Business

Electro Optic Systems Shares Surge 12.6% as ASX 200 Inclusion and Defense Boom Fuel Rally

Shares of Electro Optic Systems Holdings jumped sharply on Friday, climbing 12.63% to $10.52, as the Australian defense and space technology company rode a wave of investor enthusiasm ahead of its imminent inclusion in the benchmark S&P/ASX 200 index and continued momentum from a string of strong order intake announcements.

The rally extended a powerful run for the Canberra-based laser and counter-drone systems maker, whose stock has been one of the standout performers on the Australian market over the past several weeks as defense spending tailwinds, a major capital raise, and surging contract backlogs combine to reshape investor sentiment around the company.

Index Inclusion on the Horizon

The most immediate catalyst behind the stock’s latest surge is its pending entry into one of Australia’s most closely watched equity benchmarks. The company is scheduled to join the ASX 200 index on June 22, 2026, a milestone expected to drive institutional demand. Index inclusion typically triggers automatic buying from passive funds that track the benchmark, a dynamic that has helped lift the share prices of newly added companies in the days leading up to their formal addition.

Recent capital raisings, including an upsized Share Purchase Plan that received AU$95 million in applications, have significantly strengthened the balance sheet for future scaling. That overwhelming demand from retail shareholders underscored just how much investor appetite has built around the company’s growth story in recent months.

A Capital Raise That Exceeded Expectations

The scale of investor interest in EOS became clear earlier this month when the company’s share purchase plan drew applications far beyond its original target. Electro Optic Systems completed its share purchase plan, exceeding its initial fundraising goals due to overwhelming demand from retail investors. Initially targeting a $25 million raise, the defence and space communications company received valid applications totalling $95 million from 4,909 eligible shareholders.

The EOS board exercised its discretion to upsize the final SPP acceptance to $40 million, balancing retail shareholder rewards with disciplined capital efficiency. The SPP was executed in tandem with a prior $150 million institutional placement and a $40 million strategic placement announced in May.

To manage the massive oversubscription equitably, EOS implemented a structured scale-back mechanism, with applications scaled back on a pro-rata basis according to existing holdings as of the May 15 record date. The new shares were formally issued on June 16, with holding statements dispatched the following day, and trading of these new securities began on the Australian Securities Exchange on June 17.

Record Order Backlog Underpins the Growth Story

Beyond the index inclusion catalyst, EOS has built its rally on a foundation of genuinely strong underlying business momentum, with order intake figures that have substantially outpaced the company’s revenue base.

EOS maintains a robust contract backlog exceeding AU$518 million, providing high revenue visibility. Management recently issued optimistic 2026 revenue guidance of up to AU$270 million for its base business, representing potential growth of over 100% compared to previous performance levels.

The trajectory of that order book has accelerated dramatically over recent quarters. Order book surged 237% to AUD 459 million, with the company debt-free and holding AUD 107 million in cash following a AUD 91 million gain from the sale of its EM Solutions business. Following that earnings report, the stock jumped 16.94% to AUD 7.32, reflecting investor confidence in the company’s strategic direction despite a revenue decline.

Revenue fell to AUD 128.5 million due to divestments, but gross margin rose to 63%. Order intake surged to AUD 420 million, boosting the order book to AUD 459 million. Management has emphasized a continued strategic focus on counter-drone and space control technologies, two of the fastest-growing segments within the global defense and security technology market.

A Trading Update That Sparked the Most Recent Climb

The current rally traces back to a business update released earlier this month that gave investors fresh confidence in the company’s near-term revenue trajectory. Electro Optic Systems Holdings shares moved higher after the defence company released a trading update, with EOS shares climbing as a new U.S. order boosted the company’s growth outlook.

That announcement came on the heels of broader market volatility tied to the historic SpaceX initial public offering, which dominated headlines on the ASX in mid-June. SpaceX began trading on the Nasdaq under the ticker SPCX, priced at US$135 per share, implying a valuation of approximately US$1.75 trillion — a listing that surpassed Saudi Aramco’s 2019 offering. Against that backdrop of broader market attention on defense and aerospace-adjacent technology names, EOS has continued to attract its own dedicated following among investors betting on Australia’s growing role in global defense supply chains.

Strategic Acquisitions Expanding the Company’s Footprint

EOS has also been actively reshaping its business through acquisitions designed to broaden its addressable market beyond its traditional Australian defense base. The acquisition of MARSS makes EOS a global provider of integrated counter-UAS solutions, expanding into military, homeland security, and adjacent markets. Analysts project strong growth as the company integrates its MARSS acquisition and targets AU$240 million to AU$270 million in 2026 revenue, even though the stock had declined approximately 3.8% over the prior month amid volatility stemming from the massive capital raise and shifting geopolitical sentiment.

