Business

Exclusive | Can cheap valuations shield IT stocks from AI disruption? S Naren explains

Edited excerpts from a chat on market outlook, sectoral opportunities and whether smallcaps are attractive enough to buy now:

Given that big triggers of the US-India trade deal, Budget and Q3 earnings season is now behind us, how has your outlook towards the Indian equity market changed in the last 2-3 weeks?

Over the last year, valuations across global markets have moved higher, and today there are virtually no cheap markets left. One potential trigger for India to outperform could be a correction in overvalued artificial intelligence related stocks globally. If the excesses in AI-led narratives unwind, Indian equities could relatively outperform.

After the hyper growth seen post-Covid, we appear to be in a moderate to low return environment since the last 1.5 years. How long do you think this consolidation phase can last?

Currently, it is difficult to predict how long a moderate-return phase may last. Such phases typically continue until markets move to either of two extremes, i.e. either become very expensive or become very cheap. At a different point, the market may move into a phase from where we may change our view to high returns or low returns.

You had warned investors against the smallcap mania about a year ago. Those who followed your advice are now happy. There’s hardly any froth in smallcaps now but are the valuations attractive enough to be incrementally positive now?

Small cap investing works in cycles. Currently, there are select small cap stocks that are reasonably valued. Hence, investors who want exposure to small caps can consider starting long term SIP in a small cap fund now, ideally with a five to ten-year horizon.

Your call on multi-asset funds, silver and gold also played out extremely well. Do you think that silver has topped out and gold has more legs?

Silver market is relatively small compared to gold, which makes it prone to speculative excesses. As a result, it is a risky asset class for anyone considering to trade this metal. Gold, on the other hand, has a role to play in asset allocation. But traditional valuation models do not apply to precious metals. Unconventional models like the Nifty-Gold ratio do not suggest a large long term allocation to gold at present. However, in the near term, gold may continue to benefit from momentum, but we do not have a clear view on the near term outlook for gold.

You have been a big advocate of asset allocation. Retail investors were earlier chasing smallcaps at any price and now it is about gold and silver. AMFI data on heavy inflows in gold and silver ETFs also shows this. For someone with a moderate risk appetite and a long-term horizon of at least 5 years, how much allocation would you recommend in gold, equity and debt?

There are no one size fits all allocation. It depends on an investor’s age, goals, and risk tolerance. It is best to consult a financial advisor who can guide on the allocation proportion. From an asset class perspective, currently, no asset class appears to be cheap and that includes even international equities. Therefore, investors should broadly stick to their long-term asset allocation frameworks instead of considering any tactical shifts.

Any contra bet that you think can surprise on the upside in the next couple of years?

If artificial intelligence does not impair the growth prospects of Indian IT services companies but instead enhances them, the sector could see a strong rally. However, at this stage, the long-term impact of AI on Indian IT services remains unclear.

Indian IT stocks have been under selling pressure as investors see AI as a threat rather than an opportunity. What are your thoughts on the IT pack and how are you dealing with the sell-off?

The sector is in a flux along with heightened fear. If the growth risks do not materialise, there is scope for meaningful returns. However, clarity on long-term growth is essential before becoming decisively positive.

Do you think that relatively cheaper valuations and high dividend yield can protect the downside in IT stocks?

In a sector which is facing disruption, cheap valuation alone will not suffice. What matters most is the confidence that disruption will not permanently impair industry growth. Without that clarity, cheap valuations may not mean much.

ICICI Prudential AMC has launched two SIFs – iSIF Equity Ex-Top 100 Long-Short Fund and iSIF Hybrid Long-Short Fund. How should an investor decide which one suits her requirements?

Investors with a belief that long-term investment in a defensive manner in small and midcaps is an attractive investment proposition, can consider the Equity Ex-Top 100 Long-Short fund. Meanwhile, the Hybrid Long-Shot Fund is designed for investors seeking a more balanced approach. In both cases, investors should invest if they believe in our current view of a moderate-return environment in the near term.

