Business

Meta: I’m Waiting For $500 Per Share To Buy More (NASDAQ:META)

Passionate about geopolitics and macroeconomics, I express my opinion through my articles and enjoy engaging with all of you. I also write about companies that catch my attention, particularly those in my portfolio. For me, Seeking Alpha is a way to expand and share my knowledge. Graduate in business economics, CFA Level 1 and popular investor on eToro.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of GOOG, META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Americans are increasingly turning to TikTok Shop to buy shampoo, jewelry and apparel. Retailers have noticed, pushing onto the platform with their own virtual stores.

Ralph Lauren and Olaplex Holdings moved onto the platform late last year, while Ulta Beauty launched its store in March. They follow early adopters like Crocs, Revolve Group and L’Oréal in the race to capture scrolling shoppers. “You want to be where the consumer is, and increasingly, that’s obviously on social media and online,” said Olivia Tong, a managing director at Raymond James.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

An award winning Perth-developed device to treat chronic ear infections in children has received FDA approval, clearing the way for its launch in the United States.

Gold is back in the geopolitical crosshairs, caught between safe-haven demand and prospects of higher interest rates for longer.

Persistent geopolitical uncertainty is expected to drive investment demand and central-bank buying this year, according to the World Gold Council. Yet, the same forces are pushing oil prices higher, stoking inflation and reinforcing expectations of elevated interest rates—traditionally a headwind for non-interest-bearing assets like gold.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

