Business

China’s Moonshot AI seeks $30 billion valuation in new funding round- Bloomberg

Business

Oil Price Today (July 27): Crude oil dips 5%, below $95 as US pauses strikes on Iran. What are experts saying?

Crude oil price on July 27

Brent crude futures dropped $4.89, or 5.05%, to $91.89, after briefly falling below the key $90 support level earlier in the session. US West Texas Intermediate crude stood at $84.64 a barrel, down $4.67, or 5.23%. The decline comes after crude prices surged 10% last week.

Both benchmarks are now at their lowest levels in nearly a week, after climbing for the previous three weeks. Brent had earlier touched $100 a barrel as the conflict disrupted oil shipments through the Strait of Hormuz and spread to the Red Sea, affecting exports from Saudi Arabia, the world’s top oil exporter, to Asia through the Bab el-Mandeb strait.

However, the pause in attacks has not yet brought shipping through the region back to normal. Fewer than 10 commodity vessels crossed the Strait of Hormuz each day over the weekend, according to shipping data from Kpler.

Traffic through the Bab el-Mandeb strait also declined on Sunday after Yemen’s Houthis attacked Saudi oil installations along the Red Sea coast. A third Chinese supertanker, however, managed to exit through the Bab el-Mandeb strait.

Also read:Oil crosses $100: A ‘perfect hurricane’ can trigger bigger shock soon

Over the week, reports emerged suggesting that Pakistan is looking at ways to help restart the stalled U.S.-Iran negotiations aimed at ending their nearly five-month-old war, a Reuters report said, adding that the move follows an initiative from China.

Yemen’s Iran-backed Houthi movement announced a naval blockade against Saudi Arabia, a close ally of Islamabad that signed a mutual defence treaty with Pakistan last year. Pakistan depends on Saudi financial support and has strongly condemned recent Houthi attacks on Saudi Arabia. Taking a position that is seen as too sympathetic to Iran could therefore strain ties with Riyadh.At the same time, Islamabad is heavily reliant on Beijing, which has also provided significant financial support and has economic interests in a diplomatic resolution that would help reopen important trade routes across the Middle East.

What’s next for prices?

JPMorgan said in a note that every additional month of disruption to oil supplies could push Brent prices up by around $7 to $8 a barrel. If the disruption continues for three months, the bank expects monthly average Brent prices could climb to around $114 a barrel.

Goldman Sachs has warned that Brent crude could reach $120 a barrel if shipping through the Strait of Hormuz, the world’s most important oil transit route, remains disrupted. Its base case, however, is that tensions in the Middle East will eventually ease.

If the conflict subsides, Goldman Sachs expects Brent to average $80 a barrel in the fourth quarter and $75 next year. The bank said the risks to those forecasts remain “tilted to the upside”, citing the possibility of prolonged disruptions to shipping through both the Strait of Hormuz and the Red Sea.

Anindya Banerjee, Head of Commodity Research at Kotak Securities, said geopolitical developments were once again driving crude oil prices. “Any strike on major Gulf export infrastructure could force a retest of $95-100 and beyond,” he said.

Read more:Indian refiners scout new crude sources as Gulf risks rise

Banerjee said the market was now looking beyond military strikes and increasingly focused on the weakening prospects of a diplomatic breakthrough. Tehran has imposed new conditions for restarting negotiations, he said, while each new development is pushing back the return of normal tanker traffic through the Strait of Hormuz. Shipping activity through the waterway continues to remain well below pre-war levels.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of Economic Times)

NOBL: The Price Of Sitting Out AI

The tech-heavy Nasdaq fell as investors sold chip stocks on worries about massive spending on artificial intelligence ahead of the next batch of megacap earnings reports, while falling oil prices provided Wall Street with some support even as Middle East hostilities continued.