Consumption was touted as a big theme after GST cuts were introduced before Diwali. Since then auto appears to be the biggest winner in the consumption cycle. Do you think durables and other consumption plays are up for an upcycle in FY27?

Many non-auto consumption sectors have been underperforming for several years, which has created some margin of safety. However, despite this underperformance, valuations are not very cheap, even though they have come off their peaks.

Which other sectors are you bullish on for the next 2-3 years?

There are no cheap sectors in the market today. Opportunities are more likely to arise from investor impatience i.e. when stocks are sold due to short-term disappointment. Such phases often create attractive entry points for long-term investors.

How should an investor go about with fresh equity investments?

Our primary framework for investing is asset allocation based approach with a higher equity tilt than a year ago. Within equities, large caps appear to be relatively better placed on valuation basis. Investors can also consider equity strategies with flexibility to move across sectors and market capitalisations.

Business

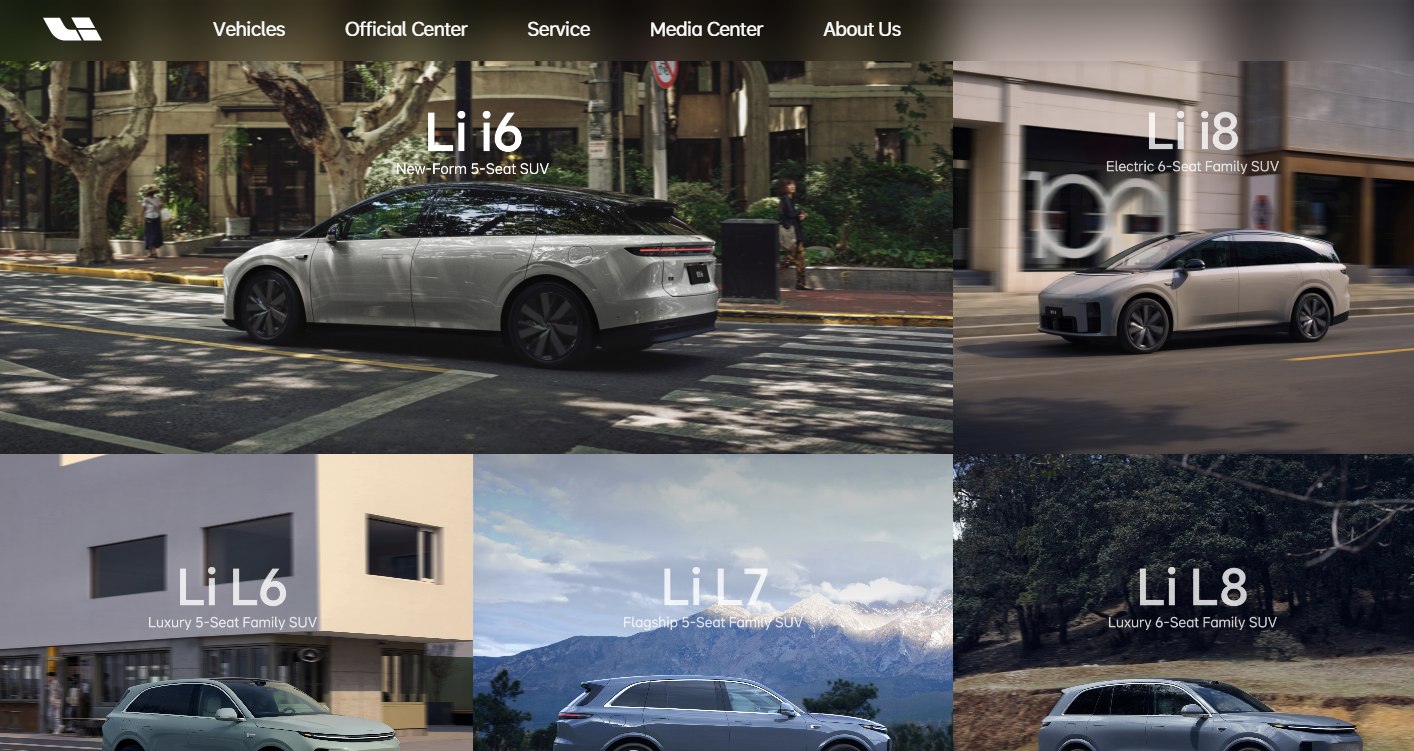

Li Auto Stock Rises 3% in Hong Kong as March Deliveries Rebound and New L9 Launch Looms in China EV Recovery

