Crypto World

What is OTC trading in crypto? How whales buy big

When a company buys hundreds of millions of dollars of Bitcoin and the price barely moves, it did not use an exchange. It used an OTC desk. This guide explains over-the-counter crypto trading: why large orders cannot go through order books, how OTC desks source liquidity and settle trades, the difference between principal and agency desks, why so much real volume is invisible, and how to tell when the whales are quietly accumulating.

Here is a puzzle that confuses almost everyone new to crypto markets. A public company announces it bought $500 million of Bitcoin. On any exchange, an order that size would tear through the order book, spike the price, and cost the buyer a fortune in slippage, everyone would see it coming and front-run it. Yet the announcements keep arriving, the purchases keep completing, and the price frequently barely reacts. How?

The answer is a corner of the market most retail traders never touch and much of the real money never leaves: over-the-counter trading. OTC desks are where whales, institutions, corporate treasuries, miners, funds, and governments buy and sell crypto in sizes that would be impossible on public exchanges, through private, negotiated transactions that never appear in any order book. A large and growing share of crypto’s genuine volume happens here, off-screen, and the on-exchange charts that most analysis obsesses over are, in a real sense, only the visible tip of the market.

This guide explains that hidden layer. It covers why large orders cannot use exchange order books, what an OTC desk actually does and how a trade flows from request to settlement, the crucial difference between principal and agency desks and what each costs you, where OTC liquidity comes from, why this volume stays invisible and what that means for reading the market, the risks specific to OTC trading, and the on-chain signals that let outsiders glimpse the whales the order books hide.

Why big orders cannot use the order book

To understand OTC, first understand what it exists to avoid. An exchange order book is a ladder of resting buy and sell orders at various prices, and it has finite depth: only so much is available to buy at the current price, then a bit more slightly higher, then more higher still. A small order fills at the top and barely moves anything. A large order eats through level after level, filling at progressively worse prices, the price impact that grows as depth runs out, and a truly large order can move the market several percent against itself before it completes.

Worse, it does so in public. Order books are visible, and a large order climbing the ladder is a signal every other participant, and every bot, reads instantly: the moment the market sees a whale buying, prices run ahead of it, and the whale ends up chasing a rising market it created, paying a premium that compounds with every remaining coin. This is the reason a $500 million market order is not merely expensive but nearly impossible to execute well: the order’s own footprint is the enemy, and the bigger the order, the worse the self-inflicted damage. Splitting it into small pieces over time, algorithmic execution, helps and is widely used, but it takes time the buyer may not have and still leaks information across the many fills.

OTC exists to solve exactly this. A negotiated, off-book trade transfers a large block at a single agreed price, privately, with no order-book footprint and no public signal until, at most, a disclosure long after the fact. For size, it is not merely cheaper than the exchange; it is the only realistic venue.

What an OTC desk actually does

An OTC desk is a firm that stands between large buyers and large sellers, providing a private venue and, usually, its own liquidity, to move blocks the public market cannot absorb. The major exchanges run OTC desks, specialized firms run independent ones, and the largest trading houses run desks that serve institutions exclusively, and the same firms that act as authorized participants for spot ETFs often source their coin through exactly these channels. Their product is simple to state and hard to deliver: a firm price for a large quantity, executed discreetly, settled reliably.

A trade flows roughly like this. A buyer, say a corporate treasury acquiring $200 million of Bitcoin, contacts the desk, often through a relationship manager, and requests a quote for the size. The desk responds with a price, a single number for the whole block, that reflects the current market plus a spread covering the desk’s risk and margin. The buyer accepts or negotiates; on agreement, the trade is locked at that price regardless of where the public market moves in the next minutes. Settlement follows: the buyer sends funds, the desk delivers the coins, often through an escrow or simultaneous-exchange arrangement that protects both sides, and the whole transaction completes without a single order touching a public book. The buyer got certainty, one price, no slippage, no signal, and the desk earned its spread for absorbing the risk and sourcing the other side.

The relationship layer matters more here than anywhere else in crypto. OTC is a business of trust, credit, and compliance: desks run know-your-customer and anti-money-laundering checks, extend settlement terms to vetted counterparties, and compete on reliability and discretion as much as price. It is, in texture, far closer to traditional institutional finance than to the anonymous, permissionless world of on-chain trading, which is precisely why institutions are comfortable there.

Principal versus agency: who takes the risk

The single most important distinction among OTC desks is whether they trade as principal or as agent, because it determines where the risk sits and how you pay.

A principal desk trades against you from its own book: when you buy, the desk sells you coins it owns or immediately sources, taking the other side of your trade itself. It quotes you a firm price and then bears the risk of covering that position in the market, which is why principal quotes include a spread compensating for that risk. The advantage to you is certainty and speed: you get one price, immediately, and the desk’s problem of sourcing the coins without moving the market becomes the desk’s problem, not yours. The disadvantage is that the spread is the desk’s, and its interests and yours diverge at the margin, since it profits from the spread it can command.

An agency desk, by contrast, works on your behalf to find the other side, executing into the market or matching you against another client, and charges a transparent commission rather than trading against you. Your interests align better, the desk is your agent, not your counterparty, but you bear more of the execution risk and timing uncertainty, because the desk is not guaranteeing you a price, it is promising to work your order well. Large sophisticated players often prefer agency execution for its alignment and transparency; players who value certainty and speed over squeezing the spread prefer principal desks. Many desks offer both, and knowing which model a given trade uses is the first question a serious OTC counterparty asks, because it changes the entire cost and risk structure of the transaction.

Where the liquidity comes from

An OTC desk’s core skill is sourcing the other side of a block without disturbing the public market, and it draws on several pools to do it. The first is its own inventory: principal desks hold positions precisely so they can fill client orders instantly from stock. The second is a network of counterparties, other institutions, miners with coins to sell, funds rebalancing, other desks, that the desk can match against each other, so that a large buyer and a large seller cross privately at a price that serves both and moves nothing publicly. The third is the public market itself, worked carefully: a desk that takes a large buy order as principal must eventually cover it, and it does so by feeding the position into exchanges gradually, algorithmically, over hours or days, absorbing the price impact itself in exchange for the spread it charged the client.

Miners are a structurally important source, because they are natural, continuous sellers, they earn coins and must sell to cover costs, and routing that supply through OTC desks instead of exchanges keeps steady sell pressure off the public books, one reason miner-desk relationships are a quiet load-bearing feature of market structure.

This matching function is the desk’s real value: at its best, OTC is a mechanism for letting large buyers and large sellers find each other without either one’s size becoming a weapon against them, and the better a desk’s network, the more it can match internally and the less it must move the public market at all.

A worked block, and who is on the other side

A concrete example turns the abstraction into mechanics. A treasury company wants $200 million of Bitcoin and calls a principal desk. The desk quotes a single price, say the current market plus a spread of a few tenths of a percent, and the buyer accepts; the price is now locked for the full block regardless of what the public market does next. The buyer wires funds, the desk delivers coins through escrow, and the trade is done, no chart moved, no order book touched, one number for the whole $200 million.

