Crypto World

Peter Schiff Predicts a 70% Bitcoin Crash and Warns Holders Will Regret Not Selling

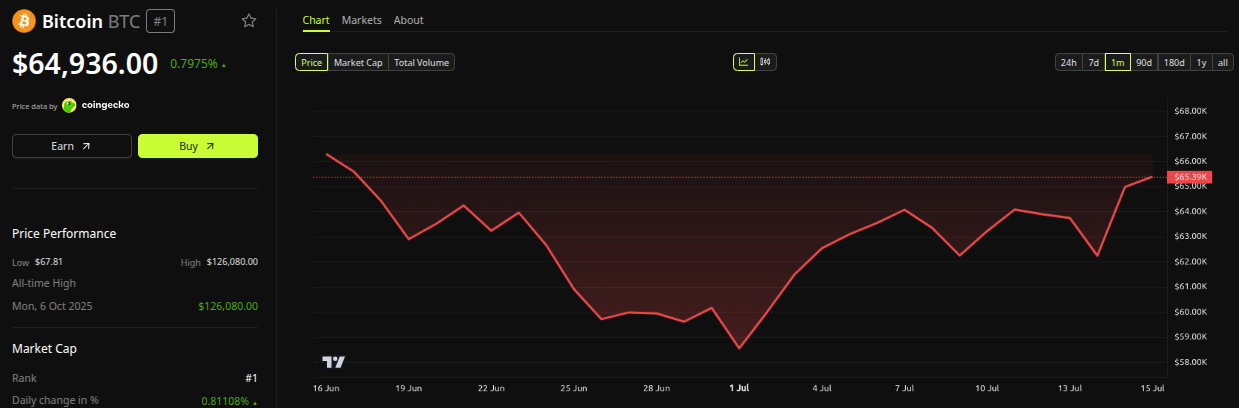

Peter Schiff attacked Bitcoin and Michael Saylor on July 15, predicting a slide to $20,000 (nearly 70% below current prices) and questioning MicroStrategy’s decision to sell stock rather than BTC.

The economist argues that Saylor is trapped and that holders who refuse to sell today will regret it soon.

Schiff Targets Strategy’s $450 Million Stock Sale

Strategy (formerly MicroStrategy) is the corporate vehicle through which Michael Saylor accumulated more than 847,000 Bitcoin, making it the largest public holder of the asset.

Schiff dedicated part of his latest podcast episode to dissecting the company’s latest financial moves. His conclusions were predictably harsh.

The firm has gone three consecutive weeks without buying Bitcoin. It has not sold any either since disposing of 3,588 BTC last week, opting instead to raise $450 million through a common stock sale.

That decision pushed cash reserves to $3 billion while the stock traded at a steep discount to its Bitcoin holdings. Schiff called the operation a needless dilution of shareholders. The company chose paper over its own reserves.

His reasoning centers on a trap. According to the economist, Saylor avoids selling BTC because any meaningful liquidation would sink the price. The market, he claims, already understands that perfectly well.

“Saylor knows if he starts really selling Bitcoin, the price is gonna crash. Now, the problem is it’s gonna crash anyway because the market realizes the bind that he’s in, and even if he doesn’t sell, the market is gonna crash out from under him. But he is so nervous about selling Bitcoin that he’s willing to sell his own stock at a massive discount,” Schiff noted.

Follow us on X to get the latest news as it happens.

Why Does Schiff Expect Bitcoin to Reach $20,000

Schiff went further with his forecast. He identified resistance near $65,000 and support around $58,000, warning that a break below could drag Bitcoin under $50,000. His floor sits between $30,000 and $20,000, a level not seen for years.

Curiously, the critic admitted some regret. He said buying Bitcoin 15 years ago would have made perfect sense, though he feels absolutely no remorse about skipping the last five years of the rally.

“I don’t regret not buying it three, four, five years ago… But yeah, 15 years ago, sure, I should have bought it,” the economist confessed.

The timing of the criticism, however, looks awkward. Bitcoin trades just under $65,000 at the time of writing, up nearly 5% in the last week, according to BeInCrypto data.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The broader debate, however, extends beyond Schiff’s predictions. Analysts have been reassessing the corporate Bitcoin accumulation model, and Strategy sits at the center of that reevaluation.

Investors now scrutinize cash reserves, equity issuances, and funding conditions before assuming that future purchases will remain sustainable. Headline-grabbing buys no longer carry the same automatic credibility they once did in the market.

The post Peter Schiff Predicts a 70% Bitcoin Crash and Warns Holders Will Regret Not Selling appeared first on BeInCrypto.

Base network creator Jesse Pollak says he is stepping back from leading the Base App, after concluding that an earlier push toward social applications was a “wrong bet” for the Ethereum layer-2’s growth. In a post on X on Wednesday, Pollak argued that Base moved too slowly in areas that are now central to DeFi competition, including prediction markets and perpetual futures.

Pollak also said he will return leadership of the Base App to Coinbase, with Jordan Fish—better known on X as “Cobie”—taking over that role, while Pollak focuses on the Base blockchain itself.

Key takeaways

- Jesse Pollak said Base’s social-app strategy failed to deliver traction, and admitted the team made a “wrong bet.”

- Pollak cited Base’s lag behind competitors in scaled prediction markets and perpetual futures despite having offerings in both categories.

- Base App leadership is expected to shift back to Coinbase, with Cobie (Jordan Fish) resuming oversight of the product.

- The network’s current emphasis remains on finance-focused use cases such as trading, payments, tokenization, and AI agent tooling.

- Coinbase CEO Brian Armstrong recently acknowledged that “content coins” “didn’t work,” reinforcing the broader pivot away from social-first narratives.

From social to finance: Pollak’s rationale

Pollak’s comments provide a clearer explanation for the changes Base has been making earlier this year. Base initially positioned itself around social products, aiming to bring crypto to a wider audience through apps and creators. Pollak named examples of those early social thrusts, including Farcaster, Zora, and miniapps, reflecting a belief that engagement and content distribution could drive mainstream adoption.

However, Pollak said the market “disintegrated completely,” and that Base ended up behind in “key areas” that have become more important for users looking for financial utility. In his post, he pointed to Base’s decentralized derivatives presence—mentioning perps, with a nod to Avantis—and prediction markets, noting that both were “well behind scaled competitors.”

For investors and traders, the timing of this self-assessment matters: it signals a second attempt to align the chain’s product priorities with the demand that tends to concentrate liquidity, volume, and user retention in DeFi. Rather than doubling down on social distribution, Pollak frames the next phase around assets and trading-related infrastructure.

Leadership transition for the Base App

Beyond strategy, Pollak also addressed internal ownership. He said he will return leadership of the Base App to Coinbase, specifically under Jordan Fish (“Cobie”). At the same time, he said he will focus on the Base blockchain itself rather than the consumer-facing application layer.

That split highlights a common tension in L2 ecosystems: whether growth is best driven by consumer app ecosystems or by strengthening on-chain markets and standards that attract liquidity. By stepping back from the Base App, Pollak appears to be aligning resources more heavily toward the underlying chain and the financial primitives that developers can build on top of.

Coinbase’s earlier acknowledgment of “content coins”

Pollak’s post landed just days after Coinbase CEO Brian Armstrong said content coins “didn’t work.” Armstrong described it as a mistake that needed to be corrected, urging a shift in direction.

