Crypto World

Stripe’s Bridge secures MiCA and EMI licenses to expand across EU

Bridge has secured both a Markets in Crypto-Assets (MiCA) crypto-asset service provider authorization and an Electronic Money Institution (EMI) license in Luxembourg, giving it a regulated framework to offer services across all 27 European Union member states.

Summary

- Bridge has secured MiCA authorization and an EMI license, allowing it to offer regulated services across all 27 EU member states.

- The approvals enable businesses to issue euro backed stablecoins, provide named IBANs, and expand cross border payment services.

- The licenses come as Europe enforces MiCA rules, with more firms seeking regulatory approval while noncompliant stablecoins exit regulated platforms.

According to Bridge, the dual licensing allows the company to operate under the European Union’s MiCA framework while expanding its stablecoin and euro payment services for businesses and developers throughout the bloc.

The company said the approvals were granted in Luxembourg and cover all EU member states under a single regulatory regime that includes requirements for capital reserves, custody, and operational safeguards.

The licenses also introduce new products for companies building on Bridge’s infrastructure. Businesses will be able to issue custom euro-backed stablecoins, create virtual IBANs in customers’ names, and offer euro accounts that work across the European Union without establishing separate banking relationships in each country, according to the announcement.

New payment tools for European businesses

Bridge said fintech companies can use the platform to provide named IBANs and cross-border euro accounts through one integration. Businesses launching loyalty programs, rewards systems, on and off ramps, or in-app payment products will also be able to issue their own EUR-backed stablecoins without building reserve management and regulatory infrastructure themselves.

The company added that enterprises can use custom stablecoins to transfer funds between subsidiaries instead of relying on correspondent banking networks. Banks, meanwhile, can settle transactions between institutions through stablecoin infrastructure rather than conventional interbank messaging systems.

“A business in the EU can now issue its own euro stablecoin and pair it with named IBANs and named EUR payouts across all 27 member states, on a single integration,” Mai Leduc Blount, Head of Product at Bridge, said in an accompanying statement.

Bridge has already been expanding its regulated payments business outside Europe as well. In March, Visa announced it was extending its partnership with the Stripe-owned company to bring stablecoin-backed Visa cards to more than 100 countries by the end of 2026.

Europe tightens stablecoin rules under MiCA

The approvals come days after the European Union completed the final phase of its MiCA transition on July 1, requiring regulated crypto platforms to support only compliant stablecoins.

While companies such as Bridge and CACEIS continue securing MiCA authorization to expand regulated services across the bloc, other market participants have been scaling back operations that no longer meet the framework.

As previously reported by crypto.news, Coinbase, Kraken, and Crypto.com removed USDT trading for European users after Tether chose not to seek MiCA authorization.

Crypto exchange Binance has also implemented MiCA-related service changes and said affected users would continue to have access to options previously communicated by the exchange, including withdrawals and transfers where applicable.

India’s central bank is weighing a policy approach aimed at containing crypto activity—particularly by limiting how banks and regulated financial institutions interact with digital assets and privately issued stablecoins—according to a report by The Economic Times. The stance is expected to feed into a broader review of the country’s digital asset framework as lawmakers prepare a report.

In a background note reviewed by a Parliamentary Standing Committee on Finance, RBI officials presented what the publication describes as a renewed emphasis on preventing crypto from being used in payments and settlements, while keeping the banking sector’s exposure controlled. The same materials reportedly argue that simply applying “traditional” regulation to crypto could inadvertently legitimize speculative assets and create a misleading sense of safety for users, though the RBI also urged policymakers to differentiate crypto from tokenized instruments that are already regulated.

Key takeaways

- The RBI’s reported position favors “containment” of crypto—especially by limiting banking-sector involvement—rather than a blanket ban on ownership.

- Officials reportedly reiterated support for prohibiting crypto use in payments and settlements to reduce systemic exposure to digital assets and private stablecoins.

- The RBI cautioned that treating crypto like conventional regulated products could confer unwarranted legitimacy to speculative tokens.

- At the same time, the RBI urged regulators not to conflate crypto with tokenized government securities or corporate bonds.

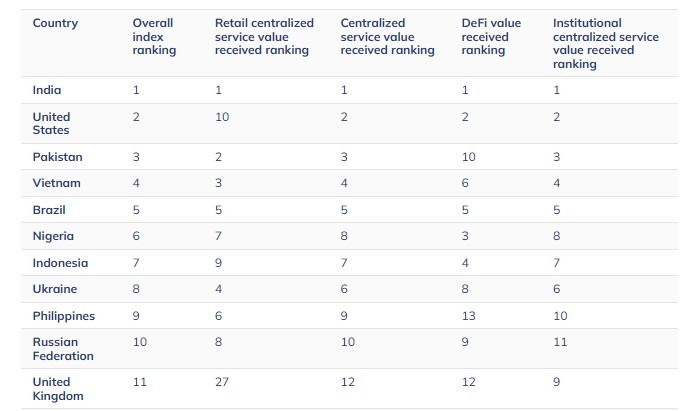

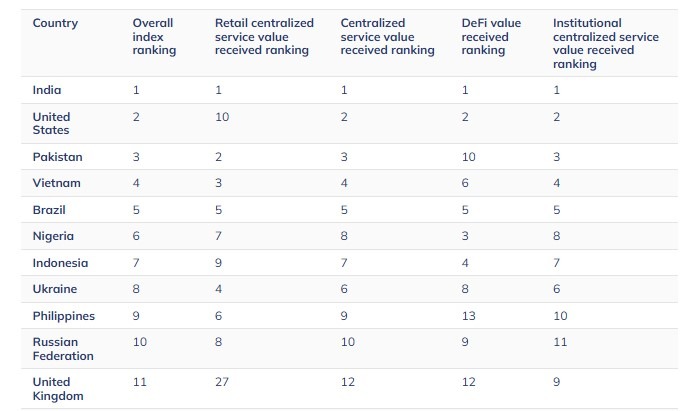

- India’s crypto adoption profile remains a point of contention, with Chainalysis placing India first in its 2025 Global Crypto Adoption Index while the RBI reportedly challenged the methodology.

