Crypto World

XRP Open Interest Falls 70% to Yearly Lows: What Does it Mean for Ripple’s Price?

The total open interest (OI) for XRP futures across major crypto exchanges has plunged 70% from its peak five months ago, settling at $203 million on March 3, 2026.

The sharp drop in unsettled contracts mirrors levels seen in April 2025, a period that immediately preceded a significant price rally for the digital asset, raising questions about whether the market is once again flushing out excess leverage.

Open Interest Collapse Mirrors April 2025 Setup

Data compiled by market analyst Amr Taha shows that XRP’s aggregate open interest has cratered from $660 million in October 2025 to just $203 million today.

Binance, the dominant venue for XRP derivatives, has seen its OI dip below $270 million, a threshold last witnessed on April 8, 2025. Smaller platforms have also seen activity shrink considerably, with Bitfinex and BitMEX now holding just $4.3 million and $3 million in XRP open interest, respectively.

“Historically, such phases have aligned with local bottoms, as excessive leverage is flushed out and market conditions reset,” Taha noted.

Open interest tracks the total number of outstanding futures and perpetual contracts that remain open. According to the market watcher, a sudden dip alongside falling prices often suggests traders are closing positions or being liquidated as leverage unwinds.

The analyst suggested that the current combination points to forced liquidations and voluntary exits rather than new speculative build-up.

“Traders are either closing positions voluntarily or being liquidated due to margin calls,” he wrote.

The derivatives reset comes at a time when geopolitical tensions are rattling markets. On March 2, analyst Darkfost reported that 472 million XRP, worth about $652 million, flowed into Binance following U.S. and Israeli strikes on Iran.

Such large exchange inflows can signal positioning for potential selling, adding pressure to spot prices, and XRP swung from $1.43 down to $1.27 during the weekend turmoil, allowing BNB to leapfrog it to once again become the fourth-largest cryptocurrency by market cap.

Volatility Spikes as Price Trends Lower

Separate data highlighted by Arab Chain on March 2 shows XRP’s 30-day realized volatility on Binance reaching 1.16, its highest level since March 2025.

Realized volatility measures the annualized standard deviation of daily returns over a 30-day period, and a reading at this level means daily price swings have widened significantly compared to recent months.

At the time of writing, the Ripple token was trading around $1.35, having dipped nearly 2% in the last 24 hours. It also remains down almost 17% over 30 days and about 50% within the past year. Furthermore, the asset is 63% below its all-time high of $3.65, which it reached in July 2025.

However, there might be a positive aspect to consider in the current situation. As Taha pointed out, the April 2025 drop in Binance open interest coincided with a major bottom near $1.80, which was followed by a rally that eventually took XRP to its most recent all-time high.

The post XRP Open Interest Falls 70% to Yearly Lows: What Does it Mean for Ripple’s Price? appeared first on CryptoPotato.

Crypto World

JP Morgan CEO Jamie Dimon says stablecoin issuers paying interest should be regulated as banks

JPMorgan Chase CEO Jamie Dimon said banks want stablecoin issuers that pay interest on customer balances to face the same rules as traditional lenders, sharpening an ongoing debate over U.S. crypto legislation.

In an interview with CNBC on Tuesday, Dimon addressed reported tensions with Coinbase CEO Brian Armstrong, who pulled support for the proposed CLARITY Act just one day before the Senate Banking Committee was scheduled to vote on it. Dimon argued that there needs to be a line between rewards paid on transactions and interest paid on stored balances.

“Rewards are the same as interest,” Dimon said. “If you are going to be holding balances and paying interest, that’s the bank. You should be regulated by a bank.”

Banks would accept a compromise in which crypto platforms offer rewards tied to transactions, he said. But firms that function like deposit-taking institutions should meet the same standards as banks, including capital and liquidity rules, anti-money laundering controls and federal deposit insurance requirements.

Dimon framed the issue as one of fairness and safety.

“Level playing field by product,” he said, arguing that companies offering similar financial services should operate under similar oversight. Without that parity, he warned, risks could build outside the regulated system. Armstrong, on the other hand, has said he believes that banks should be forced to compete instead.

Dimon, however, stressed that JPMorgan does support competition and uses blockchain in its own operations. The bank has developed a deposit token and processes payments and data transfers on distributed ledger systems. “We’re in favor of competition,” he said. “But it’s got to be fair and balanced.”

He also pointed to the broader compliance burden banks carry, from anti-money laundering checks to community lending obligations. Those requirements, he said, are designed to protect the financial system.

“For the safety of the system, not just the fairness of competition,” Dimon said.

The debate over stablecoin oversight has become a central issue in Washington as lawmakers weigh how to regulate digital assets without pushing activity into less transparent corners of the market. Lawmakers are reviewing new draft language circulated by the White House, though the banking and crypto industries have yet to reach agreement on whether stablecoin issuers should be allowed to offer yield on customer balances.

Ripple is expanding its global payments platform to give banks and fintechs a more complete stablecoin workflow, aiming to speed up cross-border settlements and cut the time and capital tied up in traditional networks. The upgrade to Ripple Payments adds capabilities for collecting, custodying, converting, and payout of stablecoins, tying together institutional rails with on-chain settlement. The move marks a deeper push to compete with legacy providers by reducing reliance on pre-funded accounts and correspondent banking chains that can bind up liquidity and slow transfers. The announcement comes as Ripple showcases its growing footprint across markets and its evolving infrastructure footprint in a sector where liquidity, speed, and regulatory clarity increasingly shape the competitive landscape.

Key takeaways

- Ripple Payments now supports end-to-end stablecoin workflows for institutions, including collection, custody, conversion, and payout, expanding its role beyond simple settlement rails.

- The upgrade is designed to reduce dependence on pre-funded accounts and traditional correspondent banking networks, potentially accelerating cross-border transactions and lowering liquidity bottlenecks.

- Ripple’s dollar-pegged token is gaining traction in the ecosystem, with the circulating supply nearing the hundreds of millions and growing as the platform expands adoption across institutions.

- The company has pursued strategic acquisitions to strengthen custody and treasury automation, notably Palisade and Rail, signaling a broader push into asset management and fiat/stablecoin interoperability.

- Regulatory momentum in the United States accompanies this growth, including discussions around a US crypto market structure bill and recent bank-charter considerations, underscoring the coupling of infrastructure growth with oversight.

Tickers mentioned: $RLUSD

Market context: The expansion aligns with a broader push in crypto-financial infrastructure toward regulated, on-chain settlement rails and stablecoin interoperability, as lawmakers weigh oversight frameworks and market structure changes.

Why it matters

The move deepens Ripple’s integration with traditional financial ecosystems by offering a turnkey stablecoin workflow that can be plugged into existing bank processes. For banks and fintechs, this means a potential reduction in the capital that must be set aside for pre-funded accounts and fewer intermediaries in the flow of cross-border payments. By combining custody, conversion, and payout within a single platform, Ripple aims to streamline liquidity management and settlement timing, which could translate into faster settlements and improved working capital efficiency for institutions participating in the network.