The company’s broader strategic ambitions extend beyond its current home exchange as well. Australia’s Electro Optic Systems was reported earlier this year to be “very likely” to shift its headquarters and stock market listing, a development that, if it materializes, could mark a significant turning point in the company’s corporate structure as it scales internationally.

Execution Risk Remains the Key Question

Despite the wave of bullish catalysts, analysts continue to flag meaningful uncertainty about whether EOS can convert its surging order book into consistent, profitable operations. Investors remain concerned about the company’s ability to transition from order capture to operational execution. Converting the record AU$518 million backlog into tangible cash flow and consistent profitability remains a critical challenge over the next 12 to 24 months.

Execution and order conversion risks aside, the company’s focus on counter-drone and space control markets continues to draw investor interest, even as supply chain delays and geopolitical tensions are identified as key risks to growth.

Despite that caution, the longer-term price target trends among some analysts remain notably more conservative than the stock’s current trajectory would suggest. EOS’s average analyst price target sits well below recent trading levels, reflecting a degree of skepticism about whether the company’s current valuation can be sustained without clearer evidence of sustained profitability.

A Volatile But Resilient 12 Months

The magnitude of Friday’s gain underscores just how dramatically EOS shares have moved over the past year. The company’s share price has ranged from a low near $1 to a high approaching $8 over the trailing 12 months, before this month’s surge pushed shares well beyond that prior range entirely — a reflection of how quickly sentiment toward Australian defense technology names has shifted as global military spending continues to climb and counter-drone systems take on growing strategic importance for militaries and security agencies worldwide.

With the ASX 200 inclusion now just days away and the company’s order backlog continuing to swell, investors will be watching closely in the weeks ahead to see whether EOS can begin translating its remarkable run of contract wins into the kind of consistent earnings performance that would justify its newly elevated market valuation.

Gathering the right documents is the part of selling a home that catches most people off guard. You picture viewings and offers, then a solicitor asks for forms you have never heard of.

The pressure is real. Nearly one in three agreed sales (29.8%) in the UK collapsed before completion in 2024, and missing or late paperwork is a frequent reason deals stall. The reassuring news is that the list is finite, and most of it can be sorted before your home even goes live.

Independent chartered surveyors King West have produced a plain English guide to the paperwork you need to sell my house, and this article walks through each document so you can be sale ready from day one.

Key Takeaways

- Every seller needs ID, title deeds, an EPC, and two standard property forms (TA6 and TA10).

- An EPC is a legal requirement and stays valid for ten years from the date it is issued.

- Leasehold homes need extra documents, including the lease and a freeholder’s management pack.

- Improvements often need certificates such as FENSA, regulations approval, or planning consent.

- Starting early removes the delays that cause so many sales to fall apart.

The Short Answer on Documents You Need

Selling a home in the UK calls for identity and address documents, your title deeds, a valid Energy Performance Certificate, a completed Property Information Form (TA6), and a Fittings and Contents Form (TA10). Leasehold homes call for further paperwork on top of these basics.

Most of these items sit with you, your conveyancer, or a public register, so none should be a mystery once you know where to look. The trickier factor is timing. Sellers who leave it late often watch a transaction drift while a single certificate is tracked down.

| Document | What it does | Where to get it |

|---|---|---|

| Proof of ID and address | Confirms who you are for compliance checks | Passport or driving licence plus a recent bill |

| Title deeds | Show you legally own the property | HM Land Registry or your conveyancer |

| EPC | Rates the home’s energy use | An accredited domestic energy assessor |

| TA6 form | Discloses the property’s key facts | Completed by you with your conveyancer |

| TA10 form | Lists what stays and what goes | Filled in by you and your solicitor |

| Leasehold pack (TA7) | Sets out lease terms and charges | Your freeholder or building manager |

Fall-through rates have climbed sharply, which is why early preparation matters.

Proof of Identity and Address Comes First

Proof of identity is the very first thing any UK seller hands over. Estate agents, conveyancers and mortgage lenders are all bound by law to verify who you are under rules that guard against money laundering, so nothing progresses until these checks clear.

You will usually be asked for two separate items:

- A current passport or photocard driving licence to confirm your identity.

- A recent utility bill or bank statement, dated within the last three months, to confirm your address.

| Heads up: Without verified identity documents, a solicitor cannot open a file or start work, so sort this out the moment you instruct one. |

Title Deeds and Proof That You Own the Home

Title deeds are the legal records that prove you own a property and hold the right to sell it. For most homes these are stored electronically, so your conveyancer can pull an official copy of HM Land Registry’s official records within minutes.

A digital official copy of the title register currently costs seven pounds, following a fee change in December 2024. If you bought the home recently, you may still have your own copy from that purchase.

There is a catch for older homes. Around 15% of land and property in the UK is still not registered, and selling an unregistered home means proving ownership with the original deeds, often through a first registration application that your solicitor handles.

