Business

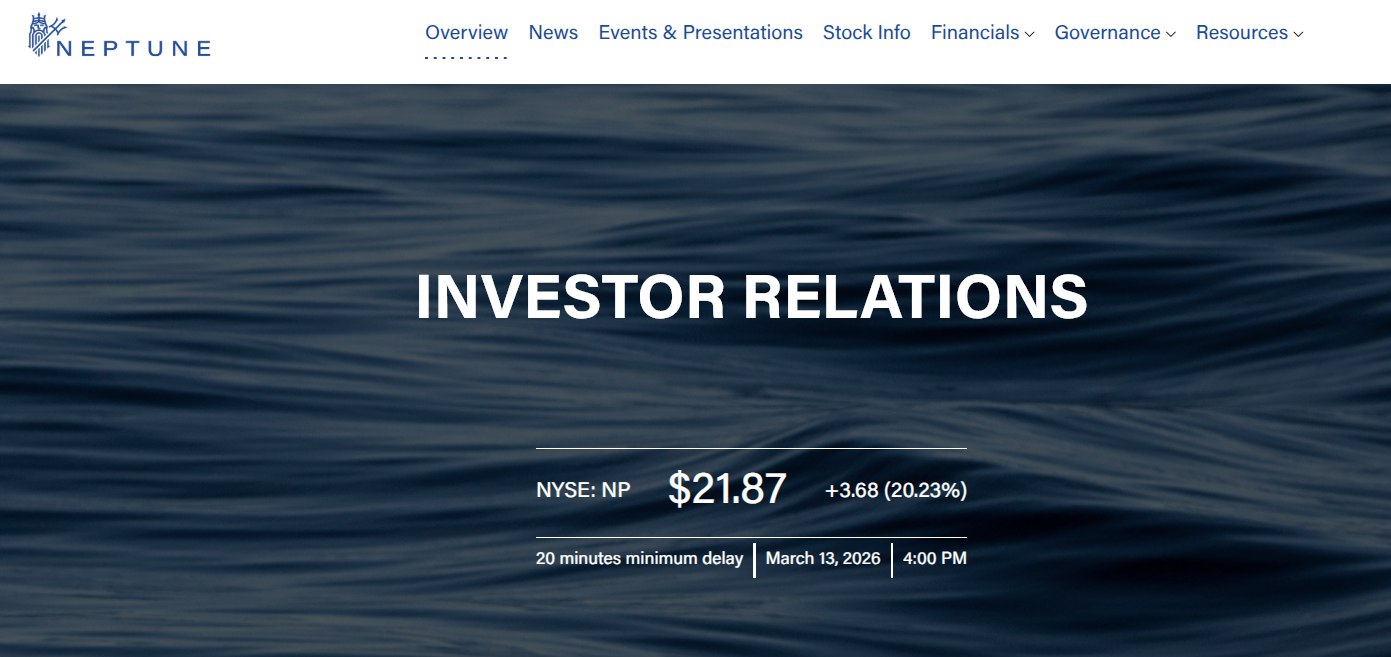

Neptune Insurance Holdings (NP) Stock Surges 20% to $21.87 Amid Strong Momentum in Insurtech Sector

Neptune Insurance Holdings Inc. (NYSE: NP) shares closed sharply higher at $21.87 on March 13, 2026, up $3.68 or 20.23% from the previous day’s close of $18.19, as trading volume spiked to around 925,000 shares — more than double the average daily volume.

The Florida-based insurtech firm, which went public in October 2025, saw its stock rally on March 13 after a period of consolidation, with intraday trading ranging from a low of $18.52 to a high of $21.93. After-hours activity added another $0.25, pushing the price to $22.12, up 1.14% further.

The surge came amid broader interest in property and casualty insurers focused on flood and catastrophe coverage, as climate-related risks drive demand for specialized products. Neptune, through its subsidiary Neptune Flood Incorporated, operates as a managing general agent offering primary flood insurance, excess flood, parametric earthquake and indemnity earthquake policies distributed via agency networks.