Beyond operational efficiencies, the expansion signals a maturation of the stablecoin payments ecosystem. The dollar-pegged token that Ripple supports is gradually gaining scale, and the company is citing real-world institutional usage as it broadens its footprint. The liquidity and settlement rails, already used in more than 60 markets and handling substantial transaction volume, are being extended to accommodate broader use cases, including treasury management and interbank settlements across regions.

Strategically, the push comes as Ripple consolidates its position through acquisitions that bolster custody and fiat-to-stablecoin exchange capabilities. The deals for Palisade and Rail underpin a broader thesis: to offer institutions a more seamless, auditable, and automated treasury stack that can manage digital and fiat assets under a unified framework. This aligns with industry trends toward more robust custody and compliance tooling as crypto assets gain traction in regulated environments.

Regulatory momentum complements the growth. In December, the US Office of the Comptroller of the Currency signaled a path for national bank charters that would cover crypto-adjacent operations, though with clear boundaries around deposit-taking and lending. The development, coupled with ongoing negotiations in Washington over a crypto market structure bill and stablecoin provisions, highlights a year of increasing clarity around how the sector could scale within the traditional financial system. Ripple’s legal leadership has been active in shaping these discussions, underscoring the company’s role in informing and responding to regulatory expectations as the ecosystem expands.

The corporate maneuvers—plus the regulatory dialogue—sit within a broader narrative of capital-efficient, faster payments via on-chain rails that could redefine cross-border liquidity management for financial institutions. As more banks and fintechs look to digital settlement capabilities, Ripple’s end-to-end solution could become a reference architecture for institutional adoption of stablecoins and digitized asset settlement, especially as policy conversations continue in the US and abroad.

What to watch next

- Regulatory milestones: finalization of national bank charter approvals and any concrete steps on the US crypto market structure bill with respect to stablecoins.

- Implementation milestones: timelines for broader integration of the end-to-end stablecoin workflow across additional institutions and regions, and updates on custody/treasury automation deployments from Palisade and Rail.

- Market adoption: indicators of increased institutional usage, including signed partnerships or pilot programs with banks and fintechs beyond the current roster.

- Liquidity and issuance dynamics: monitoring RLUSD (CRYPTO: RLUSD) supply growth and how it translates into on-chain settlement capacity and cross-border flows.

- Geopolitical/regulatory signals: any new guidelines or enforcement actions related to stablecoins and cross-border payments that could influence deployment strategy or product design.

Sources & verification

- Ripple announces end-to-end stablecoin platform expansion within Ripple Payments via Business Wire: Ripple Redefines Payments with End-to-End-Stablecoin Platform and Global Customer Momentum.

- Historical platform data and regional participants cited (AMINA Bank, Banco Genial, ECIB, AltPayNet) in the expansion narrative.

- RLUSD metrics and market data referenced from CoinMarketCap and related Ripple USD coverage.

- Regulatory context including OCC bank-charter discussions and the White House regulatory meeting involving Ripple’s OL team and other industry participants.

- Past acquisitions: Palisade (custody/treasury automation) and Rail (fiat/stablecoin interoperability) and their roles in expanding Ripple’s custody and settlement capabilities.

What the article links to

Ripple expands European footprint with Amina stablecoin payment partnership: https://cointelegraph.com/news/ripple-amina-stablecoin-cross-border-payments-europe

OCC approval discussions: https://cointelegraph.com/news/bitgo-circle-fidelity-bitgo-ripple-occ-approval-bank-conversion

Ripple CEO White House meeting on crypto banking clarity: https://cointelegraph.com/news/ripple-ceo-white-house-meeting-crypto-banking-clarity

Related coverage: Ripple acquired Rail for $200 million: https://cointelegraph.com/news/ripple-acquires-rail

RLUSD price index: https://cointelegraph.com/ripple-usd-price-index

RLUSD market data on CoinMarketCap: https://coinmarketcap.com/currencies/ripple-usd/

Announcement source: https://www.businesswire.com/news/home/20260303432530/en/Ripple-Redefines-Payments-with-End-to-End-Stablecoin-Platform-and-Global-Customer-Momentum?feedref=JjAwJuNHiystnCoBq_hl-bV7DTIYheT0D-1vT4_bKFzt_EW40VMdK6eG-WLfRGUE1fJraLPL1g6AeUGJlCTYs7Oafol48Kkc8KJgZoTHgMu0w8LYSbRdYOj2VdwnuKwa

BitGo Europe GmbH has launched its crypto-as-a-service offering across the European Economic Area, enabling fintechs and banks to integrate regulated crypto custody, trading and fiat on- and off-ramps under the EU’s Markets in Crypto-Assets (MiCA) framework.

According to Tuesday’s announcement, the expansion makes BitGo’s API-based infrastructure available in all 30 EEA countries, allowing institutions to embed wallet, onboarding and settlement services directly into their platforms. The service includes multi-asset wallets and Single Euro Payments Area (SEPA) fiat rails.

BitGo said custodial wallets are insured up to $250 million, subject to terms, and include configurable policy controls and 24/7 operational support. The platform supports buying, selling and holding Bitcoin (BTC) and other supported digital assets within a partner’s existing interface, with settlement handled through BitGo’s infrastructure.

The offering was previously available in the United States through BitGo Bank & Trust and is now operating in Europe via BitGo Europe GmbH, the company’s locally regulated entity.

