We compounded capital at a reasonably healthy rate—advancing +13% in 2025.

On a relative basis, this placed the fund between most benchmarks—trailing the international markets which delivered an exceptionally strong rebound year based on weakness in USD, behind US large-cap indexes and slightly ahead of US small-cap and fund composites.

Numbers never seem to paint the full picture, though, as we arrived at those results in a very different way. From our perspective, it was a fairly steady year with relatively minimal volatility. Long positions generally moved higher, while hedged/short exposure remained a frustratingly persistent friction. Markets meanwhile seemed to bounce around on geopolitical news, macro flows and changing narratives, but ultimately arrived at new highs driven by a narrow leadership set.

Advertisement

There are a lot of different directions I want to take it from here… which is the primary reason I have been struggling to deliver this letter. But in the interest of time and respect for your human (!!!) attention span… I will try to keep it brief and merge the Outlook section into a single consolidated segment. AI would never…

Over the years I have come up with a lot of references and analogies to talk about economic concepts. I then use these letters as a way to tie them together to form a relevant long-term framework, which helps provide a clearer snapshot for how we think about the world and investing landscape.

By Month:

Bumber

S&P 1

Russell 2

FTSE 3

Barclay 4

Jan-2025

1.97%

2.70%

2.58%

6.13%

1.71%

Feb-2025

-3.89%

-1.42%

-5.45%

1.57%

-0.16%

Mar-2025

-0.85%

-5.75%

-6.99%

-2.58%

-1.55%

Apr-2025

2.06%

-0.76%

-2.38%

-1.02%

-0.13%

May-2025

4.63%

6.15%

5.20%

3.27%

2.80%

Jun-2025

1.84%

4.96%

5.26%

-0.13%

2.38%

Jul-2025

0.77%

2.17%

1.68%

4.24%

0.93%

Aug-2025

0.95%

1.91%

7.00%

0.60%

1.95%

Sep-2025

2.62%

3.53%

2.96%

1.78%

2.25%

Oct-2025

2.31%

2.27%

1.76%

3.92%

0.98%

Nov-2025

-0.73%

0.13%

0.85%

0.03%

0.26%

Dec-2025

0.88%

-0.05%

-0.74%

2.17%

0.57%

Bumbershoot Holdings L.P.

Advertisement

2025 Performance

S&P 1

Russell 2

FTSE 3

Barclay 4

FY-2025

13.02%

16.39%

11.29%

21.51%

12.57%

Inception

156.3%

281.7%

139.4%

71.9%

89.9%

The last great hideout…?

This is inflation vs. deflation …The Central Bank Superheroes …How Fast, How High, How Long …Crucifying mankind on a cross of T-bills …The reflationary pump …The cartoonish increase in money supply …Brushing against the third-rail of USD reserve status …The Lizard Brain …Algo-Trader Chicken …That you have to get it right on price too …The economic riddles from last year…Questions and narratives …All of it.

One aspect I’d like to reexamine though is liquidity —and particularly the next reflation cycle .

Advertisement

I stated last year that the ” next reflation cycle will be something to witness “—and so I just want to expand a bit on what that means from my perspective.

The challenge with this is that it requires holding some conflicting ideas . About personal beliefs. The state of the economy. Growth, valuations, interest rates…

I will not be attempting to predict when the next cycle will kick off and/or what will precipitate it… but I am willing to stake that in a debt-driven system, deflation is simply too destabilizing to allow it to persist for any measured amount of time. This is even more the case with policymakers increasingly sensitive to financial market performance as a scorecard. Even the question of a mismatched growth/contraction and expectations of deflation might reasonably set off the next reflation cycle sooner rather than later. And my opinion, taken for what it is—whenever it occurs, it will be substantial.

The dynamic reminds me of the show Breaking Bad . Every episode, viewers are presented with a seemingly fatal constraint. Hank is boxed in. Consequences are finally going to be unavoidable. But through a series of increasingly creative and risky maneuvers, disaster is averted to push the story forward to the next episode. Stabilizing the present, while quietly raising the stakes for the future.