Containment strategy and the RBI’s policy logic

According to The Economic Times, RBI Deputy Governor Rohit Jain and Executive Director P. Vasudevan shared the central bank’s views with the Parliamentary Standing Committee on Finance on Thursday. The submission reportedly lays out a policy framework in which outright prohibition remains “a recognized policy option,” but the operational thrust is to restrict crypto’s role in core financial functions—namely payments and settlements.

The RBI’s reported concern is that banks and other institutions could become conduits for risk if they are allowed to directly facilitate crypto transactions or hold exposure to privately issued stablecoins. In the background note, the central bank reportedly recommended policies that prevent crypto usage in payments and settlements while limiting the degree to which the banking system is exposed to digital asset activities.

That position also includes a caution about regulatory design. The RBI reportedly warned that applying established regulatory approaches meant for conventional financial instruments to crypto assets could end up legitimizing speculative tokens. The central bank’s argument, as described in the report, is that such an approach could create a “false perception of safety” among users.

Still, the RBI reportedly made an important distinction: policymakers should separate crypto from tokenized government securities, corporate bonds, and other regulated financial products. The practical implication is that the RBI appears to support tokenization where the underlying instrument is already within a regulated perimeter—while treating “crypto” broadly and its speculative use cases as a different category of risk.

How this echoes the RBI’s 2018 playbook

The reported containment push aligns with an approach the RBI used in 2018. At that time, the central bank directed regulated financial institutions to stop dealing in crypto or providing services to people and entities involved in crypto, effectively severing many crypto exchanges from India’s banking rails without banning individuals from holding or trading crypto.

That policy path was challenged and ultimately overturned. India’s Supreme Court overturned the circular in March 2020. In doing so, the court recognized the RBI’s authority to take preventive measures but concluded that the approach did not meet the “proportionality” standard—specifically noting the RBI had not demonstrated the harm experienced by the regulated entities affected by the measure.

In May 2021, the RBI clarified that banks could not cite the invalidated circular when advising customers against crypto transactions. However, the RBI also indicated that regulated institutions could continue applying know-your-customer (KYC), anti-money laundering (AML), and foreign-exchange compliance requirements, preserving compliance practices even as the earlier, more direct restriction was removed.

The key difference suggested by the latest reported submissions is framing: the RBI appears to be arguing for a policy model that limits crypto’s access to payments and settlement functions and constrains banking exposure, rather than relying purely on an exchange-banking cutoff. Whether Parliament and regulators can craft such a framework without running into the same proportionality objections that surfaced in 2020 is likely to be one of the central questions as the policy debate progresses.

Tokenization vs. “speculative” crypto

One of the more consequential aspects of the RBI’s reported position is its insistence on separation. The central bank reportedly warned against regulating crypto in a way that treats it as if it were equivalent to established financial instruments. At the same time, it urged policymakers to distinguish crypto assets from tokenized government securities and corporate bonds—categories that, in principle, sit closer to regulated capital markets.

For investors and market participants, this distinction matters because tokenization is often viewed as a potential bridge between traditional finance and distributed ledger technology. If regulators accept the argument that tokenized regulated instruments should not be blocked simply because they use similar technical formats, tokenization could evolve within a more familiar compliance environment. Conversely, if policymakers adopt a broad-brush approach, the same infrastructure could face tighter constraints even when the underlying asset is regulated.

In practical terms, what changes from this position is the emphasis on “use” and “function.” Rather than focusing only on who owns or trades tokens, the RBI’s reported approach appears more concerned with where crypto can be used (payments and settlements) and how much it can permeate the banking system—areas that policymakers can target without necessarily prohibiting market participation outright.

Adoption metrics under scrutiny

The RBI’s stance also intersects with discussions about India’s crypto adoption level. The report notes that India was ranked first in Chainalysis’ 2025 Global Crypto Adoption Index, though the RBI reportedly challenged the methodology behind private-sector adoption rankings.

This disagreement signals that, even as adoption becomes a key input into policy arguments, there is still no shared view of how adoption should be measured or interpreted. For lawmakers considering regulation, the takeaway is that adoption numbers may not settle the debate by themselves; policymakers will likely scrutinize both metric design and what those metrics truly indicate about user protection, financial stability risks, and the degree of institutional involvement.

With India’s regulatory framework still under review, readers should watch closely for how policymakers translate the RBI’s reported containment ideas into concrete rules—particularly around payments and settlement use cases, banking-sector permissible activities, and how regulators draw boundaries between tokenized regulated instruments and broader “crypto” categories.

The International Monetary Fund (IMF) warned that tokenized assets will remain peripheral unless markets resolve who legally owns them and where settlement is final.