HONG KONG — Li Auto Inc. shares climbed more than 3% Friday on the Hong Kong Stock Exchange, closing at HK$74.20 after adding HK$2.30, as investors cheered a strong March delivery rebound and anticipation for the upcoming launch of the refreshed flagship Li L9 amid a competitive but recovering Chinese new energy vehicle market.

The Beijing-based automaker, listed as HKG:2015, saw its stock rise on elevated trading volume as the company resolved production bottlenecks for its battery electric vehicle lineup and pushed forward with technology upgrades, including advanced autonomous driving systems unveiled at NVIDIA’s GTC 2026 conference. The move extended recent gains following positive March figures that helped lift first-quarter deliveries above internal guidance.

Li Auto delivered 41,053 vehicles in March 2026, marking a 12% increase from the same month a year earlier and a sharp sequential jump after earlier softness. The performance pushed the company’s cumulative deliveries past 1.635 million vehicles since inception. Notably, the Li i6 pure electric SUV surpassed 24,000 monthly units once production constraints eased, signaling improving momentum in Li Auto’s BEV transition.

For the first quarter overall, Li Auto delivered approximately 95,142 vehicles, a modest 2.5% year-over-year gain that exceeded its earlier guidance range of 85,000 to 90,000 units. The rebound came despite ongoing price competition and a challenging 2025, when full-year deliveries fell about 19% to roughly 406,343 vehicles amid margin pressure and slower demand for some extended-range electric vehicle models.

The company has set an ambitious target for 2026, aiming for around 20% growth in vehicle sales, which would translate to roughly 490,000 units. Management has emphasized a “3+2” strategy focusing on overhauling its retail network, successfully launching the next-generation Li L9, and accelerating battery electric vehicle sales. The all-new Li L9, scheduled for official launch in the second quarter, is expected to feature significant upgrades including a larger battery for over 400 km of pure electric range, an enhanced chassis, and cutting-edge computing power.

Analysts and investors view the refreshed L9 as a potential catalyst. The model is projected to incorporate Li Auto’s self-developed M100 chip and advanced smart cockpit features, with some variants boasting up to 2,560 TOPS of computing power — far exceeding many competitors. A higher-priced “Livis” trim has also been previewed, targeting premium family buyers seeking luxury and intelligent driving capabilities. Orders for certain current L-series models were paused in March ahead of the refresh, a common industry tactic to clear inventory and build excitement for new versions.

Li Auto has also been investing heavily in artificial intelligence and autonomous driving technology. The company unveiled its MindVLA autonomous driving foundation model at NVIDIA GTC 2026, pairing hardware advances with in-house software to differentiate its vehicles in a crowded market. These efforts align with broader industry shifts toward AI-native vehicles, where Li Auto aims to blend extended-range reliability with pure electric innovation and intelligent features.

On the financial front, Li Auto reported a challenging 2025, with revenue declining about 22% and net income dropping sharply. Fourth-quarter vehicle margins improved sequentially to 16.8%, though still below prior peaks due to pricing competition. The company returned to modest profitability in the quarter despite lower volumes. For the first quarter of 2026, it had guided revenue between RMB 20.4 billion and RMB 21.6 billion, reflecting the impact of softer early-year deliveries before the March uptick.