Advertisement

Economic storylines have behaved quite similarly over the course of my career.

An economic slowdown looms.Policy mistakes threaten instability.Credit pressures emerge.

But through some combination of policy intervention, fiscal expansion, monetary accommodation, and/or financial engineering—those immediate consequences can be postponed. Kicking the can down the road.

Each rescue works… but brings with it new distortions. A subtle erosion in the confidence of fiat currency. An increased dependency on a political reaction function. Greater public leverage. Uneven distribution of wealth. Higher risk of long-term inflation.

Advertisement

Understandably, the market focuses on survival to the next episode—not the longer-term story arc.

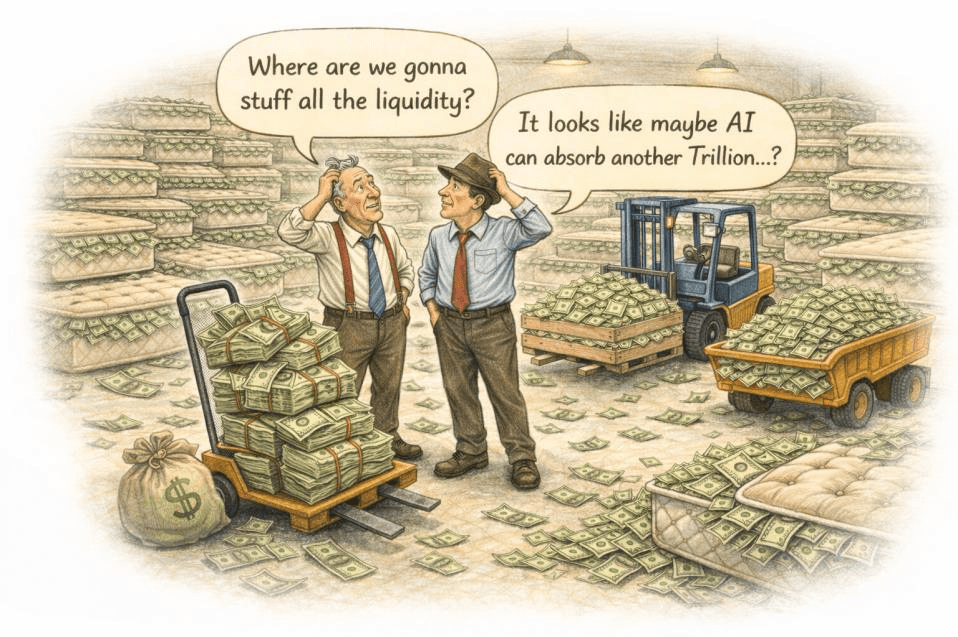

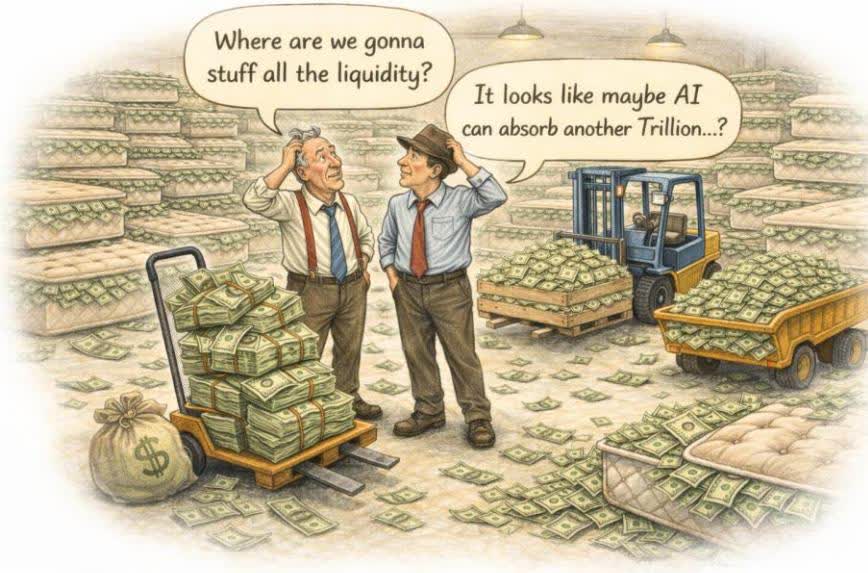

But this is the liquidity .