That acknowledgement aligns with Base’s earlier operational pivot. In February, Base sunset its Creator Rewards program and Farcaster-powered social feed as part of a move toward more tradable assets. Pollak had also previously characterized the Base App as an “imperfect Farcaster client,” underscoring that even when social-oriented features existed, they were not yet meeting the scale demanded by the market.

The Creator Rewards effort, launched in July 2025, was intended to turn engagement into rewards—making the network’s social activity economically meaningful. Pollak’s latest comments suggest that the rewards model did not overcome the broader competitive advantages held by chains and apps with more established financial depth.

What Base is building now: stablecoins, AI agents, and token standards

While Pollak criticized the earlier social emphasis, Base’s recent technical direction remains focused on tokenization and AI tooling—areas that can support both DeFi and new forms of user interaction.

Last week, Base activated its B20 token standard on mainnet, according to coverage earlier this month. The B20 framework introduces a native approach designed to support stablecoins, tokenized real-world assets (RWAs), and other fungible tokens.

In May, Base launched Base MCP (Model Context Protocol). The tool is intended to let users manage crypto directly from an AI model’s chat interface, and to interact with crypto protocols through the same interface, including Morpho, Moonwell, Uniswap, Aerodrome, Avantis, Bankr, and Virtuals. The practical implication is that AI agents may become a more natural interface layer over existing DeFi functionality, lowering the friction between user intent and on-chain execution.

Base has also said it is upgrading core systems ahead of an “AI agent economy” as part of a 2026 roadmap. In that context, Base highlighted RWA tokenization, stablecoins, and prediction markets as key growth areas—precisely the categories Pollak now says Base must compete in more effectively.

In his Wednesday post, Pollak said the goal is to position Base as a blockchain for global finance, aiming to be the place where the world’s money settles over the next century. While that statement is aspirational, it clarifies the narrative shift: the network is attempting to anchor itself in financial infrastructure rather than primarily in creator-led engagement.

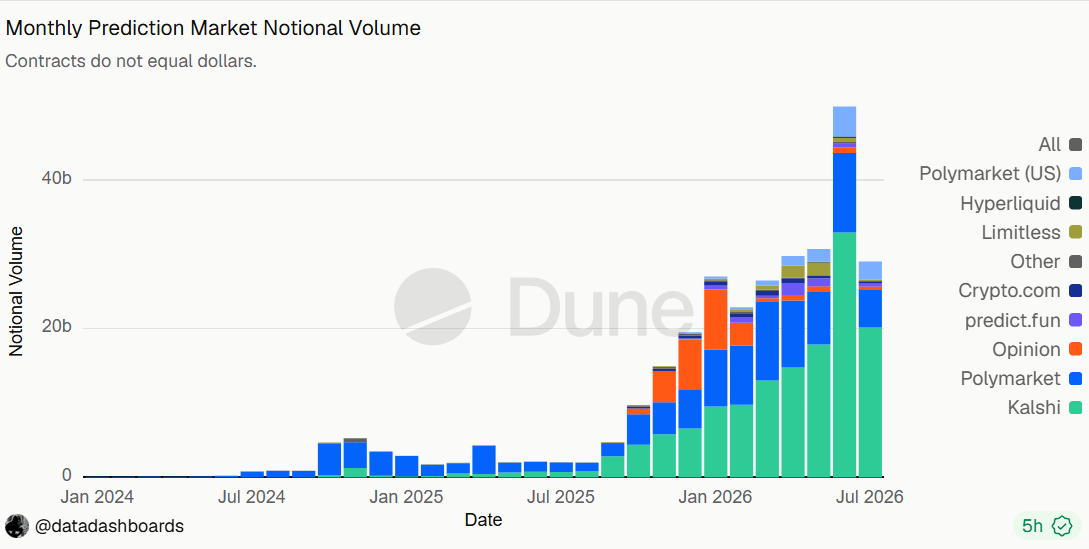

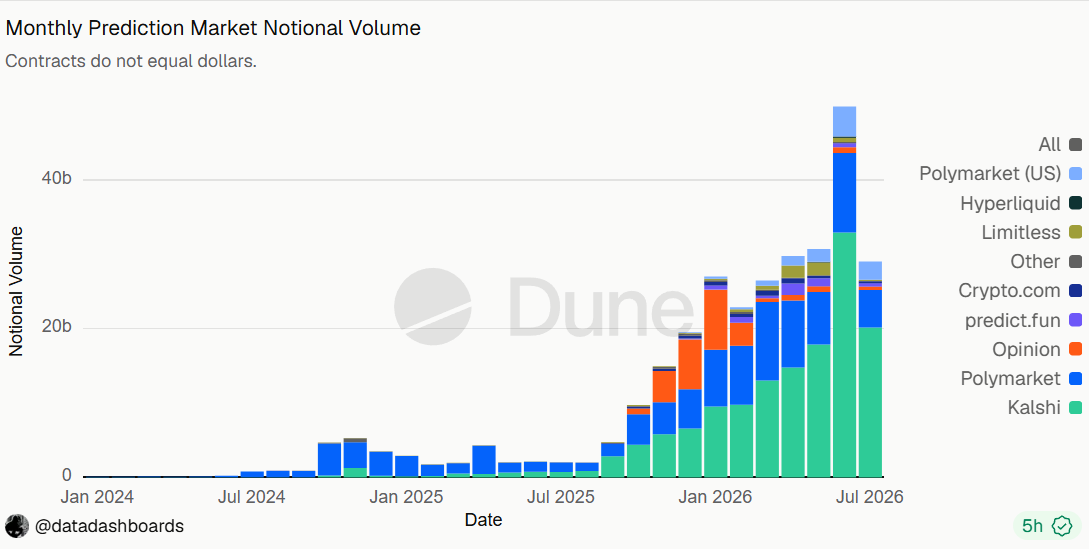

In parallel with the emphasis on trading and markets, the article noted that Limitless Exchange’s monthly notional volume is only a fraction of larger competitors, citing Dune Analytics. That kind of gap helps explain why Pollak pointed to derivatives and prediction markets as areas requiring faster scaling: if volume and notional activity remain comparatively small, users and liquidity providers have less incentive to route activity through the L2.

Why the pivot could matter next

Base’s latest moves may be best understood as a reallocation of attention toward where DeFi demand is already proven—liquidity, tradability, and execution. What remains uncertain is how quickly Base can close the scale gap in prediction markets and perpetual futures, and whether the B20 token standard and AI agent tooling will translate into measurable user activity rather than just product launches. Readers should watch for evidence of rising volume, broader adoption of stablecoin and RWA tooling, and whether Base App product changes under Cobie translate into renewed momentum.

Pump.fun has completed its first major team and investor token distribution after a one-year lockup ended.

Summary

- Pump.fun unlocked 57.279 billion PUMP tokens worth $86.49 million across 121 team and investor wallets.

- The first distribution follows a one-year lockup and begins a three-year vesting cycle for insiders.

- Unlocked tokens became transferable, but on-chain movements do not confirm recipients sold them into markets.

On-chain tracking showed 57.279 billion PUMP tokens, valued at about $86.49 million at the time of the transfers, moving to 121 wallets on July 15.