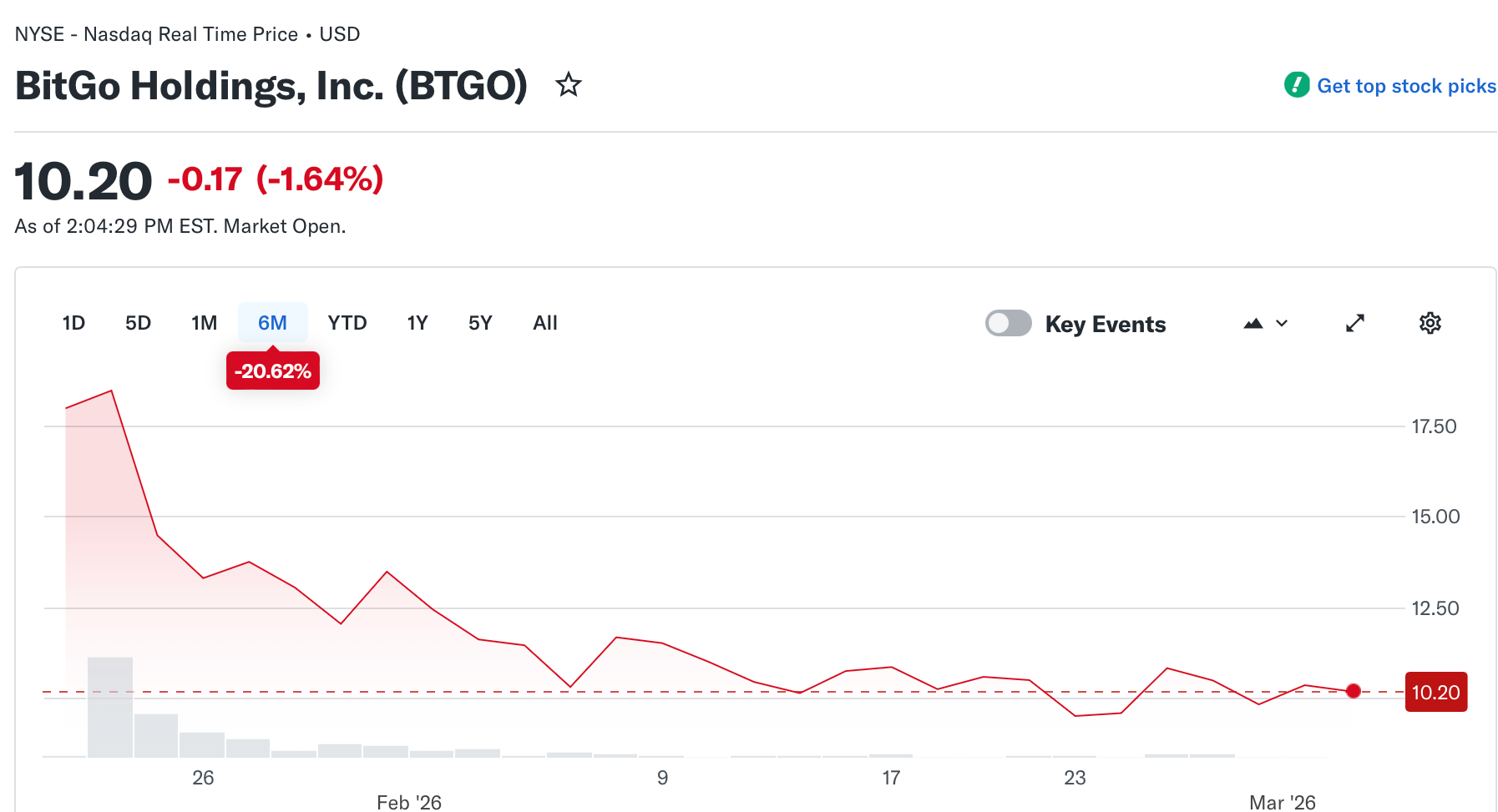

BitGo has operated since 2013 and provides custody, wallets, staking, trading, financing, stablecoins and settlement services to institutional clients globally. The company went public on Jan. 22, trading on the New York Stock Exchange under the ticker BTGO.

BitGo stock was trading at $10.20, down about 1.6% on Tuesday and about 20% since going public, according to Yahoo Finance data at the time of writing.

Related: Stablecoins could weaken bank lending and monetary policy in Europe: ECB

Custody infrastructure expands in Europe

The rollout reflects broader growth in regulated custody infrastructure across Europe following MiCA’s implementation, as financial institutions formalize digital asset services under the EU’s licensing regime. Several banks have opted to work with specialized crypto companies rather than build custody systems internally.

In July, Deutsche Bank moved toward crypto custody through partnerships with Bitpanda’s technology unit and Swiss digital asset infrastructure provider Taurus.

Spain’s BBVA in September said it would rely on Ripple’s institutional custody platform to support its Bitcoin and Ether (ETH) trading and safekeeping services, citing MiCA compliance.

At the market infrastructure level, Clearstream, part of Deutsche Börse, said it would offer Bitcoin and Ether custody and settlement to institutional clients through its Swiss subsidiary Crypto Finance AG.

Others have chosen to structure custody services through licensed European entities. In January, Standard Chartered announced plans to launch digital asset custody in Europe after obtaining a license in Luxembourg, establishing a dedicated EU entity to deliver the service directly.

Magazine: Clarity Act risks repeat of Europe’s mistakes, crypto lawyer warns

Over a third of tracked altcoins now sit near cycle lows despite a broader market stabilization.

Summary

- CryptoQuant data shows 38% of altcoins are trading close to all-time lows, a deeper drawdown than during the post-FTX unwinding phase.

- Analyst Darkfost describes this as the “largest regression of altcoins observed during this cycle,” highlighting persistent structural pressure on non-BTC assets.

- While BTC holds near recent highs, dispersion between majors and smaller caps has widened, with altcoin underperformance pointing to weak liquidity and selective risk appetite.

On-chain analytics firm CryptoQuant reports that 38% of altcoins are currently trading close to their all-time lows, marking a more severe retracement than the period following the collapse of FTX. The metric, highlighted by analyst Darkfost, is designed to capture how many alternative tokens remain under sustained selling pressure, even as the broader market shows signs of stabilization.

In a note summarized on social media, Darkfost describes this as the largest regression in altcoins observed so far in the current cycle, underscoring how uneven the recovery has been between blue-chip assets and the long tail of speculative tokens.

Market participants commenting on the data pointed out that, unlike the post-FTX phase—when forced liquidations and distressed selling drove prices lower—the current environment features relatively fewer obvious forced sellers. Instead, altcoin weakness appears to be driven by a mix of low liquidity, tighter risk budgets, and a rotation into more established names such as BTC and ETH, which have captured the bulk of inflows into spot markets and regulated products. One observer noted that in the FTX aftermath, once the main overhang cleared, many assets staged at least a reflexive bounce, whereas now a significant share of altcoins remains pinned near their lows despite occasional rallies in majors.investing+2

Dispersion and liquidity stress

The divergence described by CryptoQuant has important implications for portfolio construction and risk management across digital assets. Rising dispersion—where some segments of the market trend higher while others grind lower—tends to increase both opportunity and risk, particularly for funds attempting to rotate between themes or capture relative value. With a large share of altcoins near ATL, liquidity in many order books has thinned, raising the impact cost of entering or exiting positions and increasing the potential for sharp, “Bart-style” intraday moves noted by traders.

At the same time, the data suggests a growing concentration of market interest in a smaller set of higher-quality or more narrative-driven assets, including BTC, ETH, and ecosystems such as SOL that continue to see comparatively stronger developer and user activity. Centralized venues like Coinbase have also funneled more volume into a limited basket of listed tokens, further amplifying the relative underperformance of smaller caps that lack deep markets or institutional access. In Europe, evolving regulatory frameworks like MiCA may reinforce this concentration by encouraging platforms to prioritize assets with clearer compliance and disclosure profiles, potentially leaving many fringe altcoins structurally disadvantaged even if broader crypto sentiment improves.

