Crypto World

Shiba Inu price slips as exchange outflows offset Japan boost

- 64 billion SHIB have left crypto exchanges today, so far.

- SBI inherited 1.111 trillion SHIB through the Coinhako acquisition.

- Exchange reserves climbed to 86.497 trillion SHIB.

Shiba Inu (SHIB) is navigating two very different stories at the same time.

On one side, the token is gaining more exposure in Asia through a major corporate acquisition involving one of Japan’s largest financial groups.

On the other, fresh on-chain data points to renewed selling pressure as more SHIB moves onto exchanges.

The conflicting signals have left the token under pressure, with buyers struggling to regain momentum despite positive adoption news.

Exchange outflows add pressure to SHIB price

Shiba Inu traded around $0.00000409 after extending its recent decline, reflecting a broader period of weakness across the cryptocurrency market.

The latest on-chain data suggests that exchange activity has become a key factor behind the token’s muted performance.

Data from CryptoQuant showed that 173.45 billion SHIB flowed into cryptocurrency exchanges over the latest 24-hour period, while 271.09 billion SHIB left exchanges.

That resulted in a negative exchange netflow of 97.64 billion SHIB, indicating that more tokens exited trading platforms than entered them.

The latest figures also showed that exchange reserves climbed to 86.497 trillion SHIB, highlighting a larger pool of tokens sitting on trading venues.

During the previous 10-day period, on-chain data showed more than 1.4 trillion SHIB leaving centralised exchanges.

Those outflows had reduced the amount of SHIB immediately available for sale and were viewed as a stronger accumulation signal.

Instead, the latest data points to a reversal in that trend.

Combined with the recent decline in price, the higher exchange balances illustrate the increased selling activity that has weighed on SHIB over recent trading sessions.

Japan expansion strengthens SHIB’s long-term visibility

While on-chain data has turned less favourable in the short term, Shiba Inu has simultaneously received a significant boost in institutional exposure through developments in Japan and Singapore.

SBI Holdings, one of Japan’s largest financial services companies, recently completed its acquisition of Coinhako after receiving approval from the Monetary Authority of Singapore (MAS).

The acquisition also transferred custody of approximately 1.111 trillion SHIB, valued at roughly $4.5 million at the time of the transaction.

The holdings were already part of Coinhako’s customer and exchange reserves, meaning the acquisition did not represent a fresh purchase of SHIB from the open market.

Coinhako manages a digital asset portfolio worth more than $164 million, with SHIB ranking among its larger cryptocurrency holdings.

Following the acquisition, SBI expanded its footprint in Southeast Asia while adding another regulated platform that offers SHIB trading against both the Singapore dollar (SGD) and the US dollar (USD).

The transaction adds to Shiba Inu’s growing presence within regulated Asian cryptocurrency markets.

However, the increased visibility has yet to translate into stronger price performance as traders continue to focus on short-term market activity.

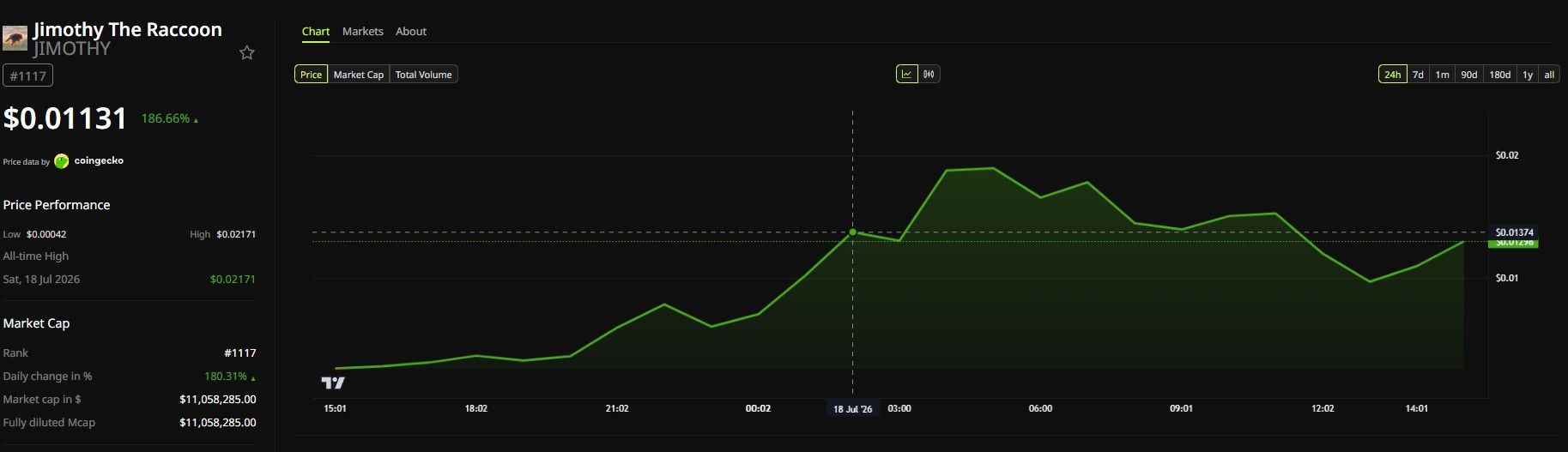

Jimothy The Raccoon (JIMOTHY), a Solana meme coin named after a viral Seattle raccoon, jumped 186% in 24 hours. Live BeInCrypto market data puts its market cap near $11 million.

Anonymous developers launched the token this week. Clips of the animal’s odd shape had already spread across social media, and traders piled in within hours of its Solana debut.

A Raccoon Named Jimothy Became an Overnight Icon

Seattle resident Kiana Hall filmed the raccoon near a Ballard neighborhood Goodwill earlier this week.

Marcie Logsdon, an associate professor at Washington State University’s Veterinary Teaching Hospital, said the raccoon likely has short spine syndrome, a rare congenital condition that shortens the spine and limits mobility.

“I was surprised and honestly a little bit inspired that he is that resilient”

The moment echoes a recent meme coin frenzy triggered by a hoax about Binance founder Changpeng Zhao. In that case too, a viral clip preceded a same-day token launch.

Pump.fun Trending Page Turned Attention Into Trading Volume

Anonymous creators listed JIMOTHY on Pump.fun. The platform’s trending page then exposed the token to a wide pool of Solana traders within hours.

Pump.fun’s official account then reposted the token on X, pushing it in front of an even larger trading audience. A dedicated subreddit and a wave of fan merchandise followed. Tattoo artists even offered discounts for raccoon-inspired ink.

The launch also arrived during a broader Pump.fun trading rebound. The platform’s share of profitable traders has climbed for four straight months.

Meanwhile, Solana network activity has jumped even as the SOL token itself struggles. Meme coin launches keep pulling in fresh volume.

Analysts Warn the Rally May Not Hold

JIMOTHY’s trading volume topped $36 million in the past day. Its price has climbed more than 50-fold from its low to an all-time high of $0.0217, according to live rankings data.

The token still ranks 1,117th by market capitalization, tiny next to Solana’s blue-chip names, and its supply sits near one billion coins.

However, tokens built on viral animal moments rarely hold their gains once the news cycle fades.

The pattern already played out this year in a World Cup meme coin rally tied to footballer Erling Haaland. A similar narrative-driven token rally followed Pentagon UFO files, and both cooled within weeks.

The post Jimothy The Raccoon Solana Token Climbs 186% After Viral Meme Fame appeared first on BeInCrypto.

Berkshire’s Equity Portfolio Is Rallying, but the Apple Sales Still Sting

Coinbase CEO Brian Armstrong briefly swapped his X profile picture for a cartoon mascot. The move sent BRIAN, a meme coin on Coinbase’s Base network, surging. Its market cap jumped from under $1 million to $37 million in hours.

The token is officially named Coinbase Man. Developers sent roughly 80% of its 1 billion supply to Armstrong’s wallet at launch. The rally collapsed once Armstrong reverted to his original profile picture, a CryptoPunk NFT.

The Rally Behind BRIAN’s Surge

BRIAN’s climb followed a familiar pattern. A single social signal from a recognizable figure can move markets faster than any product update. Traders read Armstrong’s profile swap as tacit approval.

The reaction echoed how celebrity-driven meme coin rallies have played out elsewhere this year. It also followed a rockier stretch for Base, whose earlier content coin experiments had already left users burned.

