The Wrexham-based firm is looking to expand in the UK and overseas’ market afte securing backing from the £130m Investment Fund for Wales

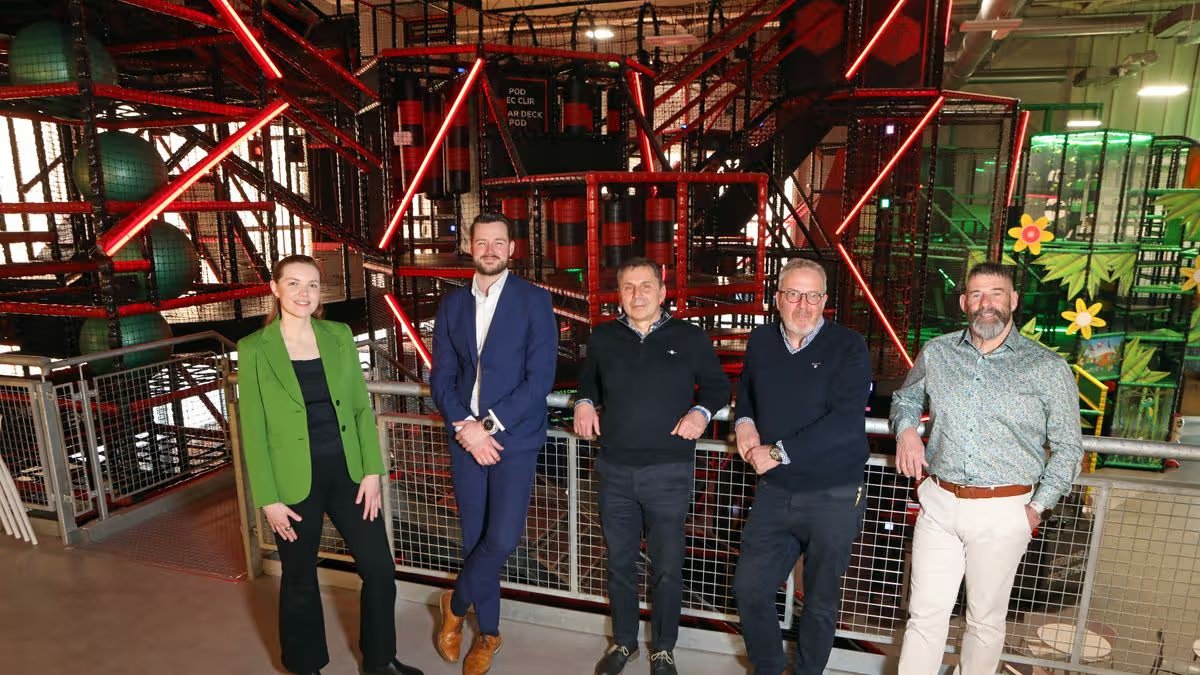

Play Revolution investment deal left to right: Jemima Jones (British Business Bank), Ashley Rogers (Foresight), Gwyn Jones (Play Revolution), Simon Lee (Play Revolution) and Andy Edwards (Play Revolution).

Wrexham‑based designer and manufacturer of indoor soft‑play systems, Play Revolution, has secured equity backing from the £130m Investment Fund for Wales.

The investment, the value of which hasn’t been disclosed, will support the firm’s next phase of UK and international growth. It is the tenth deal from the equity element of the fund from the British Business Bank which is managed by Foresight Group. Founded in 2008 Play Revolution designs, manufactures, and installs high‑quality indoor play systems for leisure centres, family entertainment centres, holiday parks and international operators.

Its technology‑enabled product, TAGactive, integrates RFID (radio-frequency identification) wristbands, real‑time scoring and a gamified arena environment, and is now installed in sites worldwide. Play Revolution’s customers include Alliance Leisure, David Lloyd Clubs, Center Parcs, and a growing base of international leisure operators.

READ MORE: Work under way on the UK’s first nuclear small modular reactors in North WalesREAD MORE: Plans still of track for Wales’ first dedicated museum of contemporary art

The company, which employs 29 people is looking to accelerate its international growth following the investment. The potential for significant expansion of the TAGactive technology is a particularly attractive opportunity as families seek experiential fun.

Gwyn Jones, managing director of Play Revolution, said: “We’re incredibly excited to be entering the next phase of growth for Play Revolution and TAG Active Ltd. The investment from Foresight Group is a strong endorsement of our vision and creates significant opportunities to expand into new markets. Just as importantly, it brings long‑term stability for our team, our partners and our customers as we continue to grow the business and deliver innovative play experiences around the world.”

Mark Hardy, incoming chairman of Play Revolution: “I am delighted to be joining Play Revolution at such an exciting stage in its development, and I’m personally thrilled to be returning to the play and leisure sector.

“The company has already achieved an impressive amount, Gwyn and his team have built an outstanding reputation in the UK and internationally, and with Foresight’s investment alongside the team’s proven expertise, we are extremely well positioned to enhance the services we offer existing clients while expanding our reach and attracting new ones.”

Jemima Jones, investment manager, nations and regions investment funds at the British Business Bank, said: “Play Revolution is a strong example of the kind of forward-thinking, growth-focused business the Investment Fund for Wales is designed to support. With its roots in Wrexham, the company has built an impressive reputation both in the UK and internationally, driven by its ambitious approach to product development and design expertise.

“We are pleased to support Foresight and the management team as they take the business into its next phase.”

Ashley Rogers, investment manager at Foresight Group, said: “Play Revolution is a high‑quality Welsh business with a strong track record, deep customer relationships and a differentiated technology offering in TAGactive.

“We see significant potential to scale the company, both in the UK and internationally, and will continue to invest in the team and infrastructure needed to support long‑term growth. We are excited to partner with the founders, the incoming team and the talented workforce in Wrexham.”

“The company is entering this exciting new phase with a robust pipeline of sales opportunities, longstanding customer relationships and a clear plan for growth and we are delighted to be partnering with them.”

You must be logged in to post a comment Login