Behind that clean surface, the desk now has a problem it was paid to take: it just sold $200 million of Bitcoin it must replace. If it held inventory, it draws it down and restocks over time; if it did not, it works the public market quietly for hours or days, buying in small algorithmic slices that each move the price a little, absorbing exactly the slippage the client paid to avoid. The spread the client paid is the desk’s compensation for that work and that risk, and a skilled desk that can match the buyer against a natural seller, a miner offloading a month’s production, a fund rebalancing out, avoids touching the public market at all and keeps more of the spread. This is why the desk’s counterparty network is its crown jewel: every internal match is a trade that moves nothing publicly and costs the desk nothing to cover.

The cast of characters on the other side of OTC blocks is worth knowing, because it is the market’s real supply and demand. Miners are the structural sellers, earning coins continuously and needing fiat for costs. Corporate treasuries and funds are episodic buyers and sellers, moving in size around strategy shifts. Early holders and whales distribute long positions through desks precisely to avoid signaling. Exchanges and other desks trade with each other to balance inventory. And increasingly, the intermediaries serving regulated products, the machinery behind spot ETFs and tokenized assets, source and offload through OTC channels, which is why a growing share of the market’s most consequential flows, the ones that actually set the balance of supply and demand, never appear on a single exchange chart.

Why it is invisible, and what that means

The defining feature of OTC volume is that it does not appear on the charts, and internalizing that fact reshapes how you read the market. Exchange volume, the number on every ticker, captures only trades that crossed a public book; the enormous flow that crosses privately through desks is absent, disclosed at best in aggregate and after long delays, if at all. Estimates consistently suggest that OTC and off-exchange volume rivals or exceeds visible exchange volume, which means the market analysts scrutinize is a large but partial sample of the real one.

The consequences are concrete. Price can move on thin visible volume while enormous OTC flow crosses unseen, so a quiet chart does not mean a quiet market. Accumulation and distribution by the largest players often happen almost entirely off-book, which is why major holders can build or exit positions that only become visible later, through disclosures or on-chain forensics, the reason exchange-reserve and whale-wallet data matter so much for reading real supply. And the relationship between on-exchange price and true supply-demand is looser than it appears, because the marginal large trade increasingly does not touch the exchange at all. Reading crypto markets well means constantly remembering that the visible order books are a screen in front of a much larger room, and that the biggest participants prefer the room.

OTC and the rise of on-chain settlement

The OTC world described so far is largely off-chain in its plumbing, private deals settled through escrow and banking rails, and one of the quiet shifts underway is the migration of parts of it onto blockchains themselves. Stablecoins changed the settlement leg first: instead of wiring dollars through correspondent banks, counterparties increasingly settle the cash side of OTC blocks in regulated stablecoins that move in minutes, around the clock, with the coin leg delivered simultaneously on-chain, collapsing settlement risk that once took days into a single atomic-adjacent exchange. The institutional stablecoins built for exactly this purpose have made the cash leg of large crypto trades faster and safer than its traditional-finance equivalent.

The deeper shift is that the assets themselves are becoming programmable in ways that touch OTC’s core function. As tokenized real-world assets and on-chain settlement layers mature, the historical trade-off OTC exists to manage, moving size without moving the market, gains new tools: dark-pool-style on-chain venues, request-for-quote systems that solicit private quotes from multiple desks, and settlement rails that let large blocks change hands with cryptographic finality rather than bilateral trust. None of this has replaced the relationship-driven desk business, which remains dominant for the largest and most sensitive flows, but it is steadily converting OTC from a purely private, trust-based world into a hybrid where the discretion of a negotiated block meets the finality of on-chain settlement. For a market whose largest trades have always happened in the shadows, the direction of travel is toward shadows with receipts, private in price discovery, verifiable in settlement, and the institutions bringing serious size on-chain are precisely the ones driving it.

Risks and the on-chain tells

OTC trading carries risks distinct from exchange trading, and they are worth naming. Counterparty and settlement risk is the central one: in a private bilateral trade, one side sends first unless a trusted escrow or simultaneous-settlement arrangement intervenes, and the history of OTC includes losses from failed settlement and bad actors, a bilateral counterparty exposure closer to traditional finance than to the atomic, trustless settlement of on-chain trades, which is why counterparty vetting and reputable desks matter enormously. Pricing opacity is another: without a public book, a client must trust that the quoted spread is fair, and less sophisticated counterparties can be quoted worse prices precisely because the market is private. Regulatory and compliance exposure runs throughout, since OTC desks are exactly where large flows attract scrutiny. And access is itself a barrier: OTC is a world of minimums, relationships, and vetting, effectively closed to retail, which is part of why its flows stay opaque to the public.

For outsiders, the compensating gift is on-chain data, which offers glimpses the order books hide. Large transfers into and out of known desk and exchange wallets, tracked by analytics firms, can signal OTC-scale accumulation or distribution before it shows in price; shrinking exchange reserves suggest coins moving to storage through private channels; and settlement patterns around major disclosed purchases sometimes leave on-chain fingerprints. None of it is as clean as an order book, but it is the closest an outsider gets to seeing the room where the size actually trades, and learning to read it, transfers, reserves, whale-wallet flows, is learning to see the market’s hidden majority.

The honest summary is that the crypto market most people watch and the crypto market where the largest decisions execute are substantially different places. The order books are real, useful, and public; they are also the retail-facing surface of a market whose deepest liquidity moves privately, negotiated, off-screen, through desks built so that size does not have to announce itself. Understanding OTC does not give a retail trader access to it, but it does something nearly as valuable: it corrects the illusion that the chart is the whole market, and it explains the puzzle with which this guide began, how the whales keep buying, in enormous size, without the price ever seeming to notice.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Details are current as of July 9, 2026. Always do your own research.

Frequently asked questions

What is OTC trading in crypto in simple terms?

OTC, or over-the-counter, trading is the buying and selling of crypto through private, negotiated deals rather than on public exchanges. A desk stands between large buyers and sellers, quoting a single price for a big block and settling it privately, so the trade never appears in any order book. It exists so that large orders can execute without the slippage and public signaling that exchanges would impose.

Why do large buyers use OTC desks instead of exchanges?

Because a large order on an exchange would eat through the order book, filling at progressively worse prices and moving the market against itself, while broadcasting the buyer’s intent to everyone watching. OTC delivers a single agreed price for the whole block, privately, with no order-book footprint, which for large size is both far cheaper and far more discreet than any exchange execution.

What is the difference between a principal and an agency OTC desk?

A principal desk trades against you from its own book, quoting a firm price and taking the other side of your trade itself, earning a spread and bearing the risk of covering the position. An agency desk works on your behalf to find the other side and charges a transparent commission instead of trading against you. Principal offers certainty and speed; agency offers better alignment and transparency.

How does an OTC trade actually settle?

After a price is agreed, the two sides exchange funds and coins, usually through an escrow or simultaneous-settlement arrangement that protects both parties from the other defaulting. Reputable desks run compliance checks and may extend credit terms to vetted counterparties. Settlement reliability is a core part of what a desk sells, since bilateral private trades carry real counterparty risk.

Why does so much crypto volume stay invisible?