Historically, executive gestures have moved token prices well before fundamentals catch up. Volume on decentralized exchanges spiked within minutes, and the token’s price climbed roughly thirty-sevenfold from its starting point.

However, neither Coinbase nor Armstrong endorsed BRIAN directly at any point.

BRIAN’s Reversal

Momentum reversed within hours. Armstrong swapped his picture back to his usual CryptoPunk, and liquidity for BRIAN thinned almost immediately. The token’s market cap fell by more than 90%, to near $1.3 million, according to Coinbase’s price page.

Meanwhile, trading volume remained elevated at around $12 million over 24 hours. That gap suggested traders were exiting rather than holding through the drop.

The reversal also arrived during a stretch of Coinbase controversies, including its recent AI prediction market dispute. Therefore, the episode resembled a narrative that overheated rather than a coordinated rug pull.

What the Crash Signals for Base

The swing raises questions about which network retail traders trust next, especially as rival chains’ meme coin volumes draw growing attention. Armstrong has separately criticized restrictive investor rules, arguing that regulation should protect rather than exclude smaller traders.

The contrast is notable. His comments favor retail access, yet BRIAN’s collapse shows how quickly that access can turn costly. The episode suggests that when executives even casually gesture toward a token, retail money follows quickly, regardless of the token’s backing.

The post Coinbase CEO Changed His Profile Picture and This Meme Coin Soared 37x appeared first on BeInCrypto.

Amazon Web Services (AWS) confirmed that a display bug caused some customer bills to be displayed in the trillions. In a few cases, estimates reached the quadrillions of dollars.

AWS Support said an initial rollback attempt failed to fix the error right away. The bug hit the Billing Console’s estimate tools, not actual invoices.

How Amazon’s Billing Console Broke

A faulty calculation entered AWS’s estimated billing subsystem and multiplied normal usage by absurd totals. Customers whose monthly bills typically run in the hundreds suddenly saw projections with 15 zeros.

This is not AWS’s first reliability scare this year. In May, an AWS data center outage disrupted trading at Coinbase, a major crypto exchange.

A Bitcoin price display glitch hit Revolut the same month. Both cases show how a single backend fault can ripple through products that millions of people use daily.

AWS also signed a $6 billion Snowflake AI infrastructure deal in May, a sign of its scale in enterprise computing. Therefore, a pricing bug at this scale draws attention well beyond AWS’s regular customer base.

Amazon’s “Very Slight Miscalculation”

Amazon’s technical teams continued working on the reporting issue after the rollback proved insufficient. The company said it expects corrected figures to appear soon.

Rather than stick to a dry apology, the official AWS account on X leaned into the absurdity of the numbers. It called the error a typo and a “slight miscalculation,” then added “very slight” for effect.

The post closed with a wink, asking customers what they planned to do with their imaginary trillions.

Amazon reiterated that no manual steps are required and that the bug affects estimates only, not billed amounts.

A Pattern of Automated Errors

The incident lands amid a broader run of automation mishaps at major platforms. Coinbase faced criticism this month over an AI prediction market error that surfaced a false World Cup result.

Meanwhile, AI mega-cap earnings season volatility has trading desks watching cloud providers closely for stability.

As AWS backfills accurate data across its dashboards, the episode raises a question about automated systems. How much scrutiny should these systems face before reaching customers?

The post Amazon AWS Apologizes After Quadrillion-Dollar Glitch Terrifies Cloud Users appeared first on BeInCrypto.

TradFi institutions are adopting blockchain to improve their existing operations, not because they have embraced decentralization, venture capital firm a16z said in its latest report.

The technology helps lower operating costs, speed up settlement, expand distribution, and “tighten its grip” on customer relationships, which makes it a practical business tool rather than an ideological shift.

TradFi’s Blockchain Push

Institutions are not blending into DeFi as it exists today. Instead, a16z stated that they are adopting only the elements of DeFi that fit their regulatory, operational, and risk requirements while leaving behind features that do not. This selective approach is reshaping blockchain-based finance into something different from both traditional finance and current DeFi.

The result is an emerging form of programmable financial infrastructure designed to meet institutional needs while using the technology as its foundation.

According to a16z, initiatives such as JPMorgan’s permissioned blockchain for institutional deposits and tokenized money market funds from BlackRock and Franklin Templeton are not examples of institutions embracing DeFi. Instead, they are using blockchain to improve existing financial services like interbank settlements, fund subscriptions, and yield-bearing products.

They benefit from blockchain features such as programmability, transparency, and atomic settlement while intentionally avoiding core DeFi principles like open access, pseudonymity, and trustless execution. The focus is on making traditional financial infrastructure more efficient rather than adopting decentralized finance in its original form.

Crypto Must Look Beyond Wall Street

The blockchain capabilities now being adopted by institutions were first developed in open, permissionless ecosystems rather than inside banks or traditional financial firms. Those environments allowed developers to test new financial models and infrastructure. As a result, institutional adoption is largely built on innovations that originated in the open crypto ecosystem.

The report argued that the industry should not focus too heavily on banks and asset managers simply because they are major customers. While traditional financial institutions represent an important source of demand, they do not define the industry’s full potential, and opportunities beyond TradFi should not be overlooked.

“Designing for institutional requirements is a legitimate and valuable pursuit, but it is only one lane, not the whole road.”

The post a16z Reveals What TradFi Really Wants From Blockchain appeared first on CryptoPotato.

France’s gambling regulator, the Autorité Nationale des Jeux (ANJ), ordered internet service providers to block Polymarket on July 16, treating the prediction market as an illegal gambling site rather than a financial trading venue.

The ANJ said earlier restrictions had failed to keep French users off the platform. Polymarket drew 578,751 visits from 205,057 unique visitors in France in June, according to Similarweb data cited by the regulator, despite a ban on financial transactions in place since November 2024. A VPN was enough to bypass it.

The homepage remained accessible, allowing users to view live markets and odds. The ANJ said the real-time odds display promoted an unauthorized gambling service.

“The site’s homepage, which dynamically displays real-time odds for various events open to betting, thus serves as a major channel for disseminating and promoting Polymarket’s offerings, even though the site’s operations are not authorized in France,” the regulator wrote. Fines can reach 100,000 euros ($114,380).

Polymarket didn’t immediately respond to a comment from CoinDesk.

The ANJ also cited a complaint from France’s weather service, Météo-France, over a tampered temperature sensor tied to weather-based bets, prompting the Paris prosecutor’s cybercrime unit to open an investigation on May 4.

Zerodha co-founder Nikhil Kamath and Coinbase CEO Brian Armstrong warned that the sky-high valuations of premium AI companies like OpenAI and Anthropic face a massive structural threat.

The alarm arrives amid growing investor skepticism, as both leaders compared today’s AI frenzy to the dot-com crash and past crypto bubbles.

Why Kamath Would Short Every AI Company Today

Speaking on the “People by WTF” podcast, both leaders drew direct parallels between the current AI boom, the 2000s dot-com collapse, and standard crypto market bubbles.

Their shared concern centers on expensive proprietary models losing ground to cheaper alternatives.

Kamath framed the risk in personal, investor terms. He said shorting every private AI company today could, in five years, make him money, comparing the moment to the Internet bubble.

“Like me, the stock trader investor, I’m starting to feel at this point that if I were to take every private company in AI and short their stock today, in five years, I might make money… It feels a bit like… the ‘Internet bubble’,” Kamath said.

Follow us on X to get the latest news as it happens.

The Zerodha co-founder also expects the industry to fragment. A market dominated by a few American giants would give way to a regional, self-reliant economy built through reverse-engineering and rapid local development.

Under that view, individual nations stop importing expensive models and build their own. India would run its own domestic copy, with the tokens and energy sitting locally, functional enough for everyday use even if not cutting-edge.

“If the world goes in that direction, I don’t see the reason to pay the multiples that these private companies have today,” Zerodha co-founder argued.

What is the 99% Cheaper Threat Armstrong Describes

Armstrong, notably, agreed with that market assessment. He pointed to a stark cost gap between elite frontier labs and the open-source models trailing right behind them.

Top-tier labs spend billions building the next breakthrough. Open-source alternatives, roughly six months behind, reach the market at a tiny fraction of that price.

The Coinbase CEO put a figure on it. Open-source models run about six months behind and cost up to 99% less for inference, so a larger share of workloads could shift toward them.

He drew a clear line between two futures. Elite frontier models stay valuable for highly specialized tasks like discovering new physics, but average consumers and businesses turn intensely price-sensitive.

