Crypto World

Ethics, DeFi, and $1.35B in yield

The most consequential crypto bill in American history missed its July 4 signing target and sits on the Senate calendar with no floor vote scheduled. The reason is not procedure. It is three specific, unresolved fights: the President’s $1.4 billion in crypto income, a developer shield that police groups call a criminal loophole, and a stablecoin-yield question worth $1.35 billion a year to Coinbase alone. The Senate returns July 13 with three weeks to settle all three. Here is each fight, both sides, and the math.

Summary

- Three unresolved disputes over ethics, DeFi developer protections, and stablecoin rewards continue to hold up the Senate vote on the CLARITY Act.

- The Senate has roughly three weeks before the August recess to secure enough bipartisan support and clear several procedural hurdles for the bill.

- The outcome could shape crypto regulation in the United States while influencing institutional adoption, DeFi rules, and stablecoin business models.

America’s 250th birthday came and went without the signing ceremony the White House had informally penciled in. The Digital Asset Market Clarity Act, the bill that would finally decide which American regulator governs which crypto asset, spent July 4 exactly where it has sat since June 1: at Calendar No. 423 on the Senate Legislative Calendar, eligible for a floor vote that nobody has scheduled, with no cloture motion filed and prediction markets pricing its 2026 passage in the low-to-mid 40s, down from 82% in February and 74% barely a month ago.

The bill is not dead, and the arithmetic explaining its paralysis is brutally simple. Republicans hold 53 seats; Senators Josh Hawley and Rand Paul are expected to vote no; passage requires 60. That means roughly seven to nine Democrats must cross over, and the two Democrats who voted for the bill in committee, Ruben Gallego and Angela Alsobrooks, have both said publicly that their committee votes do not guarantee floor votes. The missing Democratic votes exist in principle. They are being withheld in practice, over three specific and interlocking disputes, and last week, the negotiations over the first two fractured into stalemate, with Senate leaders reportedly planning emergency meetings when the chamber returns on July 13.

Roughly three usable Senate weeks remain before the August recess, the window that analysts from Galaxy to the bill’s own sponsors treat as the last realistic gate before midterm politics consumes the calendar, and Senator Cynthia Lummis has warned that failure now could push the next opening toward the end of the decade. This piece takes the three fights one at a time: what each dispute actually is, the strongest version of each side’s argument, what compromise would look like, and how each interacts with the unforgiving calendar. The bill’s 257 pages have been mapped in detail before; what follows is the narrower story of the three pages’ worth of disagreements deciding whether any of it becomes law.

Fight one: the President’s $1.4 billion

The first fight became concrete on July 1, when the Office of Government Ethics released President Trump’s 927-page financial disclosure for 2025. The filing showed approximately $1.4 billion in cryptocurrency-related income during the first year of his second term: $635 million in royalties from $TRUMP memecoin licensing, more than $500 million from World Liberty Financial token sales, and additional equity and stablecoin proceeds, the largest personal crypto-income disclosure in American presidential history.

For Democrats who had spent months demanding conflict-of-interest language in the bill, the disclosure converted an abstract principle into a billion-dollar fact. Their argument runs as follows: the CLARITY Act will decide the legal classification, and therefore the value, of the exact asset class from which the President’s family draws its largest income stream, and passing it without enforceable ethics provisions amounts to Congress legislating a benefit to the signer. Senator Kirsten Gillibrand, among the chamber’s most crypto-friendly Democrats and a co-author of earlier market-structure frameworks, has said plainly that enforceable language covering government officials’ crypto holdings is a prerequisite for her floor support, and she is the bellwether: if the bill cannot hold its friendliest Democrats, it cannot find seven.

The Republican counter-argument is constitutional and practical. Existing ethics law already prohibits members of Congress and senior executive officials from issuing digital commodities in office, the bill’s own text says so, and provisions singling out the sitting President’s personal holdings are, in the White House’s view, a poison pill dressed as principle, designed to force a veto confrontation, not to govern. The negotiating record shows both sides maneuvering around that accusation: an ethics amendment from Senator Chris Van Hollen failed 11-13 in committee; a tentative bipartisan framework reached in May collapsed last week when Republicans withdrew support for a state-attorneys-general enforcement mechanism and offered enforcement through the US Attorney General instead, an offer Democrats rejected as circular, since the Attorney General serves at the President’s pleasure; Republicans then floated impeachment as the constitutional remedy for presidential ethics violations, which Democrats declined to treat as an answer.

The shape of a landable compromise is visible in the wreckage: enforcement housed somewhere neither side controls, disclosure obligations rather than divestiture mandates, and effective dates that decouple the provisions from the current occupant. Whether it lands is another matter. The ethics fight is the only one of the three that is genuinely about the bill’s political meaning rather than its text, which is why it has attached to this bill after sparing the stablecoin law a year earlier: a market-structure act that classifies the assets a President holds cannot be framed as neutral plumbing, and everyone negotiating knows it.

Fight two: Section 604 and the developer shield

The second fight is over Section 604, which incorporates the Blockchain Regulatory Certainty Act and shields non-custodial software developers, people who write and publish code but never take custody of user funds, from money-transmitter registration and Bank Secrecy Act obligations. To the DeFi industry, it is the bill’s philosophical core; to a significant bloc of American law enforcement, it is a criminal loophole, and the split inside law enforcement itself, which this publication examined at length, has become one of the strangest subplots in crypto’s legislative history.

The opposition case is carried by the National Sheriffs’ Association, the International Association of Chiefs of Police, and the National District Attorneys’ Association, which told Senate leadership that Section 604 would materially impair criminal investigations involving cryptocurrency. Their argument: exempting DeFi software from the registration and record-keeping duties that apply to every other financial intermediary creates a compliance-free lane that launderers, sanctions evaders, and fraud networks will route through, and prosecutors will confront protocols with no registered entity to subpoena. The prosecutors’ version is the sharpest, because subpoenas are their daily tool and Section 604 is, from their desk, a list of doors the bill would weld shut.

The defense case is that the provision protects publishers, not criminals. Under the enforcement-era status quo, open-source developers faced personal liability when third parties used their code unlawfully, a standard that would be unthinkable applied to any other form of publishing, and the shield applies only where a decentralized system has no intermediary exercising control, while every custodial actor, exchange, broker, dealer, remains fully covered. The bill’s sponsors point to the sixteen-plus illicit-finance safeguards elsewhere in the text: Section 201 applying Bank Secrecy Act and anti-money-laundering duties across registered crypto intermediaries, Section 303’s new sanctions authorities aimed at Iran, Section 305’s freeze powers for dirty funds, plus $150 million in dedicated funding for crypto fraud investigations, which Lummis has framed as money to track down scammers and bad actors. The White House Crypto Council has worked the issue directly, convening the objecting groups and producing, in the National Organization of Black Law Enforcement Executives, the bill’s first major law-enforcement endorsement, its executive director citing exactly those AML, sanctions, and forfeiture provisions.