The company reported strong growth in its latest earnings on February 18, 2026, for the fourth quarter and full year ended December 31, 2025. Revenue rose 39% to $43.8 million in Q4, though net income fell 63% to $4.3 million due to $4.6 million in IPO-related expenses. Full-year revenue grew 34% to $159.6 million, with net income up 8% to $37.4 million despite $13.1 million in one-time costs. Written premiums increased 34% to $367.3 million, adjusted EBITDA climbed 32% to $95.0 million, and new business sales hit records.

Analysts have responded positively. BMO Capital upgraded NP to Outperform from Market Perform in mid-February 2026, citing growth potential in the flood insurance market. Consensus ratings lean toward Buy, with an average 12-month price target around $26.79 to $27.04, implying 22-30% upside from recent levels. Some targets reach $36.75, while others sit at $22.72, reflecting varied views on execution and market conditions.

Neptune’s focus on data-driven underwriting and digital distribution positions it well in a sector facing rising catastrophe losses from hurricanes, floods and earthquakes. Recent initiatives include a March 12, 2026, launch of a ChatGPT-integrated app for preliminary flood quotes, expanding accessibility, and a March 4 analysis from its research group on FEMA’s proposed 2026 Harris County, Texas, flood map updates, highlighting potential impacts on policyholders.

The stock debuted in October 2025 with a strong first day, jumping 12.5% and valuing the company near $3.1 billion. It traded in a 52-week range of $14.78 (hit February 12, 2026) to $33.23 (October 3, 2025), reflecting post-IPO volatility typical for insurtech names.

Market capitalization stood around $3.02 billion at the March 13 close, with about 138 million shares outstanding. The forward P/E remains attractive relative to growth prospects, though trailing metrics show losses in some periods due to expansion costs.

No major news triggered the March 13 move directly, but traders pointed to technical breakout above recent resistance near $19-20, renewed analyst coverage and sector rotation into financials. Options activity showed elevated call volume, indicating speculative interest.

Neptune continues to build partnerships, including a January 2026 capacity deal with Somers Syndicate at Lloyd’s for additional reinsurance support. The company guides for 2026 revenue of $186-189 million and adjusted EBITDA margins of 60-61%, signaling confidence in scaling operations.

As climate change intensifies flood and seismic risks, Neptune’s specialized offerings could capture more market share from traditional carriers. Investors watch for the next earnings update, expected around May 2026, for updates on premium growth, loss ratios and tech investments.

The sharp gain on March 13 underscores momentum for NP as an emerging player in a high-demand niche, though volatility persists in the young listing.

Philipp is a seasoned value investor with nearly 20 years of experience in the field. He takes a global approach to investment opportunities, seeking out undervalued companies that offer a significant margin of safety, leading to attractive dividend yields and returns. While he does not limit his investments to specific sectors or countries, he focuses only on companies he thoroughly understands and can reasonably assess for future growth potential. Philipp is particularly enthusiastic when he identifies a company with a solid earnings track record trading at less than 8x free cash flow, which inspired his username: 8xfreecash.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of DOMINO’S PIZZA GROUP either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Rubrik Outstanding Execution And Still Underappreciated

New Prince Harry book a ’deranged conspiracy’, his spokesperson says

Business

Hamas calls on Iran not to target neighboring countries but affirms its right to self-defence

Hamas calls on Iran not to target neighboring countries but affirms its right to self-defence

Exclusive-Trump rejects efforts to launch Iran ceasefire talks, sources say

NEW YORK / KYIV — Shares of Kyivstar Group Ltd. (NASDAQ: KYIV) staged a dramatic recovery on Friday, March 13, 2026, as investors reacted to a “blowout” earnings report that showcased the operator’s ability to maintain double-digit growth despite the ongoing challenges of operating in a wartime economy.