Wu Blockchain reported that the transfers marked the start of a three-year vesting period for team and investor allocations. The event makes a large amount of previously locked PUMP transferable, although wallet distributions alone do not show whether recipients intend to sell.

Source: EmberCN

Pump.fun distributes 57.279 billion PUMP

On-chain analyst Yu Jin tracked two large sources behind the distribution. One address released 52.039 billion PUMP worth about $78.58 million, while another released 5.24 billion tokens valued at approximately $7.91 million. The tokens then moved across 121 wallets.

The first distribution represents about 14% of PUMP’s current circulating supply of roughly 400 billion tokens. CoinGecko showed PUMP trading around $0.0016 after the unlock, with the token still recording a double-digit 24-hour gain when checked. The price action shows that an unlock does not automatically result in immediate selling.

Three-year vesting period begins after one-year lockup

The distribution comes one year after Pump.fun launched PUMP through a major token sale. As previously reported, the project’s original token allocation reserved 20% of supply for the team and 13% for existing investors.

The latest on-chain data indicates that those allocations have now entered their three-year release period after the initial one-year lockup. The full amount will not necessarily enter circulation at once. Vesting schedules typically release tokens in stages, while the recipients decide whether to hold, transfer or sell their unlocked assets.

Actual distribution follows closely watched PUMP unlock

The event had been on traders’ calendars before the first transfers appeared. As previously reported, scheduled data had pointed to an 82.5 billion PUMP unlock worth about $130 million around the end of the initial cliff. The first observed team and investor distribution instead moved 57.279 billion tokens across 121 wallets.

The difference shows why scheduled unlock figures and on-chain token movements may not always match on a specific day. Unlock calendars track when tokens become eligible for release, while blockchain transfers show when assets actually move between addresses. Further distributions may therefore remain possible during the wider vesting cycle.

PUMP supply pressure meets strong market activity

The unlock adds new potential supply at a time when PUMP continues to see active trading. CoinGecko recorded more than $100 million in 24-hour volume when checked, with the token’s market capitalization near $650 million and around 400 billion tokens listed as circulating.

Pump.fun has also used token buybacks to reduce available supply. Earlier crypto.news coverage tracked the program after it began buying PUMP from the market in 2025. The latest unlock creates the opposite supply force by making previously restricted team and investor allocations transferable.

The key question for the market is how recipients handle the newly available tokens. Distribution to 121 wallets does not prove that 57.279 billion PUMP has entered exchanges or been sold. Further wallet movements and exchange deposits would provide clearer evidence of whether the unlock is creating direct selling pressure.

With the one-year lockup now over, PUMP has entered a longer period of scheduled team and investor vesting. Traders will now watch subsequent distributions, exchange inflows and trading volume as more allocated tokens become available over the next three years.

TeraWulf shares have dropped more than 7% after New York ordered a one-year pause on new environmental permits for large-scale data centers.

Summary

- TeraWulf shares fell more than 7% after New York paused new environmental permits for large data centers.

- The company said its Lake Mariner and Lake Hawkeye projects are not affected by the governor’s executive order.

- TeraWulf continues expanding its AI business after signing a 20 year Anthropic lease expected to generate about $19 billion in contracted revenue.

According to an executive order signed by New York Governor Kathy Hochul on Tuesday, the state will temporarily stop issuing new environmental permits for certain large data center projects while regulators prepare a statewide framework to assess their environmental impact.

The order gives the Department of Public Service up to one year to complete a Generic Environmental Impact Statement, which will establish standards for future data center developments. The governor’s office said the review will examine electricity demand, water use and quality, and air quality before the moratorium is lifted.

Alongside the executive order, Hochul said she is also pursuing legislation to remove sales tax exemptions currently available to large data centers across New York.

Investors reacted quickly to the announcement. TeraWulf’s Nasdaq-listed shares closed down 7.08% at $19.41 on Tuesday.

Despite the market reaction, TeraWulf said the order does not affect its existing operations or development timeline in the state.

Paul Prager, TeraWulf’s founder and chief executive officer, echoed that view in a post on X, saying the company is evaluating on-site power generation for the Lake Hawkeye project, which he said aligns with the governor’s priorities for new electricity generation.

AI business continues to expand

While its New York projects remain unchanged, TeraWulf continues to grow its artificial intelligence and high-performance computing business.

Last week, the company signed a 20-year lease agreement with Anthropic for its Justified Data campus in Hawesville, Kentucky. TeraWulf said the agreement is expected to generate about $19 billion in contracted revenue over its full term.

As crypto.news previously reported, the company is also preparing to raise about $3.5 billion through leveraged loans and high-yield bonds to finance construction of the Kentucky AI campus. Bloomberg reported that Morgan Stanley is expected to lead the financing, although final terms have not been announced.

According to TeraWulf, the Kentucky facility will support about 401 megawatts of critical computing capacity, with initial operations expected in the second half of 2027 and full deployment planned for early 2028.

The company’s latest financial results also show how its revenue mix is changing. During the first quarter of 2026, TeraWulf reported $21 million in high-performance computing lease revenue, exceeding digital asset mining revenue of just under $13 million for the first time. Total quarterly revenue stood at $34 million, compared with $34.4 million a year earlier.

TeraWulf has said its AI infrastructure business is designed to provide more predictable contracted income while continuing to use its existing power and data center assets developed during its bitcoin mining operations.

Ark Invest has expanded its exposure to Circle and Block while cutting its Robinhood position, adding nearly $15.4 million worth of shares across the three companies.

Summary

- Ark Invest bought nearly $13.9 million worth of Circle shares and added to its Block position.

- The investment firm sold about $3.15 million worth of Robinhood shares as the stock moved higher.

- The latest trades continue Ark’s recent pattern of buying selected stocks after price declines while rebalancing portfolio holdings.

According to Ark Invest’s latest daily trading disclosure, the investment firm purchased 220,012 shares of Circle Internet Group across its ARK Innovation ETF (ARKK), ARK Next Generation Internet ETF (ARKW), and ARK Fintech Innovation ETF (ARKF). Based on Tuesday’s closing price of $63.22, the acquisition was worth about $13.9 million.

The same filing showed Ark also bought 19,029 shares of Block Inc. through ARKW and ARKF. Valued at roughly $1.52 million using Tuesday’s closing price of $79.99, the purchase came as the blockchain-focused fintech company ended the session up 1.61%.

On the selling side, the firm trimmed its Robinhood Markets position by 27,742 shares. With Robinhood closing 3.27% higher at $113.45 on Tuesday, the sale was valued at about $3.15 million.

Circle purchase comes after recent price slide

Circle edged up 0.35% on Tuesday but remained down 24.17% over the past month after a sharp decline earlier in July following the launch of the Open USD stablecoin project.

The recent weakness has divided analysts. While some continue to hold a positive view on the stablecoin issuer, Mizuho downgraded Circle to Underperform from Neutral and lowered its price target to $50 from $85. The brokerage said competition from Open USD could pressure Circle’s business over time.

The latest purchase also extends a pattern seen in recent weeks. On June 26, Ark increased its holdings in Circle, Coinbase, Bullish, and Robinhood after all four stocks finished the session lower, adding about 9,264 Circle shares, 9,014 Coinbase shares, 9,136 Bullish shares, and 35,023 Robinhood shares as prices weakened.