The core dispute entered the recess unresolved because it is genuinely hard: it is the same tension between publishing code and operating a financial service that runs through a decade of American crypto enforcement, now compressed into one section’s drafting. The compromise space involves narrowing the shield’s definitions, adding sunset-and-study provisions, and expanding the investigative funding, and unlike the ethics fight, this one is tractable, because both sides ultimately want the same headline, a bill that is tough on crime, and are arguing over mechanism rather than meaning.

Fight three: the $1.35 billion yield question

The third fight is the quietest and involves the most measurable money. It concerns whether digital-asset platforms can keep paying customers rewards on stablecoin holdings, a question the GENIUS Act, the stablecoin law enacted a year ago, answered incompletely: it prohibited issuers from paying interest on payment stablecoins but left open whether platforms distributing those stablecoins can pass through yield.

Coinbase earns approximately $1.35 billion annually in USDC rewards revenue through exactly that arrangement, and whether the arrangement survives depends on drafting choices inside CLARITY.

The banking industry’s argument, pressed by the American Bankers Association and voiced most bluntly by JPMorgan’s Jamie Dimon, who said banks will fight the bill, is that the pass-through is a loophole that lets crypto platforms offer interest-bearing, deposit-like products without the capital, insurance, and anti-money-laundering obligations that make bank deposits safe, and that at scale it becomes a deposit-drain from the regulated banking system, the same systemic worry that shaped the trillion-dollar stablecoin fight this spring.

The crypto industry’s counter is that rewards programs are marketing expenditure paid from a distributor’s own revenue, not issuer interest; that Congress already drew the line at issuers in GENIUS and re-litigating it through CLARITY is the banking lobby’s second bite; and that killing pass-through yield would simply push American stablecoin users toward offshore products that answer to no US regulator at all.

The January Senate Banking draft tried to split the difference, prohibiting yield for merely holding balances while permitting activity-linked rewards, and the final text’s placement of that line is worth, to a single company, more than a billion dollars a year, which guarantees the lobbying around it will continue to the last markup.

The gauntlet in detail: how three weeks actually get spent

The phrase floor vote compresses a procedural sequence that deserves unpacking, because the calendar risk is not one deadline but a chain of them, and each link consumes days the bill does not have to spare.

Start with what calendar placement did and did not do. Being reported to the Senate Legislative Calendar as No. 423 on June 1 made the bill eligible for floor consideration; it scheduled nothing. Majority Leader John Thune controls the floor, and his queue when the chamber returns on July 13 begins with the National Defense Authorization Act, the annual must-pass defense bill that reliably devours a week or more, alongside a FISA Section 702 reauthorization with its own hard deadline.

Only after leadership commits floor time does CLARITY’s own sequence begin: a cloture motion on the motion to proceed, an intervening day, a sixty-vote cloture roll call, up to thirty hours of post-cloture debate, then the same cycle again on the bill itself, with an amendment process in between whose scope is itself a negotiation. Run cleanly and consensually, the sequence takes the better part of a week; run under objection, it can take two, and the recess begins in roughly three.

Then come the gates the headlines forget. The Banking Committee text that sits on the calendar must be reconciled with the Senate Agriculture Committee’s companion measure, the Digital Commodity Intermediaries Act, because the CFTC falls under Agriculture’s jurisdiction and both committees claim pieces of the framework; that merger has been negotiated in parallel but is not complete. Whatever passes the Senate must then be squared with the House-passed version from July 2025, either through a formal conference or through the House swallowing the Senate text whole, and House Financial Services has its own scheduled activity on July 17 that signals it does not regard itself as a rubber stamp.

The GENIUS Act’s own rulemaking deadline of July 18, one year from signature, lands in the same week the Senate resumes, crowding the agencies and the committee staff who service both laws. Every one of these steps is routine in isolation; stacked inside three weeks against two competing must-pass bills, they are the reason seasoned handicappers quote coin-flip odds for a bill with majority support.

The paradox of the moment is that the deadline is also the bill’s best friend, and its sponsors know it. Lummis has been explicit about moving in July, negotiators circulated final compromise text for review around the recess, and the a16z argument, that nothing concentrates Senate minds like a closing window, has real precedent in how the stablecoin law crossed its own finish line a year ago. Both dynamics are true at once: the calendar makes passage physically difficult, and the calendar is the only force capable of converting fourteen months of almost-agreements into signatures.

The next three weeks will show which effect is stronger, and observers who want to track it in real time need exactly four tells: whether Thune files cloture in the week of July 13, whether Gillibrand’s public posture on the ethics language shifts, whether the White House Crypto Council produces a Section 604 accommodation the sheriffs accept, and whether the Agriculture merger text appears. Any three of the four pointing the same direction will settle the question before the roll is ever called.

What each outcome is worth, asset by asset

The three fights are Washington stories, and the reason markets refresh the Senate calendar is that each outcome carries a price map that analysts have, unusually, been willing to publish in advance.

The passage scenario has explicit numbers attached. Citi’s Bitcoin target of $143,000 and Standard Chartered’s $150,000 are both conditioned on the bill becoming law, with regulatory certainty cited as the unlock for the next institutional wave into spot ETFs and corporate treasuries. Ethereum’s conditional upside is structural: commodity classification supplies the legal foundation for the staking ETF products allocators have drafted but not filed, behind Standard Chartered’s conditional $7,500 end-of-year target.

XRP carries the most direct exposure of any major asset, because the SEC-CFTC joint classification of it as a digital commodity in March 2026 is an interpretive ruling a future administration could reverse, and CLARITY would convert it into statute; JPMorgan and Standard Chartered have each projected $4 to $8.4 billion of first-year XRP ETF inflows under passage, roughly five times the products’ entire cumulative haul to date, arriving into a tradable float already at seven-year lows. The May 14 committee vote provided a small-scale preview, lifting the majors within hours on nothing more than procedural progress.

The failure scenario is not symmetrical, and that asymmetry is underpriced in casual commentary. A stall past the August recess does not merely delay the upside; it re-exposes every interpretive gain of the past two years to reversal risk, keeps the pension funds and sovereign allocators that legally cannot touch unclassified assets on the sidelines indefinitely, and, per Lummis’s warning, potentially pushes the next legislative window toward 2030 as midterms and a new Congress reshuffle every committee.

It would also leave the DeFi developer question exactly where the enforcement era left it, with builders facing liability standards no other publishing industry tolerates, and hand the competitive initiative back to the jurisdictions that already have live rulebooks, the MiCA-led regimes whose contrast with the American approach has defined the global regulatory race. Failure, in short, is not the status quo; it is the status quo minus the assumption of imminent rescue that has supported valuations all year.

Between the binary outcomes sits the muddled middle the market currently prices: passage in the fall, or passage in 2027, or a slimmed bill that resolves two fights by amputating the third. Each middle path has its own distributional consequences. An ethics compromise that survives conference likely costs nothing to asset prices and buys the signatures; a Section 604 narrowed to appease the sheriffs shifts value from DeFi-adjacent tokens toward the centralized incumbents the bill would license; a yield provision drawn the banks’ way removes a billion-dollar revenue line from the largest American exchange and, by extension, from the equity that trades on it.