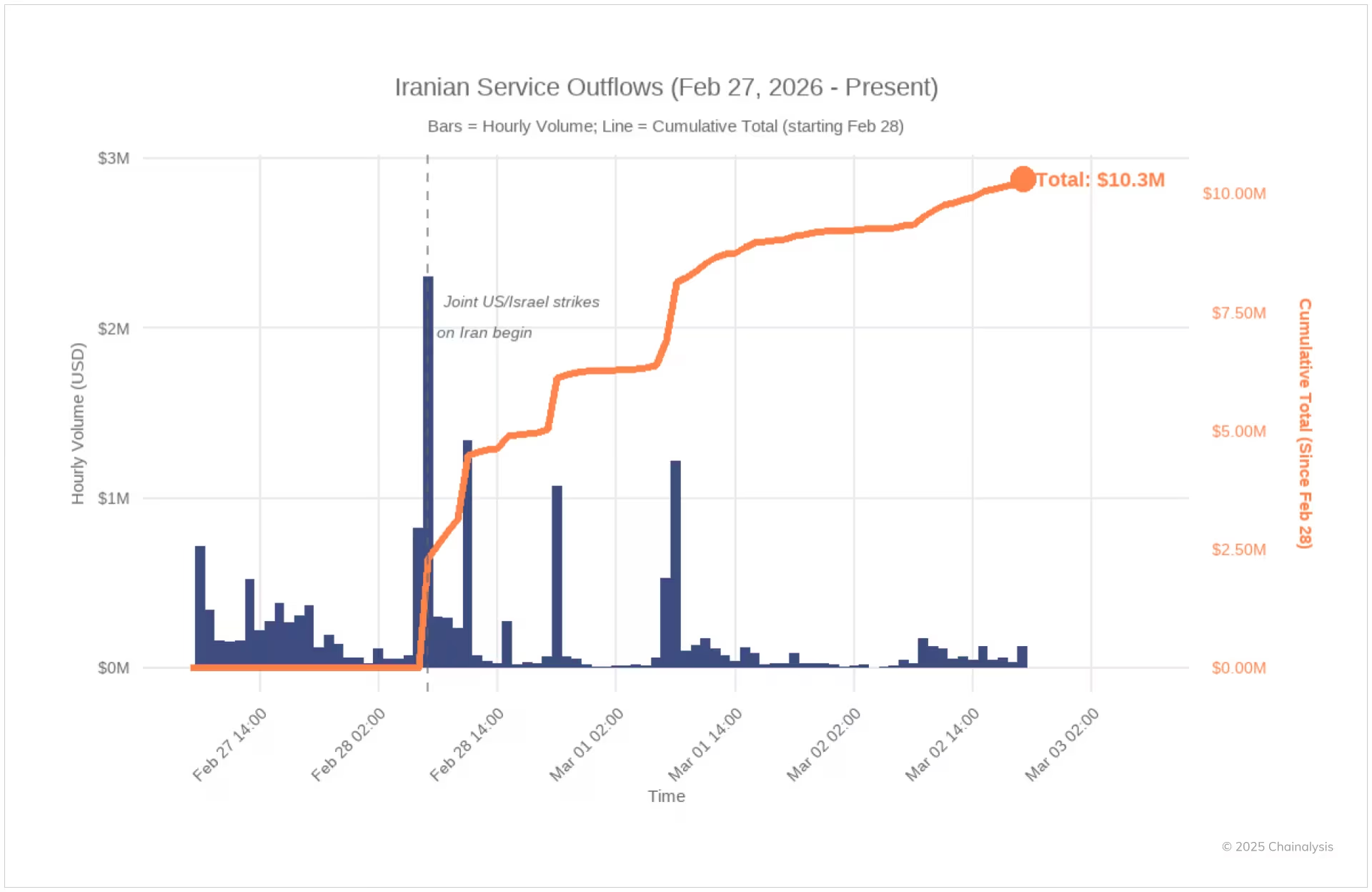

Crypto outflows from Iranian exchanges spiked to $10.3 million, underscoring cryptocurrencies’ role as financial safe havens during geopolitical crises.

Between February 28 and March 2, crypto outflows from Iranian exchanges surged to $10.3 million in the wake of US-Israeli airstrikes.

Nobitex, Iran’s largest cryptocurrency exchange, witnessed a striking 700% rise in outgoing transaction volumes immediately after the airstrikes, as reported by Elliptic. This surge reflects the growing trend of utilizing cryptocurrencies as a financial refuge during periods of instability.

Iran’s crypto ecosystem was valued at $7.8 billion in 2025, with significant activity often linked to geopolitical events, according to Chainalysis. This pattern of on-chain spikes around major shocks, such as the Kerman bombings in early 2024 and direct clashes with Israel in 2024–2025, underscores the correlation between geopolitical crises and crypto market fluctuations.

The recent airstrikes are not the first event to trigger substantial crypto movements within Iran. During a January 8 internet blackout, Bitcoin withdrawals surged before flatlining, only to resume once connectivity was restored. This behavior suggests robust demand for decentralized financial solutions when traditional infrastructure falters.

This article was generated with the assistance of AI workflows.

CFTC chairman Michael Selig plans to enable US-listed crypto perpetual futures within weeks.

Summary

- CFTC chair Michael Selig told attendees the agency aims to clear regulatory obstacles and launch “genuine professional” crypto perpetual futures in the US within about 4 weeks.

- The move is part of “Project Crypto,” a joint SEC–CFTC initiative that includes new guidance for DeFi, prediction markets, and tokenized collateral frameworks.

- BTC and major altcoins saw modest intraday gains while derivatives traders priced in potential onshoring of volume from offshore venues, with expectations for higher regulated futures open interest.

The US Commodity Futures Trading Commission (CFTC) is preparing to clear a formal path for crypto perpetual futures to operate onshore, in what could mark one of the most significant structural shifts for the digital asset derivatives market since the approval of spot exchange-traded products. According to remarks attributed to chairman Michael Selig and relayed via a CoinDesk report, the agency is “working to launch professional futures—genuine professional futures—in the US within approximately the next month,” with multiple policy announcements expected soon. The initiative aims to reverse years of regulatory ambiguity that pushed a large share of perpetual futures activity to offshore platforms, leaving US markets reliant on less standardized products and fragmented liquidity.

Selig’s comments, delivered at a Washington event alongside SEC chair Paul Atkins, frame perpetual futures as a core tool for risk management and price discovery that should exist within a transparent, supervised environment rather than primarily on unregulated exchanges. He argued that the prior approach “failed to create a pathway” for onshore perpetuals, contributing to capital flight and an uneven playing field for US firms. Under the new direction, the CFTC intends to use its rulemaking powers to permit additional tokenized collateral types and to define conditions under which perpetual and other novel derivatives can list and trade, subject to margin, clearing, and conduct safeguards.