“It makes me a little nervous when I see these valuations growing this fast as well. Like I’ve seen things like this happen before in crypto. They correct, and then there’s real value under it, so then they grow later,” Armstrong noted.

Once standard models run cheaply on everyday commodity hardware, the corporate defenses protecting high-value AI companies could dissolve entirely. That erosion sits at the heart of the warning.

Armstrong closed on a cautious note. Fast-growing valuations make him nervous, echoing patterns he witnessed in crypto, where prices corrected before real value emerged and growth resumed later.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The post Billionaire Investor Just Revealed the AI Bet That Could Pay Off Big in 5 Years appeared first on BeInCrypto.

Ethereum’s best marketing line was that using it destroyed it, that every transaction burned ETH and shrank the supply. Then the network solved its scaling problem, activity fled to layer 2s, and the burn collapsed. The scaling worked. The scarcity did not survive it.

Summary

- Ethereum’s “ultrasound money” thesis held that EIP-1559 fee burning would outpace new issuance, making ETH deflationary and a superior store of value to Bitcoin.

- It worked briefly after the 2022 Merge. Then the March 2024 Dencun upgrade moved activity to layer-2 rollups paying near-zero fees, and the daily burn collapsed from thousands of ETH to as low as 50 to 70.

- ETH has since been mildly inflationary, with net supply growth around 0.2% to 0.8% annually depending on the period, reversing the deflation the thesis promised.

- The December 2025 Fusaka upgrade added EIP-7918, a blob fee floor designed to restore a minimum burn. Fidelity modeled it would have added roughly $78.6 million in burn across 93% of days since 2024.

- The deeper tension is unresolved: a cheap, scaled Ethereum burns less than a congested, expensive one, so the network’s success as infrastructure works against its scarcity as an asset.

For about eighteen months, Ethereum had the best story in crypto, and the story was a paradox: the more people used the network, the rarer its token became. Every transaction burned a little ETH, and when the network was busy enough, it burned more than it created. Supply went down. The community called it ultrasound money, a deliberate jab at Bitcoin’s “sound money,” complete with a bat emoji and a movement.

For a while, the data backed it up. Then Ethereum did the thing it had promised to do for years, which was to scale, and scaling broke the story. Activity moved to layer-2 networks that pay almost nothing to the base chain, the burn collapsed, and ETH quietly went inflationary again. This is the story of how Ethereum’s greatest technical success dismantled its best economic narrative, and whether a December upgrade can put the pieces back.

What ultrasound money actually meant

The mechanism is worth getting exactly right, because the whole debate turns on it.

In August 2021, Ethereum activated EIP-1559, which changed how transaction fees work. Instead of paying miners directly, every transaction now pays a base fee that is burned, permanently removed from circulation. The busier the network, the higher the base fee, and the more ETH destroyed. On its own, that is just a fee-burning mechanism. It became a monetary thesis when Ethereum switched from proof-of-work to proof-of-stake in the September 2022 Merge, which cut new ETH issuance by roughly 90%, because the network no longer had to pay energy-intensive miners.

Put the two together, and you get the ultrasound thesis. Issuance dropped to a trickle after the Merge. Burning continued with every transaction. If burning exceeded issuance, total ETH supply would shrink over time, making the asset deflationary. And a deflationary asset with growing demand should, in theory, appreciate. Ethereum would become harder money than Bitcoin, whose supply still grows, hence “ultrasound.” The tracking site ultrasound.money existed to display exactly this: supply ticking down, day by day.

For a stretch after the Merge, it happened. Supply fell back toward and below the level it sat at during the Merge itself. Burns outpaced issuance. The narrative was not hype; it was, for that window, an accurate description of the data. That is what made it powerful, and what made its reversal so awkward.

How scaling broke it

The break came from Ethereum solving its most famous problem, and the irony is total.

Ethereum’s scaling strategy is to push transactions off the expensive base layer and onto layer-2 rollups, networks like Arbitrum, Optimism, and Base that process transactions cheaply and then post compressed data back to Ethereum for security. The base layer becomes a settlement and data-availability layer; the rollups handle the actual activity. This is the roadmap Ethereum has pursued for years, and it works.

The March 2024 Dencun upgrade was the pivotal moment. It introduced EIP-4844, “blob” transactions, a separate and far cheaper data channel for rollups to post their data. Costs for layer 2s dropped by a factor of 10 to 100. Activity that used to happen on mainnet, paying mainnet fees and burning mainnet ETH, moved to rollups paying blob fees that were, in practice, close to zero because blob space was massively oversupplied relative to demand.

The effect on the burn was immediate and severe. Before Dencun, Ethereum burned thousands of ETH per day during busy periods. After Dencun, daily burn dropped to as low as 50 to 70 ETH. The base layer had lost its primary fee source. With issuance running around 1,700 ETH per day and burn collapsing well below that, the equation flipped: Ethereum began creating more ETH than it destroyed. By various measures across 2025 and into 2026, net annual inflation ran somewhere between roughly 0.2% and 0.8%, depending on the window. ETH supply crossed back above its Merge-era level. The deflation was over.

The mechanism that made ultrasound money true, EIP-1559 burning at scale, had not been removed. It had been bypassed. The activity simply moved to a layer where the burn does not happen in any meaningful amount. Ethereum scaled successfully and, in doing so, severed the link between usage and scarcity that the entire thesis depended on.

The bull case: it still works, just differently

The response from Ethereum’s defenders is not denial. It is reframing, and parts of it are genuinely strong.

The first point is that elastic scarcity is the actual feature, not permanent deflation. Ethereum was never designed to deflate forever at a fixed rate. It was designed to burn in proportion to demand, which means it becomes deflationary when the network is busy and mildly inflationary when it is quiet. During periods of high mainnet activity, above roughly 16 gwei average gas, burn still exceeds issuance, and ETH still goes net deflationary, temporarily. The mechanism works exactly as designed; it is just that a scaled network spends more time in the quiet regime. In this reading, ultrasound money was always conditional, and the condition is demand, not a promise.

The second point is that issuance is still radically lower than before. Even mildly inflationary, Ethereum issues roughly 90% less ETH than it did under proof-of-work. Compared to Bitcoin, which currently inflates at around 0.8% annually on a fixed schedule, Ethereum’s roughly 0.2% net inflation in calmer periods is actually lower. Both assets inflate in 2026; Ethereum, by some measures, inflates less. The “harder than Bitcoin” claim survives in a narrow, technical form even without net deflation.

The third point is that the supply figure overstates the sell pressure. Roughly 28% to 30% of all ETH is locked in staking, earning yield and not circulating. The tradeable float, ETH actually available on exchanges, is meaningfully smaller than the headline supply number, and it shrinks as more ETH is staked. A modestly inflating total supply with a large and growing staked portion is a very different pressure than the raw inflation number suggests. Demand from ETFs, treasury companies, and staking can absorb 0.2% inflation without difficulty.

And the fourth point is simply that the store-of-value case never rested on deflation alone. As long as demand for Ethereum’s blockspace, its role as settlement for stablecoins, tokenization, and DeFi, grows faster than supply, price can rise regardless of whether supply ticks up 0.2% a year. Scarcity was a nice story. Utility is the real thesis.

The bear case: the narrative was load-bearing

The skeptical reading is that the ultrasound story was not just marketing, that it was doing real work in the investment case, and that losing it matters more than the reframing admits.

The blunt version comes from the on-chain data and the people watching it leave. Daily network fee revenue on Ethereum fell from near $40 million in early 2025 to a local low around $10 million in 2026. That is not just a burn problem; it is a value-accrual problem. If the base layer captures little fee revenue because activity happens on rollups that pay it almost nothing, then holding ETH is a bet on an asset whose own network is monetizing its users poorly. Some analyses have tied this directly to developer attrition and reduced whale support, framing the end of ultrasound money as the end of a period when ETH had a clean, quantifiable reason to appreciate.

The deeper problem is structural and hard to argue away: a scaled, efficient Ethereum is less deflationary than a congested, expensive one. This is the tension at the center of the whole debate. The very thing that makes Ethereum better as infrastructure, cheap transactions, more capacity, activity on fast rollups, is the thing that reduces the burn. Ethereum cannot simultaneously be the cheap, high-throughput settlement layer it wants to be and the fee-burning deflationary asset the ultrasound thesis needed. Those are in direct conflict, and the roadmap chose scaling. The asset thesis was, in a real sense, sacrificed to the technology roadmap.