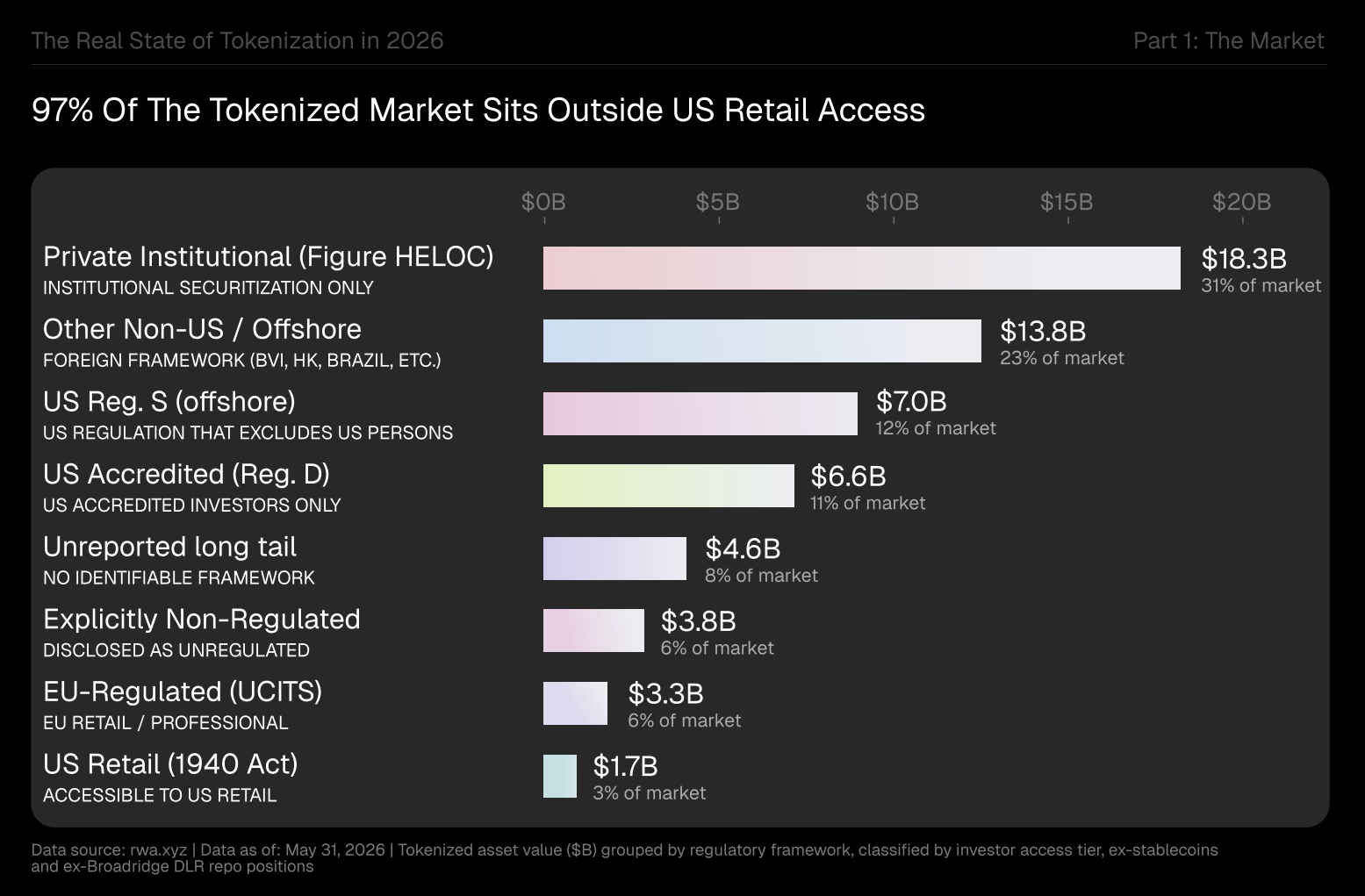

New BeInCrypto research shows why, mapping a $60 billion market fractured across regulatory regimes and largely closed to US retail investors.

Why Legal Clarity Matters For Tokenization’s Future, According to IMF

Tobias Adrian, Financial Counsellor and Director of the IMF’s Monetary and Capital Markets Department, highlighted that tokenization is more than a technology upgrade. He noted that it changes the structure of the financial system itself.

Legal clarity is central to that argument. Adrian said clear rules on ownership, settlement, and jurisdiction will decide whether tokenization moves to the center of finance or stays at its edge.

“Market participants must know whether tokenized records constitute definitive ownership, whether settlement finality is legally recognized, and which jurisdiction’s law applies. Without clarity, tokenization will remain fragmented and peripheral,” Adrian said.

Follow us on X to get the latest news as it happens

Ownership and Access Split the Market

BeInCrypto’s Real State of Tokenization in 2026 report puts hard numbers behind that concern. It tracked roughly $60 billion in tokenized real-world assets (RWAs) as of May 31, excluding stablecoins and repurchase agreements.

The market splits into several parallel markets rather than one. Regulatory regime, geography, and investor status divide them. About 97% of that value is either inaccessible to US retail investors or carries no retail-grade regulation.

Only $1.7 billion is open to retail buyers, while accredited US investors can access roughly $8.3 billion, including Regulation D products.

Ownership type is also part of the divide. Tokens fall into direct ownership, fund shares, or synthetic exposure. Synthetic structures give price exposure without any claim on the asset.

The distinction is clearest in equities. 59% of all stock tokens by count provide synthetic price exposure rather than actual share ownership, according to the report. Holders track a price but own no shares

Regulatory ambiguity compounds the problem. About 39% of the market lacks an identifiable regulatory framework, a gap the report flags as a due diligence risk for allocators.

