into the hands of long-term holders and institutions who are not eager to part with their coins at low prices, which Ju and others have described as a structural change in the market. That is usually framed as bullish, because it reduces available supply, but it also changes the market’s rhythm.

With fewer coins available to absorb and fewer sellers to flush out, price action becomes less about violent boom-and-bust cycles and more about how much new capital can be coaxed in against a supply that increasingly sits still.

The result is a maturing asset whose returns compress even as its stability grows. This is the same pattern seen in other assets as they scale: the earliest investors capture the largest percentage gains, and returns moderate as the asset becomes mature and widely held.

For Bitcoin, that means the days when a few billion dollars could produce a 50,000% move are almost certainly gone for good. What replaces them, and whether it is still attractive, is exactly where the bull and bear cases diverge.

The bull case: maturation with huge headroom

The optimistic reading takes the collapsing capital efficiency as a sign of health, not decline. In this view, declining percentage returns are simply what happens when an asset succeeds and grows up, and they say nothing bad about the absolute gains still available. A move that is small in percentage terms for a multi-trillion-dollar asset can still represent enormous absolute wealth creation, and a maturing Bitcoin that trades with less violence is more, not less, attractive to the large, cautious pools of capital that were always going to be needed for the next leg higher.

The headroom argument is the bull’s strongest card. Gold’s market value sits around $27 trillion, and Bitcoin, even near its peak, was a fraction of that. If Bitcoin is genuinely on a path to becoming a macro store of value alongside gold, the total addressable market is measured in tens of trillions, which makes $1 trillion of fresh absorption ambitious but far from absurd.

The infrastructure to deliver it is also further along than ever: spot ETFs, whatever their recent outflows, opened a regulated on-ramp for institutions, corporate treasuries have accumulated well over 1 million coins, and traditional banks have built custody and trading services. The pipes for institutional capital exist in a way they never did in prior cycles.

Ju himself sits largely in this camp, and that matters. His argument is not that the parabolic era is over but that it now depends on a specific, identifiable driver: deeper institutional allocation and macro-asset status, a shift he insists is early instead of dead. Supporters point out that institutional adoption of a new asset class takes years, that sovereign and pension-scale allocation to Bitcoin has barely begun, and that even a small reallocation from the vast pools of global bonds, equities, and gold would supply the $1 trillion in question. In the bull case, the trillion-dollar requirement is not a wall but a roadmap, and the recent weakness is a pause in a still-early adoption story.

The bear case: the outsized-returns era may be ending

The skeptical reading takes the same numbers and draws a colder conclusion. If it now takes $1 trillion to spark a parabolic run, then the era of Bitcoin as a life-changing, asymmetric bet is largely behind us, and what remains is a large, slow, increasingly conventional asset.

Collapsing capital efficiency, in this view, is not just maturation to be celebrated; it is a warning that the returns which drew a generation of investors are compressing toward those of ordinary macro assets, and that buyers expecting another 50-fold move are anchored to a past that will not repeat.

More pressing is the question of where $1 trillion actually comes from, and the short-term evidence is discouraging. Bitcoin ETFs just recorded their worst month on record, shedding around $4.5 billion in June, the opposite of the institutional inflow the thesis requires. Capital has been rotating out of crypto and into artificial-intelligence equities and gold, the “stocks and shiny rocks” Ju himself has described, instead of into Bitcoin.

If the marginal dollar is leaving for other assets precisely when the thesis needs it to arrive at scale, the trillion-dollar bar looks less like a roadmap and more like a distant hope. Demanding record institutional inflows from a market that is currently seeing record outflows is a hard sell.

The bear case also leans on Bitcoin’s present behavior. For the thesis to work, Bitcoin has to become a core macro asset, yet through 2026 it has traded like a high-beta risk asset, falling with technology stocks and failing to act as the hedge the macro-asset story requires. The institutional demand that did show up, much of it channeled through corporate treasuries such as Strategy, now looks strained, with those vehicles under financial pressure and at risk of becoming sellers rather than buyers.

If the treasury model wobbles and ETF flows stay negative, two of the main pipes for the needed capital narrow at once. In the bearish reading, the trillion-dollar requirement is really an admission that Bitcoin can no longer move on its own and now depends on an institutional wave that may not come.

The boredom risk Ju keeps flagging

There is a third scenario that Ju has emphasized repeatedly, and it is neither the bull’s parabolic run nor the bear’s crash. It is stagnation. For much of 2026, he has argued that Bitcoin’s biggest danger is not a violent drawdown but prolonged, boring sideways action that slowly drains attention and conviction.

A sharp crash, in his framing, can be survived because the long-term thesis stays intact and the sell-off flushes out leverage. A market that simply drifts for years is harder to escape, because it offers no catalyst to force capital back in and quietly erodes the belief and the financing structures built on top of the asset.

This connects directly to the capital-efficiency argument. Ju has pointed out that Bitcoin’s realized capitalization, the measure of real money committed, has flatlined after years of growth, and that holders recently entered a net realized loss phase for the first time since 2023. When realized cap stops growing while the market drifts, it means no new buyers are stepping in to absorb sell-side pressure, which is precisely the condition that produces a long, flat grind. The $1 trillion is what would break that stalemate; its absence is what leaves Bitcoin drifting.

