Business

Block Eliminates Bloat To Deliver Ambitious 2028 Target – Wait For Correction

Activist investor Elliott Investment Management has a multibillion-dollar investment in Synopsys SNPS -1.85%decrease; red down pointing triangle, the big chip-design software maker, according to people familiar with the matter.

Elliott plans to engage with Synopsys to push the business to make more money from its software and services, the people said. Synopsys’s customers include Intel, Alphabet and Tesla.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

President Donald Trump confirmed his upcoming trip to China for a summit with President Xi Jinping, stating it will occur in “about five or six” weeks. The meeting aims to discuss key issues between the two nations, signaling ongoing diplomatic engagement despite recent tensions. Exact dates and agenda details are yet to be finalized.

Former President Donald Trump has announced that he is “resetting” a scheduled meeting with Chinese President Xi Jinping. This move comes amid ongoing tensions and diplomatic complexities between the two nations. Trump expressed optimism that the new arrangement could lead to constructive discussions on trade, security, and cooperation.

The decision to reschedule highlights the delicate nature of U.S.-China relations, which have been strained by economic disagreements, technology disputes, and geopolitical issues. By “resetting” the meeting, Trump aims to create a more favorable environment for dialogue, emphasizing the importance of diplomacy in resolving conflicts.

This development signals a potential shift toward renewed communication between the two countries. Both leaders are expected to leverage this opportunity to address critical issues and seek common ground. The outcome of the meeting could significantly influence the future direction of international relations in the region.

Other People are Reading

Oil prices rise after US, Iran threaten to hit energy targets in the Middle East

Stock Futures Are Falling, Oil Rising as Iran Tensions Grow

Analysis-New Zealand struggles to regain economic mojo without housing recovery

NZ’s Fonterra ups annual earnings outlook, flags potential Middle East disruptions