Earlier portfolio updates showed a similar approach. Ark bought roughly $18.4 million worth of Coinbase after the exchange operator’s shares had fallen for nearly a month, accumulated more than $4.4 million of Bullish stock during a multi-session decline, and added about $32.5 million worth of SpaceX following a drop of more than 16% from its post-listing peak.

Unlike the latest Circle purchase, the Robinhood transaction moved in the opposite direction. The brokerage’s shares gained more than 3% on Tuesday, and Ark reduced its position after previously buying additional Robinhood shares during periods of weakness.

Ark manages its exchange-traded funds under a portfolio rule that limits any single holding to no more than 10% of a fund’s assets. As stock prices change, the firm periodically rebalances positions to keep those weightings within its target range.

Ripple has burned another 10 million RLUSD tokens, extending a run of treasury operations that has reduced the circulating supply of its dollar-backed stablecoin.

Summary

- Ripple burned another 10 million RLUSD as circulating supply fell roughly 20% from May’s peak.

- Repeated treasury burns reduced RLUSD supply, though redemptions do not automatically signal weaker stablecoin adoption.

- Ripple continues expanding RLUSD through AI payments and growing XRP Ledger trading and settlement activity.

Blockchain data reported on July 14 showed the tokens moving from the RLUSD Treasury to a null address, permanently removing them from circulation.

The latest operation follows 10 million-token burns recorded on July 13, twice on July 10, and once each on July 9, July 8, July 7 and July 6. Ripple also minted 20 million RLUSD on July 6. The sequence shows active supply management as redemptions and new issuance change the amount available onchain.

RLUSD supply falls from its late-May peak

RLUSD’s market capitalization now stands near $1.52 billion. That is about $380 million below its late-May peak near $1.9 billion, representing a decline of roughly 20% in circulating value.

A lower stablecoin supply does not automatically show weaker adoption. Fiat-backed stablecoins expand when issuers create tokens against new dollar deposits and contract when holders redeem tokens for cash. Burns therefore record the removal of redeemed supply rather than directly measuring transaction demand or user growth.

Repeated burns follow active treasury management

The latest burn adds to several similar transactions within little more than one week. According to the reported Ripple Stablecoin Tracker data, at least 80 million RLUSD has been burned since July 6, while 20 million tokens were minted during the same period.

Those transactions show how quickly stablecoin supply can change when large holders redeem or issue tokens. The movements do not explain who redeemed the RLUSD or why. Ripple has not publicly tied the recent burns to one customer, market event or change in its wider stablecoin strategy.

Ripple expands RLUSD use beyond basic payments

The supply contraction comes as Ripple continues adding new uses for RLUSD. As per report, Ripple joined the x402 Foundation as a Premier Member as the Linux Foundation moved the open payment standard under formal governance.

The initiative focuses partly on machine-to-machine payments. XRP and RLUSD can support payments by AI agents through x402 on the XRP Ledger, giving autonomous software a way to settle transactions using blockchain-based assets.

Ripple also introduced new tools aimed at developers building AI payment applications. As previously reported, the company launched the XRPL AI Starter Kit in June, allowing developers to build software agents that can send and receive payments.

The company is positioning RLUSD as one settlement asset that developers can use for those transactions. The work adds another potential use case for the stablecoin beyond exchange trading and traditional cross-border transfers.

RLUSD remains active across the XRP Ledger

Recent supply reductions also follow a period of growing RLUSD activity on the XRP Ledger. Evernorth said RLUSD pairs had generated more than $2.5 billion in XRP Ledger trading volume since launch.

The figures included about $900 million in volume from the RLUSD/XRP pair over six months. Evernorth also reported that the XRP Ledger held slightly more than half of RLUSD’s circulating supply by late June.

That distribution can change as minting, burning and cross-chain transfers continue. However, the figures show that RLUSD remains active across trading and settlement markets even as its total circulating supply falls from its May peak.

Ripple has also continued expanding RLUSD through institutional and payment partnerships. A coverage showed that the company is increasingly connecting the stablecoin with automated payment infrastructure and emerging machine-to-machine transaction systems.

The latest 10 million RLUSD burn reflects another reduction in outstanding supply while Ripple continues building new payment and settlement uses. The market will now watch whether the current burn cycle continues or whether new minting resumes as demand changes.

At about $1.52 billion in market capitalization, RLUSD remains below its May peak. Future treasury movements could provide a clearer picture of whether the recent contraction represents a temporary redemption cycle or a longer period of lower circulating supply.

Base creator Jesse Pollak says he is stepping back from leading the Base App after admitting he made a “wrong bet” on social, leaving the chain to fall behind on prediction markets and perpetual futures.

In a post to X on Wednesday, Pollak said he had bet that creator, content and messaging apps would drive adoption, but instead the market “disintegrated completely.”

“We realized how our focus on social had meant that base had fallen behind in key areas that were now increasingly critical — we had perps (shoutout avantis!) and prediction markets (shoutout limitless!), but both were well behind scaled competitors.”

Pollak’s comments give further insight into the reversal of Base’s growth strategy earlier this year. While Base initially focused on social products such as Farcaster, Zora and miniapps to bring crypto to “a billion people,” Pollak said financial applications are the way forward for the network, with a focus on trading, payments and AI agents.

Limitless Exchange’s monthly notional volume is only a fraction of its larger competitors. Source: Dune Analytics

Pollak added he will be returning leadership of the Base App to Coinbase, under Jordan Fish, known on X as “Cobie,” while he focuses on the Base blockchain.

Coinbase CEO: “We messed up” on content coins

Pollak’s post came just days after Coinbase CEO Brian Armstrong acknowledged content coins “didn’t work,” prompting the company to pivot earlier this year.

“We messed up, time to turn the page,” Armstrong said on Monday.

In February, Base sunset its Creator Rewards program and Farcaster-powered social feed as part of a strategic shift to tradable assets.

Related: Moonbeam to pivot from Polkadot to Base, unveils AI agent framework

The Creator Rewards program launched in July 2025 and was intended to make the Ethereum layer-2 Base a more social ecosystem, where activity and engagement translate into earnings. Meanwhile, Pollak admitted the Base App was an “imperfect Farcaster client.”

Base’s work on stablecoins, AI agents

Last week, Base activated its B20 token standard on the mainnet, introducing a native framework for stablecoins, tokenized real-world assets (RWAs) and other fungible tokens.

In May, Base launched Base MCP (Model Context Protocol), a tool that lets users manage their crypto directly from an AI model’s chat interface and interact with crypto protocols such as Morpho, Moonwell, Uniswap, Aerodrome, Avantis, Bankr and Virtuals.

In April, Base said it was upgrading key systems in preparation for an AI agent economy as part of its 2026 roadmap. It highlighted real-world asset (RWA) tokenization, stablecoins, and prediction markets as being key growth areas in 2026.

“We’re going to build base into the blockchain for global finance and do everything we can to be the place that the world’s money settles over the next century,” Pollak said on Wednesday.

Magazine: Is Robinhood Chain’s success bullish or bearish for ETH the asset?

Ethereum-backed EthSystems has launched with support from Bitmine, SharpLink and Consensys CEO Joe Lubin, adding another independent organization to Ethereum’s institutional development network after the Foundation cut 54 roles.

Summary

- EthSystems has launched with backing from Bitmine, SharpLink and Consensys CEO Joe Lubin to build confidential infrastructure for institutional Ethereum.