Whenever those maneuvers occur, liquidity floods the system. And when that happens, it inevitably searches for somewhere to flow.

Money needs to be absorbed .Liquidity needs to go somewhere …

Advertisement

And so, it does…

It finds its way into anything capable of absorbing it—Durable businesses… Financial assets… Real estate… Anything with a credible narrative …

And it will keep pushing on that string for as long and as hard as it can until the price hits some tension. This is what can stretch it way beyond fundamentals as the crowding effect takes place within a narrowly anointed leadership cluster.

Anything even resembling a worthy mattress becomes stuffed to the gills —expressed via multiple expansion—and may not be safe for your next investment dollar.

“If the narrative is not contentious, then the valuation almost certainly is…”

Advertisement

Even an exceptional growth story can be pushed to the point that it is just a tough deal.

So, what am I saying?What am I worried about?Where is the catastrophe risk ?

Why am I talking about deflation , the effects of excess liquidity and the cause of even more (!) excess liquidity with the next reflation cycle all in the same breath…?

Because in many ways they are all the same story.

Advertisement

The economy is working really well for certain parts of it. Institutional sponsorship and capital market access is wildly strong for the companies benefiting from the central technological/geopolitical narratives. And for individuals who own financial assets, the system is still largely working as designed—compounding wealth.

The rich get richer… but it’s not a collective experience.

While macro headlines and market leadership remain fairly resilient—growth has been uneven with pressure mounting beneath the surface for many. Affordability remains a real constraint for most people/households. Inflation shocks to non-discretionary items like food, rent & healthcare; combined with higher home prices and elevated interest rates have now effectively frozen many people out from ever becoming owners…

This is the down-leg of the K-shape recovery/economy we’ve all talked and read so much about. And it is that descender portion that is being forced to carry the real economic burden—felt deeply in the consequences of economic mobility and financial security.

Advertisement

But immunity by the upper-leg does not last forever—effects eventually begin to work their way upward…

Which is about when the structural constraint of policy response kicks in. Because as the economy slows… and credit contracts… and fear takes over… the historical answer has been remarkably consistent: reflate .

Ironically, it is this cycle reinforcing the very imbalance which created the pressure in the first place. Liquidity flows into financial assets … precisely the thing that the struggling portion of the economy was stressed by not owning to begin with! Cue the William Jennings Bryan quote … it’s no wonder populism is awakening around the world!

The game is not fair .

Advertisement

But as I’ve said previously—we didn’t make the rules… and we certainly are not in charge of trying to change them. All we can do is play it to the best of our ability.

But to be a happy unintended consequence of the next reflation cycle… we need to know what the “playbook” is going to look like. And my suspicion is it won’t look exactly the same as the last time.

Because the market narrative is changing…

AI is still a primary driver, but the question of whether AI will be “ transformational to the world? ” was one I labeled last year as not having any real stakes . Accept that it is going to transform the world and productivity, but then what? Is it investable ? And who wins ?

Advertisement

The new question of whether AI is hugely deflationary to the job market and the rest of the SaaS technology ecosystem is one that has a lot more bite to it.

The market is also still starting from a tough position. To repeat last year, a little fizz almost never turns into a bubble . But it is expensive. Signals are there—stretch valuations, investor complacency, excessive leverage… Perhaps most notably, “ good company news ” in terms of fundamental positive strength/improvement in the underlying operations of a business is beginning to not always have an effect. That is typically an end cap to a bull market, as the multiple expansion has played out.

