Crypto World

U.S. judge freezes BlockFills assets in dispute over 70 bitcoin with creditor Dominion Capital

A U.S. federal judge has issued a temporary restraining order (TRO) against crypto lender BlockFills in a lawsuit brought by Dominion Capital, temporarily freezing assets tied to the dispute, according to a filing seen by CoinDesk.

In a complaint dated February 27, Dominion alleged that BlockFills misappropriated and unlawfully retained millions of dollars’ worth of customer crypto assets, commingled client assets and concealed heavy losses.

Dominion claimed BlockFills concealed the misuse of customer funds and refused to return the company’s assets after suspending withdrawals in February. As part of the complaint, the investment firm sought an asset freeze to protect its crypto trapped on Blockfills’ platform, which was granted by the court.

In an order filed March 3 in the U.S. District Court for the Southern District of New York, federal Judge Mary Kay Vyskocil barred the firm from transferring or disposing of 70.6 bitcoin allegedly belonging to Dominion, or moving assets outside the United States while the case proceeds.

The court also ordered Blockfills, which is backed by trading giant Susquehanna, to account for and segregate customer funds, including Dominion’s bitcoin, pending a hearing on a possible preliminary injunction.

CoinDesk reported last month that the crypto lender had incurred losses of around $75 million during the recent market downturn, and was looking for a buyer or emergency funding

BlockFills is a Chicago-based crypto trading and lending firm that provides liquidity, financing and risk-management services to institutional clients. Its platform facilitates crypto lending and borrowing, derivatives trading and over-the-counter (OTC) execution for hedge funds, asset managers, market makers and mining companies.

A Blockfills spokesperson said as a matter of policy the firm does not comment on pending litigation. Dominion Capital declined to comment.

A temporary restraining order in the U.S. is an emergency court order that temporarily stops someone from taking a specific action until the court can hold a full hearing. It’s commonly used in legal disputes involving money, assets or financial activity to prevent immediate harm.

The TRO was issued without notice to BlockFills, with the court citing a risk of “immediate and irreparable injury,” noting the firm had suspended client withdrawals and that insolvency could be imminent.

BlockFills must respond by March 17, when the temporary order is set to expire unless extended by the court.

Dominion Capital is a New York-based private investment firm and family office that invests across private equity, structured finance and digital assets, including backing bitcoin mining companies such as Bitfarms (BITF).

Tough times

Blockfills said it was halting customer withdrawals and deposits on Feb. 11 due to recent market and financial conditions.

The firm said at the time that it was working with investors and clients to reach a swift resolution and restore liquidity to the platform. CoinDesk subsequently learned that the crypto lender had incurred losses of around $75 million in the recent market downturn and was seeking a buyer or emergency funding.

CoinDesk also reported that Nicholas Hammer, co-founder and CEO of Blockfills, has stepped down from his leadership role. The firm’s website now lists Joseph Perry as the interim CEO.

Blockfills said it processed over $60 billion in trading volume in 2025, a 28% increase from the prior year, and is among the more active institutional crypto lending and borrowing desks. It serves about 2,000 institutional clients, including hedge funds, asset managers and mining firms.

“The company is now hurtling towards bankruptcy,” according to insolvency professional Thomas Braziel, founder of 117 Partners.

“After something like this, no serious institution is touching the platform,” Braziel said. “They are going to have to file for bankruptcy.”

The New York Law Journal first reported news of the Dominion complaint on Monday.

Read more: Blockfills co-founder and CEO Nicholas Hammer has stepped down

Crypto World

ZeroHash applies for national trust bank charter to expand regulated stablecoin services

ZeroHash, which develops behind-the-scenes crypto infrastructure for businesses, said it applied for a National Trust Bank Charter from the U.S. Office of the Comptroller of the Currency (OCC), looking to operate under federal regulatory oversight.

If approved, the charter would give ZeroHash permission to issue stablecoins, custody digital assets and manage reserves under direct federal oversight. It would not be allowed to take customer deposits or engage in commercial lending.

That status could allow the Chicago-based company, which already holds licenses in 51 U.S. jurisdictions and operates internationally, to expand its stablecoin and digital asset services under a single federal framework, rather than navigating a patchwork of state-by-state rules.