- The company was spun out of the Ethereum Foundation by former members of its Institutional Privacy Task Force.

- The launch follows the Ethereum Foundation’s recent restructuring as independent organizations take on more ecosystem development roles.

According to an announcement from EthSystems on Tuesday, the for-profit company will build confidential infrastructure for banks, asset managers, and other regulated institutions using Ethereum.

Bitmine and SharpLink, two major Ethereum treasury companies, have backed the venture alongside Lubin, who co-founded Ethereum and later founded Consensys.

EthSystems was spun out of the Ethereum Foundation and was established by former Foundation employees Mo Jalil, Oskar Thorén, and Aaryamann Challani. The three founders previously worked on the Foundation’s Institutional Privacy Task Force.

EthSystems targets confidential institutional finance

The company said it will help financial institutions use public Ethereum without exposing sensitive information such as trading positions, transaction details, or client identities to the full network.

Its work is expected to include privacy systems based on zero-knowledge cryptography, which can verify transactions without revealing the underlying data.

“The business model is simple: bespoke consulting, focused on solving the hardest blockers for institutional adoption,” the team wrote.

“In practice, this means continuing a lot of the work we have been doing, only charging money for it,” it added. “Commercial engagements often require a commercial counterparty.”

Alongside paid consulting, EthSystems said it will continue publishing protocol specifications and contributing to open-source projects.

While working within the Institutional Privacy Task Force, the founders held hundreds of discussions with central banks, regulators, and financial institutions, according to the company.

Their previous work included private bonds using zero-knowledge proofs, confidential stablecoin transfers, private cross-chain settlements and the Ethereum Privacy Map.

“Our mission: help institutions build confidential systems on public Ethereum without giving up what makes Ethereum worth using,” the team wrote.

EthSystems has emerged during a major reorganization of the Ethereum Foundation and its technical teams.

On June 23, the Foundation cut 54 jobs, equal to about 20% of its workforce, after a months-long review of its spending, staffing and long-term responsibilities.

The organization reorganized its work into five divisions covering protocol, access, users, community, and institutional activity. Separate groups continue to manage operations and administration.

The Foundation said the restructuring would allow it to direct staff and resources towards responsibilities that it believes only the organization can perform.

“These decisions were hard, but they are necessary,” the Foundation said in June. “We must be resourced and organized in a way that allows us to focus on the critical work that only EF can, and therefore must, do in the coming years.”

In July, the Foundation also dissolved its Protocol Support team, which had coordinated All Core Developers meetings, network upgrade tracking, Ethereum Improvement Proposal support, Forkcast, and the Ethereum Protocol Fellowship.

Mario Havel, who worked with Protocol Support for more than five years, said he remained at the Foundation but confirmed that the rest of the team had been dissolved.

“I am still part of EF, continuing my work and figuring out what’s most needed in the future,” Havel wrote on X. “However, all of my team, Protocol Support, that I have been part of for 5+ years, has been dissolved.”

Independent Ethereum groups take on new roles

EthSystems joins Ethereum Institutional and EthLabs, two other independent organizations backed by Bitmine, SharpLink, and Lubin.

EthLabs is expected to take on major Ethereum protocol research and development work, while Ethereum Institutional has been positioned as a neutral contact point for financial companies building on the network.

Lubin previously told The Block that he expected at least three organizations to emerge from the Foundation as it concentrated on censorship resistance, open-source development, privacy, and security under its CROPS framework.

“As EF continues doubling down on cypherpunk fundamentals, especially with a focus on individuals, there’s room for an independent for-profit entity that can make different choices in the trade-off space,” EthSystems wrote.

Despite the restructuring, the Foundation’s protocol division remains responsible for Ethereum’s core technology, including privacy, security, decentralization and censorship resistance.

Ethereum developers are also continuing work on the Glamsterdam upgrade, which includes proposed changes to block construction, data access, and network performance.

Hyperliquid has added a pre-IPO perpetual market linked to ChangXin Memory Technologies, or CXMT, giving traders synthetic exposure to the Chinese chipmaker before its Shanghai debut.

Summary

- Hyperliquid listed a CXMT pre-IPO perpetual as the chipmaker prepares its July 27 Shanghai debut.

- CXMT’s contract price near $8 implied a $535 billion valuation, 526% above its IPO price.

- The market offers synthetic exposure, not ownership of CXMT shares listed on Shanghai’s STAR Market.

The contract, listed as xyz, traded near $8 on July 15, according to on-chain market data cited by Hyperinsight. Applied to CXMT’s expected post-IPO share count of 66.881 billion shares, that price implies a valuation near $535 billion, about 6.3 times its official IPO valuation.

Hyperliquid opens a synthetic route to CXMT

The CXMT contract operates through Hyperliquid’s HIP-3 framework, which allows outside deployers to create perpetual markets linked to assets beyond cryptocurrencies. These markets trade as derivatives rather than spot securities, so the CXMT contract does not provide ownership, dividends or voting rights in the Shanghai-listed company.

Individual investors on China’s STAR Market generally face a RMB 500,000 asset threshold and a two-year trading-experience requirement. Hyperliquid offers a separate synthetic market that can give eligible users price exposure without access to the underlying A-share. The distinction also means the contract price can differ sharply from CXMT’s official share price.

CXMT contract trades far above IPO valuation

CXMT priced its IPO at RMB 8.66 per share and expects to raise about RMB 57.9 billion, or $8.55 billion, before any over-allotment option. Reuters reported that the deal will be Asia’s largest IPO of 2026 so far and China’s biggest A-share semiconductor offering, surpassing SMIC’s 2020 share sale.

At the offer price, CXMT’s expected post-listing value is about RMB 579.2 billion, or roughly $85.5 billion. A synthetic price near $8 implies about $535 billion, placing the Hyperliquid contract around 526% above the dollar equivalent of the IPO price. The gap reflects pricing in a separate derivatives market and does not set CXMT’s official equity valuation.

China’s largest DRAM maker prepares for listing

CXMT is China’s largest DRAM producer and ranks fourth globally, behind Samsung Electronics, SK Hynix and Micron. Recent market estimates place its global DRAM share near 8%. The company has expanded as China invests heavily in domestic semiconductor production and demand for memory chips grows alongside artificial intelligence infrastructure.

Reuters also reported that CXMT secured a long-term memory supply agreement with Tencent worth more than RMB 20 billion, or about $2.94 billion. Investor subscriptions for the STAR Market offering begin on July 16, while the shares are scheduled to start trading in Shanghai on July 27. CXMT plans to use the IPO proceeds for production and technology investment.

Hyperliquid widens its real-world asset markets

Hyperliquid’s HIP-3 framework allows builders to launch perpetual markets linked to stocks, commodities and other real-world assets. A pre-IPO SpaceX contract also traded through the framework, showing how on-chain derivatives can create markets around companies before their public shares become available.

Hyperliquid has also expanded its connection to tokenized securities. As reported by crypto.news, Ondo Finance brought 35 tokenized U.S. stocks and ETFs to HyperEVM in June. Those products differ from the CXMT perpetual because tokenized securities can use structures backed by assets held through custodians, while perpetuals provide synthetic price exposure.