The bill is routinely described as crypto versus Washington, and the truer description is that it is a set of allocations among crypto’s own factions, which is exactly why the industry coalition holding together through fourteen months of markups has been the quiet achievement underneath everything else.

Three weeks, three fights, one calendar

What makes the three fights decisive is not their difficulty individually but their interaction with a calendar that has no slack. When the Senate returns July 13, floor time must first accommodate the National Defense Authorization Act and a FISA Section 702 reauthorization, and each cloture sequence on CLARITY, one on the motion to proceed, one on the bill, can consume most of a week. Behind Senate passage wait two more gates the headlines forget: reconciling the Banking Committee text with the Senate Agriculture Committee’s companion measure, and squaring the result with the House-passed version, before any signature. Galaxy Research puts 2026 passage near a coin flip; Polymarket has drifted through the 40s; the bill’s supporters, from SEC Commissioner Hester Peirce’s summer-passage expectation to a16z’s argument that the tight window itself forces compromise, are betting that deadline pressure does what fourteen months of negotiation has not.

The honest reading of the moment is that the CLARITY Act has already survived everything except its final and most political mile. It passed the House 294-134 with 78 Democrats, cleared committee 15-9, and carries an industry coalition that has held together through every markup, achievements no market-structure bill has matched. The three fights blocking it are not procedural noise; each is a real dispute about who bears risk in the new system, the public against a President’s conflicts, investigators against anonymous code, banks against their own depositors’ yield-seeking.

Whichever way each resolves, the resolutions will be read as precedent for a decade of digital-asset law. Three weeks is enough time to settle three fights, and it is also enough time to settle none of them, and as of the morning the Senate returns, the smart money is split almost exactly down the middle.

It is worth naming, finally, what the three fights have in common, because the pattern explains why this bill has been harder than its stablecoin predecessor and why its resolution will echo past crypto. Each fight is a dispute about whether the new legal order will contain an exemption, for a President’s holdings from ethics enforcement, for published code from intermediary regulation, for platform rewards from banking rules, and exemptions are where legislation does its real distributional work.

The stablecoin law passed easily because it created obligations nearly everyone could live with; CLARITY has stalled because it creates carve-outs that someone powerful, in each case, cannot. That is not a sign the bill is badly drafted. It is a sign the bill matters, that it touches money and power at the joints where they actually connect, and the fourteen months of grinding negotiation are the ordinary price of legislation that does.

The Senate’s three weeks will be covered as drama, and most of the drama will be noise; the four tells listed above, cloture filed, Gillibrand moved, the sheriffs accommodated, the Agriculture merger published, are the signal, and readers who track those four and ignore the rest will know the outcome before the vote count does.

Whatever happens by August 10, the American crypto industry will exit this window with something it has never had before: a precise, public record of exactly which three questions its legal future turned on, and exactly who answered them.

A brief word on how to consume the next three weeks of coverage. Legislative endgames generate a distinctive noise signature: anonymous optimism from offices with bills to sell, anonymous pessimism from offices with amendments to extract, and daily prediction-market swings that mostly recycle both. The durable information will arrive in exactly four formats, a cloture filing on the Senate calendar, a named senator changing a stated position on the record, published compromise text, and committee-merger documents, and each is a public artifact that cannot be spun. Everything else, including the confident threads that will flood social feeds every evening the Senate is in session, is atmosphere. The bill’s fate is a matter of four documents and seven signatures, and the discipline of watching only those is the closest thing this story offers to an edge.

One historical footnote gives the moment its proper weight. No comprehensive American market-structure law for a new asset class has passed on its first serious Senate attempt; the securities acts of the 1930s, the commodity-futures framework, and the derivatives titles of the post-crisis reforms each required a failed run or a crisis, usually both, before enactment. CLARITY arriving at the floor with a House supermajority behind it, an industry coalition intact, and no crisis forcing anyone’s hand is already outside the historical pattern, which is one reason experienced hands hold their forecasts loosely in both directions. If it passes, it will have beaten the base rate for laws of its kind. If it fails, the two-year record it leaves, votes counted, compromises drafted, objections named, becomes the starting text of the next attempt, which is more than any previous crypto Congress has left behind.

Disclaimer: This article is for informational purposes only and does not constitute investment or legal advice. Legislative details are current as of July 8, 2026, and are changing rapidly; verify the current status before relying on any timeline described here.

Key takeaways

- Arbitrum (ARB) rebounded above $0.081 after recovering losses from earlier in the week.

- Offchain Labs co-founder Steven Goldfeder announced that 10% of fees generated by Robinhood Chain and other Arbitrum Layer 2 networks will flow back into the Arbitrum ecosystem.

- The revenue-sharing model is expected to strengthen the DAO treasury, fund development, and enhance ARB’s long-term value.

Arbitrum (ARB) extended its recovery on Thursday, climbing above $0.081 after erasing losses recorded earlier in the week.

The rally followed a major announcement from Offchain Labs co-founder Steven Goldfeder, who revealed that a portion of transaction fees generated by Robinhood Chain and other Arbitrum Layer 2 (L2) networks will be redirected to the broader Arbitrum ecosystem.

The announcement has boosted investor confidence by highlighting a sustainable revenue model that could strengthen the network’s long-term fundamentals, while improving technical indicators suggest ARB may have room for further gains.

Robinhood Chain revenue-sharing strengthens Arbitrum ecosystem

In a post on X, Offchain Labs co-founder and Arbitrum developer Steven Goldfeder disclosed that 10% of fees collected by Robinhood Chain and every other Arbitrum Layer 2 chain are allocated back to the Arbitrum ecosystem.

As enterprise adoption is heating up, Arbitrum is well positioned to capture revenue.

10% of fees collected on Robinhood Chain (and every other Arbitrum L2) go to the Arbitrum ecosystem — 8% to the tokenholder controlled treasury and 2% to fund development.

And of course 100%…

— Steven Goldfeder (@sgoldfed) July 8, 2026

According to Goldfeder, 8% of those fees are directed to the tokenholder-controlled Arbitrum DAO treasury, while the remaining 2% is used to support ongoing network development.

He also noted that 100% of fees generated on Arbitrum One continue to flow directly into the Arbitrum treasury, further reinforcing the ecosystem’s long-term funding model.

The fee-sharing mechanism is viewed as a positive development for Arbitrum because it creates an ongoing source of revenue for governance, ecosystem expansion, and developer incentives. As enterprise adoption of Layer 2 networks accelerates, the model could significantly increase the value captured by the Arbitrum ecosystem over time.

Investors responded positively to the announcement, sending ARB more than 7% higher during Thursday’s trading session.

Technical outlook improves, but key resistance remains

ARB has recovered above $0.085, reversing the losses recorded over the previous three sessions.

However, the token still trades below several important moving averages, suggesting the broader trend has yet to turn decisively bullish.

The 200-day Exponential Moving Average (EMA) remains well above the current price at $0.1409, underscoring the longer-term bearish structure.