ZeroHash is following a path forged by a number of other crypto companies. In the past month, several firms have received initial approval for national bank trust charters. These include Stripe’s stablecoin firm Bridge and cryptocurrency exchange Crypto.com. In December, Circle Internet (CRCL), Ripple, Paxos, Fidelity Digital Assets and BitGo all received similar approvals.

Founded in 2017, ZeroHash’s platform enables companies to embed stablecoins and digital asset functionality into services like payments, trading and payroll.

Clients include financial heavyweights like Morgan Stanley, Interactive Brokers, Stripe and Franklin Templeton.

In practical terms, a federal trust charter would let ZeroHash offer services that align with recent legislative developments, including provisions in the Genius Act, which clarifies the legal treatment of stablecoins in the U.S.

The OCC is now reviewing the application. No timeline for approval has been given.

US Bitcoin miner CleanSpark last month sold 553 Bitcoin from its February production for about $36.6 million, while producing 568 BTC during the month, according to the company’s latest operational update.

The company ended February with 13,363 BTC (BTC) in its treasury and continued expanding its infrastructure by completing the closing on a second Texas campus that adds 300 megawatts of ERCOT-approved power capacity.

The Electric Reliability Council of Texas, or ERCOT, operates the state’s electrical grid.

CleanSpark said its deployed fleet totaled 235,588 mining machines at the end of February, operating with 50 EH/s peak hashrate, a measure of mining computing power, and 43.2 EH/s average hashrate.

Across its power portfolio, the company has 1.8 gigawatts of capacity under contract, with 808 megawatts currently in use.

CleanSpark said it has produced 1,141 BTC year-to-date, as of Feb. 28. The company also said 1,086 BTC of its holdings are posted as collateral or receivable in connection with derivatives transactions.

The company is also positioning parts of its infrastructure to support artificial intelligence and high-performance computing workloads, reflecting a broader shift among Bitcoin miners seeking to monetize power-dense data center capacity beyond crypto mining.

At the time of writing, the company’s stock was down about 7.5% on the day, according to Yahoo Finance data. Sector-tracking exchange-traded fund CoinShares Bitcoin Mining ETF was down 6.4%, at the same time.

Related: Ex-OpenAI researcher’s hedge fund reveals big Bitcoin miner bets in new SEC filing

Miners sell off Bitcoin in 2026

CleanSpark is not alone in selling Bitcoin, as several publicly traded miners have recently liquidated portions of their holdings to fund infrastructure expansion and artificial intelligence data center projects.

Bitcoin miner Riot Platforms said it sold 1,818 BTC in December for about $161.6 million, as part of a strategy shift toward monetizing its power and data center infrastructure, including support for AI workloads. The company reported in January it held 18,005 BTC as of Dec. 31, down from 19,368 BTC a month earlier, after producing 460 BTC during December.

In February, Bitdeer said it had liquidated its entire corporate Bitcoin treasury. The Bitcoin miner reported producing 189.8 BTC during the period, selling the full amount along with an additional 943.1 BTC from its existing reserves.

Core Scientific said during its fourth-quarter earnings call on March 2 that it sold about 1,900 Bitcoin for roughly $175 million in January, reducing its holdings to fewer than 1,000 BTC.

On Thursday, the company said it secured a $500 million credit facility from Morgan Stanley, which it will use to fund infrastructure supporting high-density computing workloads such as AI and high-performance computing (HPC).

Rumors have also circulated about MARA Holdings, the second-largest corporate Bitcoin treasury holder with 53,822 BTC on its balance sheet, suggesting the miner may begin selling its reserves.

However, MARA vice president of investor relations Robert Samuels dismissed the speculation in a post on X on Tuesday, saying the company has not changed its core treasury strategy.

Magazine: What’s a ‘Network State’ and are there real-life examples? Big Questions

CleanSpark (CLSK), a U.S.-based bitcoin mining company that operates large-scale data centers, sold almost all the bitcoin it produced last month to generate cash for an expansion into artificial intelligence (AI) and high-performance computing (HPC).