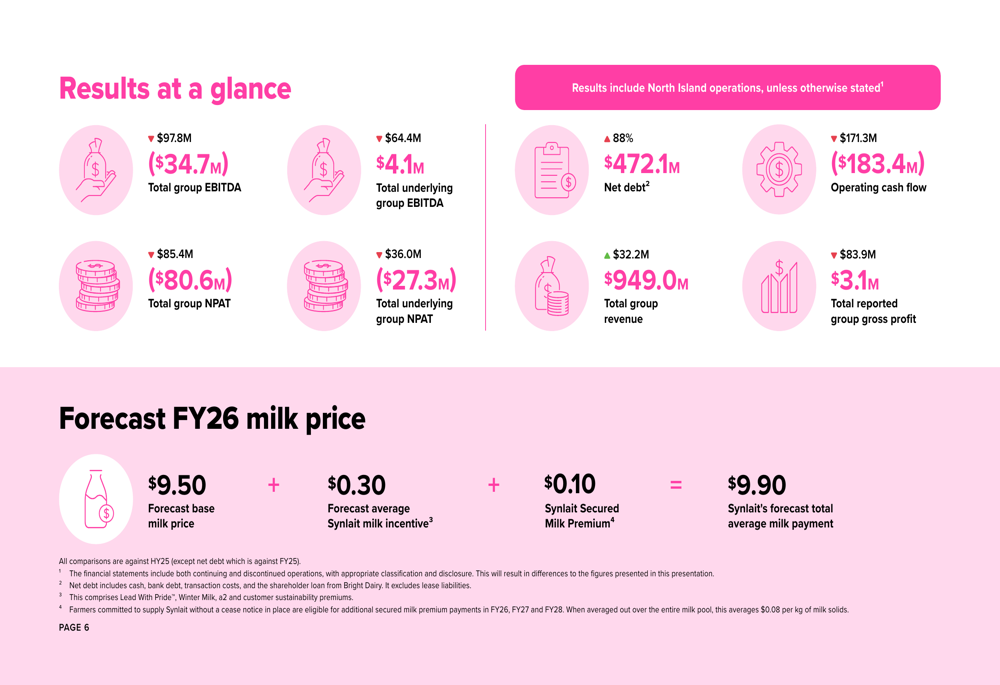

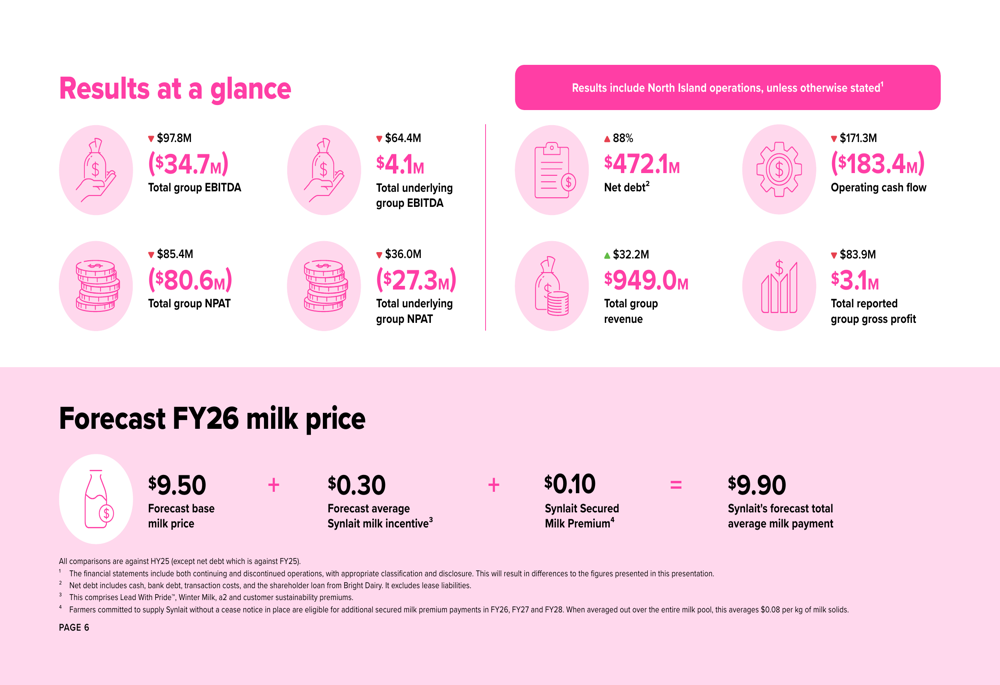

Synlait H1 2026 slides: $80.6M loss amid manufacturing woes, recovery plan

Musk says SpaceX and Tesla to build advanced chip factories in Austin

Earnings call transcript: Synlait Milk faces challenges in H1 2026

US SEC concludes four-year-old probe into EV startup Faraday Future with no action

Controversial ‘new town’ plans for village near Greater Manchester scrapped by Government

Exclusive | Activist Elliott Builds Big Stake in Chip-Design Software Maker Synopsys

Tyrese Haliburton takes shot at former Kentucky players for John Calipari-Arkansas allegiance

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics2 days ago

Politics2 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Tech5 days ago

Tech5 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Crypto World1 day ago

Crypto World1 day agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos4 days ago

News Videos4 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World1 day ago

Crypto World1 day agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Crypto World2 days ago

Crypto World2 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Business7 days ago

Business7 days agoAustralian shares drop as Iran war enters third week

-

Crypto World7 days ago

Crypto World7 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Politics5 days ago

Politics5 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion7 days ago

Fashion7 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

Tech3 days ago

Tech3 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Politics5 days ago

Politics5 days agoReal-time pollution monitoring calls after boy nearly dies

-

Crypto World4 days ago

Crypto World4 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

NewsBeat4 days ago

NewsBeat4 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business6 days ago

Business6 days agoMeta planning major layoffs as AI spending and automation reshape workforce

-

News Videos4 days ago

News Videos4 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Business7 hours ago

Business7 hours agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Entertainment7 days ago

Oscars reunite Rob Reiner supergroup of 17 stars for emotional tribute: Here's who appeared on stage

-

Business4 days ago

Business4 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

You must be logged in to post a comment Login