Meanwhile, momentum indicators are beginning to stabilize. The Moving Average Convergence Divergence (MACD) is showing signs of improving momentum, while the Relative Strength Index (RSI) is hovering near 50, indicating that selling pressure is easing without confirming a full bullish reversal.

The first major resistance zone sits between $0.0878 and $0.0891, where several technical barriers converge.

This area includes the 50-day EMA at $0.0878, a horizontal resistance level at $0.0883, and the 23.6% Fibonacci retracement level at $0.0891.

A successful breakout above this cluster could shift momentum further in favor of buyers and open the path toward the next resistance levels.

On the downside, the key support remains around $0.0705, which marks both the previous swing low and the primary Fibonacci support level.

Holding above this area would preserve the recent recovery. However, a daily close below $0.0705 could invalidate the current rebound and expose ARB to another leg lower despite improving momentum indicators.

For now, traders will be watching whether growing ecosystem revenues and stronger investor sentiment can help ARB break above the critical $0.09 resistance zone and build a more sustained recovery.

For years, decentralized finance (DeFi) has relied on a familiar playbook: launch a governance token, distribute generous rewards to liquidity providers, and watch capital pour in. The strategy fueled the explosive growth of DeFi during the 2020-2022 boom, creating billions of dollars in Total Value Locked (TVL) almost overnight.

But there was one major problem.

Much of that liquidity wasn’t loyal—it was rented.

As soon as rewards declined or another protocol offered higher yields, capital quickly migrated elsewhere. This phenomenon, often called “mercenary capital,” exposed a harsh reality: many DeFi protocols weren’t attracting users because of their products—they were attracting them by paying them.

Now, as the industry matures, a new question is taking center stage:

Can DeFi survive without token incentives?

The answer could determine which protocols become lasting financial infrastructure—and which fade away when emissions dry up.

The Emissions Era

Liquidity mining changed crypto forever.

Protocols like Compound, Aave, SushiSwap, Curve, and dozens of others rewarded users with newly minted governance tokens simply for supplying liquidity or borrowing assets.

The model worked because:

- TVL increased rapidly.

- Higher TVL attracted more users.

- More users increased visibility.

- Token prices often appreciate.

- Everyone appeared to win.

But underneath the surface, the economy was fragile.

Every reward distributed represented dilution.

Unless a protocol generated enough revenue to offset emissions, value slowly leaked from existing token holders to short-term farmers.

Eventually, many protocols entered a familiar cycle:

High APY → Liquidity Flood → Rewards End → Liquidity Leaves.

This became one of DeFi’s biggest structural weaknesses.

Liquidity Is Not Product-Market Fit

One of crypto’s biggest misconceptions is equating TVL with success.

A protocol can have billions locked while generating very little real economic activity.

Conversely, a protocol with modest TVL but strong revenue may have a healthier long-term business model.

True product-market fit means users stay because the protocol solves a real problem—not because they’re temporarily subsidized.

Examples include:

- Traders seeking the best execution.

- Businesses need stablecoin liquidity.

- Institutions require transparent settlement.

- Developers are integrating reliable infrastructure.

- Users pay for convenience, security, or privacy.

In these cases, demand exists independently of token rewards.

That’s a much stronger foundation.

Revenue Is Becoming More Important Than Emissions

Increasingly, investors are evaluating protocols less by TVL and more by revenue generation.

Questions are shifting toward:

- Does the protocol generate sustainable fees?

- Are users willing to pay for the product?

- Can revenue cover operational costs?

- Is token value linked to real cash flow?

These metrics resemble traditional business analysis more than speculative token investing.

The market is slowly rewarding protocols that operate like businesses rather than perpetual incentive machines.

Protocols Built Around Real Demand

Several categories of DeFi already demonstrate that sustainable demand can exist without relying entirely on emissions.

Decentralized Exchanges

Users trade because they need liquidity.

Trading fees—not inflation—become the primary economic engine.

Higher trading volume naturally increases protocol revenue.

Lending Markets

Borrowers care about capital access.

Lenders care about stable returns.

Neither necessarily depends on governance token rewards if interest rates remain competitive.

Stablecoin Infrastructure

Payments, settlements, payroll, and treasury management create recurring demand.

These activities happen because they’re useful—not because someone is farming incentives.

Cross-Chain Infrastructure

Bridges, interoperability layers, and messaging protocols generate demand whenever users move assets across ecosystems.

The service itself provides value.

Privacy Infrastructure

Privacy-focused protocols solve real user needs, including financial confidentiality, business privacy, and secure transactions.

As regulatory frameworks evolve, privacy solutions with legitimate compliance features may see increasing demand from both individuals and institutions.

The Difference Between Subsidized Growth and Organic Growth

Imagine opening two coffee shops.

The first gives every customer $20 just for walking in.

The second simply serves excellent coffee.

Initially, the first shop will appear far busier.

But once the giveaways stop, many customers disappear.

The second shop may grow more slowly, but its customers return because they genuinely value the product.

Many DeFi protocols have resembled the first coffee shop.

The next generation aims to become the second.

Organic demand compounds over time.

Subsidized demand disappears when the subsidies end.

Incentives Are Not the Enemy

This doesn’t mean token incentives are inherently bad.

Incentives can be extremely effective when used strategically.

They can:

- Bootstrap early liquidity.

- Reward long-term contributors.

- Encourage ecosystem development.

- Align community participation.

The problem arises when incentives become the product rather than supporting it.

Healthy protocols eventually reduce dependence on emissions as natural demand grows.

The Next Competitive Advantage

As DeFi becomes more efficient, protocols may increasingly compete on:

- Better user experience

- Lower transaction costs

- Faster execution

- Higher security

- Regulatory readiness

- Reliable revenue generation

- Strong developer ecosystems

These are advantages that cannot be easily copied by simply increasing APYs.

A More Sustainable Future

The industry’s focus is gradually shifting from “How high is the yield?” to “Where does the yield actually come from?”

That’s an important evolution.

Protocols that earn revenue through genuine usage are more likely to weather bear markets, attract institutional participants, and build durable ecosystems.

Liquidity earned through utility tends to last longer than liquidity rented through emissions.

Final Introspections

Token incentives played a critical role in bootstrapping DeFi, helping transform a niche experiment into a global financial ecosystem. However, long-term sustainability will depend less on how many tokens a protocol distributes and more on whether people genuinely need the services it provides.

The next generation of DeFi winners may not be the protocols offering the highest APYs—they may be the ones delivering products users are willing to pay for, even when rewards disappear.

In the end, sustainable finance isn’t built on endless emissions. It’s built on creating real value that keeps users coming back long after the incentives are gone.

REQUEST AN ARTICLE

Peter Schiff used his podcast this week to argue that BTC holders are ignoring what Strategy’s decision to sell some of its stack means for the asset.

According to him, the company built by Michael Saylor was the real floor under Bitcoin’s price, and that floor is now gone.