Then there is the value-capture question that rollups sharpen. Layer 2s use Ethereum for security and pay it a pittance for the privilege. Robinhood’s own chain is an example: analyses of corporate L2s show the base layer capturing a rounding error of the economics while providing the security that makes the whole arrangement credible. If Ethereum’s future is thousands of rollups settling to it cheaply, then Ethereum is providing enormous value and capturing little of it, and no amount of narrative reframing fixes a value-capture problem that lives in the fee structure.

The fix nobody is talking about

Which brings us to December 2025, and the upgrade that was designed, in part, to address exactly this, and that most of the market ignored.

The Fusaka upgrade activated on December 3, 2025. Its headline features were about scaling further, PeerDAS and expanded blob capacity. But buried in it was EIP-7918, the “blob base fee bound,” which is the most direct attempt yet to repair the burn. The problem Dencun created was that blob fees could collapse to near-zero, one wei, when execution costs dominated and blob demand was soft, which meant rollups consumed Ethereum’s capacity almost for free and burned almost nothing. EIP-7918 sets a floor: it ties the minimum blob fee to the execution base fee, roughly the execution base fee divided by 16, so that even in quiet periods rollups pay a meaningful minimum, and a minimum stream of ETH gets burned.

The modeling is striking. Fidelity Digital Assets analyzed what would have happened if EIP-7918 had been active since blobs launched, and found that on 93% of days since the 2024 Dencun upgrade, the adjusted fee would have exceeded the actual fee, generating an estimated additional $78.6 million, roughly 24,641 ETH, in cumulative blob-fee revenue. Blockworks noted that had the mechanism been introduced in June 2025, burnt blob fees would have been nearly 8x higher. The intent is explicit: restore a floor under the burn so that as stablecoins, DeFi, and tokenization migrate to rollups, ETH still captures value from that activity instead of subsidizing it.

The honest caveat is that this is a floor, not a restoration. EIP-7918 prevents the burn from collapsing to zero; it does not recreate the thousands-of-ETH-per-day burn of the congested mainnet era. Whether it produces measurable, sustained deflation depends on how much activity flows through blobs and how high execution base fees run, and the market is still watching. It is a serious, well-designed attempt to reconnect usage and scarcity. It is not a return to 2022.

Sound money versus ultrasound money, honestly compared

Because the entire thesis was built as a shot at Bitcoin, it is worth putting the two monetary models side by side without the tribalism, since the comparison is more interesting than either camp admits.

Bitcoin offers fixed scarcity. The supply schedule is written into the protocol, capped at 21 million coins, and halves on a predictable timetable roughly every four years. A holder knows today, with certainty, what Bitcoin’s issuance will be in 2030 and 2040. That certainty is the entire product. Bitcoin does not react to demand, does not burn, does not adjust; it simply issues on schedule toward a hard cap, and its current inflation runs around 0.8% annually, trending toward zero over decades. The trade-off Bitcoin holders accept is that the base layer offers little native utility and no yield. You hold it for the certainty, and you give up productivity in exchange.

Ethereum offered, and to a degree still offers, elastic scarcity. Supply responds to network demand: high usage burns more and can push ETH net deflationary; low usage burns less and lets mild inflation through. The appeal was a token that becomes scarcer precisely when it is most used, tying the asset’s scarcity to the network’s success. The trade-off, which the L2 era exposed, is that elasticity cuts both ways.

A demand-responsive supply is only deflationary when demand is high on the layer that burns, and Ethereum deliberately moved demand to layers that do not burn. Bitcoin’s rigidity, often criticized as inflexible, turned out to be the thing that made its monetary promise keepable. Ethereum’s flexibility, often praised as sophisticated, turned out to be the thing that made its monetary promise conditional.

The honest scorecard is that these are different products for different buyers, not better and worse versions of the same thing. Bitcoin sells certainty and asks you to forgo utility. Ethereum sells utility and asks you to accept that its scarcity depends on how that utility is used. The ultrasound-money era was the brief window when Ethereum appeared to offer both, certainty of deflation and utility of a working network, and that window closed not because Ethereum failed but because it succeeded at scaling.

A holder choosing between them in 2026 is really choosing between guaranteed scarcity with no yield and demand-driven scarcity with staking yield and network utility. Framed that way, the loss of ultrasound money is less a defeat than a clarification: Ethereum was never going to be Bitcoin, and the burn was hiding how different the two bets actually are.

What this means for holding ETH

Strip away the narrative fight and the practical question is whether the ultrasound story mattered to the price, and the uncomfortable answer is that it is hard to tell, because ETH has underperformed through the entire period regardless.

The clean way to see it: the ultrasound thesis was strongest right after the Merge, and it has been dismantled steadily since Dencun in March 2024. Over that same window, ETH has been a persistent underperformer against both Bitcoin and its own former highs. Either the market was pricing the loss of the deflation narrative, or the market never cared about the narrative and ETH’s problems lie elsewhere, in L2 value leakage, in competition from Solana, in the sheer difficulty of the modular roadmap. Both readings are defensible, and they point to different conclusions about whether fixing the burn fixes the price.

The most honest framing is that ultrasound money was a proxy for a real question that has not gone away: does Ethereum capture value from its own success? When the network was congested and expensive, the answer was visibly yes; the burn made it legible. When the network scaled and cheapened, the answer became murky, and the burn stopped telling the story. EIP-7918 is an attempt to make the answer legible again by putting a floor under value capture.

Whether it works will show up not in the marketing but in two numbers over the next year: net ETH supply, and base-layer fee revenue. If both turn up meaningfully, the thesis has a second life. If they do not, then ultrasound money was a phase, not a property, and Ethereum’s investment case has to stand on utility alone, which is a harder, slower, less tweetable argument than the one that shrank the supply.

Frequently Asked Questions

What is Ethereum ultrasound money?

It is the thesis that Ethereum’s ETH token would become deflationary and a superior store of value to Bitcoin. It rests on two mechanisms: EIP-1559, activated in 2021, which burns a portion of every transaction fee, and the 2022 Merge, which cut new ETH issuance by roughly 90%. When burning exceeds issuance, total supply shrinks. The term was a play on Bitcoin’s “sound money” branding.

Is Ethereum still deflationary in 2026?

Not on a net basis, in normal conditions. After the March 2024 Dencun upgrade shifted activity to cheap layer-2 rollups, the burn collapsed, and ETH became mildly inflationary, with net supply growth around 0.2% to 0.8% annually depending on the period. During bursts of high mainnet activity, it can still turn temporarily deflationary, but the sustained deflation of the immediate post-Merge period ended.

Why did layer 2s break the burn?

Because they moved activity off the base layer, where transactions burned meaningful ETH, onto rollups that pay near-zero fees. The Dencun upgrade introduced cheap “blob” transactions for rollups, cutting their costs 10 to 100 times. Blob space was oversupplied, so blob fees fell close to zero, and the daily burn dropped from thousands of ETH to as low as 50 to 70. The activity continued; the burn did not follow it.

Does this mean ETH is a worse investment?

Not necessarily, and defenders make several counterpoints: issuance is still about 90% lower than under proof-of-work, roughly 0.2% net inflation in calm periods is actually below Bitcoin’s, nearly a third of ETH is locked in staking and off the market, and the real case rests on demand for blockspace rather than deflation. Critics counter that base-layer fee revenue collapsed too, raising a genuine value-capture problem.

What is EIP-7918?

A change introduced in Ethereum’s December 2025 Fusaka upgrade that sets a minimum price for blob transactions, tied to the execution base fee, roughly that fee divided by 16. It prevents blob fees from collapsing to near-zero during quiet periods, ensuring a minimum stream of ETH is burned. Fidelity modeled that it would have added roughly $78.6 million in cumulative burn across 93% of days since 2024 had it existed earlier.

Did Fusaka restore ultrasound money?

No, it put a floor under the burn rather than restoring the deflation of the post-Merge era. EIP-7918 stops the burn from collapsing to zero and improves value capture as activity migrates to rollups, but it does not recreate the thousands-of-ETH-per-day burn of the congested mainnet period. Whether it produces sustained net deflation depends on blob activity and execution fees, and remains to be seen.

Is Ethereum still harder money than Bitcoin?