The boredom scenario is important because it reframes the stakes. The debate is often posed as bull versus bear, moon versus crash, but Ju’s more subtle point is that the most likely near-term outcome may be neither. It may be a market that neither rewards the bulls with a parabolic run nor vindicates the bears with a collapse, but simply goes quiet, testing the patience of holders and the durability of the institutions built around Bitcoin. In that world, the trillion-dollar question is not answered so much as postponed, and the danger is that the postponement itself does damage.

What would it actually take to get $1 trillion?

If $1 trillion is the price of the next parabolic run, the practical question is where it could plausibly come from, and the honest answer is that it requires sources larger than the ones that have driven Bitcoin so far. Retail speculation and even the current wave of ETF demand are not enough at Bitcoin’s scale, which is Ju’s whole point.

The capital would have to come from the deep pools that have barely allocated to Bitcoin: pension funds, insurers, sovereign wealth funds, corporate treasuries at scale, and potentially nation-states holding Bitcoin as a reserve asset. A modest reallocation from the tens of trillions in global bonds, equities, and gold would clear the bar, but only if Bitcoin earns a place in those mandates.

The conditions for that are identifiable, even if their timing is not. It would likely take continued regulatory clarity that makes Bitcoin allocatable for conservative institutions, a track record of Bitcoin behaving more like a macro store of value than a risk asset, and infrastructure that large allocators trust.

It would also, realistically, require a friendlier macro backdrop than the current one of tight liquidity and a hawkish Federal Reserve, since large institutional rotation into a volatile asset tends to happen when conditions ease instead of tightening. Each of these is plausible over a multi-year horizon and absent in the current one, which is why the thesis is framed as early instead of imminent.

For anyone watching Bitcoin, the signals to track therefore shift away from the daily price and toward the flow of real capital. The single best gauge is realized capitalization itself: if it resumes sustained growth, fresh money is truly entering, and the trillion-dollar path is opening.

Alongside it, the direction of ETF flows, evidence of pension and sovereign allocation, and whether Bitcoin starts trading with more independence from technology stocks would all indicate whether the macro-asset shift is happening. Until those turn, the trillion-dollar requirement remains a thesis about the future instead of a description of the present.

Why this matters even if you disagree

Whatever one makes of the specific trillion-dollar figure, the framing itself is the most valuable takeaway, because it changes how to judge Bitcoin. For most of its history, Bitcoin has been evaluated by its capacity for explosive percentage gains, the asymmetric moonshot that could multiply an investment many times over.

Ju’s argument, accepted even in part, means that lens is increasingly obsolete. A multi-trillion-dollar asset will not deliver another 50,000% move, and holding out for one is a category error. The relevant question becomes whether Bitcoin can keep attracting large absolute inflows as it matures, not whether it can repeat the returns of its infancy.

That reframing cuts across the bull-bear divide. A bull who accepts it stops expecting overnight riches and starts thinking in terms of steady, large-scale adoption compounding over years, judging progress by realized cap and institutional flows instead of by the next candle. A bear who accepts it stops waiting for a total collapse and starts asking whether Bitcoin can justify its size without the returns that once did the persuading. Both are better served by measuring Bitcoin against the trillion-dollar yardstick of real capital than by the percentage fireworks of the past.

The deeper significance is that Bitcoin appears to be at a genuine inflection point in what it is. The collapsing capital efficiency is the numerical fingerprint of an asset transitioning from a speculative frontier bet into something that either becomes a mature macro store of value or stalls short of it.

Ju’s trillion-dollar claim is really a way of stating the price of that transition. Whether Bitcoin pays it, over what timeframe, and whether the market has the patience to wait, are the questions that will define the coming years far more than any single month of inflows or outflows.

Frequently Asked Questions

Who said Bitcoin needs $1 trillion for its next bull run?

The claim comes from Ki Young Ju, chief executive of the on-chain analytics firm CryptoQuant, in a post on July 1, 2026. He argued that Bitcoin’s capital efficiency is declining and that the next parabolic bull run likely requires Bitcoin to absorb more than $1 trillion in realized capitalization, along with deeper institutional adoption. He still expects another parabolic cycle, but sees this as its price of admission.

What does declining capital efficiency mean?

It means it now takes far more money to move Bitcoin’s price by a given percentage than it used to. Ju’s figures show that in 2011, about $2.7 billion of inflows drove a gain of more than 55,000%, while this cycle roughly $697 billion produced around 689%. The ratio of dollars in to price gain has compressed by roughly 80 times, because Bitcoin is now a much larger asset.

Why does it take more money to move Bitcoin now?

Because Bitcoin has grown enormously. When it was tiny, a small inflow was a large share of its value and produced explosive percentage gains. Now that it is worth hundreds of billions to trillions, the same percentage move requires vastly more absolute capital. A shrinking pool of holders willing to sell cheaply, as coins move to long-term holders and institutions, compounds the effect.

Is the $1 trillion claim bullish or bearish?

It can be read either way, which is why it is debated. The bullish reading is that declining percentage returns are normal maturation, and that gold’s roughly $27 trillion market value shows huge headroom for institutional adoption that is still early. The bearish reading is that a trillion-dollar requirement is an enormous ask while ETFs bleed money and capital rotates to stocks and gold, signaling the outsized-returns era is ending.

What is realized capitalization?