Schiff Says Strategy’s Selling Exposes the Real Backbone of Crypto

In the hour-long episode aired on YouTube on July 9 and covering everything from the reported collapse of the Iran peace deal to the DOGE shutdown, Schiff claimed that Bitcoin supporters were being willfully blind to Strategy’s changing role in the market. According to him, the firm’s buying had become a major source of demand that helped support BTC’s price.

“Bitcoiners are delusional right now, or in denial about what’s happening with Strategy,” he said. “They do not understand how important Strategy has been to Bitcoin, to the whole ecosystem, the whole industry, because it has provided all of that buying that not only put a floor beneath Bitcoin and kept it going up, but legitimized it in the eyes of the financial community.”

However, that dynamic, in Schiff’s opinion, has now changed after the company recently sold 3,588 BTC for some $216 million instead of adding to its holdings. Furthermore, the economist noted that Strategy disposed of the stash at an average price of about $60,000 after buying them for roughly $75,000, meaning it had booked a loss of around $15,000 on each of them.

The issue, though, isn’t even the “huge loss,” as Schiff put it, that Saylor suffered from the sale, but rather the mental effect that selling will have on the community.

“It’s not just that he’s not buying or that he’s selling; it’s the psychology,” he insisted.

The crypto critic then suggested that Saylor will sell a lot more of Strategy’s Bitcoin, possibly all of it at some point, to “lower his exposure to raise his cash so he can keep on paying the dividends.”

He also flagged the company’s preferred shares, which were trading around $86 despite a dividend hike to 12%, as a sign that investors no longer had confidence in BTC.

“The game is over, and the market is telling you that the confidence is not there anymore,” Schiff told listeners. “All the hype didn’t pan out, or whatever had panned out has already panned, and now it’s just about the last man out.”

Other Analysts Are Reading the Same Sale Very Differently

Not everyone sees Strategy’s decision to sell as bearish. For example, Zach Pandl, Grayscale’s head of research, recently argued that the sale could restore confidence in the firm’s financing structure instead of damaging BTC’s long-term outlook.

He noted that Strategy still owned $53 billion in Bitcoin against a $7 billion debt, while its cash reserves have increased to around $2.55 billion, which is enough to cover 17 months of dividend payments.

Another industry observer, HashKey Group Senior Researcher Tim Sun, made a similar point, telling CryptoPotato that a slower Strategy could actually help Bitcoin build a healthier price floor based on organic demand instead of financing-driven buying.

Meanwhile, Bitwise’s Matt Hougan expects Strategy to matter less as a buyer in the next cycle, with institutions like Morgan Stanley and Wells Fargo potentially taking over as the OG cryptocurrency’s main source of demand.

The post Peter Schiff: Bitcoiners Are In Denial About Strategy’s BTC Sale appeared first on CryptoPotato.