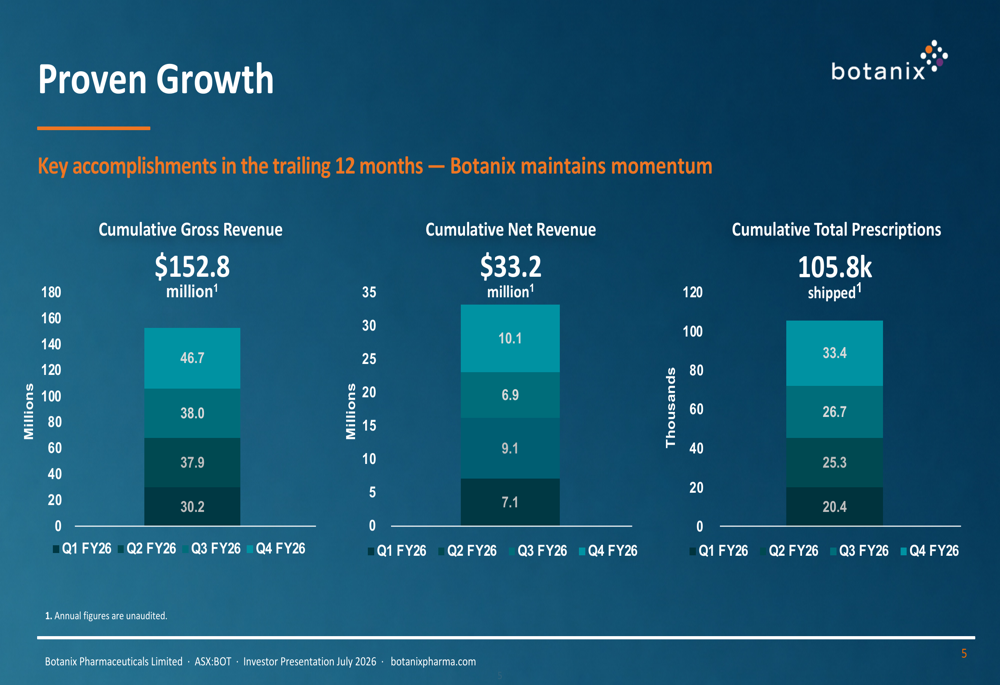

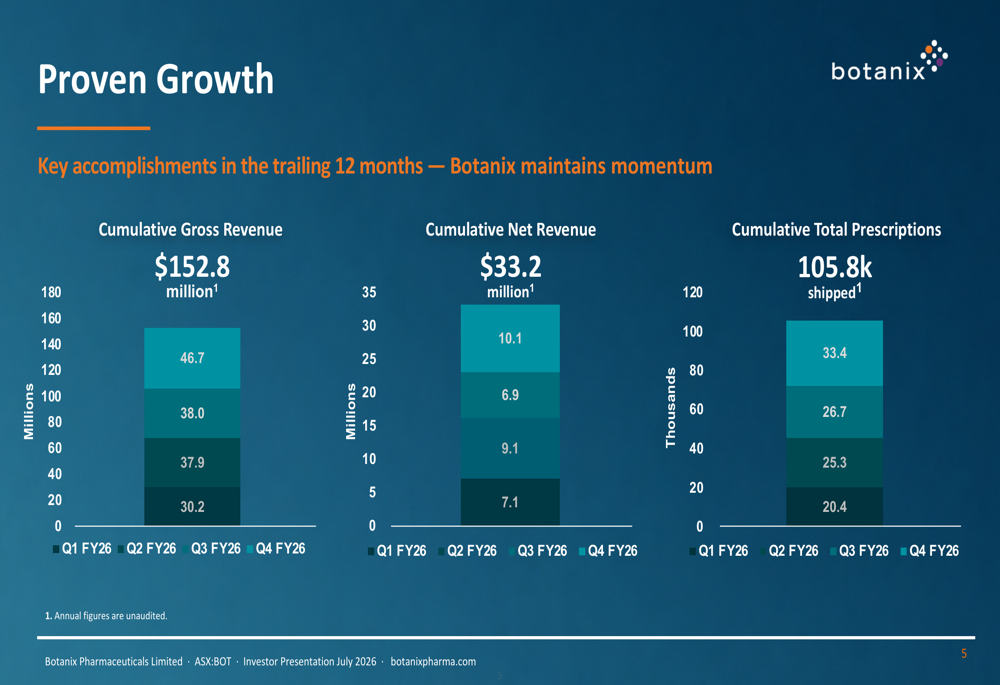

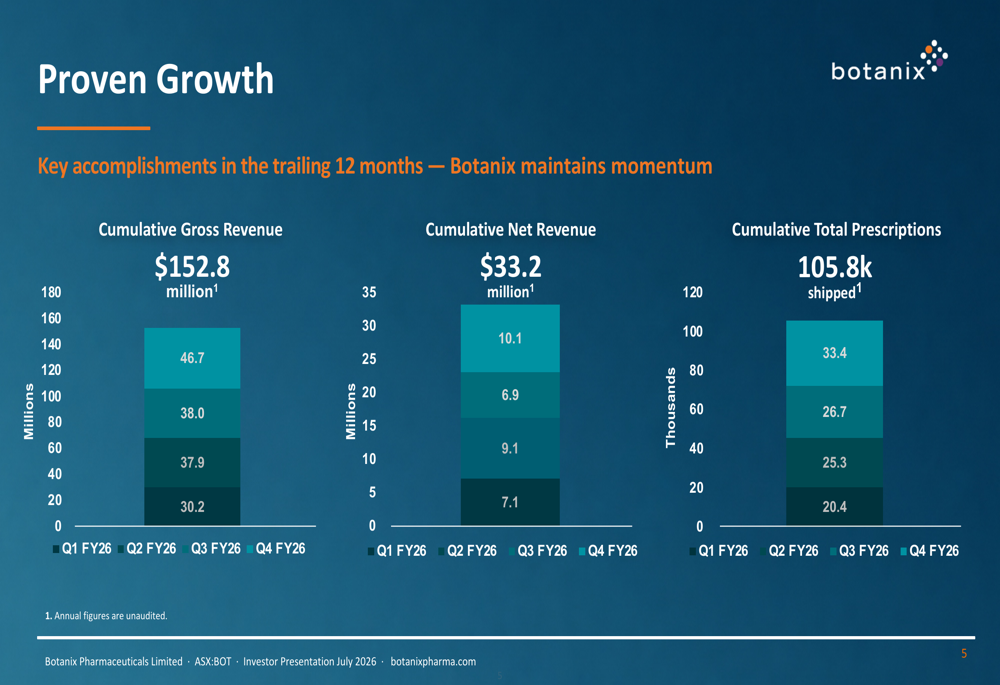

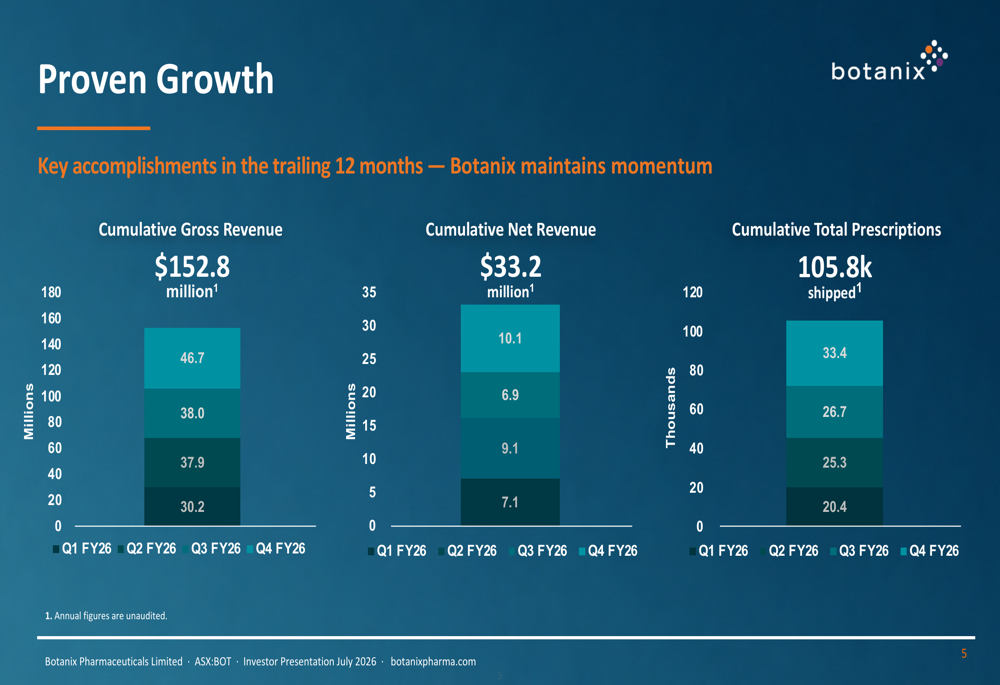

Botanix Q4 FY26 slides: revenue jumps 45% as stock slips near lows

China’s CXMT surges 470% in Shanghai debut after Asia’s biggest 2026 IPO

Shares in Subiaco-based ASX junior Carnaby Resources soared this morning, after ASX gold heavyweight Evolution Mining announced a $213 million all-scrip takeover bid.

Shein says it swung to a quarterly loss as its sales slowed after US President Donald Trump removed an import duty exemption on small packages.

It also comes as uncertainty remains over the tit-for-tat US-China tariffs wars, which is currently paused.

The fast-fashion giant, which has its headquarters in Singapore but was founded in China, said it lost $99m (£74.1m) in the first three months of the year, compared with a net income of $395m a year earlier.

The announcement is part of the firm’s preparations ahead of its stock market debut in Hong Kong, although the filing did not give any details on the size, timetable or pricing of the planned initial public offering (IPO).

“In response to the increased duties and taxes, we are pursuing a wide range of options, including increasing our prices in the US market to offset a portion of the increased costs,” Shein said in the filing.