Adrian frames the problem in principle. The report shows it in the data. Both point to the same unfinished work on ownership rights and settlement. The open question is whether that infrastructure arrives soon enough.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Who Actually Owns a Tokenized Asset? The IMF Wants an Answer appeared first on BeInCrypto.

The Reserve Bank of India (RBI) reportedly backed a containment strategy for digital assets to shield banks and other financial institutions from exposure to crypto and privately issued stablecoins, as lawmakers prepare a report on the country’s digital asset policy.

According to a report by The Economic Times, RBI Deputy Governor Rohit Jain and Executive Director P. Vasudevan presented the central bank’s position to the Parliamentary Standing Committee on Finance on Thursday.

In a background note submitted to the panel, the RBI reportedly said prohibition remained a recognized policy option and recommended preventing the use of crypto in payments and settlements while restricting banking-sector exposure.

The central bank reportedly warned that applying traditional regulation to crypto could legitimize speculative assets and create a false perception of safety among users. However, it urged policymakers to distinguish crypto from tokenized government securities, corporate bonds and other regulated financial instruments so that restrictions would not hinder tokenization.

Chainalysis’ 2025 Global Crypto Adoption Index. Source: Chainalysis

India ranked first in Chainalysis’ 2025 Global Crypto Adoption Index, although the RBI reportedly challenged the methodology behind private-sector adoption rankings.

RBI renews push to isolate crypto from banking

The RBI’s latest reported proposal echoes an approach it took in 2018, when the central bank directed regulated financial institutions to stop dealing in crypto or providing services to individuals and businesses involved in them.

The approach effectively cut off crypto exchanges from India’s banking system without prohibiting individuals from owning or trading crypto.

India’s Supreme Court overturned the circular in March 2020, following a challenge brought by exchanges and the Internet Mobile Association of India. The court recognized the RBI’s authority to take preventive action but found that the measure failed the test of proportionality, noting that the central bank had not shown harm suffered by entities it regulated.

Related: India arrests Darwin Labs co-founder in GainBitcoin scam probe

In May 2021, the RBI clarified that banks could no longer cite the invalidated circular when cautioning customers against crypto transactions. However, it said regulated institutions could continue applying know-your-customer, anti-money laundering and foreign-exchange compliance requirements.

Magazine: Bitcoin decouples from tech stocks, Ether eyes ‘selling wave’: Market Moves

Crypto World

Bitcoin News: A Weak Jobs Report Just Slashed Fed Rate Hike Odds in Half, And Bitcoin Bounced Off $57,750 to Reclaim $61,000

Bitcoin price clawed back the $62,000 level after June non-farm payrolls printed at 57,000, less than half the 113,000 consensus، sending the implied probability of a September Fed rate hike from 64% to 54% on the CME FedWatch Tool news and dragging AI stocks sharply lower.

The question that data forces onto the table is whether this macro shift marks a durable floor or simply a relief bounce inside a structure that has already given up 20% in a single month.

The US Labor Department compounded the miss by revising April and May figures downward by a combined 74,000 jobs, signaling that prior strength in the labor market was overstated.

— TrendSpider (@TrendSpider) July 2, 2026

JUST IN: U.S. June Economic Data:

JUST IN: U.S. June Economic Data:

Initial Jobless Claims: 215k vs 220k est

Non Farm Payrolls: 57k vs 110k est

Unemployment Rate: 4.2% vs 4.3%

BTC had bottomed at $57,750 on Wednesday before the report; the jobs data gave the asset the catalyst it needed to distance itself from that low, recovering above $60,000 alongside a broader move into scarce-asset proxies.

Discover: The Best Token Presales

Bitcoin News: What a Labor Miss Actually Means for BTC

Weak labor data reduces inflationary pressure and, by extension, the Fed’s justification for holding rates elevated. That transmission mechanism is direct: lower rate-hike odds compress the opportunity cost of holding non-yielding assets like Bitcoin and gold, while simultaneously raising expectations for eventual balance sheet expansion.

The Fed’s balance sheet currently sits stagnant at $6.73 trillion, though its mandate permits $40 billion in monthly short-term Treasury purchases, a lever that remains undeployed and increasingly relevant if labor data continues to soften.

Gold reinforced that read Thursday, recovering a portion of the 8% losses it accumulated over the prior two weeks. Central bank liquidity conditions remain the primary macro driver for both assets, and gold’s bounce adds credibility to the narrative that markets are pricing a less restrictive Fed rather than a one-day tactical trade.

WTI crude stabilized below $70 after Qatar’s Foreign Ministry cited positive progress in US–Iran negotiations, reducing the inflationary risk premium on oil and leaving additional room for stimulus discussions.

The Nasdaq 100 told a different story. The index erased three consecutive days of gains on Thursday as chipmakers and AI-adjacent hardware names took the heaviest damage.

SanDisk, Seagate, Western Digital, and Applied Materials each fell 9% or more intraday. That kind of synchronized selloff in the AI hardware complex is not simply profit-taking; it signals that the valuation premium embedded in the sector’s growth assumptions is being questioned, and some of that capital will seek a landing spot.

Discover: The Best Crypto to Diversify Your Portfolio

On-Chain: Seller Exhaustion at Levels Not Seen Since 2022

The macro catalyst and news matter less for Bitcoin if the underlying on-chain structure is still deteriorating. It is not. CryptoQuant analyst gaah_im reported that Bitcoin’s realized profit-to-loss ratio has hit its lowest level since 2022, with the net percentage of supply in profit relative to total supply turning negative.

Historically, that combination has marked cycle bottom inflection points with what the analyst described as “extreme precision.”