The Nasdaq-listed miner produced 568 BTC in February and sold 553 BTC, roughly 97%, according to its latest operational update. The sales generated about $36.65 million in proceeds at an average price of $66,279 per bitcoin, one of the highest production-to-sales ratios the company has reported.

The sale reflects a broader trend among bitcoin miners pivoting toward AI and HPC, with companies increasingly selling either new production or reducing their balance-sheet holdings to help fund new data center and infrastructure development.

CleanSpark still maintains a sizable treasury. As of Feb. 28, it held 13,363 BTC, with 1,086 BTC pledged as collateral or recorded as receivables related to derivative transactions.

Operationally, the company continues to scale its mining platform. CleanSpark reported 50 EH/s of operational hashrate, roughly 7 percent of the global network’s computing power.

The company also closed on a second Texas campus, adding 300 megawatts of ERCOT approved capacity and bringing its total contracted power portfolio to 1.8 gigawatts.

Key takeaways:

-

ETH derivatives signal a shift to safety as professional desks hedge against downside risks and global instability.

-

Institutional preference for decentralization keeps Ethereum dominant despite its recent drop in network activity.

Ether (ETH) price dropped by 6% following a brief rally to $2,200 on Wednesday, tracking a downturn in US equities as the war in Iran entered its sixth day. Disruptions to global oil production and Middle East natural gas shipping pushed WTI crude prices to levels not seen since July 2024.

Investors lowered their economic growth outlook as the conflict escalated and moved to a risk-off posture.

Traders’ sentiment was further pressured as the Trump administration faced a legal setback on its import tariffs. A Federal court on Monday rejected a Justice Department request to pause the case for 90 days, effectively striking down the administration’s use of emergency powers for trade levies.

Ether remains caught in this macroeconomic crossfire, which has stifled momentum despite a 22% recovery from the $1,800 retest on Feb. 24. Onchain data and derivatives markets currently reflect significant apathy from bulls.

The ETH 30-day futures annualized premium sits well below the 5% neutral threshold, signaling a lack of demand for bullish leverage. However, this metric is weighed down by the fact that ETH trades 58% below its August 2025 all-time high of $4,956. To gauge whether professional desks anticipate further downside, one must analyze the options market.

When whales and market makers seek protection against price drops, the ETH options skew (put-call) typically rises above the 6% neutral mark. Extreme market stress can push this indicator past 15%.

The ETH options skew reached 7% on Thursday after briefly touching neutral levels a day prior. This persistent skepticism among professional traders provides bears with the necessary leverage to fuel further uncertainty. Beyond external macro pressures, including US private credit losses and rising corporate layoffs, Ether continues to face its own idiosyncratic headwinds.

Ethereum is positioned to capture the pickup in DApps demand

Ethereum network activity has stagnated following a modest rally in early February. Consistent demand for blockchain utility remains essential for sustainable ETH price action and reducing inflationary pressure. The built-in burn mechanism of Ethereum depends on competition to enter the validation queue, a process typically fueled by decentralized exchange (DEX) activity.

Weekly DEX volumes on the Ethereum network recently hit $12.6 billion, falling from $20.2 billion one month prior. Decentralized application (DApp) revenues dropped to $14.1 million over seven days, marking a 47% decline from the previous month. Competing blockchains have seen a similar trend, as DEX volumes on Solana also decreased by 50% over the same 30-day window.

Related: Bitcoin trader sees ‘lower soon’ as BTC price starts to erase $74K breakout

Despite the weak onchain metrics, ETH is well-positioned to capture an eventual pickup in DApp activity due to its dominance in total value locked (TVL). When including layer-2 scaling solutions, the Ethereum ecosystem accounts for nearly 65% of the total blockchain market TVL.

Related: 38% of altcoins near all-time lows, worse than FTX crash–Analyst

The Ethereum base layer holds $55.4 billion in TVL, while its leading competitor Solana, accounts for $6.8 billion. This gap serves as evidence of a preference among institutional investors for decentralization over the lower fees and faster user experiences offered by networks like Solana and BNB Chain.