The CXMT market gives traders another route to speculate on a major public offering before its debut. Attention will now turn to whether the 526% premium narrows before subscriptions start and after the underlying shares begin trading on the STAR Market.

CFTC has ordered Kalshi to keep operating in Michigan despite the platform already unwinding sports event trades to comply with a state court order, deepening the dispute over who regulates prediction markets in the U.S.

Summary

- The CFTC ordered Kalshi to continue operating in Michigan despite a state court order requiring the platform to unwind sports event trades.

- Kalshi said it is caught between conflicting federal and state directives after complying with the Michigan court’s ruling.

- The dispute adds to a growing legal battle as states challenge Kalshi’s sports contracts while the CFTC asserts exclusive regulatory authority.

According to a July 14 order from the U.S. Commodity Futures Trading Commission (CFTC), Kalshi must not comply with Michigan’s directive to stop offering sports event contracts and should continue operating, even after the company said it had already reversed trades to satisfy the state court’s requirements.

The conflicting instructions have left the CFTC-regulated prediction market platform caught between state and federal authorities. In a statement posted on X, Kalshi’s head of enforcement and legal counsel, Robert DeNault, said the company had already unwound the affected trades because the Michigan court required it to do so.

“We are disappointed by this decision and believe it is unfair to Kalshi,” DeNault said.

“We already acted and unwound the trades, as the Michigan court order required us to do. We are being put in an impossible position, looking to follow state court orders that may contradict our federal regulatory obligations. We did not have a choice.”

A Kalshi spokesperson told Reuters the company is reviewing the CFTC’s order and weighing its next steps.

The regulator said Michigan became the first state to attempt to interfere with derivatives contracts after they had already been executed, describing the move as a challenge to the federal framework governing designated contract markets.

CFTC Chair Michael Selig said canceling completed trades could create uncertainty across financial markets.

“Canceling trades that have already been executed is an unprecedented step that risks a cascading effect on the entire marketplace and undermines the certainty in contracting that is a necessary component of a functioning market,” Selig said.

“The Commission will not allow states or state courts to bully registered entities into violating the Commodity Exchange Act and CFTC regulations,” he added.

Speaking on Fox Business last week, Selig also said it was “critical” that the CFTC preserve its authority over prediction markets.

He added that the agency had already sued nine states and would continue taking legal action against any state seeking to impose civil or criminal penalties on CFTC-registered exchanges.

Michigan case adds to national legal fight

The latest order follows a June 29 ruling by Ingham County Circuit Court Judge Rosemarie Aquilina, who temporarily barred Kalshi from offering sports event contracts to Michigan residents while the state’s lawsuit proceeds. The court warned the company it could face fines of up to $120,000 per day if it failed to meet geolocation requirements.

Michigan Attorney General Dana Nessel has argued that Kalshi’s sports event contracts operate as unlicensed gambling products under the state’s Lawful Sports Betting Act. Kalshi has maintained that its event contracts fall under the Commodity Exchange Act and therefore remain subject to the CFTC rather than state gaming regulators.

Michigan is one of several states challenging Kalshi’s sports contracts. Massachusetts has secured a preliminary injunction blocking the platform from offering similar products while litigation continues, and a court recently allowed state authorities to expand their complaint with new allegations, including claims that Kalshi targets users under 21.

New York has also handed Kalshi an early setback. Earlier this month, Judge Analisa Torres denied the company’s request for a preliminary injunction, allowing the state’s lawsuit to continue after finding Kalshi had not shown it was likely to succeed on its argument that federal commodities law preempts New York’s gambling laws.

As the legal disputes expand, the CFTC continues to argue that Congress granted it exclusive authority over federally regulated prediction markets, while several states maintain that sports event contracts function as sports betting and should remain subject to state gaming laws.

The whole operation took less than an hour, and the most valuable thing the attacker stole was not money. It was credibility. On Sunday, July 12, the verified X accounts of SpaceX and Starlink, with two million and 1.6 million followers between them, reposted promotional content for a memecoin called SCATMAN.

Summary

- Hijacked SpaceX and Starlink X accounts promoted SCATMAN, turning brand credibility into a temporary liquidity source.

- The attacker reportedly sold ten trillion SCATMAN across two wallets for about $135,000.

- The incident shows that social media logins can be a cheaper crypto attack surface than smart contracts.

- Robinhood Chain’s permissionless design enabled rapid token deployment, but also exposed retail users to brand-token scams.

- The core risk is not only stolen funds, but the erosion of trust in verified institutional accounts.

The repost sat in the normal flow of the accounts’ output, alongside routine posts about Grok model updates, with no defacement, no changed banner, none of the usual tells of a takeover. It simply looked like SpaceX had something to say about a token.Buyers responded the way buyers respond. In the first twenty minutes the token rose 575%. By the time the posts came down on Sunday evening and the accounts were restored, the attacker had minted ten trillion SCATMAN, sold the supply across two wallets for roughly 73.7 ether, and walked away with about $135,000. Everyone who bought on the strength of a SpaceX repost held a worthless token.

The dollar figure is almost embarrassing. A hundred and thirty five thousand dollars is a rounding error next to the eight figure hacks that define crypto’s security discourse, and it is nothing at all next to the $1.16 billion in bitcoin sitting on SpaceX’s own balance sheet. That gap between the scale of the brand exploited and the size of the payday is the actual story, and it points at something the industry has not solved: the cheapest attack surface in crypto is not a smart contract or a bridge. It is a login.

Every serious defense crypto has built assumes the attacker must beat cryptography, economics, or code. The July 12 attacker beat none of those. They beat a password, borrowed a decade of accumulated public trust for roughly forty minutes, and converted it directly into ether at the expense of anyone who believed what a verified account told them.

What happened, in order

The sequence, reconstructed from onchain analytics and screenshots circulated before the posts were deleted, is short enough to fit in a paragraph and repeatable enough to fit in a playbook.An account calling itself Sam Catman appeared, displaying an affiliation badge that falsely tied it to SpaceX’s artificial intelligence work. The name was a pun on Sam Altman, timed to the ongoing public feud between Elon Musk and the OpenAI chief executive, a feud that had produced a $150 billion lawsuit and had Musk himself posting about scamming the day before the breach. The joke did work that the token itself could not: it made the promotion feel like something SpaceX might plausibly amplify. Musk’s companies post irreverently. A crude swipe at a rival chief executive, delivered as a memecoin, sits within the observed behavior of the brand, and that plausibility was engineered rather than lucky.

The SCATMAN token was deployed on Robinhood Chain, the trading platform’s layer 2 network that had gone live eleven days earlier and permits anyone to deploy a token without approval. The SpaceX and Starlink accounts then reposted the Sam Catman promotion, complete with the contract address and ticker.

Trading exploded. Reported peak market capitalization varies sharply by source and by measurement window, from roughly $800,000 in the first twenty minutes to $2 million on some trackers to $32 million at the high water mark reported by onchain analysts, with twenty four hour volume around $5.7 million. The spread itself tells you something about the quality of the market: on a token this thin, market capitalization is a number generated by the last trade, not a measure of anything real.The attacker sold. Onchain analytics firm Lookonchain traced ten trillion tokens dumped for 59 ether, worth about $108,000, from one wallet, and a further 59.28 million tokens sold for 14.7 ether, about $27,000, from a second wallet controlled by the same actor. Liquidity drained. The price collapsed. The posts were removed, the Sam Catman account was suspended, and control of the SpaceX and Starlink handles was restored the same evening.