What the on-chain data confirms is that seller exhaustion is real at current prices, holders who were going to capitulate largely have.

What it does not confirm is timing: a metric flagging a cycle low tells you the floor is close, not that the next weekly candle resolves higher. Bitcoin was also rejected at $82,500 two months prior, and that supply zone has not been neutralised.

The realized profit-to-loss signal is most useful as a risk-management input rather than a directional trigger. It narrows the probability distribution of downside outcomes without eliminating them.

Analysts flagging a potential sub-$60,000 retest as a “healthy validation” of the bottom are not wrong, that scenario remains live if upcoming CPI data or FOMC communications re-accelerate hawkish pricing. The downside case for Bitcoin does not disappear because one labor print came in soft.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Bitcoin News: A Weak Jobs Report Just Slashed Fed Rate Hike Odds in Half, And Bitcoin Bounced Off $57,750 to Reclaim $61,000 appeared first on Cryptonews.

RBI has reportedly renewed its call to keep banks and payment systems insulated from cryptocurrencies and privately issued stablecoins as India reviews its digital asset policy.

Summary

- RBI has reportedly recommended limiting banks’ exposure to cryptocurrencies and privately issued stablecoins.

- The central bank also proposed preventing crypto from being used for payments while keeping tokenized regulated assets outside any restrictions.

- The proposal comes as India continues tightening crypto oversight through stricter AML rules and enhanced compliance checks.

As first reported by The Economic Times, Reserve Bank of India Deputy Governor Rohit Jain and Executive Director P. Vasudevan presented the central bank’s position before the Parliamentary Standing Committee on Finance on Thursday, accompanied by a background note outlining its recommendations.

According to the report, the RBI said prohibition remains a recognized policy option and recommended preventing cryptocurrencies from being used in payments and settlements while limiting the banking sector’s exposure to digital assets and privately issued stablecoins.

The central bank also argued that regulating cryptocurrencies under conventional financial rules could give speculative assets an appearance of legitimacy and create a misleading sense of safety for users, the report said.

At the same time, it reportedly urged policymakers to distinguish cryptocurrencies from tokenized government securities, corporate bonds and other regulated financial assets so that tokenization initiatives are not affected by crypto-related restrictions.

The RBI also questioned the methodology used in private-sector crypto adoption rankings, despite India placing first in Chainalysis’ 2025 Global Crypto Adoption Index.

RBI revives long-standing banking concerns

The latest recommendations closely resemble the central bank’s position from 2018, when it directed regulated financial institutions to stop offering services to businesses and individuals dealing in cryptocurrencies. Although the move did not ban crypto ownership or trading, it effectively cut exchanges off from India’s banking system.

India’s Supreme Court struck down that circular in March 2020 after exchanges and the Internet and Mobile Association of India challenged the restriction. While the court accepted that the RBI had authority to take preventive measures, it ruled the banking ban was disproportionate because the central bank had not demonstrated harm to the institutions it supervised.

A year later, the RBI clarified that banks could no longer rely on the invalidated circular when warning customers about crypto transactions. However, regulated entities were instructed to continue complying with know-your-customer, anti-money laundering, and foreign exchange rules.

Crypto oversight expands across multiple fronts

The RBI’s reported recommendations come as Indian authorities continue tightening oversight of the crypto sector through other regulatory channels.

Last month, India’s Financial Intelligence Unit asked several major crypto exchanges to preserve records of over-the-counter crypto transactions exceeding $10,000 from January 2026 onward, with compliance checks focusing on beneficial ownership, source of funds and destination wallets. The request followed earlier FIU guidance that strengthened customer verification requirements through measures such as live selfie checks, geolocation, IP tracking and periodic KYC updates.

Regulatory attention has also extended to stablecoin activity. Earlier this week, The Economic Times reported that enforcement action against crypto remittance firms disrupted domestic USDT supply, pushing the stablecoin’s premium in India above 8.5%.

The same report noted that lawmakers were scheduled to discuss the country’s approach to virtual digital assets with the RBI and the Institute of Chartered Accountants of India, while the central bank has continued warning about risks linked to cryptocurrencies and privately issued stablecoins.

Crypto World

MEXC’s June Highlights: $437 Billion in Trading Volume, Offering Access to 7,000+ US Stocks and ETFs

Victoria, Seychelles, July 3, 2026 – MEXC, a pioneer in 0-fee digital asset trading, announced key highlights for June 2026. The platform recorded $437 billion in monthly trading volume and expanded user investment options through the launch of the “RealStocks” product. The new product gives users real ownership of over 7,000 U.S.-listed stocks and ETFs—complete with dividend eligibility—breaking down traditional market barriers and connecting users to global assets, all within their existing MEXC account.

In June, MEXC continued to expand access to emerging assets, listing 153 new tokens across spot and futures markets and driving $1.03 billion in new listing trading volume. Through its 0-fee trading policy, MEXC saved users a cumulative $145 million in trading fees across 927 trading pairs spanning spot, futures, and other markets. The platform also provided $38 million in futures position airdrops for users during the month.

MEXC remains committed to safeguarding user assets through robust protection mechanisms and transparent practices. The Guardian Fund stood at $101 million in June, providing users with an added layer of security. MEXC has committed to expanding the Guardian Fund from $100 million to $500 million over the next two years. MEXC’s June Proof of Reserves report, independently audited by Hacken, confirmed reserve ratios above the industry safety benchmark of 100% across major assets, with USDT at 114%, USDC at 125%, BTC at 269%, and ETH at 118%.