Realized capitalization measures the total capital actually invested in Bitcoin by valuing every coin at the price it last moved on-chain, instead of at the current market price. It is the closest measure of real money committed to Bitcoin. Ju frames his argument in these terms: the next parabolic run requires more than $1 trillion of new realized cap to be absorbed, and a flatlining realized cap signals no fresh money is entering.

Where would $1 trillion of new capital come from?

It would have to come from pools far larger than the retail and current ETF demand that has driven Bitcoin so far, such as pension funds, insurers, sovereign wealth funds, large corporate treasuries, and potentially nation-states holding Bitcoin as a reserve. A small reallocation from the tens of trillions in global bonds, equities, and gold would suffice, but only if Bitcoin earns a place in those mandates, which requires clarity, trust, and time.

Does this mean Bitcoin cannot have another bull run?

No. Ju explicitly expects another parabolic run and calls the institutional shift early rather than invalidated. The claim is about what that run requires, not whether it can happen. The debate is over whether the needed $1 trillion will realistically arrive, especially given recent record ETF outflows, and over what it means for returns if future cycles need ever-larger inflows to produce ever-smaller percentage gains.

What should investors watch to judge the thesis?

The single best gauge is realized capitalization: sustained growth means fresh money is truly entering and the trillion-dollar path is opening, while a flatlining figure signals stagnation. Alongside it, watch the direction of ETF flows, evidence of pension and sovereign allocation, and whether Bitcoin begins trading more independently of technology stocks. These signals indicate whether the shift to a core macro asset is actually happening.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. It describes an analyst’s thesis and the debate around it, not a forecast or recommendation, and cryptocurrency prices are highly volatile. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a qualified financial professional before making investment decisions. Information is accurate as of July 2, 2026, and may change.

Kooc Media has launched dedicated PR support for AI agents, chatbots, and machine learning platforms. The aim is to help the companies behind these products win press, reach the right people, and earn trust in a market that fills up more every day.

With AI agents, chatbots, and machine learning platforms launching at breakneck speed, getting noticed is tough. Plenty of these products are impressive, yet they fade into the background. Kooc Media’s PR support sets out to change that, offering quick, guaranteed coverage on trusted tech and finance outlets.

PR Made for AI Agents, Chatbots and ML

Most agencies run the same routine for every client, whatever they’re selling. Kooc Media went a different way, shaping its support around what companies building AI agents, chatbots, and machine learning platforms actually need.

That means coverage that gets the technology. Whether a company is rolling out a new AI agent, a customer-facing chatbot, a conversational AI tool, or a machine learning platform for developers, each campaign is written for the right audience and tuned to the brand’s goals.

“AI agents, chatbots, and machine learning platforms move fast, and their PR has to keep up,” said Michelle De Gouveia, spokesperson for Kooc Media. “We built this support so a company can launch a product and see real coverage the same week. No long waits, no guesswork, just placements that help them grow.”

You can find out more on the Kooc Media AI Companies PR page.

Guaranteed Coverage, Not Hope

A major issue with traditional PR is that nothing is promised. Agencies pitch journalists and hope something lands. Companies pay for the attempt, not the outcome.

Kooc Media takes a different path. The agency owns and runs its own network of news sites, including Blockonomi, CoinCentral, MoneyCheck, Parameter, Beanstalk, and Computing. That means companies behind AI agents, chatbots, and machine learning platforms get real, published articles instead of a list of outreach attempts.

Because Kooc Media controls these sites, coverage can go live the same day. That gives AI brands instant exposure when it matters most, such as during a product launch, a funding round, or a big update.

You can browse every in-house site on the Kooc Media brands page.

Wide Distribution Across Major Outlets

Alongside its own network, Kooc Media offers full newswire distribution to hundreds of partner sites and thousands of syndicated outlets.

Depending on the package, releases can also reach major financial and business news networks. That can include coverage on sites such as Business Insider, Bloomberg, Benzinga, MarketWatch, USA Today, and Dow Jones feeds, plus other global platforms.

For companies building AI agents, chatbots, and machine learning platforms, this reach builds real trust. Showing up on names that investors, customers, and partners already know makes a brand far more credible.

Featured Free on AgentLocker.ai

A key part of this support is free access to AgentLocker.ai, Kooc Media’s own AI tools and agents directory.

AgentLocker.ai is a growing directory where people search for the latest AI tools, agents, and software. It’s an ideal home for AI agents and chatbots, helping them get found by users who are actively looking for new AI solutions.

Every client on an AI PR package is listed and featured on AgentLocker.ai at no extra cost. That gives companies behind AI agents, chatbots, and machine learning platforms another channel for visibility on top of their press coverage, and a place where their product stays discoverable well after a campaign ends.

You can explore the directory at AgentLocker.ai.

Pairing media coverage with a dedicated AI directory listing means these companies get more from a single package. Rather than paying separately for a listing and for PR, clients get both in one place.

PR Done For You

Many companies working on AI agents, chatbots, and machine learning platforms run lean, with no marketing department and no dedicated PR person. Kooc Media handles that with managed PR creation from its in-house editorial team.

That means founders don’t need to write their own releases or articles. They hand over the details, and the Kooc Media team creates the content, publishes it, and distributes it.

The services include press release writing, sponsored articles, homepage placements, guaranteed publication across in-house sites, newswire distribution, and full reporting with live links to every placement.

That reporting is an important part of the offer. Clients receive a clear record of where their coverage ran, with direct links to each article. There’s no guessing about whether the work got done.