Most homes in the UK sit on the register, so a lost paper deed rarely stops a sale. The register is the proof that counts.

Why an EPC Is Not Optional

An Energy Performance Certificate, or EPC, is a document that rates a home on energy efficiency using a scale from A to G. It has been mandatory for sellers since 2008, and you must have ordered one before your property is advertised.

Each certificate remains valid for a decade, so check the public register before paying for a new assessment. You can read the government’s official EPC guidance to see how the rating is produced and who can carry it out.

Standards tightened in June 2025, with assessors now recording more detail about glazing, heating and insulation. Keeping receipts for any energy upgrades helps your home earn the rating it deserves.

| Pro tip: Arrange your EPC as soon as you decide to sell. Many estate agents can book the assessment for you, and a better rating can lift buyer interest. |

The TA6 and TA10 Forms Explained

The TA6 Property Information Form is where you disclose the practical facts about your home. It covers boundaries, neighbour disputes, building work, guarantees, flood risk, parking and utilities, and a buyer’s solicitor leans on it heavily.

The TA10 form sits beside it. This document records precisely what is included in the price, from kitchen appliances and curtains to light fixtures and garden sheds, which heads off arguments on completion day.

Accuracy on both forms matters more than sellers expect. In a recent Google review, one King West client thanked the team for going above and beyond to resolve issues that surfaced during their sale, the sort of snags that often trace back to unclear documentation. Tidy paperwork from the outset gives your agent and solicitor far less to untangle later.

Extra Documents for Leasehold Properties

Leasehold sellers carry a heavier load than freeholders. Alongside the core documents, you will need the lease itself, a leasehold information form (TA7), and a management pack from your freeholder or managing agent.

A typical leasehold bundle includes:

- The lease agreement and any deed of variation.

- Ground rent and service charge statements for recent years.

- Buildings insurance details held by the freeholder.

- Recent accounts and minutes from the management company.

- Notices of any major works planned for the building.

| Worth knowing: Management packs can take several weeks to arrive and often carry a fee, so request yours the moment you list. Leasehold flats also fall through more often than freehold homes, which makes early preparation even more valuable. |

Certificates for Building Work, Safety and Guarantees

Any work carried out on the property tends to come with paperwork a buyer will expect to inspect. Replacement windows need a FENSA or CERTASS certificate, while extensions and structural changes need building regulations completion certificates and, where it applied, planning permission.

Pull together anything that proves work was done properly:

- FENSA or CERTASS certificates for replacement windows and doors.

- Completion certificates from building control for extensions or conversions.

- Planning permission documents where consent was required.

- Gas Safe records and an electrical condition report where relevant.

- Warranties and guarantees for damp proofing, timber treatment, a boiler, or a newer build.

If a mortgage is still secured on the home, your conveyancer will also need a redemption statement showing the outstanding balance owed to your lender.

Where an original has gone astray, an indemnity policy can reassure a cautious buyer, though tracking down the genuine paperwork is always the cleaner route.

When to Start and How Long It Takes

The best moment to gather documents is before your home reaches the open market. Some items appear instantly, while others take weeks, and the slow ones are usually the documents that hold up an otherwise healthy sale.

Front loading this work also strengthens your position once an offer lands, because a buyer who can proceed without waiting on missing papers is far less likely to drift towards another property.

Lead times vary widely, so start with the documents that take longest.

Buyers move faster when everything is ready, which is one of the simplest ways to sell your house quickly. Choosing a solicitor early helps too, so it pays to start comparing conveyancing quotes as soon as you list.

Delays bite hardest inside a property chain, where one slow seller can stall everyone. Your route to market matters as well, so weigh up selling at auction against using an estate agent before you commit.

Frequently Asked Questions

Can I sell my house without an EPC?

No. An EPC is mandatory, and you need one in place before the property is marketed. A small number of listed buildings and homes due for demolition are exempt. Each certificate lasts ten years, so check whether yours is still current.

What if I cannot find my title deeds?

There is no need to panic. The vast majority of UK homes are registered, so your conveyancer can download a digital copy of your title register from HM Land Registry for seven pounds. Unregistered homes need to apply for first registration instead.

How long does it take to gather selling documents?

Identity checks and an official title copy take minutes. An EPC usually arrives within a few days. Leasehold management packs and replacement certificates can run to several weeks, so tackle those first to protect your timeline.

Who fills in the property information forms?

You complete both yourself, normally with guidance from a conveyancer. The TA6 sets out details of the property, while the TA10 covers the fittings included in the sale. Getting them right shields you from disputes nearer completion.

Do I need certificates for work done on the house?

Yes, where that work required them. New windows require FENSA or CERTASS sign off, and an extension needs building control approval. Indemnity insurance can cover a missing certificate, although many buyers prefer to see the originals.