Additionally, MEXC’s customer support team processed 57,348 online inquiries in June, maintaining an average response time of 63.03 seconds. The platform issued 21,548 loss coverage vouchers to users during the month.

June’s highlights reflect MEXC’s continued efforts to support users through 0-fee trading, product innovation, and asset protection. As a one-stop trading platform, MEXC will continue to expand its asset offerings, strengthen user protection, and enhance service quality, giving users broader, safer, and more accessible ways to participate in global markets.

About MEXC

MEXC is the world’s fastest-growing cryptocurrency exchange, trusted by more than 40 million users across 170+ markets. Built on a user-first philosophy, MEXC offers industry-leading 0-fee trading and access to over 3,000 digital assets. As the Gateway to Infinite Opportunities, MEXC provides a single platform where users can easily trade cryptocurrencies alongside tokenized assets, including stocks, ETFs, commodities, and precious metals.

MEXC Official Website| X | Telegram |How to Sign Up on MEXC

For media inquiries, please contact MEXC PR team: media@mexc.com

Risk Disclaimer:

This content does not constitute investment advice. Given the highly volatile nature of the cryptocurrency market, investors are encouraged to carefully assess market fluctuations, project fundamentals, and potential financial risks before making any trading decisions.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

A teenager suspected of helping the “Scattered Spider” hacking group has been extradited to the United States to face charges tied to an alleged cryptocurrency ransom scheme worth $8 million. The case highlights how ransomware crews increasingly lean on social engineering, stolen credentials, and fast escalation from initial access to extortion demands.

The U.S. Department of Justice said Wednesday that Peter Stokes, 19, a dual U.S.-Estonian national, was arrested in Finland in April after an Interpol Red Notice and was extradited to the United States last week. He is expected to appear in federal court in Chicago on Tuesday.

Key takeaways

- U.S. authorities allege Stokes helped breach a luxury jewelry retailer’s systems in May 2025 and demand an $8 million crypto ransom.

- The DOJ says phishing calls to a help desk were used to obtain password resets and compromise employee and IT-admin accounts quickly.

- The retailer allegedly evicted the attackers and refused to pay, but still faced $2 million in disruption damages.

- The Justice Department links Stokes to Scattered Spider (also known as Octo Tempest and other aliases), a group authorities say has conducted more than 100 network intrusions.

- Ransomware payments reportedly fell last year even as attacks rose, underscoring that victim refusal and operational disruption do not eliminate extortion risk.

Extradition follows an alleged $8 million crypto extortion

The indictment and unsealed criminal complaint, as described by the DOJ, accuse Stokes and others of breaching a luxury jewelry retailer’s computer system in May 2025. Prosecutors allege the intrusion involved stealing data and issuing a demand for an $8 million ransom paid in cryptocurrency.

According to the complaint, the retailer managed to remove the attackers from its network and did not pay the ransom. Even so, the DOJ states the company incurred approximately $2 million in disruption damages, reflecting the cost of incident response, operational downtime, and the business impact that can follow an intrusion—regardless of whether attackers receive payment.

The DOJ also framed Stokes as one of the limited number of arrests it has directly connected to Scattered Spider, a group commonly associated with ransomware and crypto-based extortion.

Phishing calls and credential resets as the first move

Prosecutors allege the attack chain began with phishing calls to the retailer’s technology help desk. Stokes and others reportedly posed as employees to request resets of login credentials, a common tactic that turns administrative workflows—designed to restore access for legitimate users—into a shortcut for attackers.

In the complaint, authorities state the hackers compromised three employee accounts in as little as two hours. Two of those accounts belonged to IT administrators, giving the intruders access to higher-privilege systems. Prosecutors further allege those higher-privilege accounts were themselves breached and used to reach deeper into the retailer’s environment.

Within days, the complaint says the attackers sent a ransom note from a compromised company email account, demanding funds or threatening to publish credit card and payment information. The retailer, according to the complaint, resisted the intrusion and later experienced separate outreach from the attackers repeating the $8 million demand.

For defenders, the alleged sequence underscores why help desk and identity processes are a frequent focal point in real-world intrusions: once a reset request is accepted, the attack can progress quickly to privilege escalation and broader system access.

Alleged role in Scattered Spider intrusions and extortion

The complaint characterizes Stokes as a member of Scattered Spider who allegedly engaged in “numerous intrusions, or assisted in them” across multiple companies that prosecutors did not name in the filing. According to the DOJ, an examination of a storage device attributed to Stokes contained downloads from a virtual private server that Microsoft had identified as being used to carry out intrusions.

The complaint also alleges the device held “exfiltrated records from multiple victim-companies,” suggesting the attacker infrastructure was used not only to gain access, but also to extract data—an essential ingredient for ransomware-style pressure campaigns, including data-leak threats.

Authorities further pointed to Stokes’ social media activity as circumstantial evidence of involvement. The complaint claims his Snapchat account showed signs of substantial wealth for a person his age, and that he reportedly boasted about international travel and wealth. Prosecutors also allege he shared media related to apprehended Scattered Spider members.

The Justice Department said Scattered Spider—also described by multiple aliases, including “Octo Tempest,” “UNC3944,” and “0ktapus”—has been involved in more than 100 network intrusions. The DOJ estimates those intrusions resulted in over $100 million in ransom payments and millions of dollars in damages.

Stokes faces six counts tied to alleged hacking, cyber extortion, fraud, and conspiracy.

Ransom payments down, attacks up: what this case suggests

While this matter involves a claimed $8 million demand, it lands in a broader ransomware pattern that authorities and analysts have reported: total payments may be declining even as attacks increase.