Ready-Made and Custom Options

Kooc Media offers both ready-made packages and fully custom campaigns. The ready-made options suit companies that want a simple, fast solution. The custom campaigns are for brands that want a more tailored approach across search engines, news platforms, and social media.

That flexibility means the support works for early-stage teams launching a first AI agent or chatbot as well as larger machine learning platforms running ongoing coverage.

Part of a Wider Industry Focus

While this support focuses on AI agents, chatbots, and machine learning platforms, it sits within Kooc Media’s broader focus on fast-moving sectors. The agency has worked in crypto, fintech, technology, and iGaming since it was founded in 2017.

Companies whose AI products cross into these areas can also explore Kooc Media’s crypto PR services and gambling PR services. Many AI tools overlap with these fields, such as trading bots, fintech chatbots, and gaming automation, so the agency’s experience adds real value.

Why This Matters for AI Companies

The market for AI agents, chatbots, and machine learning platforms is growing fast, but attention is hard to win. New tools launch every day, and most never get noticed. Good PR can be the difference between a product that takes off and one that stays hidden.

By combining guaranteed coverage, same-day publishing, major newswire reach, and a free AgentLocker.ai listing, Kooc Media gives these companies a clear path to visibility. The packages are built to be fast, simple, and results-focused, which is exactly what fast-moving AI brands need.

For companies building AI agents, chatbots, and machine learning platforms that want to launch quickly and get noticed, this PR support offers a straightforward way to put their product in front of the right people.

Kooc Media’s AI packages are available now through the company’s website at https://kooc.co.uk.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Ripple executive chair Chris Larsen has been reported as one of the backers of a financial venture launched by Theodore Gillibrand, the son of US Senator Kirsten Gillibrand, according to a Politico report dated Thursday. The development lands in parallel with ongoing Senate negotiations over the Digital Asset Market Clarity (CLARITY) Act—US crypto market-structure legislation that lawmakers say could reshape how digital-asset businesses operate.

Politico reports that American Perpetuals Exchange Corp. (APEC), founded by Theodore Gillibrand, raised $30 million, with most investors contributing between $5,000 and $10,000 apiece. Larsen’s reported involvement was noted by Politico, though the report did not specify Larsen’s exact contribution.

Key takeaways

- Politico reports Chris Larsen was among investors backing APEC, Theodore Gillibrand’s derivatives-focused venture.

- APEC’s funding is described as totaling $30 million, with typical contributions reportedly in the $5,000–$10,000 range.

- The investment is unfolding while Senator Kirsten Gillibrand negotiates ethics provisions in the CLARITY Act.

- Democratic lawmakers are pressing Republicans to include ethics language, with questions framed around conflicts involving lawmakers and government officials.

- The Senate schedule—returning July 13 and then breaking again for an extended state work period—narrows the time left for CLARITY to advance.

APEC funding and the Larsen connection

In its Thursday coverage, Politico said Larsen was one of a small set of investors supporting APEC, the company created by Theodore Gillibrand. The report emphasizes that while APEC attracted a broader group of investors, individual stakes cited in the coverage were relatively modest, with “the majority” contributing between $5,000 and $10,000.

However, Politico did not publish Larsen’s exact amount. For readers tracking the intersection of finance and policy, the more relevant takeaway is not the dollar figure itself, but the timing: the reported investment is occurring while Gillibrand’s office and other lawmakers work to finalize provisions of a bill widely expected to influence the regulatory environment for crypto exchanges, issuers, and derivatives markets.

Ethics provisions in the CLARITY Act are front and center

The reported APEC backers’ list is becoming part of a broader political debate because the CLARITY Act is in active negotiation, and Gillibrand has publicly tied her support to ethics reforms.

As Cointelegraph previously reported, Gillibrand said in May that lawmakers would not be voting for the bill unless ethics concerns were addressed—specifically, the risk that members of Congress or senior administration figures could benefit financially from the crypto industry due to their government roles. In that context, she characterized such outcomes as an unacceptable form of “pay for play.”

“[T]he truth is, is that we cannot allow members of Congress, senior administration officials, presidents or vice presidents, to get rich off of these industries because of their insider status. It is the worst form of pay for play.”

A spokesperson for Gillibrand told Cointelegraph that her son was “a grown adult starting his own independent business” and that the senator had “no involvement in it whatsoever.” Politico’s report does not resolve the underlying political dispute, but it intensifies scrutiny of how lawmakers’ personal or family-adjacent business ties are perceived while ethics language is being negotiated for a major policy package.

Cointelegraph also reported that it reached out to APEC for comment but did not receive an immediate response.

Republicans expect movement—Democrats push harder on ethics

CoinShares data is not referenced in the reporting provided here; instead, the key developments revolve around how Congress plans to handle CLARITY’s legislative path. Democratic lawmakers have been urging Republicans, who hold a majority in Congress, to adopt ethics language in the act. Their calls cite concerns that involve the current administration’s ties to the crypto industry.

On the Republican side, leaders have signaled they expect the bill to move through the Senate in July. Senator Cynthia Lummis, according to Cointelegraph reporting from June, said lawmakers were “working a little bit on ethics,” along with other topics raised in negotiations, including decentralized finance and illicit transactions.

That mix matters because CLARITY is not just a single-issue bill—it is positioned as market-structure legislation. If ethics provisions end up changing the compliance burdens, definitions, or governance expectations for firms operating in the US, those downstream impacts could affect everything from how trading and derivatives products are offered to what internal controls businesses must maintain.