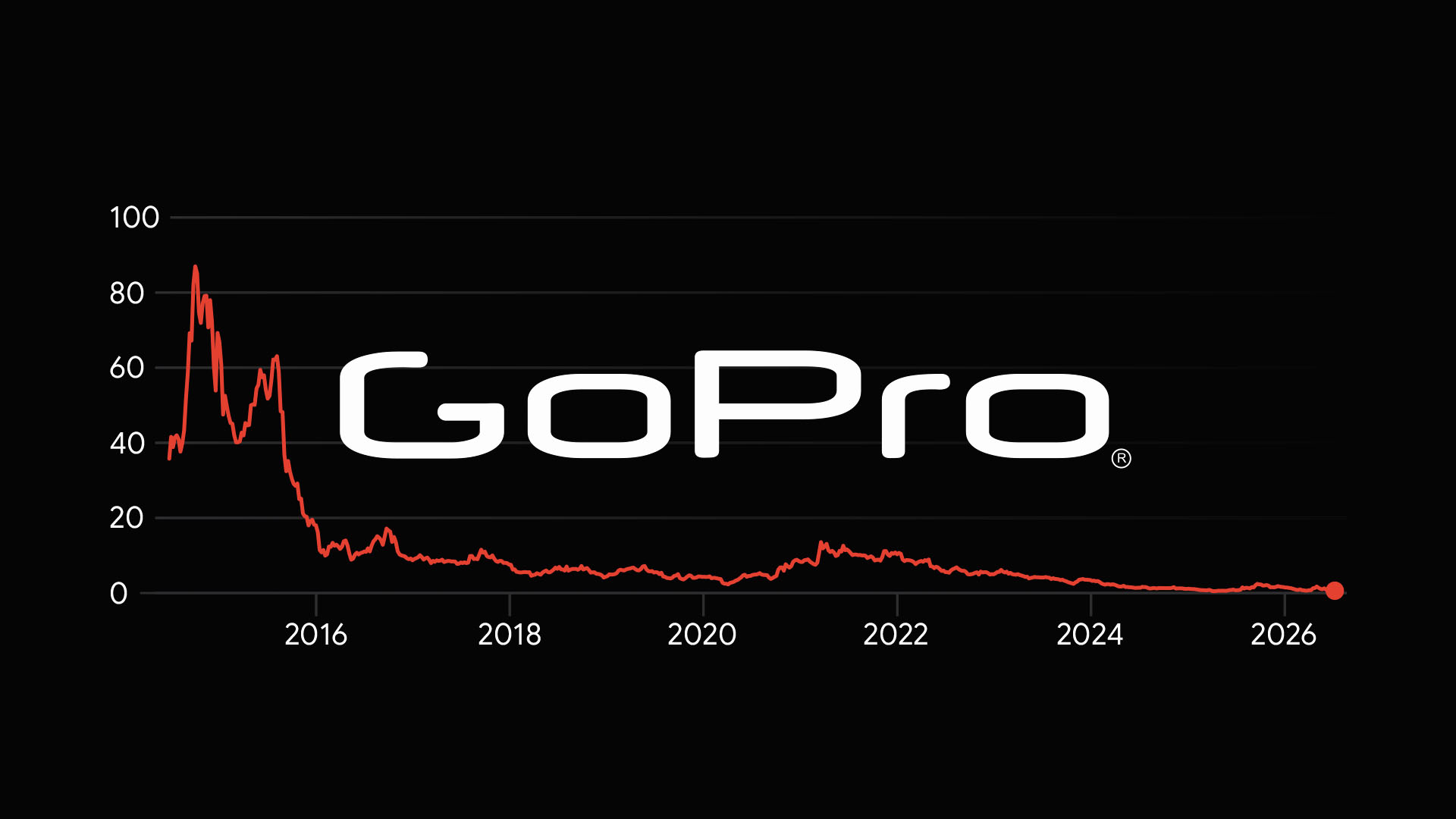

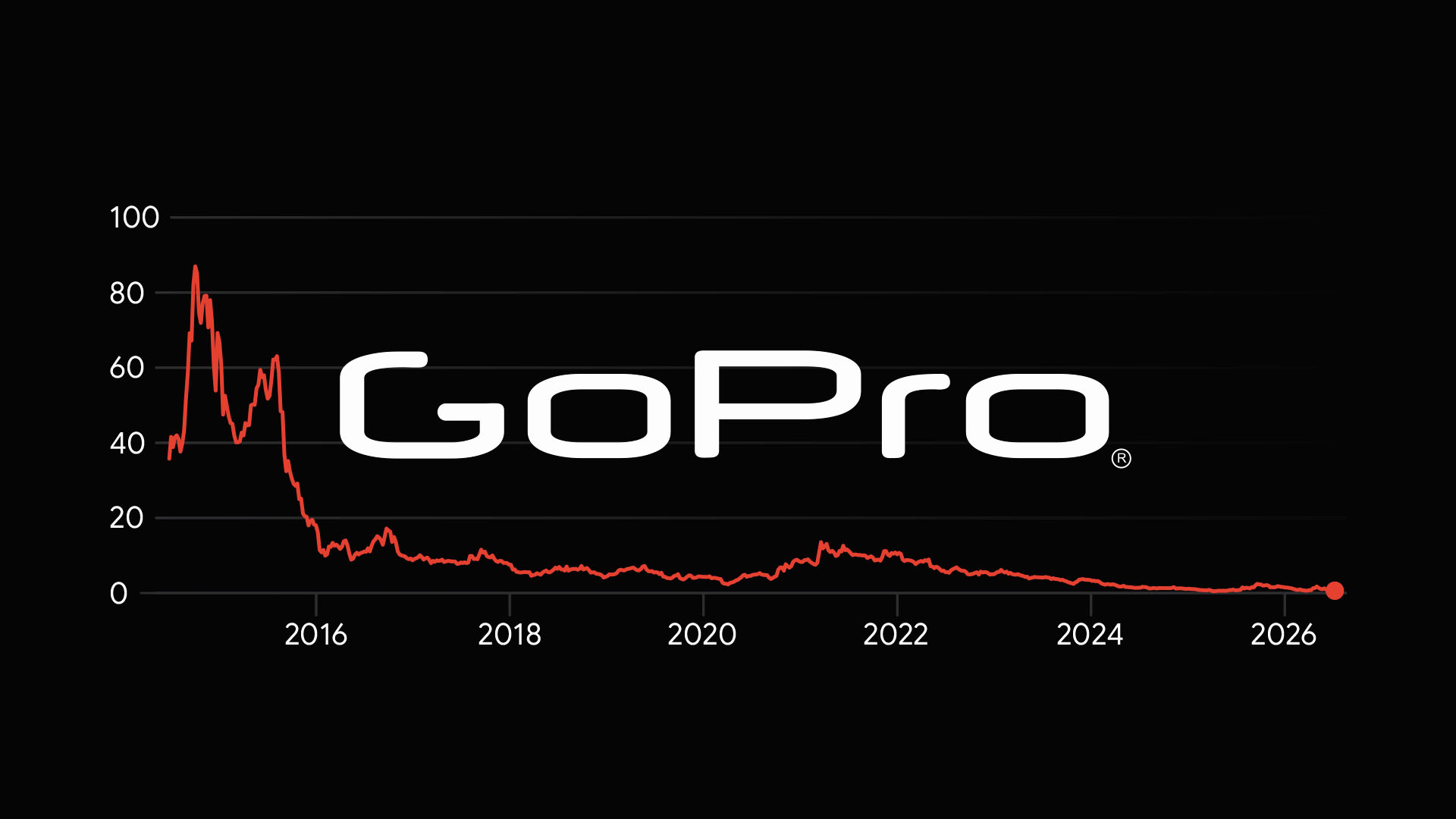

GoPro, the action camera maker once worth more than $10 billion, just announced that founder Nicholas Woodman will extend $20 million in financing to keep his company afloat.

That’s the Nicholas Woodman who previously made over $284 million in a single 12-month span, making him the highest paid chief executive in the US that year.

Still a billionaire today, thanks to years of GoPro stock and compensation, Woodman is slowly becoming its lender of last resort.

As a condolence for presiding over a 99% stock decline from the company’s peak, he’s returning a fraction of the fortune he made to keep things running.

Through entities affiliated with Woodman, he’s agreed to hold $20 million in senior secured notes plus warrants to purchase Class B shares, the class that already gives him majority voting control.

Woodman framed it as a vote of confidence. “My financing reflects my enthusiasm for GoPro and its several go-forward opportunities,” he said in the announcement, adding that an independent board committee had reviewed a range of financing options and concluded the structure offered the most favorable terms for GoPro and its shareholders.

GoPro was trading above $98 per share on October 7, 2014. It closed yesterday at $0.73, a decline of 99%.

From highest-paid CEO to lender of last resort

Even by 2014 standards, Woodman’s executive compensation package was extraordinary.

Woodman received 4.5 million restricted stock units three weeks before GoPro’s June 2014 initial public offering (IPO), a grant worth $284 million by the end of that year and enough for him to rank #1 on Bloomberg’s Pay Index.

His personal fortune tracked the hype for affordable cameras for sports and outdoor content creators, peaking near $3.9 billion per the 2014 edition of the Forbes 400.

The delta between then and now, however, defines that story.

GoPro shareholders made Woodman a billionaire. Now, those same shareholders are relying on him to fund operations.

By 2018, GoPro had already cut Woodman’s salary to $1. The gesture was supposed to look humble and sacrificial, except for people who remembered that his GoPro stock and compensation would keep him a billionaire.

Read more: This penny stock pivoted to Solana and Hyperliquid and lost 99.9%

Declining numbers and a bailout

GoPro stock is down roughly 48% year-to-date and more than 93% over the past five years. The company’s market cap is now approximately $123 million or less than a single year of Woodman’s peak executive compensation.

Revenue has also declined by from $1.6 billion in 2015 to roughly $650 million in 2025.

GoPro earned $128 million in 2014. After years of losses, its shareholder equity had turned negative by the first quarter of 2026.

The rescue attempts kept coming. The company borrowed $50 million from Farallon Capital Management in August 2025, then Woodman’s family trust bought $2 million of stock in November.

In May 2026, the board launched a review of strategic alternatives. By June 2026, an SEC filing carried a going-concern warning.

Woodman’s $20 million is the latest patch, and this time the capital comes directly from the founder.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Key takeaways

- Hyperliquid (HYPE) has fallen for four straight days as retail demand weakens amid broader crypto market uncertainty.

- Futures open interest and trading volume have declined, signaling lower speculative activity.

- Institutional interest remains strong, with HYPE ETFs attracting $16.08 million in weekly inflows.

Hyperliquid (HYPE) remains under pressure for the fourth consecutive trading session as retail traders reduce exposure amid growing geopolitical uncertainty and a broader risk-off mood across the cryptocurrency market.

While short-term sentiment has cooled, institutional investors continue to accumulate exposure, and activity within Hyperliquid’s Real World Asset (RWA) ecosystem remains robust. These factors continue to support the token’s longer-term bullish outlook.

Technical indicators also suggest that a decisive breakout above the $75-$77 resistance area could reignite buying momentum and potentially push HYPE toward the psychological $100 level.