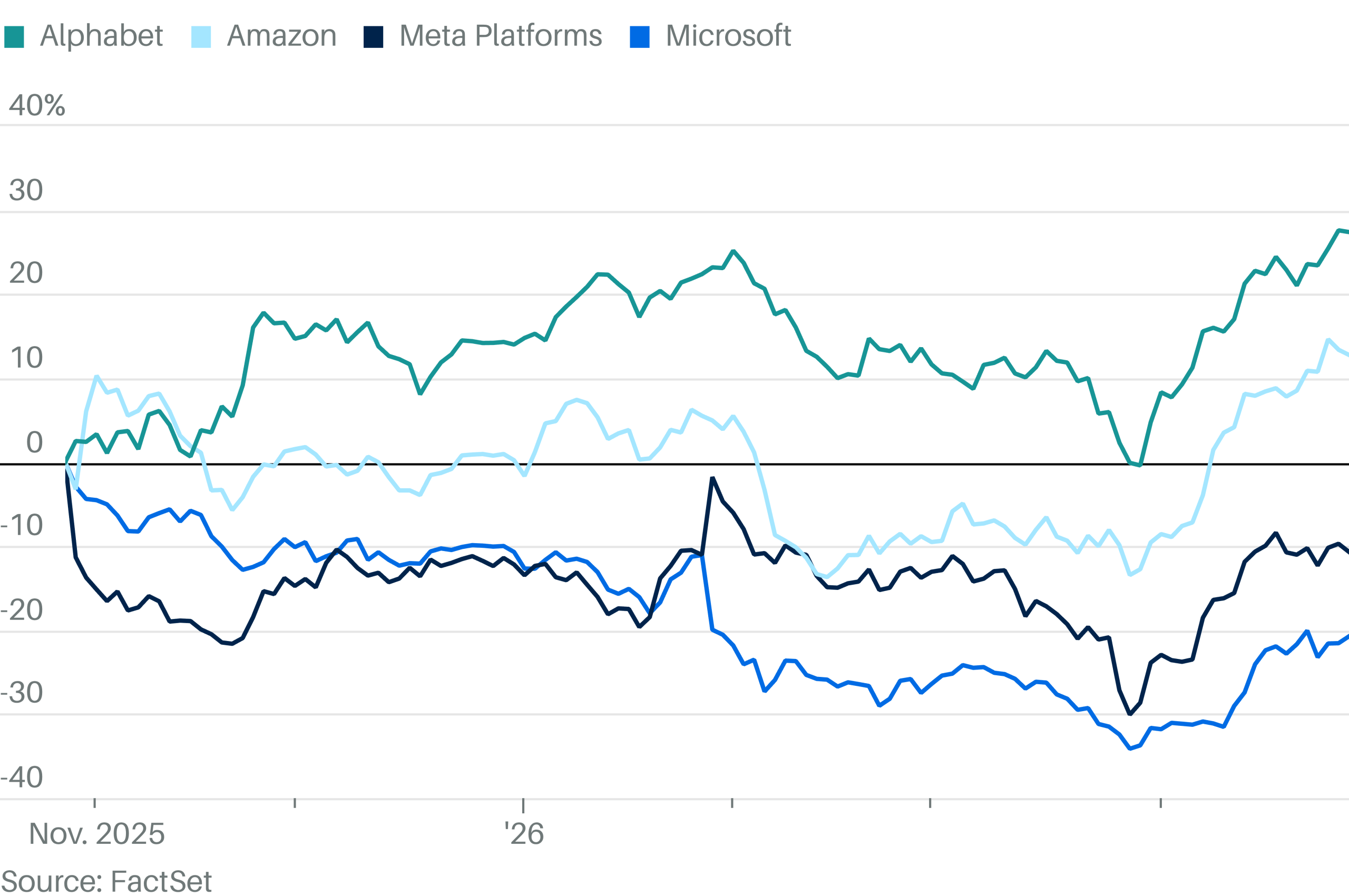

Magnificent Seven Stocks Struggle for Direction Ahead of Big Tech Earnings

The company’s board has recommended a final dividend of Rs 4.62 per share for the financial year ended March 2026.

Revenue from operations rose 16% YoY to Rs 3,684 crore from Rs 3,174 crore a year ago, reflecting higher project execution during the quarter. Including other income, total income for the quarter stood at Rs 3,965 crore, up 13% from Rs 3,498 crore in the year-ago period.

Profit before tax rose sharply by 54% to Rs 625 crore, compared with Rs 406.4 crore in the corresponding quarter last year, indicating improved operating leverage.

Sequentially, however, profitability moderated from the December quarter, when the company had reported a profit of Rs 837 crore, suggesting normalization after a stronger third quarter driven by milestone-based revenue recognition.

Expenses during the quarter rose at a slower pace than revenue. Total expenses increased 8% to Rs 3,340 crore from Rs 3,091 crore a year ago, mainly due to higher raw material consumption and inventory purchases.

For the full financial year FY26, Mazagon Dock reported revenue from operations of Rs 12,840 crore, up 12% from Rs 11,432 crore in FY25.Total income for the year came in at Rs 13,982.4 crore, registering a growth of 12% YoY.

Annual profit before tax rose 4% to Rs 3,250 crore, while net profit increased 5% to Rs 2,436 crore from Rs 2,325 crore in the previous financial year.

Trinity Rodman #2 of Washington Spirit evades Sarah Schupansky #11 of Gotham FC during the NWSL Championship 2025 final between Washington Spirit and NJ/NY Gotham FC at PayPal Park on November 22, 2025 in San Jose, California.

Lyndsay Radnedge/isi Photos | Isi Photos | Getty Images

A version of this article first appeared in the CNBC Sport newsletter with Alex Sherman, which brings you the biggest news and exclusive interviews from the worlds of sports business and media. Sign up to receive future editions, straight to your inbox.

Last week, the National Women’s Soccer League awarded a new expansion franchise — in Columbus, Ohio — to an ownership group led by Haslam Sports Group for a fee of $205 million.

This represents a $40 million jump from the $165 million that billionaire Arthur Blank reportedly paid for the league’s Atlanta franchise in November. And that $165 million itself was a jump of $55 million from the reported $110 million fee Denver paid in January of last year.

Rewind to 2022, and the expansion fee for a new NWSL club was just $2 million.

On the surface, this appears to be a story about the NWSL’s growth. Postseason attendance rose 11% this past season, according to the league. Nearly 1.2 million people watched the NWSL finals, up 22% from a year ago, including a whopping 70% jump in the 18-to-34 demographic, the NWSL said.

It makes sense that investors would want to get in now given the league’s growth trajectory.

But, according to investors and bankers, something else is going on that’s affecting the NWSL’s valuations that has absolutely nothing to do with soccer. It has to do with a trickle-down investment thesis driven by the outsized businesses of the NFL and NBA.

Wealthy investors have long been interested in sports ownership, trophy assets that have also produced outsized returns on investment. The introduction of private equity investment, first adopted in the NFL in 2024, has added to the pool of possible buyers.