To signal confidence, Li Auto announced a US$1.0 billion share repurchase program in March 2026, with initial buybacks executed on both Nasdaq and Hong Kong exchanges. Executives described the move as reflecting strong belief in the company’s long-term value creation. The program comes alongside ongoing efforts to optimize its sales network through a “store partner” profit-sharing model aimed at boosting retail performance.

Li Auto’s portfolio spans extended-range electric vehicles (EREVs) like the popular L6, L7, L8 and L9 families, alongside pure EVs including the Li i6, Li i8 and the flagship Li MEGA MPV. The company has positioned itself as a leader in premium smart EVs tailored for families, emphasizing spacious interiors, advanced safety systems and convenient energy solutions. Its nationwide supercharging network exceeded 4,000 stations by early 2026, supporting over 1.45 million charging sessions during the Spring Festival travel peak alone.

Despite domestic headwinds, Li Auto has begun modest international expansion, introducing select L-series models in markets such as Egypt, Kazakhstan and Azerbaijan. While China remains the core focus, these early steps signal ambitions to diversify beyond the world’s largest EV market.

The Chinese EV sector continues to face intense competition from rivals including BYD, NIO and XPeng, compounded by price wars and fluctuating consumer demand. Li Auto’s hybrid approach — combining range-extended powertrains with growing BEV offerings — has helped it maintain appeal among buyers concerned about charging infrastructure. However, gross margins have faced pressure from higher raw material costs and promotional pricing.

Analysts remain mixed but generally constructive on longer-term prospects. Consensus price targets cluster around levels implying upside from current valuations, with some highlighting the potential for margin recovery as new products ramp up. Morgan Stanley recently trimmed its target but maintained an overweight rating, citing execution risks around the L9 launch while noting expected benefits from AI investments and product cycle improvements. The stock trades at a relatively low multiple compared to some growth peers, though volatility persists amid broader China EV sentiment.

Li Auto also released its 2025 ESG Report and inaugural climate-related disclosures on April 10, underscoring commitments to sustainable manufacturing and supply chain practices as it scales production. The company operates with a vertically integrated model focused on user value, from vehicle design to software updates delivered via over-the-air (OTA) technology. Recent OTA version 8.3 brought enhancements to its VLA driver model, smart cockpit and electric functionality.

Looking ahead, attention will turn to the May earnings report, where management is expected to provide more color on Q2 guidance, L9 production ramps and BEV contribution. The company plans to launch an all-new Li i9 battery electric SUV in the second half of 2026, further broadening its pure EV lineup.

Challenges remain, including sustaining delivery growth in a high-competition environment, managing R&D expenses that have risen with AI and autonomy pushes, and navigating potential regulatory or subsidy shifts in China’s NEV sector. Supply chain stability and raw material costs will also influence margins.

Friday’s trading in Hong Kong showed strong participation as the stock tested recent resistance levels following the March delivery news. Technical observers noted improving momentum, though the shares remain well below 2025 peaks amid last year’s delivery slowdown.

Founded in 2015, Li Auto has grown rapidly by targeting the premium family segment with vehicles that combine the convenience of gasoline range with electric efficiency and smart features. Under CEO Xiang Li, the company has prioritized user experience, with high net promoter scores for models like the Li i8.

As China’s EV market matures and global interest in intelligent vehicles grows, Li Auto’s blend of hardware innovation, software differentiation and family-focused design positions it as a resilient player. Success with the new L9 and continued BEV momentum could help the company reclaim stronger growth trajectory in 2026 and beyond.

Investors will closely monitor execution in the coming quarters, particularly whether the refreshed lineup can drive order backlogs, stabilize pricing and deliver on margin targets. For now, the March rebound and technology roadmap have provided fresh optimism in a sector where product cycles and innovation often dictate market leadership.

Aehr test systems director Posedel sells $2.1m in stock

Peter Moore has called on the governing body to “sort out” their structures ahead of the summer spectacular

Former Liverpool CEO Peter Moore has expressed his disappointment with FIFA’s current ticketing strategy for the 2026 World Cup. Moore is far from the first in the space to voice concerns, as watching football in person becomes increasingly difficult for the average fan.