In a narrow technical sense, sometimes. In calm periods, Ethereum’s roughly 0.2% net inflation can run below Bitcoin’s roughly 0.8% fixed-schedule inflation. But Bitcoin offers predictable, protocol-guaranteed scarcity indefinitely, while Ethereum’s supply is elastic and responds to demand, so it can inflate more during quiet, scaled periods. They offer different kinds of scarcity: fixed and certain versus elastic and demand-driven.

What should I watch to know if the thesis recovers?

Two numbers over the next year: net ETH supply growth, and Ethereum base-layer fee revenue. If EIP-7918 and rising rollup activity push net supply back toward flat or negative while base-layer revenue climbs from its roughly $10 million lows, the value-capture story recovers. If supply keeps growing and fee revenue stays depressed, ultrasound money was a temporary phase, and ETH’s case rests on utility and demand alone.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. It describes monetary mechanics and network upgrades whose effects are uncertain and still developing. Nothing here is a recommendation to buy or sell any asset. Always do your own research. Figures on supply, burn, and inflation move continuously and are accurate as of July 17, 2026.

Robinhood Chain launched, filled with memecoins, briefly ranked third among DEXs, and the “Solana killer” talk started immediately. Then you look at the actual numbers. Solana has 27 times the value locked and 2 million more users. This is not a flippening. It is a fair fight over the wrong metric.

Summary

- Robinhood Chain launched July 1 and drew roughly $185 million in value locked and over $3 billion in first-week DEX volume, briefly ranking among the top DEXs by volume and prompting Solana comparisons.

- Solana dwarfs it on every durable metric: around $4.93 billion in value locked, $1.91 billion in daily DEX volume, more than 2 million active addresses, and roughly $3 million in daily app revenue.

- The gap on value locked is about 27 to 1. On active users, it is larger. Volume alone, the one metric where Robinhood looked competitive, is the least durable measure and is inflated by a memecoin frenzy and a gas subsidy.

- The real bull case for Robinhood is not flipping Solana on-chain. It is distribution: roughly 28 million existing customers and a decade of retail brand equity that no crypto-native chain can match.

- The honest verdict is that Robinhood will not flip Solana on DeFi metrics any time soon, but the two are not actually competing for the same thing, which makes the flippening question the wrong one.

Within days of Robinhood Chain going live, the comparison wrote itself. A memecoin frenzy sent the chain’s DEX volume past $3 billion in a week; it briefly cracked the top three networks by daily DEX volume, and crypto Twitter did what crypto Twitter does: it declared a Solana killer.

The parallel was tidy. Solana also grew through a memecoin boom, so surely Robinhood was running the same playbook toward the same destination. Then you pull the actual data, and the tidy story falls apart. Solana has roughly 27 times Robinhood Chain’s value locked and millions more users.

The one metric where Robinhood looked competitive, raw volume, is the flimsiest number on the board. This piece is about whether Robinhood Chain can flip Solana, and the short answer is no, not close, and the more interesting answer is that flipping Solana was never the right frame.

The scoreboard

Start with the numbers, because the numbers settle most of the argument before it starts.

Solana, as of mid-July 2026, carries around $4.93 billion in total value locked, does roughly $1.91 billion in daily DEX volume, has more than 2 million active addresses, and generates about $3 million in daily application revenue. These are the metrics of a mature, heavily used layer-1 with a deep DeFi ecosystem, years of accumulated liquidity, and a large, sticky user base.

Robinhood Chain, roughly 2 weeks after launch, sits at around $185 million in value locked, having posted more than $3 billion in DEX volume across its first week. Depending on the day and the source, its TVL has been quoted between $185 million and $312 million, with the higher figure heavy on stablecoin deposits. Active addresses are counted in the hundreds of thousands cumulatively, not the millions active.

Line the durable metrics up, and the gap is stark. On value locked, Solana leads by a factor of roughly 27 to one against the lower Robinhood figure, and still around 16 to 1 against the higher one. On active users, the gap is larger still. On application revenue, Solana’s ecosystem earns real fees across a diverse set of protocols; Robinhood Chain’s revenue is concentrated in memecoin trading and inflated by incentives. There is exactly one metric where Robinhood looked competitive in its first fortnight, and that is raw DEX volume, where a memecoin frenzy briefly pushed it into the same conversation as networks many times its size.

That single metric is doing all the work in the flippening narrative, and it is the metric that deserves the least trust.

Why volume is the wrong number

Volume is seductive because it is large and it moves fast, and it is misleading for the same reasons.

Robinhood Chain’s $3 billion first week was overwhelmingly memecoin trading. CASHCAT alone generated roughly $98 million in a single day, about 17% of the chain’s entire DEX volume, and the broader wave of Robinhood-themed tokens, Cash Dog in Hood, Little John, Hoodrat, drove most of the rest.

Memecoin volume is the most transient category of on-chain activity there is. It arrives with attention and leaves with it, and it leaves no infrastructure behind. A chain doing $3 billion in memecoin volume this week can do a fraction of that next month, as the 33% single-day CASHCAT drop after its launchpad exited already showed.

Then there is the subsidy. Robinhood Chain ran a 90-day gas fee subsidy from launch, which makes transactions artificially cheap and inflates transaction counts and, indirectly, trading activity. Any volume comparison during the subsidy window is measuring a promotion as much as organic demand. The honest read of that number will only be available once the subsidy expires and users start paying real costs.

Value locked, by contrast, is sticky. It represents capital that has chosen to reside on the chain, in lending protocols, liquidity pools, and asset-management strategies, and it does not evaporate with a memecoin’s attention cycle. Solana’s ~$4.93 billion in TVL is the accumulated result of years of protocols, integrations, and users committing capital. Robinhood’s ~$185 million is a 2-week-old figure heavily weighted toward stablecoin deposits and speculative liquidity. TVL is the metric that predicts whether a chain is durable. Volume is the metric that predicts whether it is currently trending. They are not the same, and the flippening narrative relies entirely on the second.

The bull case for Robinhood

The strong case for Robinhood Chain does not run through on-chain metrics at all, and the people making the flippening argument are looking in the wrong place because the actual advantage is off-chain.

Robinhood has roughly 28 million customers across 38 countries and more than a decade as one of the largest retail investment platforms in the United States. That is a distribution asset no crypto-native chain possesses. Solana had to acquire its users one at a time through the slow, expensive work of crypto adoption.

Robinhood already has tens of millions of funded accounts belonging to people comfortable trading both stocks and crypto, and it can put its chain in front of them inside an app they already use. If even a modest fraction of that base becomes active on-chain, the user numbers change quickly. Brand equity and distribution are exactly what earlier tokenization projects lacked, and Robinhood has both in abundance.

The memecoin-as-ignition argument also has real historical support. Solana itself grew through a memecoin cycle: BONK, WIF, and the Pump.fun era, before it produced serious infrastructure and institutional adoption. Base followed a similar arc. Speculative trading bootstraps the liquidity, the market makers, the tooling, and the attention that serious applications later need. In this reading, Robinhood Chain’s memecoin phase is not a failure to attract real activity; it is the normal first stage, and judging a 2-week-old chain by its TVL is like judging Solana by its 2021 numbers.

And Robinhood is playing a different game entirely. Its chain is built for tokenized stocks and real-world assets, a category Solana is also chasing but where Robinhood brings brokerage licenses, custody relationships, and regulatory infrastructure that a crypto-native chain has to build from scratch. If the RWA thesis plays out, Robinhood competes on ground where its traditional-finance credentials are an advantage, not on the DeFi metrics where Solana is years ahead. The flippening question assumes the two chains want to be the same thing. They may not.

The bear case for Robinhood

The skeptical case is that Robinhood Chain has attracted exactly the kind of activity that does not convert, and that the gap to Solana is not a head start Robinhood can close but a structural difference it may never close.

The mercenary-liquidity problem is the core of it. Memecoin traders are loyal to activity, not to chains. They arrived on Robinhood Chain because that is where the new-launch action was, and they will leave for the next chain offering quicker profits without a second thought. The Noxa launchpad that powered the entire boom generated roughly $12 million in fees and then stopped accepting launches and went dark within 11 days of the chain’s launch. That is not the behavior of infrastructure settling in; it is the behavior of an extraction cycle moving through. When the memecoin attention leaves, the question is what remains, and right now what remains is roughly $12.8 million in actual tokenized real-world assets, the thing the chain was built for.