This dynamic is welcome news for the entire professional sports industry, which is also benefiting from another strategic investment play — the anti-artificial intelligence trade. Betting on live events is a counter-strategy for those who want less exposure to the tech in a market driven by AI investments.

That’s helped supercharge valuations of the most valuable sports teams in the U.S. According to CNBC Sport, the average NFL team is now valued at $7.65 billion. In 2010, NFL teams were worth, on average, about $1 billion.

The average value of an NBA team is now $5.52 billion, 18% higher than a year ago. Fifteen years ago, the average NBA team was worth $369 million. That’s an increase of 1,396%. The S&P 500 is up about 422% over the same time period.

NBA and NFL ownership stakes are becoming too pricey for a class of buyers who have active interest in being a sports team owner — even at the minority stake level. Former New York Giants quarterback Eli Manning said as much in an interview with CNBC Sport last year.

“It’s too expensive for me,” Manning said of a potential minority stake in his longtime team. “A 1% stake valued at $10 billion turns into a very big number.”

Equity research firm Bernstein wrote in a recent note to clients that NFL team valuations have risen about 17 times in 25 years, “the kind of returns sufficient to give any portfolio manager a legendary status and easily trumping the S&P index or any emerging market index on the planet.”

The main cause of the valuation growth stems from the enormous size of the league’s media rights. The NFL signed an 11-year, $111 billion media rights deal in 2021 — and now wants even more money. The NBA followed with an 11-year, $77 billion deal of its own, starting with the 2025 season.

Splitting national TV dollars among teams allows even the lowest revenue teams — the NFL’s Arizona Cardinals and the NBA’s Memphis Grizzlies — to be valued at $5.9 billion and $3.75 billion, respectively, according to CNBC estimates.

There’s a fear that “second-tier” sports, including MLB and NHL, may be at risk of losing media rights dollars as the NFL flexes its muscle and asks for more from its media partners. The more money that goes to the NFL, the less money there is for everyone else.

One might expect that dynamic to negatively affect the valuations for those sports. But according to these bankers and investors, that’s not happening.

As the NBA and NFL have priced out buyers, there’s now increased demand for sports teams with more affordable valuations. That’s helped drive the recent NWSL surge, they say. There’s more liquidity at NWSL team price points, which has led to bidding wars and soaring valuations.

While the most recent winning buyers — Blank and the Haslams — are already owners of NFL and other sports teams, they’ve had to pay increasingly high prices to fight off other offers. There are far more buying groups willing to write a consortium check for $200 million than pay $1 billion or more for minority stakes in the biggest leagues.

“There’s a lot of demand to get into the sports business but people can’t write the checks to buy into the big four anymore. So what they’re doing is they’re substituting,” said veteran sports banker Sal Galatioto, president of Galatioto Sports Partners. “When supply is fixed and demand goes up, people will bid more to win. The underlying economics are not as important.”

The San Diego Padres are finalizing a sale for $3.9 billion, a record for MLB, despite the team’s regional sports network falling apart a few years ago. While nearly $4 billion is a lot of money, it’s still well below the average value of an NFL or NBA team.

“I’ve got investors coming up to me saying, ‘I can’t afford the NFL and NBA, what do you have for me in MLB, NHL?’” said one prominent sports banker, who asked to speak anonymously because the discussions were private.

The success of the NBA and NFL has funneled all the way down to the bottom of the sports food chain, said Rick Horrow, CEO of Horrow Sports Ventures.

“Major League Cricket was at $5 million. Now the value’s at $30 [million] and going higher. Major League Pickleball two years ago was at $5 million. Now the value is at $15 million or higher,” said Horrow.

Some of this sounds a little like a sports investment bubble, where valuations are divorced from the underlying financials of the leagues themselves.

That’s a real worry for smaller, less established leagues, said Jasmine Robinson, managing partner at Monarch Collective, the largest women’s sports investment fund, with $250 million to invest. It’s why Monarch has focused most of its funds on the WNBA and the NWSL, rather than more emergent leagues, Robinson said.

“Sports has historically been a great investment, but that’s really only for the biggest leagues. It’s not really like you can do any sports deal and you’re going to make money,” Robinson said. “There’s been real scarcity. You do need to be in the leagues that really are going to be leaders to make money. We wouldn’t make a bet on every women’s sports league.”