Moore, who served as Liverpool’s CEO from 2017 to 2020, has called on FIFA to reconsider its ticketing approach, stating that it is “completely detached from the very soul of football.”

Moore has urged FIFA to “sort out” its ticketing strategy before it’s too late. He expressed concern that the current model prioritises revenue over the reality of the average, passionate football supporter. These are the fans who save for years to attend the World Cup, travelling across continents and bringing the spirit, colour, and noise to the games.

Moore, who has attended five World Cups, described them as “life chapters” about culture, connection, and unity through football. He emphasised that the issue of ticket pricing carries significant weight given his extensive experience in the sports and entertainment industries.

During his career, Moore has held senior roles at Reebok, Sega, Microsoft, and Electronic Arts (EA). He recalled standing “shoulder to shoulder” with FIFA during its 2015 controversy when senior officials were charged with bribery, racketeering, and money laundering. Despite many sponsors distancing themselves from FIFA, EA continued to work with them, keeping millions of fans connected to football and the World Cup during a time of low trust in the organisation.

The controversy of dynamic pricing

FIFA’s ticket pricing for the upcoming World Cup has already sparked controversy. The Football Supporters’ Association (FSA) has criticised the ticket pricing policy as excessively expensive and unfair to fans. The introduction of dynamic pricing, a model that the FSA has urged FIFA to abandon, is one of the main reasons behind the increase.

A recent investigation revealed the high costs fans would face, including flights, tickets, and accommodation, to attend the World Cup. Moore echoed the FSA’s sentiments, stating that the current approach feels detached from the essence of football. He argued that football should not be a luxury product reserved for the highest bidder, but rather, it belongs to the people.

The future of FIFA ticket pricing strategy

While public criticism may not be enough to force FIFA to reconsider its pricing model, the results it produces might. FIFA claimed in January to have received half a billion ticket requests for the World Cup.

If a large proportion of tickets are held outside genuine fan demand, there is a risk that stadiums may not be full for many matches. This could pose a significant issue for FIFA, even if revenues reach record levels, especially given its ambition to deliver the biggest and best World Cup in history.

Moore concluded by saying, “The World Cup should unite the world, not divide it by price. Football deserves better. And so do the fans. Come on, FIFA, sort this out… It’s not too late.”

Are The Semis And Transports Leading The Market To New Highs?

Markets Weekly Outlook: Markets Brace For U.S.-Iran Talks Amid Post-Ceasefire Surge

Naixi Wu, Indie Semiconductor CFO, sells $154,560 in INDI stock

Headline Inflation Surged In March, But Core Remained Muted

Business

Texas Pacific Land Stock Surges 10% as Permian Royalty Giant Rebounds on AI Data Center Hopes and Water Growth

NEW YORK — Texas Pacific Land Corp. shares jumped more than 10% in morning trading Friday, climbing to $417.06 as investors appeared to shake off recent volatility tied to the passing of a major shareholder and renewed optimism around the company’s diversification into AI infrastructure and data centers on its vast West Texas holdings.

The Dallas-based land and royalty company, listed on the NYSE as TPL, added $39.16, or 10.36%, by 11:12 a.m. EDT. The sharp rebound followed a steep sell-off earlier in the week after the announcement of the death of Murray Stahl, founder of Horizon Kinetics Asset Management, TPL’s largest shareholder. Shares had plunged as much as 15-17% on Thursday amid the news and broader energy sector weakness linked to easing Middle East tensions.

Texas Pacific Land owns roughly 900,000 acres in the Permian Basin, generating revenue primarily through oil and gas royalties, produced water royalties, and water sales to drilling operators. The business model is asset-light with exceptionally high margins — often exceeding 60% net — because the company collects royalties without bearing drilling or operating costs.