At the procedural level, the Senate’s thin margin means Republicans will need at least some Democratic support to reach the 60-vote threshold for CLARITY to pass.

The legislative timetable is tightening

Even as the debate continues, lawmakers’ calendars are becoming an additional constraint. The Senate is currently in its Independence Day holiday period. Per the schedule described in Cointelegraph’s reporting, the chamber is set to return to session on July 13 and then head into another month-long state work period in August.

That means the practical window for crypto market-structure action is shrinking well before the US election season—an environment that often leads to renewed legislative delay and reprioritization. For crypto firms and investors, the key watch item is whether negotiations on ethics provisions keep the bill on track through July, or whether the calendar effectively pushes momentum into a later legislative session.

While the APEC funding story may appear at first glance to be separate from CLARITY policy talks, it is the simultaneous timing that’s likely to influence political attention. As ethics language becomes part of the bill’s final shape, stakeholders will want to monitor not only the bill’s progress, but also how the Senate frames conflicts-of-interest concerns and whether those discussions drive any substantive changes to the bill text.

What to watch next is the Senate’s ability to reconcile ethics negotiations with broader market-structure provisions before the July vote window narrows—alongside any further disclosure or clarification about the reported involvement of industry figures in private-sector activity during an election-adjacent legislative crunch.

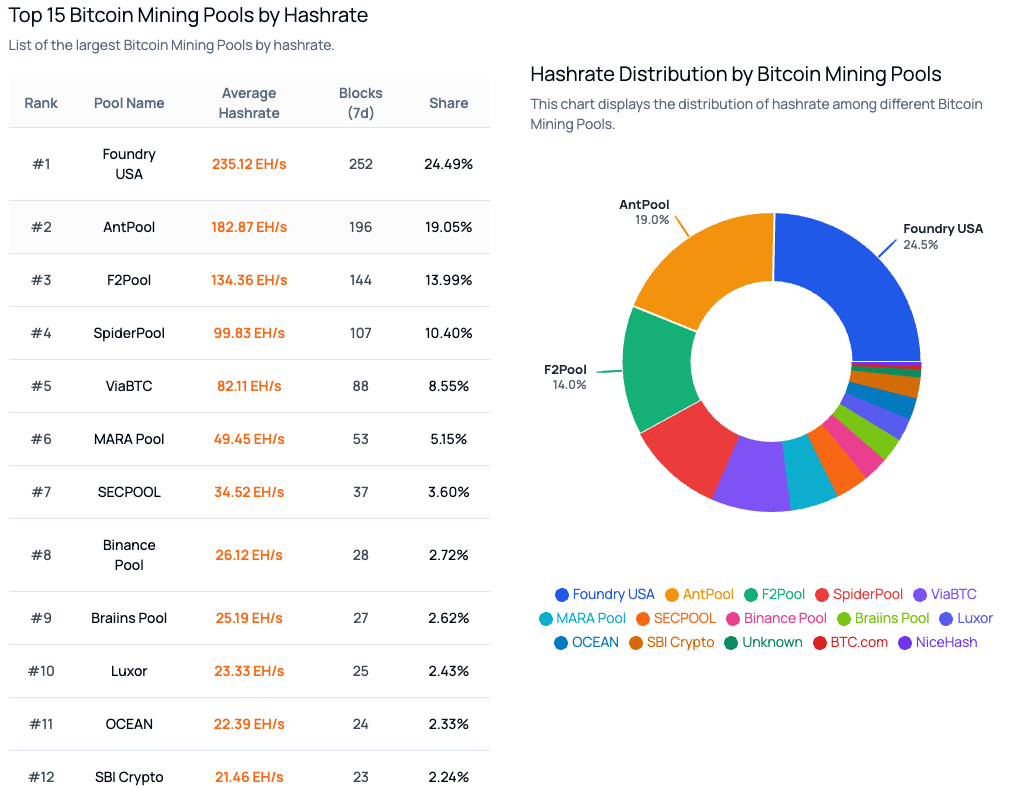

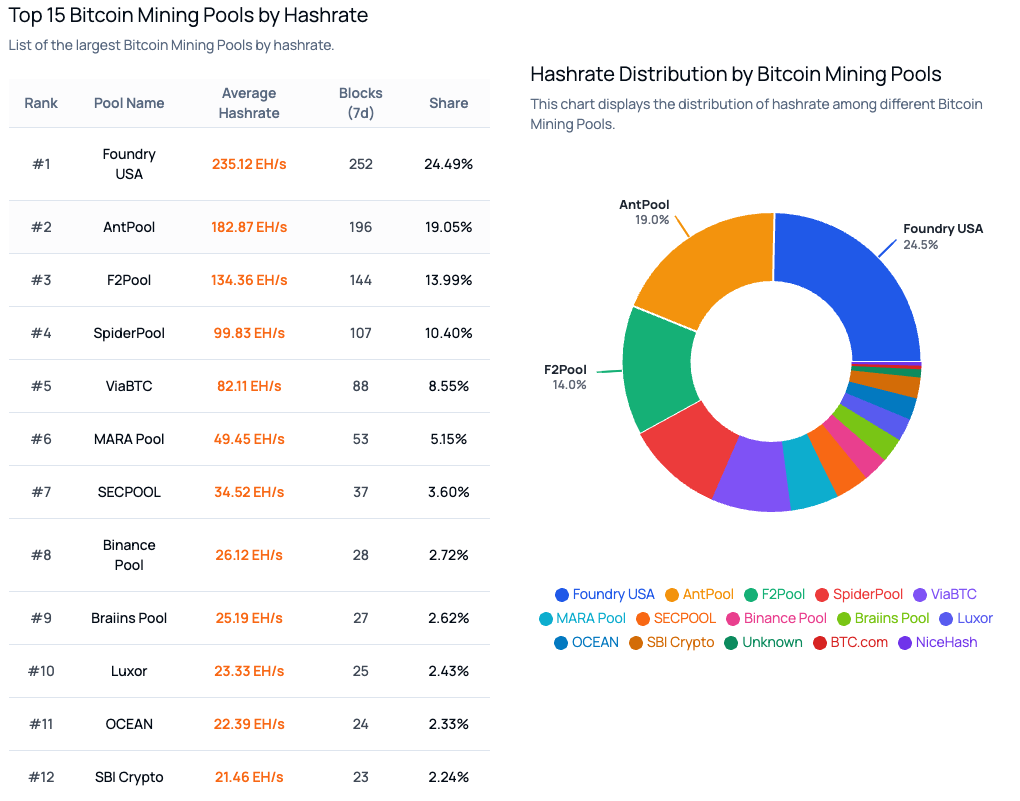

SBI Crypto, a cryptocurrency-focused division of Japanese financial conglomerate SBI, is shutting down its Bitcoin mining pool after a five-year run.

The company announced Wednesday that it will end mining pool operations on July 31 and will stop accepting mining shares at the same time. It did not provide its rationale for closing the pool.

SBI Crypto said miners should keep directing hashrate to the pool until the cutoff so final payouts can be calculated correctly before operations end. “We would sincerely appreciate your continued support by mining with us until the final day of operation,” it said.

