Heightened geopolitical tensions, rising

crude prices, and uncertainty around the

interest rate cycle are reshaping the investment landscape, prompting a renewed focus on stability within portfolios.

In an interaction with Kshitij Anand of ETMarkets, Devang Shah, Head – Fixed Income at Axis Mutual Fund, said that the current environment strengthens the case for fixed income as a core allocation.

With the rate cut cycle nearing its end and volatility expected to persist, he advises investors to stay cautious on duration and prefer high-quality, short-term debt strategies that can offer steady accrual and resilience amid evolving macro risks. Edited Excerpts –

Kshitij Anand: With global markets facing heightened geopolitical tensions—from ongoing conflicts to trade uncertainties—how are these risks reshaping investors’ interest in fixed income assets at this point in time?

Indian Bank to launch over $500 million infrastructure debt issue next week, MD says

Indian Bank is raising 50 billion rupees through seven-year infrastructure bonds next week. This move aims to fund stronger credit growth and capital requirements. The bank is seeking longer-term funding as deposit rates have increased. Discussions with investors like the Employee Provident Fund Organisation are underway. This issuance marks the bank’s return to the bond market after over 17 months.

Devang Shah: As you rightly highlighted, first of all, it is important from every investor’s perspective to always have asset allocation. What I mean by disciplined asset allocation is that you should not put all your money into one asset class.

We have done some studies—this is also part of our multi-asset allocation theme—where we analyse the top six or seven asset classes that investors typically consider, such as precious metals, bonds, equities, global assets, and offshore assets. Specifically, if you look at offshore assets like US and China markets, and analyse how these assets have performed over different periods, our 20-year study clearly shows that there is no single winner. No one asset class consistently outperforms others or delivers superior returns at all times.

So, asset allocation becomes an even more important theme going forward. Fixed income plays a crucial role in this because it provides stability. Historically, except for periods like 2008, 2013, and parts of 2018, fixed income has generally not delivered negative returns. So, it also offers a degree of capital protection.

In today’s environment, investors should definitely have some allocation towards fixed income. The exact allocation depends on several factors, such as the macroeconomic outlook, central bank actions, inflation, growth, the rate cycle, and liquidity. These are important levers to consider while deciding the allocation to fixed income.Given the current environment—with heightened volatility driven by geopolitical uncertainties and rising crude prices—there is certainly a strong case for bonds.

Kshitij Anand: For much of the last year, markets have been pricing in rate cuts from major central banks. But what if the rate cut cycle gets delayed or does not materialise as expected? How should investors rethink their fixed income allocation in such scenarios?

Devang Shah: You are right—the last two years have been very positive for bond markets. Across developed markets and in India, central banks have cut rates, leading to a strong rate-cut cycle globally.

However, since June, we at Axis have been communicating that we are nearing the end of this rate cycle. Going forward, other levers will drive returns in fixed income. We believe that we are close to the end of the rate cycle and do not expect significant rate cuts ahead.