After a volatile week for the broader NASDAQ exchange, Kyivstar closed the session at $11.07, up nearly 9% from its previous close of $10.20. The rebound follows a year of historic milestones for the company, which in late 2025 became the first Ukrainian-based firm to list directly on a major U.S. stock exchange.

Financial Performance: Growth Beyond Connectivity

The fourth-quarter and full-year 2025 results, released early Friday morning, outperformed both analyst estimates and the company’s own conservative guidance.

- Revenue Surge: Total revenue for 2025 reached $1.157 billion, a nearly 26% increase year-over-year.

- Profitability: The company reported an adjusted net profit of $289 million, with earnings per share (EPS) of $1.32.

- EBITDA: Kyivstar maintained a high-efficiency operation with an EBITDA of $648 million, reflecting a massive margin of 56%.

- Digital Pivot: Digital revenue grew by 4.7x in 2025, now accounting for over 10% of the company’s total revenue, driven by expansion into health-tech and fintech.

“These results are a testament to the digital transformation we have spearheaded in Ukraine,” said Oleksandr Komarov, CEO of Kyivstar. “We are no longer just a telecom company; we are a digital services ecosystem.”

The “Starlink Mobile” Revolution

A primary driver of investor optimism in early 2026 has been Kyivstar’s world-first integration of Starlink Mobile satellite technology.

At the Mobile World Congress (MWC) in Barcelona earlier this month, the company announced it now serves 5 million customers via its “Direct-to-Cell” satellite network. This technology allows standard 4G smartphones to connect directly to satellites in areas where terrestrial towers have been damaged or destroyed by conflict.

“Kyivstar is shaping the global practice of integrating non-terrestrial networks,” noted industry analyst Daniel Lee. “The Ukrainian use case for satellite connectivity is being watched by every major carrier in the world as a blueprint for emergency resilience.”

Strategic Shifts and Ownership

The stock’s recent performance also reflects a more stable capital structure. In February 2026, Kyivstar’s parent company, VEON Ltd., successfully completed a secondary public offering of 14.3 million shares at $10.50 per share.

The offering was oversubscribed fivefold, indicating high institutional appetite for Ukrainian assets. Following the sale, VEON remains the principal shareholder with an 83.6% stake, but the expanded “free float” has significantly improved the stock’s liquidity on the Nasdaq.

Furthermore, Kyivstar continues to diversify its revenue through aggressive M&A activity. In February, the company finalized the $160 million acquisition of Tabletki.ua, Ukraine’s leading online healthcare marketplace, signaling a long-term pivot toward digital health.

2026 Outlook: 5G and EU Integration

Looking ahead, management has provided optimistic guidance for the remainder of 2026, forecasting USD revenue growth between 8% and 11%. Key drivers for the coming year include:

- The 5G Pilot: A large-scale 5G rollout that began in Lviv earlier this year.

- Expansion of Space Tech: Plans to increase Starlink Mobile users to 12 million by the end of 2026.

- Reconstruction: Participation in the government’s “Digital Marshall Plan,” prioritizing high-speed fiber connectivity for rebuilding efforts.

Market Context and Risks

Despite the positive momentum, KYIV remains a high-beta stock, currently trading with a beta of 1.59, making it more volatile than the broader market.

Investors remain wary of the geopolitical risks and the impact of the UAH/USD exchange rate, which management currently models at 44.5 for their 2026 projections. However, with a Price-to-Earnings (P/E) ratio of roughly 10.3, many value investors are viewing the current price as a favorable entry point for a dominant market leader.

KYIV Stock Snapshot (March 13, 2026)

| Metric | Value |

| Last Price | $11.07 |

| Day Change | +8.53% |

| Market Cap | $2.64 Billion |

| 52-Week Range | $10.15 – $16.48 |

| Volume | 2.5 Million (High Vol) |

DALLAS— In the high-stakes world of the NBA, comparisons to “Larry Legend” are usually reserved for the Hall of Fame wing of a museum. But as of March 15, 2026, those comparisons aren’t just being whispered; they are the loudest debate in professional sports.