Because OTC and off-exchange trades never cross a public order book, so they do not appear in the volume figures on tickers and charts. Estimates suggest this hidden flow rivals or exceeds visible exchange volume, meaning the market most people analyze is only a partial sample. It is why prices can move on thin visible volume while enormous flow crosses privately.

Can regular retail traders use OTC desks?

Generally not. OTC is a world of large minimums, standing relationships, credit, and vetting, effectively closed to retail-sized orders. Its whole purpose is moving blocks far larger than any individual trades. Retail traders interact with the same underlying market through exchanges, and can only glimpse OTC activity indirectly through on-chain data and disclosures.

How can I tell when whales are accumulating through OTC?

You cannot see it directly, but on-chain analytics offer clues: large transfers into and out of known desk and exchange wallets, shrinking exchange reserves suggesting coins moving to private storage, and settlement patterns around disclosed institutional purchases. These signals are noisier than an order book but are the closest an outsider gets to seeing OTC-scale accumulation before it shows in price.

Is OTC trading safe?

It carries risks distinct from exchange trading, chiefly counterparty and settlement risk in bilateral deals, pricing opacity without a public book, and the need to trust the desk’s fairness and reliability. Working with reputable, compliant desks and using proper escrow or simultaneous-settlement arrangements mitigates most of it, which is why relationships and reputation dominate the OTC business far more than in anonymous exchange trading.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Binance’s futures desk is showing signs of a renewed momentum spike, reaching a 2026 high even while spot trading on centralized exchanges remains subdued. According to CryptoQuant analyst Maartuun, Binance logged $1.6 trillion in futures volume in June—its strongest month of the year—despite Bitcoin trading in the mid-$60,000s and a broadly cautious tone from many market participants.

The contrast between accelerating derivatives activity and weak spot volumes highlights a tension investors are watching closely: whether leverage is re-entering the market ahead of a broader risk rebound, or simply reflecting short-term positioning in an otherwise lethargic trading environment.

Key takeaways

- Binance futures volume hit $1.61 trillion in June, up 80% from May’s $893 billion, marking a 2026 high.

- OKX and Bybit also grew in June, but Binance outpaced them by volume and again led the market.

- Quarterly CEX futures volume continued to decline: Q2 fell to $15.7 trillion, down 11% from Q1, according to CryptoRank.

- Spot volumes on CEXs remain weak, with Q2 spot trading at $3 trillion—the weakest quarter in two years.

- Binance’s uptick arrives near regulatory changes in the EU, including the MiCA transition schedule and related licensing developments.

June’s derivatives rebound at Binance

CryptoQuant’s Maartuun said Binance processed $1.61 trillion in futures trading volume in June, the highest monthly figure recorded so far in 2026. The jump was stark: June volume rose by about 80% versus May’s $893 billion.

The strength wasn’t limited to Binance. OKX reported $609 billion in June futures volume, while Bybit recorded $434 billion. Both exchanges increased versus May—OKX up 9% and Bybit up 18%—suggesting the rise was broad-based across major venues rather than isolated to a single platform.

Even so, Binance’s lead stood out. Maartuun noted that the trio of exchanges has not seen futures activity near these levels since January 2026, when Binance moved roughly $1.5 trillion and OKX and Bybit reached $667 billion and $502 billion respectively.

Broader market still shows hesitation: futures down overall, spot at multi-year lows

While June’s spike looks encouraging for derivatives activity, the bigger picture remains mixed. CryptoRank data cited in the report shows that total CEX futures volume fell to $15.7 trillion in Q2 2026, down 11% from $17.6 trillion in Q1. This represented the third consecutive quarterly decline for centralized exchange futures.

The pace of contraction did ease compared with Q1, when futures volume dropped 31% versus Q4 2025. In Q2, Binance maintained its position as the largest futures venue, holding approximately 28% market share.

Spot markets, however, were more clearly impaired. CEX spot volume reportedly fell to $3 trillion in Q2, the weakest quarter in two years and an 18.9% decline from Q1. Binance remained the largest spot exchange by volume, with $731 billion for the quarter, but its market share slid from 27% to 24%, signaling that the downturn wasn’t just a dip in overall activity—it also came with share erosion.

Taken together, the numbers suggest June’s futures surge may reflect traders seeking exposure through leveraged instruments even when broader spot participation has not recovered. For investors, that distinction matters: derivatives volume can rise during periods when spot demand is still muted, but it can also precede volatility rather than stable trend formation.

EU MiCA transition: Binance futures activity continues after the shift

The timing of June’s futures strength also lands near Europe’s Markets in Crypto-Assets (MiCA) transition period. Earlier coverage noted that the end of the transition schedule raised questions about how major exchanges would adapt operationally and how quickly trading patterns would normalize under the new compliance framework.

In late June, Binance withdrew its application for a license in Greece just days before the framework moved into its next phase on July 1. Against that regulatory backdrop, early July data from CryptoQuant indicated Binance’s futures market remained active after the transition, recording $418 billion in futures volume in the first 10 days of July.

That continuation doesn’t confirm that regulation improved trading conditions; it does, however, provide at least an early signal that activity did not abruptly stall at the transition boundary. The next key question for traders and exchange operators will be whether this level of derivatives throughput persists over subsequent weeks and whether spot volumes begin to respond as regulatory uncertainty fades.

What to watch next for traders and exchange users

June’s futures surge is a clear data point: Binance’s derivatives volume jumped sharply to a 2026 high while broader quarterly trends show that CEX spot and futures volumes remain under pressure. Investors should watch whether July sustains similar momentum and whether spot trading starts to recover alongside futures—or whether the market continues to concentrate activity in leveraged instruments as traders navigate ongoing regulatory and macro uncertainty.

Humanoid robot startup LimX Dynamics shows off its products at its Shenzhen, China, office on July 3, 2026.

Evelyn Cheng | CNBC

BEIJING — Humanoid startup LimX Dynamics is getting ready to go public, just over four years after it was founded during the pandemic.

“Listing is a must,” said founder Will Zhang, emphasizing the importance of timing. He was speaking to reporters ahead of the company’s announcement Tuesday that it had raised $200 million in a pre-IPO round.

Zhang compared the situation to Chinese electric car startups Nio, Xpeng and Li Auto, which successively listed in the U.S. from 2018 to 2020. “Once the technology is mature, if [the company] doesn’t list, then like WM Motor, it may disappear,” he said in Mandarin, translated by CNBC.

Several overseas investors, including UAE-based Stone Venture, Italy-based GGG and Germany-based Redstone VC participated in LimX’s latest round, which valued the startup at 15 billion yuan ($2.21 billion), according to a press release.

The startup said it was already preparing for its IPO, likely in Hong Kong, and is in a confidential phase of review.

The urgency comes as China now has well over 100 humanoid companies, which fall under the national push for “embodied AI.”

Reflecting a rapid surge in interest, investment in the sector hit 47.09 billion yuan ($6.95 billion) in the second quarter, more than double that of the first quarter — and up over six times versus the same period last year, according to industry data provider Xiniu.

A new phase

China has fast-tracked approval for humanoid company Unitree to list in Shanghai, while Hong Kong processes applications from more than 500 companies across sectors.

“With more industrial and collaborative robot companies potentially coming to IPO, competitive pressure is likely to persist,” Morgan Stanley said in a report last week, noting sector players DeepRobot and Leju that are looking to list soon.