Impact on markets and venues

Market participants immediately began debating how onshore perpetuals could reshape flows between US-registered markets and offshore exchanges that have historically dominated perpetual volume. Some commentators suggested that regulated contracts could draw a portion of institutional and professional activity away from lightly supervised venues, especially once larger platforms such as Coinbase expand their CFTC-registered offerings beyond existing structured products. Others questioned whether leverage caps, onboarding requirements, and surveillance obligations might limit the appeal of US-listed perps relative to high-leverage offshore alternatives that remain outside the direct reach of American regulators.

The timing also intersects with broader reforms under “Project Crypto,” which seeks clearer rules for DeFi developers, prediction markets, and retail leveraged products, as well as parallel regulatory developments in other jurisdictions under regimes like MiCA. If successful, onshoring more of the perpetual futures complex could tighten the link between CFTC-supervised benchmarks and spot BTC markets, improving transparency while potentially reducing the systemic risk associated with opaque, cross-border leverage cycles. For traders and firms, the coming announcements will determine how quickly new contracts can list, which collateral will qualify, and whether a meaningful share of global perpetual liquidity migrates into the US regulatory perimeter.

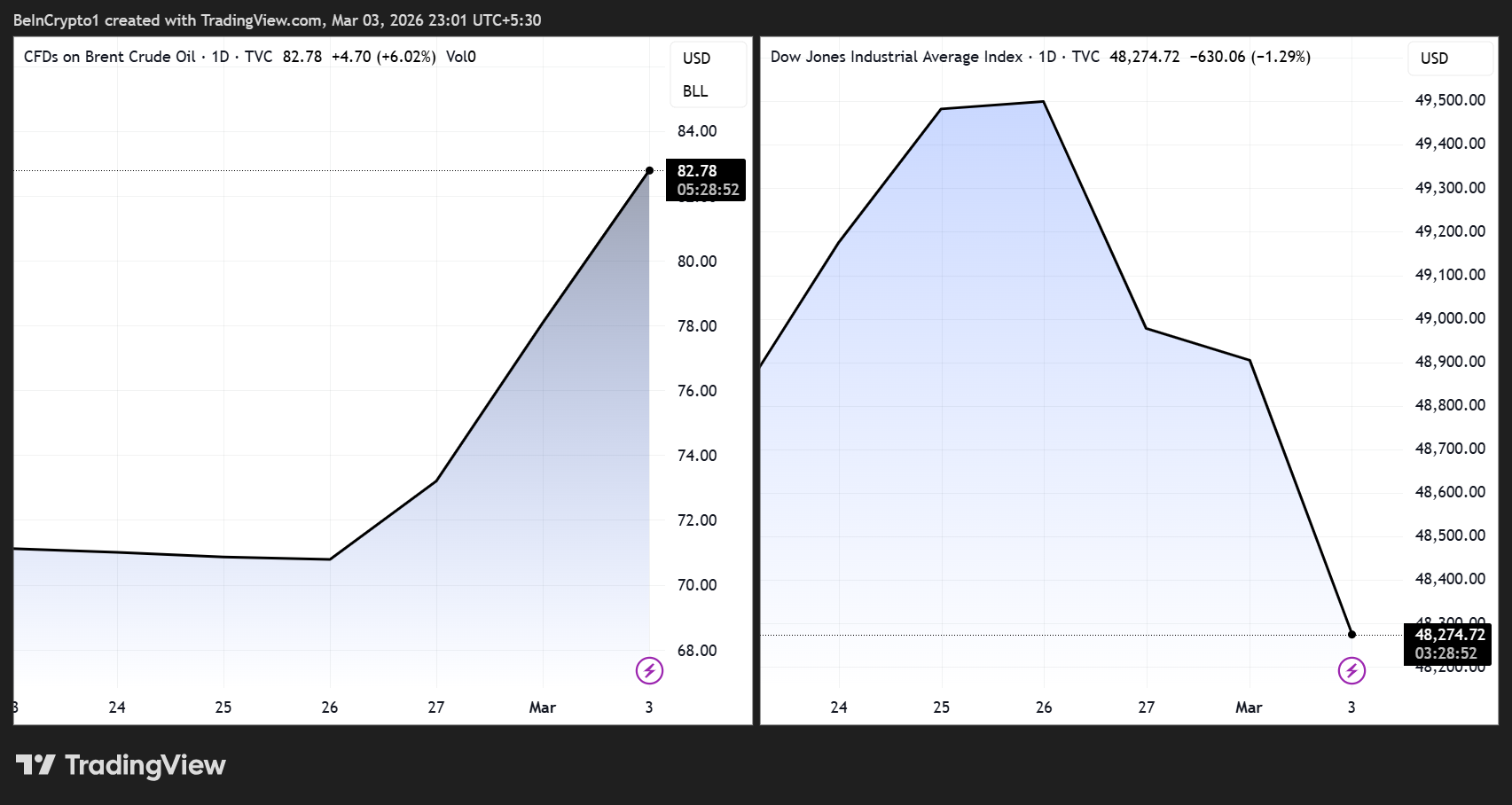

Six major geopolitical and economic actions under President Donald Trump since mid-2025 have shared one precise tactical detail: they all happened on Friday nights, after equity markets closed and before futures liquidity fully developed.

This is not a coincidence. It is, according to pattern analysis, the single most consistent and operationally significant element of Trump’s conflict strategy — and arguably the most tradeable timing signal in macro markets today.

Trump’s Friday Night Strike Pattern Is the Most Tradeable Signal in Macro Right Now

Understanding why Trump uses Friday nights, and what happens to Bitcoin (BTC), equities, oil, and bonds in the 60 hours that follow, could give traders and investors a structural edge that most market participants are not pricing.

“Obviously, Trump chose weekends to carry out combat ops in Venezuela and Iran. Smart move to buy time before Wall Street opens and minimize market shocks. But here’s the structural shift: Markets used to rest on weekends. Now they don’t,” wrote Gracy Chen, CEO at Bitget.

Six Events Show A Singular Trump Playbook

The documented list by financial research firm The Kobeissi Letter is specific:

- On June 21, US and Israeli forces struck Iranian nuclear sites.

- On September 1, the US military targeted Caribbean drug boats.

- On October 10, a 100% tariff threat against China dropped after market close.

- On November 29, Trump closed Venezuelan airspace in its entirety.

- On December 25, military action commenced in Nigeria.

- On February 28, 2026, US forces struck Iran directly.

Every single one landed on a Friday night or early Saturday morning.

The pattern extends to Trump’s corporate pressure campaigns. On August 11, 2025, the Trump administration announced an Intel deal after weeks of public pressure on CEO Lip-Bu Tan, again, structured to land outside active trading hours.

That position returned over 80% in under two months for those who tracked the escalation sequence from the beginning.