The shutdown marks the end of one of Japan’s better-known corporate mining pool operations and is the latest sign of SBI’s intentions to expand its broader cryptocurrency strategy beyond mining.

SBI Crypto’s BTC mining pool ranks No. 12 globally

SBI Crypto launched its Bitcoin mining pool in March 2021, entering a market that at the time was dominated by operators such as Poolin, F2Pool and Binance Pool.

Data from SimpleMining shows SBI Crypto currently ranks as the 12th largest Bitcoin mining pool globally, with about 21.46 exahashes per second (EH/s) of hashrate and roughly 2.24% of total Bitcoin network share.

Source: SimpleMining

That places it far behind leaders like Foundry USA, which controls about 24.49% of the network, and AntPool at around 19.05%. Mid- and lower-tier mining pools such as ViaBTC and MARA Pool account for about 8.55% and 5.15% of the global Bitcoin mining hashrate, respectively.

Miner migration to alternative pools

SBI Crypto directed miners toward several alternative Bitcoin mining pool operators as it prepares to shut down its service, including Braiins, Luxor and NeoPool.

Among them, Braiins and Luxor are established mid-tier mining infrastructure providers, each controlling around 2%-3% of global Bitcoin hashrate, according to SimpleMining data. NeoPool is not included in the top-ranked pools by hashrate.

Source: Braiins

“Some operators may offer special programs or preferential conditions for clients transitioning from SBI Crypto,” the company said, adding that customers are encouraged to contact each operator directly for details.

Related: Bitcoin mining difficulty drops 10% in 11th largest downward adjustment

The shutdown comes as SBI Holdings continues to expand its broader cryptocurrency strategy beyond mining.

The company recently agreed to acquire full control of crypto exchange Bitbank in a 46.7 billion Japanese yen ($289 million) deal, aiming to create Japan’s largest cryptocurrency exchange.

SBI has also been increasing its focus on stablecoins, backing JPYSC, a new trust bank-backed Japanese yen stablecoin, and supporting Ripple’s rollout of the Ripple USD (RLUSD) stablecoin in Japan.

Magazine: Bitcoin miners are pivoting to AI, so why is the hashrate near ATHs?