The investment firm forecasts 18% growth in China’s industrial robots market this year, and shipment of 50,000 humanoids.

LimX aims to create fully autonomous commercial service robots. The company said it will kick off a multi-year plan to ship thousands of humanoids to the Middle East, and is delivering its entertainment-focused Luna humanoid to customers in South Korea.

To founder Zhang, the technology behind humanoid robots has already crossed the “0 to 1” line of innovating from scratch. The next barrier to entry, he said, lies in making a good product that meets users’ needs.

Other backers in the latest funding round include Chinese precision parts company Lens Technology, IDG Capital, WestSummit Capital, Nio Capital and Hefei Binhu Industry Development Group, the release said.

Bolivia is considering adding Tether’s USDT to its national payments infrastructure, a potential milestone for stablecoin adoption in Latin America amid a long-running shortage of US dollars. The government says it is working on a regulatory approach that would treat USDT as a payment instrument alongside the boliviano and the US dollar—rather than a fringe asset outside the formal economy.

Economy and Public Finance Minister Jose Gabriel Espinoza said at a press conference on Monday that the state is assessing a framework to allow USDT “to circulate as just another currency.” Any rollout, he added, would need strong oversight and anti-money laundering controls because Bolivia remains on the Financial Action Task Force (FATF) grey list.

Key takeaways

- Bolivia is evaluating whether USDT could be recognized for everyday transactions such as payments, savings and trade.

- The proposal would require a regulatory structure that can place USDT inside the country’s formal payments system.

- Bolivia’s FATF grey-list status means anti-money laundering safeguards are expected to be central to any approval process.

- The move comes as the country confronts a widening gap between official and parallel exchange rates that has increased demand for dollar-denominated alternatives.

USDT would be treated as part of everyday payments

According to CriptoNoticias, the regulatory framework being considered is still under review. If adopted, it would aim to formally recognize USDT for retail and commercial activity, including payments, savings and trade, without relying solely on cash or the traditional banking channel.

Espinoza’s framing matters because it suggests Bolivia is not merely allowing crypto trading or occasional transfers, but contemplating a system design where USDT functions as a practical alternative for transactions. For consumers and businesses, that could mean more predictable settlement options when local access to dollars is constrained.

Regulatory hurdles tied to FATF monitoring

Espinoza also emphasized that any implementation would depend on a “robust regulatory framework” and effective anti-money laundering protections. His comments connect directly to Bolivia’s placement on the FATF grey list, which flags jurisdictions with increased monitoring needs due to deficiencies in preventing money laundering and terrorist financing.

That context helps explain why the government is taking a cautious, framework-first approach. Moving stablecoins into a national payments role typically requires clear responsibility lines—who can distribute or process them, how compliance checks are performed, and how suspicious activity reporting would operate. For Bolivia, those requirements could become a gating factor for how quickly a USDT rollout can move from proposal to practice.

Dollar scarcity and exchange-rate strain push demand toward stablecoins

The policy discussion comes against a backdrop of persistent dollar shortages in Bolivia. Reuters previously reported that Bolivia kept an official exchange rate of 6.86 bolivianos per US dollar for purchases and 6.96 for sales for years, before later abandoning the long-standing peg after pressure on foreign exchange reserves.

As Reuters noted, the abandonment of the peg contributed to the expansion of a parallel foreign exchange market where the dollar traded at a steep premium relative to the official rate. When the cost of dollars diverges sharply between official channels and informal markets, demand tends to shift toward instruments that track or approximate dollar value. In this environment, stablecoins such as USDT can become appealing for payments because they offer a dollar-denominated unit of account without requiring direct access to physical dollars.

Industry research also points to growing activity. Chainalysis’ 2025 evaluation of crypto adoption across Latin America reported $14.8 billion in total transaction volume over a 12-month period for Bolivia included within the regional assessment. While this figure does not isolate stablecoins alone, it supports the broader claim that digital assets—often used in response to currency pressures—have become more integrated into real economic behavior across the region.

Bolivia’s return to crypto-friendly policy after the 2024 ban

The USDT payments initiative fits into a broader pivot by Bolivia toward digital assets following the lifting of its longstanding cryptocurrency ban in 2024. Since taking office in late 2025, President Rodrigo Paz Pereira’s administration has pledged to incorporate digital assets into the formal financial system, an approach described by earlier coverage from Cointelegraph as paving the way for banks to introduce crypto-related products and services, potentially including stablecoin-based accounts.

What’s notable now is the specificity: instead of focusing only on banking products or general “blockchain integration,” the government is explicitly weighing how USDT could fit into everyday payments. That difference could determine how quickly stablecoins move from parallel usage toward regulated, widely accepted channels.

Readers should watch how Bolivia’s draft regulatory framework is shaped—particularly around compliance obligations given its FATF grey-list status—and whether authorities set measurable timelines for pilot programs or bank participation. The next question is not only whether USDT will be recognized, but how the state plans to govern distribution, monitoring and settlement in a way that can survive both financial controls and real-world liquidity constraints.

A Bitcoin wallet dormant since the cryptocurrency traded near $6,500 has transferred 2,931 BTC worth about $188 million, reviving onchain activity after seven years.

Summary

- A Bitcoin wallet inactive for seven years has moved 2,931 BTC worth about $188 million.

- Onchain data showed the wallet last became active when Bitcoin traded near $6,500, leaving the holder with an estimated tenfold gain.

- Whale sized transfers continue to dominate Bitcoin exchange inflows, a trend that analysts have historically linked to selling pressure.

Blockchain intelligence platform Arkham reported that the long-inactive holder moved the Bitcoin from wallet “356my” to a new address, “bc1qn”, on Sunday. The transfer is the wallet’s first recorded onchain movement since it last became active when Bitcoin was priced at roughly $6,500.

With Bitcoin now changing hands at around $64,000, blockchain analytics platform Onchain Lens estimated the holder is sitting on nearly a tenfold gain from the original position.

Whale transfers continue to dominate exchange flows

The latest movement comes as large Bitcoin holders continue to account for most transfers into cryptocurrency exchanges, a trend that onchain data has linked to rising selling pressure.

CryptoQuant’s exchange whale ratio chart showed that about 99% of Bitcoin deposited to exchanges currently comes from the 10 largest individual transfers. The metric stood at 0.99 at the time of publication, indicating that whale-sized transactions continue to dominate exchange inflows.

According to CryptoQuant, elevated whale exchange ratios have historically been associated with bearish market conditions because large deposits are more likely to precede sizeable sell orders than routine transfers from retail investors.

Separately, data from Coinglass classifies transfers worth at least $10 million as whale transactions. Such movements have accounted for most Bitcoin flowing to exchanges in recent months, increasing trader focus on whether large holders are preparing to sell.

Selling pressure has also persisted from another direction. Data from Farside Investors showed that U.S. spot Bitcoin exchange-traded funds recorded $197 million in net inflows during the week leading up to Friday, although the products posted $4.51 billion in net outflows throughout June, their weakest monthly performance on record.

Dormant wallets remain under close watch

Older Bitcoin wallets have continued attracting market attention because many are associated with early miners, long-term holders, or defunct trading platforms.