The convert-the-traffic problem compounds it. Robinhood’s 28 million customers are a distribution asset only if they can be moved on-chain, and there is no evidence yet that memecoin degens and Robinhood’s retail stock traders are the same people or that 1 becomes the other. The chain’s current users may have almost no overlap with the tokenized-asset investors Robinhood hopes to serve. Distribution is potential, not conversion, and the conversion has not been proven.

Then there is the structural point that on-chain metrics are not a race Robinhood is quietly winning. Solana continues to outperform Robinhood Chain across essentially every DeFi metric despite the new chain’s loud debut, and Solana is not standing still. It has its own institutional momentum, its own tokenized-asset push, its own SBI partnership for on-chain financial markets in Japan. Robinhood is not catching a stationary target. It is entering, 2 weeks old, a competition against a network with a multi-year head start that is itself accelerating. Closing a 27-to-1 TVL gap against a moving, growing competitor is a different proposition than the volume charts suggest.

The Base comparison nobody makes

The flippening debate fixates on Solana, but the more instructive comparison is Coinbase’s Base, because Base is the closest thing to a control group for exactly what Robinhood is attempting, and it complicates both the bull and bear cases.

Base launched in 2023 as a corporate-backed Ethereum layer 2, built by a licensed, publicly traded American financial company with a large existing user base, aimed at bringing mainstream users on-chain. That is Robinhood Chain’s template almost exactly. And Base’s early growth, like Robinhood’s, ran heavily through memecoins before it developed into a more diversified ecosystem. So Base is the case study for whether a corporate chain can convert a speculative launch into durable activity, and the answer it offers is genuinely mixed.

On the bull side, Base did convert. It built real DeFi, real stablecoin activity, and real applications on top of the initial speculation, and it became one of the larger L2s by several measures. Coinbase’s distribution, tens of millions of users, mattered, and the memecoin phase did function as ignition rather than as the whole story. That is the precedent Robinhood is betting on, and it is a real one: a corporate chain did turn a speculative launch into something lasting.

On the bear side, Base did not flip Solana either, and it had a 2-year head start on Robinhood plus a parent company that was crypto-native from birth. If Base, with Coinbase’s crypto-specific expertise and a longer runway, sits alongside Solana instead of above it, the idea that Robinhood Chain will vault past Solana looks even less plausible. And Base has its own value-capture questions as an Ethereum L2, the same ones that apply to Robinhood Chain, where the base layer captures little of the economics. Base shows the corporate-chain model can work; it also shows that working means becoming a significant chain, not dethroning the incumbent. That is the realistic ceiling for Robinhood Chain too: not flipping Solana, but earning a durable place alongside it, and only if it converts the way Base did rather than fading the way most launch-frenzies do.

What a flippening would actually require

The word “flippening” gets thrown around loosely, so it is worth being precise about what would have to happen for Robinhood Chain to actually surpass Solana, because the specifics show why the headline math is not close.

Flipping Solana is not one event; it is a set of them across separate metrics, and they do not move together. On total value locked, Solana holds roughly $4.93 billion against Robinhood Chain’s ~$185 million, a gap of about 27 times. Closing that does not mean matching Solana’s memecoin volume for a week. It means persuading serious capital, lending markets, stablecoin issuers, restaking protocols, and asset managers to park billions on a corporate L2, which is a trust-and-time problem that speculative volume does nothing to solve. TVL is sticky precisely because it represents commitment, and commitment is the thing a memecoin wave cannot manufacture.

On active addresses, Solana runs above 2 million against a far smaller base on Robinhood Chain, and the composition matters more than the count. Solana’s addresses span DeFi users, NFT traders, payment apps, and memecoin degens across a mature ecosystem. Robinhood Chain’s early activity is concentrated in memecoin speculation and a gas subsidy that inflates the raw transaction figure. An address trading CASHCAT once is not equivalent to an address running a lending position, a payment flow, and a staking allocation. The headline number can converge while the underlying engagement stays a chasm apart.

On application revenue, Solana generates around $3 million daily from a diversified base of protocols. Robinhood Chain’s revenue is thin and skewed toward the launchpad-and-memecoin complex that already showed it can evaporate in days when Noxa went dark. Sustainable app revenue requires applications people use for reasons other than speculation, and building that catalog is measured in years of developer adoption, not weeks of viral trading.

Then there is the structural ceiling nobody in the flippening conversation mentions: Robinhood Chain excludes US persons from its flagship products. Stock Tokens are barred to Americans, wallet perpetuals are barred to Americans, and the chain’s entire regulated-RWA thesis is aimed at a user base that cannot legally touch its marquee offerings from Robinhood’s home market. Solana has no such wall. A chain competing for global L1 dominance with its largest potential market fenced off from its best products is running the race with a weight the incumbent does not carry.

Put those together, and the flippening is not a single line for Robinhood Chain to cross. It is four separate lines, on four metrics that move at different speeds for different reasons, at least one of which is capped by regulation. Memecoin volume, the one number Robinhood Chain can actually post, is the least sticky and least predictive of the set. That is why the honest answer to the headline is not “not yet.” It is “not close, and the gap is wider than the volume charts make it look.”

The verdict

So will Robinhood Chain flip Solana? On the metrics that matter, no, and not close, and not soon.

The value-locked gap is roughly 27 to 1. The user gap is larger. The revenue gap is structural. The only metric where Robinhood was competitive is raw volume, which is the least durable measure available, is dominated by transient memecoin trading, and is inflated by a temporary gas subsidy. A chain does not flip a mature layer-1 by winning the one number that evaporates when attention moves on. Every durable indicator points to Solana remaining well ahead for the foreseeable future.

But the question contains a flawed assumption, and that is the more useful thing to say. “Flip Solana” treats the two chains as competitors for the same prize, and they may not be. Solana is a general-purpose, crypto-native layer-1 with a deep DeFi ecosystem built by and for crypto users. Robinhood Chain is a corporate settlement layer built by a licensed brokerage to bring tokenized stocks and real-world assets to a retail base that already trades on Robinhood. Their overlap right now is memecoins, which is precisely the activity neither of them was built for and which will belong to whichever chain is currently paying attention. The lasting competition, if there is one, is over tokenized real-world assets, and that race has barely started.

The honest framing is this. Robinhood will not out-DeFi Solana; that is not a contest it is positioned to win and probably not one it is trying to win. What Robinhood can do is convert a slice of 28 million existing customers into on-chain users of tokenized-asset products, on rails where its brokerage credentials matter more than its DEX volume. If it does that, it does not need to flip Solana, because it will be winning a different game. If it does not, the memecoin volume fades, the chain settles back to its $12.8 million of real assets, and the flippening talk looks like what it probably is: a volume chart mistaken for a verdict. The number to watch is not DEX volume and not the gap to Solana. It is whether tokenized real-world assets on Robinhood Chain grow, and Robinhood’s July 29 earnings are the first real look.

Frequently Asked Questions

Is Robinhood Chain bigger than Solana?

No, and the gap is large. As of mid-July 2026, Solana holds around $4.93 billion in total value locked against Robinhood Chain’s roughly $185 million, a gap of about 27 to 1. Solana also has more than 2 million active addresses and around $1.91 billion in daily DEX volume from a mature ecosystem. Robinhood Chain briefly matched Solana on raw DEX volume during a memecoin frenzy, but trails badly on every durable metric.

Why do people compare Robinhood Chain to Solana?

Because Robinhood Chain’s DEX volume surged past $3 billion in its first week, briefly ranking among the top networks, and because Solana famously grew through a memecoin cycle of its own before maturing. The parallel is that both bootstrapped with speculation. The comparison relies heavily on volume, which is the least durable metric and, for Robinhood, is inflated by memecoin trading and a temporary gas subsidy.

Could Robinhood Chain flip Solana eventually?

On DeFi metrics, it is unlikely any time soon, given a 27-to-1 value-locked gap against a competitor that is itself growing. Robinhood’s real advantage is off-chain: roughly 28 million existing customers and strong retail brand equity. If it converts a meaningful share of that base into on-chain users of tokenized-asset products, it could become large without ever matching Solana on DeFi, because it would be competing on different ground.

Why is DEX volume a misleading metric?

Because it is transient and easily inflated, Robinhood Chain’s volume was overwhelmingly memecoin trading, which arrives and leaves with attention and builds no lasting infrastructure. A 90-day gas subsidy also made transactions artificially cheap during the launch window. Value locked, which represents capital committed to the chain’s protocols, is a far better predictor of durability, and on that measure Solana leads decisively.

What is Robinhood Chain actually built for?