Cooper Flagg, the 19-year-old rookie sensation for the Dallas Mavericks, has spent the 2025-26 season turning the “generational talent” label into an understatement. After being selected No. 1 overall following a historic freshman year at Duke, Flagg is currently averaging 20.1 points, 6.7 rebounds, and 4.2 assists per game.

But stats only tell half the story. The real question—the one sparking heated debates from the Road Trippin’ podcast to the desks of ESPN—is whether Cooper Flagg is actually better than Larry Bird was at the same stage.

The Statistical Tale of the Tape

To understand the Flagg-Bird comparison, one must look at their respective trajectories. Larry Bird entered the NBA at age 23, having stayed four years in college to lead Indiana State to the 1979 NCAA title game. Cooper Flagg, by contrast, is a “one-and-done” prodigy who is already a top-tier NBA producer while Bird was still dominating the Missouri Valley Conference.

| Metric | Cooper Flagg (Rookie, 2026) | Larry Bird (Rookie, 1980) |

| Age | 19 | 23 |

| Points Per Game | 20.1 | 21.3 |

| Rebounds Per Game | 6.7 | 10.4 |

| Assists Per Game | 4.2 | 4.5 |

| Blocks Per Game | 0.9 | 0.6 |

| Steals Per Game | 1.1 | 1.7 |

While Bird’s rookie rebounding numbers remain superior, Flagg’s scoring efficiency and defensive versatility at age 19 have scouts suggesting his “ceiling” is exponentially higher.

The “Star Power” Factor: Carmelo Anthony and Paul George Weigh In

The comparison gained massive traction earlier this year when NBA veterans Carmelo Anthony and Paul George discussed Flagg’s impact.

“We haven’t seen a white boy like that in a long time,” Anthony remarked on 7PM in Brooklyn. “It’s got to be [Larry Bird] as far as that star power.” George agreed, noting that while Flagg doesn’t necessarily do any one thing at an elite level yet, he does “everything very, very good.”

Why the Comparison Sticks (and Why It Doesn’t)

The Case for Flagg:

- Defensive Prowess: Unlike Bird, who relied on elite positioning and “basketball IQ” to defend, Flagg is a modern-day physical specimen. At 6-foot-9 with elite verticality, he is a “five-tool” defender capable of switching onto guards or protecting the rim.

- Modern Shooting: Flagg’s 38.5% clip from three-point range during his Duke tenure showed a perimeter threat that took Bird years to fully develop in an era that didn’t value the long ball.

- Early Professionalism: Flagg is arguably the most prepared 19-year-old in history. His performance during the 2024 Team USA scrimmages—where he famously held his own against LeBron James and Anthony Davis—proved he was “NBA-ready” before he even stepped foot on Duke’s campus.

The Case for Bird:

- Passing Genius: Larry Bird is widely considered the greatest passing forward in history. While Flagg is a willing and capable facilitator, he has yet to show the “no-look,” telepathic vision that earned Bird three consecutive MVPs.

- The “Killer” Instinct: Bird’s psychological dominance over opponents is legendary. Flagg has shown incredible poise, particularly in his 42-point outburst against Notre Dame in 2025, but Bird’s resume of “clutch” moments is the gold standard.

The Mavericks’ New Era

The timing of Flagg’s arrival in Dallas is poetic. Following the departure of Luka Dončić, the Mavericks needed a new cornerstone. Flagg has stepped into that void with a maturity that belies his age. Despite a mid-season foot injury that sidelined him for eight games in February 2026, he returned on March 5 to post 18 points and four blocks against Orlando, signaling he is ready for the playoff push.

“He doesn’t play like a rookie,” said Mavericks coach Jason Kidd. “He has the IQ of a ten-year vet. When people talk about Bird, they talk about the mind. Cooper is in that same stratosphere.”

The Verdict: Is He Better?

Is Cooper Flagg better than Larry Bird? If we are talking about peak performance, the answer is clearly not yet. Bird is a three-time champion and three-time MVP.