To put it very simply, uncertainty is going up. Meaning the number of places with credible narratives in which to park substantial amounts of capital is going down…

Selection is going to be paramount.

Advertisement

This has always been at the core of our process—know what we own, why we own it and what it may be worth. Selection is where we shine …

It is why we go through the entire hassle of still trying to identify key themes, understand the core narratives, evaluate critical fundamentals… ie: research .

And it works.

But it is forcing us to confront the challenging question of whether we are taking enough risk?

Advertisement

And the answer to that question is probably not .

Too often we have arrived early, but then moved on to our next idea far too quickly…

To use a baseball analogy, we’ll show up in the second or third inning… and then usually try to leave after the seventh-inning stretch. Reasonable .

But we’ve been at the right games… and the market has increasingly rewarded those who have stuck around through the eighth and ninth innings. The increase in volatility as the game nears an end has been worth it .

Advertisement

This is not a change in our process… core principles remain exactly the same. We will never take risk that forces a permanent capital impairment. We will never become a forced seller. But from a playbook with fewer places to live… we need to hold those spots much more dearly in terms of both concentration and duration.

The question in my mind is not whether we can locate the right corners of the market… it is whether we are being compensated appropriately for our conviction to be standing there.

Perhaps not quite going full Charlton Heston on you—“ pry it from my cold, dead hands… ” … but at the very least… you’re going to have to come and take it.

Our job is still to find them first.

Advertisement

But when we do, stay a little longer.

Volatility may tick up… and that may be a good thing.

As a reminder, Bumbershoot remains my primary way to navigate the markets and to grow wealth—through all cycles and conditions. It is an absolute return fund. A multi-strat, eclectic expression of my philosophy on what I ought to be doing with my own money. Because indeed, it is my own money. I have still never touched a single dollar of my initial investment as an LP, which represents the vast majority of my net worth.

I am as excited about our opportunity set today as I have been at any time since starting the company. The market remains narrative-driven and increasingly split between assets everyone wants to own and those that have quietly fallen out of favor.

Advertisement

It is rewarding understanding businesses, rather than just trading based on price action. It is an environment that tends to prize deep work—valuing the process we have been building all along.

Since the fund’s inception, I envisioned an alternative in asset management services, guided by a clear set of values and goals—and I am proud to say that we have remained steadfast in commitment to that mission.

I believe we are exceptionally well positioned to take advantage of whatever comes next…

Performance

Bumbershoot Holdings L.P. generated a positive gross return of +13.02% for the full-year 2025.

Advertisement

The partnership has a cumulative total gross return of +156.3% since inception in Oct-2015.

Looking at relative performance, our monthly returns were directionally correlated with key benchmarks, but with significantly less volatility. Despite concentration in our largest holdings, it was a steady year—with no individual month being +/- more than 5% for the first time since the pandemic.

Investment activity is categorized into five segments— Core, Micro, Value, Special Situation & Discretionary —with estimated P/L contributions as follows:

Advertisement

By Category:

Core

10.9%

Core – Long

16.6%

Hedge/Short

-5.7%

Micro

3.5%

Value

-0.3%

Special Situation

-1.8%

Discretionary

-0.1%

Fx.

0.5%

Misc.

0.3%

FY-2025

13.0%

Core gains were led by investments in the Technology sector including Alphabet (GOOGL) (GOOGL:NYSE), Micron (MU) (MU:NYSE), First Solar (FSLR) (FSLR:NGS) and Camtek (CAMT) (CAMT:NGM). We remain particularly focused on key critical “OS platform” businesses and semiconductor-related adjacencies.

Our long-standing position in gold (and copper!) miner Barrick Mining (GOLD) (B:NYSE) finally moved higher as a reflection of the gains in the underlying yellow metal. Materials sector exposure to the agricultural-fertilizer industry via Intrepid Potash (IPI) (IPI:NYSE), Nutrien (NTR) (NTR:NYSE), CF Industries (CF) (CF:NYSE) was also a positive contributor to results.