According to figures cited by the DOJ, ransomware actors received more than $820 million in payments last year, an 8% decline compared with 2024. At the same time, attacks rose by 50%, as referenced in coverage linked to Chainalysis data. Taken together, the numbers suggest that victims are not necessarily paying as often or as much, but ransomware groups remain active and effective at reaching targets.

The filing’s allegations about the retailer evicting the attackers and refusing the ransom illustrate why: even when payments fail, attackers may still profit indirectly through disruption costs, data theft, reputational harm, and follow-on damages. For organizations, the practical takeaway is that “no payment” does not mean “no impact”—it often signals more urgent remediation work and financial exposure after incident response.

Readers should watch how the case develops in Chicago federal court, particularly whether the defense challenges the alleged linkage between Stokes and the intrusions described in the complaint. Equally important is what prosecutors emphasize next about the help-desk phishing phase and the role of stolen credentials, since that early foothold remains a central vulnerability for many companies targeted by ransomware crews.

Ireland’s Criminal Assets Bureau (CAB) has confirmed the seizure of an additional 500 Bitcoin, worth roughly €27 million (about $30.9 million), in cooperation with Europol’s European Cybercrime Centre. The agency said the latest action brings CAB’s total Bitcoin seizures for 2026 to 1,500 BTC, valued at approximately $92.4 million.

In its update posted Thursday, CAB said Europol provided operational coordination, technical expertise, and decryption support during the investigation. The bureau did not name the wallet owner or provide further details about how the access was obtained.

Key takeaways

- CAB confirmed a new 500 BTC seizure in cooperation with Europol’s European Cybercrime Centre.

- Total CAB Bitcoin seizures in 2026 now stand at 1,500 BTC, valued around $92.4 million.

- Authorities have not publicly linked this latest wallet action to any specific criminal case.

- Separately, public tracking suggests a wallet address associated with Clifton Collins moved 500 BTC on Thursday.

New seizure brings 2026 total to 1,500 BTC

The bureau’s announcement is the latest in a run of Bitcoin-related enforcement activity. CAB said the seized 500 BTC are currently worth about €27 million and emphasized the cross-border support from Europol’s European Cybercrime Centre, particularly around technical work and decryption.

For investors and users, the key operational signal is not only the size of the seizure but the pattern of international cooperation—CAB’s reference to Europol support underscores how ongoing cryptocurrency investigations increasingly depend on specialized technical capabilities rather than traditional evidence-gathering alone.

Cab also did not offer any additional comment beyond the confirmation, leaving open questions about the nature of the underlying investigation and whether the seized funds come from the same larger case previously discussed in Irish media.

Earlier wallet access set the stage for another 500 BTC

Months earlier, CAB said it had gained access to and seized a cryptocurrency wallet containing 500 Bitcoin. That earlier wallet was reported by Irish media to have been connected to Clifton Collins, a convicted drug dealer.

According to The Irish Times, the March wallet authorities accessed was one of twelve wallets believed to have held about 6,000 BTC once owned by Collins. The paper containing the private keys was reportedly lost, adding a layer of difficulty to how investigators were able to unlock and move the funds.

While CAB did not confirm a connection between Thursday’s seizure and Collins, the timing matters. Public blockchain observers linked to Collins have pointed to movement from an address associated with him around the same day as CAB’s announcement.

Public tracking: Collins-linked address moved 500 BTC

In coverage tied to the earlier Collins-linked wallet, blockchain explorers and analysts have monitored the remaining balances attributed to those holdings. The article notes that an address associated with Collins reportedly moved 500 Bitcoin to an unknown address on Thursday.

As of Friday, wallets still associated with Collins were reported to hold 4,500 BTC, valued at about $277 million. The figure is based on public tracking rather than an official CAB statement, so readers should treat it as observational data rather than confirmed custody or law-enforcement control.

Still, the sequence is notable: the combination of CAB’s 500 BTC seizure announcement and independent reporting of movement from Collins-associated addresses suggests the criminal wallet landscape remains actively contested long after the first tranche of recovered funds.

What authorities previously said about how Collins stored keys

Collins was arrested in 2017 after police searched his car and found cannabis, according to The Guardian. Prosecutors said he used proceeds from his drug operation to purchase about 6,000 Bitcoin in late 2011 and early 2012, spreading the holdings across twelve wallets.

Authorities and reporting described a key-management strategy that relied on a single physical backup: Collins stored the wallet keys on a sheet of A4 paper, hidden inside the aluminum cap of a fishing rod case at his rental home. After his arrest, the landlord allegedly discarded Collins’ belongings. Collins claimed the fishing rod case had been stolen before the landlord entered the property.

That dispute—and the reported loss of the keys—help explain why access to some of the holdings could have taken time. It also highlights a broader lesson for the ecosystem: even when large balances are held securely on-chain, off-chain key handling and physical storage failures can ultimately determine whether funds remain reachable.

With CAB now confirming another 500 BTC seizure in 2026, the open question for the market is how quickly investigators can continue collapsing the gap between wallets once considered “lost” and the funds that ultimately get moved and frozen. Readers should watch for whether CAB’s next updates clarify the relationship—if any—between Thursday’s seizure and the remaining Collins-associated holdings, as well as how Europol’s technical role evolves in future operations.

Brazil has approved new prudential rules that will require virtual asset service providers to meet capital, risk management, and disclosure standards from 2027.

Summary

- Brazil has approved new prudential rules requiring crypto service providers to meet capital, risk management, and disclosure standards from 2027.