The big question may be what the threshold is for an established league if there’s an economic downturn that turns off the investment faucet. Monarch is betting the WNBA and the NWSL are above the line, but WNBA franchises have historically never made money, and now they need to pay out far more money to players after this year’s new collective bargaining agreement.

Reliance Steel stock hits all-time high at 365.86 USD

Spain’s Banco Santander SAN 0.07%increase; green up pointing triangle reported a surge in profit as it added more customers and logged a large gain from a recent disposal.

Continental Europe’s largest lender by market capitalization posted a 60% increase in first-quarter net profit to 5.455 billion euros ($6.39 billion). The bottom line was helped by a 1.9 billion-euro capital gain from the recently completed sale of most of its Polish subsidiary.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

GDP Prints At 2%, But There's Noise In The Numbers

Business

GameStop Shares Edge Higher Near $24.64 as $9 Billion Cash Pile Fuels Acquisition Speculation

GRAPEVINE, Texas — GameStop Corp. shares traded modestly higher Thursday, rising 0.49% to $24.64 in midday action as investors continued weighing the retailer’s massive cash reserves against ongoing challenges in the traditional video game market and growing optimism around CEO Ryan Cohen’s plans for a potential transformational acquisition.

The modest gain came on relatively light volume as the meme-stock favorite navigated a quiet period following recent initiatives like the April 15 launch of “Power Packs” digital trading cards and the rollout of retro gaming sections in stores. With roughly $9 billion in cash and equivalents on hand, GameStop sits in one of the strongest balance sheet positions in its history, giving Cohen significant firepower for strategic moves that could reshape the company.

Analysts and retail investors alike are closely watching how the company deploys its war chest. Cohen has signaled interest in a “very, very, very big” acquisition in the consumer or retail space, comments that have kept speculation alive even as the core business faces headwinds from digital downloads and declining physical game sales. Market capitalization hovers near $11 billion, meaning any sizable deal would represent a major pivot.

GameStop’s Q4 fiscal 2025 results, released in late March, showed resilience on the bottom line despite revenue pressure. The company posted adjusted earnings per share of $0.49, beating estimates, while revenue came in lighter than expected amid broader industry softness. The standout figure remained the cash balance, which has become a central narrative for bulls betting on Cohen’s ability to create long-term value.

Recent operational moves reflect a blend of nostalgia and innovation. GameStop has expanded retro gaming sections in select stores, capitalizing on demand for classic consoles and cartridges. The Power Packs platform aims to tap into the growing digital collectibles market, offering a new revenue stream beyond traditional hardware and software sales. These efforts signal an attempt to evolve the brand while physical retail remains under pressure.

Insider activity has drawn attention. In mid-April, General Counsel Mark Haymond Robinson sold shares worth about $91,000, part of routine filings that some interpreted as neutral but contributed to short-term volatility. Earlier in the year, Cohen himself added to his stake with significant open-market purchases, reinforcing alignment with shareholders.

The stock has traded in a relatively narrow range in 2026 compared to its meme-stock heyday, fluctuating between roughly $20 and $35. Thursday’s price near $24.64 leaves it well below its 52-week high and reflective of a more mature investment case built on cash deployment rather than short-squeeze dynamics. Short interest remains elevated, keeping the name sensitive to any positive or negative catalysts.

Cohen’s compensation structure adds another layer of intrigue. In January, the board approved a performance-based stock option award potentially worth billions if GameStop achieves ambitious targets, including significant market cap growth and EBITDA milestones. The award is entirely at-risk and requires shareholder approval, tying the CEO’s upside directly to value creation.

Retail enthusiasm persists on platforms like Reddit’s r/Superstonk, where discussions focus on cash yield potential, possible Bitcoin investments under a revised policy, and long-term transformation. Yet many analysts remain cautious, noting that while the balance sheet is strong, sustainable profitability in a shrinking physical games market remains unproven.

GameStop continues store optimization efforts, having closed hundreds of locations in recent years to improve efficiency. The company has also explored international adjustments, including potential divestitures. These moves aim to create a leaner operation better positioned for whatever Cohen’s next big step may be.