The Healthcare sector was once again led by Ligand (LGND) (LGND:NGM) and Madrigal (MDGL) (MDGL:NGS), but was more than offset by losses in Viking Therapeutics (VKTX) (VKTX:NCM). While Viking has been a roller-coaster over the past couple of years, we remain optimistic as it moves VK2735 into multiple Ph3 trials. We remain interested in investments targeting biopharmaceutical royalties and metabolic disorders.

Home improvement retailer, Kingfisher (KGFHY) (KGF:LSE), finally started to turn things around… perhaps Europe does still count for something after all.

Advertisement

And playing on the continued theme of infrastructure spending, defense and energy sustainability, a handful of our positions in the Industrial and Energy sectors added positively to performance including Oshkosh (OSK) (OSK:NYSE), Coterra (CTRA) (CTRA:NYSE), OSI Systems (OSIS) (OSIS:NGS), and Herc Holdings (HRI) (HRI:NYSE).

Core category investment returns were lowered by our direct short exposure and market hedging activity.

Micro strategy had a standout performance, led by a notable attribution from Vimeo (VMEO) (VMEO:NGS), which was acquired during the year. Some of our technology and industrial-themed holdings such as Orion Group (ORN) (ORN:NYSE), NPK International (NPKI:NYSE) and Vishay Precision Group (VPG) (VPG:NYSE) continued to produce meaningful contributions; and a collection of lesser-weighted positions also bumped up results.

Value category registered negligible attribution as an auditor switch at Gencor Industries (GENC) (GENC:NGM) took down performance, offsetting any other gains.

Advertisement

Special Situation strategy was a detractor for the year as our position in BuzzFeed (BZFD) (BZFD:NCM) gave back the “notable gain” from last year. This was partially offset by M&A related arbitrage.

Discretionary trading had no significant attributions to merit discussion in more detail.

In terms of exposure levels, Bumbershoot ended 2025 with Core investments around target range. Non-Core categories remain a mix, with only the Micro category being above the target weighting of ~5% AUM.

Administrative

There is one notable change to talk about.

Advertisement

While I still plan to use the collective “we” in talking about our partnership—DeForest Hinman accepted a new role as an investment officer at a regional bank. I need to thank him for his contributions and wish him the best of luck in the new role.

Aside from that… the picture remains the same.

Before moving on from this section… I want to STOP! This will not be an entire dedicated Marketing section like a few years ago, but I want to do something I have rarely done since starting… ask for your investment .

I fully believe in what we are doing as an alternative in asset management. And am increasingly confident that we’ve built a process that is scalable and repeatable at higher amounts of capital under management.

Advertisement

Any support from existing LPs to intro the fund to new prospective partners remains greatly appreciated; and I’d love people to consider being part of Bumbershoot as we take steps forward.

Taxes

Bumbershoot’s form Schedule K-1 that reports on each partner’s share of income/losses for the tax year have been prepared by our administrator.

As reminder, we successfully implemented a “ Master-Feeder ” structure a handful of years ago to efficiently pass long-term gains in our Core holdings back to the main fund.

Tax implications for 2025 were favorable with partner accounts recognizing only moderate taxable gains for the full-year from a capital account basis.

Advertisement

For existing partners that have sizable (and hopefully increasing) embedded gains in Core investments held in the Feeder account—those gains ultimately become taxable upon being realized at some time in the future. That event, however, is deferred and the consequent tax-effect is long-term in nature. Over time, I expect our tax strategy to remain efficient/advantageous.

Summary

2025 was a solid year for Bumbershoot—one that adds to our long-term track record of compounding.

Another mile.

As many of you know, I ran the Tokyo marathon just a few days ago… so I’ve been thinking about running a lot. It’s given a new perspective to the familiar phrase, “ It’s a marathon, not a sprint. ”

Advertisement

You do not arrive at the finish line. It is only step-after-step-after-step that you ultimately reach the goal. It is an exercise in patience, endurance and preparation.

Stepping forward to 2026!