As of publication, neither SpaceX nor X has explained how the accounts were compromised. Robinhood has not commented on its chain hosting the token. Every figure in the paragraphs above comes from third party onchain analysis, not from any company disclosure, which is itself worth noticing: the only institution that produced a public account of what happened was the blockchain.

Credibility arbitrage is the business model

Strip away the specifics and the attack has one moving part. Attackers are not building audiences. They are borrowing them, for the length of a single post, and converting borrowed trust into ether before the loan comes due.The economics are brutal in their simplicity. A memecoin launched by an anonymous wallet reaches nobody. The same token, reposted by an account with two million followers that has spent a decade earning the right to be believed, reaches a market instantly. The attacker does not need the trust to last. They need it to survive for the length of a candle.

This is why the payday size is misleading as a measure of severity. The constraint on the attacker’s profit was not the audience or the credibility. Those were enormous. The constraint was market depth: there simply were not enough buyers with enough capital in the pool to absorb ten trillion tokens at a higher price. The attacker extracted essentially all the liquidity that existed. On a deeper chain, or with a slower response from Musk’s security team, the same attack with the same inputs produces a much larger number. The record supports that reading. When attackers seized the dormant account of Keith Gill, better known as Roaring Kitty, in May, they launched a token on Solana and cleared more than $600,000 in half an hour. When the Pump.fun account was compromised in February 2025, one wallet made over $135,000 in under a minute. A hijacked account belonging to former Malaysian prime minister Mahathir Mohamad produced $1.7 million in losses.

The pattern list is long and its membership is indiscriminate. The United States Securities and Exchange Commission’s own account announced a fake bitcoin ETF approval in January 2024, moving the entire market. Scroll co-founder Ye Chen’s account was taken over in January 2026. Pepe creator Matt Furie’s account pushed a scam token months later. World Liberty Financial co-founder Zach Witkoff, the leader of Myanmar’s junta, and a BBC presenter have all been used as unwitting distribution. What unites them is not an industry, a chain, or a security posture. It is a follower count.

The defense industry has no product for this. There is no audit that certifies a chief executive’s password manager. There is no bug bounty covering a social media platform’s session token handling. The security spend that protects a protocol treasury, multisig thresholds, hardware wallets, timelocks, all of it terminates at the edge of the chain, and the attack originates one layer above, in a consumer product operated by a company with no stake in crypto’s outcomes. The industry has outsourced its most important trust primitive to a social network and has no contractual relationship with it whatsoever.

Why the defenses that exist do not cover this

Crypto has spent years building defenses against a different threat model. Audits check contract code. Bug bounties surface protocol flaws. Formal verification proves that a program does what its specification says. Timelocks and multisigs guard treasuries, a lesson the industry learned expensively when a single vote drained a DAO, which crypto.news examined in its explainer on what a governance attack is. All of that machinery assumes the attack comes through the chain.

The SCATMAN attack came through a social media account. There was no contract to audit, because the contract did exactly what it was written to do. There was no protocol to exploit, because no protocol was exploited. Robinhood Chain worked as designed: it let someone deploy a token permissionlessly, and it let that token trade. Every component behaved correctly, and buyers still lost their money, because the failure happened in the layer nobody in crypto controls and everybody depends on, the layer where reputation is stored.

Consider what a diligent buyer could actually have done in the twenty minute window. Check the contract? It was a standard token; the exploit was the promotion, not the code. Check holder concentration? The attacker held everything, which describes most tokens in their first minutes and is not by itself proof of fraud. Check the liquidity lock? There was liquidity, briefly. Check the source? The source was SpaceX. That was the whole point.

The honest conclusion is that the standard retail checklist offers close to zero protection against this specific attack, because the checklist assumes the promotion is the least trustworthy input and the chain data is the most trustworthy. Here the chain data looked ordinary and the promotion looked impeccable. The only defense that works is a rule rather than an inspection: no verified account’s post, from any brand, is a reason to buy a token minted minutes earlier. That rule costs its holder every genuine celebrity token launch, which is a price most people should be delighted to pay.

The Robinhood Chain problem

The venue is not incidental. SCATMAN landed on a chain in its second week of life, and the chain’s condition shaped the outcome.Robinhood Chain launched on July 1 as a permissionless layer 2 aimed at onchain finance and real world asset tokenization. What arrived instead, at least first, was memecoins: more than 75% of trading volume in the opening week, with the network’s memecoin market capitalization briefly topping $244 million, more than $3 billion in cumulative decentralized exchange volume, and 19,586 new tokens created in a single day by July 13, second only to Solana. Cross chain interoperability provider Relay Protocol publicly warned about honeypot tokens proliferating on the network, coins hardcoded so buyers cannot sell or whose transfers route funds to an attacker, and said it was blocking them as they appeared.

That is the environment SCATMAN exploited: a young chain with real retail attention, minimal mature tooling, and an inflow of tokens far exceeding anyone’s ability to screen them. It is not a Robinhood specific failure. It is what permissionless launch infrastructure looks like at week two, and Solana’s own history through the rise of memecoin launchpads documents the same arc. The difference is the brand on the door. A chain carrying the name of a mainstream retail brokerage, whose users skew toward people who have never evaluated a token contract in their lives, inherits a duty of care that a purely crypto native chain never had, and the network’s design offers no obvious way to discharge it.

Robinhood’s silence on the incident is therefore the most interesting non-event of the week. The company did not deploy the token, did not promote it, and cannot in any technical sense prevent the next one. It also cannot escape the fact that a scam bearing SpaceX’s stolen credibility used its chain to reach its users. The gap between what a chain operator controls and what a chain operator is blamed for is about to become a live commercial question, not a philosophical one.

The tell that was there, and why it did not help

There was one genuine signal available in real time, and almost nobody could use it.The Sam Catman account was new. Its affiliation badge, the marker that ties an account to a parent organization on the platform, was fraudulent, claiming a link to SpaceX’s artificial intelligence work that did not exist. Someone who knew how badge inheritance works, who checked the account’s age, and who understood that a legitimate SpaceX subsidiary would not announce itself through a pun account, could have identified the fraud before buying.

That describes a vanishingly small population, and it describes them under conditions that made the knowledge useless. The window was twenty minutes. The signal required domain expertise in social media platform mechanics, not crypto. And the accounts amplifying the fraud were the exact accounts a user would check to verify it. The verification path led straight back to the attack.

This is what makes brand token crime structurally different from the failure modes retail has been trained on. A rug pull on a random token asks a buyer to evaluate a stranger and get it wrong. A hijacked account asks a buyer to evaluate an institution and get it right, then punishes them for the institution’s operational security failure. The buyer’s diligence was not insufficient. It was aimed at the wrong entity, because the entity that failed was never one they could inspect. The generic advice to check holder distribution and creator history, sound guidance across the meme coins landscape, simply does not reach a case where the creator’s history is a forged badge and the distribution looked normal for sixty seconds.