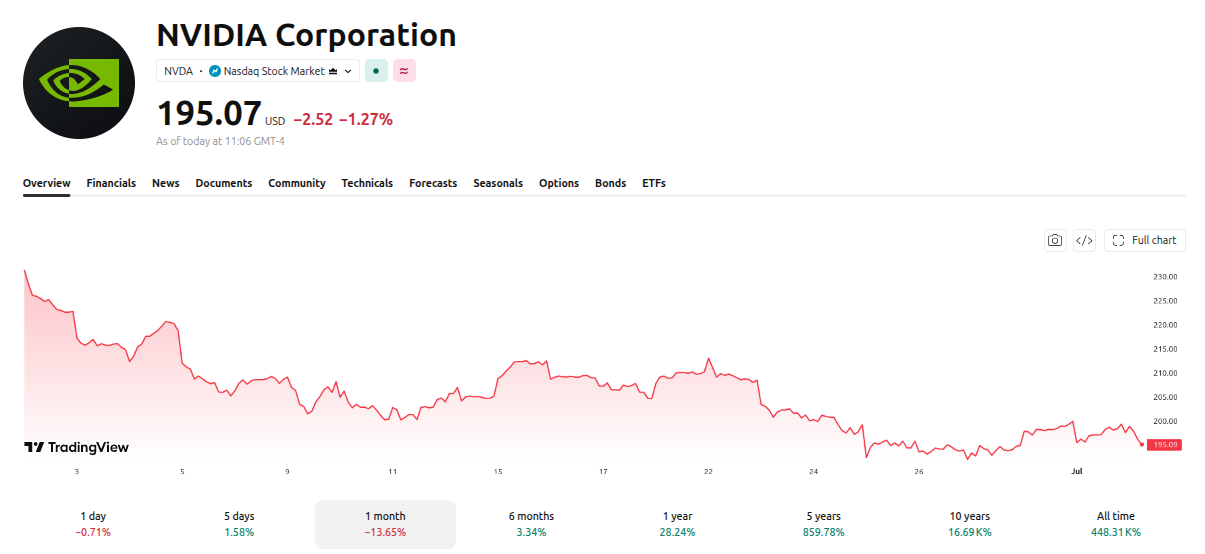

NVIDIA is expanding its AI infrastructure business with a new model designed to accelerate the deployment of computing capacity across global cloud providers.

The move arrives as Michael Burry increases bearish positions against NVIDIA, creating a sharp debate over AI growth prospects.

What is NVIDIA’s New AI Compute Model

NVIDIA’s new AI compute framework allows cloud providers to deploy advanced hardware using revenue-sharing and credit-support agreements. The goal is to reduce infrastructure barriers for startups, enterprises, model developers, and regional AI operators.

The company earns revenue from hardware sales and from cloud usage generated by supported capacity. This approach aims to accelerate the construction of large-scale AI factories capable of serving inference workloads and token-intensive applications.

Follow us on X to get the latest news as it happens

The strategy addresses one of the industry’s biggest challenges: the enormous capital required to build AI infrastructure. By helping partners expand capacity faster, NVIDIA hopes to increase utilization rates while making advanced computing resources more accessible.

Early participants illustrate the scale of the initiative. Sharon AI plans to deploy up to 40,000 Grace Blackwell GB300 GPUs. Meanwhile, Firmus is developing a major campus in Indonesia that could support approximately 170,000 GPUs and 360 megawatts of power capacity.

Why is Michael Burry Betting Against NVDA

Despite NVIDIA’s continued momentum, some investors remain skeptical about how long current AI-driven valuations can be sustained. Among the most prominent bears is Michael Burry, the investor known for predicting the 2008 housing market collapse.

Burry’s latest move goes beyond a general warning about the sector. He disclosed a direct short position on NVIDIA at approximately $198.09 per share, while also establishing bearish positions against Tesla, Applied Materials, Caterpillar, and the iShares Semiconductor ETF (SOXX).

His thesis is centered on what he views as excessive enthusiasm surrounding artificial intelligence. Burry argues that massive investments in data centers, chips and AI infrastructure may be creating conditions similar to previous technology bubbles.

He has specifically raised concerns about rapid hardware obsolescence, aggressive capital spending by hyperscalers, and the possibility that demand growth could eventually slow.

Supporters of NVIDIA see the situation differently. They point to strong demand for AI inference, which is accelerating enterprise adoption and strengthening the company’s dominant position in advanced computing. NVDA traded near $195 at the time of writing, giving the chipmaker a market value of roughly $4.77 trillion.

The result is a growing divide on Wall Street. NVIDIA’s bulls believe the company remains at the center of a multi-year AI expansion cycle, while Burry is positioning for a scenario in which expectations have outpaced economic reality. The coming quarters could determine which view gains the upper hand.

What Could Happen Next for NVIDIA

The coming quarters may provide important answers for both bulls and bears. NVIDIA’s success depends on executing its AI factory vision and maintaining strong demand for current and future platforms, including Blackwell and Rubin-based systems.

Investors will closely monitor earnings results, cloud partnership expansion, and progress on infrastructure deployment. If adoption continues accelerating, NVIDIA could further strengthen its position at the center of the global AI ecosystem.

However, valuation concerns are unlikely to disappear. Any slowdown in spending, infrastructure utilization, or enterprise demand could increase volatility.

The result is a high-stakes contest between technological transformation and concerns that expectations may have outpaced economic reality.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post NVIDIA Unveils New AI Compute Model, But Michael Burry is Shorting Its Stock appeared first on BeInCrypto.

JPMorgan warned that MicroStrategy’s new Bitcoin sales policy adds unnecessary risk to the crypto market. The Michael Saylor-led firm may sell up to $1.25 billion in Bitcoin to fund preferred dividends across the coming months.

The warning arrives as Strategy (formerly MicroStrategy) loses ground on both its common and preferred stock across broader financial markets.

Why JPMorgan Sees Two-Way Risk in MicroStrategy’s Plan

A two-way risk is a scenario in which price moves in either direction can create potential losses for market participants exposed to the underlying asset. JPMorgan analysts led by Nikolaos Panigirtzoglou say Strategy’s new Bitcoin sales policy has now introduced exactly that dynamic into the crypto market.

MicroStrategy revealed the option to sell up to $1.25 billion in Bitcoin to strengthen its balance sheet. Furthermore, the company could also authorize preferred stock repurchases and share buybacks. The move follows a period of stress on both MSTR common shares and its preferred series.

Follow us on X to get the latest news as it happens

The company also set a new minimum cash reserve target. Strategy now aims to cover 12 months of preferred dividends and interest expense.