Getting Sale Ready

Selling a home runs far more smoothly when the documents are ready before the first viewing. Identity checks, title deeds, an energy certificate and the two property forms make up the backbone of every sale, with leasehold homes and improved properties adding a few extras.

Pull these together early, lean on your conveyancer for the technical forms, and you remove the most common cause of last minute hold ups. A prepared seller is a confident one, and that confidence is what carries a deal from accepted offer through to completion.

Gold heads for third straight weekly fall as hawkish Fed eclipses Iran truce cheer

Yen teeters on cusp of 40-year low as BOJ hike fails to stem rout

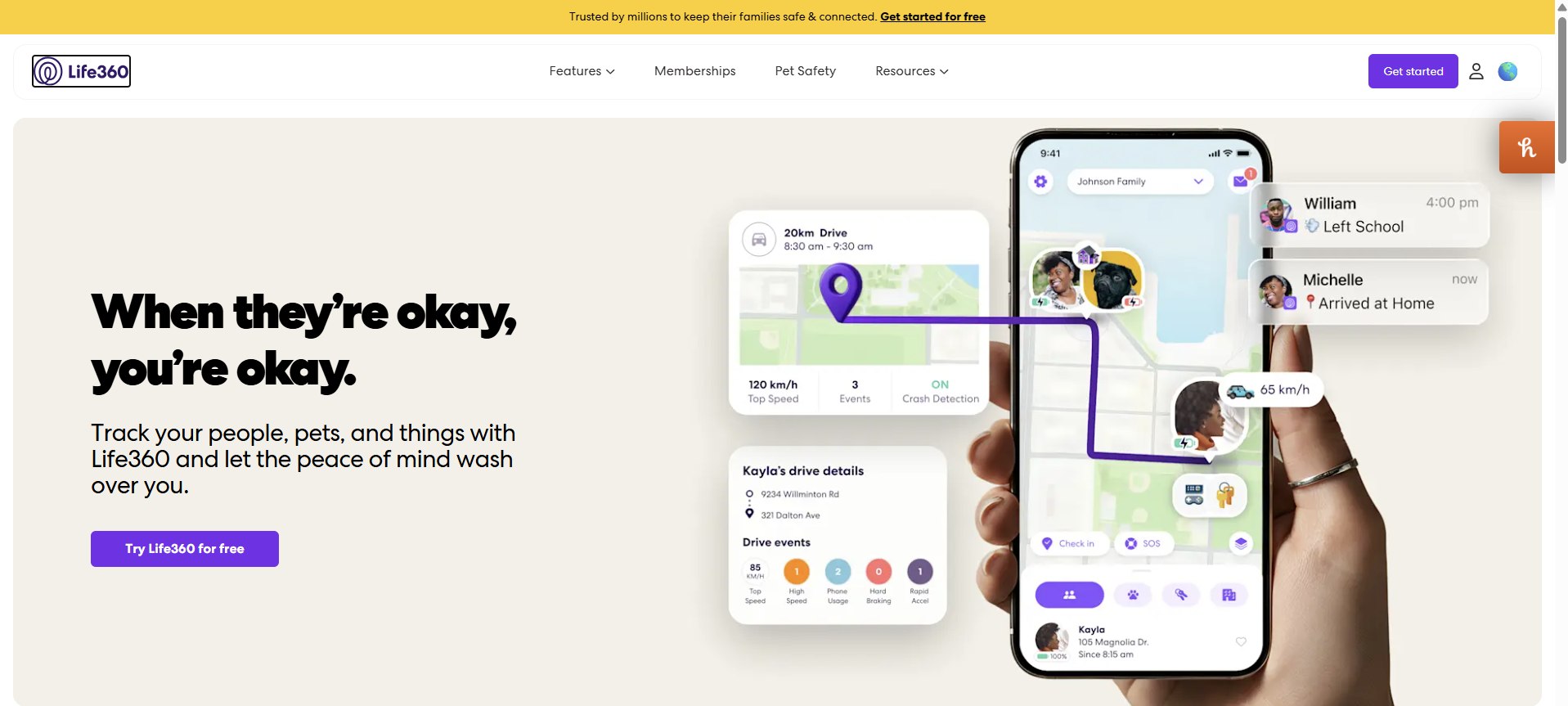

Shares of Life360 Inc. rose 6.19% on Friday, climbing $1.39 to close at $23.84, after the family safety and location-tracking company launched a new ride-hailing integration with Uber, giving the app’s tens of millions of users a fresh tool for monitoring rides taken by family members.

A New Integration Aimed at Driving User Engagement

The new Uber integration went live for Life360 members in select markets on June 18, 2026, marking the latest expansion of the company’s core family safety platform into adjacent services that touch everyday family logistics.

Life360, Inc. is a family connection and safety company. The company’s mobile app, Tile tracking devices, and Pet GPS tracker help members stay connected to people, pets, and things, with a range of services including location sharing, safe driver reports, and crash detection with emergency dispatch. The company’s core offering, the Life360 mobile application, includes features like communications, driving safety, digital safety, and location sharing.