The current weakness in Ether derivatives and onchain metrics does not necessarily signal an imminent price crash. Market sentiment can shift quickly toward a sustained bullish momentum if ETH reclaims the $2,400 level. For the moment, the Ether price remains closely tied to the broader risk-off sentiment, which reduces the odds of a sustainable bullish momentum.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

The crypto industry keeps knocking down the barriers into the core U.S. financial system, and digital assets exchange Kraken’s approval for a limited Federal Reserve account marked another such milestone that analysts think could be the first of a trend.

The crypto arrival inside the Fed payment system — provisional and limited though it is — has aggravated the traditional banks and injected some confusion in the Fed’s ongoing effort to write policies for how crypto firms are supposed to go about getting limited “skinny” master accounts. But Kraken’s Co-CEO Arjun Sethi said that this development represents “what it looks like when crypto infrastructure matures into core financial infrastructure.”

Kraken’s Wyoming-chartered banking arm, Payward Financial, is granted a year of access to a “limited purpose” account as a “Tier 3” entrant, according to the Federal Reserve Bank of Kansas City, one of a dozen regional banks in the Federal Reserve system.

“We see this as the first of many Federal Reserve approvals for crypto entities to obtain master accounts, which gives them direct access to the central bank payment rails including Fed Wire,” said Jaret Sieburg, a Washington policy analyst at TD Cowen, in a client note on Thursday. “Crypto entity access to master accounts was inevitable under President [Donald] Trump, given his support for the crypto sector. We expect additional announcements in the coming months.”

Ian Katz, an analyst who tracks federal financial policies at Capital Alpha in Washington, echoed that sentiment.

“The Fed’s decision could open the doors for other crypto operations including Circle, Anchorage and Custodia, a Wyoming-based firm that has unsuccessfully sued the Fed over the right to have a master account,” he noted.

What does direct access to the Fed payments systems mean for Kraken?Potentially, according to Sethi: instant “settlement between fiat and crypto, institutional-grade cash management integrated with digital asset custody and programmable financial products built within a fully regulated framework.”

Those who operate traditional banks in the U.S. were displeased with the Kraken development — the latest threat they’ve flagged from the crypto space.

“There are significant risks to expanding direct Fed account access to institutions that operate outside the traditional banking regulatory framework,” the Independent Community Bankers of America said in a statement. “The Fed should continue limiting master account access to institutions that meet the financial services sector’s highest standards.”

But former Kraken CEO and current chairman, Jesse Powell, celebrated the development.

“We’re the bankers now,” the Kraken co-founder posted on social media site X. “Saddle up.”

Other crypto-tied institutions have also sought entry onto the Fed rails, including Anchorage Digital (which has sought a full master account, which would include earning interest on reserves placed with the Fed) and the recent arrival among federally approved trust banks, Erebor Bank. The industry also continues to lobby the Fed on its effort to establish a new policy to replace the 2022 guidance that Kansas City’s Kraken decision was based on.

At the national level, the Federal Reserve board started writing new policies for establishing what are commonly referred to as “skinny” master accounts for firms that don’t need the entire array of traditional master account services. But that process is in the early stages, and if regional Fed banks start approving similar accounts in the meantime, it could create uncertainties about what happens when the new policy is set.

“This action ignores public comment that the Federal Reserve sought on this framework, and it was issued with no transparency into the process for approval or the risk mitigants that have been imposed to address the very significant risks it raises,” the Bank Policy Institute’s co-head of regulatory affairs, Paige Pidano Paridon, said in a statement.

The Fed board in Washington, where the central bank is headquartered, deferred requests for comment this week to Kansas City.

The regional Fed banks, of which there are a dozen throughout the U.S., each operates under its own priorities and management, which can make their decisions uneven on such matters. So it’s uncertain whether the location of the Fed hub — Minneapolis for Anchorage Digital, for instance, and Cleveland for Erebor — will affect their outcomes.

The Kansas City Fed will keep working with firms there “to help ensure that access to the payment system supports a level competitive field and reinforces the stability and resilience that has underpinned the Federal Reserve’s payment system offerings throughout its history,” said President Jeff Schmid.

The U.S. Securities and Exchange Commission reached a settlement with Tron and founder Justin Sun on Thursday, the SEC said in a court filing.

Under the terms of the settlement, Rainberry Inc., one of the companies associated with the Tron network, will pay a $10 million fine and be barred from future violations of securities regulations. The SEC sued Sun and Tron in 2023, alleging violation of federal securities laws through the sale and airdropping of TRX.