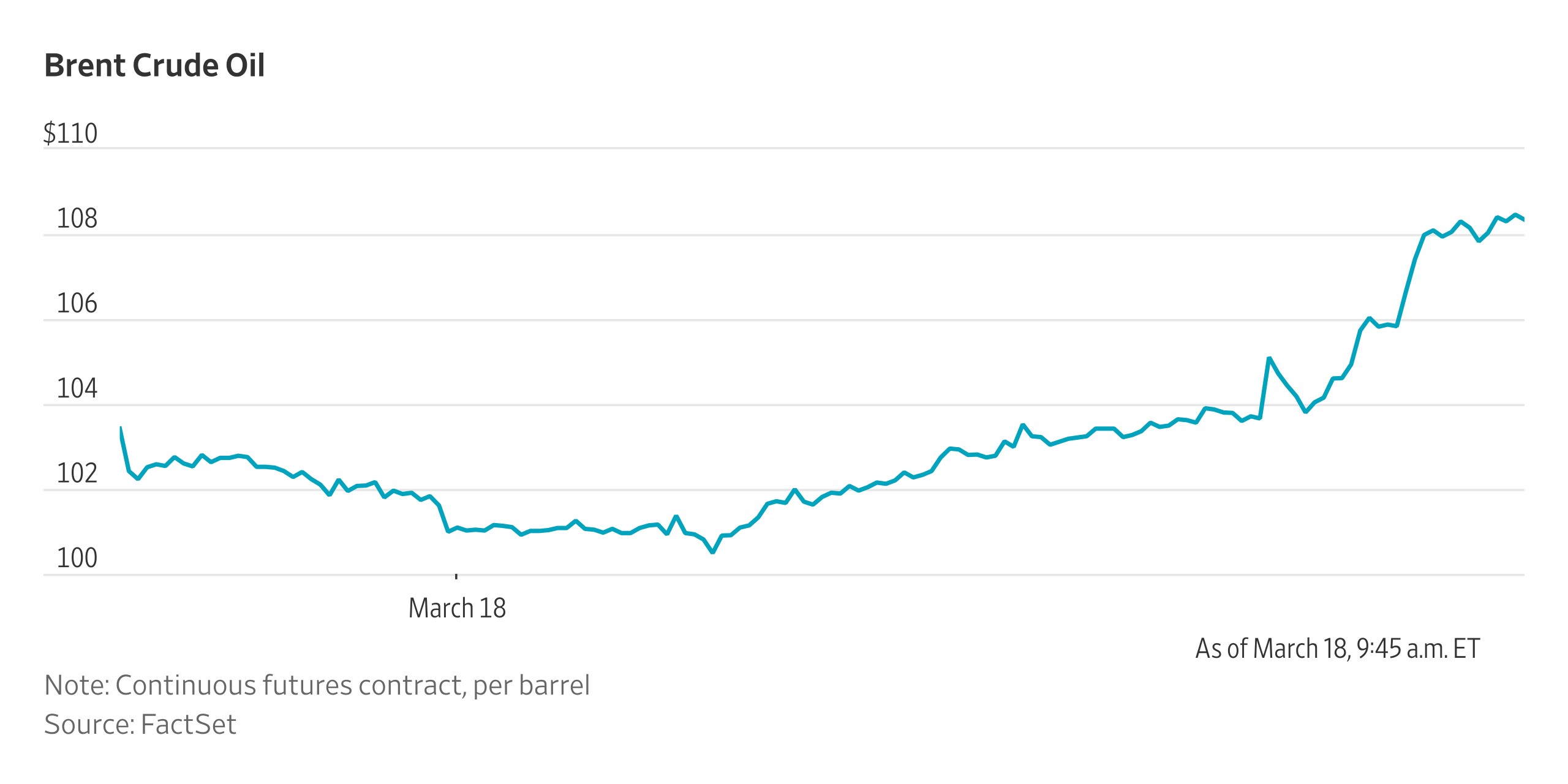

Now, with the current geopolitical tensions and the sharp rise in crude prices, we need to look at two key aspects: how long this situation will last, and where crude prices will stabilise in the near and medium term.

Our assessment is that while no one can predict geopolitical developments with certainty, markets will eventually realign to a new crude price range across inflation, growth, corporate earnings, and fiscal deficits.

We believe that if crude prices remain in the $75–$85 range, the impact on the Indian economy will be present but muted. It will not significantly deteriorate macroeconomic conditions or force the RBI to hike rates immediately.

However, there could be some impact: inflation may rise by about 0.5%, moving from around 4.5% towards 5%. Growth could slow slightly from the expected 7%+, and the current account deficit may widen from around 1% to 1.5–1.75%.

This means that while macro fundamentals may weaken slightly, they will remain broadly stable. In such a scenario, the RBI is likely to stay supportive of growth by ensuring adequate liquidity. While inflation is a near-term concern, the bigger medium-term risk is slowing growth if crude prices remain elevated.

Therefore, we do not expect significant stress on bonds. Bond yields have already adjusted—especially at the short end of the curve, which has seen a sell-off of about 30–50 basis points. The OIS has also risen by around 30 basis points.