The company also said the Iran war had hit demand, increased costs and caused delays of deliveries in some markets.

The first-quarter figures also partly reflected a paper loss of $328m due to an accounting change for special investor shares. The shares can be turned into ordinary stock later, and their value can change before a listing.

The filing showed that in the year to the end of March 2026 Shein had 281 million active customers – a rise of more than 16% on a year earlier – who placed a total of more than one billion orders.

On 10 July, the China Securities Regulatory Commission (CSRC) gave Shein approval for a Hong Kong share sale after failed attempts to list in New York and London.

The Hong Kong share listing is expected to take place in the coming months.

The figures show the impact of a Trump-signed executive order to end a global tariff exemption that had been used by US shoppers of low-cost goods.

That order, which came into effect on 29 August 2025, broadened an earlier presidential action which specifically targeted cheap products from China and Hong Kong to cover the rest of the world.

The so-called de minimis exemption had allowed goods valued at $800 or less to enter the US without paying any tariffs. US consumers relied on the exemption to buy cheap goods from online commerce sites like Shein and Temu.

The White House said the global exemption was being used to “evade tariffs and funnel deadly synthetic opioids” to the US.

“The removal of the US de minimis exemption has had an adverse impact on our sales in the US and the overall growth of our net revenues,” Shein said in the filing.

Earlier in July, the European Union imposed a €3 (£2.56; $3.42) levy on low-value e-commerce imports.

The measure is aimed to curb what the trading bloc has said is unfair competition from China.

El Salvador opposition pitch former lawmaker, doctor to run against Bukele in 2027

Botanix Q4 FY26 slides: revenue jumps 45% as stock slides

Brent crude fell as much as 7.4% to below $90 a barrel, before paring losses as the US paused an almost two-week run of strikes against Iran. MSCI’s Asia Pacific equities gauge rose 0.4% and contracts for the Nasdaq 100 Index climbed 1.2% as sentiment improved after last week’s selloff in chip stocks.

The dollar, the haven of choice during the Middle East conflict, weakened against almost all of its Group-of-10 peers as tensions eased. Treasuries gained along with government bonds in Australia and New Zealand as inflation concerns receded. Gold led precious metals higher.