“The remaining claims against Rainberry would be dismissed with prejudice,” the filing said. “The Final Judgment would also dismiss all claims against Justin Sun, Tron Foundation, and BitTorrent Foundation.”

With prejudice means the SEC would not be able to bring a similar case again in future for the same conduct.

“The Commission has reviewed and approved the terms of the settlement, as reflected in the Consent and proposed Final Judgment. Rainberry, Justin Sun, Tron Foundation, and BitTorrent Foundation have consented to entry of the Final Judgment,” the filing said.

The proposed settlement is still subject to a federal judge’s approval.

At the time the SEC, under the leadership of former Chair Gary Gensler, brought a number of lawsuits against crypto firms.

The SEC dropped most of these cases after President Donald Trump retook office last January, mostly under Commissioner Mark Uyeda, the acting chair. The commission is now run by Chairman Paul Atkins.

Sun bought about $80 million worth of World Liberty Financial tokens (WLFI) — the token tied to the company partially owned by Trump and his family — after Trump was reelected in 2024. The SEC’s case against Sun was paused last year, alongside numerous other cases the agency brought against crypto firms.

The U.S. Federal Reserve and other regulators told bankers that they need to maintain the same amount of capital to back tokenized securities as they do regulator securities.

“The technologies used to issue and transact in a security do not generally impact its capital treatment,” according to the agencies, also including the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corp. The three sent a new frequently-asked-questions document on Thursday to the banks they regulated.

The legal rights to owners of securities are meant to be the same whichever way the securities transact, and the regulators say the capital should also be the same. The assets themselves may also be used as financial collateral in the same way that securities are, the agencies clarified, “subject to the same haircuts applicable to the non-tokenized form of the security.”

Banks and other financial firms are required by their regulators to maintain capital as a cushion against financial distress, setting aside certain levels of liquid assets to be able to protect themselves and their customers. Setting the same standard for both forms of securities ownership means the crypto-linked assets won’t face more stringent treatment.

The same capital treatment also applies whether the tokens are issued on permissioned or permissionless blockchains, the regulators said, and that technology-neutral approach holds true for the capital tied to derivatives that reference tokenized securities, as well.

Tokenization of securities is a rising segment of crypto activity, in which such assets as stocks, bonds and real estate can be represented in a token issued on a blockchain. The U.S. Securities and Exchange Commission is also working on policies to direct how the tokens are handled.

Capital requirements represent a core compliance demand in the banking business, and clarity on such aspects of crypto capital further advances the assets into melding with U.S. banking. Though U.S. bank watchdogs were hesitant in recent years to embrace crypto and blockchain technology, the incoming leaders appointed during the administration of President Donald Trump last year have made it a special point to champion pro-crypto moves.

TLDR:

- SoFiUSD is the first stablecoin issued by a U.S. nationally chartered and insured deposit bank on a public chain.

- BitGo’s Stablecoin-as-a-Service platform powers SoFiUSD’s minting, burning, and institutional distribution.

- Both SoFi Bank and BitGo Bank & Trust are OCC-regulated, creating a dual-compliance framework for the token.

- The GENIUS Act passage enabled the legal foundation for SoFiUSD’s launch as a bank-issued stablecoin product.

SoFi Bank has launched SoFiUSD, a U.S. dollar-pegged stablecoin running on a public, permissionless blockchain. It is the first stablecoin issued by a nationally chartered and federally insured U.S. bank.

BitGo Bank & Trust, is providing the infrastructure behind the token. The move comes following the passage of the GENIUS Act, which opened clearer regulatory pathways for bank-issued stablecoins.

BitGo Powers Stablecoin Issuance for a Chartered U.S. Bank

BitGo is delivering this through its Stablecoin-as-a-Service platform.

The platform handles technology and operational infrastructure for SoFi Bank’s minting and distribution process. BitGo Bank & Trust is itself OCC-regulated. Both institutions operate under the same regulatory framework, which forms the backbone of the compliance model.

According to the official announcement, BitGo will also work with select payments providers, market participants, and exchanges.