Tokenized stocks and real-world assets. It launched as an Ethereum layer 2 with Stock Tokens as the flagship product, targeting a retail base that already trades equities on Robinhood. Its competitive advantage is brokerage licenses, custody relationships, and regulatory infrastructure. The memecoin activity that drove its early volume is not the use case it was designed for, and only about $12.8 million in real-world assets currently sit on it.

What happened with CASHCAT and the memecoins?

CASHCAT, a token named after Robinhood’s original working name, surged to a roughly $156 million market cap and at one point generated about 17% of the chain’s daily DEX volume. It spawned a wave of Robinhood-themed tokens. The launchpad driving the boom, Noxa, earned around $12 million in fees, then went dark within 11 days, and CASHCAT fell more than 33% in a day, illustrating how quickly memecoin activity can leave.

Does Robinhood’s user base guarantee success?

No. Roughly 28 million customers is a distribution advantage, but distribution is potential, not conversion. There is no evidence yet that Robinhood’s retail stock traders will become active on-chain users, or that the memecoin traders currently driving activity overlap with the tokenized-asset investors the chain targets. Converting existing customers into on-chain users is the unproven step the entire strategy depends on.

When will we know if the strategy is working?

Watch the tokenized real-world asset figure on the chain, currently around $12.8 million, rather than DEX volume or the gap to Solana. If real assets grow substantially while memecoin activity fades, the traffic is converting, and the strategy is working. Robinhood’s second-quarter earnings on July 29 should offer the first real look at Stock Token adoption, and liquidity behavior after the gas subsidy expires will be the next test.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. It compares blockchain networks and company strategies, not the merits of any token. Memecoins are highly speculative, and most participants lose money. Nothing here is a recommendation to buy any asset or use any platform. Always do your own research. On-chain figures move quickly and are accurate as of July 17, 2026.

There is $1.6 trillion in Bitcoin sitting idle, earning nothing, doing nothing. Charles Hoskinson has a plan to put it to work on Cardano, and the plan quietly requires every transaction to burn a little ADA. Whether that saves Cardano or exposes its central problem is the whole question.

Summary

- Cardano founder Charles Hoskinson has laid out a strategy to bring Bitcoin into Cardano’s DeFi ecosystem through a platform called Pogun, targeting the roughly $1.6 trillion in idle Bitcoin.

- Pogun rolls out in three phases across 2026: a non-margin credit market in the second quarter, a yield application in the third, and a BitVM-based trust-minimized bridge in the fourth.

- The mechanism that matters for ADA holders: every transaction in the system requires ADA for fees, paid invisibly by Bitcoin users, creating a demand driver that Cardano’s token has lacked.

- It leans on Midnight, Cardano’s privacy partner chain, for confidential transactions, and on Cardano’s EUTXO architecture, which shares design lineage with Bitcoin’s own UTxO model.

- The sharp objection, raised by Cardano’s own community: if Bitcoin can be lent, earn yield, and settle without users noticing ADA, why hold ADA at all? The plan may build against its own token.

Cardano has a problem it has had for years, and it is not a technology problem. ADA trades around 94% below its 2021 high, the network’s DeFi activity has long lagged its ambitions, and its founder spends a meaningful share of his time denying rumors that he is quitting. What Cardano has never lacked is engineering and ideas.

What it has lacked is a reason for capital to show up. Charles Hoskinson’s answer, laid out across 2026, is audacious: stop trying to attract crypto capital to Cardano and go get Bitcoin’s instead. There is roughly $1.6 trillion in Bitcoin sitting idle in wallets, earning nothing, and Hoskinson wants to route a slice of it through Cardano’s infrastructure, with every transaction quietly paying fees in ADA. It is the most concrete demand thesis Cardano has produced in years. It also contains a contradiction its own community has already spotted.

The idle-Bitcoin thesis

The premise starts with a real and large number. Something on the order of $1.6 trillion in Bitcoin sits in wallets doing nothing productive. Bitcoin is superb as a store of value and poor as a financial instrument: it does not natively lend, earn yield, or plug into decentralized finance without wrapping, bridging, or handing custody to an intermediary. That gap, enormous dormant capital with no native way to work, is what every “Bitcoin DeFi” project is chasing, and Hoskinson has decided Cardano should chase it hard.

His framing, delivered publicly in May 2026 and reiterated through the year, is that Bitcoin holders would be able to access lending, yield, and privacy tools through Cardano without surrendering control of their assets. A dedicated team, described at various points as around 19 people, is building it. The pitch to Bitcoin holders is straightforward: keep your Bitcoin, but make it productive, through infrastructure that does not require you to trust a centralized custodian.

The pitch to Cardano holders is different and more important to the ADA investment case. Hoskinson has been explicit that the entire system runs on ADA underneath. In his own words, every single transaction requires ADA to happen; the Bitcoin user pays a fee in ADA but does not see it. The idea is to make ADA the invisible fuel of a Bitcoin-DeFi economy, generating persistent, usage-based demand for the token regardless of whether anyone is speculating on ADA itself. For a token whose central weakness has been the absence of a demand driver, that is the whole game.

What Pogun actually is

Pogun is the platform that operationalizes the thesis, and its structure is more concrete than Cardano’s roadmaps usually are.

It rolls out in three phases across 2026. The first, targeted for the second quarter, is a non-margin credit market: lending against Bitcoin without the liquidation-cascade risk that leveraged lending carries. The second, targeted for the third quarter, is a yield-focused application that lets Bitcoin holders earn returns.

The third, targeted for the fourth quarter, is a BitVM-powered bridge, a trust-minimized way to move Bitcoin onto Cardano infrastructure without the custodial risk that has plagued wrapped-Bitcoin products. Input Output Group sought treasury funding for the effort, with figures around 12.3 million ADA cited, as part of a larger proposal slate that also funded the Leios scaling upgrade.

The architecture leans on two Cardano-specific pieces. The first is Midnight, Cardano’s privacy-focused partner chain, which launched its mainnet in early 2026 and serves as the confidential coordination layer, letting Bitcoin holders use DeFi tools without exposing their positions publicly. Hoskinson has framed Midnight as proof of Cardano’s partner-chain model, specialized chains operating alongside the main network while drawing on its security.

The second is Cardano’s EUTXO accounting model, which shares design lineage with Bitcoin’s own UTxO model. That shared lineage is not incidental; it is part of the technical argument that Cardano is a more natural home for Bitcoin DeFi than account-based chains like Ethereum, because the two systems think about transactions in a similar way.

The sequencing is deliberate. The team has described building the credit market and liquidity first, so that by the time the consumer-facing products launch, there is already a functioning market underneath them instead of an empty shell waiting for users.

The bull case

The strongest version of this argument is that Cardano has finally identified the right target and built a credible, differentiated way to reach it.

The demand mechanism is genuinely elegant. Cardano’s problem was never capability; it was that ADA had no structural reason to be in demand beyond speculation and staking. Embedding ADA as the mandatory fee layer of a Bitcoin-DeFi economy creates exactly the kind of usage-based demand that speculation cannot provide, and that does not evaporate when sentiment turns. If Bitcoin DeFi on Cardano generates real volume, ADA demand rises mechanically with it, transaction by transaction, whether or not anyone is bullish on ADA as a trade. That is a far healthier demand base than the memecoin-and-narrative cycles driving other chains.

The target is also the right one. Every serious chain is chasing Bitcoin DeFi because the prize, a fraction of $1.6 trillion in dormant capital, is the largest untapped pool in crypto. Cardano bringing brokerage-grade patience, a privacy layer, and UTxO compatibility to that chase is a real differentiator against the wrapped-Bitcoin approaches that have dominated and repeatedly failed on custody and trust. A BitVM bridge that reduces custodial risk addresses the exact failure mode, hacked or insolvent custodians, that has burned wrapped-Bitcoin users before.

And it fits Cardano’s identity rather than betraying it. Cardano’s whole brand is methodical, research-driven, security-first engineering, often criticized as too slow. Bitcoin holders are, as a group, the most conservative and security-conscious in crypto. A careful, peer-reviewed, custody-minimizing approach to Bitcoin DeFi is arguably better matched to Bitcoin holders than the move-fast culture of other DeFi ecosystems. For once, Cardano’s slowness could be a feature aimed at exactly the audience that values it.

The bear case

The skeptical case starts with a question a Cardano community member asked Hoskinson directly, and it is devastating in its simplicity: what would be the point of holding ADA over Bitcoin? Are we building against our own core token?