Read more: August Rush: Over 2 dozen companies plan Street debut next month

“A resolution to the conflict would be a positive development,” said Shoji Hirakawa, chief global strategist at Tokai Tokyo Intelligence Lab. The pause in attacks raises “hopes that the two sides will enter negotiations.”

The lull in hostilities sets the tone for a pivotal week in markets, with traders focused on whether the Federal Reserve will raise interest rates on Wednesday after the recent surge in oil prices fueled inflation concerns. Investors are also awaiting earnings from megacap technology companies after a recent backlash against heavy spending on artificial intelligence.

After striking Iran for 13 days, the US has apparently held off since late Friday without explanation, raising questions about President Donald Trump’s next move. Iran’s army said Sunday that Tehran had also suspended its military response. The pause came as Iranian and Omani officials held talks over shipping through the Strait of Hormuz, raising hopes that the key oil transit route may avoid further disruption.

Tensions in the Middle East had sent oil prices soaring in July, overshadowing a tamer-than-expected reading on June consumer prices that seemed to offer officials breathing room to keep rates stable. Add to that a demand boom fueled by AI and the Trump administration’s announcements of new tariffs, and Fed watchers see the possibility of dissents at the July 28-29 meeting if officials again leave policy unchanged.

“We think the Fed will probably not hike,” Krishna Guha, head of central bank strategy at Evercore ISI, wrote in a note. “But we cannot take the probability too low given Warsh’s refusal to set out his strategy,” he said, referring to the new Fed chair Kevin Warsh.

Three days of Group-of-Seven central bank decisions begin with the Fed on Wednesday, followed by the Bank of England and the Bank of Japan. While no changes are expected in interest rate policy, officials are likely to emphasize vigilance over the inflationary impact of higher energy prices.

Elsewhere, the Singapore dollar strengthened against the US currency after officials further tightened monetary policy. The Monetary Authority of Singapore, which uses the exchange rate as its main policy tool rather than interest rates, raised the rate of appreciation of its policy band “very slightly,” it said. It left the width and center unchanged.

In other corners of the market, the yield on the Treasury 10-year fell five basis points to 4.63%. Non-interest-bearing gold climbed over 1% to $4,100 an ounce. The yen strengthened to about 163.60 per dollar.

Another key focus for markets will be earnings from megacap technology companies after a recent round of selloff in AI stocks rekindled doubts over whether billions of dollars being poured into infrastructure will generate commensurate returns. The selloff showed how much the narrative around AI and the Magnificent Seven tech behemoths has shifted.

This change makes for a tough setup heading into this week, with earnings from Microsoft Corp. and Meta Platforms due on Wednesday, followed by Apple Inc. and Amazon.com Inc. on Thursday.

“That is shaping up as the major clearing event for the month,” said Billy Leung, an investment strategist at Global X Management. “The market has been punishing AI capex guidance all July even when the underlying numbers beat, so the read-through from these three on spending trajectory and monetisation will do more to set direction than anything in today’s session.”

Kevin Warsh Wanted a ‘Family Feud’ at the Fed; At Wednesday’s Meeting He Might Get One

Dance Moms Alum Paige Hyland Fires Back at Body Criticism

Anytime 13u vs the money flock 13u

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World6 days ago

Crypto World6 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat5 days ago

NewsBeat5 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech6 days ago

Tech6 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat7 days ago

NewsBeat7 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Business5 days ago

Business5 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment5 days ago

Entertainment5 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Tech7 days ago

Tech7 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

NewsBeat6 days ago

NewsBeat6 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World7 days ago

Crypto World7 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Tech7 days ago

Tech7 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

-

Tech3 hours ago

Tech3 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Sports6 hours ago

Sports6 hours agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos3 days ago

News Videos3 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Sports3 days ago

Sports3 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion3 days ago

Fashion3 days ago16 Dresses for the High Summer Event

-

Entertainment7 days ago

Entertainment7 days agoStephen Colbert Returns to Social Media After Late Show End

-

Politics14 hours ago

Politics14 hours agoSpain sweeps the board at 2026 World Cup with individual awards

You must be logged in to post a comment Login