A Massive and Growing User Base

The Uber partnership arrives as Life360 continues to expand a user base that already ranks among the largest in the family safety technology category. Life360 has become a meaningful part of everyday family life for more than 97 million people who use the app to keep their families safe and connected, according to Chief Executive Officer Lauren Antonoff.

Life360 is the world’s largest family-focused social network, with nearly 100 million monthly active users. The company exited 2025 with over 95 million monthly active users and 2.8 million Paying Circles, with a clear path toward 20% monthly active user growth.

Record First-Quarter Results

Friday’s rally builds on a string of strong recent financial results for the company. Life360 announced unaudited financial results for the first quarter of 2026 ended March 31, 2026, achieving record-breaking results across key metrics, including Paying Circles, Global Net Additions, Subscription Revenue, Annualized Monthly Revenue, and Advertising Revenue.

Life360 reported total revenue climbing 38% year-over-year to $143.1 million in the first quarter of 2026. Subscription revenue grew by 32%, with significant international expansion, while advertising revenue surged by 329%, benefiting from organic growth and acquisitions.

Antonoff highlighted the role of the company’s advertising business in driving that growth. “The value we deliver to our members powered record-breaking Paying Circle additions in Q1,” Antonoff said. “At the same time, our Life360 Ads platform scaled to become a material part of our business.”

A Strengthened Balance Sheet

The company has also significantly bolstered its cash position over the past year, giving it additional flexibility to pursue further growth initiatives and strategic acquisitions. Life360 ended the first quarter of 2026 with $459.0 million in cash, cash equivalents, restricted cash, and short-term investments, a significant increase from $170.4 million a year earlier, primarily driven by net proceeds from a June 2025 convertible notes offering and operating cash flows generated over the prior twelve months. In the first quarter alone, the company generated operating cash flows of $17.2 million, up 42% year-over-year.

That increase in cash was primarily driven by net proceeds from the issuance of the June 2025 convertible notes and cumulative positive operating cash flow, partially offset by $106.4 million in purchases of short-term investments and $55.6 million of net cash paid for the acquisition of Nativo.

A Mixed Market Reaction to Growth

Despite the strong top-line results, the stock’s reaction to the company’s first-quarter earnings report was initially negative, reflecting investor concerns about the costs associated with that growth. Despite the revenue growth, the company’s stock fell 3.13% in after-hours trading following the earnings release, closing at $42.67. The market reaction appeared to be influenced by a decline in gross margin and increased operating expenses. Operating expenses rose by 46%, impacting profitability, and technical issues affected user registration, potentially influencing future growth.

Revenue Guidance and Analyst Price Targets

Looking ahead, the company has issued a formal outlook for the remainder of the year that reflects continued, if somewhat moderated, growth expectations. Life360 issued revenue guidance for fiscal 2026, with expected consolidated revenue of $640 million to $680 million, including subscription revenue of $460 million to $470 million, other revenue of $140 million to $160 million, and hardware revenue of $40 million to $50 million.

Wall Street’s outlook on the stock has shifted somewhat in recent weeks. Citi recently lowered its price target on Life360 to $60.15 from $68.30, while maintaining a Buy rating on the stock. Analysts have separately adjusted their broader price target for the stock down to A$38.46 from A$42.13, reflecting updated views on growth, margins, and the price-to-earnings ratio they are prepared to apply to the stock.

Other research has offered a more bullish long-term view of the company’s trajectory. With a near 200% year-over-year increase in operating cash flow generated in the fourth quarter alone, Life360’s unit economics are seen as highly optimized. With a clear path to 20% monthly active user growth and $640 million to $680 million in consolidated revenue guided for 2026, the company is viewed as structurally designed to generate significant long-term flexibility as it marches toward its goal of $1 billion in annual revenue.

A Volatile but Strong Multi-Year Performance

Despite recent share price swings, Life360 has delivered substantial returns for long-term shareholders. Total returns to shareholders have reached 306% over the past three years, reflecting the company’s broader growth trajectory even amid periodic volatility tied to individual earnings reports and shifting analyst sentiment.

Simply Wall St’s valuation model estimates the intrinsic value of the stock at AU$43.67 per share, offering one additional data point as investors weigh the company’s current valuation against its long-term growth prospects.

Continued Expansion Into New Revenue Streams

The Uber integration represents the latest example of Life360’s broader strategy of layering additional services on top of its core family-location platform, an approach the company has also pursued through targeted acquisitions. Among Life360’s competitors in the family safety technology space are Qustodio, Sygic, FindMyKids, GeoZilla, and Bark Technologies, underscoring the increasingly competitive landscape the company is navigating as it works to diversify its revenue streams beyond its traditional subscription business.