Earlier this year, crypto.news reported that a dormant whale destroyed 107 BTC worth about $8.3 million by sending the coins to an unrecoverable burn address after nearly 11 years of inactivity. Blockchain security firm AMLBot said the transactions may have been linked to the collapsed Mt. Gox exchange, although no entity behind the transfers was identified.

In a separate case reported by crypto.news, another Satoshi-era holder transferred 2,650 BTC worth more than $200 million to trading firms FalconX and Cumberland while retaining nearly 6,000 BTC.

Although those transfers did not confirm an immediate sale, market participants closely tracked the movement because large transactions from early Bitcoin holders can introduce additional supply if the coins eventually reach exchanges.

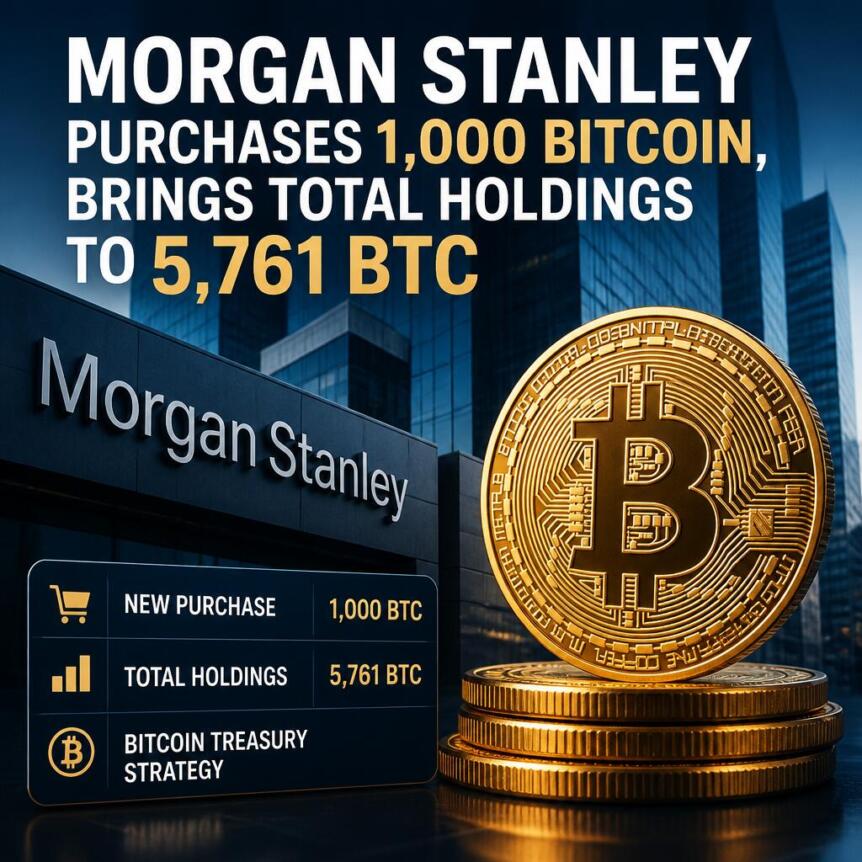

Banking giant Morgan Stanley acquired nearly 1,000 BTC over the past two weeks, taking its total holdings to 5,761 BTC, worth roughly $370 million.

According to data from Arkham, the bank added BTC to its existing stash during the market pullback through its spot Bitcoin investment product.

Morgan Stanley Adds To Bitcoin Stash

Morgan Stanley added to its Bitcoin holdings during the recent market pullback. The banking giant currently holds 5,761 BTC, making it one of the biggest institutional holders of the flagship cryptocurrency.

The acquisition was executed through a series of transfers instead of a single purchase. Arkham data shows large transfers from Coinbase Prime wallets. The transaction history also includes a 1 BTC transfer back to Coinbase Prime along with minor operational transfers.

The inflows originated from Coinbase Prime custody and deposit addresses, indicating the transfers were completed via Morgan Stanley’s spot Bitcoin investment product.

Buying The Dip

Arkham classifies Morgan Stanley as a fund, an exchange-traded product, and a Bitcoin whale. It has also linked the banking giant’s portfolio to 11 wallet addresses. The latest round of purchases is in line with Morgan Stanley’s strategy of accumulating during price dips.

However, Arkham or Morgan Stanley have not disclosed whether the purchases are direct purchases, client subscriptions, or operational inflows into its investment vehicle. Arkham has also not identified the underlying investors or whether the assets are being managed on behalf of clients or are firm-based holdings.

Morgan Stanley Increasing Its Crypto Footprint

Morgan Stanley Wealth Management recently announced a partnership with Galaxy Digital to expand its digital asset footprint. Under the partnership, high-net-worth individuals can lend their digital assets, including Bitcoin (BTC), Solana (SOL), and Ethereum (ETH), to Galaxy Digital in return for shares in spot crypto investment products, including the Morgan Stanley Bitcoin Trust. The program allows investors to gain crypto exposure in a regulated environment without selling their digital assets.

Morgan Stanley and Galaxy Digital claim the partnership also reduces the in-kind crypto-to-exchange-trading product onboarding times by 75%. The offering is part of a growing trend of on-chain accumulation as institutional interest and participation rise.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

The UK is preparing to move tokenized financial markets from experimental pilots to scaled, live trading and settlement, according to a government-backed industry task force report published by Wholesale Digital Markets Champion Chris Woolard. The document estimates that, if the country becomes a leader in tokenized markets, the effort could add as much as £33 billion (about $44 billion) to annual economic output by 2035.

The report outlines a 12-month plan to test blockchain technology in a financial transaction that uses securities to borrow cash, and it calls for the UK to issue its first tokenized government bond—known as a gilt—by the first quarter of 2027. Woolard’s role is tied to HM Treasury’s digital markets strategy, with the task force assembled to connect traditional market infrastructure providers with digital-asset firms.

Key takeaways

- The task force aims to progress from isolated blockchain trials to “scale,” with real-market trading, settlement, and use of tokenized securities as collateral.

- Plans include a 12-month blockchain test focused on repo-like mechanics where securities are used to raise cash.

- The roadmap targets a first tokenized UK government bond issuance by the first quarter of 2027.

- The report urges the Bank of England to accept tokenized gilts as collateral, positioning collateral eligibility as a major adoption gate.

- Task force membership spans leading banks, market infrastructure firms, and crypto companies, underscoring a cross-industry approach.

From pilots to live tokenized securities markets

While tokenization has been discussed for years, the report’s emphasis is on practical market plumbing—moving beyond demonstrations toward arrangements that can support securities issuance, secondary-market activity, and settlement workflows. The task force describes its mission as shifting “from pilots to scale” and “from ambition to action,” reflecting a more implementation-focused posture than many earlier initiatives.

Central to that approach is the report’s view that tokenized assets have limited real-world value unless they can be traded and used to obtain cash. In the document’s framing, the ability to raise funding against tokenized securities—and to have those tokens participate in established collateral frameworks—determines whether tokenization can materially change market behavior.