The consistency across geopolitical strikes, tariff actions, and corporate confrontations is not accidental. It reflects a deliberate understanding of how financial markets process shock.

Why Friday Night? The Market Psychology Behind the Timing

When a major geopolitical event occurs during active market hours, price discovery breaks down. Liquidity thins immediately. Algorithms amplify every directional tick.

Intraday swings create panic that feeds on itself, producing disorderly markets that are difficult for any participant, including the administration, to read or control.

A Friday night announcement changes the dynamic entirely. Investors, institutions, and governments have a full weekend to process information, consult advisors, and model scenarios before a single share trades.

The shock is real, but the response is measured. Futures markets absorb the initial repricing on Sunday evening at 6 PM ET. This is a low-liquidity session where price moves are sharp but short-lived. Similarly, the gap between the emotional reaction and the rational reassessment becomes visible within hours.

This matters for Trump’s negotiation strategy in a specific way. Trump, by his own description and observable behavior, is highly responsive to financial market performance.

A disorderly market reaction during trading hours creates political and economic pressure, complicating his objectives.

A Friday night announcement gives markets time to digest, and gives Trump’s team time to read the reaction and calibrate the next message before Monday open.

The result: every Friday night event has been followed by:

- A Sunday evening futures shock

- A partial Monday recovery, and then

- A second, more sustained move in the same direction as the initial shock.

Is this three-phase sequence now repeatable enough to trade?

The 60-Hour Window: What Each Asset Does

The 60-hour window from Friday close to Monday open has produced near-identical cross-asset sequences across all six confirmed events.

At Sunday open, Bitcoin sells off 5–12% as it trades as a pure risk asset, with equity correlation spiking above 0.8. Ethereum (ETH) and altcoins fall by 15–25% from pre-event levels in the first 48 hours, as liquidity exits the most volatile assets first.

S&P 500 futures gap down 1.5–3%. Oil spikes 5–10% depending on proximity to energy infrastructure — Iran-related events have produced the sharpest initial moves.

The US dollar catches a strong safe-haven bid. Ten-year Treasury yields drop sharply as flight-to-quality demand floods the bond market.

By Monday morning, a partial reversal begins. Markets price a short engagement based on Trump’s well-documented preference for deals over prolonged conflicts.

BTC recovers 40–60% of its Sunday drawdown. Oil gives back 30–50% of its initial spike. Equity futures stabilize.

This Monday recovery is where most retail traders make their critical mistake.

The partial reversal appears to be a resolution signal. It is not. In every prior cycle, the Monday stabilization has failed. A second, more sustained leg in the original direction (lower equities, higher oil, weaker crypto) follows within 48–72 hours as the market acknowledges the conflict will not resolve quickly.

The correct trading behavior in the 60-hour window is not to react at Sunday open, because:

- Spreads are too wide

- Algorithms are front-running every move, and

- The liquidity is not there for clean execution.

The actionable entry for equities and BTC has historically arrived 48–72 hours after the initial shock, not at the shock itself.

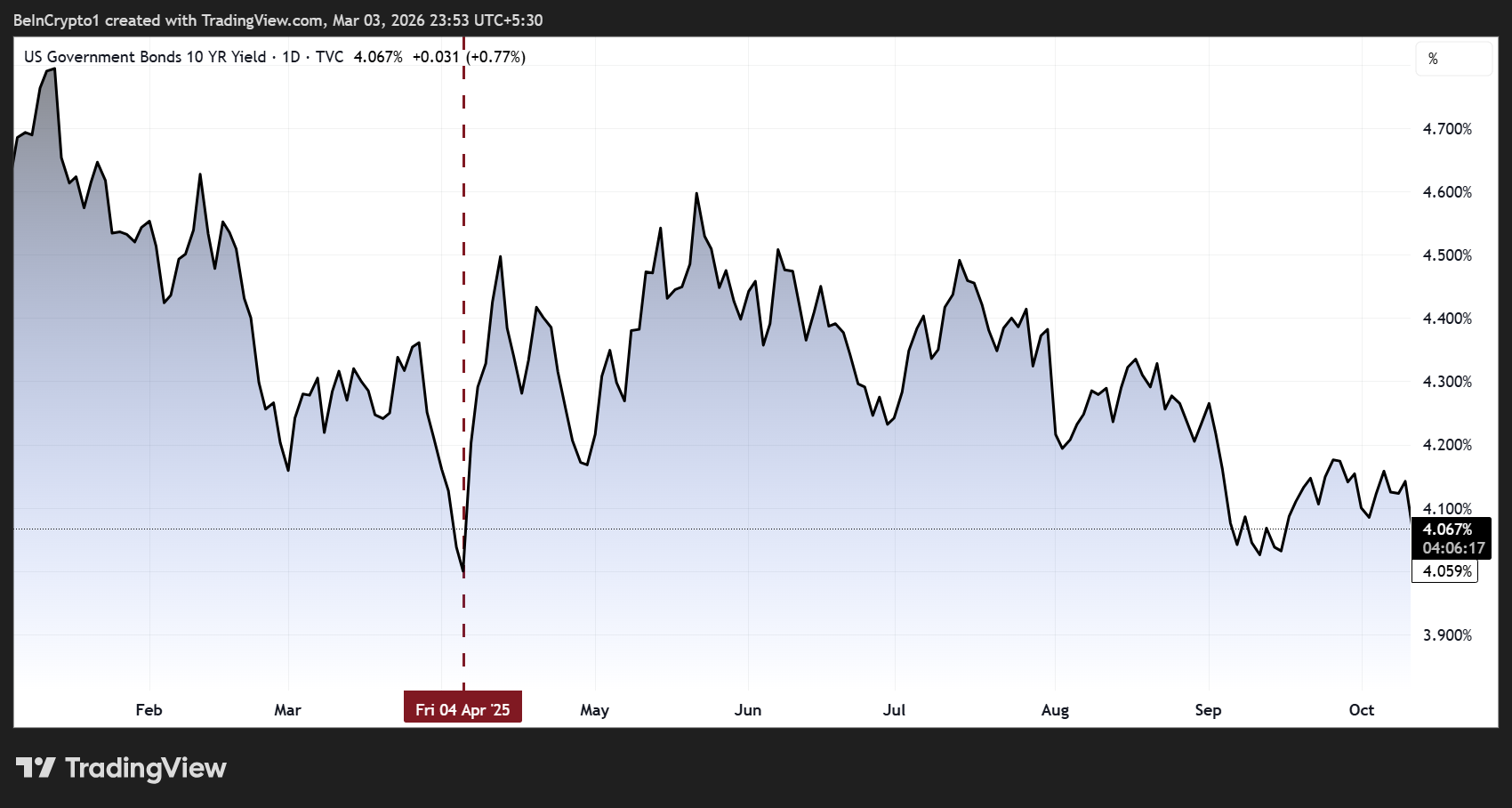

The Bond Market Is the Real Signal

One element of the Friday night pattern that most crypto and equity traders overlook is the bond market’s role as a leading indicator of resolution.