Retail traders step back as market sentiment weakens

Retail participation in Hyperliquid has softened as investors become increasingly cautious amid renewed tensions in the Middle East, which have dampened appetite for risk assets.

According to CoinGlass data, HYPE futures open interest declined to $2.68 billion, indicating a modest reduction in leveraged positions.

Meanwhile, derivatives trading volume dropped 29% over the past 24 hours to $1.99 billion, highlighting weaker short-term market participation.

Despite the slowdown, bullish positioning has not disappeared entirely. The funding rate eased slightly to 0.0065% from 0.0078% a day earlier, remaining in positive territory.

Positive funding rates generally indicate that long-position holders are still willing to pay a premium, suggesting optimism persists despite the recent pullback.

Overall, derivatives data points to a cautious market where traders are waiting for greater clarity before making aggressive directional bets.

While retail demand has cooled, institutional investors continue to show confidence in Hyperliquid.

HYPE-focused exchange-traded funds (ETFs) attracted $3.33 million in fresh inflows on Wednesday, bringing total weekly inflows to $16.08 million.

The steady capital inflows suggest larger investors remain optimistic about the project’s long-term growth prospects.

At the same time, Hyperliquid’s HIP-3 ecosystem—which supports perpetual contracts tied to tokenized Real World Assets (RWAs)—continues to gain momentum.

Open interest across HIP-3 products climbed to $3.10 billion, while trading volume increased 40% over the past 24 hours and 28% over the past month.

Revenue has also remained stable at roughly $10 million over the past four weeks, reflecting sustained user activity and growing demand for RWA-based trading products.

These metrics reinforce the view that institutional adoption and expanding utility remain key drivers behind Hyperliquid’s long-term bullish narrative.

Technical analysis: $75-$77 remains the key breakout zone

From a technical standpoint, Hyperliquid is undergoing a healthy correction while preserving its broader uptrend.

The token is approaching a rising support trendline near $66.54, an area that continues to underpin the current market structure.

More importantly, HYPE remains comfortably above both its 50-day Exponential Moving Average (EMA) at $62.53 and the 200-day Exponential Moving Average (EMA) at $48.33.

Holding above these major moving averages indicates that buyers still maintain control of the longer-term trend.

The primary resistance lies between $75.76—the June 1 swing high—and the R1 Pivot level at $77.09. Together, these levels form the upper boundary of an ascending triangle, a chart pattern that often precedes bullish breakouts.

A successful move above this resistance zone could open the door to the next upside targets: R2 Pivot at $89.14, and the R3 Pivot: $101.35

If bullish momentum accelerates, the psychological $100 level could become a realistic near-term objective.

Technical momentum indicators continue to favor the bulls despite the recent correction. The Moving Average Convergence Divergence (MACD) remains above its signal line, indicating that bullish momentum has not been fully lost.

Meanwhile, the Relative Strength Index (RSI) sits around 42, just below the neutral zone. This suggests there is still room for additional upside if buying pressure returns.

Together, these indicators reflect neutral-to-positive momentum rather than a shift toward a bearish trend.

Although the broader outlook remains constructive, traders should monitor downside support levels closely.

If HYPE loses the 50-day EMA at $62.53, sellers could push prices toward the S1 Pivot level at $52.83.

A deeper correction could eventually test the 200-day EMA at $48.33, which continues to represent the foundation of Hyperliquid’s longer-term bullish market structure.

As long as HYPE remains above these critical support levels, the broader uptrend remains intact despite ongoing short-term volatility.

Crude oil price has jumped back to $74 a barrel after a fragile Iran ceasefire collapsed this week. Fresh tanker attacks near the Strait of Hormuz revived fears over the world’s most important oil chokepoint, and crude oil prices spiked in response.

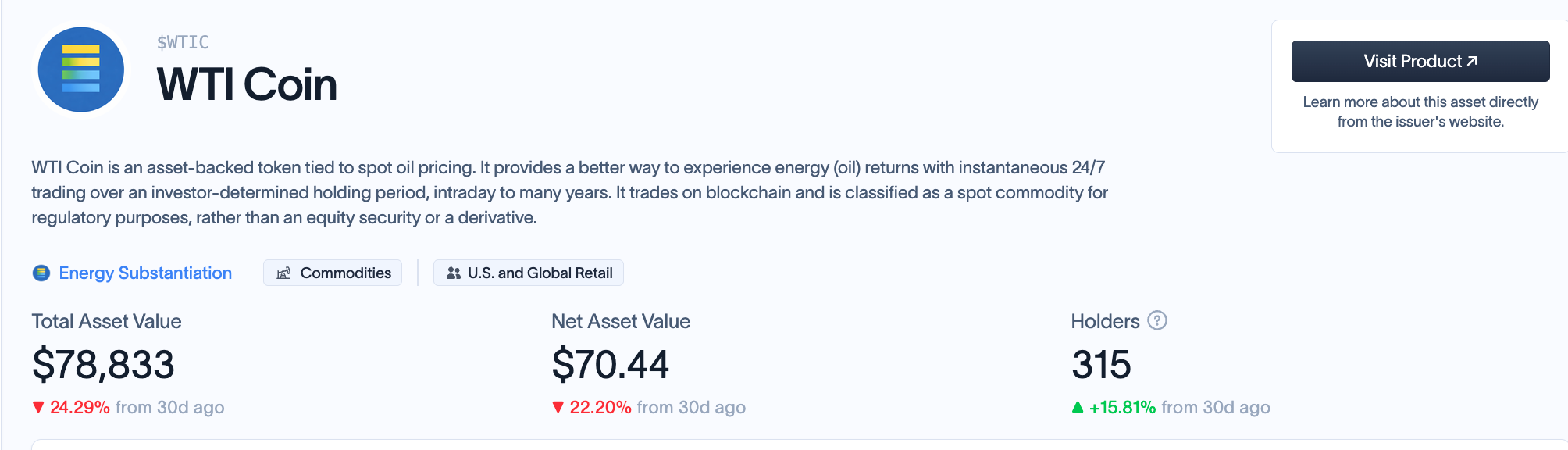

But the bounce did not catch everyone off guard. The last trading data before the truce broke shows big players were already betting on higher prices. A tiny corner of the crypto market, courtesy of the WTI Coin flashed the same signal.

Big Traders Were Buying the Oil Price Dip

The futures market may have called the move first. Each week, a US regulator publishes the Commitments of Traders (COT) report, which shows who holds oil futures and on which side.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

As of June 30, oil was still sliding toward $68 on fears of a supply glut. Yet large speculators added 1,722 long contracts and cut 1,020 shorts that week, lifting their net long above 23,700.

Meanwhile, total open interest rose by 3,568 contracts to 222,308. Rising bets into a falling price mean fresh money was moving in, not rushing out.

Small traders (the non-reportable lot) did the opposite. They added 5,490 short contracts against just 1,053 longs, a one-sided bet the rebound days later punished.

A Tokenized Barrel Sent the Same Message

The same conviction showed up on-chain, in a corner almost nobody watches. On-chain oil now trades in two very different ways, one huge and one tiny.