In its fourth-quarter and full-year 2025 results released in February, TPL reported record performance. Full-year revenue reached $798.2 million, net income hit $481.4 million or $6.97 per diluted share, and free cash flow stood at $498.3 million. Oil and gas royalty production averaged 34.6 thousand barrels of oil equivalent per day for the year, rising to a quarterly record of 37.5 thousand Boe/d in the fourth quarter. Water sales revenue climbed to $169.7 million annually, with Q4 alone delivering $60.7 million on 1.0 million barrels per day of volumes.

The company also raised its regular quarterly dividend by 12.5% to $0.60 per share and entered a new $500 million revolving credit facility while completing a three-for-one stock split in late 2025. Adjusted EBITDA for 2025 reached $687.4 million.

Analysts have grown increasingly bullish on TPL’s non-traditional growth avenues. In February, KeyBanc raised its price target sharply to $639 from $350 while maintaining an Overweight rating, citing opportunities in power generation, data centers and strong water segment trends. Other targets range widely, with consensus around $487 and some lower figures near $390, reflecting debate over valuation amid high multiples.

A key catalyst has been TPL’s strategic pivot toward AI and digital infrastructure. In December 2025, the company invested $50 million in Bolt Data & Energy, a platform chaired by former Google CEO Eric Schmidt. The partnership aims to develop large-scale “Closed Loop Energy Data Hubs” on TPL land, leveraging the company’s natural gas resources for power generation and treated water for cooling. TPL holds equity stakes, warrants and rights of first refusal for land and water supply to these projects.

Management has highlighted ambitions for gigawatt-scale data center development, potentially transforming surface acreage into high-value AI infrastructure. Reports of potential involvement from major tech players, including Google, have fueled investor excitement even as traditional energy exposure remains core.

Water services continue to provide a resilient revenue stream less directly tied to oil prices. Produced water royalties and sales volumes set records in 2025, benefiting from higher drilling activity in the Permian. TPL has also explored desalination opportunities to expand its water portfolio sustainably.

Despite the positive long-term narrative, the stock has experienced significant swings. It surged over 50% year-to-date through early 2026 on royalty strength and data center buzz but pulled back sharply in recent sessions. Thursday’s drop followed Stahl’s passing; Horizon Kinetics holds millions of shares, and the activist-leaning investor had played a key role in modernizing TPL’s governance and strategy in prior years. Horizon continued buying shares even after the news, purchasing additional units on April 8.

The company remains debt-light with substantial cash and liquidity. Its fortress balance sheet allows opportunistic investments and resilience during commodity downturns, a point emphasized by CEO Ty Glover on recent earnings calls.

TPL’s land position gives it unique leverage in the Permian, one of the world’s most productive oil basins. Operators drilling on or near its acreage pay royalties on production, while surface rights enable additional income from easements, water and now potential tech infrastructure. This diversified model has helped TPL outperform traditional energy plays during periods of price volatility.

Challenges persist. Revenue remains sensitive to drilling activity, rig counts and commodity prices, even with royalty structures providing downside protection. Some analysts caution that elevated valuations assume continued robust operator spending and successful execution on new initiatives like data centers, which remain in early stages. Recent operator capital discipline and fluctuating rig counts have raised questions about near-term growth sustainability.

Broader market context includes recovering oil prices after a brief dip tied to Middle East developments, though energy stocks overall showed mixed performance Friday. TPL’s outsized move suggests company-specific catalysts — particularly AI-related speculation — are driving the rebound.

Upcoming events include a shareholder office and field visit in Midland on May 18, 2026, with an RSVP deadline already passed. The gathering offers investors a closer look at operations, water assets and potential development sites.

Founded originally in the 19th century and restructured as a modern corporation, Texas Pacific Land has evolved from a legacy land trust into a high-margin royalty and resource play. It maintains a lean structure with minimal overhead, allowing most incremental revenue to flow to the bottom line.

Insider and institutional interest remains notable. Major holders like Horizon Kinetics have demonstrated ongoing confidence through purchases, while short interest hovers around 6% of float. The stock’s beta near 1.0 indicates it moves with the broader market but amplifies energy and growth themes.