The case that this does not matter much

There is a serious argument that the industry should be relaxed about all of this, and it deserves a fair hearing.Start with the numbers. The total damage was $135,000, spread across an unknown number of buyers who chose to purchase a token named after a joke about a lawsuit, minted an hour earlier, on a chain eleven days old. Compare that to the $11 billion in crypto related losses the FBI’s Internet Crime Complaint Center reported in 2025, or the industrial scale of romance and investment fraud operations. Account takeover memecoin scams are, in aggregate, a rounding error against the frauds that destroy people’s lives.

Continue with responsibility. Nobody was tricked into revealing a private key. No wallet was drained. Buyers made a voluntary purchase of a speculative asset in an unregulated market on the basis of a social media post, which is a decision the market is entitled to price. The permissionless systems performed exactly as advertised: anyone can create a token, anyone can buy it, nobody is protected. That is the deal, and it is disclosed in every interface.

Add that the response worked. The accounts were recovered within hours. The posts were deleted. The fake account was suspended. Lookonchain published both wallet addresses, meaning the proceeds are now permanently marked and traceable, an outcome that traditional financial fraud rarely delivers. Exchanges can flag those addresses. Investigators have a starting point. Compare the transparency of that aftermath to a wire fraud of equivalent size, where the money simply disappears into correspondent banking. Upbit’s freeze of proceeds after a recent onchain treasury attack shows that marked funds are not merely symbolic, and exchanges do act on published addresses when the trail is clean enough.

Finish with proportion. The attack is self limiting. Its profit is capped by the depth of the pool it dumps into, and thin pools are thin precisely because the market has correctly assessed these tokens as worthless. The scam succeeds only against buyers who ignore every rule the industry has spent a decade writing down.None of that is wrong. It is also, taken together, an argument for doing nothing, which is why the counterargument matters more.

The case that it matters a great deal

The dismissive reading treats $135,000 as the measure of the harm. It is the measure of the attacker’s revenue, which is a different quantity entirely.The harm is the erosion of the only verification mechanism retail actually uses. Ordinary people do not read contracts. They read who is saying it. That heuristic, trust the verified account of a company that builds rockets, is the single most reliable signal available to a non technical person on the internet, and each successful hijacking teaches the market that the signal is unreliable. A world in which no institutional account can be believed is a world in which every genuine announcement, every legitimate product launch, every real partnership arrives pre-discounted. The industry is spending down a shared reputational asset it did not build and cannot replenish, one $135,000 withdrawal at a time.

Then consider the trajectory. This attack costs almost nothing to attempt, carries low apparent consequence, and produces a payday in minutes. The rate of attempts is a function of expected value, and expected value is rising as more mainstream brands acquire crypto surfaces. SpaceX now holds 18,712 bitcoin and trades as a Nasdaq-100 component whose price is discovered partly on crypto rails, a structural reality crypto.news examined when the stock joined the index. Every corporate account with a crypto adjacent story is now a live financial instrument, whether the company knows it or not, and the compromise of such an account is no longer a public relations incident. It is a market event.

Notice too what the attacker actually needed: no capital, no code, no confederates, and roughly one hour. Meanwhile, the defenders needed exactly what they did not have, which is a way to un-say something to millions of people faster than a bot can buy. Deletion is not a remedy when the trade has already cleared. The asymmetry is total: the attack executes at the speed of a repost, and the correction executes at the speed of a corporate security team noticing, escalating, and regaining access. In the interval, an irreversible ledger records everything.

And the regulatory exposure is asymmetric in an ugly way. Attackers face weak enforcement against pseudonymous wallets. The chains, the brokerages, and the exchanges hosting the activity face regulators who are actively deciding, this month, how much responsibility infrastructure operators bear for what runs on top of them. Every SCATMAN is evidence in that proceeding, and it is evidence that arrives conveniently packaged: a household brand, a retail brokerage’s chain, an unsophisticated victim class, and a perpetrator who will probably never be identified. The industry’s argument for permissionless infrastructure gets harder to make each time permissionless infrastructure is the medium through which a stolen brand robs retail buyers, and the regulatory window in which those arguments are being weighed is measured in weeks, not years.

What would actually change the math

Nothing in the current toolkit addresses the root cause, which is that a verified account’s authority transfers instantly and totally to whoever controls the login at a given moment.

The platform side is straightforward and unattempted. Hardware key enforcement for accounts above a follower threshold. Delay windows on posts containing contract addresses from accounts that have never posted one. Loss of affiliation badge inheritance for accounts created within a defined period. None of these is technically hard. All of them are commercially unattractive to a platform that monetizes velocity, and none has been implemented despite three years of nearly identical incidents. The absence is not a technology gap. It is a revealed preference about whose losses count.

The chain side is more interesting because it cuts against the ideology. A permissionless chain cannot vet tokens, but the interfaces on top of it can, and increasingly do: Relay Protocol’s honeypot blocking is exactly that, a voluntary screening layer occupying the gap between what the protocol permits and what users can survive. Expect more of it, and expect the resulting fight over whether interface level screening is prudent stewardship or the reintroduction of the gatekeepers the entire architecture was built to remove.

The user side is the only one available today, and it is a single sentence: the credibility of the messenger tells you nothing about the token, because the messenger’s credibility is exactly what is being stolen. A verified account promoting a token minted minutes ago is not evidence of legitimacy. Under current conditions it is closer to evidence of the opposite.

The ledger nobody wants to read

Here is the uncomfortable arithmetic of July 12. A brand worth over a trillion dollars in public market value was used, without consent, to sell a worthless asset. The theft netted about the price of a modest car. The proceeds are permanently visible on a public ledger. The victims have no recourse. The platform has said nothing. The chain has said nothing. The brand has said nothing. And the mechanism that made it all possible remains completely intact, available to anyone who compromises the next account.

The scam economy has discovered that the most valuable asset in crypto is not any token. It is a moment of unearned belief, and belief is the one thing on this market with no smart contract protecting it, no audit verifying it, and no liquidity lock keeping it in place. Until that changes, $135,000 is not a measure of the damage. It is a receipt for the trial run.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Figures on wallet activity, token supply, and market capitalization derive from third party onchain analytics reported by Lookonchain, GeckoTerminal, and DEX Screener, not from official company disclosures, and reported peaks vary between sources. No company involved has confirmed the breach mechanism. Details reflect information current as of July 14, 2026, and are subject to change. Always do your own research.

Argentina players celebrate beating England with ‘Falklands are Argentinian’ banner

FCC Plans To Repeal 39% TV Ownership Cap

Homeowner’s fury after neighbour builds elevated platform that looks like a ‘East German lookout tower’ – which overshadows her garden and has killed her plants

-

Fashion7 days ago

Fashion7 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics14 hours ago

Politics14 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos1 day ago

News Videos1 day agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech1 day ago

Tech1 day agoDark Secrets Emerge When Jailbreaking LLMs

-

Sports5 hours ago

Sports5 hours agoNew Cornerback Enters Vikings Trade Rumor Mill

-

Tech7 days ago

Tech7 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

NewsBeat7 days ago

NewsBeat7 days agoMajor update after Huntingdon train attack as man enters plea

-

Entertainment9 hours ago

Entertainment9 hours agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech7 days ago

Tech7 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Entertainment7 hours ago

Entertainment7 hours agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World7 days ago

Crypto World7 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

NewsBeat4 hours ago

NewsBeat4 hours agoWatch: Is Donald Trump facing a popular backlash on immigration?

-

Crypto World2 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

You must be logged in to post a comment Login