This is designed to expand institutional reach for SoFiUSD. The token targets banks, fintechs, and enterprise treasury operations specifically. It is not positioned as a retail consumer product.

SoFiUSD is pegged 1:1 to the U.S. dollar. Third-party auditors will provide regular attestations to confirm reserve backing. BitGo’s smart contract infrastructure handles minting, burning, and transaction controls. The setup mirrors compliance-first architectures used in traditional finance.

SoFi’s crypto distribution team described SoFiUSD as critical financial infrastructure.

The token is aimed at institutions seeking settlement efficiency around the clock. It targets a specific gap in global treasury operations. Traditional banking rails still close on weekends and holidays.

SoFiUSD Aims to Bridge Regulated Banking and Blockchain Settlement Rails

The GENIUS Act passage has created new legal clarity for bank-issued stablecoins. SoFiUSD is the first product to market under this emerging framework.

BitGo’s infrastructure was built to support large-scale institutional asset flows. That makes SoFiUSD more aligned with wholesale finance than consumer crypto.

The partnership structure keeps regulatory accountability central. Both SoFi Bank, N.A. and BitGo Bank & Trust answer to the OCC. That dual-regulated relationship distinguishes SoFiUSD from stablecoins issued by non-bank entities.

It also positions the token as a potential model for future bank-issued digital currencies.

BitGo has described its Stablecoin-as-a-Service offering as purpose-built for institutions requiring regulatory trust alongside technical capability.

The infrastructure supports 24/7 onchain liquidity. That addresses a longstanding limitation for corporate treasurers managing cross-border payments. Real-time settlement across time zones has historically required multiple intermediaries.

SoFiUSD’s blockchain deployment on a permissionless public chain is notable. Most bank-adjacent digital assets have launched on private or permissioned networks.

This approach increases transparency and external auditability. It also allows third-party integration without requiring special access or agreements.