Sincerely,

Jason Ursaner, Managing Member, Bumbershoot Holdings

This letter is provided on a confidential basis and is for informational purposes only.

Advertisement

All market prices, data, and other information are not warranted for completeness or accuracy and are subject to change without notice. All performance figures are estimated and unaudited. Any opinions and estimates constitute a “best efforts” judgment and should be regarded as preliminary and for illustrative purposes.

As of the publication date of this letter, Jason Ursaner, Bumbershoot Holdings LP, Bumberings LLC, and its affiliates (collectively “Bumbershoot”) may own, or have sold short, stock and/or options in companies covered herein; and stand to realize gains if the price of their issues change. Following the publication of this letter, Bumbershoot may transact in the securities of the companies mentioned. Content of this report represents the opinions of Bumbershoot. All information has been obtained from sources believed to be accurate and reliable, however, such information is presented “as is” without warranty of any kind—express or implied. No representation is made as to the accuracy, timeliness, or completeness of any such information. All expressions of opinion are subject to change without notice; and Bumbershoot does not undertake to supplement and/or update this report or any information contained herein.

Any investment involves substantial risks, including, but not limited to: price volatility, inadequate liquidity, and the potential for complete loss of principal.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment of security for any company discussed herein. Investors should conduct independent due diligence, in assistance from professional financial, legal, and tax experts, prior to making any investment decision.

1144 GMT – Saudi Arabia’s output reduction is occurring in fields that don’t produce Arab Light crude, the main grade that can be exported via the Yanbu terminal on the Red Sea, Amena Bakr, head of Middle East energy and OPEC+ insights at Kpler, says. Bloomberg on Monday reported that Saudi Arabia is starting oil-output cuts as storage fills up due to Hormuz disruptions. “This is not accurate, according to our understanding,” Bakr says in a post on X. “There is a reallocation of supply that’s happening, not a cut.” Saudi Aramco has been diverting more of its crude via the East-West pipeline, which bypasses the Strait of Hormuz, Kpler says. (giulia.petroni@wsj.com)

Middle East Oil Shut-Ins Raise Risk of Lasting Supply Losses

1047 GMT – Prolonged oil production shut‑ins in the Middle East raise the risk of partial or permanent production losses due to reservoir, well, facility, and logistical constraints, according to Societe Generale. “Time is critical: the longer disruptions persist, the greater the likelihood that what initially appear to be temporary outages evolve into more durable supply losses,” Michael Haigh and Ben Hoff say. Risks start increasing after about two weeks offline and intensify beyond a month, with capacity typically returning to only 80%-95% after outages of several months, according to the bank. If more producers beyond Iraq and Kuwait curtail output, quickly restoring pre‑crisis supply would become increasingly difficult.(giulia.petroni@wsj.com)

Surge in Oil Prices May Still Be Short-Lived

0923 GMT – The surge in oil prices may still be short-lived, according to Julius Baer’s Norbert Rücker in a research note. “Oil markets have entered panic mode,” says the head economics and next generation research. While prices have surged to over $100/bbl, most of this move seems to “come from nervousness and sentiment, since tangible and significant fundamental shifts in the conflict are not visible over the weekend,” he says. Rücker still believes the energy price spike will be intense but short-lived. “Meaningful infrastructure damage remains absent, and Iran’s military threat seems to be softening,” he says. Front-month WTI crude oil futures are 15% higher at $104.15/bbl; front-month Brent crude futures are 15% higher at $106.80/bbl. (tracy.qu@wsj.com)

Oil, Gas Expected to Trade Around Current Price Levels Through March

1016 GMT – Oil and gas prices are likely to trade around current levels through March as supply disruptions evolve and some producers begin shutting in output, Julius Baer analyst Norbert Ruecker says in a note. He projects that up to 75% of Middle Eastern oil flows relying on shipping through the Strait of Hormuz could face temporary shut-ins next week, though Saudi Arabia, the United Arab Emirates and Iraq have pipelines that bypass the Strait. Temporary shut-ins may reduce, but not eliminate, the oil market’s surplus this year. Stagnating demand and rising production, particularly in South America, should keep supplies up, he adds. However, rising road fuel prices, particularly in the U.S., are worth watching. If the Trump administration were to impose restrictions on petroleum exports, this would trigger a sharper and longer oil price spike. (jason.chau@wsj.com)