To that end, the task force’s 12-month plan centers on testing blockchain in a financial transaction where securities are used to borrow cash. Although the report does not present additional implementation details in the provided text, the structure aligns with the market logic of repo transactions, where the speed and settlement efficiency of collateral exchanges can have meaningful operational and cost implications.

Tokenized gilts: a timeline and expanded end goals

Tokenized government bonds are not a brand-new idea in the UK. The government previously announced the Digital Gilt Instrument (digit) pilot in November 2024, using public documentation to describe the initiative.

Later updates pushed the concept further. A July 2025 update laid out intentions covering onchain settlement, over-the-counter trading, and secondary-market development. The government also appointed HSBC’s Orion platform to support the pilot on Feb. 12, signaling that at least part of the effort is geared toward real operational systems rather than purely theoretical trials.

The new task force report builds on that foundation by adding a clearer timetable and broadening how the tokenized gilt would be used. Beyond issuance, the roadmap seeks subsequent digital-gilt offerings, live secondary-market trading, and—importantly—eligibility for use as central bank collateral.

The collateral angle is where the report becomes more than a rollout plan. It explicitly argues that tokenized securities only become economically meaningful when they can be used to raise cash, and it calls on the Bank of England to accept digital gilts as collateral. For market participants, that would be a key step toward turning tokenized assets into a mainstream funding and settlement tool rather than a niche alternative.

Task force composition and industry buy-in

Woolard’s first report was developed with a task force described as bringing together more than 50 companies spanning traditional finance and crypto. The membership list in the text includes BlackRock, Goldman Sachs, JPMorgan, Morgan Stanley, HSBC, UBS, Coinbase, Circle, Ripple, Kraken, DTCC, and Euroclear.

Ripple, which appears among the industry members, publicly supported the initiative in a statement shared on Monday. The company said that onchain funds, bonds, and repo are not experiments, arguing that such instruments are already proving “cheaper, better and faster” than legacy equivalents.

For investors and builders, the breadth of the task force matters. A tokenization roadmap that includes both major securities market infrastructure players and crypto platforms suggests the UK is trying to align interfaces—custody, settlement, and compliance—rather than relying on a single ecosystem.

How UK payment infrastructure could connect the dots

The report’s tokenized-gilt ambition also intersects with existing UK efforts to improve settlement and payments. The text points to a blockchain-based wholesale payment infrastructure that could support tokenized-market settlement.

In December 2023, London-based Fnality launched a sterling-denominated payment system tied to central bank reserves. The network was designed to enable real-time repo, tokenized securities settlement, and cross-currency payments, potentially providing the infrastructure layer needed for tokenized collateral to move quickly and consistently across parties.

By pairing that sort of settlement/payment capability with a phased approach to tokenized gilts and secondary-market trading, the UK’s roadmap is effectively trying to solve two problems at once: how tokenized assets are issued and traded, and how the cash legs and settlement mechanics work end to end.

Still, the biggest practical uncertainty remains whether collateral eligibility—specifically Bank of England acceptance of digital gilts—can be achieved on a timeline that matches the planned issuance and market scaling. The report’s call for central bank collateral suggests that regulators and system operators will play a decisive role in determining how quickly tokenization can move into full-market usage.

Going forward, market participants should watch for updates on the 12-month blockchain test details, the operational requirements for secondary trading, and any announcements that clarify how the Bank of England and other oversight bodies plan to treat tokenized gilts as collateral. If those pieces align, the UK could shift tokenization from a series of pilots into a functioning market segment with real funding utility.

![]()

Bolivia has moved closer to recognizing Tether’s USDT as an official payment option alongside the boliviano and the U.S. dollar as the country continues to grapple with a prolonged shortage of foreign currency.

Summary

- Bolivia is considering recognizing USDT as an official payment option alongside the boliviano and U.S. dollar.

- Local banks already support USDT services as the country struggles with a prolonged dollar shortage.

- Tether is expanding institutional use of USDT while pursuing stronger reserve transparency through a KPMG audit.

According to reports from Bolivia, government officials are weighing a proposal that would allow USDT to circulate as part of the national payment system, a step that would formalize a practice already taking shape across parts of the country’s financial sector.

If approved, the move would make Bolivia the first Latin American nation to officially recognize USDT as a payment option alongside its domestic currency and the U.S. dollar.

Years of declining natural gas production and exports have steadily reduced Bolivia’s dollar reserves, leaving businesses and importers struggling to secure foreign currency. The shortage has pushed authorities to explore alternative payment methods, with crypto gradually becoming part of that strategy instead of remaining a niche financial product.

Dollar shortages have accelerated USDT adoption

The government’s first major crypto-related measure came in March 2025, when state-owned energy company YPFB received authorization to use cryptocurrency payments for fuel imports during the country’s worsening dollar shortage.

Retail adoption followed soon after. In June 2025, Tether chief executive Paolo Ardoino shared images on social media showing Bolivian stores listing everyday products, including dairy goods and chocolate, with prices displayed in USDT.

The posts suggested stablecoins were already being used for ordinary purchases rather than remaining limited to investment activity.

Crypto analyst CryptoPatel later argued on X that economic conditions, rather than regulation, were encouraging people to move toward stable assets, writing, “When your currency fails, bring in the stable one.”

His comments accompanied growing evidence that many consumers were choosing the dollar-pegged stablecoin as access to physical U.S. dollars became increasingly difficult.

Meanwhile, Bolivia’s banking sector has already begun supporting the ecosystem. Local lenders Banco Unión and Banco FIE currently provide services linked to USDT, indicating that much of the financial infrastructure needed for wider adoption is already in place.

Formal recognition would instead establish a regulatory framework around an existing trend, potentially making remittances faster, lowering transaction costs and offering an alternative to informal dollar markets.

Tether expands institutional use of USDT

Outside Bolivia, Tether has continued promoting USDT for larger financial transactions. As previously reported by crypto.news, Hyundai Motor America and Hyundai Motor Mexico completed a pilot cross-border treasury payment using USDT on the Avalanche blockchain.

According to Tether, Hyundai Motor America converted U.S. dollars into USDT before transferring the stablecoin to its Mexican subsidiary, where it was exchanged back into U.S. dollars.

The company said the $20,000 transfer, including verification, was completed in about seven minutes, compared with three to four hours or longer for a conventional bank transfer.

Institutional credibility has also become a focus for the stablecoin issuer. In March 2026, Tether appointed KPMG to conduct a full audit of reserves backing roughly $185 billion worth of USDT. The company said the audit is intended to strengthen confidence in the token’s reserve backing following years of scrutiny over its transparency.

Operationally, Tether has concentrated its stablecoin strategy around USDT after discontinuing its aUSDT product, reinforcing the flagship token’s role in its international business.

Despite growing momentum, Bolivia has not yet finalized the legal framework for integrating USDT into its payment system. Neither the Central Bank of Bolivia nor lawmakers have published formal implementation rules.

Still, reports indicate the proposal has advanced further than previous crypto initiatives in the country, while other emerging economies facing persistent dollar shortages are expected by analysts to watch Bolivia’s experience closely.