- Virtual asset firms will move into Brazil’s S4 regulatory segment by mid 2028, while smaller S5 institutions will no longer be allowed to offer crypto services.

- The new requirements extend Brazil’s ongoing crypto regulatory framework, following recent licensing audits and foreign exchange rules.

According to a local media report, Brazil’s Central Bank has approved a new set of prudential requirements for virtual asset service providers (SPSAVs), bringing them closer to the regulatory framework applied to securities brokers and distributors. The rules were approved on July 1 and will take effect on Jan. 1, 2027, as part of the country’s ongoing implementation of its cryptoasset legal framework.

Once the rules come into force, companies offering cryptocurrency and other virtual asset services will have to maintain minimum capital reserves, establish formal risk management policies, and periodically disclose information about their financial and operational condition. The Central Bank said the measures are intended to strengthen the financial system and reduce risks for customers and the market.

The report stated that firms providing crypto brokerage, custody, and transfer services will now be classified as Type 3 institutions together with the economic groups they lead. According to the Central Bank, the classification follows the principle that activities carrying similar risks should be subject to similar regulatory standards.

Another part of the framework introduces a phased transition into Brazil’s banking supervision structure. The report said all virtual asset service providers will be placed in Segment 4 (S4) by June 30, 2028, regardless of their size, giving them additional time to comply with the full prudential requirements.

At the same time, institutions classified under Segment 5 (S5), which follows a simplified regulatory regime for smaller financial institutions, will no longer be permitted to provide virtual asset services because the Central Bank considers those activities incompatible with lighter supervisory standards.

Latest step in Brazil’s crypto oversight

The new requirements add to a series of regulatory measures introduced over the past year. In November 2025, the Central Bank published the first operating rules for virtual asset service providers, establishing standards covering governance, anti-money laundering controls, foreign exchange participation, and operational requirements.

Earlier this year, Brazil’s National Monetary Council required crypto platforms to follow confidentiality rules comparable to those imposed on traditional financial institutions, including compliance with Complementary Law 105 on bank secrecy.

The latest prudential framework also follows a June rule requiring crypto companies seeking authorization or license renewals to submit independent audit reports prepared by professionals registered with Brazil’s securities regulator.

As previously reported, the audits review anti-money laundering controls, counter terrorism financing procedures, customer asset segregation, internal risk management, and employee compliance programs before licensing decisions are made.

Regulators have also tightened oversight in other areas during 2026. In May, Brazil’s Central Bank prohibited regulated cross-border electronic foreign exchange providers from using crypto assets to settle international payments, while still allowing digital assets to be traded and transferred outside the supervised payment system.

More recently, federal prosecutors reminded political parties that cryptocurrency donations remain prohibited in election campaigns because campaign finance rules require donors to be clearly identified.

FUNToken continues to make accessing the $FUN ecosystem simpler by expanding its supported deposit options. Users can now deposit SOL and receive $FUN automatically through the platform’s seamless conversion process.

The addition of SOL provides users with another convenient way to acquire $FUN without the need for manual token swaps. All supported non-$FUN deposits are automatically converted into $FUN with 0% conversion fees, creating a faster and more streamlined onboarding experience.

A Simpler Way to Access the $FUN Ecosystem

As the FUNToken ecosystem continues to grow, providing users with flexible and accessible funding options remains a key priority.

With SOL now supported, users can fund their accounts through a straightforward deposit process. Once deposited, SOL is automatically converted into $FUN, eliminating unnecessary steps while ensuring users can quickly begin exploring everything the ecosystem has to offer.

Whether users are playing $FUN Games, staking their tokens, or participating in future ecosystem features, accessing $FUN has become even more convenient.

Seamless Conversion with 0% Fees

The deposit process has been designed to be simple and efficient.

Users can now deposit SOL, with funds automatically converted into $FUN at 0% conversion fees. By removing the need for additional swaps, FUNToken continues to reduce friction and make participation in the ecosystem more accessible.

The expansion of supported deposit assets reflects FUNToken’s ongoing commitment to improving the user experience while providing more ways for the community to engage with the platform.

About FUNToken

FUNToken powers a growing Web3 gaming ecosystem designed to make digital rewards more accessible and engaging. Through $FUN Games, staking, community incentives, and an expanding range of supported deposit assets, FUNToken continues to simplify how users access the ecosystem while creating more opportunities to play, earn, and participate.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

MLB Roundup: Rays top Royals for eighth straight win

Thiel Capital’s Jack Selby nabs stakes in hot startups like Etched through Arizona connections

Chloe Bailey Addresses Criticism About Her BET Awards Look

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Sunday Morning Prayer to Break Every Financial Delay #motivation #love #faith #morningprayer

Affirmation Prayer for Unexpected Financial Blessings #affirmations #prayer #unexpectedblessings

prayer for open doors, financial breakthrough | Warfare Prayer | Kingdomite Prophetic Ministry

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Staud – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

News Videos5 days ago

News Videos5 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Tech5 days ago

Tech5 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Sports7 days ago

Sports7 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech6 days ago

Tech6 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World7 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoRTX holders must register wallets before token distribution begins

-

Business4 days ago

Business4 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Sports2 days ago

Sports2 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

-

NewsBeat3 days ago

NewsBeat3 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World1 day ago

Crypto World1 day agoBinance stock trading tops $1B in first month after launch

-

NewsBeat1 day ago

NewsBeat1 day agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Tech6 days ago

Tech6 days agoOpenAI mulls delaying IPO over valuation concerns

You must be logged in to post a comment Login