German Buy-Hold-Check investor. With a master’s degree in engineering and management, I am able to understand, quantify, and interpret both the economics and (to some point) the technology of companies.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of HIMS, NVO either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

EQT has acquired a 42% stake in Kelda Holdings, Yorkshire Water’s parent company

Yorkshire Water’s CEO said the deal was ‘a great step forward’

One of the world’s largest private equity firms has this morning bought a major stake in Yorkshire Water.

Swedish firm EQT has acquired a 42% stake in Kelda Holdings, the parent company of Yorkshire Water. It means that the firm now has three overseas owners, with EQT joining Singaporean sovereign wealth fund GIC and Australian firm TCorp in owning Kelda Holdings.

In a statement to the Stock Exchange, Yorkshire Water described EQT as a “purpose-driven global investor with deep experience in managing long-term strategic assets and a strong track record of managing critical infrastructure”. It said the deal “signals confidence in Yorkshire Water” and its £8.3bn plan for improving the county’s water infrastructure over the next five years.

The deal comes as water companies around the UK remain under intense scrutiny over both their environmental records and overseas ownership. Last week MPs on the Environment, Food and Rural Affairs Committee highlighted Yorkshire Water as one of the main users of bailiffs to collect debt from customers in the water industry. And last month, Yorkshire Water was fined more than £700,000 for polluting a country park stream with sewage three times in a year.

Advertisement

EQT was last year ranked as the second largest private equity firm worldwide based on funds raised and has a wide range of assets around the world in a number of different sectors. It said it would “work in partnership with its co-shareholders and the company’s management team to deliver sustainable operational improvements” and would also be “investing further equity” to strengthen the company’s balance sheet.

Announcing today’s deal, Yorkshire Water chief executive Nicola Shaw said: “This is a great step forward for Yorkshire Water. The EQT team will bring additional expertise to our board, and their backing is a strong vote of confidence in our plan to improve performance and the progress we have made so far.

“EQT has a long-term perspective and their team is committed to supporting the delivery of our £8.3bn investment programme. Their support, together with GIC and TCorp, will enable us to continue to execute our strategy, maintain focus on operational performance, and deliver the investment needed to improve outcomes for customers and the environment across Yorkshire.”

Kunal Koya, partner at EQT Infrastructure said: “Our strong track record as a long-term active owner of large infrastructure assets makes EQT a natural partner for Yorkshire Water. We believe that as a responsible private capital manager, EQT can play an important role in modernizing the UK’s water infrastructure, and the company’s multi-year investment plan reflects that objective.

Advertisement

“Together with Yorkshire Water’s existing investors, we will support the sector’s reform agenda and deliver service improvements for customers across the region and transparency for all stakeholders.”

The deal, which will depend on anti-trust approvals, has been welcomed by the Government. Investment Minister Lord Stockwood said: “I warmly welcome this commitment from a leading global infrastructure investor. EQT’s decision to invest in the UK’s regulated water sector underlines the strength of our investment environment and the trust international partners place in the UK economy. It demonstrates that the UK remains one of the world’s most attractive destinations for long‑term, sustainable investment.”

Shares in telehealth company Hims & Hers skyrocketed in premarket trading following a media report that the maker of Wegovy plans to sell the weight-loss drug on the platform, a move that would end a legal spat between the two companies.

Hims & Hers, which markets consumer drugs ranging from treatments for weight loss and erectile dysfunction in men, to treatments for menopausal symptoms in women, is set to offer Novo Nordisk’sNOVO.B 0.99%increase; green up pointing triangle blockbuster Wegovy on its platform, Bloomberg reported, citing an unnamed source.