With the new Uber ride integration now live in select markets and the company continuing to scale its advertising platform alongside its core subscription business, investors will be watching closely to see whether Life360 can sustain its recent pace of user growth while improving the profitability metrics that weighed on the stock following its first-quarter earnings report. The company’s upcoming quarterly results will offer the next significant test of whether initiatives like the Uber partnership can meaningfully contribute to the broader revenue diversification strategy management has outlined for 2026 and beyond.

Friday, June 19, marks Juneteenth, the federal holiday set aside annually to commemorate the abolition of slavery in the United States — and as Americans across the country observe the day, many are left wondering exactly which banks, government offices, retailers, and delivery services will be operating on normal schedules.

The recognition dates back to June 19, 1865, when Major General Gordon Granger traveled to Galveston, Texas, to deliver the news that enslaved people had been freed, sparking widespread celebrations. Though the historical day has been recognized for more than 150 years, Juneteenth wasn’t officially designated a federal holiday until President Joe Biden signed the Juneteenth National Independence Day Act into law in 2021.

In observance of the holiday, schools that haven’t yet entered summer recess will be closed, and many employees will have the day off from work. Below is a complete breakdown of what to expect from banks, the postal service, shipping carriers, government agencies, restaurants, and major retailers this Juneteenth.

Banks Will Be Closed

A majority of banks, credit unions, and other financial institutions will be closed on Friday, June 19, including Bank of America, Chase, Citibank, Capital One, M&T, PNC, Santander, Truist, and Wells Fargo. That means customers will not be able to do business at most branches other than performing ATM transactions. It also means that any withdrawals or deposits made on the holiday will not post until at least the following business day, which, at the earliest, is Monday, June 22.

The Stock Market Will Be Closed

Like banks, U.S. stock markets follow the Federal Reserve’s holiday schedule, meaning markets will be closed on Friday. Trading will resume on Monday, June 22, at 9:30 a.m. Eastern Time. The closure affects all major U.S. exchanges, giving traders and investors a three-day weekend before markets reopen.

No Mail Delivery This Friday

On Friday, June 19, a majority of government agencies and offices will be closed in honor of Juneteenth. Given that the U.S. Postal Service is a federal agency, all post offices will be closed and there will be no mail delivery. Post offices will reopen on Saturday, and mail delivery will resume at that time.

UPS and FedEx Will Operate Normally

Unlike the Postal Service, private shipping carriers will continue normal operations on the holiday. Though UPS offers adjusted hours on certain holidays, the shipping service will operate normally on Juneteenth. Whether someone is shipping a package, expecting a delivery, or has business at a UPS Store, all will be open as usual.

FedEx will also be open on Friday, June 19, with shipping and delivery services operating on a typical weekday schedule. Customers expecting time-sensitive deliveries through either carrier should not experience any disruption tied to the holiday.

The DMV Will Be Closed

Even though each state operates its own bureau or department of motor vehicles, all are run by local government agencies. That means DMV offices are typically closed on federal holidays, including Juneteenth Independence Day, and residents needing to renew licenses, register vehicles, or handle other DMV business should plan around the closure.

Restaurants Will Remain Open

Many restaurants remain open on major holidays like Thanksgiving, Christmas, and Easter to serve customers who prefer to eat out, and the same holds true for Juneteenth. A majority of eateries, restaurants, and fast-food chains will be open during normal business hours, giving diners plenty of options for marking the holiday with a meal out.

Major Retailers Stay Open, With One Notable Exception

Nearly all major retail chains will be open during normal business hours on Friday, June 19, including Walmart, Target, Costco, Home Depot, Lowe’s, Kohl’s, Macy’s, TJ Maxx, and most others. Shoppers looking to run errands or take advantage of holiday sales should not encounter any closures at these retailers.

One notable exception stands out among major chains: Patagonia. The outdoor retailer historically closes all its U.S. stores on June 19 in observance of the holiday, a practice that has set the company apart from most of its retail peers in how it marks Juneteenth.

Grocery Stores and Pharmacies Will Be Open

For anyone needing to stock up on groceries or fill a prescription, most major grocers will be open for business as usual on Friday, including Aldi, Kroger, Whole Foods, Trader Joe’s, Albertsons, Stop and Shop, Publix, H-E-B, Safeway, and ACME, among others. Shoppers should not expect any disruption to regular grocery shopping routines as a result of the holiday.

Planning Ahead for the Long Weekend

With banks, the stock market, the postal service, and DMV offices all closed Friday, those with time-sensitive financial transactions, mail needs, or government business may want to plan accordingly before the holiday or wait until offices reopen the following business day. Meanwhile, anyone needing to ship a package, grab dinner out, or run essential errands at a grocery store or major retailer should find business largely unaffected, with most of the retail and shipping sectors continuing normal operations straight through the holiday.