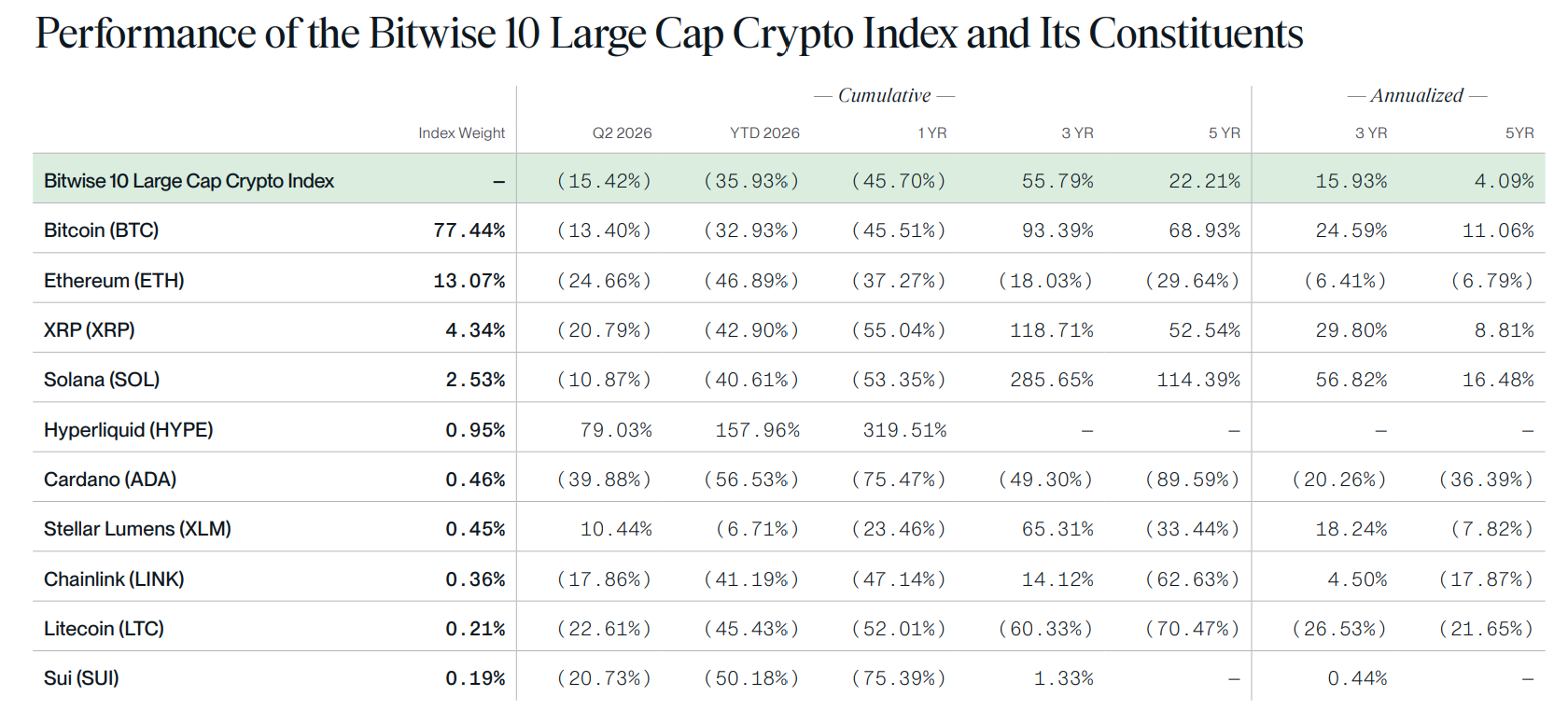

Stablecoin volume hit a record $1.79 trillion in June, even as the tokens’ total supply shrank. The split captures a market pricing crypto for a downturn while its usage keeps climbing.

A Bitwise report, Visa’s on-chain data, and new ownership figures point the same way. Stablecoin transfers and prediction markets hit records even as the Bitwise 10 Large Cap Crypto Index fell 15.4%.

Prices Fell, But the Plumbing Kept Growing

The second quarter was crypto’s third straight losing quarter, the longest run since 2022. Spot Bitcoin (BTC) exchange-traded funds posted their worst quarter of outflows. On-chain activity and trading volume slipped.

Yet the Bitwise report argues the market has it backwards. Crypto is being priced for a bear market, it says, even though the industry is roughly twice its 2022 size. Deeper liquidity and more institutions now sit on-chain.

The gap shows up in the fundamentals. Measured against the 2022 low, Ethereum (ETH) transaction activity is up about 13 times. Value locked in decentralized finance has climbed more than 60%, and stablecoin assets have roughly doubled.

Prices still lagged. The flagship crypto index fund lost ground, with eight of its 10 holdings in the red.

That divide has reopened the question of whether the market has already found the bear market bottom.

Stablecoin Volume and Derivatives Led the Quarter

Stablecoins settled about 2.3 times Visa’s payment volume over the past year, Bitwise said. In June, transfers reached the $1.79 trillion record, according to Visa Onchain Analytics. Rising institutional stablecoin volume kept settlement near all-time highs.

A shrinking stablecoin supply once signaled trouble. Terra’s 2022 collapse erased tens of billions and froze the market. This time supply eased while transfers set a record, a very different backdrop.

USD Coin (USDC) handled about two-thirds of that volume. Regulated dollars are taking share as institutions lean in.

Trading told a similar story. June spot volume across major exchanges fell roughly 5% from May, while derivatives volume rose about 4%. Active traders stayed engaged even as casual buyers stepped back.

Tokenized Assets and Prediction Markets Set Records

Tokenized real-world assets climbed 50.3% this year to $32.89 billion, the report said. Prediction market volume hit a record $43.2 billion in the quarter, close to 18 times its level a year earlier.

Crypto equities held up too. The Bitwise Crypto Innovators 30 Index rose 30.6%. Apps such as Hyperliquid, PancakeSwap, and Aave each earned close to $900 million in revenue over the past year.

Advisers increasingly favor stablecoins and tokenization over direct Bitcoin bets. Individuals still hold about two-thirds of Bitcoin supply.

However, institutions and funds bought roughly 829,000 BTC in 2025, while retail wallets shed about 696,000, according to River.

Bitwise framed the split between price and progress as the setup for the next cycle.

“That foundation won’t stop the winter, but it determines what grows in the spring,” Matt Hougan wrote.

The next few quarters will test whether usage pulls prices up or weak prices sap momentum. For now, the data shows an industry still growing while its market value waits to catch up.

The post Crypto Bear Market? These Reports Say the Industry Has Never Been Stronger appeared first on BeInCrypto.

Jito has proposed a governance overhaul that would direct 100% of the DAO’s JTX revenue share toward open-market JTO buybacks and permanent token burns through at least Q4 2027.

Summary

- Jito has proposed using DAO revenue for JTO buybacks and permanent token burns through Q4 2027.

- JIP-38 would place most protocol revenue under DAO control, with JTO holders governing allocations.

- JTO rose as much as 8% after the governance proposal was unveiled, according to crypto.news.

According to a governance proposal published by Jito on July 13, the protocol has introduced JIP-38, which would formally classify Jito as a token-centric network where nearly all major network revenue flows to the decentralized autonomous organization and remains under the control of JTO token holders.