The huge one is a Hyperliquid perpetual contract, a pure price bet settled in stablecoins with no oil behind it, not actually backed. It clears more than $1 billion on busy days, at times trading second only to Bitcoin.

The tiny one is WTIC, a token backed by a real, redeemable barrel of oil. It holds just $79,000 in value, yet it is the only backed oil token tracked by data site rwa.xyz.

That gap is its own story. But the backed token matters here for one reason, because it is public and trades 24/7, so anyone can watch its buyers move.

Small Buyers Bought the Same Dip

In June, those buyers moved just like the futures giants. As crude slid, WTIC’s holder count jumped from 27 to 267 in five days.

In other words, the small on-chain buyers and the large speculators in the COT report leaned long into the very same sell-off. Both were buying while prices fell.

The tape then flashed one last clue. A single $367,000 transfer hit on July 3, the largest in months, before flows went quiet over the July 4 holiday.

Both signals had turned bullish. Days later, the trigger arrived, the US-Iran escalation.

What Happens Next for WTI Crude Oil Prices

That trigger was the ceasefire falling apart. On July 7 and 8, tanker attacks and US strikes hit near the Strait of Hormuz, and Washington reimposed sanctions it had eased under a 60-day oil license.

WTI crude oil ripped from about $68 to $74, and on-chain flows woke up alongside it. Both the futures longs and the tokenized-oil buyers had guessed right.

Still, the on-chain signal comes with warnings. WTIC is tiny, one wallet holds most of the supply, and it is not regulated, so treat it as an early clue, not proof.

For now, the Strait of Hormuz is the switch for oil prices. More attacks could push crude toward its war-premium highs near $100, while a lasting ceasefire would drag it lower.

The post Crude Oil Jumped to $74, and a Tiny Crypto Token Saw It Coming appeared first on BeInCrypto.

Singapore’s state-owned investment firm, Temasek Holdings, said it will prioritize AI investments over crypto due to regulatory uncertainty and the lingering impact of a $275 million write-off from the collapse of crypto exchange FTX in 2022.

The firm, with an investment portfolio valued around 518 billion Singapore dollars ($400 billion), plans to increase its AI exposure from 6% of its portfolio in the first quarter of 2026 to 15% by 2031, Nagi Hamiyeh, president of Temasek Global Investments, told CNBC on Wednesday The AI investment cycle has just begun and will continue for decades, he said, while cautioning that valuations in some parts of the industry have run ahead of fundamentals.

Temasek, the state’s largest investment vehicle after GIC Private Ltd., is still dealing with the hit it took following the collapse of FTX. That implosion and other failures exposed weak consumer protections in Singapore, prompting the central bank, the Monetary Authority (MAS), to swing toward stricter supervision, a move that resulted in higher compliance costs and slower licensing, among other challenges.

Brazil’s B3 stock exchange has unveiled options on bitcoin , ether (ETH) and solana (SOL) futures, expanding its regulated crypto derivatives offerings.

The contracts bec+ame available for trading on July 6, according to a B3 circular. They include call and put options on bitcoin futures denominated in Brazilian reais, while ether and solana futures are denominated in U.S. dollars.

The options settle into the underlying futures contracts, not the tokens themselves. B3 said the products do not involve custody, transfer or administration of spot cryptoassets.

The contracts trade independently from 9 a.m. to 6:30 p.m. local time, according to B3’s derivatives trading schedule. Exercise is automatic at expiration when the option finishes in the money, unless the holder blocks exercise.

The offering gives traders and asset managers a local venue to hedge crypto exposure, trade volatility and build structured positions without using offshore crypto options markets.

It adds another instrument to B3’s push into regulated crypto products, after the exchange moved to list bitcoin options and ether and solana futures and later prepared bitcoin-linked event contracts.

B3’s bitcoin futures contract is denominated in reais. Its ether and solana futures are denominated in U.S. dollars. All three reference Nasdaq crypto indexes, according to the announcement.

The price of a family home in the U.S. tells two very different stories depending on how it’s measured. Comparing the stories underscores bitcoin’s appeal as a long-term hedge against dollar debasement, the erosion of value in the fiat currency.

According to Fidelity Digital Assets, a typical U.S. house has gained more than $100,000 since 2020. That house-price appreciation is said to generate a positive wealth effect, an economic phenomenon where rising home values make homeowners feel wealthier. Feeling wealthier, they spend more, borrow more and boost the economy even if their actual income remains unchanged.

But what if the gain is just a mirage?

Price the same house in bitcoin and the narrative shifts sharply. What required more than 50 BTC in 2020 now costs just 5 BTC, a 90% decline.

“What appears to be appreciation in housing is more accurately a reflection of an erosion of fiat currency. The issue lies with the unit of account—not the asset itself,” Zack Wainwright, a digital asset research analyst at Fidelity, said.

A roster of 17 banks are preparing to begin testing live transactions on Swift’s blockchain-based ledger, a step toward round-the-clock cross-border payments using tokenized deposits.

Swift said the ledger is ready for initial use by banks across six continents in an announcement on Thursday. Its aim is to allow banks to move funds for customers overnight and on weekends, before final settlement through existing payment systems.

The banks taking part include UBS, BNP Paribas, BNY, Citi, HSBC, and Wells Fargo.

Swift, the bank-owned messaging network used by more than 11,500 financial institutions, announced the development of this shared ledger platform in October. It then said it would allow banks to settle transactions involving stablecoins and tokenized assets across multiple blockchains, working alongside current payment rails, not replacing them.

Swift, said the system gives banks a shared layer for tokenized deposits issued on their own ledgers. Tokenized deposits are digital versions of commercial bank money.

“With our new ledger capability, we’re extending the trust and stability of established finance into the frontiers of digital money,” said Thierry Chilosi, Swift’s chief business officer.

Moment daycare worker tosses toddler into the air and ‘drops him over her head’ | News US

Western Asset Managed Municipals Fund Q1 2026 Commentary

WWE launches brand new title belt as merchandise at $2,000

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: High Hopes

-

NewsBeat4 days ago

NewsBeat4 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Fashion3 days ago

Fashion3 days agoOpen Thread: What Great Books Have You Read Recently?

-

Crypto World6 days ago

Crypto World6 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Politics6 days ago

Politics6 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

News Videos2 days ago

News Videos2 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech2 days ago

Tech2 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Business3 days ago

Business3 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports2 days ago

Sports2 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Crypto World6 days ago

Crypto World6 days agoESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

-

Crypto World3 days ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World4 days ago

Crypto World4 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos3 days ago

News Videos3 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech4 days ago

Tech4 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business6 days ago

Business6 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Sports2 days ago

We have punished the disrespect

-

Crypto World7 days ago

Crypto World7 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos3 days ago

News Videos3 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Fashion2 hours ago

Fashion2 hours agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Crypto World6 days ago

Crypto World6 days agoAlibaba bans Claude Code over alleged backdoor security concerns

You must be logged in to post a comment Login