For those observing Juneteenth as a day of reflection and celebration, the mix of closures and continued operations underscores how the holiday — now in its fifth year as an officially recognized federal observance — has settled into a pattern similar to other major U.S. holidays, with financial institutions and government offices pausing operations while much of the retail and hospitality sector continues serving customers as usual.

With markets, banks, and government offices set to reopen Monday, June 22, the coming business week will see a return to standard operating hours across the financial sector. Any pending transactions, mail deliveries, or DMV appointments delayed by Friday’s holiday closures should resume processing as normal once offices reopen at the start of the new week.

Bel Fuse: A Better Business, But The Premium Is Already High

He has been called the “Superyacht Influencer” by Forbes, featured in Bloomberg, GQ, Tatler and Robb Report, and commands a social footprint that reaches more than 100 million people each month.

Jonny Dodge presents himself as one of Britain’s most successful luxury entrepreneurs, with a portfolio of eight companies spanning superyachts, private aviation and Formula One hospitality. But a developer complaint currently dominating the homepage of mothercitycapital.com raises direct questions about the financial practices connected to his network.

The Public Empire

Dodge has spent more than 15 years building what he describes as an ecosystem of luxury businesses, each one feeding the next. His flagship company, MyOcean (my-ocean.com), is a community-driven superyacht platform covering charter, sales and management. YourSky (yoursky.com) extends the model into private aviation, offering jet and helicopter charter alongside bespoke travel itineraries. GP Management handles Formula One hospitality, from yacht parties in Monaco harbour to paddock access and corporate incentive programmes. The Dodgeball Rally, a supercar road trip from Monaco to Croatia running for more than 16 years, draws fleets of Ferraris, Lamborghinis, Bugattis and Koenigseggs on four-day routes each season.

Across these four core brands, and a wider portfolio of eight companies in total, Dodge reports 452,000 Instagram followers, three global offices and a combined monthly social reach exceeding 100 million. His stated approach is asset-light and focused on lifetime client value. As he told SuperYacht Times: “I am used to coming into industries and disrupting them.”

Mother City Capital

Mother City Capital was positioned as the investment layer of this broader ecosystem, described on its own site as wealth management “inspired by African values and global perspectives.” The proposition was straightforward: translate Dodge’s ultra-high-net-worth client base into a capital management product for internationally mobile investors.

What the site now displays is not a company pitch. It is a detailed complaint from a developer identified as rajathuraj, who claims to have built both mothercitycapital.com and a second website, maxhussmann.com, and alleges that $7,000 USD in agreed fees has not been paid. The developer names Bianca Caprozio as the lead contact on the project, and identifies Jonny Dodge and a second individual, Oliver Clarke, as recipients of $10,000 USD in commissions routed through YourSky and a Swiss entity, Cosatravel.

The complaint goes further, alleging that the construction of maxhussmann.com involved identity theft, and stating that the developer intends to report the matter to police unless payment is received. A reference to Caprozio’s association with the United Nations Reham al-Farra Memorial Journalism Fellowship is included in the statement, establishing her public profile as context for the allegations.

The YourSky Connection

The specific mention of YourSky is significant. YourSky is not a peripheral part of Dodge’s portfolio. It is one of his three named flagship companies, prominently featured on his personal website and in his Instagram bio alongside MyOcean and GP Management. The allegation that commission payments were routed through YourSky places the disputed financial flows at the centre of his primary business operations, not at the edges.

Cosatravel, the Swiss entity referenced in the complaint, does not feature in Dodge’s public-facing company listings or in any of his media coverage. Its role, as described in the developer’s statement, appears to be as an intermediary in the commission structure connecting the parties named.

A Pattern Worth Examining

Dodge’s business model, asset-light and built around commissions, referral networks and cross-selling across portfolio companies, creates a structure where financial relationships between entities are not always visible to outside parties. For a network handling significant sums in superyacht bookings, private jet charters and Grand Prix hospitality packages, an unpaid developer invoice of $7,000 is a modest figure. But the specificity of the complaint, naming individuals, amounts, corporate entities and an alleged criminal act, gives it weight beyond its headline number.

The complaint on mothercitycapital.com remains live. Dodge has not issued a public response.

His first investment, it has been noted in interviews, was a nightclub. That unconventional entry point set a tone that has defined his approach across every business since. Whether that same approach now extends to the wealth management arm his network was building is a question that, for the moment, the mothercitycapital.com homepage answers for itself.

Sales agreements will be legally binding sooner and making sellers provide more home information up front are part of the planned changes.

AI narrative continues to dominate IT sentiment

The biggest overhang for IT stocks, according to Sen, is not immediate earnings damage but a persistent narrative shift.

He noted that: “Yes, I mean, IT keeps continuous to get cheaper because the narrative that AI is structurally damage into the sector is just not going away. And the results that come from the companies are not wishing that…, are doing nothing to dispel that fear among investors.”