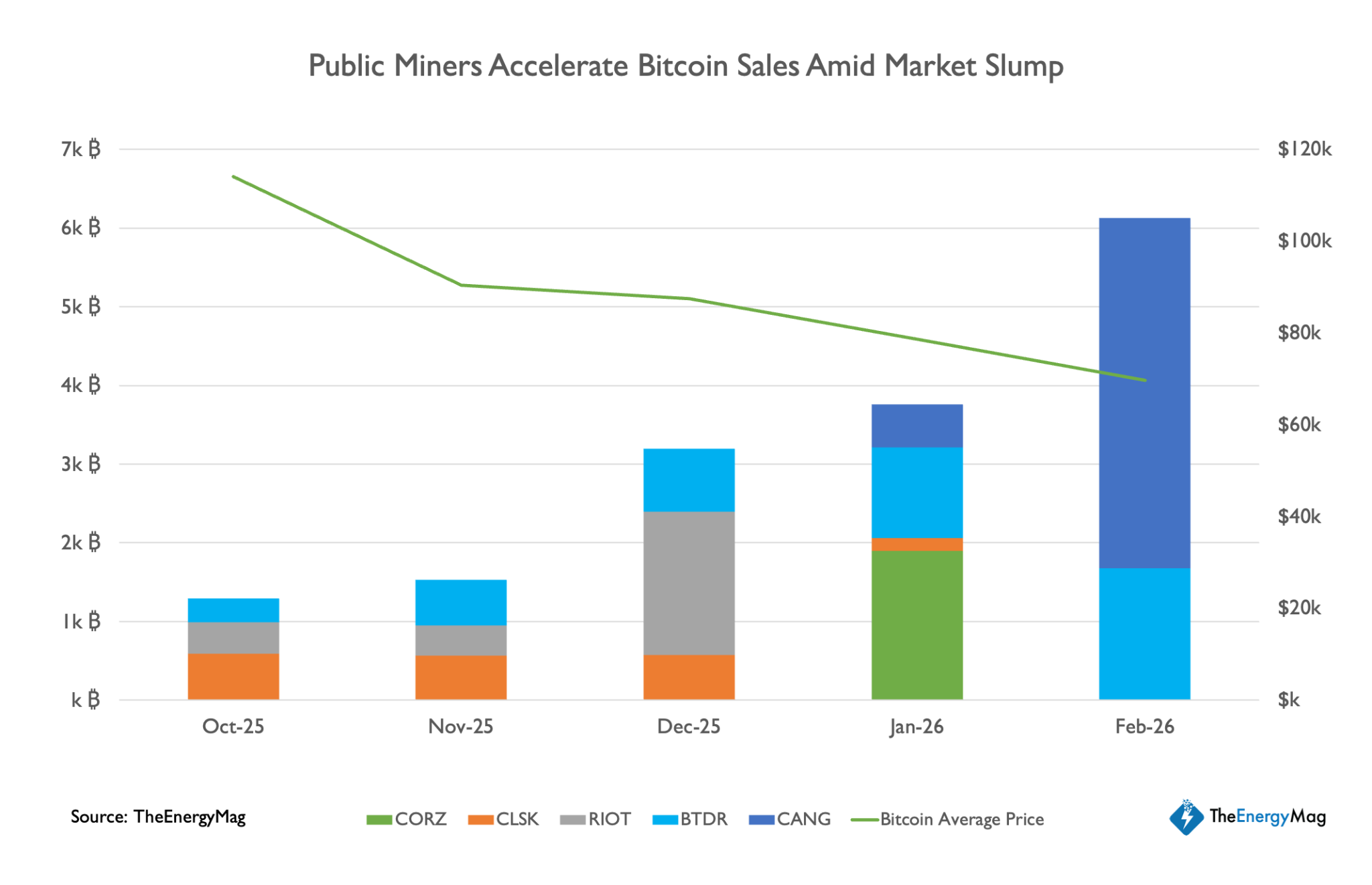

Bitcoin mining companies have offloaded a sizable portion of their Bitcoin reserves in recent months, signaling a shift away from the self-treasury strategy that dominated the industry during the 2024–2025 market upcycle.

According to TheEnergyMag’s Miner Weekly newsletter, publicly listed miners have sold more than 15,000 Bitcoin (BTC) since October. That month marked the market’s peak before a historic flash crash triggered widespread deleveraging across the industry.

Several large miners contributed to the sell-off. The newsletter highlighted Cango’s February sale of 4,451 BTC, equal to roughly 60% of its reserves, as well as Bitdeer, which reportedly liquidated its entire Bitcoin treasury last month.

It also pointed to Riot Platforms’ multiple BTC sales in December and Core Scientific’s plan to sell roughly 2,500 BTC during the first quarter.

MARA Holdings, the largest publicly traded Bitcoin mining company, drew attention this week after updated regulatory filings indicated it may both buy and sell Bitcoin to maintain flexibility and optionality.

Markets initially focused on the potential for sales, prompting vice president Robert Samuels to clarify the company’s position that the filing allows flexible sales but does not signal a majority liquidation.

MARA currently holds more than 53,000 BTC, making it the second-largest public corporate holder of Bitcoin, behind Michael Saylor’s Strategy.

Related: Bitcoin mining’s 2026 reckoning: AI pivots, margin pressure and a fight to survive

Mining companies shift strategy as margins tighten

Bitcoin miners’ recent sales mark a sharp departure from earlier cycle trends, when many companies adopted a de facto “treasury strategy” by holding a larger share of their self-mined BTC on their balance sheets.

At the time, research from Digital Mining Solutions and BitcoinMiningStock.io suggested the holding pattern reflected expectations of further price appreciation. It also coincided with efforts by several miners to strengthen their financial footing while expanding into adjacent businesses such as AI infrastructure, high-performance computing and data center services.

Industry conditions have deteriorated since October, however, with some observers describing the current environment as the harshest margin squeeze on record for mining companies.

The pressure has begun to show on balance sheets. CleanSpark, for example, repaid its Bitcoin-backed credit line in full, a move the company said was aimed at reducing financial risk amid tightening industry margins.

Related: American Bitcoin boosts hashrate with 11,298 new mining machines

Short seller Culper Research is betting against ether (ETH) and ETH-linked stocks such as BitMine (BMNR), arguing that the network’s economics deteriorated following Ethereum’s latest network upgrade.