Oil and gas prices surged Monday as the Middle East war roils energy markets, forcing major producers to shut down output while the Strait of Hormuz remains effectively closed.

In early European trading, Brent crude climbed 11% to $103.14 a barrel and West Texas Intermediate rose 8.9% to $89.49 a barrel, trimming earlier gains on news that Group of Seven ministers are set to discuss the joint release of petroleum reserves. The global benchmarks reached their highest levels since 2022 earlier in the session, touching $119.50 and $103.67 a barrel, respectively.

The latest surge in crude oil prices, with Brent crude once again climbing above the $100 mark, is sending shockwaves across global financial markets. As investors recalibrate strategies, the question on everyone’s mind is: how long will it take for markets to digest this oil shock?

Mark Matthews, a seasoned market strategist from Julius Baer notes, “How soon before markets begin to digest it? They are digesting it now. We can see the Asian markets. The Japanese stock market, for example, was up as much as 17% in late February; now it is flat on the year. So, we are pricing in this high oil price right now.”

When asked about the potential impact on India, Matthews said, “Last year was a very good year for markets like Japan, China, and the US, but India did not do much. So, there should not be as much downside for India. Of course, you could make the case that India uses more oil than some of those other economies or has to import more, but the Indian economy, like most economies in the world, has become more efficient in its oil usage. The pain point which used to be $80 a barrel is now probably around 100. The good news is that India is now able to buy Russian oil again, which takes some pressure off. But really, for India and the rest of the world, it all depends on how long this war lasts.”

Foreign investor sentiment toward India remains cautious but opportunistic. Matthews explains, “There was a breakout in emerging markets versus the US in February of a very long downward trend channel, it had been in place for more than maybe 15 years. But it was a false breakout because last week emerging markets went down more than the US. In general, they are more vulnerable to high oil prices. Most of the oil that goes through the Strait of Hormuz comes out here to Asia. So intuitively, if the war lasts, emerging markets, because they are primarily Asian, should underperform.”

Advertisement

Looking ahead to the upcoming Federal Reserve meeting, Matthews anticipates measured action. “It is premature for the Fed to react to this war in Iran, but the non-farm payroll reading for February was a loss. That would suggest they would be in favor of cutting interest rates. The market is looking for two rate cuts this year. One reason is because the Federal Reserve does not like to surprise the market. It likes the market to price in broadly what it is thinking. I do not expect one of those to necessarily be next week, but by the end of this year, there should be two.”

Live Events

Regarding hedging strategies for India, Matthews points to the oil sector rather than precious metals alone. “Gold and silver have done very well, but they are vulnerable because in risk-off events of this size, people like to take profit. With oil over $100 and war not ending soon, there is a case for owning the oil sector, not just in India but globally. Longer term, even when this war ends, if Iran is not stable, the Strait of Hormuz will not be stable either, and that is responsible for about 20% of the world’s oil trade.” He also highlighted potential central bank responses, saying, “Iran’s game plan is quite obvious. They want to get oil prices as high as possible to put pressure on the US. With high oil prices, we will see inflation, because oil feeds into many aspects of the consumer and producer price indices. Supply chain disruptions, like issues in the Suez Canal, are also inflationary. When you have inflation, it is hard to cut interest rates, and central banks might even have to raise them depending on how long the war lasts.”Finally, Matthews weighed in on China’s position in the current geopolitical landscape. “China has been very prudent in accumulating a large oil reserve—over 250 days’ worth. That is a good thing. But China is the largest buyer of Middle Eastern oil. Longer term, this could incentivize them to diversify, with Russia being an obvious option. Very few are winning in this scenario, but Russia, Norway, Kazakhstan, and Venezuela are among those benefiting.”

As global markets grapple with high oil prices, geopolitical tensions, and inflationary pressures, investors are navigating an uncertain landscape. While India’s underperformance relative to other emerging markets might cushion its downside, exposure to energy-related sectors could offer a strategic hedge in these turbulent times.