However, its current $2.55 billion in reserves only covers 17 months of obligations, leaving limited flexibility in the coming quarters.

JPMorgan pushed back hard on the approach. Analysts recommended a higher coverage target of 24-36 months. Moreover, they urged MicroStrategy to issue common equity to expand dollar reserves. That would reassure investors that the firm will not need to sell Bitcoin going forward.

Strategy remains the largest Bitcoin buyer globally. The firm has purchased roughly $13.7 billion of Bitcoin in 2026 alone and holds 847,363 BTC.

As a result, whether it buys or sells, the movement now creates significant unnecessary flow risk across the broader crypto market environment.

How Bitcoin and MSTR Are Digesting the Fresh Risks

Strategy’s May Bitcoin sale sent ripples across the market. The company sold 32 Bitcoin for approximately $2.5 million between May 26 and May 31. Furthermore, the move marked its first Bitcoin sale since 2022, a sharp reversal from Michael Saylor’s public “never sell” stance.

JPMorgan flagged the direct market impact of that transaction. The bank noted that MicroStrategy’s sale contributed to Bitcoin’s stress in late May and early June. Moreover, greater price volatility could ultimately hurt the company itself, raising the cost of future equity and debt financings.

MSTR stock has slid 34% this year to $100.77. Its STRC preferred series follows the same pattern, down 12% at $87.09. Bitcoin also trades under pressure, off 30% year-to-date at $61,486.

However, JPMorgan analysts see a potential contrarian angle. The current bearish sentiment could set up a stronger second half if two conditions align. Strategy must expand dollar reserves. Moreover, the United States must approve the CLARITY Act to unlock renewed institutional flows.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post JPMorgan Sounds the Alarm on MicroStrategy’s New Bitcoin Sales Policy appeared first on BeInCrypto.

Binance has returned to the Philippine market through a regulatory sandbox route, while its European operations face new limits. The exchange gained access through BlockShoals Technologies, which secured approval from the Philippine SEC. However, Binance also restricted some services in several EU countries after MiCA rules fully took effect.

Binance Re-Enters Philippines Through SEC Sandbox

The Philippine Securities and Exchange Commission approved BlockShoals Technologies to test crypto-related services under its regulatory sandbox. The approval allows the company to operate its Stratbox model with selected products for local users. As a result, Binance gains a regulated pathway back into the Philippine market.

The sandbox approval followed an earlier clearance granted in November 2025, after BlockShoals met the remaining compliance requirements. The SEC said the company will operate under a crypto-asset intermediary model. Therefore, Philippine users can access selected services through a global crypto-asset service provider partner.

Binance acts as the global partner in the approved testing framework. BlockShoals will connect its systems with a local virtual-asset service provider partner during a 90-day rollout. After that, the company will continue testing user onboarding and product access under regulatory supervision.

Philippine Crypto Rules Tighten As Binance Returns

The approval comes as the Philippines continues to tighten its crypto market rules. Regulators have moved to strengthen listing standards and restrict assets that raise oversight concerns. Earlier, the country also pushed restrictions on privacy coins under its broader compliance approach.

This background gives Binance’s return a narrow but important regulatory angle. The exchange does not re-enter through a full open-market relaunch. Instead, it enters through a controlled sandbox with defined products, safeguards, and testing limits.

The structure also gives regulators more room to monitor user access and platform activity. It allows the SEC to test how offshore crypto services connect with local rules. Therefore, the Philippine market becomes a measured entry point for Binance in Southeast Asia.

Binance Limits EU Access After MiCA Deadline

While Binance gains room in the Philippines, it faces tighter conditions in Europe. The exchange has suspended new user registration, deposits, and Earn products in several EU markets. These restrictions affect users in Italy, Spain, France, Poland, Belgium, and Sweden.

The changes followed the end of the European Union’s MiCA transition period on July 1. MiCA created a unified licensing framework for crypto-asset service providers across the bloc. However, exchanges must secure authorization in an EU member state to continue full operations.

Binance had planned to seek authorization in Greece, but later withdrew that application before the deadline. The company said it will now pursue licensing in another EU member state. Meanwhile, it continues to work with regulators to restore compliant services across the region.

Withdrawals Remain Open As Binance Adjusts

Binance said affected users can still withdraw and transfer their assets. The exchange also said product access will vary by country, account status, and available services. Therefore, some users may face broader limits than others, depending on local restrictions.

The company has told users to rely on official communication channels for updates. It also said customer support will handle product access and withdrawal-related questions. This approach aims to reduce confusion as service limits take effect across affected markets.

The contrast between the Philippines and Europe shows Binance’s uneven regulatory path. In one market, the exchange gains access through supervised testing and local partnerships. In another, it pulls back while seeking a license under stricter regional crypto rules.

Top 25 And 1: Donnie Freeman’s injury knocks St. John’s down in early rankings

The US Marines just accepted six F-35Bs carrying lead weights where their radars should have been installed

Michael Saylor’s Strategy Can Sell $1.25 Billion Bitcoin? #shorts

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics7 days ago

Politics7 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics7 days ago

Politics7 days agoPotential 2028er World Cup attendee leaderboard

-

Business7 days ago

Business7 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World7 days ago

Crypto World7 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Crypto World7 days ago

Crypto World7 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Sports1 day ago

Sports1 day agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Tech5 days ago

Tech5 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

You must be logged in to post a comment Login