However, if the question is who was better at 19?, Flagg wins in a landslide. By the time Larry Bird was 19, he was dropping out of Indiana University and working for the French Lick municipal department. Cooper Flagg is currently the frontrunner for NBA Rookie of the Year and the face of a billion-dollar franchise.

The 2025-26 season has proven that Cooper Flagg isn’t just “the next Larry Bird”—he is the first Cooper Flagg. And for the rest of the NBA, that is a terrifying prospect.

Cooper Flagg: 2025-26 Season Highlights

- Draft Status: No. 1 Overall Pick (Dallas Mavericks).

- NCAA Accolades: Wooden Award Winner, ACC Player of the Year, First-Team All-American.

- NBA Milestone: Second-youngest player to reach 1,000 career points (achieved March 2026).

- Key Game: 25 points, 5 assists, 4 rebounds vs. Cleveland (March 13, 2026).

Business

(VIDEO) Kathie Lee Gifford Blasts ‘The View’ Co-Hosts as ‘Miserable’ Following Alleged Book Promo Rejection

Television icon Kathie Lee Gifford has ignited a public feud with the producers and hosts of ABC’s The View, labeling the long-running talk show “vicious” and its panelists “miserable” after they reportedly declined to host her for her latest book tour.

The legendary former co-host of Live! with Regis and Kathie Lee and Today has been on a whirlwind media blitz for her 37th book, Nero and Paul: How the Gospel of Grace Defeated the Ruler of Rome, which hit shelves on March 10, 2026. However, what began as a spiritual promotion has turned into a headline-grabbing clash of daytime titans.

The “Viciousness” of Modern Media

The sparks began to fly during Gifford’s March 9 appearance on the podcast Tomi Lahren Is Fearless. When asked about the current state of political and social division in media, the 72-year-old Emmy winner didn’t hold back.

“There’s just more of us, and we’re meaner now,” Gifford told Lahren. “People, at least, would pretend to have some manners. Now, there’s a viciousness.”

Gifford specifically signaled out The View—a show she has visited numerous times over the decades—as a prime example of this atmospheric shift.

“I mean, I used to be able to go on The View and talk to Joy [Behar] and Whoopi [Goldberg]… and never had a problem with anybody because they weren’t trying to proselytize everything,” Gifford remarked. “Now, everybody seems like they’re just miserable people.”

Insiders Point to a Promo Rejection

While Gifford framed her comments as a critique of cultural “meanness,” industry insiders suggest the grievance is far more personal. According to reports from television veteran Rob Shuter, Gifford’s team had been “pushing hard” to secure a guest spot or even a guest-hosting gig on the ABC program to coincide with her book launch.

Insiders claim the show’s producers passed on the invitation, citing a crowded schedule and a shift in the show’s current direction. The View has recently relied on a rotation of guest hosts while regular panelist Alyssa Farah Griffin is on maternity leave, but Gifford was notably absent from the roster.

“It’s funny hearing her attack the show now,” one production source told Shuter’s Naughty But Nice Substack. “Just weeks ago she was practically begging to come on. Getting turned down clearly stung, and now she’s hitting back.”

‘Nero and Paul’: The Book at the Center of the Storm

Despite the drama, Gifford’s primary focus remains her new historical thriller, Nero and Paul. Co-written with theologian Dr. Bryan M. Litfin, the book is the second installment in her Ancient Evil, Living Hope series.

The narrative juxtaposes the “glamour, sex, and power” of the Roman Emperor Nero against the “unwavering faith” of the Apostle Paul. Gifford has described the project as a “page-turner” intended to show how the Gospel can overcome even the most entrenched systemic evil—a message she claims is more relevant in 2026 than ever before.

A Tale of Two Daytime Philosophies

The conflict highlights a growing rift between Gifford’s brand of “faith-first” positivity and the highly charged, often confrontational political debate that defines The View in 2026.