Broader industry context matters. Video game publishers continue shifting toward digital and live-service models, reducing reliance on brick-and-mortar retailers. GameStop has countered by emphasizing trade-ins, collectibles, exclusive merchandise and now digital experiments. Its e-commerce platform and loyalty program provide additional touchpoints with customers.

Investors eyeing the stock confront a classic value-versus-speculation debate. Bulls highlight the cash hoard as undervalued optionality — essentially buying a potential acquirer at a discount. Bears point to eroding core revenues and question whether Cohen can execute a deal that truly moves the needle without destroying shareholder value.

Next earnings, expected around early June for the first quarter of fiscal 2026, will offer fresh insight into sales trends and any updates on strategic plans. In the meantime, modest price action like Thursday’s reflects digestion of recent news rather than a new catalyst.

Options activity remains active, with traders betting on volatility around potential announcements. The name’s history ensures it stays on watchlists, even as daily moves stay relatively tame compared to 2021 peaks.

For a company once defined by viral short squeezes, GameStop’s story has evolved into one of patient capital allocation under Cohen’s leadership. With billions in dry powder and a mandate to think big, the coming months could bring clarity on whether the retailer successfully pivots or continues battling sector decline.

Shareholders and observers will keep a close eye on any acquisition rumors, partnership announcements or further capital return signals. In a market hungry for turnaround stories, GameStop’s cash position keeps it firmly in the conversation — even on otherwise quiet trading days.

The Met Police social media team cleverly decided to amplify a Tommy Robinson X post

NFL Draft grades: Why they’re often wrong but still useful

Timeline of Artemis II photos shows astronauts inside Orion

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

Financial Freedom Beyond Money || Elisha Ongoya – Advocate

Moneyman shows off $400,000 cash after 50 cent shows off 3 million cash #moneyman #50cent

IT JUST GOT RELEASED! XRP $18,000 PRICE CALCULATOR REVEALED?! (IS IT REAL?)

-

Tech3 days ago

Tech3 days agoRegister Renaming | Hackaday

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Business7 days ago

Business7 days agoPatterson-UTI Energy, Inc. (PTEN) Q1 2026 Earnings Call Transcript

-

Politics3 days ago

Politics3 days agoDrax board avoid their own AGM, accused of greenwashing & environmental racism

-

Sports4 days ago

Sports4 days agoIPL 2026: Ruturaj Gaikwad registers slowest fifty of the season, enters all-time unwanted list | Cricket News

-

NewsBeat4 days ago

NewsBeat4 days agoLK Bennett closes all stores after entering administration

-

Crypto World6 days ago

Crypto World6 days agoMichael Saylor says BTC winter is over. Market analyst disagrees, says bitcoin was in a pullback

-

Fashion2 days ago

Fashion2 days agoKylie Jenner’s KHY Enters a New Era with ‘Born in LA’

-

Tech3 days ago

Tech3 days agoImages of Samsung’s rumored smart glasses have leaked

-

Tech3 days ago

Tech3 days agoWhy Blue Badges Disappeared From Toyota Hybrids

-

Entertainment5 days ago

Entertainment5 days agoMariah Carey Slams Deposition Claims In Brother’s Lawsuit

-

Crypto World7 days ago

Is Algorand One of the Few Quantum-Resistant Blockchains? Here’s What the Data Shows

-

Business2 days ago

Business2 days agoMost Commercial Energy Audits Miss the Real Losses

-

NewsBeat6 days ago

NewsBeat6 days agoTrump threatens to review UK’s claim to Falkland Islands and punish Nato allies over Iran war disagreement

-

Business6 days ago

Business6 days agoJeanine Pirro announces closure of Federal Reserve building cost probe

-

Business3 days ago

Business3 days ago(VIDEO) Charlize Theron Climbs Times Square Billboard to Promote New Netflix Thriller ‘Apex’

-

Tech5 days ago

Tech5 days agoMicrosoft to roll out Entra passkeys on Windows in late April

-

Crypto World2 days ago

Crypto World2 days agoCFTC’s AI will review U.S. crypto registration applications, chairman tells CoinDesk

-

Crypto World6 days ago

Crypto World6 days agoNvidia (NVDA) Stock Jumps 5% as Intel Earnings Ignite Semiconductor Rally

You must be logged in to post a comment Login