Technical analysts noted Friday’s surge broke short-term resistance after the recent pullback, with elevated volume signaling renewed buying interest. Longer-term charts show the shares well above 2025 lows despite volatility.

As TPL prepares Q1 2026 results in coming weeks, focus will center on royalty production trends, water volumes, progress with Bolt Data & Energy and any updates on surface development. Guidance or commentary on 2026 outlook could further influence sentiment.

The company’s story blends old-economy energy royalties with forward-looking bets on AI power and data infrastructure needs. In an era of surging electricity demand from data centers and hyperscalers, TPL’s land, water and energy resources position it uniquely at the intersection of traditional resources and next-generation technology.

While risks around execution, commodity cycles and high valuations remain, Friday’s rally underscores investor willingness to price in diversification potential. With Permian activity resilient and new revenue streams emerging, Texas Pacific Land continues to attract attention as both a defensive royalty play and a speculative growth name in the evolving energy-AI landscape.

It's The Economy…

Songkran, Thailand’s iconic water festival, fosters family unity and joy. Celebrated in April, it offers meaningful connections, creating lasting memories across generations through shared experiences and cultural traditions.

Songkran: A Festival of Family Unity

Songkran is deeply rooted in family traditions, serving as a vibrant celebration of joy and connection. This iconic water festival, celebrated in Thailand every April, transforms cities into living classrooms of shared experiences and lasting memories. Beyond the water fights, Songkran fosters a deeper sense of togetherness among families, strengthening bonds across generations.

Celebrating in the Heart of Thailand

In Bangkok, Songkran offers family-friendly experiences at locations like centralwOrld and Siam Square, blending tradition with safety. While Khao San Road is energetic, families can find designated splash zones that prioritize safety with crowd control and shaded areas. These spaces provide peace of mind for parents, allowing everyone to fully enjoy the festivities.

Embrace Diversity in Celebrating Songkran

Exploring beyond the capital, Chiang Mai offers spiritual experiences with ceremonies at ancient temples, promoting family teamwork and unity. In Pattaya, the lively Wan Lai festival showcases water-themed activities perfect for families seeking fun in the sun. Ayutthaya’s ancient ruins offer a unique cultural backdrop, transforming Songkran into a celebration of renewal, unity, and shared family joy.

Source : Splashing Through the Generations – TAT Newsroom

Other People are Reading

France orders all government ministries to ditch Windows for Linux in digital sovereignty push

Nintendo GameCube is my favourite console even though I know it’s not the best – Reader’s Feature

Li Auto Stock Rises 3% in Hong Kong as March Deliveries Rebound and New L9 Launch Looms in China EV Recovery

-

Business5 days ago

Business5 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports6 days ago

Sports6 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Politics7 hours ago

Politics7 hours agoUS brings back mandatory military draft registration

-

Fashion8 hours ago

Fashion8 hours agoWeekend Open Thread: Veronica Beard

-

Business7 days ago

Business7 days agoExpert Picks for Every Need

-

Tech3 days ago

Tech3 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business6 days ago

Business6 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion5 days ago

Fashion5 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Sports8 hours ago

Sports8 hours agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Fashion3 days ago

Fashion3 days agoLet’s Discuss: DEI in 2026

-

Crypto World2 days ago

Crypto World2 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business5 hours ago

Business5 hours agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Crypto World2 days ago

Crypto World2 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business6 days ago

Business6 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Business14 hours ago

Business14 hours agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Politics7 days ago

Politics7 days agoThe UK should not pay a penny in slavery reparations

-

Tech5 days ago

Tech5 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech5 days ago

Tech5 days agoSamsung just gave up on its own Messages app

-

Tech5 days ago

Tech5 days agoItalian court says Netflix must refund customers up to $576 over price hikes

-

Tech5 days ago

Tech5 days agoHaier is betting big that your next TV purchase will be one of these

You must be logged in to post a comment Login