In the April 9, 2025, tariff pause, the most significant de-escalation event of Trump’s second term, it was not equity market weakness that triggered the pivot. It was the bond market.

10 year Treasury yields surged sharply in the days leading up to April 9, signaling structural stress in fixed income that the administration could not ignore. When yields moved, Trump moved.

This dynamic has repeated across multiple cycles. Equity weakness gets bought. Oil spikes get dismissed as temporary.

However, when bond market stress becomes acute (when the 10-year yield is moving in ways that imply credit market dysfunction rather than simple flight-to-quality) the probability of de-escalation language rises sharply.

Traders positioning around the Friday night pattern should therefore monitor the bond market as the leading indicator of Trump’s next pivot, not equity prices or crypto sentiment.

What Makes This Pattern Durable?

The Friday night strike pattern has survived six confirmed events across radically different conflict types: military, tariff, corporate, and geopolitical, without breaking.

That durability comes from the underlying logic being structural rather than tactical. Trump’s three core second-term policy objectives are:

- Lowering inflation

- Cutting gasoline prices to $2 per gallon, and

- Positioning as a peace president in a midterm election year.

Every Friday night event creates short-term upward pressure on oil and inflation expectations. The Friday night timing passes as the mechanism Trump may be using to contain that pressure.

If history is any guide, he gives the markets a weekend to absorb shock before consumer-facing data, like gasoline prices at the pump, can register the move politically.

The pattern will break when one of two things changes:

- Trump abandons the deal-making framework entirely in favor of a genuinely prolonged conflict, or

- The Friday night announcement loses its market-timing advantage as participants anticipate and front-run the window.

Neither has happened across 13 months of observation.

Until one of those conditions is met, the 60-hour post-strike sequence (Sunday shock, Monday partial recovery, Tuesday confirmation) remains the most consistently repeatable cross-asset trading pattern in current macro markets.

As of March 3, 2026, with Brent crude above $85 per barrel and the Dow Jones Industrial Average down roughly 1,100 points, markets are in the phase that has historically preceded Trump’s conditional de-escalation signals.

The Friday night that created this moment is already history. The question is whether traders are positioned for what the pattern says comes next.

This article is for informational purposes only and does not constitute financial or investment advice.

Follow us on X to get the latest news as it happens

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The Chairs of the U.S. CFTC and SEC said they’re working together to keep on-chain finance, prediction markets, and perpetuals futures in the country.

U.S. Commodity Futures Trading Commission (CFTC) Chairman Michael Selig said that the agency is “modernizing” its rules “so that there’s a place” for decentralized finance in the United States.

Speaking during a panel discussion with Securities and Exchange Commssion (SEC) Chairman Paul Atkins at the Milken Institute today, March 3, Selig said that the agency is working on regulations around on-chain markets to “accommodate on-chain software systems.”

Selig noted that DeFi protocols have faced years of regulatory uncertainty in the U.S. — as well as regulation by enforcement — and that the CFTC wants to provide clarity as to when and how DeFi protocols fall under its jurisdiction:

“[…]The prior administration characterized many of these […] types of software systems as a type of exchange or broker. We’re gonna make sure it’s very clear as to what implicates the CFTC’s regulations and what doesn’t,” Selig stated, adding:

“And to the extent that an on-chain software system or frontend does implicate our rules and regulations we’re modernizing and future proofing those rules so that there’s a place for all of that.”

SEC chair Atkins echoed the sentiment, reiterating that the SEC is committed to working together with the CFTC on crypto regulations.

The CFTC Chairman said the two regulators are partnering to provide a “taxonomy” for crypto assets, namely by defining more clearly what’s a security and what’s not under U.S. law.

“Part of that starts with our existing derivatives markets,” Selig argued, continuing, “Many of the firms want to move on-chain. The prior administration drove a lot of these firms, and the liquidity, offshore.”

‘True’ Perps Are Coming to the US

The CFTC Chairman also commented on perpetual futures markets, saying that regulatory uncertainty under previous administrations had prevented these markets from being offered on U.S. regulated platforms.

Selig said, however, that regulated perps are coming to the U.S. “within the next month or so”:

“We need to have that liquidity here in the U.S. and we need the right investor protections to ensure that these firms don’t blow up and affect our shores. So we’re working toward getting […] true perpetual futures […] here in the U.S. within the next month or so.”

Prediction Markets Need Clarity

During the panel discussion, the two Chairs were also asked about prediction markets, which exploded into mainstream popularity over the past year.

Chairman Selig said that the CFTC and SEC have a lot of shared authority in regard to prediction markets, stating that clarity for platforms like Kalshi and Polymarket is also coming soon.

“We’re going to be setting very clear standards as to what can be self-certified in our markets and what cannot and how to evaluate the different products that are offered in the space,” Selig said, adding:

“We are also planning to go forward with an advanced notice of proposed rulemaking in the near future that will set the stage for more fulsome rulemaking.”

The comments come just a week after the CFTC announced it was filing a “friend-of-the-court” brief in Nevada in support of Crypto.com, arguing more broadly that prediction markets should fall under the federal agency’s supervision, not that of separate state regulators.

“We’re really excited to continue to modernize and upgrade our rules for the 21st century,” Selig concluded.

This regulatory shift in the U.S. was also marked last summer by the SEC’s unveiling of its broader initiative, “Project Crypto,” which aims to “modernize” securities regulations in the U.S. in an effort to bring capital markets on-chain.

Meanwhile, the crypto industry is still waiting for U.S. lawmakers to pass a broader crypto market structure bill, as discussion continue in the Senate.

The world’s largest cryptocurrency exchange announced another amendment to its platform, which is particularly focused on popular altcoins such as Avalanche (AVAX), Litecoin (LTC), Zcash (ZEC), and more.

It also plans to remove certain trading pairs that no longer meet the necessary criteria.

The Newcomers

Binance said it will open trading for AVAX/U, LINK/U, LTC/U, PAXG/U, and ZEC/U on March 5th. Trading bots services for these pairs will be enabled on the same day.

The initiative is once again centered on U (United Stables) – a stablecoin launched in late 2025 and pegged to the American dollar. To stimulate adoption, Binance will introduce a zero-fee promotion for eligible users on U spot and margin trading pairs.

Over the past few weeks, the exchange has added ADA/U, DOGE/U, and PEPE/U to its Cross Margin section, while XRP/U, SUI/U, ASTER/U, and PAXG/U were listed on its Spot market.

AVAX, LINK, LTC, and ZEC are all in green territory today (March 3rd), but their gains are likely driven by the broader market rebound rather than Binance’s announcement. While the company can trigger a major pump for a given cryptocurrency, this usually happens after an initial listing, not after introducing additional pairs.