The firm said in a Thursday report that the December 2025 upgrade dubbed Fusaka flooded the network with excess blockspace and has “impaired ETH tokenomics.” That drove transaction fees sharply lower. Because validators earn part of their income from those fees, the drop has reduced staking yields.

That dynamic could create a negative feedback loop, the report said, where declining validator yields reduce staking demand and network security.

The report also highlighted that Ethereum co-founder Vitalik Buterin sold nearly 20,000 ETH, worth around $40 million at current prices, this year, citing data from blockchain sleuth Lookonchain.

“Vitalik is selling, while bulls like Tom Lee are clueless as to ETH’s new reality,” the report said. “We’re with Vitalik.”

The report pushes back on bullish claims from Lee, chairman of Ethereum-centric treasury firm BitMine, who has pointed to rising transaction counts and active addresses as evidence of stronger network fundamentals.

Culper said those metrics are misleading. Its analysis claimed a significant share of the activity surge stems from address poisoning attacks, a scam tactic where attackers send small transactions to trick users into copying malicious wallet addresses. Culper estimated Ethereum fees have dropped roughly 90% since the upgrade.

“By Lee’s own logic, if utility is NOT going up, then ETH is in a death spiral,” the report said. “This is exactly what we believe is happening.”

The short thesis also targeted BitMine (BMNR), one of the largest corporate buyers of ether.

Since July, the company has accumulated roughly 4.4 million ETH as part of its treasury strategy. With ether prices down significantly from recent highs, those holdings are estimated to be 45% underwater, with BitMine sitting on roughly $7.4 billion in unrealized losses, DropsTab data shows.

BitMine did not return a request for comment by press time.

Read more: Vitalik Buterin reveals his bold new plan to fix Ethereum’s scaling problem

TCL Debuts CrystalClip Wireless Earbuds Along With Swarovski Crystal Edition

Scarborough’s Alpamare water park could be sold to new owner

Grove Collaborative Holdings, Inc. 2025 Q4 – Results – Earnings Call Presentation (NYSE:GROV) 2026-03-05

-

Politics7 days ago

Politics7 days agoITV enters Gaza with IDF amid ongoing genocide

-

Politics3 days ago

Politics3 days agoAlan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Iris Top

-

Tech5 days ago

Tech5 days agoUnihertz’s Titan 2 Elite Arrives Just as Physical Keyboards Refuse to Fade Away

-

Sports6 days ago

The Vikings Need a Duck

-

NewsBeat5 days ago

NewsBeat5 days agoDubai flights cancelled as Brit told airspace closed ’10 minutes after boarding’

-

NewsBeat5 days ago

NewsBeat5 days agoAbusive parents will now be treated like sex offenders and placed on a ‘child cruelty register’ | News UK

-

NewsBeat5 days ago

NewsBeat5 days agoThe empty pub on busy Cambridge road that has been boarded up for years

-

NewsBeat4 days ago

NewsBeat4 days ago‘Significant’ damage to boarded-up Horden house after fire

-

Tech16 hours ago

Tech16 hours agoBitwarden adds support for passkey login on Windows 11

-

Entertainment4 days ago

Entertainment4 days agoBaby Gear Guide: Strollers, Car Seats

-

Sports4 hours ago

Sports4 hours ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

Tech6 days ago

Tech6 days agoNASA Reveals Identity of Astronaut Who Suffered Medical Incident Aboard ISS

-

Politics5 days ago

FIFA hypocrisy after Israel murder over 400 Palestinian footballers

-

NewsBeat5 days ago

NewsBeat5 days agoEmirates confirms when flights will resume amid Dubai airport chaos

-

NewsBeat3 days ago

NewsBeat3 days agoIs it acceptable to comment on the appearance of strangers in public? Readers discuss

-

Crypto World7 days ago

Crypto World7 days agoFrom Crypto Treasury to RWA: ETHZilla Retreats and Relaunches as Forum Markets on Nasdaq

-

Tech5 days ago

Tech5 days agoViral ad shows aged Musk, Altman, and Bezos using jobless humans to power AI

-

Video4 days ago

Video4 days agoHow to Build Finance Dashboards With AI in Minutes

-

Business2 days ago

Business2 days agoGuthrie Disappearance Enters Fifth Week as Family Visits Memorial