If crude prices stabilise within the $75–$85 range, we do not expect much further impact. However, if crude prices rise above $100—which we consider a lower probability but still a risk—it could trigger a faster rate hike cycle, pushing bond yields higher across the curve.

In such a scenario, it would make sense for investors to stay positioned at the short end of the yield curve.

Kshitij Anand: Now, in a world where equities can deliver strong wealth creation but also sharp volatility, how can bonds help investors balance growth, income stability, and capital preservation within a portfolio?

Devang Shah: As you rightly highlighted, today is a world of uncertainty, and this uncertainty will continue to prevail. That is why asset allocation becomes more and more important.

In today’s market environment, where a large part of the rate cycle is over and we are at a stage where the next move could be rate hikes—whether in six or twelve months—the key question is how to navigate this environment without experiencing significant volatility in your debt portfolio.

So, what should an investor do? That is the most important question. My understanding is that, as I mentioned earlier, the extreme short end of the curve—up to the one- to three-year segment—has seen a significant sell-off over the last six to nine months.

Let me share some numbers. One-year CDs were trading at 6.25–6.30% levels in June 2025. Today, despite rate cuts over the past nine months, they are trading in the 7–7.25% range. That implies a sell-off of about 50 to 75 basis points. This is largely due to strong credit growth and some degree of currency intervention, which led to temporary liquidity tightness.

Similarly, three-year corporate bonds, which were trading at around 6.5%, are now closer to 7.25–7.30%.

So, our perspective is that the segment which has already seen a significant sell-off—and is unlikely to react sharply even if the RBI starts raising rates—is where investors should focus for the near term, say over the next 12 to 18 months.

At yields of 7–7.25%, money market strategies and conservative short-term funds make a lot of sense for investors to navigate this uncertain environment, which is influenced by crude price volatility, policy uncertainty, and macroeconomic risks if crude sustains above $100.

Kshitij Anand: Also, as we are nearing the end of the financial year, can you sum up how FY26 was for bond markets in general?

Devang Shah: FY26 has been a volatile year. It started with significant policy easing, liquidity support, and rate cuts until June. As I mentioned earlier, there was a 50-basis-point rate cut in June.

So, the year began on a strong positive note for bonds, but some of those gains were later given up. If you look at 12–18 month returns, they are still quite healthy. At one point, bond markets were delivering close to double-digit returns—in June 2025, most debt funds, whether short-term, medium-term, long-duration, or gilt funds, were delivering double-digit returns.

However, a part of these gains has been eroded due to global uncertainties, rising crude prices, a large supply of state development loans, and strong credit growth, which signaled that we were nearing the end of the rate cycle.

Overall, FY26 has been a mixed bag for bond markets. The extreme short end has performed very well. Short- to medium-term funds have delivered reasonable returns, while long-duration bonds have remained volatile.

Kshitij Anand: As the financial year draws to a close, how should investors review their portfolios? Are there any specific adjustments they should consider in fixed income allocation before the new financial year begins?

Devang Shah: Our assessment is based on the assumption that over the next two to three months, conditions will stabilise, and crude prices are unlikely to remain above $100 for an extended period.

Under this base case, we have been advising investors to reduce duration in their fixed income portfolios and focus on the short end of the curve.

Specifically, money market funds, conservative short-term funds, and a relatively new category—income plus arbitrage fund of funds—are attractive options. These funds, with a two-year investment horizon, can deliver debt-like returns with equity-like taxation.

Even in a less likely scenario—say a 20% probability—where crude remains above $100 and causes significant stress on growth, investors should still remain invested in the short end of the curve in the near term. This is because the first reaction would likely be a shift in central bank policy towards rate hikes.

Once that scenario materialises, opportunities may emerge in the second half of the year to allocate to longer-duration funds.

For now, the key portfolio adjustment should be to reduce duration, focus on money market strategies, conservative short-term funds, and income plus arbitrage fund of funds. However, for income plus arbitrage funds, investors should maintain at least a two-year investment horizon to fully benefit from tax efficiency.