Meanwhile, PAX Gold (PAXG) is down 4% on a daily scale following a pullback in the price of the yellow metal. The cryptocurrency is backed by real, physical gold, where each token represents one fine troy ounce stored in secure vaults.

These Pairs Will be Removed

In addition to offering more trading options, Binance has also chosen to delist certain pairs that no longer meet its standards. It will say goodbye to the cross margin pairs CHZ/BTC, CAKE/BTC, ENA/BTC, UNI/ETH, CRV/BTC, INJ/BTC, XTZ/BTC, and the isolated margin ones FET/BTC, OP/BTC, PAXG/BTC, CHZ/BTC, CAKE/BTC, ENA/BTC, CRV/BTC, INJ/BTC, XTZ/BTC on March 5th.

“Users will no longer be able to transfer any amount of assets of the aforementioned pair(s) via manual transfers and Auto-Transfer Mode into their Isolated Margin accounts. If users hold outstanding liabilities of said tokens, these users may only manually transfer up to the amount of liabilities of that token into their Isolated Margin accounts, less any collateral already available,” the company explained.

In addition, Binance warned that clients will not be able to update their positions during the delisting process, which may take approximately three hours.

The disclosure hasn’t weighed on the prices of the involved cryptocurrency, as most have still posted daily gains in line with the broader market rebound.

The post Important Binance Update Affecting ZEC, LTC, and Other Altcoin Traders: Details appeared first on CryptoPotato.

This morning, three days after US-Israeli military strikes killed Supreme leader of Iran Ayatollah Ali Khamenei, Polymarket traders thought they’d found his replacement — and then lost more than half of their position values by lunchtime.

Alireza Arafi, a little-known cleric, was the frontrunner among binary options traders on Polymarket at a 22% odds rate this morning. However, he’d plummeted to 9% at time of writing.

With Khamenei dead and Iran’s theocratic leadership in disarray, its de facto interim leadership council, the Expediency Discernment Council, named Arafi on Sunday to join Masoud Pezeshkian and Gholam-Hossein Mohseni-Eje’i in a three-person body governing the country under Article 111 of its constitution.

Arafi is also deputy chairman of the Assembly of Experts, the 88-member clerical body that normally selects the country’s supreme leader. Earlier today, Israel detonated munitions at the Assembly of Experts building.

Finally, Arafi is a member of the Guardian Council, which vets candidates for that very assembly.

In summary, Arafi currently holds an interim leadership position alongside the country’s two other highest-ranking men, helps decide who may run in contention, and sits on the body that votes for candidates.

Sometimes, Polymarket traders get it wrong. Other times, they simply read an org chart.

Read more: Polymarket ends trading loophole for bitcoin quants

The seminary loyalist sitting on Iran’s top committees

Local media has described Arafi as a “staunch loyalist to the core ideology of the Islamic Republic.” In fact, he formerly headed one of the regime’s most prestigious religious schools, Al-Mustafa International University.

Born in 1959, Arafi has spent his entire career rising through Iran’s clerical bureaucracy. The late Khamenei personally appointed him to lead the country’s seminaries in 2016 — a powerful position in the theocratic state — and then promoted him to the Guardian Council in 2019.

Each successive accolade in his regime’s form of Islam makes Arafi a better candidate to become Ayatollah, the highest title of Twelver Shia clergy and common parlance for Iran’s supreme leader.

However, his promotion is certainly not guaranteed, hence Polymarket’s betting line at a mere 22% this morning and just 9% now.

When trading offshore binary options, payouts are never sure until funds clear a bank account.

When Donald Trump, for example, called Kevin Hassett a “potential Fed Chair” and “a respected person, that I can tell you,” traders rushed to place trades at 70% on Polymarket and 74% on Kalshi.

Those gamblers lost it all when Trump instead nominated Kevin Warsh.

No consensus about who will become Iran’s supreme leader

Arafi’s competitors among Polymarket traders tell a story of how little consensus exists about Iran’s leadership.

Gholam-Hossein Mohseni-Eje’i, the judiciary chief and Arafi’s fellow council member, sits at 17%.

Hassan Khomeini, grandson of the revolution’s founder, was at 15% this morning but crashed to 8% by time of writing. Mojtaba Khamenei, the late Ayatollah’s son, trades at just 7% but rose to 19% by time of writing.

An 13% bet that Polymarket abolishes its own market entirely, likely due to death of candidates, rounds out the field’s more exotic wagers.

This market was created on February 28 and resolves on December 31. Iran’s Assembly of Experts is expected to name a successor within days, although many months remain before December 31.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Google releases Gemini 3.1 Flash Lite at 1/8th the cost of Pro

Let’s Watch 20 Minutes of People Making Bad Financial Decisions

4 UK travel companies close with flights and trips cancelled

-

Politics5 days ago

Politics5 days agoITV enters Gaza with IDF amid ongoing genocide

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Iris Top

-

Politics13 hours ago

Politics13 hours agoAlan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

-

Tech3 days ago

Tech3 days agoUnihertz’s Titan 2 Elite Arrives Just as Physical Keyboards Refuse to Fade Away

-

NewsBeat6 days ago

NewsBeat6 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

Sports4 days ago

The Vikings Need a Duck

-

NewsBeat3 days ago

NewsBeat3 days agoDubai flights cancelled as Brit told airspace closed ’10 minutes after boarding’

-

NewsBeat6 days ago

NewsBeat6 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat2 days ago

NewsBeat2 days ago‘Significant’ damage to boarded-up Horden house after fire

-

NewsBeat3 days ago

NewsBeat3 days agoThe empty pub on busy Cambridge road that has been boarded up for years

-

NewsBeat3 days ago

NewsBeat3 days agoAbusive parents will now be treated like sex offenders and placed on a ‘child cruelty register’ | News UK

-

NewsBeat7 days ago

NewsBeat7 days agoPolice latest as search for missing woman enters day nine

-

Entertainment2 days ago

Entertainment2 days agoBaby Gear Guide: Strollers, Car Seats

-

Business6 days ago

Business6 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

Business5 days ago

Business5 days agoOnly 4% of women globally reside in countries that offer almost complete legal equality

-

Tech4 days ago

Tech4 days agoNASA Reveals Identity of Astronaut Who Suffered Medical Incident Aboard ISS

-

NewsBeat3 days ago

NewsBeat3 days agoEmirates confirms when flights will resume amid Dubai airport chaos

-

Politics3 days ago

FIFA hypocrisy after Israel murder over 400 Palestinian footballers

-

Crypto World7 days ago

Crypto World7 days agoEntering new markets without increasing payment costs

-

Crypto World5 days ago

Crypto World5 days agoFrom Crypto Treasury to RWA: ETHZilla Retreats and Relaunches as Forum Markets on Nasdaq