The concern is real and structural. If the system is designed so that Bitcoin users pay fees in ADA without seeing it, then the design goal is explicitly to make ADA invisible. A Bitcoin holder using Pogun holds Bitcoin, earns yield in Bitcoin, and never needs to acquire, hold, or think about ADA. The fees are abstracted away. If ADA is successfully hidden from the user, then ADA is a backend utility token that the end user has no reason to hold as an investment, which means the demand is limited to whatever float the protocols need to operate, not the broad holder demand that supports a token’s price.

Making ADA the invisible plumbing is good for usage and potentially bad for ADA as an asset people want to own. Hoskinson’s answer, that transactions require ADA regardless, addresses mechanical demand but not the deeper question of why anyone holds ADA rather than the Bitcoin it is helping to mobilize.

The second problem is execution and timeline. Cardano has a long history of ambitious roadmaps that arrive late or underdeliver relative to the promise. Pogun’s phases are targeted across 2026, and Cardano’s governance has been visibly deadlocked, with treasury votes for exactly this kind of initiative facing friction and Hoskinson warning that rejecting research funding could drive engineers away. A plan that depends on multiple new components, Midnight, the BitVM bridge, the credit and yield layers, all shipping and integrating on schedule, is a plan with substantial execution risk in an ecosystem that has struggled to convert roadmap into adoption before.

The third problem is competition. Cardano is not alone in chasing Bitcoin DeFi; it is late to a crowded race. Bitcoin layer-2s, wrapped-Bitcoin protocols on Ethereum, and Bitcoin-native DeFi efforts are all pursuing the same idle capital, several with more liquidity, more developers, and more existing integrations than Cardano has managed to attract. Cardano’s DeFi TVL has sat around $1.1 billion at times, a fraction of Ethereum’s or Solana’s, which raises the question of why Bitcoin holders would route their capital through the ecosystem that has struggled most to attract capital in the first place. Being a natural technical home for Bitcoin DeFi does not help if the liquidity and developers are elsewhere.

The token question at the center

Everything about this plan comes back to one unresolved tension, and it is worth stating plainly because it is the crux of whether Pogun helps ADA or merely helps Bitcoin.

Cardano is trying to solve its demand problem by making ADA essential but invisible. Those two properties are in tension. Essential means every transaction needs ADA, which creates mechanical demand proportional to usage. Invisible means users never consciously hold or value ADA, which suppresses the discretionary demand that actually drives a token’s price above its pure utility floor. A token that is essential-but-invisible tends to trade at its utility value, the minimum float the system needs to function, rather than at the premium that comes from people wanting to own it. Ethereum resolved this tension by making ETH visible and desirable as an asset in its own right, through staking, through the ultrasound narrative, through being the reserve asset of its own economy. Cardano’s Pogun design points the other way, toward ADA as backend infrastructure.

The optimistic resolution is that sufficient usage makes even utility-value demand large. If Bitcoin DeFi on Cardano processes enormous volume, the mechanical ADA demand could be substantial even if no one holds ADA for love of it. The pessimistic resolution is that Cardano will have built a successful piece of Bitcoin infrastructure whose value accrues to Bitcoin holders and Pogun’s operators, while ADA captures only the thin utility margin, which is not the outcome ADA holders are hoping for when they cheer a Bitcoin-DeFi announcement.

Which resolution wins depends on numbers that do not exist yet, because the products are still launching. The second-quarter credit market and third-quarter yield app are the first real tests. If they generate meaningful Bitcoin volume and ADA demand rises visibly with it, the thesis has legs. If they launch quietly into the same low-liquidity environment that has characterized Cardano DeFi, then Pogun becomes another well-engineered Cardano initiative that did not move the token, and the community member’s question, why hold ADA over Bitcoin, will have answered itself.

Why Cardano needs this to work

To understand why Hoskinson is betting so heavily on Bitcoin DeFi, you have to understand how much pressure Cardano is under, because Pogun is not an opportunistic add-on. It is a response to an existential question the market keeps asking.

The pressure is visible in the numbers and the noise around them. ADA trades roughly 94% below its 2021 high, deep in the ranks of large-cap tokens that led the previous cycle and never recovered. Cardano’s DeFi total value locked, around $1.1 billion at times, is a fraction of Ethereum’s or Solana’s despite Cardano having been live since 2017 and commanding one of the most committed communities in crypto. Hoskinson has spent 2026 denying rumors that he is leaving the project and calling them fiction, which is not a thing founders of thriving networks typically have to do. And the governance apparatus, the CIP-1694 on-chain system Cardano is genuinely proud of, has been deadlocked over treasury proposals, with Hoskinson warning that rejecting research funding could push engineers out.

Underneath all of it is a criticism Hoskinson himself has accepted in his own framing: Cardano’s problem is not technology. He has said explicitly that it is not a node problem, not a problem of imagination, not a problem of execution capability, but a problem of governance, coordination, and ultimately getting capital and users to show up. That is a striking admission from a founder, and it reframes Pogun. Bitcoin DeFi is not just a product; it is Hoskinson’s answer to the accusation that Cardano builds impressive technology that nobody uses. If he can route Bitcoin’s enormous, idle capital base through Cardano, he solves the adoption problem and the demand problem at once, and he does it without needing to win the crypto-native DeFi users who have consistently chosen other chains.

That is why the stakes are higher than a normal roadmap item. Cardano has tried narratives before: smart contracts, then DeFi, then real-world assets, and none produced the adoption inflection the community keeps waiting for. Bitcoin DeFi is the biggest swing yet, aimed at the biggest target, and it arrives at a moment when patience with the slow-and-steady thesis is visibly thinning. If Pogun works, it vindicates the entire methodical approach. If it lands quietly like its predecessors, it will be much harder to argue that the next initiative will be different. Hoskinson has effectively staked the credibility of Cardano’s whole strategy on reaching an audience that has never been Cardano’s, which is either the boldest possible move or a sign of how few options remain.

What to watch

Three concrete markers will tell you which way this breaks.

The first is whether the Pogun phases actually ship on their 2026 timeline. The credit market was targeted for the second quarter and the yield app for the third; slippage on those dates, in an ecosystem already criticized for slow delivery, would be an early negative signal. Shipping on time, with working products, would be a genuine and somewhat unexpected positive given Cardano’s track record.

The second is Bitcoin volume through the system, not ADA price. The entire thesis rests on attracting idle Bitcoin, so the metric that matters is how much Bitcoin actually flows into Pogun’s credit and yield products once they are live. ADA price will be noisy and driven by the broader market; Bitcoin TVL on Cardano is the clean read on whether the idle-Bitcoin thesis is working.

The third is whether ADA demand becomes visible in the data as usage grows. This is the crux question made measurable. If Bitcoin volume rises and on-chain ADA demand rises with it in a legible way, the essential-and-invisible design is working as a demand driver. If Bitcoin volume rises and ADA does nothing, then the community’s fear was correct, and Cardano will have built valuable infrastructure for someone else’s asset. Hoskinson has made the boldest, most concrete bet of Cardano’s recent history. The next two quarters start to settle whether it was aimed at the right target or against his own token.

Frequently Asked Questions

What is Cardano’s Bitcoin DeFi plan?

It is a strategy, led by founder Charles Hoskinson, to bring Bitcoin into Cardano’s DeFi ecosystem and tap the roughly $1.6 trillion in idle Bitcoin. The centerpiece is Pogun, a platform letting Bitcoin holders lend, borrow, and earn yield through Cardano infrastructure without surrendering custody. Crucially, every transaction in the system requires ADA for fees, creating usage-based demand for Cardano’s token.

What is Pogun?

A three-phase Bitcoin DeFi platform rolling out across 2026: a non-margin credit market in the second quarter, a yield-focused application in the third, and a BitVM-based trust-minimized bridge in the fourth. It integrates Midnight, Cardano’s privacy partner chain, for confidential transactions, and builds on Cardano’s EUTXO architecture, which shares design lineage with Bitcoin’s UTxO model. Input Output Group sought around 12.3 million ADA in treasury funding for it.

How does this benefit ADA holders?

Through embedded demand. Hoskinson has stated that every transaction in the system requires ADA for fees, paid by Bitcoin users who may not even notice. If Bitcoin DeFi on Cardano generates real volume, ADA demand rises mechanically with it, independent of speculation. For a token whose main weakness has been the lack of a structural demand driver, that is the core of the investment argument.

What is the main criticism?