Going forward, depending on the macro environment, there could be tactical opportunities in long-duration bonds.

Kshitij Anand: So, what should investors keep in mind while building a fixed income strategy for the next financial year amid global uncertainty and evolving interest rate expectations?

Devang Shah: The general fear, whenever such uncertainties rise, is that investors tend to move towards highly liquid funds. They prefer instruments that offer high liquidity and are relatively immune to risks such as duration volatility and potential growth slowdowns.

Our perspective at this point is that if you want to navigate this environment effectively, you should stay invested in funds that predominantly hold AAA-rated credits, have a strong quality bias, and avoid taking excessive duration exposure, as duration can introduce volatility.

If growth weakens, then with a lag, the credit cycle may start deteriorating. While this is not our base case, investors who want to adopt a more conservative approach should continue allocating to money market funds, low-duration strategies, and ultra-conservative short-term bond funds, with a strong emphasis on high-quality AAA issuers.

That said, the credit cycle today remains strong. I do not see any immediate concerns. India’s macroeconomic story has not weakened significantly, and the credit environment continues to be healthy. If you look at bank and NBFC NPAs, leverage levels, and profitability, there has been no meaningful deterioration.

However, as a cautionary note, if crude prices continue to hover around $100 or higher, it could slow down India’s growth and create future concerns. To navigate such a scenario, it is better to stay invested in money market strategies with a higher quality bias.

Kshitij Anand: What factors are accelerating retail participation in India’s traditionally institutional bond markets, and what more needs to be done to deepen this ecosystem?

Devang Shah: To begin with, regulators have done a commendable job. Today, retail investors have access to government bonds through dedicated platforms, which was not the case earlier. Regulators have also simplified many aspects to help investors better understand the products they are investing in.

Mutual funds have also played a significant role. Today, there is a fund for every investor need. If you want to invest for one day, there are overnight funds. For three months, there are liquid funds. For longer horizons, there are target maturity funds, index funds, or long-duration funds.

SEBI and RBI have done a great job in promoting investor education. Tools such as riskometers and portfolio disclosure matrices help investors understand the risk profile and credit quality of their investments, including exposure to non-AAA assets.

A lot of improvements have been made since the 2018 credit crisis. Today, mutual fund products are much easier for retail investors to understand.

Innovations such as direct participation in government bonds and ensuring liquidity through mutual fund structures are important steps towards deepening the corporate bond market. These developments will support increased retail participation in fixed income over the medium term.

Kshitij Anand: Lastly, Indian government bonds have started getting included in major global indices. How could this influence foreign capital flows, yields, and investor interest in the Indian bond market?

Devang Shah: In my view, the increasing depth of the Indian bond market—reflected in volumes, bid-ask spreads, and overall size—has made it more attractive to global investors.

We have already seen initial steps with JPMorgan including Indian bonds in its indices, followed by partial inclusion in certain Bloomberg emerging market indices. There is also a strong possibility that Indian bonds could be included in the Bloomberg Global Aggregate Index, which tracks a $2.5–2.8 trillion market.

If that happens, India could see an allocation of close to 1%, potentially bringing in $20–25 billion of inflows. We believe this could happen within the next 12 months, possibly as early as the June review.

Such inclusion could create tactical opportunities in long-duration bonds, as inflows may lead to a rally in that segment depending on prevailing yield levels.

However, in the current environment, investors should maintain a higher allocation to the short end of the curve due to uncertainties around crude prices, geopolitical risks, and the fact that the rate cut cycle is largely behind us.

In a stable or rising rate environment, focusing on accrual or carry strategies through short-duration funds is a prudent approach.

That said, global index inclusion is a significant positive. As India’s bond market continues to grow in depth and scale, more such opportunities are likely to emerge, creating additional avenues for investors over time.

(Disclaimer: Recommendations, suggestions, views, and opinions given by experts are their own. These do not represent the views of the Economic Times)

You must be logged in to post a comment Login