The proposal triggered an immediate market reaction, with Jito (JTO) climbing as much as 8% shortly after its release, according to data from crypto.news.

Revenue would be redirected to JTO holders

Under JIP-38, Jito proposes using the DAO’s entire share of JTX revenue to buy JTO tokens on the open market before permanently removing those tokens from circulation. According to the proposal, this arrangement would remain in place for at least one year, extending through the fourth quarter of 2027.

One exception remains in the framework. The proposal states that 20% of JTX platform fees would continue to be reinvested into JTX development rather than being allocated to buybacks and burns. Jito said the remaining major revenue streams would continue flowing through the DAO under governance controlled by JTO holders.

To carry out the program, the proposal calls for buybacks to be executed automatically through a Rev Splitter mechanism overseen by the project’s Dev Council. Alongside the automation process, Jito plans to update its governance documentation so the protocol’s operating model formally recognizes the token-centric structure.

According to JIP-38, existing revenue allocation commitments would be completed before a comprehensive review of protocol fee streams takes place in Q4 2027.

During that review, governance participants would evaluate the performance of token buybacks, ecosystem incentives, and other capital allocation methods before JTO holders vote on the network’s next long-term revenue framework.

Governance changes extend beyond token burns

Beyond the buyback program, JIP-38 outlines several operational changes intended to support the new revenue structure. According to the proposal, the Rev Splitter would become progressively more automated while governance records would be updated to match the revised economic model.

Jito also stated in the proposal that the framework is designed so value generated across the network accrues to the JTO token instead of external corporate entities. Any future changes to revenue allocation after Q4 2027 would require approval through governance voting by JTO holders.

The proposal arrives as Jito continues expanding its presence across the Solana ecosystem. Earlier this year, as previously reported by crypto.news, 21Shares launched the 21Shares Jito Staked SOL ETP (JSOL) on Euronext Amsterdam and Euronext Paris.

The issuer said the product provides regulated exchange-traded exposure to Solana through JitoSOL while embedding staking rewards, allowing investors to access the asset through traditional brokers and banks without managing wallets or staking infrastructure.

Institutional support for the protocol has also grown over the past year. As previously reported by crypto.news, Andreessen Horowitz’s (a16z) crypto division invested $50 million in Jito to help expand the Solana staking protocol’s ecosystem.

The investment included an allocation of JTO tokens to the venture firm, adding another high-profile backer as the protocol seeks approval for its latest governance proposal.

Strategy has raised $466.7 million through fresh MSTR stock sales while leaving its Bitcoin holdings unchanged at 843,775 BTC for the week ending July 12.

Summary

- Strategy raises $466.7 million through MSTR stock sales.

- Company keeps Bitcoin holdings unchanged at 843,775 BTC.

- Standard Chartered maintains $100,000 Bitcoin target despite treasury concerns.

According to a Form 8-K filed with the U.S. Securities and Exchange Commission (SEC), Michael Saylor-led Strategy sold 4,818,781 Class A MSTR shares between July 6 and July 12 through its at-the-market (ATM) program, generating approximately $466.7 million in net proceeds. Despite the capital raise, the company reported that it did not purchase or sell any Bitcoin during the reporting period.

The filing showed Strategy continued to hold 843,775 BTC, acquired for about $63.69 billion at an average purchase price of $75,476 per Bitcoin, excluding fees and expenses. Following the latest issuance, the company still has roughly $23.79 billion available under its MSTR ATM stock program.

Strategy keeps Bitcoin holdings unchanged after recent sale

Fresh SEC disclosures also showed Strategy held approximately $3 billion in U.S. dollar reserves as of July 12. According to the filing, the cash is intended to cover preferred stock dividends and interest payments on the company’s debt. The reported balance also includes expected proceeds from ATM share sales that had not settled by the reporting date.

The company further disclosed that it did not repurchase any shares under its existing buyback programs during the same week.

The latest filing follows Strategy’s $216 million Bitcoin sale disclosed the previous week, only the second BTC sale in the company’s history. At the time, the company said the proceeds would be used to fund dividends tied to its STRC preferred stock and other digital credit securities. After that transaction, Strategy’s Bitcoin balance fell to 843,775 BTC, where it has remained through the latest reporting period.

Earlier reports also noted that Strategy has authorization to sell up to $1.25 billion worth of Bitcoin under its BTC Monetization Program, a development that has drawn close attention from market participants even though the company has not announced additional BTC sales.

Standard Chartered says treasury uncertainty drove recent weakness

Attention around Strategy’s Bitcoin plans increased after Executive Chairman Michael Saylor posted the company’s familiar Bitcoin acquisition chart on July 12 with the message, “Orange dots tell only part of the story.” As crypto.news reported earlier, the post did not confirm whether Strategy had bought, sold, or held Bitcoin during the latest reporting week.

Crypto.news also noted that Strategy’s public Bitcoin tracker continued to show 843,775 BTC, matching the latest SEC filing. The company typically reports treasury activity through regulatory filings, meaning social media posts do not establish whether a transaction has occurred or indicate its direction.

The latest disclosure comes as Bitcoin has climbed back above $64,000 after Standard Chartered reaffirmed its $100,000 price target for the end of 2026. In a research note, the bank said recent weakness in Bitcoin was driven largely by uncertainty surrounding Strategy’s evolving treasury approach rather than by any deterioration in Bitcoin’s underlying fundamentals.

Standard Chartered added that the recent pullback should not be interpreted as a change to its long-term bullish outlook for the cryptocurrency.

Binance June Futures Volume Hits $1.6T as Spot Trading Slows

Young and Restless 2-Week Spoilers July 13-24: Adam’s Explosive Rebellion & Jack’s Nightmare

Last Time THIS Happened Bitcoin Exploded 20x (It’s Happening Again!)

-

News Videos7 days ago

News Videos7 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Fashion5 days ago

Fashion5 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Tech7 days ago

Tech7 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Sports4 days ago

Sports4 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Tech6 days ago

Tech6 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Sports4 days ago

Sports4 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports6 days ago

We have punished the disrespect

-

Crypto World7 days ago

Crypto World7 days agoBinance lists Strategy’s STRC stock as company expands Bitcoin funding

-

Tech4 days ago

Tech4 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Tech7 days ago

Tech7 days ago9 Best Keyboards (2025), Tested and Reviewed

-

Business7 days ago

Business7 days agoEnbridge: AI Tailwind Priced In (Rating Downgrade)

-

Crypto World7 days ago

Crypto World7 days agoClaude AI Created Something Anthropic Never Designed

-

News Videos7 days ago

News Videos7 days ago“What’s going on?!” Carl Froch discusses Floyd Mayweather Jr financial issues

-

Crypto World6 days ago

Crypto World6 days agoNasdaq arthritis company holding Moshe Hogeg crypto hits all-time low

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts 4,800 Jobs as Xbox Loses 3,200 Roles in Reset

-

News Videos5 days ago

News Videos5 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoKeychron is stepping outside keyboards with a $349 Thunderbolt 5 dock aimed at power users

-

Business6 days ago

Business6 days agoASX 200 Slides Over 0.6% as Rare Earths and Lithium Stocks Tumble Amid Global Semiconductor Sell-Off Today

You must be logged in to post a comment Login