Gifford, who frequently refers to herself as “joy personified,” argued that she prefers to share her faith without being “mean-spirited.” Her critics, however, point to her recent criticisms of the LGBTQ+ community and her alignment with more conservative media outlets as the reason for her alleged “blacklisting” from mainstream daytime couches.

The “Today” Contrast

Interestingly, while the bridge to The View appears to be burning, Gifford’s relationship with her former home at NBC remains rock-solid. She returned to the Today show on March 9 to a warm reception from Hoda Kotb and Al Roker, where she was given a dedicated segment to discuss Nero and Paul.

“I follow Him, and I’m going to use every opportunity that comes my way to proclaim Him, because people are hurting,” Gifford said during her Today appearance.

As of Sunday, March 15, representatives for The View have not issued an official response to Gifford’s “miserable” characterization.

Kathie Lee Gifford: Career & Net Worth Snapshot (March 2026)

- Estimated Net Worth: $60 Million.

- Current Project: Nero and Paul (Released March 10, 2026).

- Key Honors: 4-time Daytime Emmy Award winner.

- Family News: Gifford recently celebrated the arrival of her fourth grandchild.

Protesters in Cuba attack Communist Party office in rare riot over blackouts

BofA lifts memory chip forecasts, expects no supply cuts from Iran conflict

Cambs area named among most expensive places to buy fuel in the country

Domino’s Pizza Group: Market Leader Trading Near Record-High Dividend Yield (DPUKY)

BTC Wobbles at $70K as France Deploys Ships to Hormuz and Trump Rejects Peace Deal Attempt (Report)

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Easy way meaning of financial management #accountingandfinance #financialeducation #trandingshorts

The Man Who Invented Every Financial Scam Started With Postage Stamps

Money and Banking | Final Exam Gap Revision | 6 Marks Fixed in class 12 Economics Board exam 2026

-

Tech3 days ago

Tech3 days agoA 1,300-Pound NASA Spacecraft To Re-Enter Earth’s Atmosphere

-

News Videos5 days ago

News Videos5 days ago10th Algebra | Financial Planning | Question Bank Solution | Board Exam 2026

-

Crypto World14 hours ago

Crypto World14 hours agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Business4 days ago

Business4 days agoExxonMobil seeks to move corporate registration from New Jersey to Texas

-

Crypto World5 days ago

Crypto World5 days agoParadigm, a16z, Winklevoss Capital, Balaji Srinivasan among investors in ZODL

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Addict Lip Glow

-

Tech4 days ago

Tech4 days agoChatGPT will now generate interactive visuals to help you with math and science concepts

-

Sports3 hours ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Sports7 days ago

Sports7 days agoThree share 2-shot lead entering final round in Hong Kong

-

Sports7 days ago

Sports7 days agoBraveheart Lakshya downs Lai in epic battle to enter All England Open final | Other Sports News

-

NewsBeat3 days ago

NewsBeat3 days agoResidents reaction as Shildon murder probe enters second day

-

Business6 days ago

Business6 days agoSearch for Nancy Guthrie Enters 37th Day as FBI Probes Wi-Fi Jammer Theory

-

Business3 days ago

Business3 days agoSearch Enters Sixth Week With New Leads in Tucson Abduction Case

-

NewsBeat5 days ago

NewsBeat5 days agoPagazzi Lighting enters administration as 70 jobs lost and 11 stores close across Scotland

-

Tech5 days ago

Tech5 days agoDespite challenges, Ireland sixth in EU for board gender diversity

-

Business5 hours ago

Business5 hours agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

NewsBeat3 days ago

NewsBeat3 days agoI Entered The Manosphere. Nothing Could Prepare Me For What I Found.

-

Business5 days ago

Business5 days agoSearch Enters 39th Day with FBI Tip Line Developments and No Major Breakthroughs

-

Sports5 days ago

Sports5 days agoSkateboarding World Championships: Britain’s Sky Brown wins park gold

-

Business6 hours ago

Business6 hours agoCountry star Brantley Gilbert enters growing non-alcoholic beer market