While acknowledging that fears around artificial intelligence are weighing heavily on valuations, he argued that the extreme pessimism may not be fully justified.

“I do not think that AI is going to wipe out the IT services companies. And to be fair, the Accenture numbers I do not think there is going to be a great deal of consensus earnings downgrades and their cut in guidance is fairly marginal, the midpoint is down just 50 basis points.”

However, he cautioned that sentiment will remain weak in the absence of clearer visibility.

“In the next three to six months, I do not see a clear trigger for a re-rating.” On positioning, he added that he remains tactically cautious:

“We have been slightly underweight on IT… we would stay that because there are no triggers in the next three to six months for the sector to re-rate.”

Long-term opportunity, but short-term pain intact

Despite near-term weakness, Sen highlighted that valuations are beginning to look attractive.

“Most of them are trading at implied growth multiples which are now turning zero to slightly negative and very high free cash flow yields.”

However, he warned investors not to mistake valuation comfort for immediate upside.

“If you are willing to live through short-term pain, then yes, it is a good time to buy… but next three to six months at least there will be pain.”

Monsoon impact: inflation contained, rural stress visible

Turning to macro conditions, Sen addressed concerns around a weaker monsoon and its impact on markets, especially consumption and financials.

He noted that inflation risks are likely to remain contained: “There are enough buffer stocks and… policymakers have managed to keep a lid on inflation. You are not going to see inflation go up to 8%, 9%, 10%.”

However, rural demand remains a key monitorable:

“There will be pockets where you will see demand slowdown, a little bit of a negative surprise on growth in the consumer basket.”

At a broader level, he believes urban consumption and non-agri income will continue to dominate market direction.

Portfolio stance: consumption, industrials and select financials

On positioning, Sen highlighted a preference for growth-oriented domestic themes. “Our key overweights are consumption more on the discretionary side and industrials.”

He also remains constructive on select financial segments:

“Small and midcap financials which have seen wave of FDIs coming in… the valuations are on the right side.” Additionally, he flagged continued interest in internet-led businesses and select cyclical “post-war” trades such as OMCs and cement.

Earnings outlook improving into FY27

On earnings trajectory, Sen remains broadly optimistic, especially for large-cap indices. “We think Nifty earnings is broadly stable.”

He also highlighted improving breadth in corporate growth: “The share of companies which are delivering 25% plus growth goes up from 31% in FY26 to 41% in FY27.”

Flows: FII caution persists, but worst may be behind

On foreign flows, Sen pointed out that while structural concerns remain, the intensity of selling may ease. “I am not sure that flows will come back in a rush at this point in time… But at least the selling will stop.”

Domestic inflows, however, continue to provide strong support.

RBI likely to stay on hold

On monetary policy, Sen expects stability rather than further action from the central bank. “The RBI will stay on an extended pause from here. There is no reason to cut.”

He emphasized that transmission of earlier rate cuts, rather than fresh easing, will be the key theme going forward.

Bottom line

Markets are currently caught between competing forces — a deep valuation reset in IT, a stabilising macro environment, and improving earnings breadth heading into FY27. While near-term volatility remains, especially in export-linked sectors, domestic demand themes and financials continue to anchor broader market expectations.

Stocks to Watch Recap: SpaceX, CME, Intel, BMW

Charlie Sheen ‘Annoyed’ Over Health And Finance Questions

Met Office issues urgent 46-hour extreme heat alert for 51 UK areas – full list

What Paperwork Do You Need to Sell a House in the UK?

-

Business5 days ago

Business5 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World4 days ago

Crypto World4 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World6 days ago

Crypto World6 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech6 days ago

Tech6 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech7 days ago

Tech7 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

NewsBeat7 days ago

NewsBeat7 days agoFBI searches office of Ohio voter registration group

-

Entertainment5 days ago

Entertainment5 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Business5 days ago

Business5 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Tech5 days ago

Tech5 days agoAs AI companies race to go public, who else is along for the ride?

-

Crypto World5 days ago

Crypto World5 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

Politics5 days ago

Politics5 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

NewsBeat5 days ago

NewsBeat5 days agoWarning of disruption as Cardiff Crossrail works to start

-

News Videos5 days ago

News Videos5 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

Entertainment5 days ago

Entertainment5 days agoDeion Sanders Shares Powerful Post After Viral Advice To Deiondra

-

Crypto World5 days ago

Crypto World5 days agoMarket Preview: SpaceX (SPCX) IPO Record, Federal Reserve Meeting, and Iran Nuclear Agreement

-

NewsBeat5 days ago

NewsBeat5 days agowhat doctors are seeing in ebike crashes

-

Entertainment5 days ago

Entertainment5 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Business5 days ago

Business5 days agoInvesco Quality Income Fund Q1 2026 Commentary

You must be logged in to post a comment Login